GAO-17-45

SOCIAL SECURITY

OFFSETS

Improvements to

Program Design

Could Better Assist

Older Student Loan

Borrowers with

Obtaining Permitted

Relief

Report to Congressional Requesters

December 2016

United States Government Accountability Office

United States Government Accountability Office

Highlights of GAO-17-45, a report to

c

ongressional requesters

December 2016

SOCIAL SECURITY OFFSETS

Improvements to Program Design Could Better Assist

Older Student Loan Borrowers with Obtaining

Permitted Relief

What GAO Found

Older borrowers (age 50 and older) who default on federal student loans and

must repay that debt with a portion of their Social Security benefits often have

held their loans for decades and had about 15 percent of their benefit payment

withheld. This withholding is called an offset. GAO’s analysis of characteristics of

student loan debt using data from the Departments of Education (Education),

Treasury, and the Social Security Administration (SSA) from fiscal years 2001-

2015 showed that for older borrowers subject to offset for the first time, about 43

percent had held their student loans for 20 years or more. In addition, three-

quarters of these older borrowers had taken loans only for their own education,

and most owed less than $10,000 at the time of their initial offset. Older

borrowers had a typical monthly offset that was slightly more than $140, and

almost half of them were subject to the maximum possible reduction, equivalent

to 15 percent of their Social Security benefit. In fiscal year 2015, more than half

of the almost 114,000 older borrowers who had such offsets were receiving

Social Security disability benefits rather than Social Security retirement income.

In fiscal year 2015, Education collected about $4.5 billion on defaulted student

loan debt, of which about $171 million—less than 10 percent—was collected

through Social Security offsets. More than one-third of older borrowers remained

in default 5 years after becoming subject to offset, and some saw their loan

balances increase over time despite offsets. However, nearly one-third of older

borrowers were able to pay off their loans or cancel their debt by obtaining relief

through a process known as a total and permanent disability (TPD) discharge,

which is available to borrowers with a disability that is not expected to improve.

GAO identified a number of effects on older borrowers resulting from the design

of the offset program and associated options for relief from offset. First, older

borrowers subject to offsets increasingly receive benefits below the federal

poverty guideline. Specifically, many older borrowers subject to offset have their

Social Security benefits reduced below the federal poverty guideline because the

threshold to protect benefits—implemented by regulation in 1998—is not

adjusted for costs of living (see figure below). In addition, borrowers who have a

total and permanent disability may be eligible for a TPD discharge, but they must

comply with annual documentation requirements that are not clearly and

prominently stated. If annual documentation to verify income is not submitted, a

loan initially approved for a TPD discharge can be reinstated and offsets resume.

Impact of Offsets on Older Borrowers’ Social Security Benefits

View GAO-17-45. For more information,

contact

Allison Bawden at (202) 512-7215 or

.

Why GAO Did This Study

An increasing number of older

Americans have defaulted on their

federal student loans, which are

administered by Education, and have a

portion of their Social Security

retirement or disability benefits

withheld above a minimum benefit

threshold to repay this debt. Given that

Social Security is the primary source of

income for many older Americans,

GAO was asked to review these

withholdings, known as offsets.

GAO examined: (1) characteristics of

student loan debt held by older

borrowers subject to offset and the

effect on their Social Security benefit;

(2) the amount of debt collected by

Education through offsets and the

typical outcomes for older borrowers;

and (3) effects on older borrowers

resulting from the program design of

relief options. GAO examined data

from fiscal years 2001 through 2015

from Education’s National Student

Loan Data System and other

administrative data from Treasury and

SSA. GAO also examined aggregated

data provided by Education and

Treasury, reviewed documentation,

and interviewed agency officials about

Education’s processes for providing

relief from offset.

What GAO Recommends

GAO suggests that Congress consider

adjusting Social Security offset

provisions to reflect the increased cost

of living. GAO is also making five

recommendations to Education,

including that it clarify documentation

requirements for permitted relief

resulting from disability. Education

generally agreed with GAO’s

recommendations.

Page i GAO-17-45 Social Security Offsets

Letter 1

Background 3

Older Americans Often Had Held Student Loan Debt for Decades

Prior to Offset, and Many Had the Maximum Possible Amount

Withheld through Social Security Offset 11

Social Security Offsets Were a Small Share of Education’s

Collections and Primarily Paid down Fees and Interest as Many

Borrowers Remained in Default after 5 Years 17

Program Design May Impact Retirement Security for Older

Borrowers, Including Those Seeking Relief Permitted for

Permanent Disability or Financial Hardship 26

Conclusions 42

Matter for Congressional Consideration 44

Recommendations for Executive Action 44

Agency Comments and Our Evaluation 44

Appendix I Objectives, Scope, and Methodology 47

Appendix II Additional Data Analysis of Student Loan Debt for Older Americans 52

Appendix III Supplemental Data Analysis Tables for Older Americans with Student

Loan Debt 59

Appendix IV Copy of Education’s Total and Permanent Disability Servicer’s Form for

Annual Income Verification 75

Appendix V Comments from the Department of Education 78

Appendix VI Comments from the Social Security Administration 81

Contents

Page ii GAO-17-45 Social Security Offsets

Appendix VII GAO Contact and Staff Acknowledgments 82

Tables

Table 1: Voluntary and Involuntary Options to Repay Defaulted

Federal Student Loans 4

Table 2: Social Security Benefits of Older Americans Subject to

Offset Compared to Overall Benefit Distribution 16

Table 3: Average Student Loan Balance of Borrowers 50 and

Older, by Loan Status 58

Table 4: Incidence of Debt by Age of Head of Household and

Type of Debt, 2013 59

Table 5: Number of Student Loan Borrowers Less than Age 50 by

Type of Loan and Status, Fiscal Years 2005 to 2015 60

Table 6: Number of Student Loan Borrowers Age 50 to 64 by Type

of Loan and Status, Fiscal Years 2005 to 2015 60

Table 7: Number of Student Loan Borrowers Age 65 and Over by

Type of Loan and Status, Fiscal Years 2005 to 2015 61

Table 8: Outstanding Federal Student Loan Balances by Age

Group from Fiscal Years 2005-2015 61

Table 9: Student Loan Balances of Borrowers Under 50 When

First Subject to Offset, Fiscal Years 2006 to 2015 62

Table 10: Student Loan Balances of Borrowers 50-64 When First

Subject to Offset, Fiscal Years 2006 to 2015 62

Table 11: Student Loan Balances of Borrowers 65 or Older When

First Subject to Offset, Fiscal Years 2006 to 2015 63

Table 12: Average Student Loan Balance of Borrowers Under 50,

By Loan Status, Fiscal Years 2006 to 2015 63

Table 13: Average Student Loan Balance of Borrowers 50-64, By

Loan Status, Fiscal Years 2006 to 2015 64

Table 14: Average Student Loan Balance of Borrowers 65 and

Older, By Loan Status, Fiscal Years 2006 to 2015 64

Table 15: Share of Student Loan Borrowers with Various

Outcomes 5 Years after Their Initial Social Security Offset

by Age, Fiscal Years 2001 to 2010 65

Table 16: Share of Student Loan Borrowers with Various

Outcomes 5 Years after Their Initial Social Security Offset

by Duration of Offset, Fiscal Years 2001 to 2010 66

Table 17: Share of Borrowers Under 50 Whose Social Security

Benefits Are below the Poverty Guideline after Offset for

Defaulted Federal Student Loans, Fiscal Years 2001 to

2015 67

Page iii GAO-17-45 Social Security Offsets

Table 18: Share of Borrowers 50-64 Whose Social Security

Benefits Are below the Poverty Guideline after Offset for

Defaulted Federal Student Loans, Fiscal Years 2001 to

2015 68

Table 19: Share of Borrowers 65 and Over Whose Social Security

Benefits Are below the Poverty Guideline after Offset for

Defaulted Federal Student Loans, Fiscal Years 2001 to

2015 69

Table 20: Length of Time Borrowers Held Student Loans at Time

of Initial Social Security Offset, Fiscal Years 2001 to 2015 70

Table 21: Length of Time in Default Prior to Offset for Borrowers

Not Receiving Social Security Benefits At Time of Offset,

Fiscal Years 2004-2015 70

Table 22: Length of Time in Default Prior to Offset for Borrowers

Receiving Social Security Benefits At Time of Offset,

Fiscal Years 2004-2015 71

Table 23: Proportion of Social Security Offset Collections Applied

to Principal, Interest, and Fees on Defaulted Federal

Student Loans, Fiscal Years 2001 to 2015 71

Table 24: Share of Borrowers Paying Student Loan Principal Via

Social Security Offset, by Duration of Offset, Fiscal Years

2001 to 2015 72

Table 25: Number of Borrowers in Social Security Offset due to

Defaulted Federal Student Loans, by Benefit Type and

Borrower Age, Fiscal Years 2001 to 2015 73

Table 26: Age at Loan Origination For Student Loans Held at Time

of Initial Social Security Offset, Fiscal Years 2001 to 2015 74

Figures

Figure 1: Education’s Total Collections for Defaulted Student

Loans by Type of Collection Effort, Fiscal Year 2015 8

Figure 2: Number of Federal Student Loan Borrowers and Share

of Those in Default and Offset for Any Federal Payment

by Age, Fiscal Year 2015 10

Figure 3: Length of Time Older Borrowers Had Held Student

Loans At Time of Initial Social Security Benefit Offset,

Fiscal Years 2001 to 2015 12

Figure 4: Number of Borrowers Over 50 Becoming Subject to

Social Security Offset for the First Time, By Year and

Size of Loan Balance 14

Page iv GAO-17-45 Social Security Offsets

Figure 5: Distribution of Monthly Social Security Offset Amount for

Older Americans, Fiscal Years 2001 to 2015 15

Figure 6: Total Amount of Offset Collections for Education Debt

and Share Allocated to Treasury Offset Program Fees by

Type of Offset, Fiscal Year 2015 18

Figure 7: Length of Time Older Borrowers Were Subject to Offset

of Their Social Security Benefits for Defaulted Student

Loan Debt, by Borrower Age (2001 through 2010) 21

Figure 8: Share of Older Borrowers by Outcome 5 Years after

Initial Social Security Offset to Repay Defaulted Student

Loan Debt, Fiscal Years 2001 to 2010 23

Figure 9: Number of Borrowers Age 50 and Older Whose Social

Security Benefits Are below the Poverty Threshold after

Offset for Education Debt, Fiscal Years 2004 to 2015 28

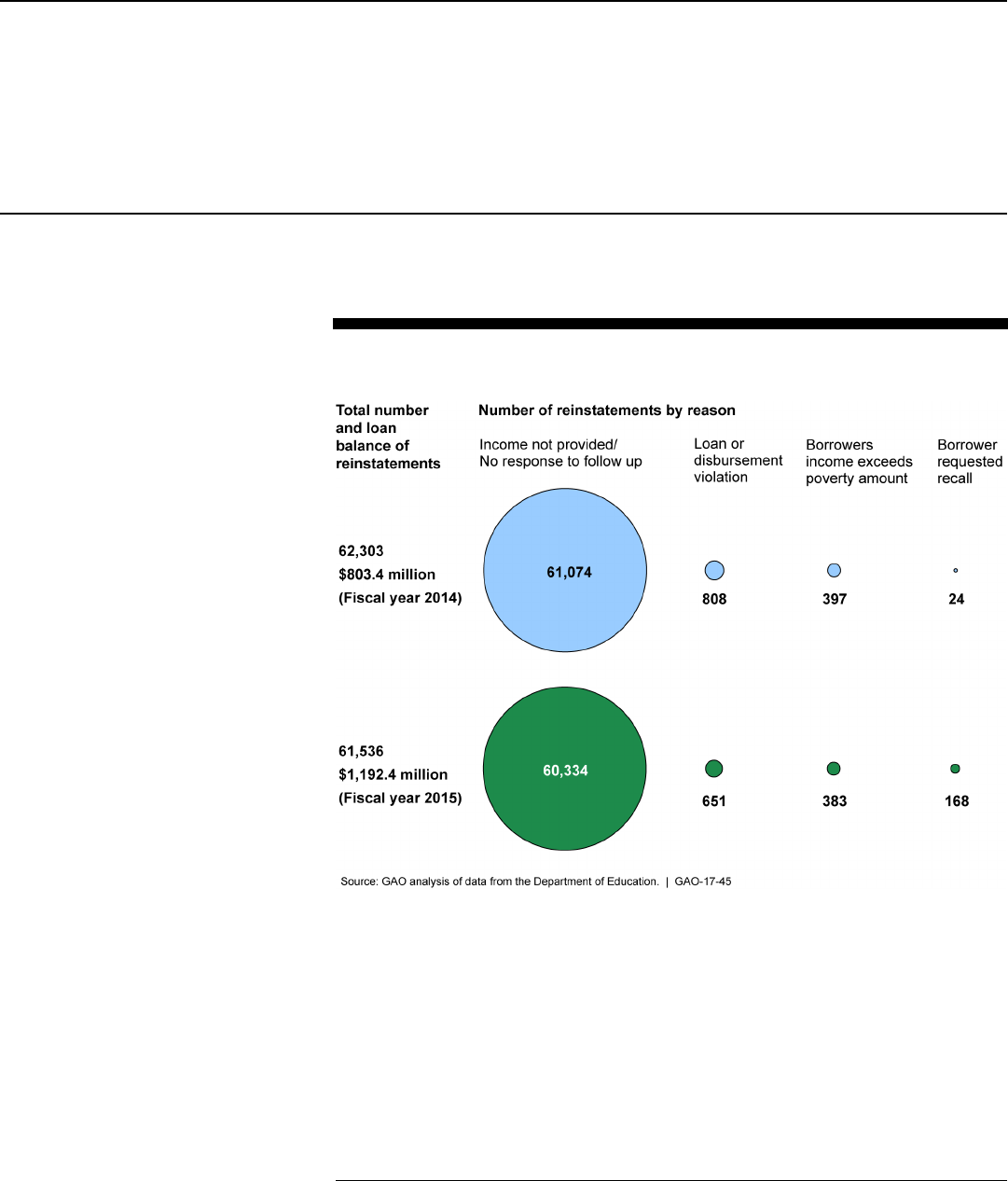

Figure 10: Number of Reinstatements of Total and Permanent

Disability Discharges (TPD) during 3-year Monitoring

Period for Borrowers of All Ages by Reason, Fiscal Years

2014 and 2015 35

Figure 11: Application and Review Process for Hardship

Exemption or Reduction from Social Security Offset 40

Figure 12: Outstanding Federal Student Loan Balances by Age

Group for Fiscal Years 2005, 2010, and 2015 52

Figure 13: Percentage Increase in the Number of Borrowers and

their Outstanding Federal Student Loan Balances from

Fiscal Years 2005 to 2015 53

Figure 14: Number of Borrowers with Social Security Offsets

for Federal Student Loan Debt in Fiscal Years 2002

and 2015 55

Page v GAO-17-45 Social Security Offsets

Abbreviations

Education Department of Education

Fiscal Service Bureau of the Fiscal Service

IRS Internal Revenue Service

NSLDS National Student Loan Data System

SCF Survey of Consumer Finances

SSA Social Security Administration

TPD Total and Permanent Disability

Treasury Department of the Treasury

This is a work of the U.S. government and is not subject to copyright protection in the

United States. The published product may be reproduced and distributed in its entirety

without further permission from GAO. However, because this work may contain

copyrighted images or other material, permission from the copyright holder may be

necessary if you wish to reproduce this material separately.

Page 1 GAO-17-45 Social Security Offsets

441 G St. N.W.

Washington, DC 20548

December 19, 2016

The Honorable Claire McCaskill

Ranking Member

Special Committee on Aging

United States Senate

The Honorable Elizabeth Warren

United States Senate

A growing number of older Americans have student loan debt as they

near or enter retirement. Compared to younger borrowers, borrowers age

50 and older have considerably higher rates of default on federal student

loans. For those who are in default on their student loans, this debt is

generally not discharged in bankruptcy, and their Social Security benefits

may be reduced to repay this debt. Specifically, under the Treasury Offset

Program, the Departments of Education and Treasury coordinate to

withhold a portion of an individual’s Social Security retirement or disability

benefit to pay off their outstanding federal student loan debt—a process

known as administrative offset.

1

Agencies are required to refer such debt

to Treasury for offset under the Debt Collection Improvement Act of

1996.

2

GAO previously reported a substantial increase in the number of

individuals whose Social Security retirement, survivor, or disability

benefits were offset to repay student loan debt for borrowers of all ages,

including those aged 65 and older, from 2002 through 2013.

3

Concerns

have been raised about the impact of such offsets given that many older

Americans rely on Social Security payments for the majority of their

income. In addition, the number of those subject to offset may continue to

1

The Treasury Offset Program was established under the Debt Collection Improvement

Act of 1996 to centralize the collection of federal nontax debt, including defaulted federal

student loans, at the Department of the Treasury. In addition to Social Security benefits,

other federal payments, such as federal tax refunds, are subject to offset.

2

Pub. L. No. 104-134, § 31001, 110 Stat. 1321, 1321-358. The Debt Collection

Improvement Act of 1996, as amended, is currently codified in Chapter 37 of Title 31 of

the United States Code. References to the Debt Collection Improvement Act of 1996 are

to current law applicable to Treasury offsets in connection with federal student loans in

default.

3

GAO, Older Americans: Inability to Repay Student Loans May Affect Financial Security of

a Small Percentage of Retirees, GAO-14-866T (Washington, D.C.: Sept. 10, 2014).

Letter

Page 2 GAO-17-45 Social Security Offsets

increase as the total amount of federal student loan debt owed by

Americans grows, as does the number of borrowers.

You asked us to study Social Security offsets for older Americans with

defaulted student loan debt. In this review, we examine the experience of

older Americans subject to Social Security offsets, including: (1)

characteristics of student loan debt held by borrowers subject to offset

and the effect on their Social Security benefit; (2) the amount of debt

collected by the Department of Education (Education) through offsets and

the typical outcomes for those in offset; and (3) effects on older borrowers

as a result of program design for offsets and related relief options for

disability or financial hardship.

To examine the experience of older Americans who are subject to Social

Security offsets for defaulted federal student loan debt, we obtained

administrative data needed for our analysis from the Department of the

Treasury’s (Treasury) Bureau of the Fiscal Service (Fiscal Service),

Education, and the Social Security Administration (SSA). To conduct our

analysis, we linked the administrative data from Fiscal Service’s Treasury

Offset Program to data on borrowers’ student loans from Education’s

National Student Loan Data System (NSLDS) and borrowers’ Social

Security benefits from SSA’s Master Beneficiary Record and Disability

Control File spanning the timeframe from fiscal years 2001 through 2015.

We used the linked record-level data to determine how long borrowers

have held loans that became subject to offset, the length of time spent in

offset, the size of the reduction in Social Security income, and outcomes

for borrowers subject to offset 5 years later. We further analyzed the

linked data to determine the effect of Social Security offsets on the

balances of defaulted federal student loans, including the proportion of

offset applied to fees, interest, and principal. To provide information on

the overall population of student loan borrowers, we obtained aggregated

data from Education on the total number of borrowers in default and offset

by age.

In addition, we reviewed relevant federal laws, regulations, and

documentation and interviewed agency officials to obtain information

about offsets of Social Security benefits, as well as Education’s

processes for (1) discharging student loan debt in cases of disability

where the borrower is considered to have become totally and

permanently disabled, and (2) claiming an exemption or reduction from

offset due to financial hardship. To further examine the Total and

Permanent Disability (TPD) discharge process, we analyzed aggregated

data provided by Education’s TPD servicer on TPD discharge

Page 3 GAO-17-45 Social Security Offsets

applications, approvals, and reinstatements, including the total volume

and dollar value. To identify the amount Education collected on defaulted

federal student loans through offsets and other payment mechanisms, we

analyzed data provided by Education’s Default Resolution Group,

including aggregated data from the Debt Management and Collection

System and information reported by guaranty agencies. In addition, we

analyzed aggregated data provided by Fiscal Service on fees assessed

by the Treasury Offset Program for Social Security offsets for Education

and other federal agencies. We assessed the reliability of all the data

sources used in this review by reviewing documentation and conducting

testing of the data and as a result determined that they were sufficiently

reliable for purposes of this report. More details on our scope and

methodology are included in appendix I.

We conducted this performance audit from September 2015 to December

2016 in accordance with generally accepted government auditing

standards. Those standards require that we plan and perform the audit to

obtain sufficient, appropriate evidence to provide a reasonable basis for

our findings and conclusions based on our audit objectives. We believe

that the evidence obtained provides a reasonable basis for our findings

and conclusions based on our audit objectives.

Older Americans—those in or approaching retirement—and other

borrowers who default on their federal student loans are subject to a

number of actions by Education to recover outstanding debt.

4

Borrowers

may elect a voluntary repayment option to avoid involuntary collection

efforts, such as Social Security offsets. (See table 1).

4

For purposes of this report, we consider older Americans—those in or approaching

retirement—to be individuals age 50 and older. As noted in the report, we also distinguish

between older Americans who are age 50 to 64 and those who are age 65 and older at

the time of their initial offset.

Background

Page 4 GAO-17-45 Social Security Offsets

Table 1: Voluntary and Involuntary Options to Repay Defaulted Federal Student

Loans

Voluntary options – borrower agrees to repayment

Option

Description

Payment in full

Borrower agrees to pay the entire balance

owed

Compromise

Borrower agrees to a reduced overall

payment to satisfy the debt(s) in full

Loan consolidation

Borrower agrees to combine multiple

federal student loans into one loan and

resume repayment

Loan rehabilitation

Borrower agrees to make 9 on-time

monthly payments within 10 months

Involuntary options – federal government takes action to collect from borrower

Option

Description

Treasury Offset Program

After notification from the Department of

Education (Education), the Department of

the Treasury or states (through agreements

with the Department of the Treasury) offset

certain federal or state payments owed to

the borrower, such as federal or state

income tax refunds and Social Security

retirement or disability benefits

Wage garnishment

Education requires borrower’s employer to

withhold funds from borrower’s pay and

send the funds to Education

Litigation

After referral from Education, Department

of Justice begins litigation against the

borrower

Source: GAO summary of documentation from Education. | GAO-17-45

While Education administers federal student loans, other agencies may

become involved in the event that a borrower fails to make repayment.

For example, as described in table 1, Education coordinates with

Treasury to offset a portion of federal payments to borrowers who have

not made scheduled loan repayments. Federal payments subject to offset

include federal tax refunds, certain monthly benefits—such as Social

Security retirement and disability payments—and wages and retirement

benefits for federal employees.

5

The Debt Collection Improvement Act of

5

The Social Security benefits that Treasury offsets are Federal Old-Age, Survivors, and

Disability Insurance Benefits, issued under Title II of the Social Security Act. Treasury

does not differentiate among retirement, survivor, and disability benefits in administering

Social Security benefit offsets, since all of these benefits are eligible for offset.

Page 5 GAO-17-45 Social Security Offsets

1996 centralized the collection of nontax debt, including defaulted federal

student loans, at Treasury. Specifically, the Treasury Offset Program

within Fiscal Service carries out the transactions for offsetting all federal

payments for nontax debt.

6

Offsets for student loan debt through the

Treasury Offset Program began in 1999 and were first applied to Social

Security benefits starting in 2001.

7

After a defaulted loan is certified as eligible for offset, certain federal

payments, such as any available tax refunds, are offset immediately.

Borrowers with monthly federal benefits available for offset, such as

Social Security benefits, are informed by mail that their benefits will be

offset in 60 days and again 30 days before the offset is taken, allowing

borrowers an additional 2 months to resume payment on their loan before

offset begins. In addition, Education sends a notice which provides details

on the loans eligible for offset and describes options a borrower has to

avoid offset. Treasury assesses a fee for each offset transaction, which is

subtracted from the offset payment.

8

For fiscal year 2015, Treasury’s fee

was $15 for each monthly offset of benefit payments and $17 for a single

tax refund offset.

Monthly Social Security benefit payments that are eligible for offset are

the primary source of income for many older Americans at or near

retirement. According to the Social Security Administration (SSA), Social

Security benefits accounted for 90 percent or more of income for about 1

in 3 beneficiaries age 65 and older in 2014.

9

Social Security’s retirement

benefits, which individuals may claim as early as age 62, provide monthly

income based on an individual’s work and earnings history and are

intended to help ensure an adequate retirement income. Disability

benefits replace a portion of an eligible workers’ income if they are unable

6

Treasury also administers a separate but similar program, the Federal Payment Levy

Program (FPLP), to offset federal payments for delinquent federal tax debt. The Taxpayer

Relief Act of 1997 authorizes the Internal Revenue Service (IRS) to collect delinquent

federal tax debt by levying up to 15 percent of certain federal payments until the debt is

paid. In the event an individual owes both delinquent tax debt and non-tax debt,

delinquent tax debt will be collected first.

7

Previously, IRS administered tax refund offsets for student loan debt.

8

31 U.S.C. § 3716(c)(4). Treasury assesses a fee to Education for each offset, and

Education passes the fee on to the borrowers.

9

Social Security Administration, Fast Facts & Figures about Social Security, 2016.

Page 6 GAO-17-45 Social Security Offsets

to work due to a long-term disability.

10

When individuals receiving Social

Security disability benefits reach Social Security’s full retirement age—

currently age 66 for people born in 1943-1954—their benefits convert

from disability to retirement. Both types of monthly Social Security

benefits are eligible for offset if the beneficiary is in default on a federal

student loan. Social Security’s Supplemental Security Income benefits,

which provide monthly cash assistance for eligible individuals with limited

financial means, have been exempted from offset.

11

Certain borrowers may be eligible to discharge their federal student loan

debt because they are totally and permanently disabled, regardless of

whether or not they are in default. For example, borrowers of any age

receiving Social Security disability benefits are eligible for a Total and

Permanent Disability (TPD) discharge if SSA has determined that they

have a disability for which medical improvement is not expected.

Borrowers who are approved for a TPD discharge are generally subject to

a 3-year monitoring period during which the discharged loans may be

reinstated for several reasons, including that the borrower earned income

over a specified threshold.

12

The value of the discharged loan is generally

treated as taxable income at the close of the 3-year monitoring period.

The Debt Collection Improvement Act of 1996 specified limits on the

amount that Treasury can offset from monthly federal benefits.

13

In 1998,

Treasury further exempted all but 15 percent of Social Security benefit

10

Adults are generally considered disabled if (1) they cannot perform work that they did

before; (2) they cannot engage in any other kind of substantial gainful work because of

their medical condition(s); and (3) their disability has lasted, or is expected to last, at least

1 year or is expected to result in death. 42 U.S.C. §§ 423(d) and 1382c(a).

11

Supplemental Security Income is a federal program funded by general revenue (not by

Social Security taxes) that provides monthly cash payments to aged (those 65 and older),

blind, and disabled people who have little or no income.

12

Veterans who qualify for a TPD discharge based on a VA determination of

unemployability due to a service-connected disability are not subject to a post-discharge

monitoring period. For borrowers who are subject to the 3-year monitoring period, loans

may be reinstated during this period for several reasons, including if the borrower’s

earnings from employment exceeds the poverty guideline amount for a family of two in

their state, if the borrower receives a new federal student loan, or if SSA determines that

the borrower is no longer disabled or that medical improvement is possible or likely for the

borrower’s disability.

13

Specifically, the Debt Collection Improvement Act of 1996 exempted benefit payments

totaling $9,000 over a 12 month period. This yearly amount is equivalent to $750 on a

monthly basis.

Page 7 GAO-17-45 Social Security Offsets

payments from offset. As a result, the amount of allowable offset is the

lesser of 15 percent of the monthly benefit payment, the amount by which

the benefit payment exceeds $750 per month, or the outstanding amount

of the debt.

14

For example, if a borrower with a Social Security benefit of

$1,000 per month owes more than $150 in student loan debt, the

borrower would have an offset of $150. This is because $150—equivalent

to 15 percent of the benefit—is less than the amount of the benefit over

$750, which is $250. In addition to the offset threshold, creditor agencies,

such as Education, are permitted to grant relief in cases of financial

hardship by certifying to Treasury that the offset allowable by law would

result in financial hardship.

15

Education established such a process in

2002 to grant financial hardship exemptions or reductions in offset.

According to Education data for fiscal year 2015, about $4.5 billion was

collected by Education, private collection agencies, and guaranty

agencies on defaulted federal student loans, excluding loan

rehabilitations and consolidations. About half of this amount came from

offsets of any federal payments through the Treasury Offset Program,

including but not limited to Social Security offsets (see fig. 1). Just over 30

percent of Education’s total collections came from administrative wage

garnishment, and about 20 percent came from voluntary payments made

by borrowers who may have been in the process of making the required

number of on-time monthly payments to eventually rehabilitate or

consolidate their loans and emerge from default.

16

According to Education

officials, borrowers may also make voluntary payments to avoid being

14

Monthly benefit payment refers to the amount of Social Security benefits paid to an

individual after any deductions, such as for Medicare Part B premiums.

15

31 C.F.R. § 285.5(d)(12). A creditor agency can certify to Fiscal Service that the offset

amount allowed by law would result in financial hardship to the debtor and that a lesser

offset amount is reasonable and appropriate based on the debtor’s financial

circumstances.

16

Borrowers who make at least three consecutive, voluntary, on-time full monthly

payments on certain defaulted student loans are eligible for direct consolidation loans

whereby they can pay off certain defaulted loans by consolidating them with one or more

Direct Loan Program or Federal Family Education Loan Program loans into a single loan

with a fixed interest rate. 34 C.F.R. §§ 685.102(b) and 685.220(d)(1). Some borrowers

who make nine on-time monthly payments during 10 consecutive months may be eligible

for loan rehabilitation, which allows them to have the default removed from their credit

history. 34 C.F.R. §§ 682.405(a)(2), (b)(1)(vi)(A) and 685.211(f)(1)(iv). However,

borrowers may only rehabilitate a loan once. 34 C.F.R. §§ 682.405(a)(4) and

685.211(f)(12).

Education’s Collection

Efforts in Fiscal Year 2015

Page 8 GAO-17-45 Social Security Offsets

subject to other collections actions, such as administrative wage

garnishment. In addition to these collections, Education publicly reports

recoveries from defaulted loans when they are successfully rehabilitated

or consolidated.

17

Figure 1: Education’s Total Collections for Defaulted Student Loans by Type of

Collection Effort, Fiscal Year 2015

Fewer older Americans hold student loan debt, but the rate of increase in

the number of older borrowers and the amount of their debt has far

outpaced younger borrowers. According to Education data for fiscal year

2015, there were about 37.4 million borrowers under age 50 compared to

about 6.3 million borrowers age 50 to 64 and 870,000 borrowers age 65

17

See ‘Default Recoveries by Private Collection Agency’ available at:

https://studentaid.ed.gov/sa/about/data-center/student/default. Rather than calculating the

value of loan payments collected over a specified time period, Education officials said that

published data on these types of recoveries include the entire value of the loans because

the loan balances are no longer recorded as being in default. In fiscal year 2015,

Education reported rehabilitated and consolidated defaulted loan balances that totaled

$6.9 billion and $1.2 billion, respectively.

Federal Student Loan

Debt and Rates of Default,

and Offset among Older

Americans

Page 9 GAO-17-45 Social Security Offsets

and older.

18

Since fiscal year 2005, these figures represented an increase

in the number of borrowers in the age 50 to 64 and 65 and older groups

of 119 percent and 385 percent, respectively. In comparison, the growth

rate for borrowers age 25 to 49 was 62 percent over this time period. The

corresponding increase in the amount of federal student loan debt held by

borrowers age 50 to 64 was from about $43 billion to $183 billion over this

decade, more than a three-fold increase.

19

Among borrowers age 65 and

older, the increase in the amount of federal student loan debt was even

larger— it grew from more than $2 billion in fiscal year 2005 to almost $22

billion in fiscal year 2015, about a ten-fold increase.

20

The loans on which

older borrowers have defaulted may have either been for their own

education or for their children’s education through Education’s Direct

PLUS Loan program.

21

In fiscal year 2015, compared to younger borrowers a greater share of

older borrowers were in default on their student loan debt and became

subject to offset from any federal payment, including federal tax refunds

18

According to 2013 data from the Survey of Consumer Finances (SCF), about 29 percent

of households headed by an individual age 35 to 44 held student loan debt compared to

about 12 percent for households headed by an individual age 55 to 64 and about 3

percent for households headed by an individual age 65 and older. These figures are

available at: Historic Tables and Charts,

http://www.federalreserve.gov/econresdata/scf/scfindex.htm. The 2013 SCF did not use

the phrase “student loans,” but rather asked respondents whether they have education

loans. Because of the inclusive wording of the question, the SCF data reflect both federal

and private loans. SCF survey responses are also based on the financial situation of an

entire household, not just the head of household. Because of this, it is possible that for

some households headed by older Americans, the reported student loan debt is held by

children or other dependents that are still members of the household. See appendix III,

table 4 for more detailed information from the 2013 SCF.

19

Over the same time period, the amount of federal student loan debt held by borrowers

age 25 to 49 increased by 187 percent. For more detailed information on the growth in the

number of borrowers and their outstanding federal student loan balances by age, see

appendix II, figure 13.

20

Data in this paragraph do not include less than 0.5 percent of borrowers for whom

Education could not determine their age. See appendix II, figures 12 and 13 for more

detailed information.

21

Education’s Direct PLUS Loan program offers parents of dependent undergraduate

students the opportunity to borrow to finance their children’s education. PLUS loans are a

form of Direct Loan that can be used by graduate or professional degree students or

parents of dependent undergraduate students to pay for educational expenses not paid for

by other assistance. Parents or step-parents are eligible for such loans if their child is a

dependent student enrolled at least half-time and the school participates in the Direct

Loan Program. For more information on Parent PLUS loans, see appendix II.

Page 10 GAO-17-45 Social Security Offsets

and Social Security benefits. As shown in figure 2, the share of borrowers

age 65 and older in default and offset in fiscal year 2015 was 37 percent

and 5 percent, respectively. By contrast, the share of borrowers under

age 50 in default and offset was 17 percent and 2 percent, respectively.

Figure 2: Number of Federal Student Loan Borrowers and Share of Those in Default

and Offset for Any Federal Payment by Age, Fiscal Year 2015

Page 11 GAO-17-45 Social Security Offsets

In addition, our analysis of data we linked from Education, Treasury, and

SSA shows that the number of borrowers, especially older borrowers,

who have experienced offsets of Social Security benefits to repay

defaulted federal student loans has increased over time. From fiscal

years 2002 through 2015, the number of defaulted federal student loan

borrowers of any age with Social Security offsets increased from about

36,000 to 173,000. For those under age 50, the number of borrowers with

Social Security offsets increased from about 15,000 to 59,000 over this

time period—a three-fold increase. For those in the age 50 to 64 and 65

and older groups, the increase was greater—about 407 percent and 540

percent, respectively. In total for fiscal year 2015, about 114,000

borrowers age 50 and older had Social Security disability, retirement, or

survivor benefits offset to repay defaulted federal student loans.

Among those subject to Social Security offsets, most received disability

benefits rather than retirement or survivor benefits. In fiscal year 2015, 69

percent of defaulted borrowers of any age whose Social Security benefits

were offset received disability benefits, including 80 percent of those 50 to

64. Since disability benefits are automatically converted to retirement

benefits once beneficiaries reach their full retirement age, the vast

majority—95 percent—of defaulted borrowers age 65 and older received

retirement or survivor benefits in fiscal year 2015.

22

Of these borrowers,

about 23 percent had previously received disability benefits.

Among borrowers 50 and older at the time of their initial Social Security

offset, about 43 percent had held their student loans for 20 years or more.

Three-quarters of older borrowers owed loans only for their own

education, and most owed less than $10,000 at the time of their initial

offset. The typical monthly offset was slightly more than $140 for older

Americans, and almost half of those had the maximum possible

reduction, equivalent to 15 percent of their Social Security benefit

payment. From 2004 to 2014, the population of older Americans in Social

Security offset became increasingly composed of those with Social

Security income below the median benefit amount.

22

Social Security’s full retirement age is 66 for beneficiaries born between 1943 and 1954.

Growth in Social Security

Offsets and Prevalence of

Disability Benefits

Older Americans

Often Had Held

Student Loan Debt for

Decades Prior to

Offset, and Many Had

the Maximum

Possible Amount

Withheld through

Social Security Offset

Page 12 GAO-17-45 Social Security Offsets

About 43 percent of older student loan borrowers with a Social Security

offset had held their student loans for 20 years or more, and about 80

percent had held their loans for 10 years or more.

23

According to linked

data from the Treasury Offset Program, Education’s National Student

Loan Data System, and the Social Security Administration from fiscal

years 2001 through 2015, the length of time borrowers had held student

loans that were in default at the time of their first Social Security offset

payment varied as shown in figure 3.

24

Figure 3: Length of Time Older Borrowers Had Held Student Loans At Time of Initial

Social Security Benefit Offset, Fiscal Years 2001 to 2015

Note: Percentages in this figure do not add to 100 due to rounding.

These older borrowers generally took out their loans at traditional mid-

career working ages, and relatively few of them took out their loans at a

traditional college-going age. Across all borrowers 50 or older, 61 percent

became subject to offset for loans taken out in their 30s and 40s. For

borrowers 50 to 64 at the time of their initial offset, 8.2 percent had

outstanding loans that were taken out when they were under 25. Among

23

Borrowers may hold loans for an extended period of time for several reasons.

Deferments and forbearances, including in-school deferments, can extend the repayment

period. Extended repayment plans offered on certain loans can last up to 30 years.

Additionally, loans remain open and accrue interest while borrowers are in default. Social

Security offset may begin after a borrower has been in default for many years if, for

instance, the borrower was not receiving Social Security benefits at the time of default.

See appendix II for additional discussion of the length of time borrowers were in default

before becoming subject to Social Security offset.

24

When borrowers held consolidation loans, we counted the underlying loans that were

paid via the consolidation loan in measuring the length of time the borrower held loans.

We excluded all other loans that were paid off or otherwise closed before the borrower

became subject to offset.

Many Older Americans

Had Held their Student

Loans for 20 Years or

More at the Time of Initial

Offset

Page 13 GAO-17-45 Social Security Offsets

borrowers 65 and older, 1.4 percent had outstanding loans that were

taken out when they were under 25.

Older borrowers who became subject to Social Security offsets

predominately defaulted on loans for their own education. Among older

borrowers subject to offset of their Social Security benefits, more than

three-quarters had defaulted on loans they took out for their own

education rather than on loans they took out for a child’s education,

known as Parent PLUS loans.

25

For borrowers 50 to 64 at the time of

initial offset, 82 percent had only ever held loans taken out for their own

education. A greater proportion of borrowers 65 or older had Parent

PLUS loans, but even among this group, about two-thirds of the

borrowers never had Parent PLUS loans.

26

Total federal student loan debt for most older Americans who became

subject to offset was less than $10,000, while a small percentage owed

$50,000 or more. Initial balances tended to be slightly higher among

borrowers 65 and older at the time of their initial offset compared to those

50 to 64.

27

(See fig. 4).

25

Parents are eligible for Direct PLUS loans to pay for educational expenses not paid for

by other assistance if their child is a dependent student enrolled at least half-time and the

school participates in the Direct Loan Program.

26

Among borrowers 50 to 64 at the time of initial offset, 11 percent held only Parent PLUS

loans for a child’s education and 7 percent of borrowers held loans both for their own

education and for a child’s education. For borrowers 65 and older, 21 percent of borrowers

held only Parent PLUS loans, and 12 percent held both types of loans.

27

For example, among borrowers 50 to 64 at the time of initial offset, 7 percent owed more

than $50,000, including 2 percent who owed more than $100,000. For those 65 and older,

11 percent owed more than $50,000, including 4 percent who owed more than $100,000.

Most Older Americans

Subject to Social Security

Benefit Offset Took Out

Loans for Their Own

Education and Owed Less

than $10,000 at the Time

of Initial Offset

Page 14 GAO-17-45 Social Security Offsets

Figure 4: Number of Borrowers Over 50 Becoming Subject to Social Security Offset

for the First Time, By Year and Size of Loan Balance

Note: Figures not adjusted for inflation.

About 44 percent of borrowers 50 and older at the time of their initial

offset saw the maximum possible amount of their Social Security benefit

withheld, equal to 15 percent of their benefit payment.

28

The offset for the

remaining 56 percent was less than the maximum 15 percent of their

benefit payment. Most of these borrowers had between 10 and 15

percent of their benefit payment offset. A small proportion of borrowers

28

The amount of a monthly benefit offset is calculated as the lesser of 15 percent of the

monthly benefit payment after any deductions (e.g., Medicare Part B premiums), the

amount of the benefit payment over $750, or the outstanding amount of the debt.

Many Older Americans

Subject to Social Security

Offset for Student Loan

Debt Have the Maximum

Amount Withheld

Page 15 GAO-17-45 Social Security Offsets

(about 5 percent of those 50 to 64 and 4 percent of those 65 and older)

were approved for a financial hardship reduction and paid a reduced

amount of offset compared to what they would have otherwise.

The typical monthly Social Security benefit offset for older Americans

across fiscal years 2001 through 2015 was slightly more than $140. The

minimum amount was $25, which is the lowest amount at which Treasury

will initiate an offset. For borrowers 65 or older at their initial offset,

monthly payments ranged up to about $240 (see fig. 5). At the median,

monthly offsets were similar for those 50 to 64 and 65 and older—$142

and $146, respectively.

Figure 5: Distribution of Monthly Social Security Offset Amount for Older Americans, Fiscal Years 2001 to 2015

A growing share of Social Security beneficiaries is potentially subject to

offset because the share of beneficiaries who have benefits below the

protected threshold of $750 has declined. Because of the offset threshold,

those receiving monthly benefits of $750 or less who hold defaulted

federal student loans are not subject to offset. However, unlike Social

Security benefits which are increased on an annual basis through cost of

living adjustments, the Social Security offset threshold of $750 has not

been adjusted. As the relative value of the offset threshold has declined

over time, it applies to a smaller share of Social Security beneficiaries.

Across all Social Security beneficiaries in 2004, about 42 percent of those

receiving Social Security disability benefits and about 33 percent of those

receiving retirement benefits had monthly benefits of less than $750 a

month and thus could not become subject to offset. By 2014, however,

the share of all beneficiaries below the $750 threshold had fallen to 19

Older Americans in Social

Security Offset

Increasingly Have Social

Security Income Below the

Median Benefit Amount

Page 16 GAO-17-45 Social Security Offsets

percent of disability beneficiaries and 16 percent of retirement

beneficiaries.

29

Over time, the population of older Americans in Social Security offset has

become increasingly composed of those with Social Security incomes

below the median benefit amount. In 2004, 21 percent of older Americans

subject to Social Security offset received benefits that would have placed

them in the bottom half of the overall benefits distribution before

considering the amount withheld through offset (see table 2). By 2014,

about 60 percent of older Americans subject to offset received benefits

that, prior to offset, would place them below the median Social Security

benefit amount—about $1,070 for disability beneficiaries and $1,320 for

retirement beneficiaries in 2014.

Table 2: Social Security Benefits of Older Americans Subject to Offset Compared to

Overall Benefit Distribution

Proportion of offset population benefit amounts in

quintiles (Q) of overall Social Security benefit distribution

Year

Q1 (lowest

20 percent)

Q2

Q3

Q4

Q5 (highest

20 percent)

Percent

below

median

benefit

2004

0

5

40

37

18

21

2009

0

30

35

23

12

49

2014

2

41

28

20

9

60

Source: GAO analysis of data from the Departments of Education and the Treasury, and the Social Security Administration. |

GAO-17-45

Note: Disability beneficiaries subject to Social Security offset for defaulted federal student loans are

compared to the overall distribution of disability benefit amounts, and retirement beneficiaries subject

to offset are compared to overall distribution of retirement benefits. Quintile cutoffs were calculated

using published Social Security Administration tables and are approximate. Benefit amounts are prior

to any deductions or offsets.

29

Across all Social Security beneficiaries, the overall distribution of Social Security benefit

amounts tends to increase over time. Cost of living adjustments increase payments to

current beneficiaries. Additionally, newly entitled beneficiaries, on average, have higher

earnings and thus higher initial benefit amounts than those whose benefits began many

years ago.

Page 17 GAO-17-45 Social Security Offsets

A small share of Education’s total collections from the Treasury Offset

Program came from Social Security offsets. Nearly three-quarters of the

collections through Social Security offset were applied to Treasury Offset

Program fees and to interest on the remaining loan balance, rather than

to loan principal. With respect to outcomes for older borrowers, about half

of borrowers remained in offset for 1 year or less while others remained in

offset for multiple years. Over a 5 year time period after becoming subject

to Social Security offset, nearly one-third of older borrowers were able to

pay off their loans or obtain a disability discharge. However, other older

borrowers remained in default on their student loans, and some had their

loan balances increase over time despite the reductions to their Social

Security benefits.

Data from Treasury show that Education collected about $171 million in

Social Security offsets in fiscal year 2015, which amounted to a small

share of the agency’s total collections from the Treasury Offset Program

(see fig. 6). In total, Education collected almost $2.3 billion from offsets of

any kind. The $171 million collected from Social Security offsets was

equivalent to about 8 percent of this total. The vast majority of offsets for

Education debt— nearly $2.1 billion, or about 91 percent—were from

federal tax refunds.

30

30

As described earlier, Education’s total collections amounted to about $4.5 billion in fiscal

year 2015. Thus, about half of this amount—nearly $2.3 billion—came from collections

through the Treasury Offset Program, including federal tax refunds and Social Security

offsets.

Social Security

Offsets Were a Small

Share of Education’s

Collections and

Primarily Paid down

Fees and Interest as

Many Borrowers

Remained in Default

after 5 Years

Social Security Offsets

Were a Small Share of

Education’s Collections

through the Treasury

Offset Program, but a

Relatively Larger Share of

These Offsets Went

toward Program Fees

Page 18 GAO-17-45 Social Security Offsets

Figure 6: Total Amount of Offset Collections for Education Debt and Share

Allocated to Treasury Offset Program Fees by Type of Offset, Fiscal Year 2015

Note: These data reflect the amount of net offset collections after any reversals of offsets initially

processed during the fiscal year.

As shown in figure 6, a relatively larger share of the total amount

collected through Social Security offsets went toward Treasury Offset

Program fees. In fiscal year 2015, the fee for each Social Security offset

was $15 compared to $17 for each federal tax refund offset. Because

offset fees are assessed per transaction, a borrower subject to monthly

Social Security offsets could pay up to $180 per year in fees compared to

$17 for a single federal tax refund transaction. According to data from

Treasury, offset fees collected through the Treasury Offset Program

amounted to about 11 percent of Social Security offsets collected for

Education debt compared to 1 percent for federal tax refund offsets.

31

31

Treasury’s data show that overall program fees for collection of federal non-tax debt

owed to Education and other federal agencies through the Treasury Offset Program

amounted to about $167 million in fiscal year 2015. Of this amount, fees for federal tax

refunds and Social Security benefits amounted to about $79 million and $73 million,

respectively. Fiscal Service charges fees to Federal agencies for offset to cover the cost

of the Treasury Offset Program. According to Fiscal Service, the fee for Social Security

offsets, decreased from $17 per offset in fiscal year 2013 to $15 per offset in fiscal year

2014 due to projected increases in the volume of offsets and funding requirements that

were relatively constant.

Page 19 GAO-17-45 Social Security Offsets

Collections on defaulted student loans through Social Security offset were

applied primarily to borrowers’ fees—including Treasury Offset Program

fees, as well as other fees charged to defaulted borrowers by

Education—and interest. Treasury’s Bureau of the Fiscal Service retains

the Treasury Offset Program fee and sends the remainder of the offset to

Education.

32

Education officials said that for each student loan, it applies

the offset first to any outstanding fee balance,

33

then to accrued interest,

and then to principal.

34

Of the approximately $1.1 billion collected through

Social Security offsets from fiscal years 2001 through 2015 from

borrowers of all ages, about 71 percent was applied to fees and interest—

12 percent to fees and 59 percent to interest—compared to 28 percent

that was applied to principal.

Among borrowers 50 or older at the time of initial offset, 53 percent had

no portion of their offset payments applied to principal. This figure was

even higher among older borrowers whose monthly benefit was below the

poverty guideline prior to offset—68 percent of these borrowers had the

full amount of their offset payments applied to fees and interest only.

35

In

contrast, 23 percent of borrowers 50 and older had the majority of their

offset payments applied to principal.

36

These borrowers came

disproportionately from those whose monthly benefit was above the

poverty guideline even after offset.

32

As described earlier, Treasury assesses offset fees to Education, and Education, in turn,

passes the fees on to borrowers.

33

These fees are distinct from the fee Treasury charges for the Treasury Offset Program.

Certain fees, including late payment fees and collections costs, may be charged to

defaulted borrowers. 34 C.F.R. §§ 682.202(e)-(f) and 685.202(d)-(e). Such fees constitute

less than 0.01 percent of the aggregate loan balance of older Americans at the time of

initial offset.

34

According to Education officials, when a borrower has multiple loans eligible for offset,

Education applies the amount offset to each loan in proportion to that loan’s share of the

total balance eligible for offset.

35

These calculations are based on the Department of Health and Human Services Federal

Poverty Guideline for a single individual, available at: https://aspe.hhs.gov/prior-hhs-

poverty-guidelines-and-federal-register-references.

36

Among borrowers who were under 50 at the time of their initial offset, 47 percent did not

have any portion applied to principal, while 27 percent had more than half of their offsets

applied to principal. For those under 50 with benefits below the poverty guideline prior to

offset, 56 percent did not have any portion of their offset applied to principal.

More Than 70 Percent of

the Amount Collected

through Social Security

Offset Was Applied to

Borrowers’ Fees and

Interest

Page 20 GAO-17-45 Social Security Offsets

About half of older Americans who had Social Security offsets to repay

student loan debt were no longer subject to offset within a year, while

slightly more than one-third remained subject to offset for 2 years or

more.

37

Looking across the approximately 126,000 borrowers 50 and

older whose initial Social Security offset was in fiscal years 2001 through

2010, 45 percent were subject to offset for a year or less, including 8

percent who were only subject to offset for a single Social Security

payment.

38

In contrast, 37 percent had their Social Security benefits

reduced for multiple years. Specifically, about 25 percent were in offset

for 2 to 5 years and 12 percent were in offset for 5 years or more. Results

were similar between borrowers 50 to 64 and borrowers 65 and older

(see fig. 7).

37

This section focuses on the longest continuous period of time borrowers were subject to

offset. Borrowers can be subject to offset for multiple periods of time. For example,

borrowers who rehabilitate their defaulted loans would no longer be subject to offset but

could later become subject to offset again if they defaulted a second time.

38

We restricted this analysis to borrowers who entered offset prior to fiscal year 2011 so

that we could track borrowers for 5 years after their initial offset. Across fiscal years 2001

through 2015, there were about 285,000 older borrowers who became subject to offset.

About Half of Older

Americans with Defaulted

Student Loans Remain

Subject to Social Security

Offsets for 1 Year or Less,

but Those with Larger

Balances Tend to Remain

Longer

Page 21 GAO-17-45 Social Security Offsets

Figure 7: Length of Time Older Borrowers Were Subject to Offset of Their Social

Security Benefits for Defaulted Student Loan Debt, by Borrower Age (2001 through

2010)

Older borrowers who were subject to offset for shorter periods tended to

owe less than those who remained subject to offset for longer periods of

time. Specifically:

• Less than 1 year: These borrowers had a median loan balance of

about $6,000 and an average balance of $12,150 at the time of initial

offset.

39

39

Because some borrowers have large student loan balances, the average amount of

student loan debt per borrower for any group of borrowers tends to be higher than the

median amount of debt for that group. This analysis includes borrowers whose initial offset

occurred in fiscal years 2006 through 2010 because loan balance histories prior to 2006

were not consistently available from Education.

Page 22 GAO-17-45 Social Security Offsets

• 2 to less than 5 years: These borrowers had a median balance of

$8,000 and an average balance of $15,250.

• 5 or more years: These borrowers had a median balance of $12,800

and an average balance $22,450.

Many older borrowers had paid off or discharged their debt 5 years after

their initial Social Security offset, but others remained in default and

offset.

40

Among those 50 and older at the time of their initial offset, about

32 percent had paid off or discharged their debt due to disability or school

closure or otherwise closed their loans after 5 years for reasons other

than death.

41

An additional 13 percent died while their loans were

outstanding (see fig. 8). The remainder—about 55 percent—had loans

that were still open 5 years after their initial offset. Most of these

borrowers with open loans were in default, but others had emerged from

default by rehabilitating or consolidating their loans. Specifically, about 36

percent of those 50 and older at the time of their initial offset were in

default after 5 years, including 20 percent who were still in offset.

42

A

small share—about 10 percent—was able to rehabilitate or consolidate

their loans and was in repayment.

40

Using data encompassing fiscal years 2001 through 2015, we examined outcomes for

borrowers 5 years after the date of their initial offset. For some borrowers, the 5-year

period included the recession from 2007- 2009, which may have impacted some

borrowers’ economic situation, including their employment prospects. For more

information about the economic impacts for older Americans from the 2007-2009

recession, see GAO, Income Security: Older Adults and the 2007-2009 Recession,

GAO-12-76 (Washington, D.C.: Oct. 17, 2011).

41

In certain circumstances, borrowers may be able to discharge their debt for reasons

other than disability or death, including if their school closes while they are enrolled or

soon after they withdrew or if their school falsely certified their eligibility to receive the

loan.

42

Some borrowers who were in offset 5 years later may not have been continuously in

offset.

Almost One-Third of Older

Americans in Social

Security Offset Paid Off or

Discharged their Student

Loans, but About 36

Percent Were Still in

Default after 5 Years

Page 23 GAO-17-45 Social Security Offsets

Figure 8: Share of Older Borrowers by Outcome 5 Years after Initial Social Security Offset to Repay Defaulted Student Loan

Debt, Fiscal Years 2001 to 2010

Notes: Data on 5 year outcomes include borrowers who became subject to offset prior to fiscal year

2011 in order to observe borrowers for a full 5 year time period through fiscal year 2015. Loan

balance data were only available from fiscal year 2006 onward.

a

Borrowers who are totally and permanently disabled may be eligible to discharge their debt through a

Total and Permanent Disability (TPD) discharge subject to several requirements, including a 3-year

monitoring period.

Page 24 GAO-17-45 Social Security Offsets

b

In certain circumstances, borrowers may be able to discharge their debt for reasons other than

disability or death, including if their school closes while they are enrolled or soon after they withdrew

or if their school falsely certified their eligibility to receive the loan.

c

Rehabilitation is a process by which borrowers can remove a loan from default by making a minimum

number of requirement payments. Consolidation allows borrowers to combine multiple loans into one

loan.

d

Under certain circumstances, borrowers who are not in default may also receive a forbearance or

deferment that allows them to temporarily postpone or reduce their student loan payments.

e

Education has also established a process to allow defaulted borrowers who are subject to offset to

apply for a financial hardship exemption or reduction in offset.

As shown in figure 8, older borrowers who had been in offset but then

paid off their loans had substantially smaller outstanding loan balances at

the time of their initial offset compared to other older borrowers subject to

offset. For example, the median outstanding balance for older borrowers

who were in offset but paid off their loans within 5 years was $2,379

compared to a median outstanding balance of $11,838 for borrowers who

were still in offset.

43

Among the 55 percent of older Americans who still had student loans

open 5 years after their initial Social Security offset, most had made some

progress toward paying down their loan balances, but the loan balances

of others increased over time. Taking into account Social Security offsets

as well as any other source of payment on a borrower’s loans, such as

tax refund offsets or voluntary payments, the majority (60 percent) of

these borrowers had decreased their loan balances. The loan balances of

the remaining 40 percent grew because the payments on their loans from

all sources did not keep up with accruing interest.

44

Borrowers who remained in Social Security offset after 5 years tended to

have made more progress in paying down their loan balances compared

to other borrowers who still had open loans but were no longer in offset.

For example, some borrowers may no longer have been in offset because

43

Additional information on outcomes of older Americans with Social Security offsets can

be found in appendix III, tables 15 and 16, including outcomes by age and duration in

offset. Outcomes for those in the age 50 to 64 and age 65 and older categories were

similar overall. Older borrowers who had a shorter duration of time spent in offset

generally had more favorable outcomes than those who remained in offset for longer

periods of time.

44

A somewhat greater proportion of borrowers younger than 50 who had open loans after

5 years had their loans increase over time; 47 percent of these borrowers owed more at

the end of 5 years than they did when their first offset occurred.

Some Older Americans in

Offset Have their Student

Loan Debt Increase over

Time

Page 25 GAO-17-45 Social Security Offsets

they rehabilitated or consolidated their loans, but were then in

forbearance or deferment and, thus, were not making payments.

Specifically:

• Borrowers who remained in offset: Among borrowers 50 and older

who still had offsets after 5 years, 32 percent had their loan balances

increase after considering all sources of payment on their loans.

• Borrowers with a financial hardship exemption from offset: 48

percent of borrowers 50 and older who still had open loans but had

secured a hardship exemption—and thus were no longer making

payments through Social Security offset—had a greater loan balance

after 5 years.

• Borrowers in forbearance or deferment: Borrowers 50 and older

who exited offset by rehabilitating or consolidating their loans but were

in forbearance or deferment at the end of 5 years—and thus not

making payments—fared particularly poorly, as 67 percent owed more

than they did when they entered offset.

More borrowers who were in Social Security offset for several years paid

down principal with their offsets than borrowers who were briefly in offset,

but some borrowers had not paid any principal after years of offsets.

Among borrowers age 50 or older who stayed in offset for less than 1

year, 60 percent paid only fees and interest. For those in offset for more

than 5 years, about one-third paid only fees and interest with their offsets,

while about two-thirds paid some principal.

45

45

Because many borrowers have accrued outstanding interest balances when they enter

offset, a borrower whose Social Security offsets do not decrease the loan principal can still

decrease their overall loan balance by paying down the outstanding interest, as long as

the amount of the Social Security offset applied to outstanding interest is greater than the

monthly interest accruing on the loan.

Page 26 GAO-17-45 Social Security Offsets

A growing number of older borrowers may experience financial hardship

in the years leading up to or during retirement because the Social

Security offset threshold has not been adjusted for increases in costs of

living since program provisions were implemented by regulation in 1998.

In addition, many older Americans subject to offset may be eligible for a

TPD discharge but they have not applied for one, and Education is taking

steps to reduce the numbers of borrowers who have not applied.

Education is also taking steps to automatically suspend offsets for certain

disabled borrowers, but these steps could adversely affect borrowers at

an older age. This is because Education does not provide these

borrowers with information that would help them make more informed

choices about applying for a TPD discharge. Further, for those who apply

for a TPD discharge, key requirements of the 3-year monitoring period

are not clearly communicated. As a result, older borrowers and others

with disabilities may not complete required documentation to continue

receiving this relief. Finally, Education established a process for granting

financial hardship exemptions or reductions from offset, but they do not

provide borrowers information about this option unless requested or

review these exemptions once granted.

Older borrowers who remain in offset may increasingly experience

financial hardship. Such is the case for a growing number of older

borrowers whose Social Security benefits have fallen below the poverty

guideline because the offset threshold is not adjusted for increases in

costs of living. The threshold for Social Security offsets was established

to prevent undue financial hardship on borrowers who rely on benefits for

a substantial part of their income and who may be unable, rather than

unwilling, to repay debts.

46

This is consistent with the policy underlying

the Social Security program that benefits are intended to help ensure

older Americans have adequate retirement incomes and do not have to

depend on welfare.

47

According to SSA, Social Security benefits

represented 90 percent or more of total income for about one-third of

beneficiaries 65 and older in 2014.

48

At the time it was set, in 1998, the

46

See H.R. Rep. No. 104-537, at 565-67 (1996) (Conf. Rep.).

47

Once payments have begun, Social Security benefits are generally adjusted annually to

reflect increases in the cost of living. For more information on the Social Security program,

see GAO, Social Security’s Future: Answers to Key Questions, GAO-16-75SP

(Washington, D.C.: Oct. 27, 2015).

48

Social Security Administration, 2016.

Program Design May

Impact Retirement

Security for Older

Borrowers, Including

Those Seeking Relief

Permitted for

Permanent Disability

or Financial Hardship

A Growing Number of

Older Borrowers with

Social Security Offsets

May Experience Financial

Hardship because the

Offset Threshold Is Not

Adjusted for Increases in

Costs of Living

Page 27 GAO-17-45 Social Security Offsets

threshold for Social Security offsets was above the poverty guideline—

$750 a month represented about 112 percent of the poverty guideline for

a single adult that year.

49

However, in the absence of cost of living

adjustments, the relative value of the offset threshold has declined over

time to well below the poverty guideline. In 2016, the poverty guideline for

a single adult equated to a monthly income of about $990, and the $750

threshold represented about 76 percent of this amount.

50

Consequently,

an increasing number of older Americans subject to Social Security

offsets received benefits below the federal poverty guideline. In fiscal year

2004, about 8,300 borrowers in the 50 and older age category had

benefits below the poverty guideline compared to almost 67,300 in fiscal

year 2015 (see fig. 9). As a share of borrowers in the 50 and older age

category, this growth was equivalent to an increase from 38 percent in

fiscal year 2004 to 64 percent in fiscal year 2015.

51

In addition, as shown

in figure 9, a growing number of these older borrowers already received

Social Security benefits below the poverty guideline before offsets further

reduced their income.

49

This figure is based on the Department of Health and Human Services Federal Poverty

Guideline in 1998 for a single individual in the 48 contiguous states and the District of

Columbia, available at: https://aspe.hhs.gov/prior-hhs-poverty-guidelines-and-federal-

register-references.

50

This poverty guideline applies to a single individual in the 48 contiguous states and the

District of Columbia.

51

Likewise, a growing number of younger borrowers subject to Social Security offset have

benefits below the poverty guideline. In fiscal year 2004, 7,600 borrowers under 50 who

had Social Security offsets received benefits—primarily for disability—below the poverty

guideline, equivalent to 47 percent of this group. By fiscal year 2015, this number had

risen to nearly 51,500 borrowers, equivalent to 76 percent of this group.

Page 28 GAO-17-45 Social Security Offsets

Figure 9: Number of Borrowers Age 50 and Older Whose Social Security Benefits Are below the Poverty Threshold after

Offset for Education Debt, Fiscal Years 2004 to 2015

Note: Borrowers’ Social Security benefit and offset amounts for each month in a fiscal year were

compared to the monthly equivalent of the Department of Health and Human Services Federal

Poverty Guideline for a single individual in the 48 contiguous states and the District of Columbia in the

relevant calendar year. Borrowers who received Social Security benefits below the poverty guideline

for the majority of months they were subject to offset in a fiscal year were categorized as being below

the poverty guideline.

Proposals to adjust Social Security offset provisions—such as by indexing

the offset threshold—have been made by Education and proposed in

legislation. In October 2015, Education proposed that the Social Security

offset threshold be indexed to inflation.

52

In its support for this proposal,

Education noted that the Debt Collection Improvement Act of 1996

recognizes that Social Security is “a key source of income for many

52

U.S. Department of Education, “Strengthening the Student Loan System to Better

Protect All Borrowers,” Oct. 1, 2015.

Page 29 GAO-17-45 Social Security Offsets

disabled and elderly Americans.” In addition to Education’s proposal,

legislation was introduced in October 2015 to index the Social Security

offset threshold to inflation.

53

It is also important to recognize that adjusting Social Security offset

provisions would reduce Education’s recoveries from Social Security

offsets. If the offset limit had been indexed to match the rate of increase

in the poverty guideline, 62 percent of all older borrowers whose Social