Board of Governors of the Federal Reserve System

International Finance Discussion Papers

ISSN 1073-2500 (Print)

ISSN 2767-4509 (Online)

Number 1359

October 2022

Geopolitics and the U.S. Dollar’s Future as a Reserve Currency

Colin Weiss

Please cite this paper as:

Weiss, Colin (2022). “Geopolitics and the U.S. Dollar’s Future as a Reserve Currency,”

International Finance Discussion Papers 1359. Washington: Board of Governors of the

Federal Reserve System, https://doi.org/10.17016/IFDP.2022.1359.

NOTE: International Finance Discussion Papers (IFDPs) are preliminary materials circulated to stimu-

late discussion and critical comment. The analysis and conclusions set forth are those of the authors and

do not indicate concurrence by other members of the research staff or the Board of Governors. References

in publications to the International Finance Discussion Papers Series (other than acknowledgement) should

be cleared with the author(s) to protect the tentative character of these papers. Recent IFDPs are available

on the Web at www.federalreserve.gov/pubs/ifdp/. This paper can be downloaded without charge from the

Social Science Research Network electronic library at www.ssrn.com.

Geopolitics and the U.S. Dollar’s Future as a Reserve

Currency

Colin Weiss

*

Abstract

I survey the role of geopolitics and sanctions risk in shaping the U.S. dollar’s

status as the primary currency used for international reserves. Without

changes in the economic incentives for holding FX reserves in U.S. dollar

assets, an increased threat of sanctions is unlikely to drastically reduce the

dollar share of FX reserves. Currently, around three-quarters of foreign

government holdings of safe U.S. assets are by countries with some military

tie to the U.S. Even a reduced reliance on the U.S. dollar for trade invoicing

and debt denomination by a large bloc of countries less geopolitically

aligned with the U.S. would be unlikely to end U.S. dollar dominance.

Keywords: Foreign Exchange Reserves, Sanctions, Security Alliances

JEL Codes: F53, F51, F31

*

Division of International Finance, Board of Governors of the Federal Reserve System, Washington DC,

20551 USA. E-mail: colin.r.weiss@frb.gov

. I thank Daniel Beltran, Carol Bertaut, Bastian von Beschwitz,

Ricardo Correa, Jeffry Frieden, Daniel McDowell, Carla Norrlof, Alexandra Tabova, and Jason Wu for

encouragement and helpful comments. Workshop participants at the Federal Reserve provided useful

suggestions as well. The views expressed in this paper are solely my own and do not reflect the views of

the Board of Governors of the Federal Reserve or anyone else associated with the Federal Reserve

system. All errors are my own.

1

I. Introduction

Following bans on transaction with the Central Bank of Russia, Russia’s Ministry

of Finance, and Russia’s National Wealth Fund by the U.S., U.K., and member nations

of the European Union (EU) in February 2022, many have questioned how these

sanctions will affect the future of the U.S. dollar as a reserve currency.

1

These bans

effectively froze assets held by the Russian government in the U.S. and Europe,

preventing their use in cushioning the blow of other economic sanctions imposed

because of Russia’s invasion of Ukraine. In the past 10 years, the U.S. government

imposed similar sanctions on assets of the governments of Afghanistan, Iran, Libya, and

Venezuela, but the relative size of the Russian economy and the multilateral nature of

these sanctions have made them unprecedented. The prominence of the Russian

example has thus brought the question of how geopolitics can affect a government’s

willingness to hold international reserves in U.S. dollar assets to the fore.

This paper assesses how a greater emphasis on geopolitical relations may alter

the U.S. dollar’s share of foreign exchange (FX) reserves both over the next few years

and the next few decades. Work by political scientists and economists has found an

association between geopolitical ties with a reserve currency issuer and that currency’s

share of FX reserves, as holdings of an ally’s assets can serve as implicit support of the

issuer’s policies or as a means of assuring security guarantees from the reserve

currency issuer (Eichengreen, Chitu, Mehl, 2019; Iancu et al., 2020; Liao and McDowell,

1

Several newspapers published articles questioning whether countries would continue to hold FX

reserves in U.S. dollars in the wake of the sanctions on Russia. See

"The $300 Billion Question Facing

Central Banks" and "How the Ukraine War Would Boost China's Global Finance Ambitions" in the

Financial Times (March 2, 2022 and March 8, 2022, respectively) and "If Russian Currency Reserves

Aren't Really Money, the World Is in for a Shock" in the Wall Street Journal (March 3, 2022). Noted

money market analyst Zoltan Pozsar appeared on a Bloomberg podcast and raised similar questions.

Dooley, Folkerts-Landau, and Garber (2022) argued the opposite: these sanctions would strengthen the

U.S. dollar’s status as a reserve currency.

2

2016; McDowell, 2021). But, the empirical literature on military alliances and reserve

currency status is still relatively sparse, and there remain several open questions

(Norrlof, 2020). I specifically address two questions related to how geopolitics affect the

U.S. dollar’s role as a reserve currency. First, to what extent are U.S. dollar FX

reserves held by allies of the U.S.? Second, should the world become more stratified

along geopolitical lines, what implication would this have for the U.S. dollar’s reserve

status?

I answer the first question using confidential data on individual foreign

governments’ holdings of U.S. assets from the Treasury International Capital (TIC) data

and information on military alliances with the U.S. to separate holdings of U.S. dollar

reserves by geopolitical relation with the U.S. government.

2

I find that the majority (50-

60 percent) of safe U.S. assets held by foreign governments are consistently—over the

past 10 years—held by countries with strong geopolitical relations with the U.S.

3

When

countries with any form of military cooperation with the U.S. are considered as allies,

nearly three-quarters of the U.S. assets held by foreign governments are in the hands of

allies. Thus, while U.S. dollar reserves are no longer exclusively held by political allies

reliant on U.S. military support as they were from the 1960s through the 1980s, these

countries are still the most important set of reserve holders (Helleiner, 2008; Kirshner,

2008).

I explore the second question considering both the short and the long term. In

both cases, the threat to the U.S. dollar’s reserve currency status is relatively limited. In

the near-term, the U.S. dollar’s reserve currency status is buttressed both by close U.S.

2

Klein (2022) performs a similar exercise for total FX reserves.

3

I define strong geopolitical relations as having a mutual defense treaty with the U.S. or the designation

of a “major non-NATO ally” by the U.S. government.

3

allies (who are less likely to incur sanctions since they receive security guarantees from

the U.S. or hold similar political ideals as the U.S.) holding the majority of dollar-

denominated FX reserves and by countries with less formal military ties having strong

economic incentives to hold their FX reserves in U.S. dollar assets. These economic

motives are likely to remain substantial over the near-term, but—over the span of

decades—the economic incentives for holdings U.S. dollar reserves can change. Thus,

when considering long-term ramifications of increased risk of U.S. sanctions and

geopolitical fissures, I study a situation where countries without close diplomatic ties to

the U.S. move away from using the U.S. dollar as an international currency more

broadly. Specifically, I explore a scenario where many emerging and developing

economies (EMDEs) cease using the U.S. dollar as the invoicing currency for trade

amongst themselves, but instead use the Chinese renminbi (RMB).

While a move away from the U.S. dollar in trade invoicing among EMDEs would

likely lead to substantial divestment from U.S. dollar FX reserves, the U.S. dollar would

still denominate the largest share of FX reserve assets. I arrive at this conclusion first

using previous econometric estimates of the relationship between the U.S. dollar’s

share in export invoicing and its share in a country’s FX reserves.

4

I also find the same

when I use new econometric evidence for export invoicing and reserve currency shares

that tries to better address potential non-linearities in this relationship. I conduct a case

study of how six EMDEs in eastern Europe shifted away from the U.S. dollar for both

export invoicing and FX reserves following the introduction of the euro. The U.S. dollar

4

Ito and McCauley (2020) and Arslanalp, Eichengreen, and Simpson-Bell (2022) provide empirical

evidence on the relationship between export invoicing share and FX reserve share. Like this paper, Chinn

and Frankel (2008) also extrapolate from regression results to address an earlier question about the

status of the euro against the U.S. dollar. Mukhin (2022) uses a quantitative structural model to similarly

study how a global switch away from pegging exchange rates to the U.S. dollar would affect the dollar’s

use in trade invoicing.

4

invoiced a significant but not overwhelming share of these countries’ exports prior to the

creation of the euro, meaning the estimated relationship between export invoicing and

FX reserve composition for these countries over time is likely to be larger than an

estimate where the sample is primarily comprised of countries where the U.S. dollar

share of export invoicing is either close to zero or one (Chinn and Frankel, 2008).

Finally, I argue this scenario is not the most likely outcome but rather a risk scenario, as

facilitating such a large divestment from U.S. dollar reserve assets would require

significant changes to the international financial system.

The role of the U.S. dollar as the premier reserve currency is one part of broader

U.S. hegemony that also encompasses the U.S. having the world’s largest economy

and its most powerful military. The loss of the U.S. dollar’s reserve currency status may

thus presage a larger decline in the global power of the U.S. That the U.S. dollar is the

dominant reserve currency likely gives the U.S. government, as well as U.S. households

and businesses, access to a much larger investor base, enabling them to borrow more

than they would be able to if the U.S. dollar was not a reserve currency. This economic

advantage allows the U.S. to finance a large and powerful military more easily.

Additionally, international use of the U.S. dollar gives the U.S. government another set

of tools it can use to achieve its foreign policy aims, along with other soft power benefits

(Kirshner, 2008). I add to existing work studying “weaponized interdependence” and

U.S. sanctions risk more specifically by considering how widespread divestment from

U.S. dollar reserves might threaten U.S. hegemony (Farrell and Newman, 2019;

McDowell, 2021).

5

5

Norrlof (2010, 2014) also argues that the U.S. possesses geopolitical and economic advantages that

allow the U.S. dollar to remain the dominant reserve currency.

5

II. Geopolitical Relations, Sanctions, and Reserve Currency Choice

That political factors, in particular geopolitical relations, may affect a currency’s

status as a reserve currency has been recognized by academics dating back to work by

Strange (1971) and Cohen (1971). I briefly review the arguments for why geopolitical

alliances should help shape reserve currency preferences along with the motives most

often studied by economists. Then, I outline how the risk of sanctions on FX reserve

holdings undermines the economic motives for investing reserves in a currency and why

geopolitical alliances should affect sanctions risk.

Countries may wish to hold more reserves in a given currency if they have

stronger diplomatic relations with the issuing country for a variety of reasons (Norrlof,

2020). While strong diplomatic relations can affect reserve currency compositions

multiple ways, I highlight two that are especially relevant for understanding how

sanctions risk may vary across countries and thus their reserve currency choices. First,

a country may choose to hold its FX reserves in a currency in return for security

guarantees from the issuing country. The classic example of this is West Germany

continuing to hold U.S. dollars as FX reserve during the Vietnam War as a means of

preserving U.S. protection against potential Soviet incursions (Zimmerman, 2003).

6

Second, countries may choose to hold FX reserves in a given currency to signal support

for the political aims of the issuing country or as a reflection of preferences for the

existing international order.

7

6

Eichengreen et al. (2019) show that countries held a greater share of FX reserves in the currencies of

diplomatic allies during the early 20

th

century and Iancu et al. (2020) find that EMDEs allocate a greater

share of reserves to currencies of countries from whom they import a greater share of weaponry.

7

As evidence for this type of diffuse benefit of holding reserves in a specific currency, Iancu et al. (2020)

find that developed economies tend to hold more U.S. dollar reserves when their voting pattern at the UN

more closely aligns with that of the U.S., while Liao and McDowell (2016) show that countries that add

RMB assets to their reserves tend to be countries with similar political preferences to China.

6

A certain mechanism may matter more depending on the broader economic and

political environment of the reserve holder. For example, the security guarantee motive

will likely be more important if the country is currently involved in an armed conflict or

lacks a possible substitute for a security guarantee from the U.S. France and Germany

are both NATO members, but only France is a nuclear power. Perhaps unsurprisingly,

then, Germany consistently holds a greater share of its FX reserves in U.S. dollar

assets compared to France. Alignment with U.S. political aims is most likely to matter

for countries that are the least aligned with the U.S. For example, countries that have

faced financial sanctions from the U.S.—though not necessarily sanctions on their FX

reserves—appear to divest their U.S. dollar reserves shortly after the imposition of

sanctions (McDowell, 2021). Notably, this may even have been the case for Turkey,

which has a security guarantee from the U.S. through its membership in NATO.

In general, the threat of sanctions will affect reserve currency choice because

sanctions interfere with the economic uses of FX reserves. Generally, FX reserves are

a tool for managing a country’s exchange rate and a form of insurance against shocks

to international trade and international capital flows. Given the U.S. dollar’s dominance

in trade invoicing and external debt denomination, as well as its importance as an

anchor currency, it is unsurprising that most FX reserves are held in U.S. dollars

(Bertaut, von Beschwitz, Curcuru, 2021; Ilzetzki, Reinhart, Rogoff, 2019). Moreover, the

U.S. dollar is supported as a reserve currency because the markets for the U.S. dollar

assets held as FX reserves, in particular U.S. Treasuries, are the deepest and most

liquid in the world, allowing governments to liquidate their FX reserves in response to

negative economic shocks (Brunnermeier et al., 2022). As a result of these significant

7

economic benefits from holding U.S. dollar reserves, even countries without close

diplomatic ties to the U.S. may choose to hold U.S. dollar FX reserves.

Sanctions impede the ability to use FX reserves as buffers against negative

economic shocks. Thus, the threat of sanctions on FX reserves introduces a chance

that at least a portion of a country’s FX reserve holdings will effectively have zero value

in some states of the world. More importantly, it is likely that sanctions on FX reserves

will be imposed when the economic benefit of liquidating FX reserves is high. From a

portfolio allocation perspective, it is this characteristic of sanctions risk that will

especially reduce the optimal share of FX reserves going to a currency where the

issuing country may impose sanctions in the future.

While the sanctions levied against the Central Bank of Russia may have

increased the salience of sanctions risk in the minds of other governments, it is unlikely

that the higher risk is felt uniformly across countries. Countries with strong geopolitical

relations with the U.S. likely perceive a smaller increase in sanctions risk. As noted by

McDowell (2021), governments under economic sanctions by the U.S. typically are

“non-democratic, known human rights abusers that have foreign policy preferences that

run contrary to U.S. preferences.” Indeed, information accompanying the

announcement of sanctions on foreign central banks by the U.S. government has

referred to threats to U.S. national security (in the cases of Libya, Iran, and Afghanistan)

or violation of international law (in the case of Russia). Thus, to the extent that closer

diplomatic ties with the U.S. reduce the chances a foreign government threatens U.S.

security interests or signal alignment with the U.S. preference for a rules-based

international order, they lower the probability of future sanctions.

III. Foreign Government Holdings of U.S. Assets by Geopolitical Relation

8

Motivated by the idea that foreign governments with closer diplomatic ties to the

U.S. are less likely to face sanctions risk, I break down foreign government holdings of

safe U.S. dollar assets by geopolitical relation with the U.S. To do this, I rely on

confidential data on foreign official investor positions in U.S. assets reported in the TIC

data.

8

I focus specifically on foreign government holdings of U.S. Treasuries, debt of

U.S. government-sponsored agencies, and short-term liabilities of U.S. financial

institutions, as these are the U.S. securities most likely to be held as FX reserves. At

the end of December 2021, foreign governments’ positions in these assets were $5.24

trillion, accounting for about 75 percent of allocated U.S. dollar reserves captured in the

IMF COFER data for 2021:Q4.

In understanding the current breakdown of U.S. liabilities to foreign governments

by geopolitical alliance, I am particularly interested in what share of total foreign

government holdings belong to countries with formal military alliances with the U.S.

since these countries likely face the smallest threat of sanctions risk and thus the

smallest likelihood of divesting from U.S. dollar reserves in the next few years.

9

For

formal military allies, both the security guarantee and political affinity mechanisms

discussed above are likely to drive holdings of U.S. assets. In general, countries with

formal military alliances with the U.S. also tend to support the U.S.-led international

political and economic order, most recently evidenced by most of these countries

repeatedly voting to condemn Russia’s invasion of Ukraine.

8

Positions that combine foreign official and foreign investor holdings are available to the public at

https://home.treasury.gov/data/treasury-international-capital-tic-system

.

9

The case of Turkey discussed above shows that a formal military alliance does not automatically

prevent a country from being sanctioned by the U.S., but, in general, countries with formal military

alliances are less likely to face extensive sanctions from the U.S.

9

I consider two specific formal alliance types. The first and strongest form of

diplomatic relationship I examine is a mutual defense partnership with the U.S.

10

The

U.S. belongs to three multilateral mutual defense pacts: the NATO alliance with Canada

and European nations, the Rio Pact with countries in Latin America, and ANZUS with

Australia and New Zealand.

11

The U.S. also has three bilateral mutual defense treaties

with Japan, South Korea, and the Philippines. Another form of formal diplomatic tie with

the U.S. is that of major non-NATO ally, a designation granted by the U.S. government.

Countries that are major non-NATO allies are eligible for cooperation with the U.S. on

military projects and granted significant access to U.S. military supplies. Major non-

NATO allies without a mutual defense treaty with the U.S. include Singapore, Malaysia,

and Thailand in east Asia and Israel, Egypt, Kuwait, and Qatar in the Middle East.

12

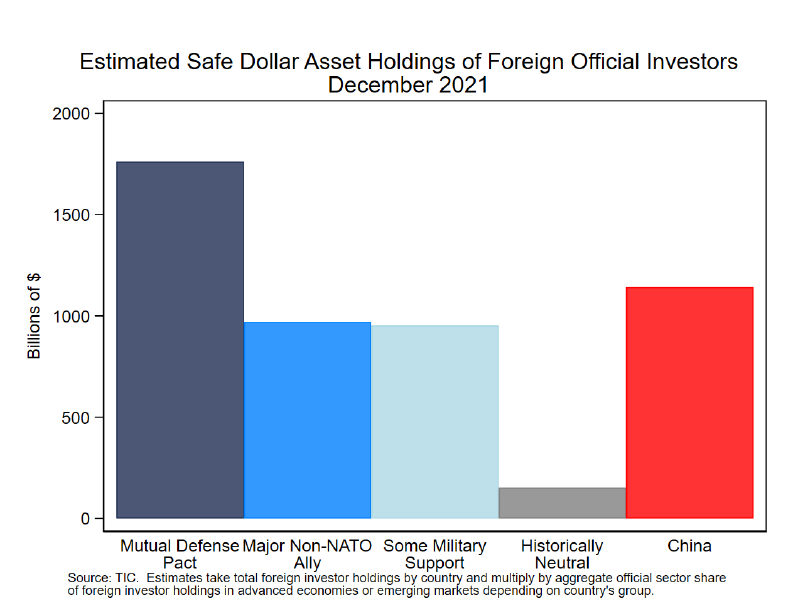

Governments with mutual defense pacts with the U.S. or the designation of a

major non-NATO ally accounted for most of the foreign government holdings of safe

U.S. assets prior to Russia’s invasion of Ukraine. In December 2021, governments of

countries in either of these two categories accounted for about 55 percent of total

foreign government holdings of safe U.S. assets. This share has been relatively stable

over time as well, as at no point in the past decade has the share held by these

countries dipped below 50 percent or exceeded 60 percent.

13

Figure 1 plots estimates

10

Mutual defense pacts are often viewed as the strongest form of formal alliance, see for example the

coding of formal alliances in the Correlates of War database that builds on Singer and Small (1966).

11

See Section A1 in the Appendix for a full list of the countries in NATO and the Rio Pact, as well as a full

list of countries in each diplomatic group. I include New Zealand as a mutual defense partner even

though it is partially suspended from ANZUS because diplomatic relations between New Zealand and the

U.S. improved in the 2010s.

12

According to U.S. law, Taiwan is to be treated as a major non-NATO ally without formal designation as

such, so I treat it as one. Other major non-NATO allies without mutual defense pacts with the U.S. are

Bahrain, Jordan, Morocco, Pakistan, and Tunisia. See https://www.state.gov/major-non-nato-ally-status/

for more information.

13

The share of U.S. safe assets held by U.S. military allies is consistent with the relative economic

resources of the U.S. and its allies. A recent study by the Economist Intelligence Unit found that 61.2

percent of global GDP was accounted for by countries that have explicitly condemned Russia’s invasion

10

of the breakdown in actual holdings between the two groups as well as three other sets

of countries that will be discussed below as of December 2021.

14

Within this set of close

U.S. allies, most holdings are accounted for by governments of mutual defense partners

of the U.S. The share held by close U.S. allies is little changed in the initial months after

Russia’s invasion and the sanctioning of its FX reserves.

That said, even among some of these close military allies, political alignment with

the U.S. may still affect willingness to hold U.S. dollars at the margin. For example,

since Argentina’s left wing returned to power in 2019, the central bank’s RMB swap line

with the People Bank of China has undergone several modifications amidst ongoing

economic turmoil. In 2020, the swap line agreement was reportedly renewed without the

inclusion of a previous clause requiring adherence to Argentina’s IMF program, while

the size of the swap line was increased in 2022.

15

In Brazil, a rise in the U.S. dollar

share of FX reserves has broadly coincided with the presidency of Jair Bolsonaro, who

is viewed as a stronger supporter of the U.S. than his predecessors (Banco Central do

of Ukraine (“Russia Can Count on Support from Many Developing Countries,” March 30, 2022).

Countries condemning the Russian invasion include most of the formal military allies of the U.S.

14

Positions for individual governments and aggregates based on these individual government positions

that are not reported by the U.S. Treasury are strictly confidential. Instead, Figure 1 uses the total

investor positions (governments and private sector investors) for each country and estimates each

government’s position based on whether the country is an advanced economy or an emerging market.

Specifically, for each country in the sample, the total investor position is multiplied by the aggregate share

held by governments in advanced economies or emerging markets, depending on the classification of the

country. The latest breakdown by investor and country type is for June 2021. Governments in advanced

economies held about 16 percent of total positions in U.S. securities by advanced economy investors.

Governments in emerging markets held about 81 percent of total positions in U.S. securities by emerging

market investors. For December 2021, the estimated share held by governments of mutual defense

partners and major non-NATO allies is within 3 percentage points of the actual share held by these

governments.

15

On the 2020 renewal, see "Central Bank Renews Currency Swap Deal with China for another Three

Years" in the Buenos Aires Times (August 7, 2020). For the expansion of the swap lines in 2022, see

Ignacio Olivera Doll, "Argentina Asks China to Expand Yuan Swap to Strengthen Reserves", Bloomberg

(January 26, 2022). The swap lines were subsequently expanded by $3 billion.

11

Brasil, 2021). I will return to the importance of political alignment with the U.S. for

holding U.S. dollar reserves in Section IV.

Additionally, many countries without a formal military alliance with the U.S. have

military ties to the U.S. either via recent imports of military equipment and weapons from

the U.S. or participation in joint military exercises with the U.S. These ties may prevent

these countries from taking actions that upset U.S. policymakers and raise the

probability of sanctions. As suggested by Figure 1, a nontrivial amount (between

roughly 15 and 20 percent of the total held by foreign governments) of safe U.S. assets

are held by countries that receive some form of military support from the U.S. but lack a

formal alliance.

16

India, Hong Kong, Vietnam, Indonesia, Saudi Arabia, the United Arab

Emirates, and Mexico comprise the largest holders among this group of countries.

Even if the governments of these countries perceive an increased risk of

sanctions being imposed on their U.S. dollar FX reserves, it is likely the economic

benefits of continuing to hold U.S. dollar reserve assets will outweigh the extra costs

associated with higher sanctions risk, at least in the near term. To see this, consider

four of the largest holders that do not have a mutual defense pact or a major non-NATO

ally designation. Hong Kong’s linked exchange rate system (LERS) establishes a

currency board for the Hong Kong dollar, rigidly pegging its value to that of the U.S.

dollar. The LERS also stipulates that the Hong Kong Monetary Authority keep at least

80 percent of its liquid FX reserves in U.S. dollar assets, limiting its ability to divest from

U.S. dollar reserves. Currently, Hong Kong holds about 90 percent of its FX reserves in

16

The “some military support” bar in Figure 1 reports estimates only for countries among the top 40

largest government holders of safe U.S. assets. The top 40 holders account for about 96 percent of all

government holdings of these U.S. assets. Countries outside the top 40 with some military tie to the U.S.

likely hold about 3percent of total foreign government holding of safe U.S. assets.

12

U.S. dollar assets (Iancu et al., 2020). Saudi Arabia and the United Arab Emirates also

peg their exchange rates to the U.S. dollar since each country has a prominent oil

exporting sector and global oil sales are typically invoiced in U.S. dollars (this feature

itself is a product of U.S. security guarantees for Saudi Arabia, see Croteau and Poast,

2020). Mexico has extremely strong trade linkages with the U.S., as about 70 percent

of Mexico’s merchandise exports went to the U.S. and 45 percent of Mexico’s

merchandise imports came from the U.S. over the 2016-2020 period. The costs of

divesting from U.S. dollar reserves would thus be substantial for these countries barring

some change in their economic structures.

Figure 1 also reports estimates for two additional groups of countries unlikely to

divest substantially from U.S. dollar reserves for differing reasons. The first set of

countries is Finland, Ireland, Sweden, and Switzerland; these are countries that have

historically remained neutral in major armed conflicts and shunned formal military

alliances, though Sweden and Finland will soon join NATO. More broadly, these

countries tend to support the existing international order and thus face limited risk of

sanctions from the U.S., as even Switzerland agreed to enforce sanctions against

Russia. The final set of estimated government holdings displayed in Figure 1 is for

China. China maintains the largest stockpile of FX reserves, and the RMB is frequently

identified as the most likely future challenger to the U.S. dollar’s reserve status, with

China the biggest competitor with the U.S. for the role of global hegemon. At the same

time, China’s ability to substantially lower the U.S. dollar’s share in its FX reserves is

limited in the near term.

17

Markets for safe assets denominated in other major reserve

17

This was reportedly the conclusion presented to Chinese government officials in April 2022, where

Chinese bankers told government officials that diversifying into more euro- or yen-backed assets was “not

practical” (see Yu, Sun, “China Meets Banks to Discuss Protecting Assets from U.S. Sanctions,” Financial

Times, April 30, 2022.)

13

currencies lack the size and depth necessary to accommodate China’s massive FX

reserve holdings, and the other major reserve currencies likely present similar

geopolitical risk as the U.S. dollar since the issuing countries are close U.S. allies.

18

Notably, at least 94 percent of allocated FX reserves in 2021:Q4 were held in currencies

of countries participating in the Russian sanctions according to COFER data.

19

But

China’s sizable FX reserves mean that even somewhat small decreases in the U.S.

dollar’s share of their FX reserves may result in large sales of U.S. assets in absolute

terms.

IV. How Geopolitical Risk May Threaten the Dollar’s Status over the Long

Run

A. Scenario Description

As the preceding section argues, without changes in the economic incentives for

holding FX reserves in U.S. dollar assets, an increased threat of sanctions is unlikely to

drastically reduce the dollar share of FX reserves. This section lays out one scenario

where the economic benefits of U.S. dollar reserves decline for countries less aligned

geopolitically with the U.S. and analyzes the implications for the dollar’s share of FX

reserves. At the root of this change is a reduction in the use of the U.S. dollar for trade

invoicing by countries that are less aligned with the geopolitical aims of the U.S. Recent

work by Gopinath and Stein (2018, 2021) argues that the use of a currency for trade

18

The key assumption underlying this conclusion is that the U.S. and its allies will jointly impose

sanctions, but the example of the U.S. unilaterally leaving the Joint Comprehensive Plan of Action and

sanctioning Iran shows this may not always be the case. Nevertheless, recent communications from U.S.

Treasury officials highlight the need for cooperation in imposing sanctions to guarantee their

effectiveness. On this point, see deputy U.S. Treasury Secretary Wally Adeyemo’s “fireside chat” with

Mark Sobel (https://www.omfif.org/videos/fireside-chat-with-wally-adeyemo/

).

19

I thank Bastian von Beschwitz for suggesting this analysis. Much of the three percent of allocated FX

reserves held in “other currencies” according to COFER data is also likely in currencies of countries

participating in sanctions against Russia if one allocates the “other currencies” share across currencies

according to foreign exchange turnover shares in the BIS triennial central bank survey.

14

invoicing and for denominating liabilities creates incentives for a government to hold this

currency in its FX reserves. Additionally, it has recently been reported that countries

with diplomatic disagreements with the U.S. may be negotiating with China to accept

RMB for their commodity exports to China, adding to the relevance of such a scenario,

though U.S. dollar reserve divestment could occur through ways not addressed here.

20

The relatively undeveloped international payments network for transactions

settled in RMB and China’s strict capital controls limiting both inbound and outbound

capital flows mean that such a scenario would most likely need to proceed gradually—if

it were to occur at all.

21

A larger number of financial institutions would need to

participate in China’s Cross-Border Inter-bank Payments System (CIPS) to facilitate

wider use of the RMB in trade invoicing. The limits on outbound portfolio investments

by Chinese residents would need to be relaxed to create deeper markets for foreign

liabilities denominated in RMB (similar conclusions are reached by Eichengreen, 2022).

According to Gopinath and Stein (2018), this would create incentives for foreign

governments to hold RMB assets as FX reserves, and this in turn would likely require

foreign investors to be able to hold greater amounts of Chinese assets than at present.

Given these possible constraints on RMB internationalization, a reasonable

sequence of events would be for China to first pay for its imports (particularly of

commodities) from countries not aligned politically with the U.S. in RMB while

developing the RMB cross-border payments network, relaxing capital controls, and

20

Saudi Arabia’s government, which has recently had disagreements with the U.S. government over its

foreign policy in the Middle East, reportedly was in negotiations with the Chinese government to accept

RMB for its sales of oil to China. See Said, Summer and Stephen Kalin, “

Saudi Arabia Considers

Accepting Yuan Instead of Dollars for Chinese Oil Sales,” Wall Street Journal, March 15, 2022.

21

Clayton, Dos Santos, Maggiori, and Schreger (2022) study the gradual opening up of China’s bond

markets to foreign investors and argue that this incremental approach helps the Chinese government

improve its reputation with foreign investors.

15

strengthening property rights for investors.

22

Should this first stage prove successful,

the next step would be for the same set of non-Western aligned countries to use the

RMB more broadly with each other. At the same time, broader use of the RMB in trade

invoicing would enhance the attractiveness of issuing RMB-denominated liabilities and

holding RMB assets in these countries. This would likely occur at the expense of the

U.S. dollar, which is used to invoice almost all trade outside the euro area and

denominates most external liabilities for EMDEs.

The key choice for designing this scenario is which countries would be most

likely to reduce their reliance on the U.S. dollar as an international currency. I argue the

countries with the greatest probability of diversifying away from the U.S. dollar are

EMDEs in Africa, Central Asia, Latin America, and the Middle East. These countries

often lack formal military alliances with the U.S., and even those that do—such as the

nations of Latin America—have also established growing relations with China and

Russia.

23

In general, governments in these regions appear unwilling to fully pick sides

in disputes between the U.S. (and its closest allies) and China (Al-Tamini, 2019;

Mazzocco, 2022). As a recent example, these governments have generally walked a

fine line diplomatically during the recent Russian invasion of Ukraine, sometimes

22

Eichengreen et al. (2022) outline a different scenario through which the RMB becomes an important

reserve currency. However, their scenario requires China to continue holding significant amounts of U.S.

dollar reserves, which contrasts some of my assumptions below.

23

China’s growing economic and political ties to Latin America have received considerable attention,

including in a recent brief by the Congressional Research Service (Lum and Sullivan, 2022). Although

economic ties have generally been larger, China also provides military support to many Latin American

nations that also have a mutual defense pact with the U.S. For example, UN Comtrade data show that

China’s arms exports to Brazil and Chile nearly equal those from the U.S. in recent years. Another close

U.S. ally that has repeatedly raised concerns from the U.S. government over its military ties to China is

Israel. For examples of these concerns see David Isenberg, “Israel’s Role in China’s New Warplane,”

Asia Times (December 4, 2002) and Michael Wilner, “Bolton Tells Netanyahu of U.S. Concern with

Chinese Presence at Haifa Port,” Jerusalem Post (January 6, 2019). Countries in these regions without

formal military alliances with the U.S. also often have significant military and economic ties to Russia and

China.

16

offering humanitarian assistance to Ukraine but refusing to outright condemn Russia’s

actions, placing them closer to China’s position on the issue relative to the stance of the

U.S. and its allies.

24

Thus, I regard political alignment as the more important mechanism

for linking diplomatic alliances to reserve currency composition for these countries,

especially as there is a greater possibility of substituting away from U.S. military support

over a longer time span.

One notable set of countries that I do not initially consider as likely participants in

this scenario are the nations of southeast Asia. While these countries have stronger

economic ties with China, they have stronger military and diplomatic connections with

the U.S. (Lin et al., 2020). Moreover, holding RMB-denominated reserve assets may be

risky venture for these countries due to ongoing territorial disputes in the South China

Sea (Stromseth, 2019). Therefore, for southeast Asian nations, I treat military support

from the U.S. as the more relevant geopolitical mechanism for influencing holdings of

U.S. dollar FX reserves.

B. Estimated U.S. Dollar Reserve Divestment

Should many EMDEs choose to reduce their use of the U.S. dollar in trade

invoicing for geopolitical reasons, how much would the U.S. dollar share of FX reserves

be expected to decline? I provide one answer here using existing estimates of the

relationship between the dollar’s share in export invoicing and its share in FX reserves

for a given country. Studies by Arslanalp et al. (2022) and Ito and McCauley (2020) find

a one percentage point fall in the dollar’s invoicing share of a country’s exports is

24

A report by the Economist Intelligence Unit found that most EMDEs either had a neutral stance towards

Russia’s invasion of Ukraine or echoed pieces of the Russian portrayal of the situation, such as refusing

to call the military operation an invasion (“Russia Can Count on Support from Many Developing

Countries,” March 30, 2022). The report also assesses alignment with the U.S. or Russia based on

information beyond countries’ response to Russia’s invasion of Ukraine.

17

associated with a 0.2-0.5 percentage point fall in the dollar’s share of that country’s FX

reserves. I apply the upper point estimate of 0.5 to changes in the dollar’s export

invoicing share for 43 of the largest holders of FX reserves in Africa, Central Asia, Latin

America, and the Middle East.

25

=

∑

0.5 ∗

∗

(1)

Equation (1) above outlines the calculations I perform for each country i in the

sample and then sum across countries. I first use bilateral export data from UN

Comtrade for the 2016-2020 period to compute the share of exports that go to non-

Western countries for each of the 43 countries in the sample (NonWestExport

i

).

26

Specifically, I assume that all merchandise exports to countries outside of NATO, the

EU, neutral Europe, Japan, Korea, Australia, New Zealand, and the member nations of

the Association of Southeast Asian Nations (ASEAN) switch from being invoiced in

dollars to invoiced in RMB. This non-Western export share is multiplied by country i’s

FX reserves in 2021 (Reserves

i

) as well as the 0.5 estimate from the previous literature

on the relationship between the currency composition of export invoicing and FX

reserves.

27

I then divide by global FX reserves (GlobalReserves) at the end of 2021 as

reported in the IMF COFER data and sum up across countries. Thus, the only limit to

how much these countries are predicted to diversify away from U.S. dollar reserves is

how much they export to non-Western countries.

25

See Section A2 of the Appendix for a complete list of countries used in the calculation.

26

I use the phrase “non-Western” to denote countries that are not geopolitically aligned with the U.S. For

countries in the Middle East, a large share of aggregate exports goes to unspecified destinations. I make

the extreme assumption that all unallocated exports are to non-Western countries for the sake of

establishing an upper bound.

27

When FX reserves data are unavailable for 2021:Q4, I use the most recent data available if it occurs

after 2018.

18

Under this proposed scenario, the U.S. dollar’s share of FX reserves would

decline by 6.2 percentage points or $800 billion using current FX reserve levels. Figure

2 shows the breakdown by region, with the two countries with the largest predicted U.S.

dollar divestments separated out. The two largest diversifiers, Saudi Arabia and India,

account for more than 40 percent of the predicted divestment, and the three largest

diversifiers account for 53 percent of the predicted divestment from U.S. dollar reserves.

Saudi Arabia is the largest diversifier due to its sizable stockpile of FX reserves

(currently around $430 billion) and the small share of exports directly allocated to

Western countries (less than 10 percent)

28

. The most important regions in terms of U.S.

dollar divestment are the Middle East and Latin America.

The predicted divestment from U.S dollar reserves for these 43 countries would

not cause the U.S. dollar to lose its majority status among FX reserve currencies, but,

when combined with realistic divestments from two other countries, it would. The first

additional divestment would come from China. China’s desire to diversify its reserves

away from the U.S. dollar is an open secret, and while its ability to shift its FX reserves

into other currencies is severely limited in the near-term, this is unlikely to be the case

over the course of a decade or two. I draw on two pieces of information to create a

prediction for China’s dollar divestment. First, Sheng (2013) estimates that China

increased its euro share of FX reserves by 15 percentage points between 2000 and

2005 (largely at the expense of the U.S. dollar share). Second, while China was able to

reduce its dollar share of FX reserves relatively quickly then, doing so over the coming

28

Just over 65 percent of Saudi Arabia’s total exports are to an unspecified destination, likely making the

non-Western export share used in the calculation an overestimate of its true value. However, the non-

Western share of allocated exports is still quite large, at just over 78 percent. Using this estimate for the

non-Western export share would still make Saudi Arabia the largest diversifier in the sample.

19

years will be considerably more difficult.

29

Therefore, I assume here that China reduces

the dollar share of its FX reserves by 10 percentage points or about $320 billion.

The second additional divestment I consider would come from Hong Kong, which

has felt the threat of Western sanctions in recent years resulting from tighter control of

the region by China.

30

Should Hong Kong abandon its LERS due to these fears, adopt

trade invoicing patterns like other non-Western countries, and allocate its reserves

based on these patterns, it would be predicted to divest $170 billion from U.S. dollar

reserve assets. These two additional sources of divestment, in combination with the

sales of U.S. dollar reserves by the original 43 sample countries, would reduce the U.S.

dollar’s share of FX reserves by 10 percentage points or $1.3 trillion at current levels of

FX reserves. Given the U.S. dollar’s 59 percent share of FX reserves in 2021:Q4

according to COFER data, this would mean the U.S. dollar would no longer comprise

the majority of reserves.

C. Is the Predicted U.S. Dollar Reserve Divestment Realistic?

The estimates of divestment from U.S. dollar reserves under a switch away from

U.S. dollar export invoicing I report are based on one estimate from one study. Thus, it

is worthwhile to check the robustness of the estimates to different assumptions. First, I

assess potential sources of bias in the calculations. I may overestimate U.S. dollar

divestment in this scenario because I use the largest estimate from previous work, I

assume all trade between non-Western countries is invoiced in U.S. dollars, and—while

29

China’s desire to evade potential Western sanctions likely means it would have to invest its

international reserves in currencies that currently comprise a miniscule portion of FX reserves or in gold,

which presents a different set of issues related to storage and liquidity.

30

Most recently, it was backlash to an anti-sanctions law proposed by the Chinese government that was

ultimately pulled (“China to Shelve Anti-Sanctions Law in Hong Kong, HK-01 Says

,” Bloomberg, October

4, 2021).

20

firms and governments might be comfortable accepting the RMB for trade purposes—

governments may not be as willing to hold RMB assets as FX reserves. I may also

underestimate U.S. dollar divestment in this scenario because the relationship between

reserve currency share and export invoicing share may be non-linear, the shares of

exports to non-Western countries are likely to grow in the coming decades, and

countries switching their invoicing currency may divest from U.S. dollar reserves for

geopolitical reasons independent of the switch in invoicing currency.

I consider the possibility of a non-linear relationship between reserve currency

share and export invoicing currency use as the consideration that most requires further

investigation. In the presence of network externalities and economies of scale (as is

almost surely the case for reserve currency use), linear regression will fail to account for

a higher derivate of reserve currency share with respect to the determinant variable

when the determinant is further away from its extreme values (Chinn and Frankel,

2008). Moreover, according to Boz et al. (2022), most EMDEs either invoice the vast

majority of their exports in U.S. dollars or hardly at all, suggesting a linear regression of

reserve currency shares on export invoicing shares may underestimate the effect for

some large changes in invoicing currency share. The scenario described above would

indeed result in large changes in invoicing currency use, as shown in Figure 3, 30 out of

the 43 countries studied would have the U.S. dollar share of both export and import

invoicing change by over 40 percentage points. Included among these 30 countries are

five of the seven countries in the sample with FX reserve holdings greater than $100

billion. Additionally, part of this “tipping phenomenon” may reflect how invoicing

currency use may influence other factors affecting reserve currency share, such as the

choice of anchor currency for exchange rate movements (Egorov and Mukhin, 2021).

21

I overcome the issue of non-linearity by studying the coevolution of the U.S.

dollar’s share in FX reserves and export invoicing for six EMDEs in Europe following the

creation of the euro.

31

Prior to the creation of the euro, Bulgaria, Croatia, Latvia,

Lithuania, North Macedonia, and Romania each had nontrivial U.S. dollar shares in

export invoicing and reserve currency allocation, with both typically between 30 and 60

percent. As shown in Boz et al. (2022), the U.S. dollar’s share of export invoicing

typically fell to single digits in the 20-year period after the euro’s creation. Further, the

change in the U.S. dollar’s share of FX reserves is larger than the change in the dollar’s

share of export invoicing over the 2000-2018 period for four of the six countries, as

shown in Figure 4.

32

I confirm this pattern in a panel regression of the U.S. dollar’s share in FX

reserves on its share in export invoicing from 1999-2019 for those six European

countries that includes country fixed effects.

33

To help make my results comparable to

those in Ito and McCauley (2020), I do not use annual observations but three-year, non-

overlapping averages of each variable. I find that a one percentage point change in the

U.S. dollar’s export invoicing share is associated with a 1.1 percentage point change in

its share of FX reserves, as shown in Table 1. This is a substantially larger estimate

than almost any estimate found in previous studies.

34

This suggests that widespread

31

An alternative approach would be to take a non-linear transformation of the reserve currency share

data and regress it on the export invoicing currency shares for a larger sample of countries, as in Chinn

and Frankel (2008).

32

Figure 4 combines the Boz et al (2022). data on currency shares of export invoicing with the reserve

currency data from Iancu et al. (2020). If data for 2000 are unavailable for one of the series, I use the

observation for the first year where both export invoicing and FX reserve currency shares are reported.

For Latvia, the end observation is 2013 because Latvia adopted the euro as the domestic currency in

2014. For Lithuania, the end observation is 2014 for similar reasons.

33

I drop the observations for Latvia and Lithuania after each country adopted the euro as the domestic

currency.

34

Some of this measured effect for export invoicing may be coming from the simultaneous change in

anchor currency from the U.S. dollar to the euro, but the point estimate on export invoicing currency is still

larger than Ito and McCauley’s estimate from a regression that excludes the anchor currency as a

22

adoption of the RMB for trade invoicing would lead to greater changes in the U.S.

dollar’s share of FX reserves than estimated in Section IV.B.

35

Based on my estimate reported in Table 1, I create an alternative set of predicted

U.S. dollar reserve divestments for countries that would experience a large shift in their

trade invoicing patterns. Specifically, for countries with non-Western export and import

shares greater than 0.4, I replace the 0.5 in equation (1) with 1, so that, for every

percentage point decline in the U.S. dollar share of export invoicing, there is a

percentage point decline in the U.S. dollar share of FX reserves. For all other countries,

I continue to use the original form of equation (1).

The predicted decline in the U.S. dollar’s share of FX reserves nearly doubles

relative to the 6.2 percentage point decrease estimated in Section IV.B using these

alternative assumptions. The predicted fall in the U.S. dollar’s share of FX reserves is

now 11.8 percent. Figure 5 indicates that most of the larger divestment results from the

new estimate being applied to the three largest divestors: Saudi Arabia, India, and

Brazil. If, as is done in Section IV.B, I also assume that China reduces the U.S. dollar

share of its FX reserves by 10 percentage points and Hong Kong abandons the LERS

and uses the RMB for invoicing non-Western trade, the predicted decline in the U.S.

dollar share of FX reserves increases to 17 percent. The international monetary system

determinant. Moreover, outside of Lithuania, the countries maintained relatively rigid pegs to the euro

throughout the sample period.

35

While there may be simultaneity, so that the U.S. dollar’s share in FX reserves also affects the

contemporaneous U.S. dollar share of export invoicing, including a lagged dependent variable and using

the Arellano-Bond estimator would not necessarily be appropriate either. With a cross-section size of

only six, the estimator may be severely biased. Nevertheless, the coefficient on the U.S. dollar’s export

invoicing share remains larger than Ito and McCauley’s (2020) estimate for a similar specification when I

include a lagged dependent variable in the regression.

23

would be much more multipolar, but the U.S. dollar would remain the dominant pole,

with a share of FX reserves still more than double that of any other currency.

D. Risk Scenario rather than Modal Outcome

I consider the scenario of a widespread, geopolitically-motivated, shift away from

the U.S dollar in trade invoicing and in turn FX reserves not to be the most likely

outcome over the coming years. Rather, the geopolitically-motivated shift away from

the U.S. dollar as an international currency is a risk to the most likely outcome where

the U.S. dollar retains its dominant role in trade invoicing and FX reserves for all

countries. It is thus worth reviewing the arguments for why this is the case. These

arguments underscore how many different factors would have to go a certain way for

the U.S. dollar’s dominance to be substantially diminished.

First, as discussed in Section IV.A, such a scenario becoming reality likely

requires substantial changes in China’s capital account policies, major developments in

the infrastructure required to support cross-border transactions denominated in RMB,

and broader structural reforms to Chinese debt markets. It may simply be a matter of

time for China’s cross-border payments infrastructure to develop, but the other two

factors are much less certain. To date, the Chinese government retains tight control

over capital flows, especially on flows into foreign assets by Chinese residents. The

government relaxed some of these restrictions in 2021 to encourage outflows by

Chinese residents, though the timing of these changes suggests they were done to help

stem appreciation pressures on the RMB at the time. Without further removal of capital

controls, it is unclear whether there would be a large enough investor base to entice

foreign entities to issue liabilities denominated in RMB that would in turn incentivize

governments in these countries to hold RMB-denominated FX reserves. In addition,

24

increasing both FX reserve demand for RMB-denominated assets and the willingness of

foreign entities to issue RMB-denominated assets will likely require structural changes

to Chinese bond markets. As one example, a lack of transparency for the default

resolution process for Chinese local currency bonds remains a key sticking point for

foreign investors.

36

In addition to the developments necessary in China, this scenario would also

require major changes in many of the countries switching to RMB trade invoicing

beyond the invoicing currency adjustment. Consider the two largest divestors of U.S.

dollar FX reserves in the scenario: Saudi Arabia and India. For Saudi Arabia to hold

substantial amounts of RMB-denominated FX reserves it would surely have to end the

riyal’s peg to the U.S. dollar. If only some of the non-Western countries switch to RMB

invoicing, the incentives for Saudi Arabia to abandon its dollar peg are much smaller. In

the case of India, it would mean greater political and economic cooperation with a

country that it faced in minor military skirmishes as recently as 2020.

37

India could

easily decide the economic benefits of RMB invoicing and RMB FX reserves are not

worth the geopolitical risks, especially if not all non-Western countries begin invoicing in

RMB. Moreover, for Saudi Arabia and India, their economic size means that their

decisions about invoicing currency would likely affect the invoicing decisions of other

non-Western countries.

36

On this issue see Lockett, Hudson and Cheng Leng, “China Under Pressure to Reform Debt Market as

Foreign Inflows Slow,” Financial Times, June 14, 2022.

37

Although I use a similar argument to justify the exclusion of southeast Asia countries from the switch to

RMB invoicing, I argue there is one important distinction between the situations in India and southeast

Asia. That distinction is India’s current ties to Russia. Russia provides the largest share of India’s

weapons imports and India has taken advantage of the heavy discount on Russian oil to increase its

reliance on Russian oil imports. India may be pushed towards cooperation with China in order to preserve

these ties to Russia.

25

V. Conclusion

Although the sanctions imposed on Russia’s FX reserves by the U.S. and its allies

may have increased the salience of sanctions risk, I find that geopolitics alone are

unlikely to end the U.S. dollar’s dominance as a reserve currency. Most government

holdings of U.S. assets belong to those with close military ties to the U.S. and countries

without these ties have strong economic incentives to hold dollar-denominated

reserves. Even a geopolitically-motivated move away from the U.S. dollar in trade

invoicing would only diminish the dollar’s role as a reserve currency and not destroy it.

U.S. hegemony is thus unlikely to end from a loss in the dollar’s reserve currency

status. That said, two caveats need to be applied to this relatively sanguine conclusion.

First, it relies on the U.S. maintaining its current diplomatic alliances, which is not

guaranteed. Second, I have only considered whether geopolitics can end dollar

dominance. There may be other factors that also reduce the U.S. dollar’s share over

time, such as the deepening of financial markets in nontraditional reserve currencies

(Arslanalp et al., 2022). Finally, future work should further explore the specific

mechanisms through which close diplomatic ties may lead to larger holdings of U.S.

dollar reserves.

References

Al-Tamini, Naser. (2019). “The GCC’s China Policy: Hedging against Uncertainty,” in

C. Lons, ed., China’s Great Game in the Middle East (European Council on Foreign

Relations).

Arslanalp, Serkan, Barry Eichengreen, and Chima Simpson-Bell. (2022). “The Stealth

Erosion of Dollar Dominance: Active Diversifiers and the Rise of Nontraditional Reserve

Currencies,” IMF Working Paper 22/58.

Banco Central do Brasil. (2021). International Reserves Management Report.

26

Bertaut, Carol C., Bastian von Beschwitz, and Stephanie Curcuru. (2021). “The

International Role of the U.S. Dollar,” FEDS Notes. Washington: Board of Governors of

the Federal Reserve System.

Boz, Ermine, Camila Casas, Georgios Georgiadis, Gita Gopinath, Helena Le Mezo,

Arnaud Mehl, Tra Nguyen. (2022). “Patterns of Invoicing Currency in Global Trade:

New Evidence,” Journal of International Economics 136: 103604.

Brunnermeier, Markus K., Sebastian A. Merkel, and Yuliy Sannikov. (2022). “Debt as

Safe Asset,” NBER Working Paper No. 29626.

Chinn, Menzie and Jeffrey A. Frankel. (2008). “Why the Euro Will Rival the Dollar,”

International Finance 11(1): 49-73.

Clayton, Christopher, Amanda Dos Santos, Matteo Maggiori, and Jesse Schreger.

(2022). “Internationalizing like China,” NBER Working Paper No. 30336.

Cohen, Benjamin J. (1971). The Future of Sterling as an International Currency.

London: MacMillan, St Martin’s Press.

Croteau, Sabreena and Paul Poast. (2020). “Dollars for Oil,” Global Monetary Order

and the Liberal Order Debate, Symposium, International Studies Perspectives 21(2):

109-153.

Dooley, Michael P., David Folkerts-Landau, and Peter M. Garber. (2022). “U.S.

Sanctions Reinforce the Dollar’s Dominance,” NBER Working Paper No. 29943.

Economist Intelligence Unit. (2022). “Russia Can Count on Support from Many

Developing Countries,” The EIU Update, https://www.eiu.com/n/russia-can-count-on-

support-from-many-developing-countries/, March 30, 2022.

Egorov, Konstantin and Dmitry Mukhin. (2021). “Optimal Policy under Dollar Pricing,”

Mimeo.

Eichengreen, Barry. (2022). “Sanctions, SWIFT, and China’s Cross-Border Interbank

Payments System,” CSIS Briefs.

Eichengreen, Barry, Camille Macaire, Arnaud Mehl, Eric Monnet, and Alain Naef.

(2022). “Is Capital Account Convertibility Required for the Renminbi to Acquire Reserve

Currency Status?” CEPR Discussion Paper No. 17498.

Eichengreen, Barry, Arnaud Mehl, and Livia Chitu. (2019). “Mars or Mercury? The

Geopolitics of International Currency Choice,” Economic Policy 34(98): 315-363.

Farrell, Henry and Abraham L. Newman. (2019). “Weaponized Interdependence: How

Global Economic Networks Shape State Coercion,” International Security 44(1): 42-79.

Gopinath, Gita and Jeremy C. Stein. (2018). “Trade Invoicing, Bank Funding, and

Central Bank Reserve Holdings,” AEA Papers and Proceedings 108: 542-546.

Gopinath, Gita and Jeremy C. Stein. (2021). “Banking, Trade, and the Making of a

Dominant Currency,” Quarterly Journal of Economics 136(2): 783-830.

Helleiner, Eric. (2008). “Political Determinants of International Currencies: What

Future for the U.S. Dollar?” Review of International Political Economy 15(3): 354-378.

27

Iancu, Alina, Gareth Anderson, Sakai Ando, Ethan Boswell, Andrea Gamba, Shushanik

Haboyan, Lusine Lusinyan, Neil Meads, and Yiqun Wu. (2020). “Reserve Currencies in

an Evolving International Monetary System,” IMF Departmental Papers 2020/02.

Ilzetzki, Ethan, Carmen M. Reinhart, and Kenneth S. Rogoff. (2019). “Exchange Rate

Arrangements Entering the 21

st

Century: Which Anchor Will Hold?” Quarterly Journal of

Economics 134(2): 599-646.

Ito, Hiro and Robert N. McCauley. (2020). “The Currency Composition of Foreign

Exchange Reserves,” Journal of International Money and Finance 102: 1-21.

Kirshner, Jonathan. (2008). “Dollar Primacy and American Power: What’s at Stake?”

Review of International Political Economy 15(3): 418-438.

Klein, Matthew C. (2022). “The Implications of Unrestricted Financial Warfare,” The

Overshoot, https://theovershoot.co/p/the-implications-of-unrestricted?s=r, March 8,

2022.

Liao, Steven and Daniel McDowell. (2016). “No Reservations: International Order and

Demand for the Renminbi as a Reserve Currency,” International Studies Quarterly 60:

272-293.

Lin, Bonny, Michael S. Chase, Jonah Blank, Cortez A. Cooper III, Derek Grossman,

Scott W. Harold, Jennifer D.P. Moroney, Lyle J. Morris, Logan Ma, Paul Orner, Alice

Shih, and Soo Kim. (2020). “Regional Responses to U.S.-China Competition in the

Indo-Pacific: Study Overview and Conclusions,” RAND Corporation Report.

Mazzocco, Ilaria. (2022). “Evolving South America-China Relations: Challenges and

Opportunities for Washington,” CSIS Trustee China Hand,

https://www.csis.org/blogs/trustee-china-hand/evolving-south-american-china-relations-

challenges-and-opportunities, August 24, 2022.

McDowell, Daniel. (2021). “Financial Sanctions and Political Risk in the International

Currency System,” Review of International Political Economy 28(3): 635-661.

Mukhin, Dmitry. (2022). “An Equilibrium model of the International Price System,”

American Economic Review 112(2): 650-688.

Norrlof, Carla. (2010). America’s Global Advantage: U.S. Hegemony and International

Cooperation. Cambridge: Cambridge University Press.

Norrlof, Carla. (2014). “Dollar Hegemony: A Power Analysis,” Review of International

Political Economy 21(5): 1042-1070.

Norrlof, Carla. (2020). “The Security Foundations of Dollar Primacy,” Global Monetary

Order and the Liberal Order Debate, Symposium, International Studies Perspectives

21(2): 109-153.

Sheng, Liugang. (2013). “Did China Diversify Its Foreign Reserves?” Journal of

Applied Econometrics 28(1): 102-125.

Singer, J. David and Melvin Small. (1966). “Formal Alliances, 1815-1939,” Journal of

Peace Research 3: 1-31.

28

Stromseth, Jonathan. (2019). “Don’t Make Us Choose: Southeast Asia in the Throes of

U.S.-China Rivalry,” Brookings Institution.

Zimmerman, Hubert. (2003). “The Quiet German: The Vietnam War and the Federal

Republic of Germany,” in C. Goscha and M. Vaisse, eds., La Guerre du Vietnam et

l’Europe 1963-1973 (Bruxelles: Bruylant).

29

Figures and Tables

Figure 1

See section A1 of the Appendix for countries included in each category.

30

Figure 2

Sources: Haver and country sources for international reserves, UN Comtrade for export shares. See

Section IV.B for details of calculations. See section A2 of the Appendix for countries included in

calculation.

31

Figure 3

Green diamonds are countries with more than $100 billion of international reserves at end-2021: Saudi

Arabia, United Arab Emirates, Brazil, India, Turkey, Israel, Mexico. Trade shares calculated using data

from UN Comtrade for 2016-2020. See Section IV.B for a definition of “non-Western.”

32

Figure 4

Calculations use first and last years that U.S. dollar share of export invoicing and FX reserves are jointly

observed. For Latvia and Lithuania, end year is last year before euro adopted as domestic currency

(2013 and 2014 respectively). Sources: Boz et al. (2022) for export invoicing share and Iancu et al.

(2020) for FX reserve share.

33

Figure 5

Alternate calculation multiplies non-Western export share from 2016-2020 by international reserves at

end-2021 for countries with non-Western export share above 0.4 and non-Western import share above

0.4. For all other countries in calculation, non-Western export share is divided in half. See Section IV.B

for a definition of “non-Western” and section A2 in the Appendix for list of countries included in

calculation.

34

Table 1

U.S. Dollar FX Reserve Share Regression

(1)

USD Export Invoicing Share

1.09**

(0.47)

Adjusted R2

0.563

Within R2

0.394

N

38

Table reports results of panel regression of U.S. dollar FX reserve share on U.S. dollar export invoicing

share using data from six European countries from 1999-2018. Each variable is 3-year average using

non-overlapping annual observations. Regression includes country fixed effects. European countries in

sample are Bulgaria, Croatia, Latvia, Lithuania, North Macedonia, and Romania. Robust standard errors

in parentheses. *** p<0.01, ** p<0.05, * p< 0.1

35

Appendix

A1. Countries by Military Alliance

Mutual Defense Pact: Belgium, Denmark, France, Germany, Greece, Iceland, Italy,

Luxembourg, Netherlands, Norway, Portugal, Spain, Turkey, United Kingdom, Croatia,

Slovenia, Albania, Czech Republic, Slovakia, Estonia, Hungary, Latvia, Lithuania,

Poland, Romania, Canada, Japan, Korea, Philippines, Australia, New Zealand,

Argentina, Brazil, Chile, Colombia, Costa Rica, Dominican Republic, El Salvador,

Guatemala, Haiti, Honduras, Panama, Paraguay, Peru, Trinidad and Tobago, Uruguay

Major Non-NATO Ally (without a mutual defense pact): Bahrain, Israel, Jordan,

Kuwait, Malaysia, Pakistan, Qatar, Singapore, Taiwan, Thailand, Morocco, Tunisia,

Egypt

Some Military Support: Ukraine, Bangladesh, Hong Kong, India, Indonesia, Iraq,

Saudi Arabia, Timor-Leste, United Arab Emirates, Vietnam, Mexico, South Africa

Historically Neutral: Finland, Ireland, Sweden, Switzerland

A2. Countries Included in long run calculation

Algeria, Angola, Argentina, Armenia, Azerbaijan, Bahrain, Botswana, Brazil, Chile,

Colombia, Congo, Democratic Republic of the Congo, Dominican Republic, Ecuador,

Egypt, Ghana, Guatemala, Honduras, India, Iraq, Israel, Jordan, Kazakhstan, Kenya,

Kuwait, Libya, Mexico, Morocco, Nigeria, Oman, Pakistan, Panama, Paraguay, Peru,

Qatar, Saudi Arabia, South Africa, Tunisia, Turkey, United Arab Emirates, Uganda,

Uruguay, Uzbekistan