SEMA MARKET REPORT

SEMA MARKET REPORT

2022

A COMPREHENSIVE OVERVIEW OF THE AUTOMOTIVE

SPECIALTY-EQUIPMENT MARKET

1

INTRODUCTION

Specialty-Equipment Market Produces Another Record Year in 2021.

For the first time, we are reporting a market size over $50 billion. Overall consumer spending on parts and

accessories jumped 6.3% last year. This new high point for industry sales reached $50.9 billion.

The truck continues to be a driving force for the industry. Pickup mods accounted for nearly one-third of parts and

accessory sales. The shift toward light-truck sales continues in the new-vehicle market, and those pickup and utility

vehicles are great platforms for accessorization.

But, it’s not just about utility. Performance mods have seen great sales too. People are always looking for more

power. Most people can’t aord a Lamborghini or even a Hellcat. Still, this industry helps anyone boost their own car

toward those lofty goals.

People have voted with their wallet. Consumers continue to show that they love their cars and accessorizing them.

Contrary to what some would have us believe, car culture is alive and well in the United States. And that culture has

driven our industry to its best sales year ever.

Enthusiasts have been taking advantage of these strange times to do what they love: work on their cars and trucks.

Even amid all the disruptions, people found the opportunity to do something fun with their cars. That’s what makes

this industry so cool.

Even as consumers continue to spend, we are facing some headwinds in 2022 and beyond. We’ve all seen the eects

of the supply-chain issues that ramped up last year. Shipping, raw material and sub-assembly shortages will likely

continue into 2023. Inflation has risen across the board, as gas prices have shot up and companies in our industry

feel the need to raise prices amid increased costs. Consumer confidence has remained down, as a pandemic,

politics, and supply issues have weighed on their minds. Some economists see a slowdown coming this year.

But unemployment is low. Many people are still eschewing some travel and entertainment options, which leaves more

time and money for other hobbies. Even with higher gas prices, “road trip” may be the hot travel buzzwords this year,

which helps further connect people to their cars. Some economists see signs of continued spending and growth.

We expect our industry to keep growing. Sales growth may slow a bit this year, but we aren’t forecasting a drop.

As we get further past the pandemic and supply-chain issues, we expect to return to the growth trend we’ve seen

for a decade.

People really do like cars. And they like personalizing their cars. They spent over $50 billion last year to prove it.

I can’t wait to tell you what our sales record becomes next year.

Gavin Knapp

Director, Market Research

SEMA

2022 SEMA Market Report

Table of Contents

2

2022 SEMA Market Report

MARKET OVERVIEW

Overview ................................................................................................................................................................................................4

Specialty-Equipment Retail Sales .................................................................................................................................................... 4

Consumer Purchase by Sales Channel ...........................................................................................................................................5

Consumer Purchase by Vehicle Segment ....................................................................................................................................... 6

MARKET SIZING

CONSUMER PURCHASE BY PARTS CATEGORY ............................................................................................................................... 7

CONSUMER PURCHASE–PARTS OVERVIEWS ................................................................................................................................. 9

Maintenance Oils and Additives ........................................................................................................................................................ 9

Wax and Cleaning Products .............................................................................................................................................................10

Paint Powdercoating and Plating ...................................................................................................................................................11

Fender, Hood and Body Upgrades ..................................................................................................................................................12

Exterior Appearance Upgrades.......................................................................................................................................................13

Body Finishing Products ..................................................................................................................................................................14

Trailer and Towing Products ...........................................................................................................................................................15

Truck Bedliners and Other Bed Accessories ................................................................................................................................16

Racks and Carriers ............................................................................................................................................................................17

Truck Bed Covers ...............................................................................................................................................................................18

Truck Caps ..........................................................................................................................................................................................19

Seats and Upholstery .......................................................................................................................................................................20

Floor Mats and Interior Appearance Products.............................................................................................................................21

Dash System and Gauges ................................................................................................................................................................22

Head / Tail Lights ............................................................................................................................................................................... 23

Exterior Accessory Lighting ............................................................................................................................................................24

Interior Lights .....................................................................................................................................................................................25

Sound System and Audio Accessories ..........................................................................................................................................26

Alarms and Security Products ........................................................................................................................................................27

Navigation Systems .........................................................................................................................................................................28

Mobile TV and Video Cameras .........................................................................................................................................................29

Wireless and Smartphone Integration Products .........................................................................................................................30

Driver Assist Systems ......................................................................................................................................................................31

Transmission Products ..................................................................................................................................................................... 32

Axles and Dierential .......................................................................................................................................................................33

Clutches and Related Products .......................................................................................................................................................34

Shifters ................................................................................................................................................................................................35

Ignition Products ...............................................................................................................................................................................36

Engine Control and Computer Products ........................................................................................................................................ 37

Batteries and Related Products ......................................................................................................................................................38

Internal Engine Products .................................................................................................................................................................39

Cooling System Products .................................................................................................................................................................40

Engine Dress-Up Products ..............................................................................................................................................................41

Exhaust Products ...............................................................................................................................................................................42

Forced Induction Systems ................................................................................................................................................................43

Air Intake Products ............................................................................................................................................................................44

Carburetor and Fuel System Products ..........................................................................................................................................45

Roll Cage and Safety Products ........................................................................................................................................................46

Racing and Protection Apparel .......................................................................................................................................................47

Suspension Products ........................................................................................................................................................................48

Brake Products...................................................................................................................................................................................49

Table of Contents

3

2022 SEMA Market Report

CONSUMER PURCHASE–PARTS OVERVIEWS (Continued)

Steering Products ..............................................................................................................................................................................50

Performance / Special Purpose Tires ...........................................................................................................................................51

O-Road / Oversize Tires .................................................................................................................................................................52

Custom Wheels ..................................................................................................................................................................................53

VEHICLE SEGMENT PROFILES

Small Car .............................................................................................................................................................................................54

Midsize / Large Car ...........................................................................................................................................................................55

Sports Car ...........................................................................................................................................................................................56

Alternative Power ..............................................................................................................................................................................57

CUV .......................................................................................................................................................................................................58

SUV .......................................................................................................................................................................................................59

Pickup ..................................................................................................................................................................................................60

Van ........................................................................................................................................................................................................61

Classic ..................................................................................................................................................................................................62

CONSUMER PROFILE

Overview ..............................................................................................................................................................................................63

How the Vehicle is Used ...................................................................................................................................................................63

Where Consumers Look for Parts Information ............................................................................................................................64

How Parts and Accessories Are Installed ..................................................................................................................................... 65

Age ........................................................................................................................................................................................................66

Where Parts are Bought ...................................................................................................................................................................66

What Part Types are Bought ............................................................................................................................................................67

Vehicle Ownership Distribution ......................................................................................................................................................68

Vehicle Ownership by Age (Accessorizers) ..................................................................................................................................68

Buyer Types ........................................................................................................................................................................................69

Moving Past the Pandemic ............................................................................................................................................................... 70

Ownership of Sports / Recreational Equipment .......................................................................................................................... 72

INDUSTRY INDICATORS

Overview ..............................................................................................................................................................................................73

National Economic and Consumer Trends ....................................................................................................................................74

State of the Industry .........................................................................................................................................................................76

Impact of Supply Chain Issues ........................................................................................................................................................77

VEHICLE INFORMATION

Overview ..............................................................................................................................................................................................78

Vehicle Sales and Registrations .....................................................................................................................................................78

Vehicle Population Composition .....................................................................................................................................................80

Vehicle Sales Forecast ......................................................................................................................................................................83

Powertrain Sales Forecast ..............................................................................................................................................................84

METHODOLOGY

Research Methodology .....................................................................................................................................................................86

Market Definitions .............................................................................................................................................................................87

ADDITIONAL INFORMATION

Consumer Insights Research ..........................................................................................................................................................88

Industry-Focused Research.............................................................................................................................................................89

Contact Information ..........................................................................................................................................................................90

4

Market Overview 2022 SEMA Market Report

OVERVIEW

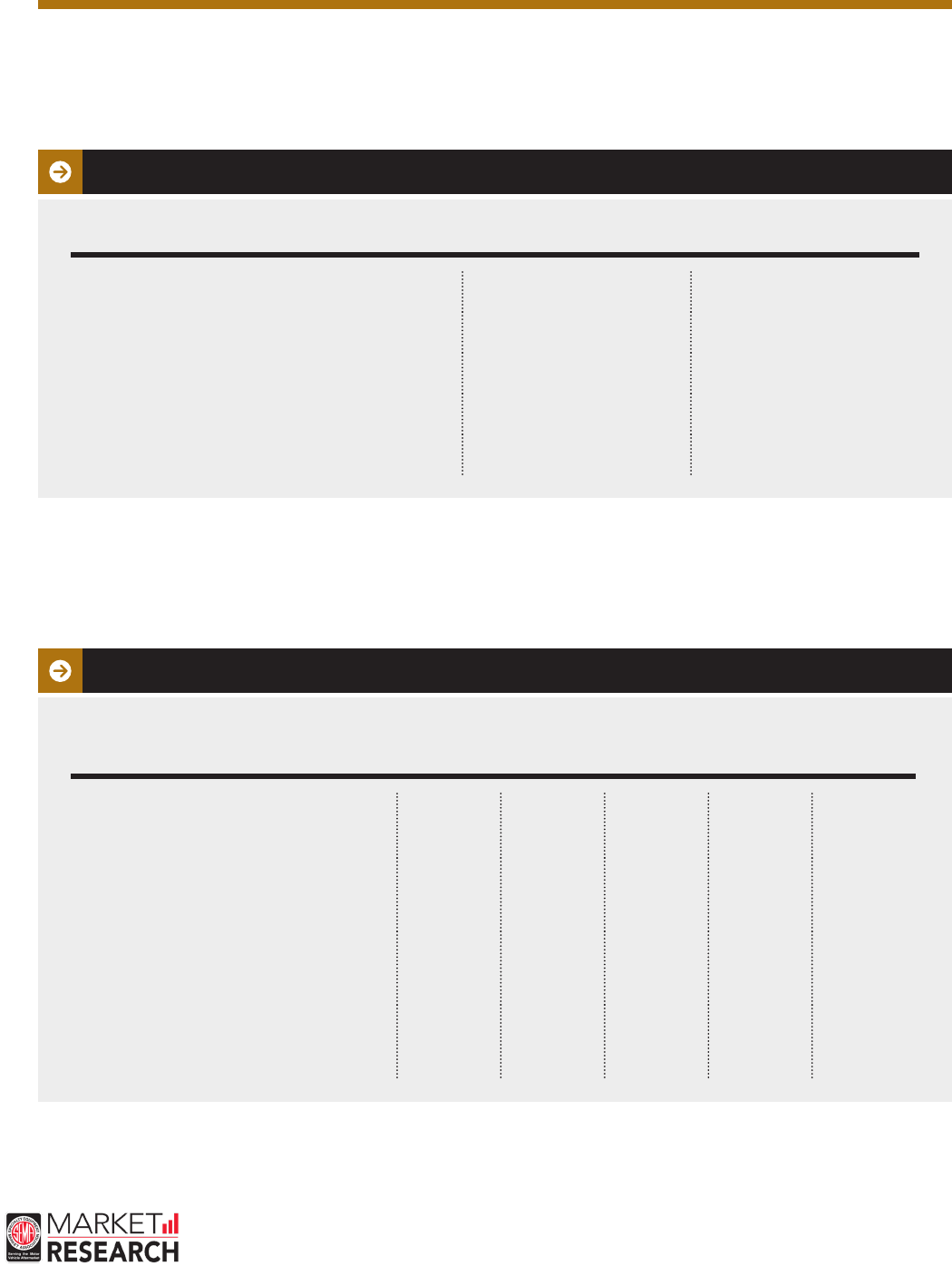

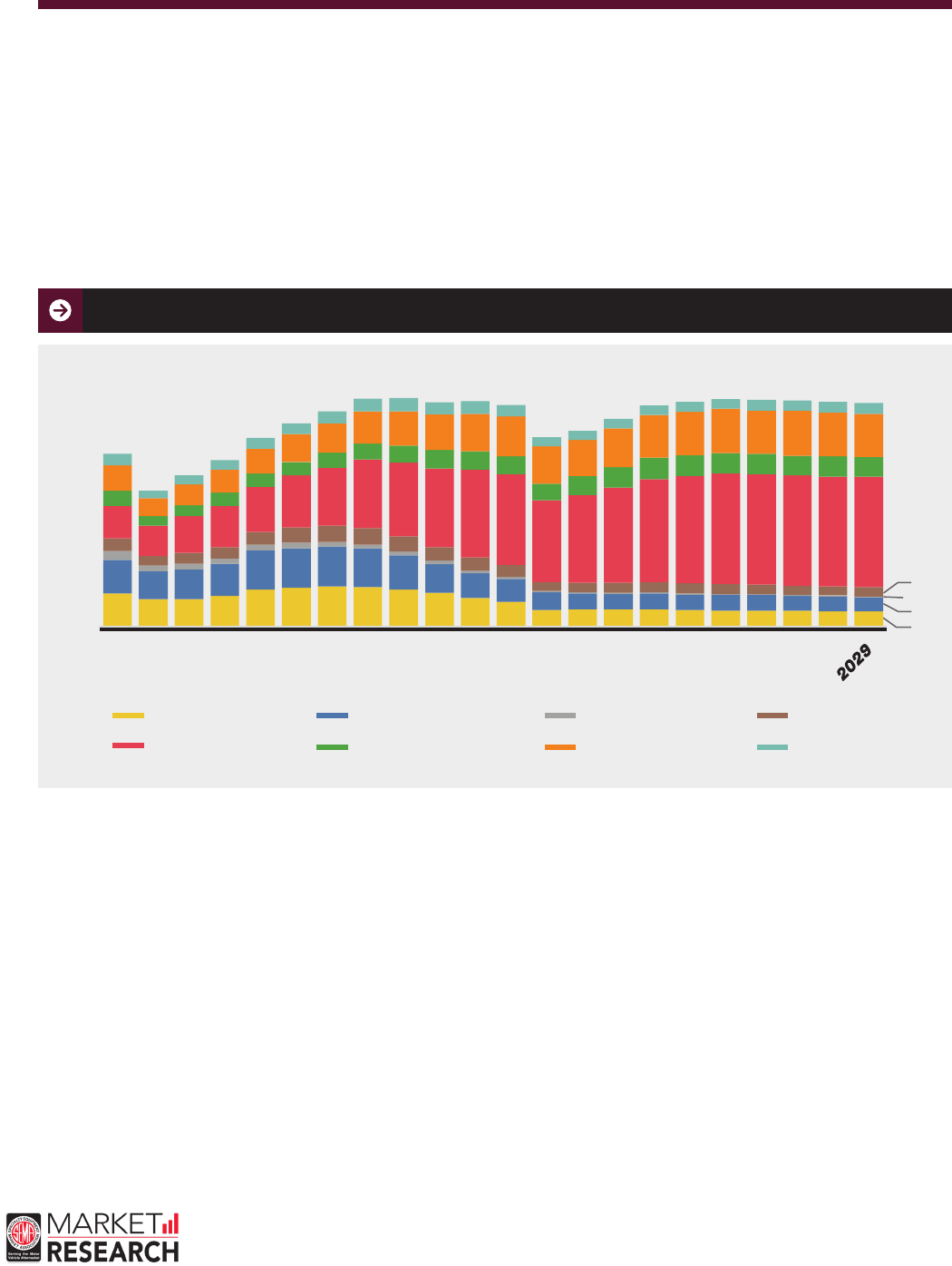

The specialty-equipment industry continues to grow. U.S. sales topped $50 billion for the first time in 2021. U.S.

consumers spent $50.9 Billion on accessorizing and modifying their vehicles last year. This represents a 6.3%

increase over 2020, and a new high for our industry.

Many businesses saw record sales in 2021, even as the U.S. continued its recovery from COVID and navigated growing

disruptions to global shipping and production. Even while dealing with supply-chain uncertainty, shipping delays,

product shortages, and reduced new-vehicle sales, 2021 was another great year for the specialty-equipment industry

overall. Consumers spent more time than in a typical year working on their vehicles and as restrictions eased on in-

person contact, returned to in-store shopping and auto events.

That said, there are still more headwinds as we head work through 2022. The supply-chain and logistical challenges

that began to emerge in 2021 have not been addressed as quickly as many had hoped, and it’s looking like they may

persist through 2022. While we do not expect sales to decline in 2022, our forecast calls for more modest growth—

though some economists believe a downturn may arrive this year, which could further dampen consumer spending.

As of now, our estimates are that supply issues will clear up in 2023 and the industry will ramp back up towards our

historical growth trend. Still, businesses should be paying attention to the economic headwinds going forward.

2022* 2023* 2025*2024*

$51.75

$53.71

$56.13

$58.66

$60.00

$0.00

$30.00

SPECIALTY-EQUIPMENT RETAIL SALES $ BILLIONS

Source: 2021 SEMA US Market Data

*FORECAST

20152014 2016 2017 2018 2019 2020 2021

$37.18

$39.09

$41.16

$42.92

$44.59

$46.20

$47.89

$50.90

5

Market Overview 2022 SEMA Market Report

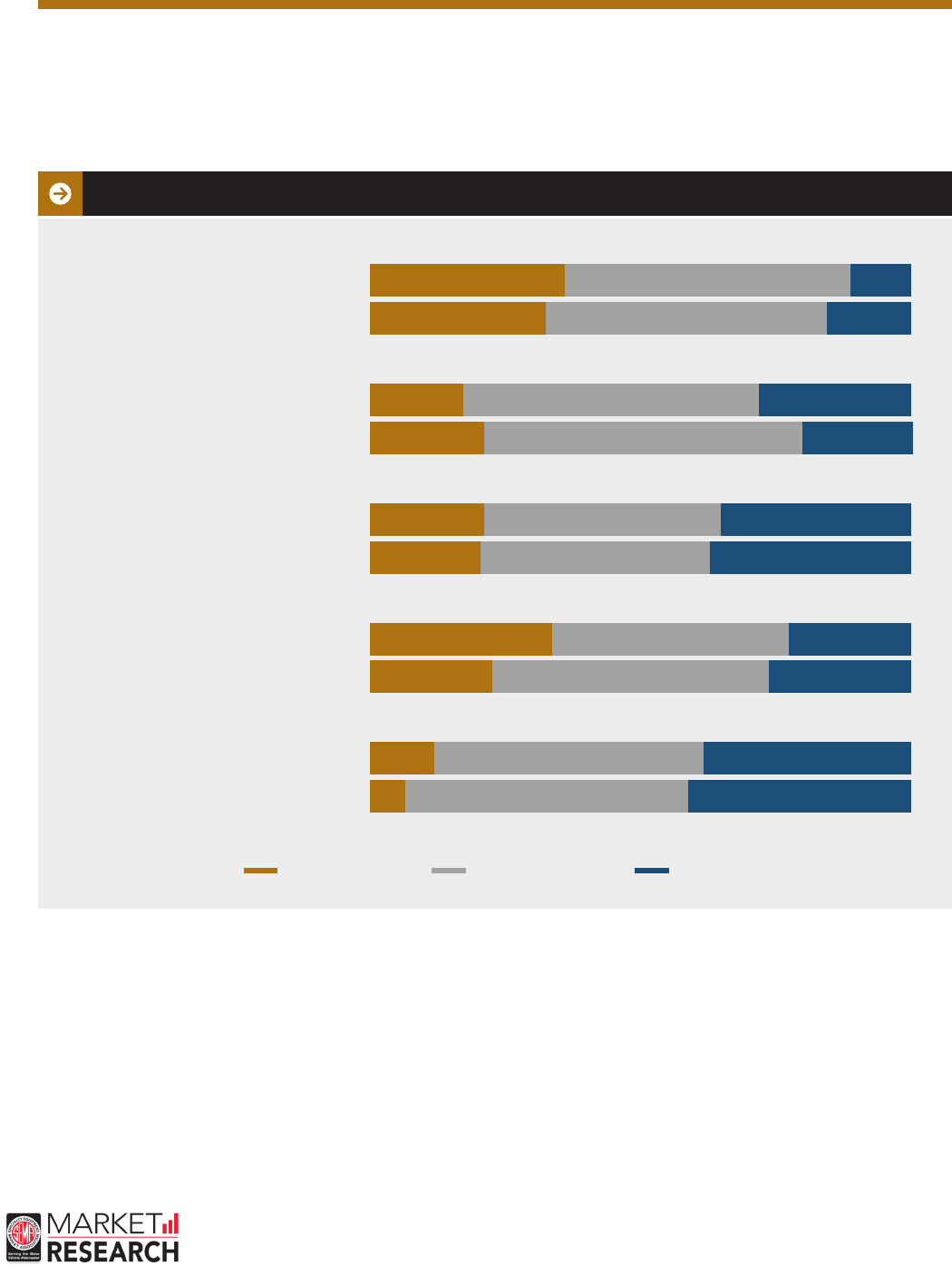

While the specialty-equipment market typically sees a higher share of online sales than the overall economy, in-

store retail channels have historically provided the bulk of automotive specialty parts to consumers. Pandemic

disruptions pushed even more sales into online channels during 2020. That online shift seems to be a short-term

spike that was partially normalized in 2021, as online and in-person sales evened out.

The cost, complexity, size, ease of install, and local availability of all impact where a given product type is likely

to be bought. Engine products, for instance, are more likely to be sourced from specialized retailers, while more

commoditized products like batteries and chemicals see a higher share of dollars flow through traditional auto-

parts chains. And for more niche vehicles or objectives, like restoring a classic, there may not be any local stores

that carry the exact parts a consumer needs. SEMA also consistently finds that accessorizers may favor going

online for inexpensive, easy-to-install parts, but value getting in-person advice and expertise with complex or big-

ticket products.

2021 CONSUMER PURCHASE ESTIMATES BY SALES CHANNEL % OF SALES Source: 2021 SEMA US Market Data

9%

7%

6%

6%

5%

4%

4%

3%

3%

1%

3%

2%

10%

10%

14%

14%

AUTO PARTS CHAINS – PHYSICAL LOCATION

AutoZone, NAPA, etc.

SPECIALTY RETAILER / INSTALLER – ONLINE

RockAuto, Speed Shop, Truck Accessory Shop, etc.

NEW VEHICLE DEALERSHIP

AUTO PARTS CHAINS – ONLINE

AutoZone, NAPA, etc.

ONLINE ONLY GENERAL RETAILER

e.g. Amazon

SPECIALTY RETAILER / INSTALLER – PHYSICAL LOCATION

Speed Shop, Truck Accessory Shop, etc.

GENERAL RETAIL CHAINS – PHYSICAL LOCATION

Target, Walmart, etc.

TIRE SHOP – PHYSICAL LOCATION

Discount Tire, Firestone Complete Auto Care, etc.

DIRECT FROM PARTS MANUFACTURER – ONLINE

GENERAL RETAIL CHAINS – ONLINE

Target, Walmart, etc.

TIRE SHOP – ONLINE

Discount Tire, Firestone Complete Auto Care, etc.

ONLINE MARKETPLACE / AUCTION SITE

e.g. eBay

DIRECT FROM PARTS MANUFACTURER – PHYSICAL LOCATION

CAR / TRUCK SHOW

OTHER – PHYSICAL LOCATION

OTHER ONLINE

6

Market Overview 2022 SEMA Market Report

Pickup parts remained big business for the specialty-equipment market in 2021, accounting for 31% of retail sales.

Crossover utility vehicles (CUVs), midsize/large cars, and sport utility vehicles (SUVs, including the Jeep Wrangler)

also account for significant shares of the market. These are also the most common vehicle types on the road today.

Some vehicle models are more likely to be modified (or modified more heavily) than others, but our industry is as

diverse as the vehicle population itself. Products are made, and sold, for all types of cars and trucks.

It’s also worth noting that dierent segments inspire dierent types of modifications. The vehicle segment section of

the report details which part categories are preferred by each vehicle-type owner.

2021 CONSUMER PURCHASE ESTIMATES BY VEHICLE SEGMENT % OF SALES

Source: 2021 SEMA US Market Data

50%

0%

25%

MIDSIZE /

LARGE CAR

SMALL

CAR

SPORTS

CAR

ALTERNATIVE

POWER

CUV SUV PICKUP VAN CLASSIC

10%

16%

6%

4%

12%

14%

3%

5%

31%

Readers of our previous reports may notice that the vehicles segments reported have changed somewhat. We follow

the vehicle segmentation of our VIO data provider Experian Automotive, who has recently updated their segments to

better represent the vehicle fleet. These changes will be reflected throughout this report.

7

Market Sizing

Source: 2021 SEMA US Market Data

2022 SEMA Market Report

ACCESSORY AND APPEARANCE PRODUCTS: $26.73 BILLION

2021 CONSUMER PURCHASE ESTIMATES $ BILLIONS

MARKET SIZE 2022 FORECAST2021

CHEMICALS

$7.77

$7.89

Maintenance Oils and Additives

$4.58

Wax and Cleaning Products

$1.94

Paint Powdercoating and Plating $1.26

EXTERIOR

BODY

$

$

Fender, Hood, and Body Upgrades

$

Exterior Appearance Upgrades

$

Body Finishing Products $

UTILITY

ACCESSORIES

$3.79

$3.87

Trailer and Towing Products

$0.96

Truck Bedliners and Other Bed Accessories

$0.84

Racks and Carriers

$0.82

Truck Bed Covers

$0.63

Truck Caps $0.54

INTERIOR

$2.68

$2.73

Seats and Upholstery

$1.04

Floor Mats and Interior Appearance Products

$0.98

Dash System and Gauges $0.67

LIGHTING

$2.39

$2.43

Head / Tail Lights

$1.40

Exterior Accessory Lighting

$0.79

Interior Lights $0.21

MOBILE

ELECTRONICS

$3.41

$3.44

Sound System and Audio Accessories

$1.12

Alarms and Security Products

$0.87

Navigation Systems

$0.49

Mobile TV and Video Cameras

$0.47

Wireless and Smartphone Integration Products $0.47

DRIVER

ASSIST

SYSTEMS

$0.76

$0.78

Driver Assist Systems

$0.76

EXTERIOR

BODY

$5.92

$6.02

Fender, Hood, and Body Upgrades

$2.10

Exterior Appearance Upgrades

$2.05

Body Finishing Products $1.77

8

Market Sizing

Source: 2021 SEMA US Market Data

2022 SEMA Market Report

2021 CONSUMER PURCHASE ESTIMATE $ BILLIONS

PERFORMANCE PRODUCTS: $12.23 BILLION

WHEELS, TIRES AND SUSPENSION: $11.94 BILLION

MARKET SIZE 2022 FORECAST2021

DRIVETRAIN

$3.61

$3.65

Transmission Products

$2.14

Axles and Dierential

$0.82

Clutches and Related Products

$0.55

Shifters $0.10

ENGINE

ELECTRICAL

AND IGNITION

$2.00

$2.03

Ignition Products

$0.91

Engine Control and Computer Products

$0.56

Batteries and Related Products $0.53

ENGINE

INTERNAL

AND COOLING

$2.26

$2.30

Internal Engine Products

$1.60

Cooling System Products

$0.39

Engine Dress-Up Products $0.27

INTAKE /

FUEL /

EXHAUST

$3.83

$3.91

Exhaust Products

$1.60

Forced Induction Systems

$0.82

Air Intake Products

$0.81

Carburetor and Fuel System Products $0.60

SAFETY

GEAR

$0.53

$0.54

Roll Cage and Safety Products

$0.38

Racing and Protection Apparel $0.14

SUSPENSION /

BRAKES /

STEERING

$5.47

$5.58

Suspension Products

$2.96

Brake Products

$2.34

Steering Products $0.18

WHEELS /

TIRES

$6.47

$6.60

Performance / Special Purpose Tires

$2.79

O-Road / Oversize Tires

$2.13

Custom Wheels $1.55

9

Market Sizing

Source: 2021 SEMA US Market Data

2022 SEMA Market Report

SALES CHANNEL – SHARE OF DOLLARS

PHYSICAL LOCATION

Auto Parts Chains

35%

Car / Truck Show

1%

Direct from Parts Manufacturer

1%

General Retail Chains

17%

New Vehicle Dealership

7%

Specialty Retailer/Installer

4%

Tire Shop

4%

Other

2%

ONLINE

Auto Parts Chains

11%

Direct from Parts Manufacturer

1%

General Retail Chains

5%

Online Marketplace/Auction Site

1%

Online Only General Retailer

5%

Specialty Retailer/Installer

2%

Tire Shop

1%

Other

1%

VEHICLE SEGMENT – SHARE OF DOLLARS

Small Car

15%

Midsize / Large Car

18%

Sports Car

4%

Alternative Power

2%

CUV

15%

SUV

10%

Pickup

27%

Van

5%

Classic

4%

ORDERED ONLINE

MANUFACTURERS WITH SALES GROWTH

96%

EXAMPLE PARTS

Engine Treatments, Engine / Injector Cleaner,

Fuel Additives, Performance ATF,

Performance Gear Oil,

Performance Motor Oil / Synthetic Oil

ORDERED IN-STORE

MAINTENANCE OILS AND ADDITIVES

DIY INSTALLATION SHARE

76%

OF PURCHASES

2018

MARKET SIZE

$4.10

BILLION

2019

MARKET SIZE

$4.23

BILLION

2020

MARKET SIZE

$4.35

BILLION

2021

MARKET SIZE

$4.58

BILLION

SHIPPED

TO HOME

16%

OF PURCHASES

IN-STORE

PICKUP/INSTALL

12%

OF PURCHASES

SHIPPED

TO HOME

7%

OF PURCHASES

IN-STORE

PICKUP/INSTALL

65%

OF PURCHASES

10

Market Sizing

Source: 2021 SEMA US Market Data

2022 SEMA Market Report

WAX AND CLEANING PRODUCTS

SALES CHANNEL – SHARE OF DOLLARS

PHYSICAL LOCATION

Auto Parts Chains

26%

Car / Truck Show

1%

Direct from Parts Manufacturer

1%

General Retail Chains

25%

New Vehicle Dealership

4%

Specialty Retailer/Installer

3%

Tire Shop

1%

Other

1%

ONLINE

Auto Parts Chains

11%

Direct from Parts Manufacturer

1%

General Retail Chains

9%

Online Marketplace/Auction Site

1%

Online Only General Retailer

11%

Specialty Retailer/Installer

4%

Tire Shop

1%

Other

1%

VEHICLE SEGMENT – SHARE OF DOLLARS

Small Car

15%

Midsize / Large Car

17%

Sports Car

5%

Alternative Power

3%

CUV

16%

SUV

11%

Pickup

23%

Van

5%

Classic

6%

ORDERED ONLINE

MANUFACTURERS WITH SALES GROWTH

91%

EXAMPLE PARTS

Cleaning Products (interior or exterior),

Polish / Wax,

Other Chemicals

ORDERED IN-STORE

DIY INSTALLATION SHARE

90%

OF PURCHASES

2018

MARKET SIZE

$1.80

BILLION

2019

MARKET SIZE

$1.85

BILLION

2020

MARKET SIZE

$1.86

BILLION

2021

MARKET SIZE

$1.94

BILLION

SHIPPED

TO HOME

30%

OF PURCHASES

IN-STORE

PICKUP/INSTALL

9%

OF PURCHASES

SHIPPED

TO HOME

6%

OF PURCHASES

IN-STORE

PICKUP/INSTALL

55%

OF PURCHASES

11

Market Sizing

Source: 2021 SEMA US Market Data

2022 SEMA Market Report

PAINT POWDERCOATING AND PLATING

SALES CHANNEL – SHARE OF DOLLARS

PHYSICAL LOCATION

Auto Parts Chains

18%

Car / Truck Show

3%

Direct from Parts Manufacturer

3%

General Retail Chains

8%

New Vehicle Dealership

14%

Specialty Retailer/Installer

9%

Tire Shop

<

1%

Other

5%

ONLINE

Auto Parts Chains

12%

Direct from Parts Manufacturer

4%

General Retail Chains

3%

Online Marketplace/Auction Site

1%

Online Only General Retailer

6%

Specialty Retailer/Installer

13%

Tire Shop

1%

Other

1%

VEHICLE SEGMENT – SHARE OF DOLLARS

Small Car

16%

Midsize / Large Car

29%

Sports Car

4%

Alternative Power

2%

CUV

6%

SUV

16%

Pickup

18%

Van

1%

Classic

8%

ORDERED ONLINE

MANUFACTURERS WITH SALES GROWTH

94%

EXAMPLE PARTS

Paint Powdercoating / Plating

ORDERED IN-STORE

DIY INSTALLATION SHARE

64%

OF PURCHASES

2018

MARKET SIZE

$1.14

BILLION

2019

MARKET SIZE

$1.16

BILLION

20120

MARKET SIZE

$1.21

BILLION

2021

MARKET SIZE

$1.26

BILLION

SHIPPED

TO HOME

26%

OF PURCHASES

IN-STORE

PICKUP/INSTALL

21%

OF PURCHASES

SHIPPED

TO HOME

6%

OF PURCHASES

IN-STORE

PICKUP/INSTALL

47%

OF PURCHASES

12

Market Sizing

Source: 2021 SEMA US Market Data

2022 SEMA Market Report

FENDER, HOOD AND BODY UPGRADES

SALES CHANNEL – SHARE OF DOLLARS

PHYSICAL LOCATION

Auto Parts Chains

8%

Car / Truck Show

3%

Direct from Parts Manufacturer

3%

General Retail Chains

1%

New Vehicle Dealership

13%

Specialty Retailer/Installer

9%

Tire Shop

2%

Other

1%

ONLINE

Auto Parts Chains

9%

Direct from Parts Manufacturer

7%

General Retail Chains

2%

Online Marketplace/Auction Site

6%

Online Only General Retailer

11%

Specialty Retailer/Installer

19%

Tire Shop

3%

Other

2%

VEHICLE SEGMENT – SHARE OF DOLLARS

Small Car

10%

Midsize / Large Car

11%

Sports Car

12%

Alternative Power

8%

CUV

11%

SUV

14%

Pickup

29%

Van

2%

Classic

2%

ORDERED ONLINE

MANUFACTURERS WITH SALES GROWTH

83%

EXAMPLE PARTS

Fenders, Hood, Body Modifications,

Bumper / Grille Guard / Step Bumper

ORDERED IN-STORE

DIY INSTALLATION SHARE

53%

OF PURCHASES

2018

MARKET SIZE

$1.84

BILLION

2019

MARKET SIZE

$1.91

BILLION

2020

MARKET SIZE

$1.97

BILLION

2021

MARKET SIZE

$2.10

BILLION

SHIPPED

TO HOME

50%

OF PURCHASES

IN-STORE

PICKUP/INSTALL

19%

OF PURCHASES

SHIPPED

TO HOME

7%

OF PURCHASES

IN-STORE

PICKUP/INSTALL

24%

OF PURCHASES

NOTE: Product category definition has changed since previous report.

NOTE: Product category definition has changed since previous report.

13

Market Sizing

Source: 2021 SEMA US Market Data

2022 SEMA Market Report

EXTERIOR APPEARANCE UPGRADES

SALES CHANNEL – SHARE OF DOLLARS

PHYSICAL LOCATION

Auto Parts Chains

8%

Car / Truck Show

2%

Direct from Parts Manufacturer

3%

General Retail Chains

2%

New Vehicle Dealership

13%

Specialty Retailer/Installer

9%

Tire Shop

1%

Other

3%

ONLINE

Auto Parts Chains

10%

Direct from Parts Manufacturer

6%

General Retail Chains

3%

Online Marketplace/Auction Site

6%

Online Only General Retailer

16%

Specialty Retailer/Installer

16%

Tire Shop

1%

Other

2%

VEHICLE SEGMENT – SHARE OF DOLLARS

Small Car

4%

Midsize / Large Car

9%

Sports Car

3%

Alternative Power

3%

CUV

12%

SUV

18%

Pickup

48%

Van

1%

Classic

2%

ORDERED ONLINE

MANUFACTURERS WITH SALES GROWTH

79%

EXAMPLE PARTS

Grille, Side Steps / Running Boards,

Mirrors, Sunroof / Moonroof,

Window Shades / Vents, Car Covers,

Other Exterior Body Upgrades

ORDERED IN-STORE

DIY INSTALLATION SHARE

66%

OF PURCHASES

2018

MARKET SIZE

$1.70

BILLION

2019

MARKET SIZE

$1.76

BILLION

2020

MARKET SIZE

$1.92

BILLION

2021

MARKET SIZE

$2.05

BILLION

SHIPPED

TO HOME

54%

OF PURCHASES

IN-STORE

PICKUP/INSTALL

13%

OF PURCHASES

SHIPPED

TO HOME

8%

OF PURCHASES

IN-STORE

PICKUP/INSTALL

25%

OF PURCHASES

NOTE: Product category definition has changed since previous report.

14

Market Sizing

Source: 2021 SEMA US Market Data

2022 SEMA Market Report

BODY FINISHING PRODUCTS

SALES CHANNEL – SHARE OF DOLLARS

PHYSICAL LOCATION

Auto Parts Chains

8%

Car / Truck Show

2%

Direct from Parts Manufacturer

2%

General Retail Chains

5%

New Vehicle Dealership

10%

Specialty Retailer/Installer

14%

Tire Shop

2%

Other

5%

ONLINE

Auto Parts Chains

7%

Direct from Parts Manufacturer

4%

General Retail Chains

5%

Online Marketplace/Auction Site

5%

Online Only General Retailer

18%

Specialty Retailer/Installer

8%

Tire Shop

2%

Other

3%

VEHICLE SEGMENT – SHARE OF DOLLARS

Small Car

10%

Midsize / Large Car

15%

Sports Car

8%

Alternative Power

6%

CUV

12%

SUV

20%

Pickup

21%

Van

5%

Classic

3%

ORDERED ONLINE

MANUFACTURERS WITH SALES GROWTH

61%

EXAMPLE PARTS

Decals / Graphics / Emblems / Wraps,

Window Tinting / Lamination

ORDERED IN-STORE

DIY INSTALLATION SHARE

54%

OF PURCHASES

2018

MARKET SIZE

$1.53

BILLION

2019

MARKET SIZE

$1.58

BILLION

2020

MARKET SIZE

$1.67

BILLION

2021

MARKET SIZE

$1.77

BILLION

SHIPPED

TO HOME

37%

OF PURCHASES

IN-STORE

PICKUP/INSTALL

16%

OF PURCHASES

SHIPPED

TO HOME

5%

OF PURCHASES

IN-STORE

PICKUP/INSTALL

43%

OF PURCHASES

15

Market Sizing

Source: 2021 SEMA US Market Data

2022 SEMA Market Report

TRAILER AND TOWING PRODUCTS

SALES CHANNEL – SHARE OF DOLLARS

PHYSICAL LOCATION

Auto Parts Chains

13%

Car / Truck Show

1%

Direct from Parts Manufacturer

3%

General Retail Chains

7%

New Vehicle Dealership

9%

Specialty Retailer/Installer

8%

Tire Shop

2%

Other

3%

ONLINE

Auto Parts Chains

11%

Direct from Parts Manufacturer

6%

General Retail Chains

3%

Online Marketplace/Auction Site

4%

Online Only General Retailer

12%

Specialty Retailer/Installer

13%

Tire Shop

2%

Other

2%

VEHICLE SEGMENT – SHARE OF DOLLARS

Small Car

<

1%

Midsize / Large Car

1%

Sports Car

0%

Alternative Power

5%

CUV

11%

SUV

14%

Pickup

60%

Van

6%

Classic

3%

ORDERED ONLINE

MANUFACTURERS WITH SALES GROWTH

96%

EXAMPLE PARTS

Trailer Hitch,

Winch

ORDERED IN-STORE

DIY INSTALLATION SHARE

71%

OF PURCHASES

2018

MARKET SIZE

$0.81

BILLION

2019

MARKET SIZE

$0.85

BILLION

2020

MARKET SIZE

$0.90

BILLION

2021

MARKET SIZE

$0.96

BILLION

SHIPPED

TO HOME

40%

OF PURCHASES

IN-STORE

PICKUP/INSTALL

15%

OF PURCHASES

SHIPPED

TO HOME

7%

OF PURCHASES

IN-STORE

PICKUP/INSTALL

38%

OF PURCHASES

16

Market Sizing

Source: 2021 SEMA US Market Data

2022 SEMA Market Report

TRUCK BEDLINERS AND OTHER BED ACCESSORIES

SALES CHANNEL – SHARE OF DOLLARS

PHYSICAL LOCATION

Auto Parts Chains

11%

Car / Truck Show

1%

Direct from Parts Manufacturer

3%

General Retail Chains

8%

New Vehicle Dealership

13%

Specialty Retailer/Installer

15%

Tire Shop

1%

Other

4%

ONLINE

Auto Parts Chains

9%

Direct from Parts Manufacturer

7%

General Retail Chains

3%

Online Marketplace/Auction Site

3%

Online Only General Retailer

6%

Specialty Retailer/Installer

14%

Tire Shop

1%

Other

2%

VEHICLE SEGMENT – SHARE OF DOLLARS

Small Car

0%

Midsize / Large Car

0%

Sports Car

0%

Alternative Power

<

1%

CUV

<

1%

SUV

<

1%

Pickup

98%

Van

0%

Classic

<

1%

ORDERED ONLINE

MANUFACTURERS WITH SALES GROWTH

86%

EXAMPLE PARTS

Pickup Bed Rack System,

Drop-in or Spray Bedliner,

Tool Box

ORDERED IN-STORE

DIY INSTALLATION SHARE

57%

OF PURCHASES

2018

MARKET SIZE

$0.72

BILLION

2019

MARKET SIZE

$0.74

BILLION

2020

MARKET SIZE

$0.78

BILLION

2021

MARKET SIZE

$0.84

BILLION

SHIPPED

TO HOME

29%

OF PURCHASES

IN-STORE

PICKUP/INSTALL

24%

OF PURCHASES

SHIPPED

TO HOME

8%

OF PURCHASES

IN-STORE

PICKUP/INSTALL

39%

OF PURCHASES

17

Market Sizing

Source: 2021 SEMA US Market Data

2022 SEMA Market Report

RACKS AND CARRIERS

SALES CHANNEL – SHARE OF DOLLARS

PHYSICAL LOCATION

Auto Parts Chains

6%

Car / Truck Show

2%

Direct from Parts Manufacturer

2%

General Retail Chains

4%

New Vehicle Dealership

14%

Specialty Retailer/Installer

10%

Tire Shop

1%

Other

2%

ONLINE

Auto Parts Chains

10%

Direct from Parts Manufacturer

6%

General Retail Chains

5%

Online Marketplace/Auction Site

4%

Online Only General Retailer

17%

Specialty Retailer/Installer

13%

Tire Shop

1%

Other

3%

VEHICLE SEGMENT – SHARE OF DOLLARS

Small Car

2%

Midsize / Large Car

3%

Sports Car

<

1%

Alternative Power

3%

CUV

30%

SUV

24%

Pickup

31%

Van

7%

Classic

1%

ORDERED ONLINE

MANUFACTURERS WITH SALES GROWTH

88%

EXAMPLE PARTS

Hitch Mounted Cargo Carrier,

Roof Rack / Carriers,

Mounted Tent (Roof / Truck Bed),

Other Exterior Accessories

ORDERED IN-STORE

DIY INSTALLATION SHARE

61%

OF PURCHASES

2018

MARKET SIZE

$0.71

BILLION

2019

MARKET SIZE

$0.80

BILLION

2020

MARKET SIZE

$0.76

BILLION

2021

MARKET SIZE

$0.82

BILLION

SHIPPED

TO HOME

49%

OF PURCHASES

IN-STORE

PICKUP/INSTALL

17%

OF PURCHASES

SHIPPED

TO HOME

7%

OF PURCHASES

IN-STORE

PICKUP/INSTALL

27%

OF PURCHASES

18

Market Sizing

Source: 2021 SEMA US Market Data

2022 SEMA Market Report

TRUCK BED COVERS

SALES CHANNEL – SHARE OF DOLLARS

PHYSICAL LOCATION

Auto Parts Chains

3%

Car / Truck Show

1%

Direct from Parts Manufacturer

1%

General Retail Chains

<

1%

New Vehicle Dealership

11%

Specialty Retailer/Installer

17%

Tire Shop

<

1%

Other

2%

ONLINE

Auto Parts Chains

5%

Direct from Parts Manufacturer

8%

General Retail Chains

1%

Online Marketplace/Auction Site

6%

Online Only General Retailer

23%

Specialty Retailer/Installer

19%

Tire Shop

<

1%

Other

2%

VEHICLE SEGMENT – SHARE OF DOLLARS

Small Car

0%

Midsize / Large Car

0%

Sports Car

0%

Alternative Power

0%

CUV

0%

SUV

0%

Pickup

99%

Van

0%

Classic

<1%

ORDERED ONLINE

MANUFACTURERS WITH SALES GROWTH

88%

EXAMPLE PARTS

Pickup Tonneau Cover

ORDERED IN-STORE

DIY INSTALLATION SHARE

67%

OF PURCHASES

2018

MARKET SIZE

$0.52

BILLION

2019

MARKET SIZE

$0.54

BILLION

2020

MARKET SIZE

$0.58

BILLION

2021

MARKET SIZE

$0.63

BILLION

SHIPPED

TO HOME

55%

OF PURCHASES

IN-STORE

PICKUP/INSTALL

10%

OF PURCHASES

SHIPPED

TO HOME

6%

OF PURCHASES

IN-STORE

PICKUP/INSTALL

29%

OF PURCHASES

19

Market Sizing

Source: 2021 SEMA US Market Data

2022 SEMA Market Report

TRUCK CAPS

SALES CHANNEL – SHARE OF DOLLARS

PHYSICAL LOCATION

Auto Parts Chains

5%

Car / Truck Show

1%

Direct from Parts Manufacturer

3%

General Retail Chains

0%

New Vehicle Dealership

13%

Specialty Retailer/Installer

12%

Tire Shop

1%

Other

4%

ONLINE

Auto Parts Chains

18%

Direct from Parts Manufacturer

9%

General Retail Chains

3%

Online Marketplace/Auction Site

1%

Online Only General Retailer

11%

Specialty Retailer/Installer

14%

Tire Shop

<

1%

Other

3%

VEHICLE SEGMENT – SHARE OF DOLLARS

Small Car

0%

Midsize / Large Car

0%

Sports Car

0%

Alternative Power

0%

CUV

0%

SUV

1%

Pickup

95%

Van

0%

Classic

4%

ORDERED ONLINE

MANUFACTURERS WITH SALES GROWTH

78%

EXAMPLE PARTS

Pickup Truck Cap / Shell

ORDERED IN-STORE

DIY INSTALLATION SHARE

68%

OF PURCHASES

2018

MARKET SIZE

$0.50

BILLION

2019

MARKET SIZE

$0.51

BILLION

2020

MARKET SIZE

$0.51

BILLION

2021

MARKET SIZE

$0.54

BILLION

SHIPPED

TO HOME

48%

OF PURCHASES

IN-STORE

PICKUP/INSTALL

17%

OF PURCHASES

SHIPPED

TO HOME

3%

OF PURCHASES

IN-STORE

PICKUP/INSTALL

31%

OF PURCHASES

20

Market Sizing

Source: 2021 SEMA US Market Data

2022 SEMA Market Report

SEATS AND UPHOLSTERY

SALES CHANNEL – SHARE OF DOLLARS

PHYSICAL LOCATION

Auto Parts Chains

13%

Car / Truck Show

2%

Direct from Parts Manufacturer

3%

General Retail Chains

7%

New Vehicle Dealership

9%

Specialty Retailer/Installer

7%

Tire Shop

2%

Other

2%

ONLINE

Auto Parts Chains

10%

Direct from Parts Manufacturer

4%

General Retail Chains

7%

Online Marketplace/Auction Site

5%

Online Only General Retailer

16%

Specialty Retailer/Installer

10%

Tire Shop

2%

Other

2%

VEHICLE SEGMENT – SHARE OF DOLLARS

Small Car

7%

Midsize / Large Car

14%

Sports Car

7%

Alternative Power

6%

CUV

17%

SUV

14%

Pickup

19%

Van

6%

Classic

9%

ORDERED ONLINE

MANUFACTURERS WITH SALES GROWTH

74%

EXAMPLE PARTS

Custom Seats, Headliners,

Seat Covers / Dash Covers, Upholstery

ORDERED IN-STORE

DIY INSTALLATION SHARE

73%

OF PURCHASES

2018

MARKET SIZE

$0.92

BILLION

2019

MARKET SIZE

$0.95

BILLION

2020

MARKET SIZE

$0.97

BILLION

2021

MARKET SIZE

$1.04

BILLION

SHIPPED

TO HOME

46%

OF PURCHASES

IN-STORE

PICKUP/INSTALL

15%

OF PURCHASES

SHIPPED

TO HOME

7%

OF PURCHASES

IN-STORE

PICKUP/INSTALL

32%

OF PURCHASES

NOTE: Product category definition has changed since previous report.

21

Market Sizing

Source: 2021 SEMA US Market Data

2022 SEMA Market Report

FLOOR MATS AND INTERIOR APPEARANCE PRODUCTS

SALES CHANNEL – SHARE OF DOLLARS

PHYSICAL LOCATION

Auto Parts Chains

12%

Car / Truck Show

1%

Direct from Parts Manufacturer

2%

General Retail Chains

8%

New Vehicle Dealership

11%

Specialty Retailer/Installer

3%

Tire Shop

2%

Other

1%

ONLINE

Auto Parts Chains

10%

Direct from Parts Manufacturer

7%

General Retail Chains

6%

Online Marketplace/Auction Site

5%

Online Only General Retailer

19%

Specialty Retailer/Installer

10%

Tire Shop

2%

Other

2%

VEHICLE SEGMENT – SHARE OF DOLLARS

Small Car

8%

Midsize / Large Car

16%

Sports Car

4%

Alternative Power

5%

CUV

21%

SUV

12%

Pickup

23%

Van

6%

Classic

5%

ORDERED ONLINE

MANUFACTURERS WITH SALES GROWTH

73%

EXAMPLE PARTS

Cargo / Trunk Mat,

Custom Floor Mats/Carpeting

Knobs / Handles, Interior Mirrors,

Pedals, Other Interior Products

ORDERED IN-STORE

DIY INSTALLATION SHARE

77%

OF PURCHASES

2018

MARKET SIZE

$0.88

BILLION

2019

MARKET SIZE

$0.90

BILLION

2020

MARKET SIZE

$0.92

BILLION

2021

MARKET SIZE

$0.98

BILLION

SHIPPED

TO HOME

52%

OF PURCHASES

IN-STORE

PICKUP/INSTALL

13%

OF PURCHASES

SHIPPED

TO HOME

8%

OF PURCHASES

IN-STORE

PICKUP/INSTALL

27%

OF PURCHASES

NOTE: Product category definition has changed since previous report.

22

Market Sizing

Source: 2021 SEMA US Market Data

2022 SEMA Market Report

DASH SYSTEM AND GAUGES

SALES CHANNEL – SHARE OF DOLLARS

PHYSICAL LOCATION

Auto Parts Chains

12%

Car / Truck Show

2%

Direct from Parts Manufacturer

4%

General Retail Chains

3%

New Vehicle Dealership

13%

Specialty Retailer/Installer

4%

Tire Shop

3%

Other

3%

ONLINE

Auto Parts Chains

16%

Direct from Parts Manufacturer

6%

General Retail Chains

5%

Online Marketplace/Auction Site

4%

Online Only General Retailer

10%

Specialty Retailer/Installer

12%

Tire Shop

4%

Other

<

1%

VEHICLE SEGMENT – SHARE OF DOLLARS

Small Car

6%

Midsize / Large Car

16%

Sports Car

6%

Alternative Power

4%

CUV

15%

SUV

12%

Pickup

20%

Van

2%

Classic

18%

ORDERED ONLINE

MANUFACTURERS WITH SALES GROWTH

88%

EXAMPLE PARTS

Aftermarket Air Conditioning Kits,

Dash Kits, Custom Gauges

ORDERED IN-STORE

DIY INSTALLATION SHARE

60%

OF PURCHASES

2018

MARKET SIZE

$0.58

BILLION

2019

MARKET SIZE

$0.61

BILLION

2020

MARKET SIZE

$0.63

BILLION

2021

MARKET SIZE

$0.67

BILLION

SHIPPED

TO HOME

52%

OF PURCHASES

IN-STORE

PICKUP/INSTALL

21%

OF PURCHASES

SHIPPED

TO HOME

7%

OF PURCHASES

IN-STORE

PICKUP/INSTALL

20%

OF PURCHASES

NOTE: Product category definition has changed since previous report.

23

Market Sizing

Source: 2021 SEMA US Market Data

2022 SEMA Market Report

HEAD / TAIL LIGHTS

SALES CHANNEL – SHARE OF DOLLARS

PHYSICAL LOCATION

Auto Parts Chains

17%

Car / Truck Show

1%

Direct from Parts Manufacturer

1%

General Retail Chains

3%

New Vehicle Dealership

7%

Specialty Retailer/Installer

4%

Tire Shop

2%

Other

1%

ONLINE

Auto Parts Chains

15%

Direct from Parts Manufacturer

4%

General Retail Chains

3%

Online Marketplace/Auction Site

6%

Online Only General Retailer

17%

Specialty Retailer/Installer

14%

Tire Shop

2%

Other

2%

VEHICLE SEGMENT – SHARE OF DOLLARS

Small Car

12%

Midsize / Large Car

17%

Sports Car

5%

Alternative Power

4%

CUV

9%

SUV

17%

Pickup

29%

Van

2%

Classic

5%

ORDERED ONLINE

MANUFACTURERS WITH SALES GROWTH

67%

EXAMPLE PARTS

Head Light / Tail Light Housings / Covers / etc,

Upgrade Replacement Bulbs

ORDERED IN-STORE

DIY INSTALLATION SHARE

74%

OF PURCHASES

2018

MARKET SIZE

$1.26

BILLION

2019

MARKET SIZE

$1.31

BILLION

2020

MARKET SIZE

$1.31

BILLION

2021

MARKET SIZE

$1.40

BILLION

SHIPPED

TO HOME

53%

OF PURCHASES

IN-STORE

PICKUP/INSTALL

13%

OF PURCHASES

SHIPPED

TO HOME

6%

OF PURCHASES

IN-STORE

PICKUP/INSTALL

28%

OF PURCHASES

24

Market Sizing

Source: 2021 SEMA US Market Data

2022 SEMA Market Report

EXTERIOR ACCESSORY LIGHTING

SALES CHANNEL – SHARE OF DOLLARS

PHYSICAL LOCATION

Auto Parts Chains

14%

Car / Truck Show

3%

Direct from Parts Manufacturer

2%

General Retail Chains

4%

New Vehicle Dealership

11%

Specialty Retailer/Installer

6%

Tire Shop

2%

Other

1%

ONLINE

Auto Parts Chains

13%

Direct from Parts Manufacturer

6%

General Retail Chains

4%

Online Marketplace/Auction Site

4%

Online Only General Retailer

17%

Specialty Retailer/Installer

12%

Tire Shop

2%

Other

1%

VEHICLE SEGMENT – SHARE OF DOLLARS

Small Car

10%

Midsize / Large Car

16%

Sports Car

4%

Alternative Power

6%

CUV

12%

SUV

16%

Pickup

32%

Van

2%

Classic

2%

ORDERED ONLINE

MANUFACTURERS WITH SALES GROWTH

87%

EXAMPLE PARTS

Exterior Lighting Add-On,

Driving / Fog Lights,

Other Lighting Products

ORDERED IN-STORE

DIY INSTALLATION SHARE

69%

OF PURCHASES

2018

MARKET SIZE

$0.69

BILLION

2019

MARKET SIZE

$0.71

BILLION

2020

MARKET SIZE

$0.74

BILLION

2021

MARKET SIZE

$0.79

BILLION

SHIPPED

TO HOME

52%

OF PURCHASES

IN-STORE

PICKUP/INSTALL

14%

OF PURCHASES

SHIPPED

TO HOME

7%

OF PURCHASES

IN-STORE

PICKUP/INSTALL

28%

OF PURCHASES

25

Market Sizing

Source: 2021 SEMA US Market Data

2022 SEMA Market Report

INTERIOR LIGHTS

SALES CHANNEL – SHARE OF DOLLARS

PHYSICAL LOCATION

Auto Parts Chains

16%

Car / Truck Show

2%

Direct from Parts Manufacturer

2%

General Retail Chains

4%

New Vehicle Dealership

10%

Specialty Retailer/Installer

2%

Tire Shop

1%

Other

1%

ONLINE

Auto Parts Chains

13%

Direct from Parts Manufacturer

4%

General Retail Chains

5%

Online Marketplace/Auction Site

6%

Online Only General Retailer

20%

Specialty Retailer/Installer

11%

Tire Shop

2%

Other

1%

VEHICLE SEGMENT – SHARE OF DOLLARS

Small Car

17%

Midsize / Large Car

23%

Sports Car

6%

Alternative Power

6%

CUV

15%

SUV

11%

Pickup

16%

Van

1%

Classic

5%

ORDERED ONLINE

MANUFACTURERS WITH SALES GROWTH

80%

EXAMPLE PARTS

Interior Lighting

ORDERED IN-STORE

DIY INSTALLATION SHARE

70%

OF PURCHASES

2018

MARKET SIZE

$0.19

BILLION

2019

MARKET SIZE

$0.20

BILLION

2020

MARKET SIZE

$0.20

BILLION

2021

MARKET SIZE

$0.21

BILLION

SHIPPED

TO HOME

53%

OF PURCHASES

IN-STORE

PICKUP/INSTALL

15%

OF PURCHASES

SHIPPED

TO HOME

7%

OF PURCHASES

IN-STORE

PICKUP/INSTALL

25%

OF PURCHASES

26

Market Sizing

Source: 2021 SEMA US Market Data

2022 SEMA Market Report

SOUND SYSTEM AND AUDIO ACCESSORIES

SALES CHANNEL – SHARE OF DOLLARS

PHYSICAL LOCATION

Auto Parts Chains

8%

Car / Truck Show

2%

Direct from Parts Manufacturer

2%

General Retail Chains

9%

New Vehicle Dealership

7%

Specialty Retailer/Installer

9%

Tire Shop

2%

Other

3%

ONLINE

Auto Parts Chains

9%

Direct from Parts Manufacturer

4%

General Retail Chains

9%

Online Marketplace/Auction Site

6%

Online Only General Retailer

15%

Specialty Retailer/Installer

11%

Tire Shop

1%

Other

2%

VEHICLE SEGMENT – SHARE OF DOLLARS

Small Car

12%

Midsize / Large Car

18%

Sports Car

3%

Alternative Power

5%

CUV

9%

SUV

18%

Pickup

26%

Van

3%

Classic

7%

ORDERED ONLINE

MANUFACTURERS WITH SALES GROWTH

76%

EXAMPLE PARTS

Satellite Radio Add-On, In-Dash Stereo System,

Speakers / Subwoofer / Amplifier,

Other Mobile Electronics Products

ORDERED IN-STORE

DIY INSTALLATION SHARE

60%

OF PURCHASES

2018

MARKET SIZE

$1.03

BILLION

2019

MARKET SIZE

$1.03

BILLION

2020

MARKET SIZE

$1.06

BILLION

2021

MARKET SIZE

$1.12

BILLION

SHIPPED

TO HOME

41%

OF PURCHASES

IN-STORE

PICKUP/INSTALL

21%

OF PURCHASES

SHIPPED

TO HOME

4%

OF PURCHASES

IN-STORE

PICKUP/INSTALL

33%

OF PURCHASES

27

Market Sizing

Source: 2021 SEMA US Market Data

2022 SEMA Market Report

ALARMS AND SECURITY PRODUCTS

SALES CHANNEL – SHARE OF DOLLARS

PHYSICAL LOCATION

Auto Parts Chains

9%

Car / Truck Show

3%

Direct from Parts Manufacturer

4%

General Retail Chains

3%

New Vehicle Dealership

19%

Specialty Retailer/Installer

15%

Tire Shop

2%

Other

2%

ONLINE

Auto Parts Chains

11%

Direct from Parts Manufacturer

4%

General Retail Chains

5%

Online Marketplace/Auction Site

2%

Online Only General Retailer

11%

Specialty Retailer/Installer

8%

Tire Shop

3%

Other

1%

VEHICLE SEGMENT – SHARE OF DOLLARS

Small Car

10%

Midsize / Large Car

17%

Sports Car

8%

Alternative Power

10%

CUV

16%

SUV

9%

Pickup

28%

Van

3%

Classic

0%

ORDERED ONLINE

MANUFACTURERS WITH SALES GROWTH

N/A

EXAMPLE PARTS

Alarm / Remote Start / Keyless Entry

ORDERED IN-STORE

DIY INSTALLATION SHARE

42%

OF PURCHASES

2018

MARKET SIZE

$0.83

BILLION

2019

MARKET SIZE

$0.82

BILLION

2020

MARKET SIZE

$0.83

BILLION

2021

MARKET SIZE

$0.87

BILLION

SHIPPED

TO HOME

30%

OF PURCHASES

IN-STORE

PICKUP/INSTALL

21%

OF PURCHASES

SHIPPED

TO HOME

8%

OF PURCHASES

IN-STORE

PICKUP/INSTALL

41%

OF PURCHASES

28

Market Sizing

Source: 2021 SEMA US Market Data

2022 SEMA Market Report

NAVIGATION SYSTEMS

SALES CHANNEL – SHARE OF DOLLARS

PHYSICAL LOCATION

Auto Parts Chains

9%

Car / Truck Show

2%

Direct from Parts Manufacturer

4%

General Retail Chains

7%

New Vehicle Dealership

13%

Specialty Retailer/Installer

6%

Tire Shop

1%

Other

1%

ONLINE

Auto Parts Chains

12%

Direct from Parts Manufacturer

4%

General Retail Chains

11%

Online Marketplace/Auction Site

3%

Online Only General Retailer

15%

Specialty Retailer/Installer

7%

Tire Shop

2%

Other

1%

VEHICLE SEGMENT – SHARE OF DOLLARS

Small Car

10%

Midsize / Large Car

17%

Sports Car

5%

Alternative Power

10%

CUV

17%

SUV

12%

Pickup

21%

Van

4%

Classic

4%

ORDERED ONLINE

MANUFACTURERS WITH SALES GROWTH

N/A

EXAMPLE PARTS

GPS Navigation System

ORDERED IN-STORE

DIY INSTALLATION SHARE

56%

OF PURCHASES

2018

MARKET SIZE

$0.47

BILLION

2019

MARKET SIZE

$0.47

BILLION

2020

MARKET SIZE

$0.47

BILLION

2021

MARKET SIZE

$0.49

BILLION

SHIPPED

TO HOME

40%

OF PURCHASES

IN-STORE

PICKUP/INSTALL

25%

OF PURCHASES

SHIPPED

TO HOME

8%

OF PURCHASES

IN-STORE

PICKUP/INSTALL

26%

OF PURCHASES

29

Market Sizing

Source: 2021 SEMA US Market Data

2022 SEMA Market Report

MOBILE TV AND VIDEO CAMERAS

SALES CHANNEL – SHARE OF DOLLARS

PHYSICAL LOCATION

Auto Parts Chains

6%

Car / Truck Show

3%

Direct from Parts Manufacturer

3%

General Retail Chains

11%

New Vehicle Dealership

11%

Specialty Retailer/Installer

6%

Tire Shop

3%

Other

1%

ONLINE

Auto Parts Chains

11%

Direct from Parts Manufacturer

4%

General Retail Chains

8%

Online Marketplace/Auction Site

4%

Online Only General Retailer

15%

Specialty Retailer/Installer

8%

Tire Shop

4%

Other

1%

VEHICLE SEGMENT – SHARE OF DOLLARS

Small Car

9%

Midsize / Large Car

15%

Sports Car

2%

Alternative Power

8%

CUV

18%

SUV

21%

Pickup

19%

Van

6%

Classic

2%

ORDERED ONLINE

MANUFACTURERS WITH SALES GROWTH

N/A

EXAMPLE PARTS

Dashboard Camera,

DVD Player / Video Monitor / Mobile Satellite TV

ORDERED IN-STORE

DIY INSTALLATION SHARE

61%

OF PURCHASES

2018

MARKET SIZE

$0.44

BILLION

2019

MARKET SIZE

$0.45

BILLION

2020

MARKET SIZE

$0.45

BILLION

2021

MARKET SIZE

$0.47

BILLION

SHIPPED

TO HOME

43%

OF PURCHASES

IN-STORE

PICKUP/INSTALL

22%

OF PURCHASES

SHIPPED

TO HOME

6%

OF PURCHASES

IN-STORE

PICKUP/INSTALL

29%

OF PURCHASES

30

Market Sizing

Source: 2021 SEMA US Market Data

2022 SEMA Market Report

WIRELESS AND SMARTPHONE INTEGRATION PRODUCTS

SALES CHANNEL – SHARE OF DOLLARS

PHYSICAL LOCATION

Auto Parts Chains

6%

Car / Truck Show

3%

Direct from Parts Manufacturer

4%

General Retail Chains

9%

New Vehicle Dealership

11%

Specialty Retailer/Installer

6%

Tire Shop

1%

Other

2%

ONLINE

Auto Parts Chains

11%

Direct from Parts Manufacturer

6%

General Retail Chains

9%

Online Marketplace/Auction Site

4%

Online Only General Retailer

15%

Specialty Retailer/Installer

10%

Tire Shop

2%

Other

1%

VEHICLE SEGMENT – SHARE OF DOLLARS

Small Car

15%

Midsize / Large Car

16%

Sports Car

7%

Alternative Power

6%

CUV

13%

SUV

16%

Pickup

22%

Van

2%

Classic

2%

ORDERED ONLINE

MANUFACTURERS WITH SALES GROWTH

N/A

EXAMPLE PARTS

In-Car Wi-Fi Access / Mobile Hot Spot,

Smartphone Integration - Hands-Free Talk,

Smartphone Integration - Stereo Connection

ORDERED IN-STORE

DIY INSTALLATION SHARE

54%

OF PURCHASES

2018

MARKET SIZE

$0.42

BILLION

2019

MARKET SIZE

$0.43

BILLION

2020

MARKET SIZE

$0.44

BILLION

2021

MARKET SIZE

$0.47

BILLION

SHIPPED

TO HOME

40%

OF PURCHASES

IN-STORE

PICKUP/INSTALL

23%

OF PURCHASES

SHIPPED

TO HOME

6%

OF PURCHASES

IN-STORE

PICKUP/INSTALL

31%

OF PURCHASES

31

Market Sizing

Source: 2021 SEMA US Market Data

2022 SEMA Market Report

DRIVER ASSIST SYSTEMS

SALES CHANNEL – SHARE OF DOLLARS

PHYSICAL LOCATION

Auto Parts Chains

8%

Car / Truck Show

2%

Direct from Parts Manufacturer

4%

General Retail Chains

3%

New Vehicle Dealership

25%

Specialty Retailer/Installer

4%

Tire Shop

1%

Other

1%

ONLINE

Auto Parts Chains

10%

Direct from Parts Manufacturer

5%

General Retail Chains

5%

Online Marketplace/Auction Site

7%

Online Only General Retailer

12%

Specialty Retailer/Installer

10%

Tire Shop

1%

Other

1%

VEHICLE SEGMENT – SHARE OF DOLLARS

Small Car

8%

Midsize / Large Car

15%

Sports Car

4%

Alternative Power

8%

CUV

21%

SUV

13%

Pickup

25%

Van

4%

Classic

0%

ORDERED ONLINE

MANUFACTURERS WITH SALES GROWTH

N/A

EXAMPLE PARTS

Backup Camera / Sensors, Blind Spot Monitoring

Front Collision Warning,

Lane Departure Warning,

Adaptive Cruise Control,

Other Driver Assist Systems

ORDERED IN-STORE

DIY INSTALLATION SHARE

40%

OF PURCHASES

2018

MARKET SIZE

$0.68

BILLION

2019

MARKET SIZE

$0.71

BILLION

2020

MARKET SIZE

$0.71

BILLION

2021

MARKET SIZE

$0.76

BILLION

SHIPPED

TO HOME

39%

OF PURCHASES

IN-STORE

PICKUP/INSTALL

26%

OF PURCHASES

SHIPPED

TO HOME

6%

OF PURCHASES

IN-STORE

PICKUP/INSTALL

29%

OF PURCHASES

32

Market Sizing

Source: 2021 SEMA US Market Data

2022 SEMA Market Report

TRANSMISSION PRODUCTS

SALES CHANNEL – SHARE OF DOLLARS

PHYSICAL LOCATION

Auto Parts Chains

11%

Car / Truck Show

6%

Direct from Parts Manufacturer

6%

General Retail Chains

1%

New Vehicle Dealership

11%

Specialty Retailer/Installer

6%

Tire Shop

3%

Other

6%

ONLINE

Auto Parts Chains

12%

Direct from Parts Manufacturer

9%

General Retail Chains

1%

Online Marketplace/Auction Site

3%

Online Only General Retailer

4%

Specialty Retailer/Installer

17%

Tire Shop

1%

Other

3%

VEHICLE SEGMENT – SHARE OF DOLLARS

Small Car

8%

Midsize / Large Car

19%

Sports Car

7%

Alternative Power

2%

CUV

7%

SUV

18%

Pickup

31%

Van

3%

Classic

6%

ORDERED ONLINE

MANUFACTURERS WITH SALES GROWTH

69%

EXAMPLE PARTS

Bellhousing, Torque Converters,

Performance Upgrade/Replacement Transmission,

Transmission Cooler, Engine/Transmission Sensors,

Other Drivetrain Products

ORDERED IN-STORE

DIY INSTALLATION SHARE

44%

OF PURCHASES

2018

MARKET SIZE

$1.88

BILLION

2019

MARKET SIZE

$1.96

BILLION

2020

MARKET SIZE

$2.02

BILLION

2021

MARKET SIZE

$2.14

BILLION

SHIPPED

TO HOME

37%

OF PURCHASES

IN-STORE

PICKUP/INSTALL

22%

OF PURCHASES

SHIPPED

TO HOME

7%

OF PURCHASES

IN-STORE

PICKUP/INSTALL

34%

OF PURCHASES

33

Market Sizing

Source: 2021 SEMA US Market Data

2022 SEMA Market Report

AXLES AND DIFFERENTIAL

SALES CHANNEL – SHARE OF DOLLARS

PHYSICAL LOCATION

Auto Parts Chains

19%

Car / Truck Show

7%

Direct from Parts Manufacturer

2%

General Retail Chains

2%

New Vehicle Dealership

12%

Specialty Retailer/Installer

8%

Tire Shop

1%

Other

1%

ONLINE

Auto Parts Chains

12%

Direct from Parts Manufacturer

8%

General Retail Chains

4%

Online Marketplace/Auction Site

3%

Online Only General Retailer

4%

Specialty Retailer/Installer

14%

Tire Shop

1%

Other

1%

VEHICLE SEGMENT – SHARE OF DOLLARS

Small Car

8%

Midsize / Large Car

12%

Sports Car

5%

Alternative Power

3%

CUV

19%

SUV

31%

Pickup

18%

Van

<

1%

Classic

4%

ORDERED ONLINE

MANUFACTURERS WITH SALES GROWTH

78%

EXAMPLE PARTS

Axles, Driveshaft,

Limited Slip / Locking Differential /

Differential Housing / Ring & Pinion,

U-Joints

ORDERED IN-STORE

DIY INSTALLATION SHARE

58%

OF PURCHASES

2018

MARKET SIZE

$0.74

BILLION

2019

MARKET SIZE

$0.76

BILLION

2020

MARKET SIZE

$0.78

BILLION

2021

MARKET SIZE

$0.82

BILLION

SHIPPED

TO HOME

32%

OF PURCHASES

IN-STORE

PICKUP/INSTALL

23%

OF PURCHASES

SHIPPED

TO HOME

19%

OF PURCHASES

IN-STORE

PICKUP/INSTALL

26%

OF PURCHASES

34

Market Sizing

Source: 2021 SEMA US Market Data

2022 SEMA Market Report

CLUTCHES AND RELATED PRODUCTS

SALES CHANNEL – SHARE OF DOLLARS

PHYSICAL LOCATION

Auto Parts Chains

11%

Car / Truck Show

2%

Direct from Parts Manufacturer

5%

General Retail Chains

2%

New Vehicle Dealership

8%

Specialty Retailer/Installer

4%

Tire Shop

4%

Other

2%

ONLINE

Auto Parts Chains

21%

Direct from Parts Manufacturer

3%

General Retail Chains

2%

Online Marketplace/Auction Site

7%

Online Only General Retailer

2%

Specialty Retailer/Installer

20%

Tire Shop

7%

Other

0%

VEHICLE SEGMENT – SHARE OF DOLLARS

Small Car

16%

Midsize / Large Car

18%

Sports Car

11%

Alternative Power

1%

CUV

7%

SUV

15%

Pickup

30%

Van

1%

Classic

1%

ORDERED ONLINE

MANUFACTURERS WITH SALES GROWTH

62%

EXAMPLE PARTS

Clutches / Clutch Plates / Flywheel

ORDERED IN-STORE

DIY INSTALLATION SHARE

57%

OF PURCHASES

2018

MARKET SIZE

$0.47

BILLION

2019

MARKET SIZE

$0.50

BILLION

2020

MARKET SIZE

$0.51

BILLION

2021

MARKET SIZE

$0.55

BILLION

SHIPPED

TO HOME

40%

OF PURCHASES

IN-STORE

PICKUP/INSTALL

25%

OF PURCHASES

SHIPPED

TO HOME

9%

OF PURCHASES

IN-STORE

PICKUP/INSTALL

26%

OF PURCHASES

35

Market Sizing

Source: 2021 SEMA US Market Data

2022 SEMA Market Report

SHIFTERS

SALES CHANNEL – SHARE OF DOLLARS

PHYSICAL LOCATION

Auto Parts Chains

5%

Car / Truck Show

3%

Direct from Parts Manufacturer

1%

General Retail Chains

3%

New Vehicle Dealership

24%

Specialty Retailer/Installer

7%

Tire Shop

3%

Other

3%

ONLINE

Auto Parts Chains

8%

Direct from Parts Manufacturer

4%

General Retail Chains

4%

Online Marketplace/Auction Site

4%

Online Only General Retailer

7%

Specialty Retailer/Installer

13%

Tire Shop

5%

Other

7%

VEHICLE SEGMENT – SHARE OF DOLLARS

Small Car

15%

Midsize / Large Car

20%

Sports Car

10%

Alternative Power

1%

CUV

11%

SUV

10%

Pickup

11%

Van

3%

Classic

18%

ORDERED ONLINE

MANUFACTURERS WITH SALES GROWTH

63%

EXAMPLE PARTS

Shifter Knob / Handle, Short Throw Shifter

ORDERED IN-STORE

DIY INSTALLATION SHARE

57%

OF PURCHASES

2018

MARKET SIZE

$0.10

BILLION

2019

MARKET SIZE

$0.10

BILLION

2020

MARKET SIZE

$0.10

BILLION

2021

MARKET SIZE

$0.10

BILLION

SHIPPED

TO HOME

46%

OF PURCHASES

IN-STORE

PICKUP/INSTALL

13%

OF PURCHASES

SHIPPED

TO HOME

19%

OF PURCHASES

IN-STORE

PICKUP/INSTALL

22%

OF PURCHASES

36