PUBLIC

Stocktake on diversity, equity and

inclusion in the insurance sector

December 2022

PUBLIC

About the IAIS

The International Association of Insurance Supervisors (IAIS) is a voluntary membership

organisation of insurance supervisors and regulators from more than 200 jurisdictions. The mission

of the IAIS is to promote effective and globally consistent supervision of the insurance industry in

order to develop and maintain fair, safe, and stable insurance markets for the benefit and protection

of policyholders and to contribute to global financial stability.

Established in 1994, the IAIS is the international standard-setting body responsible for developing

principles, standards, and other supporting material for the supervision of the insurance sector and

assisting in their implementation. The IAIS also provides a forum for members to share their

experiences and understanding of insurance supervision and insurance markets.

The IAIS coordinates its work with other international financial policymakers and associations of

supervisors or regulators, and assists in shaping financial systems globally. In particular, the IAIS is

a member of the Financial Stability Board (FSB), a member of the Standards Advisory Council of the

International Accounting Standards Board (IASB), and a partner in the Access to Insurance Initiative

(A2ii). In recognition of its collective expertise, the IAIS also is routinely called upon by the G20

leaders and other international standard-setting bodies for input on insurance issues as well as on

issues related to the regulation and supervision of the global financial sector.

For more information, please visit www.iaisweb.org and follow us on LinkedIn:

IAIS – International

Association of Insurance Supervisors.

International Association of Insurance Supervisors

c/o Bank for International Settlements

CH-4002 Basel

Switzerland

Tel: +41 61 280 8090

This document was prepared by the Governance Working Group and the Market Conduct Working

Group in consultation with IAIS members.

This document is available on the IAIS website (www.iaisweb.org

).

© International Association of Insurance Supervisors (IAIS), 2022.

All rights reserved. Brief excerpts may be reproduced or translated provided the source is stated.

PUBLIC

Content Overview

Content Overview .............................................................................................................. 3

Executive Summary .......................................................................................................... 4

A note on terminology .............................................................................................................. 6

Introduction ......................................................................................................................... 7

The IAIS’ interest in DEI ................................................................................................................... 7

Overview of this stocktake ............................................................................................................... 8

Insurance supervisors’ perspectives and activities ....................................................... 10

Perspectives on priority and mandate ............................................................................................ 10

Challenges ..................................................................................................................................... 10

Supervisory activities ..................................................................................................................... 12

2.3.1 Governance and risk management focus ............................................................................... 12

2.3.2 Market conduct focus .............................................................................................................. 18

Insurance industry action on DEI .................................................................................... 21

As observed by insurance supervisors .......................................................................................... 21

As explained by the industry through stakeholder engagement .................................................... 22

3.2.1 Why DEI is relevant and important to insurers ....................................................................... 23

3.2.2 The challenges faced in embedding DEI ................................................................................ 24

3.2.3 The role for supervisors .......................................................................................................... 24

The international-level landscape and how IAIS activity fits ......................................... 25

Across key international organisations .......................................................................................... 25

4.1.1 Overview ................................................................................................................................. 25

4.1.2 Commitments to their own DEI ............................................................................................... 25

4.1.3 Recognition of the link between DEI and good governance and risk management ............... 25

4.1.4 Global coordination and knowledge sharing among financial supervisors on DEI ................. 26

4.1.5 International organisations supporting supervisors to enhance gender inclusion .................. 27

At the IAIS ...................................................................................................................................... 28

4.2.1 IAIS work to date ..................................................................................................................... 28

4.2.2 2023 and beyond .................................................................................................................... 29

Conclusion ........................................................................................................................ 30

PUBLIC

Executive Summary

The IAIS recognises the importance of diversity, equity, and inclusion (DEI) considerations to the

objectives of insurance supervision and consequently to the IAIS' mission. DEI is particularly relevant

to governance, culture and conduct, but also to financial inclusion and sustainable economic

development as well as innovation and social responsibility.

The IAIS has committed to deepening and strengthening its work on DEI in a number of ways. They

include exploring the insurance sector's efforts and steps taken by supervisors in support of DEI,

incorporating relevant DEI aspects into ongoing IAIS projects and activities, and considering

opportunities for cooperation on DEI with other international organisations and partners, such as the

Access to Insurance Initiative (A2ii).

This report represents the first step in this work. It aims to take stock of work on DEI already being

undertaken by insurance supervisors, relevant international organisations and the insurance

industry, with a view to identifying areas where the IAIS could do further work in this area, in support

of its mission and strategic plan. The report is not intended to make recommendations or set out an

IAIS position on best practices in supervision.

Information in this report on the perspectives and activities of insurance supervisors is drawn from

an IAIS member survey conducted in March/April 2022. The survey attracted 39 responses from

jurisdictions around the world, with the largest proportion of responses coming from Western

European jurisdictions, followed by North American and Asian jurisdictions. The survey asked

supervisors about their approaches to DEI, the approaches they observe being taken within the

insurance industry in their jurisdictions, and their ideas about further work that the IAIS could

undertake in this area. It included questions about their perception of their supervisory mandate for

DEI, the priority they attribute to it, and the activities they are undertaking, as well as their thoughts

on the challenges and opportunities that arise.

Key findings include:

• Just over half of the supervisors that responded to the survey attribute a medium or high priority

to taking supervisory action to promote DEI within insurers, with the remainder viewing it as a

low priority. Those that noted a high priority generally made it one of their strategic priorities,

often with a focus on corporate governance and Board diversity. Some supervisors that attributed

DEI a medium priority indicated that their jurisdiction already had some policies in place, while

many of those that attributed a low priority considered it less relevant for their jurisdiction, outside

of their remit, or that they had already made sufficient progress.

• The majority of respondents thought they had a supervisory mandate to act, while a minority

believed they did not, or that they face other legal constraints. There was broad agreement that

a key challenge is the absence of an agreed standard, best practice guidance, or regulatory

framework for approaching DEI-related supervisory activities.

• A number of jurisdictions see insurers' governance as a key area for supervisory activity on DEI,

in line with Insurance Core Principle (ICP) 7 on Corporate Governance. This could be supported

by a combination of formal requirements and industry communications. The report outlines steps

that a number of jurisdictions are taking on DEI in the corporate governance of insurers.

• In the area of market conduct, there is less supervisory focus specifically on the concept of DEI,

although the majority of supervisors do report having conveyed to some extent their supervisory

expectations that insurers conduct their business in a way that, in effect, promotes customer DEI.

This is because most supervisors report having laws, regulations and/or guidelines that prohibit

PUBLIC

discriminatory practices in insurance, and supervisors are expected to have frameworks in place

requiring the fair treatment of customers in line with ICP 19 on Conduct of Business.

• A third of survey respondents have conducted analysis of the state of DEI in the insurance

industry in their jurisdiction. Supervisors have observed that action is being undertaken not only

by individual insurers, but also by industry associations at various levels. Industry initiatives tend

to relate either to financial inclusion/access to insurance, or to the pursuit of more diversity in the

people working in the insurance industry. The report outlines some examples and key themes of

industry initiatives in several jurisdictions.

The IAIS also engaged with a small sample of stakeholders in the insurance industry who were

asked why they saw DEI as important to insurers, the biggest challenges they face in embedding

DEI, and what they think supervisors can do. Stakeholders generally agreed that DEI can lead to

better outcomes for insurer governance and customers, listing a number of specific benefits. From

the perspective of the stakeholders involved, one of the key challenges was the current voluntary

nature of much DEI activity: more action and formal structure could help drive progress. They believe

that supervisors should send a clear message to insurers about the importance of DEI, but avoid

being overly prescriptive.

Research into the work of international organisations revealed growing interest in DEI from a number

of influential organisations, with a few examples outlined in this report, but direct action is still largely

at an early stage. The international-level landscape suggests that further work on DEI by the IAIS

could make a unique and value-adding contribution.

Arising from the outcome of this stocktake, the IAIS plans to initiate work aimed at helping

supervisors to further understand the benefits of DEI, the connection between promoting DEI and

their supervisory mandates, and the range of available supervisory practices to promote DEI. This

work will have two main focuses. One will be to examine the link between DEI within insurers’

institutions and governance, risk management and corporate culture. The other will be to examine

how DEI considerations in insurers’ conduct of business, and their supervision, may result in fairer

treatment of consumers who are vulnerable, under-served or have different needs in comparison

with a normative or majority consumer profile.

The IAIS considers that DEI is relevant to, and anticipates interlinkages with, other IAIS priority work,

particularly on the topics of financial inclusion, fintech, climate risk and protection gaps. DEI will

continue to be a strategic theme across the IAIS’ work programme.

The IAIS will continue drawing attention to the importance of DEI for the achievement of better

prudential and consumer outcomes and greater inclusion, and encourages the supervisory

community and industry to continue progressing activity on DEI.

PUBLIC

1

In South Africa, “transformation of the insurance sector” is defined within the Insurance Act, 2017 (Act No 18 of 2017) to mean

transformation as envisaged by the Financial Sector Code for Broad-Based Black Economic Empowerment issued in terms of

section 9(1) of the Broad-Based Black Economic Empowerment Act, 2003 (Act No. 53 of 2003). “Broad-based black economic

empowerment” is defined as the economic empowerment of all black people, in particular women, workers, youth, people with

disabilities and people living in rural areas through an assortment of diverse but integrated socio-economic strategies…,” and then

the definition proceeds to explain what these integrated socio-economic strategies will include.

A note on terminology

The survey of supervisors confirmed that most jurisdictions use some or all of the terms “diversity”,

“equity”, and “inclusion”. Many have adopted the term “diversity and inclusion”, and a few use

additional or different terms, such as “collectivity”.

Although 75% of respondents reported not having an applicable official definition of DEI (or

alternative relevant terminology), many reported having rules and/or regulations in place that cover

the concept, and that its meaning can adapt to the unique current and historical context of the

jurisdiction. One example of jurisdiction-

specific terminology is South Africa where the terms

“transformation of the insurance sector” and “broad-based black economic empowerment” are

defined in legislation.

1

In harmony with various definitions and interpretations reported by supervisors, this report uses

the following interpretations of the terms ‘diversity’, ‘equity’, and ‘inclusion’:

• Diversity: A reflection of the differences between people within an organisa

tion or wider

society.

This includes different perspectives, abilities, knowledge, attitudes, skills, experience and

demographic characteristics. Demographic characteristics are often considered a key factor in

diversity, and may include, but are not limited to, characteristics such as

age, disability,

ethnicity, gender, national origin, religion, sexual orientation, as well as cultural, educational

and/or socio-economic background. The notion that the differences between people can lead

them to think differently from one another and therefore have varying perspectives to contribute

to an organisation is sometimes called ‘diversity of thought’ or ‘cognitive diversity’.

• Equity: Seeking to achieve fairness and equal outcomes for all through allocating resources

and opportunities in a way that recognises the different circumstances and needs of different

groups of people, particularly where there is evidence of disadvantage among certain groups.

Equity is different from equality: equality offers the same resour

ces and opportunities to

everyone, while equity helps remove the barriers that some people may face in accessing

resources and opportunities.

• Inclusion: When all people in an organisation, regardless of their differences, feel a sense of

belonging which enables them to fully participate in and contribute to the organisation.

This includes a culture in which a mix of people, at all levels of seniority, feel empowered to

speak up and express their views. Employees at an inclusive organisation feel confident that

their views will be heard and that there will never be negative repercussions for challenging

the prevailing views.

• Financial inclusion: When individuals and businesses have access to suitable financial

products that meet their differing needs.

PUBLIC

Introduction

The IAIS’ interest in DEI

In 2021, the IAIS adopted diversity, equity, and inclusion (DEI) as one of its key strategic themes,

and published a statement

recognising the importance of DEI in insurance supervision. The IAIS

joins with others in the growing acknowledgment that advancing DEI within insurers’ organisations

and in their approach to doing business supports better prudential and consumer outcomes.

In this current work, the IAIS is interested in promoting DEI at insurers in both an internal/institutional

sense (ie the insurers’ workforce, leadership, culture, decision-making, and risk management) and

in a customer-facing sense (ie equitable and inclusive treatment of customers that recognises

diversity in the customer base). Collectively, this covers ICP 7 (Corporate Governance), 8 (Risk

Management and Internal Controls) and 19 (Conduct of Business).

Adopting a greater regard for DEI in the customer-facing sense may bring a different way of thinking

about fair treatment of customers by requiring more consideration of consumers who are not in the

majority. Vulnerable consumers are one such minority cohort, and some supervisors have already

established different expectations for their fair treatment.

2

In its Issues Paper on Insurer Culture

(2021), the IAIS noted the importance of embedding an

organisational culture that consistently promotes sound prudential and conduct outcomes. The

Issues Paper observed that the collective set of norms, practices, decision-making and behavioural

elements that make up an insurer’s culture directly influence how it manages prudential and conduct

risks. It also recognised that an insurer’s approach to DEI issues is one element likely to influence

its overall culture, and vice versa.

The IAIS considers that a focus on improving and sustaining DEI will help insurers build cultures that

better support sound prudential and consumer outcomes in a number of ways:

• Diversity embedded within an organisation and reinforced by a culture of equity and inclusion

positively impacts insurers' corporate governance and risk management by improving decision-

making and reducing the risk of groupthink.

3

Diversity brings together individuals with different

backgrounds, which means that broader perspectives can be shared, leading to a wider view of

potential risks and opportunities. People with different backgrounds and experience may notice

different things, and are therefore more likely to pinpoint risks that may be overlooked by a group

of people who all have similar backgrounds and experiences. Equity can enable diversity by

removing barriers to the recruitment, retention and promotion of individuals with a wider range of

different backgrounds and perspectives. Inclusion can also help with retention, and ensure that

2

The Financial Conduct Authority (UK) provides a definition of “vulnerable consumer”: “someone who, due to their personal

circumstances, is especially susceptible to harm - particularly when a firm is not acting with appropriate levels of care [..] These

[characteristics] could be poor health, such as cognitive impairment, life events such as new caring responsibilities, low resilience

to cope with financial or emotional shocks and low capability, such as poor literacy or numeracy skills..” Source:

Guidance for

firms on the fair treatment of vulnerable customers.

A definition from Québec of “person in a vulnerable situation” is “a person of full age whose ability to request or obtain assistance

is temporarily or permanently limited because of factors such as a restraint, limitation, illness, disease, injury, impairment or

handicap, which may be physical, cognitive or psychological in nature, such as a physical or intellectual disability or an autism

spectrum disorder”. Source: Act to Combat Maltreatment of Seniors and Other Persons of Full Age in Vulnerable Situations

.

3

Oxford Reference offers this definition of groupthink: In group decision making, the tendency to drift into ill-conceived policies or

decisions without adequate debate. This can be a result of various pressures, including the illusion of ingroup superiority and the

wish to achieve consensus and avoid painful disagreements.

PUBLIC

individuals can fully participate in the organisation by sharing their different views and providing

robust and constructive challenge. Inclusion helps ensure that people will speak up and share

their differing views, and that the rest of the group will listen, both of which are important for

effective risk management. Throughout this paper, where we refer to the importance of DEI for

improving governance, we are referring to how DEI brings wider perspectives to the table and

can inspire more robust decision-making and risk management.

• DEI may reduce misconduct by creating a stronger culture where employees feel they are valued

and they belong. Inclusion in particular supports an atmosphere where individuals are more likely

to be comfortable voicing concerns, while equity helps a wider range of individuals have an

opportunity to be part of the conversation. Diversity of thought may also mitigate the

rationalisation of poor conduct, which otherwise can allow misconduct to become systemic or

remain undetected for a long time.

• Insurers incorporating DEI considerations into the way that they operate their business (including

all aspects of managing the product life-cycle and interacting with customers) can facilitate

greater innovation and lead to better consumer outcomes. For example, it may prevent

potentially discriminatory practices and lead to the design, distribution and servicing of insurance

products that are better tailored to differing consumer needs. The IAIS also considers that DEI

within an insurer will help it attract a diverse range of consumers to its customer base, and then

treat those customers in a more equitable and inclusive manner, because diversity across the

insurer’s leadership and workforce brings a broader comprehension of the different situations

and needs in a consumer population.

Throughout this paper, where improving DEI is discussed, it is in reference to achieving the

outcomes listed above.

The IAIS aims to contribute to, and accelerate, the momentum of action by both insurance

supervisors and the industry itself to advance DEI in the insurance sector.

Overview of this stocktake

In 2022, the IAIS’ Governance Working Group and Market Conduct Working Group undertook a

survey, and other stakeholder engagement, to examine what actions IAIS member supervisors, other

international organisations and the insurance industry itself are taking to advance DEI in the

insurance sector. The IAIS had not previously undertaken dedicated work specifically on the topic of

DEI in insurance, but various IAIS supporting material has addressed interlinked issues (see section

4.2.1).

This stocktake was intended as a first step to inform possible further IAIS work to promote DEI in

insurers’ governance and conduct of business. The key findings are shared in this report, with a

particular focus on providing insights into insurance supervisors’ activity so far to promote DEI in

insurers.

Inputs to the stocktake were:

• a survey of IAIS member supervisors conducted in March/April 2022;

• research of publicly available information supplemented by direct communication with relevant

international organisations; and

• engagement with a sample of industry stakeholders.

The survey asked insurance supervisors about:

PUBLIC

• the state of DEI in the insurance sector in their jurisdiction;

• their observations of industry action(s) to embed DEI;

• their perception of their supervisory mandate/role for promoting DEI, and the priority they

attribute to this;

• the supervisory activity (if any) they are taking in connection with promoting DEI in insurers’

governance and conduct of business;

• challenges they face in their ability as a supervisor to promote DEI in insurers; and

• what future IAIS work they consider would meaningfully support progress on DEI in the insurance

industry.

Thirty-nine survey responses were received from jurisdictions around the world, as shown in Figure

1.

Thirty-six percent of respondents were from Western Europe, 16% from North America, 15% from

Asia, 8% from Sub Sahara Africa and the remaining 25% were equally spread across the other IAIS

Member Regions. The amount of responses represents roughly a quarter of IAIS members, and is

likely to reflect those members with the most interest in the topic. Nevertheless, we believe the

responses demonstrate a growing level of interest in DEI internationally. These survey results

provide a useful sample that can help inform further IAIS work in this area.

36%

16%

15%

8%

5%

5%

5%

5%

5%

Figure 1:

Respondent jurisdictions by IAIS Member Region

Western Europe

North America

Asia

Sub Sahara Africa

Central, Eastern Europe and

Transcaucasia

Offshore and Caribbean

Latin America

Oceania

Middle East and North Africa

PUBLIC

Insurance supervisors’ perspectives and activities

A key part of this stocktake has been gathering information from IAIS members on their approach to

DEI as a supervisory topic. This includes their views on the priority of DEI supervisory activity within

the context of their jurisdiction, and the key challenges encountered in engaging in supervisory

activity in this area. We consider that variance in the current priority and practice on this topic is to

be expected given the diverse backgrounds of the IAIS membership (eg historical, cultural, legal,

political). Having a better understanding of the breadth of approaches among a sample of IAIS

members will help form a basis for further development of the IAIS’ approach to deepening and

strengthening its work on DEI. In particular, understanding where the challenges lie can help

generate ideas on how the IAIS can best support its members.

Perspectives on priority and mandate

Just over half of respondents attributed a medium or high priority to taking supervisory action to

promote DEI in their jurisdiction’s insurance industry.

Supervisors that consider DEI to be a high priority generally have made it one of their strategic

supervisory priorities or indicate its priority through other communications with the insurers they

supervise and other relevant stakeholders. Many of these supervisors have a particular focus on

corporate governance and Board diversity. Some supervisors also noted that DEI issues are a matter

of broader social responsibility, rather than just a matter of compliance.

Supervisors that attribute a medium priority to promoting DEI explained that their jurisdiction already

had some DEI strategies and policies in place. These jurisdictions already recognised DEI’s

importance and identified existing elements of DEI within their policy framework, or work that was

currently underway.

Nearly half of respondents reported that pursuing supervisory activity to promote DEI in the

insurance industry is currently a low priority for them. Some supervisors described classifying it a

low priority because they consider their jurisdiction has already made sufficient progress. Others

explained that due to market specificities or the nature of their country’s demographics, they had not

identified a need to develop DEI. Some made the point that insurers already abide by local equal

opportunity legislation, or there is no authority or mandate to address DEI. Others view it as a mainly

social, rather than a supervisory, task.

From a conduct of business perspective

4

, most conduct supervisors are not directly promoting DEI

as an explicit concept or requirement for how insurers should treat customers and serve their needs.

Supervisory expectations for the fair treatment of customers pre-date the more recent attention on

DEI, and the survey results suggest that most conduct supervisors have not thought of fair treatment

of customers’ expectations specifically through a DEI lens. In recent years however, some

supervisors have adopted heightened attention on the protection of some cohorts of the population

described as vulnerable customers.

Challenges

Supervisors reported various challenges in promoting DEI, including its subjective nature and the

absence of consistent and usable data. A starting point could be for supervisors to set out some

4

Per ICP 19 Conduct of Business.

PUBLIC

foundational principles and values they consider key to DEI, which could then inform the

development of specific supervisory action.

The survey asked supervisors to choose from a list of possible challenges they might experience in

addressing DEI. These included challenges such as deciding on suitable supervisory action; lack of

supervisory mandate; legal, reputational or privacy concerns; competing superivosry priorities;

industry or other stakeholder reluctance; or other challenges stemming from the jurisdiction’s

particular national context.

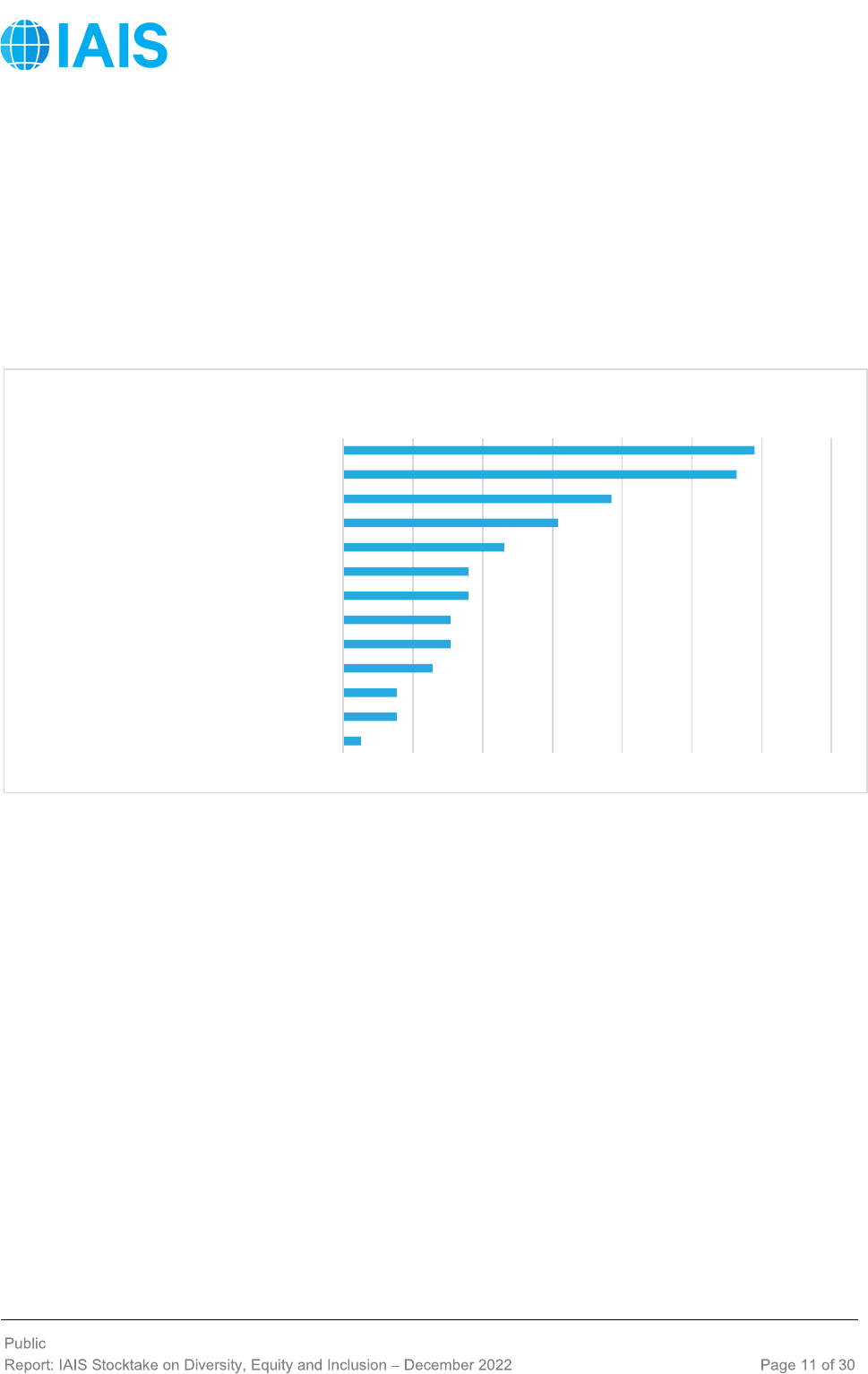

Figure 2 shows the distribution of responses to this question.

Fifty-nine percent of respondents reported that the absence of an agreed standard or best practice

guidelines was a key challenge. This was supported by 31% being uncertain over what action to

take, and 18% feeling constrained by a lack of relevant knowledge or expertise. This lack of

standards and proven best practices is a major impediment to setting expectations in this area and

underpins policy development in some jurisdictions which aims to encourage more openness on

insurers’ DEI strategies. Accordingly, some respondents mentioned they would appreciate

supervisory guidelines, material and support from international supervisory organisations such as

the IAIS. This could help increase supervisors’ confidence to make a start and develop customised

approaches for different jurisdictions.

The second most prominent challenge, mentioned by 56% of respondents, is competing supervisory

priorities: while DEI may well be considered important in many jurisdictions, there may be other

priorities that require more urgent attention. The range of emerging issues that industry faces can

make it difficult to embed DEI within current priorities. To overcome this obstacle, one respondent

suggested considering the reputational and operational DEI-related risks of not taking this aspect

into account in insurers’ general risk assessments. Another respondent has decided to integrate DEI

awareness into all of its regular supervisory activities.

Thirty-eight percent of respondents stated that they faced a lack of supervisory mandate to act.

However, this was not necessarily because these jurisdictions lacked the regulatory framework to

0% 10% 20% 30% 40% 50% 60% 70%

Resistance/reluctance of other stakeholders

Overlapping responsibility for DEI

Hypocritical risk

Resistance/reluctance of insurers

National historic, cultural or political context

Other

Lack of relevant knowledge/expertise

Data privacy concerns

Other legal constraints

Uncertainty over what action to take

Lack of supervisory mandate to act

Competing supervisory priorities

Absence of agreed standards/best practice

Figure 2: Most common supervisory challenges

PUBLIC

take action in this area. Written comments from the survey instead indicated that this perception was

related to the lack of existing legally enforceable and specific rules on DEI in many jurisdictions.

Most respondents advised there are no sensitivities that create any significant barriers to taking

action. However, for some supervisors, considering differing cultures or issues relating to indigenous

communities requires careful consideration.

On balance, the survey responses seemed to indicate a broadening of interest in DEI across many

jurisdictions. Where supervisors believe they have a mandate to act on DEI, they are considering

ways to do so, but can find it challenging due to an absence of existing legally enforceable rules,

and the lack of agreed standards or best practice guidelines in this area. This seems to be one area

where the IAIS may be able to support its members, by pooling resources gathered across

jurisdictions.

Supervisory activities

2.3.1 Governance and risk management focus

The IAIS considers that DEI within an insurer can reduce the risk of groupthink, provide the safety

to speak up and improve decision-making, thereby positively impacting governance and risk

management.

5

The survey asked IAIS members whether they thought they had a mandate to take

action on DEI in insurers’ governance, and what actions they were taking, or planning to take, in this

area.

Seventy percent of supervisors report having some level of mandate or legal framework that supports

them taking action to promote DEI in insurers’ governance. Among those taking action in this area,

many report that their work on DEI is at a fairly early stage.

There is not currently a clear picture as to which actions should be prioritised in order to embed DEI

in the industry. Many supervisors suggested that a combination of different factors is key to

supporting progress on DEI. For instance, formal requirements could help, but supervisors could

also promote DEI through best practice examples and communicating with industry about the

benefits and particular advantages. Frequent opportunities for an exchange of ideas and views

between industry, supervisors and other stakeholders are also regarded as important.

The majority of respondents (76%) were currently taking some sort of supervisory action on DEI.

Figure 3 shows the most common supervisory activities among those respondents that were taking,

or planning to take, supervisory action on DEI.

5

See section 1 for more explanation of the IAIS’ view that DEI positively impacts governance and risk management.

PUBLIC

The most frequently reported activity is advocating DEI through written and verbal communications.

Respondents approached advocacy of DEI in a range of ways, including:

• through publications such as annual reports, corporate strategies, and supervisory priority letters

addressed to industry;

• in the press or on social media;

• in speeches or blogs from senior leaders;

• through presentations to relevant stakeholders (including central banks, other supervisors, and

industry representatives);

• through participation in public fora and campaigns dedicted to DEI; and

• through setting an example by prioritising DEI in their internal operations.

The second most frequently reported activity is asking insurers about DEI during supervisory

examinations/interviews. Some examples of this include asking:

• about the local entity’s application of group-level DEI policies or strategies;

• about DEI strategies as an indicator of an insurer’s culture in this matter;

• senior leaders how DEI requirements are implemented;

• about aspects of diversity and inclusion in governance reviews related to Board effectiveness;

and

• about DEI matters in ad hoc conversations around senior appointments.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Figure 3: Supervisory activities to promote DEI

Yes Future yes

PUBLIC

Information collection and public disclosures are also amongst the more frequently reported actions.

Of those who reported these activities, many collect information on DEI and release aggregated

statistics for industry benchmarking. Some regulators also require insurers to publish information on

the diversity and composition of their Board.

Several supervisors mentioned the importance of collecting data on DEI, focusing on several key

aspects.

6

Firstly, it is important to establish whether insurers collect any DEI data, and the methods

and manner in which this is collected and analysed. Types of data collected are usually with regard

to demographic characteristics, often with a focus on gender.

The diversity data that insurers collect should also be considered in light of any specific DEI data

collection strategy and action plan that the firm may have in place. Where these things exist, some

supervisors thought it necessary to look at how this strategy is implemented as well as how the data

is tracked, monitored and assessed.

Below is a selection of current supervisory actions to promote DEI in the insurance industry:

Ireland

In 2020, the Central Bank of Ireland published a Thematic assessment of Diversity & Inclusion in

insurance firms.

The objective was to assess the adequacy and maturity of the approach to

diversity and inclusion within a sample of insurance firms.

It found that all of the firms had

commenced initiatives to improve diversity and inclusion but work was focused primarily on

diversity, with all firms at an immature phase in their approach to inclusion. It found that the majority

of firms have a significant way to go in ensuring their organisations are sufficiently diverse and

inclusive.

In addition to the thematic assessment report, the Central Bank of Ireland issued a risk mitigation

programme to each of the eleven firms, requiring them to submit a detailed action plan to address

the firm-specific issues they identified, and to ensure these issues are appropriately resolved.

Furthermore, as part of their commitment to monitor and report on the level of diversity in the

sector,

7

each year the Central Bank of Ireland reports on the demographics of the applications

received for pre-approval of certain senior roles in financial firms in Ireland. This report provides

data on gender statistics by reference to the regulated industry sector, role type, age and

nationality. This analysis helps to monitor relevant activity each year as well as progress and

trends over time.

Over the years, the Central Bank of Ireland has spoken publicly on the topic of DEI. Some of the

more recent speeches include:

• Citizenship, participation and diversity - Deputy Governor Sharon Donnery; and

• Culture, diversity and the way forward - Deputy Governor Ed Sibley.

The Central Bank of Ireland is also introducing a supervisory practice to ask questions about

diversity and inclusion during meetings with financial firms (including insurers), and is developing

question banks to assist supervisors to effectively do this.

6

In some jurisidctions, collecting data on some characteristics is prohibited for both supervisors and insurers under national

legislation. In some cases these prohibtions are intended to prevent discrimination and arise from specific historical backgrounds.

7

‘Diversity and Inclusion in Regulated Firms’.

PUBLIC

Italy

The Istituto Per La Vigilanza Sulle Assicurazioni (IVASS – the I

talian institute for insurance

supervision) published a working paper in January 2022: “Women, board and insurance

companies”. It concluded that “it is pivotal that regulators and supervisors […] take a proactive

role in supporting diversity and inclusion in the insurance sector through measures such as the

introduction of mandatory thresholds of women’s representation and the publication of benchmark

analyses”.

Malaysia

The Bank Negara Malaysia monitors insurer culture, governance structure (e.g. diversity in Board

composition) and conduct risk (especially conduct that could compromise the fair treatment of

consumers). In a 2017 report, ’Better Boards – The Path Towards Stronger Corporate Governance

in Financial Institutions’, they noted how diversity in skills and background can enhance Boards’

ability to meet the challenges inherent in uncertain and complex economic environments.

Singapore

The Monetary Authority of Singapore’s ‘Guidelines on Corporate Governance’ expect financial

institutions (including insurers) to disclose their Board diversity policies

and progress made

towards implementing these, including objectives.

United Kingdom

There has been a high degree of regulatory engagement by the Bank of England, the Prudential

Regulation Authority (PRA) and the Financial Conduct Authority (FCA) over the years with the

financial sector on the importance of diversity and inclusion. Some of the more recent speeches

include:

• in November 2022, Sheldon Mills (Executive Director of Consumers and Competition, FCA)

spoke at the Assocation of British Insurers Diversity Equity & Inclusion Conference on

“Diversity and inclusion: Driving change in our industry”; and

• in April 2021, Andrew Bailey (Governor of the Bank of England) spoke at the launch of the

“Meeting Varied People” initiative, on how it is important for the Bank to engage with a more

diverse range of people and institutions within the financial sector in order to better understand

global financial markets and their impact on the economy, to inform the Bank’s decision-

making in areas such as setting interest rates and designing market operations.

United States of America

In 2020, the National Association of Insurance Commissioners’ (NAIC)

Executive Committee

established a special committee to address issues of race and insurance.

The Special (EX)

Committee on Race and Insurance demonstrates the U.S. state regulators’ commitment to work

together to find a holistic approach to address racial disparities and promote

diversity in the

insurance industry. Workstream 1 of the Special Committee was charged with researching and

analysing the level of diversity and inclusion in the insurance sector and determining what barriers

exist in the industry that potentially disadvantage people of colou

r and historically

underrepresented groups. The workstream worked with NAIC technica

l staff to research and

summarise existing publicly available data, articles and studies, and also reached out to consumer

PUBLIC

advocates and industry representatives requesting relevant data and information. The

Workstream also highlighted the 2019 labor force statistics from the U.S. Bureau of Labor

Statistics.

Diversity requirements have been introduced for companies (including insurers) in a number of

jurisdictions, for example to require a particular number of women in leadership positions or to

impose reporting obligations such as on diversity policies and progress against diversity targets.

These requirements have generally been set with the intention of building companies with more

diverse boards, which are seen to be important for good corporate governance and decision-making.

As these initiatives are not targeted specifically at insurers or other financial institutions, they are not

discussed in more detail in this report.

Some jurisdictions are developing new legally enforceable rules directed specifically at the insurance

industry, or the broader financial services industry:

California (USA)

The California Department of Insurance has sponsored legislation to codify insurance diversity

reporting requirements in statute, including expanded reporting requirements on Board diversity.

Their Insurance Diversity Initiative aims to advance the diversity of suppliers and governing

Boards in the insurance industry.

Chinese Taipei

The Financial Supervisory Commission Republic of China (Taiwan) has stated that in 2022 they

plan to revise Regulations Governing Public Disclosure of Information by Non-

life Insurance

Enterprises

and Regulations Governing Public Disclosure of Information by Life Insurance

Enterprises. This includes adding provisions to “require an insurer to adopt a diversity policy of

board of directors’ members and to describe the company’s diversity policy in its publicly filed

statements and the state of that policy’s implementation”.

European Union

In April 2022, the European Insurance and Occupational Pensions Authority (EIOPA) wrote to the

European Parliament, the Council of the EU and the European Commission advocating for the

introduction of provisions promoting diversity in the governance of insurers as well as gender-

neutral remuneration policy and practices.

Separately, from January 2023 financial market participant companies (including insurers) of more

than 500 employees will have to report on the ratio of female to male Board members and the

unadjusted gender pay gap of the companies they invest in.

8

Italy

The Ministry of Economic Development has issued the Ministerial Decree n. 88/2022 on fit and

proper requirements of the corporate officers and persons who carry out key functions in insurers

or reinsurers. It includes a provision requiring a mandatory quota for the underrepresented gender

in the administrative and control bodies.

8

Commission Delegated Regulation (EU) 2022/1288

PUBLIC

South Africa

In South Africa, the Conduct of Financial Institutions (COFI) Bill is under development. The aim of

the COFI Bill is to consolidate the conduct requirements of financial institutions (FIs) housed in

various pieces of legislation into one statute, while also strengthening the Financial Sector

Conduct Authority’s (FSCA)’s role in implementing the changes laid down in law. DEI is addressed

in various parts of the COFI Bill. It includes principles relating to culture and governance for

financial institutions, which stipulates that financial institutions (including insurers) must conduct

their business in accordance with the objectives of financial inclusion and promoting, in particular,

racial equality through compliance with the requirements of the Broad-

Based Black Economic

Empowerment Act, 2003 (in local terms referred to as “transformation of the financial sector”).

The FSCA and the Prudential Authority are also developing a Joint Standard setting governance

requirements for financial institutions, which includes principles related to embedding DEI.

Future activities planned or under consideration by supervisors include:

United Kingdom

In July 2021, the PRA, FCA, and the Bank of England published a discussion paper “Diversity and

Inclusion in the financial sector – Working together to drive change” (DP21/2), which outlined how

improving diversity and inclusion in regulated firms can help them achieve their regulatory and

business objectives. It put forward a number of ideas on how this can be achieved, with a focus

on embedding diversity and inclusion into firms’ governance frameworks, and invited industry

responses.

Key considerations from DP21/2 include:

• Leadership and culture: Leaders need to set a compelling strategy and empower their teams

to develop and implement initiatives that deliver cultural change at all levels within their

institutions. Boards should monitor and challenge progress on diversity and inclusion.

• Remuneration: Linking progress on diversity and inclusion to remuneration could be a key tool

for driving accountability in firms and incentivising progress.

• Firm-wide policies and practices: Diversity and inclusion policy should b

e a central

consideration for all firms, as it forms the foundation of a strategy and action plan. Clearly

documented policies help set out the expectations to staff of the meaning of diversity and

inclusion and their respective roles.

• Reporting and discl

osure: Good data can help firms understand the current state of play,

monitor progress, identify potential barriers to progress on diversity and inclusion, and select

the most effective interventions. The regulators are considering implementating reporting

requirements in order to help them assess individual firms’ progress as well as observe trends

and benchmark progress across the industry. They are also considering requiring firms to

publicly disclose information on their diversity data and strategy, as disclosure sets a clear

statement of intent and creates transparency for stakeholders.

• Conduct: Regulators are exploring whether adverse findings in relation to individuals’ conduct

with regard to diversity and inclusion issues could affect their assessmen

t of fitness and

propriety in the future.

Following DP21/2, the PRA and FCA plan to publish parallel consultation papers on diversity and

inclusion in the financial sector, including for insurance firms, in the near future. These will be

based on the responses received to the discussion paper, and would propose

rules and

expectations aimed at improving diversity and inclusion across the industry.

PUBLIC

Overall, IAIS research shows that many insurance supervisors across different international

jurisdictions consider DEI to be relevant to insurers’ governance, and are either taking, or planning

to take, specific actions in this area. The IAIS will continue to monitor developments in this area,

taking note of further innovative ideas and examples of good practice.

2.3.2 Market conduct focus

The IAIS considers that DEI built into the way an insurer conducts its business can lead to better

consumer outcomes.

9

The survey asked IAIS members with responsibility for conduct of business

supervision (per ICP 19) about the extent to which they are promoting DEI considerations in the way

insurers conduct their businesses.

Approximately 63% of respondents reported conveying, to at least some extent, supervisory

expectations that insurers conduct their business in promotion of customer DEI. A further 16% said

that they do this to a great extent. Supervisors addressing DEI in a customer-facing sense have

focused their expectations on product suitability, vulnerable groups, and customers with disabilities.

Some have also focused on equity, prohibiting discriminatory business conduct, design, pricing, and

coverage.

Most supervisors report having high-level laws, regulations, and/or guidelines that prohibit

discriminatory insurance practices that affect customers, and most consider that DEI principles can

be addressed under fair treatment of customers and/or wider conduct of business standards and

principles. Responses indicated that supervisors do not necessarily need to adopt DEI in conduct

supervision through a new framework or set of rules, but rather could address this through making

adjustments to the use of existing frameworks.

The survey also asked whether supervisors had done any work to analyse, or had encountered

supervisory examples of, a correlation between the state of DEI at an insurer (ie in an

internal/institutional sense) and the insurer’s conduct-related outcomes. The majority answered no.

Activities by supervisors to ensure insurers are delivering good consumer outcomes among diverse

consumer populations include:

9

See section 1 for more explanation of the IAIS’ view that DEI considerations in the way insurers operate their businesses will

lead to better consumer outcomes.

Australia

The Australian Securities and Investments Commission (ASIC) administers legislation in relation

to Design and Distribution Obligations which require product issuers, including insurers, to

consider the objectives, financial situation, and needs of customers in determining their target

markets. ASIC Regulatory Guide 274 Product design and distribution obligations explains that,

when considering the design of a financial product and how it will reach consumers in the target

market, in order to have a consumer-centric approach product issuers should consider consumer

vulnerabilities. Consumer vulnerabilities may include personal or social characteristics that can

affect a person’s ability to manage financial interactions such as, speaking a language other than

English, having different cultural assumptions or attitudes about money, or experiencing cognitive

or behavioural impairments due to intellectual disability, mental illness, chronic health problems or

age.

PUBLIC

10

Practice of increasing premiums at the renewal stage based on the analysis of characteristics specific to a particular

consumer to predict behaviours not related to risk or cost of services, such as how much of a premium increase an individual

consumer will tolerate before shopping for coverage with other product manufacturers.

ASIC has also secured remediation for consumers exposed to poor life insurance sales practices,

including consumers residing in high indigenous populated areas,

who were unlikely to have

English as their first language.

Chinese Taipei

The Financial Supervisory Commission Republic of China (Taiwan) has established “Financial

Inclusion Indicators” to evaluate the accessibility, usability and quality of financial services (not

only insurance) in their jurisdiction, with a view to encouraging financial institutions to adjust their

service strategies. One stated goal of the Financial Inclusion Indicators is encouraging financial

institutions to introduce financial products or services that meet the needs of all sectors of society.

European Union

Th

e European Union implemented new Product Oversight and Governance requirements in

October 2018. They require insurance product manufacturers to design and market insurance

products that are compatible with the needs, objectives and characteristics of their customers –

including aspects like gender, age and vulnerability. They also require that the staff designing

products have the necessary skills, knowledge and expertise to understand these needs,

objectives and characteristics.

Given evidence of price walking practices,

10

in July 2022 the EIOPA issued a Supervisory

Statement for public consultation, which aims at strengthening consumer protection by preventing

the unfair treatment of consumers and to promote greater convergence in the supervision of

differential pricing practices, to ensure that detriments to consumers are prevented via adequate

Product Oversight and Governance processes. This followed EIOPA’s thematic review of Big Data

Analytics, which found evidence of these practices, and the issuance of a report on Artificial

Intelligence Principles which aimed to ensure ethical and trustworthy usage of Artificial Intelligence

in the European insurance sector.

Germany

German supervisors have analysed age discrimination in auto (motor vehicle) insurance

provisions, but did not find any indications of ageism.

Italy

IVASS has published a working paper on “Governance of Artificial Intelligence in the insurance

sector between ethical principles, board responsibility and business culture”, which considers how

to use artificial intelligence to help design more inclusive insurance products and protect consumer

interests.

Malaysia

PUBLIC

With regards to future opportunities, some supervisors noted that an area of development is to

connect conduct issues with some clear DEI principles. Accessibility and underserved segments of

consumers are indicated as two focus areas by some authorities. About one third of the respondents

are considering how other requirements interact with the insurer conducting its business in

Malaysian supervisors have noted the risks of financial exclusion for some customer segments

due to age, socioeconomic disparities, or financial literacy gaps. They consider how to ensure the

insurance industry delivers products to meet the needs of lower income consumers, to avoid

deepening existing disparities and contribute to social resilience.

A policy document on

“Perlindungan Tenang” (a microinsurance scheme) has been issued on 2 July 2021 to clarify Bank

Negara Malaysia’s expectations in this regard.

Netherlands

Growing diversity in the population of the Netherlands as a result of the proportion of Dutch

nationals with a migration background

prompted the Dutch Authority of the Financial Markets

(AFM) to conduct an exploratory study of the financial vulnerability

of Dutch nationals with a

migration background and their relationship with financial services. The AFM hopes to increase

awareness and contribute to the public debate on this issue. The study (published in December

2021) found that Dutch nationals with a migration background, particularly a non-Western

background, are on average more financially vulnerable and, with respect to insurance, there are

factors (including language barrier, complexity of insurance and limited familiarity with the concept

of insurance) that could lead to them being either over-insured or under-insured.

Québec, Canada

The Autorité des marchés financiers (AMF) carried out a cross-sectoral monitoring exercise after

being alerted to potential discriminatory behaviour in First Nations Communities’ access to auto

and home insurance. It stated that, “the insurers covered by the cross-sectoral monitoring exercise

will receive customised recommendations through a private monitoring report. A public

communication of AMF’s findings could probably follow”.

United States of America

Workstreams 3, 4 and 5 of the NAIC’s Special (EX) Committee on Race and Insurance are focused

on identifying issues related to race, diversity and inclusion in access to the insurance sector and

insurance products. Each of the workstreams allows for U.S. state insurance supervisors to

individually highlight one of the three lines of busine

ss: Property & Casualty Insurance, Life

Insurance & Annuities, and Health Insurance. These workstreams are a forum for understanding

practices within the insurance sector that potentially disadvantage people of colou

r and/or

historically underrepresented groups. One specific market conduct-related example is a focus on

the marketing, distribution and access to life insurance products in minority communities, including

the role that financial literacy plays. Another is an examination of the use of network adequacy

and provider directory measures (eg provider diversity, language and cultural competence) to

promote equitable access to culturally competent care. U.S. state insurance supervisors have

given themselves solution-oriented tasks and goals to address a

nd fix insurance access and

affordability concerns that may exist in the marketplace.

PUBLIC

accordance with DEI considerations, such as defining a target market for insurance products, the

freedom of contract, and a premium price reflecting the risk assessment.

As with governance, the IAIS will continue to seek out examples of supervisors’ work in the area of

DEI and market conduct, and facilitate further conversation among stakeholders.

Insurance industry action on DEI

As observed by insurance supervisors

The survey asked whether supervisors had conducted any analysis of the state of DEI within the

insurance industry and what trends they had observed. The survey then asked supervisors what

they consider is driving any industry action taking place, and what they believe will drive further

industry action. A third of the supervisors have conducted analysis of the state of DEI within insurers

in their jurisdiction, and a few have not done so yet, but plan to.

Various supervisors reported a clear sense that the increase in the number of insurers pursuing

greater internal DEI is gaining momentum. Supervisors reported observing insurers taking a number

of actions, both voluntarily and due to government initiatives or regulatory requirements:

• incorporating DEI considerations into their corporate governance framework;

• making disclosures on Board composition;

• looking at their human resources processes in order to recruit from a more diverse talent pool;

• considering barriers to entry into the industry, and how to mitigate these, such as by introducing

sponsorship and scholarship schemes; and

• focusing on ways to promote women into management positions.

Overarching observations from supervisors about the industry’s DEI action include:

• Industry initiatives most commonly relate either to financial inclusion/access to insurance, or to

the pursuit of more diversity in the people working in the insurance industry.

• There is more concentration on increasing diverse representation than on equity or inclusion.

• While insurers are increasingly implementing DEI initiatives, they are not as often tracking,

monitoring or assessing the effectiveness of those initiatives.

• Gender diversity is the most frequent focus of industry’s diversity effort. However, the diversity

focus can vary from one jurisdiction to another and supervisors noted some level of focus on

ethnicity/race, sexual orientation, military veterans, persons with disabilities and socio-economic

diversity.

• Initiatives related to increasing diversity in the composition of insurer Boards and senior

management are quite prevalent. Some respondents observed that in many cases, women are

still underrepresented in those cohorts, and some also found gender pay gaps. Respondents

also considered that Board compositions do not always adequately match the demographic

distribution of the local jurisdiction in terms of representation of ethnic backgrounds.

• Internationally active insurers are more likely than other insurers to have DEI aspects

incorporated into their organisation and approach to doing business.

PUBLIC

• Insurers are typically not as far along in their efforts to embed DEI into their approach to

customers, compared to their efforts to improve their internal DEI.

• Industry sometimes considers their investment activity as part of their DEI action, for instance by

setting up initiatives to expand their investment in underserved and underprivileged communities.

Insurance supervisors observe action on DEI being undertaken not only by individual insurers, but

also by industry associations at various levels including at global, regional, and national levels.

Supervisors consider that a variety of factors combine to drive industry action in order to increase

internal/institutional DEI, the more significant of which are:

• mandatory requirements;

• industry’s belief that DEI is good for their business and for their reputation, including from the

perspective of employee attraction and retention; and

• societal shifts that have created an expectation or pressure from key stakeholders and therefore

the need to commit time and resources to it.

Respondents also observed that, in many cases, action to increase DEI within the composition of

insurers’ workforce and leadership is part of a broader transition occurring across the financial sector

in general, and across the wider corporate/business world, rather than being insurance sector-

specific.

Supervisors gave varied responses regarding what they consider would bring about more industry

action on DEI, but agreement did coalesce around the point that a combination of different factors

would have the greatest success. The following actions are considered by supervisors as most likely

to lead to further industry action to improve insurers’ internal DEI:

• Formal requirements were mentioned often as a powerful catalyst for industry action. Some

supervisors proposed that requirements could be helpfully supplemented by regulatory

recommendations and guidelines laying out non-binding expectations.

• Supervisors nudging and encouraging the industry, by promoting DEI initiatives, e.g. by showing

and promoting best practice examples and informing the industry about not only the benefits and

advantages of improving DEI, but also about the dangers and consequences of ignoring it.

• Opportunities for the exchange of ideas and views between industry, supervisors and other

stakeholders.

• Education and promotion of DEI in society in general. This will then translate into more action on

DEI in the insurance sector specifically.

Overall, through the eyes of insurance supervisors, there is a clear picture that the insurance industry

is increasingly interested in how DEI may be relevant to their organisations. This is inspired by

various factors, some of which involve supervisory actions, while others are due to wider trends in

local jurisdictions and internationally. This research suggests that it may be useful for insurers and

their supervisors to continue to have an open dialogue, sharing their ideas and experiences on how

to develop industry and regulatory approaches to DEI.

As explained by the industry through stakeholder engagement

As an input to the stocktake, the IAIS undertook engagement with a sample of external stakeholders

to help in an initial, exploratory way:

PUBLIC

• understand if and why, from the industry’s perspective, DEI is considered relevant and important

to both governance and to conduct of business in the insurance sector;

• learn about DEI action being taken by industry and other relevant stakeholders;

• understand what the industry sees as the biggest challenges or obstacles in embedding DEI;

and

• receive views on what the global supervisory community can do to further promote DEI in the

insurance sector.

The sample of stakeholders included insurers, industry bodies and a consultant, representing

jurisdictions spanning Global, Asia Pacific, Middle East & Africa, South Africa, Switzerland, UK, and

USA. The IAIS looks forward to continuing to discuss DEI with other interested stakeholders.

The following key insights have emerged to date:

3.2.1 Why DEI is relevant and important to insurers

Industry stakeholders support the role DEI plays both from an internal/institutional perspective and

an external, customer-serving perspective. They characterised DEI as a rapidly evolving area where

the conversation keeps expanding.

Industry stakeholders expressed the view that embedding DEI in governance across an organisation

is a predictor of organisational success. Industry stakeholders believed the following benefits can

arise from embedding DEI within an insurer:

• Better business performance. Linked to this was recognition that insurers face many new

challenges and hence new, diverse skillsets are needed for success.

• Risk reduction by creating diversity of thought, which means there is less chance of groupthink

and likely overall better risk management.

• A more representative/diverse workforce can support better understanding of the diverse needs

of consumers, therefore allowing insurers to deliver a better service to customers and to design

the right products for customers needs. Some stakeholders did note that data to provide evidence

of this is limited and imperfect, which hampers insurers’ ability to easily assess how they are

serving diverse populations.

• There may be an immediate benefit in insurers’ ability to attract more talent. In the longer term,

having more diverse staff may organically grow DEI within the insurer, which could then naturally

embed DEI into the culture and continue to attract talented and diverse staff.

• The psychological advantage of an inclusive culture results in happier employees, which can

lead to benefits for employee retention and productivity.

Some stakeholders described seeing the merits of DEI in relation to conduct of business as linked

to the fundamentals of having a successful business: DEI better positions an insurer to understand

the market it is in, to meet the needs of that market and to do it in an innovative, competitive and

solvent way.

Stakeholders generally recognised that DEI from a conduct/consumer perspective is not as well

developed in its thinking, and that there is an opportunity to explore it more. Stakeholders noted that

market conduct is heavily influenced by the respective supervisory or cultural background. This could

be a reason why a variety of drivers as well as a variety of actions exist. Additionally, regulatory

regimes differ in their conceptualisation of DEI, as well as their approach to the concept of fair

treatment, discrimination, and unfair practices.

PUBLIC

3.2.2 The challenges faced in embedding DEI

Some industry stakeholders thought that the voluntary nature of DEI makes it challenging to

crystallise sufficient action across the sector. They described that there are many discussions around

DEI, but if there is no follow-up action, not much will change. Relatedly, the challenge of inertia was

cited: people may be likely to follow engrained behaviour and be unwilling to embrace change, most

DEI initiatives are fuelled by a small number of advocates, and there is a need to have a larger

collaborative movement to create change.

In response to these challenges, stakeholders pointed to the need for action and formal structures

to promote DEI, and also the view that supervisors have a key role to play in raising awareness and

evaluating if insurers are ethically embedding DEI in their businesses in a sustainable manner.

A lack of diversity in the talent pool is another key challenge to creating a diverse and representative

workforce. Given the action being taken by some insurers, stakeholders expressed hope that this

will get better over time, but recognised that continued action is needed. In jurisdictions with diverse

cultural and demographic populations, developing appropriate products for different consumers is a

DEI challenge that insurers need to deal with together, considering how to best make insurance

accessible to diverse consumers.

It was also noted that industry associations trying to drive regional or global action on DEI need to

have sensitivity and awareness of cultural and legal differences across jurisdictions.

3.2.3 The role for supervisors

Industry stakeholders believed that the IAIS making DEI a priority is helpful for motivating change.

Likewise, several stakeholders said that advocacy for DEI by the local supervisor was a powerful

driver of industry action.

As a general message, industry stakeholders recommended that supervisors should crystallise their

position regarding the necessary principles and values around DEI and send a clear message to

insurers and the industry at large. Some thought it may also be beneficial to communicate

supervisory expectations such as expectations around insurers having an accountability regime that

supports DEI.

Some stakeholders felt that supervisors should avoid overregulation, being too prescriptive or

directive, and creating unnecessary burdens. They instead expressed the view that the regulatory

landscape must be agile. They thought supervisors should raise awareness at a principled level, for

example, through the publication of best practice papers and case studies. Some cautioned that

supervisors should avoid introducing initiatives (eg setting quotas) that may actually cap ambitions

to progress DEI. Some stakeholders also expressed that supervisors need to recognise the

differences between large, medium and small insurers and cautioned against expecting a ‘one size

fits all’ approach to DEI.

With respect to DEI in a conduct of business consumer-facing sense, industry stakeholders

acknowledged that it can be addressed through fair treatment of consumers, but suggested that

discussions were required with supervisors about how to provide a DEI lens to the fair treatment of

customers that would not be prescriptive and therefore difficult to implement and supervise, given

differences in markets and products.

PUBLIC

The international-level landscape and how IAIS activity fits

Across key international organisations

The stocktake included examining whether DEI features in the current and planned work of

international bodies with mandates linked to the international financial system. Assessing the degree

of attention on DEI as a supervisory topic at the international level assists the IAIS in understanding

the current landscape, and in turn, the contribution it can make on this topic.

4.1.1 Overview

There is a growing recognition of the benefits of DEI to good governance, and hence a growing

promotion of more DEI within financial institutions, by international organisations. However, it is not

as dominant on their work programmes as other topics, nor is it currently the subject of many official

publications. Instead, work linked to the umbrella term ‘Environmental, Social and Governance’ (or

ESG) remains more often focused on the E (for environment), with much of this work linked to climate

change. There is some registered recognition of the increasing prominence of DEI as an issue under

the ESG umbrella.

11

Plenty of work directed at both financial inclusion and consumer protection is being advanced by

international organisations. These are well established areas of work that have been on the agenda

since before DEI came to prominence. Notwithstanding this, both financial inclusion and consumer

protection can be regarded as promoting DEI, given they focus on the inclusion of typically

underserved segments of the population, and they seek to ensure fair treatment and suitable

products and processes for all consumers, especially those who are vulnerable. An area for ongoing

consideration is how a DEI focus integrates with, or necessitates something additional to, existing

bodies of work directed at financial inclusion and consumer protection.

4.1.2 Commitments to their own DEI

Many international organisations have published DEI statements on their internal commitment to DEI

as employers.

12

In some cases, the statements particularly recognise the link between the

organisation itself being more diverse and inclusive, and the enhanced suitability of its output and

policies.

While adopting DEI statements of this kind is not the same as progressing DEI-focused work as part

of the execution of their mandates, it does constitute leading by example. It may also be indicative

of growing recognition of the importance of DEI at that organisation, which may in time lead it to its

incorporation in the organisation’s external-facing work.

4.1.3 Recognition of the link between DEI and good governance and risk management

Across the published material of international organisations, there are some references made to the

advantages resulting from DEI within a financial institution. Where they exist, the references draw

11

For instance, in Report on Sustainability-related Issuer Disclosures (June 2021) IOSCO (International Organization of Securities