SAF/No.13/February 2017

Studies in Applied Finance

INVESTMENT THESIS FOR

CHIPOTLE MEXICAN

GRILL, INC. (NYSE: CMG)

Alexander Mabie

Johns Hopkins Institute for Applied Economics,

Global Health, and the Study of Business Enterprise

!

!

Investment Thesis for Chipotle Mexican Grill Inc. (NYSE:CMG) by Alexander Mabie

Investment Thesis for Chipotle Mexican Grill, Inc. (NYSE:CMG)

By Alexander Mabie

Disclaimer: These research reports are primarily student reports for academic purposes and are

not specific recommendations to buy or sell a stock. Potential investors should consult a

qualified investment advisor before making any investment.

About the Series

The Studies in Applied Finance series is under the general direction of Professor Steve H.

Hanke, Co-Director of the Johns Hopkins Institute for Applied Economics, Global Health, and

Study of Business Enterprise ([email protected]) and Dr. Hesam Motlagh ([email protected]), a

Fellow at the Johns Hopkins Institute for Applied Economics, Global Health, and Study of

Business Enterprise.

This working paper is one in a series on applied financial economics, which focuses on company

valuations. The authors are mainly students at the Johns Hopkins University in Baltimore who

have conducted their work at the Institute as undergraduate researchers.

About the Author

Alexander Mabie is an incoming long-only equity analyst at Goldman Sachs Asset Management

in New York. He conducted the research for this paper while serving as Prof. Hanke’s research

assistant at the Institute for Applied Economics, Global Health, and Student of Business

Enterprise during the fall of 2016. Alex will graduate in May of 2018 with a B.A. in Economics

and a minor in Financial Economics and Entrepreneurship & Management.

Summary

This working paper is an in-depth analysis of Chipotle Mexican Grill Inc. The analysis examines

the economic factors that impact Chipotle’s underlying business fundamentals. This analysis is

then combined with a proprietary Discounted Cash Flow (P-DCF) model to determine Chipotle’s

financial position. The model will be presented along-side Monte-Carlo simulations to reveal the

distribution of probable free cash flows and the potential for future earnings. In addition to these

quantitative factors, we I assess the alignment of Chipotle’s executives with shareholders based

on the company’s proxy report. At the conclusion of this analysis, I aim to clearly convey

Chipotle’s business strategy and the company’s financial standing to arrive at a sound investment

decision.

Acknowledgements

Many thanks to Prof. Steve H. Hanke, Dr. Hesam Motlagh, and Abigail Biesman for guidance

and draft comments.

Investment Thesis for Chipotle Mexican Grill Inc. (NYSE:CMG) by Alexander Mabie

Investment Thesis for Chipotle Mexican Grill, Inc. (NYSE:CMG) by Alexander Mabie

Rating: Sell – Average Free Cash Flow per Share: $264.80

Company Profile

($ in MMs except per share data)

!

!

Company Name Chipotle Mexican Grill

Date 12/19/16

Fiscal year ends (current period) 12/31/2016 (3Q)

Current Price $ 392.07

52 week high (date) $ 544.88

52 week low (date) $ 352.96

Market Cap $ 11,350.10

Enterprise Value $ 10,990.95

Total Debt $ -

Cash $ 359.15

Net Debt/Enterprise Value -3.27%

Dividend N/A

Shares Outstanding/Float 28.9M/28.5M

Current P/E 130.80

2018 P/E (EPS) 30.87 (12.69)

2017 P/E (EPS) 42.90 (9.13)

2016 P/E (EPS) 256.93 (1.53)

2015 EPS $ 14.75

2014 EPS $ 14.08

2013 EPS $ 10.44

*Consensus Estimates as of 12/19/16

!

!

Investment Thesis for Chipotle Mexican Grill Inc. (NYSE:CMG) by Alexander Mabie

Table of Contents

Executive Summary.......................................................................................................................4

Company Background and Recent Developments .....................................................................4

Catalysts and Risks........................................................................................................................7

Historical Performance .................................................................................................................7

Model Assumptions .......................................................................................................................9

Model Results...............................................................................................................................11

Qualitative and Other Analyses .................................................................................................12

Conclusion ....................................................................................................................................19

!

!

!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!

! !

Investment Thesis for Chipotle Mexican Grill Inc. (NYSE:CMG) by Alexander Mabie

Executive Summary

Chipotle Mexican Grill, Inc. (NYSE:CMG) operates fast-casual Mexican food

restaurants. By analyzing historical averages, forward guidance from management, and the

macro environment, our Proprietary Discounted Cash Flow (P-DCF) model estimates that

Chipotle’s probable free cash flow per share is $264.80; i.e. a significant discount compared to

the current market price of $392.07. This result was obtained using bullish near-term revenue

growth estimates in the face of Chipotle’s public relations fiasco pertaining to food safety. Given

my sell recommendation, applying optimistic assumptions in the P-DCF will result in a more

conservative model output. I took a relatively bullish stance with regard to future revenue growth

rates to illustrate the degree to which the market the company must grow in order to justify

today’s valuation.

Reiterating this theme of bullishness, I hold the absolute margins on the majority of

Chipotle’s expense line items constant over the ten-year model forecast period. I use this

approach despite minimal signs of historical operating leverage and the high likelihood of lofty

requirements for marketing expenses and other promotional activities to improve public

relations. In particular, food, beverage and packaging expenses are given a negative 10 basis

point annual step even though Chipotle is rolling out new menu items that could potentially

increase the firm’s food costs. In light of a very expensive valuation, weak management with

decent compensation policies, secular trends affecting the company’s popularity, and recent

incidents tarnishing the Chiptole brand, I assign a sell rating.

Company Background and Recent Developments

Chipotle is a fast-casual Mexican food restaurant operator, with a focus on burritos, tacos,

burrito bowls, and salads. The company was founded in 1993 and is based in Denver, Colorado.

As of September 30, 2016 the company operated 2,129 Chipotle restaurants in the United States,

none of which the company franchises. The company also oversees 15 restaurants in Canada, six

in England, five in France, and one in Germany. Furthermore, Chipotle operated 15 ShopHouse

Southeast Asia Kitchen (“ShopHouse”) restaurants, which serve fast-casual Asian cuisine (the

company has since shut down this business after the concept did not catch on). Chipotle has also

invested in a consolidated entity that owns and operates seven Pizzeria Locale locations, a fast

casual pizza restaurant. Chipotle manages its operations based on nine regions and aggregates

them to one reportable segment

1

.

Chipotle’s popularity exploded between the start of 2012 through 2015 as health and

wallet-conscious consumers nationwide embraced the company’s commitment to “food with

integrity.” Chipotle’s mission has been to use high quality ingredients grown with respect for the

environment, animals, and the people who grow or raise this food. Initially, this business method

effectively distinguished them from competitors that have applied a more formulaic and less

nutritious approach to fast food (read: McDonald’s)

2

.

However, significant food safety incidents in 2015 impacted hundreds of customers

around the country and had direct effects on Chipotle’s performance and brand. From July to

December, various outbreaks of E. coli, norovirus, and Salmonella occurred in Washington,

1

https://www.sec.gov/Archives/edgar/data/1058090/000105809016000058/cmg-20151231x10k.htm#Item_1

2

https://www.sec.gov/Archives/edgar/data/1058090/000105809016000058/cmg-20151231x10k.htm

Investment Thesis for Chipotle Mexican Grill Inc. (NYSE:CMG) by Alexander Mabie!

!

Oregon, California, Minnesota, Oklahoma, Kansas, and Massachusetts

3

. In response, Chipotle

closed all of its restaurants on February 8, 2016 for an all-staff meeting on food safety. Company

founder and co-CEO Steve Ells affirmed the company’s commitment to food safety. The

consumer and market reactions to the various incidents, however, were not mild. Shares of

Chipotle stock, which peaked in August 2015 at $758, now hover around $400. Comparable

restaurant sales declined 24.9% in the nine months ended September 30, 2016

4

. This dramatic

decline reflects increasingly negative perceptions of the Chipotle brand and the safety and

quality of its food.

In an effort to increase sales and customer loyalty, management spearheaded several

promotional activities, such as Chiptopia Summer Rewards, which offered rewards that

incentivized customers to visit restaurants more frequently

5

. Third quarter results for FY 2016

illustrate that despite Chiptopia, the company could not lure back customers

6

. Chipotle has

engaged in three consecutive quarters of discounting and is now becoming more aggressive with

advertising, digital ordering, and new additions to its long-outdated menu. It is currently testing

TV ads, a method of marketing the company had previously avoided

7

. Additionally, management

recently introduced chorizo to the restaurant’s menu, an item that now accounts for roughly 7%

of entire sales. The team plans to continue adding items. Lastly, Chipotle is fleshing out a

mobile-friendly website that customers can use, as well as in-store tablet ordering. It remains to

be seen whether these initiatives will have a material impact on top-line and bottom-line

performance.

In addition to revamping the stores, per se, to increase profit, activist hedge fund investor

William Ackman of Pershing Square Capital Management disclosed a 9.9% stake in Chipotle

stock in September. Ackman is known for taking positions in underperforming companies and

advocating for change, often lobbying for a seat on the board of directors. Indeed, the Wall Street

Journal reported earlier in November that Ackman and Chipotle were nearing a settlement that

could give Ackman’s firm a voice in the boardroom, although there were not any specific details

about how many seats he might win

8

.

Shareholders who are long CMG stock may interpret Ackman’s stake in either a positive

or negative light. However, I choose the latter for three reasons. First, Ackman has already begun

to put pressure on the company to broaden its share repurchase program and to take on debt for

the first time, a questionable decision.

9

. Chipotle’s management has already misallocated capital

in spending free cash flow on buying back its overpriced stock. There is little merit to borrowing

to fund the repurchase of overvalued Chipotle shares. The company cannot afford interest

expense at this juncture and risks destroying long-term shareholder value if our valuation is

indeed correct.

Next, Chipotle has long been criticized for its clubby board. The company operates a co-

CEO structure and also combines the roles of chairman and CEO. Essentially, all nine board

members have ties (either through previous business ventures or personal matters) to co-CEO

and chairman Steve Ells. New board members with experience in marketing, crisis

!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!

3

https://web.archive.org/web/20151222031147/http://www.cdc.gov/ecoli/2015/O26-11-15/index.html

4

https://www.sec.gov/Archives/edgar/data/1058090/000105809016000088/cmg-20160930x10q.htm

5

https://www.sec.gov/Archives/edgar/data/1058090/000105809016000081/cmg-20160630x10q.htm

6

https://www.sec.gov/Archives/edgar/data/1058090/000105809016000088/cmg-20160930x10q.htm

7

http://www.wsj.com/articles/chipotle-provides-optimist-outlook-though-profit-plunges-95-1477429929

8

http://www.wsj.com/articles/chipotle-ackman-near-settlement-1479470401

9

http://seekingalpha.com/article/4024072-chipotle-mexican-grill-best-thing-happens-us-great-company-gets-

temporary-trouble

Investment Thesis for Chipotle Mexican Grill Inc. (NYSE:CMG) by Alexander Mabie!

!

communication, and technology will likely be key for the company to meet its troubles, and it is

easy to see Ackman rallying for such changes. However, at the same time, many investors on the

Street say a shakeup to the entrenched board has been a long time coming and probably does not

require Ackman. Furthermore, dismantling the co-CEO structure should also help (read: Whole

Foods).

Third, I fundamentally disagree with Ackman’s perspective on the company’s strategic

positioning and performance drivers. The following excerpts are taken from Pershing Square’s

3Q letter to investors

10

.

We have always believed that a good time to buy a great business is when it is in temporary

trouble. While Chipotle’s reputation has been bruised, we think that with the passage of time and

improved marketing, technology and governance initiatives, the business will not only recover but

become much stronger. Chipotle’s sales recovery will be neither smooth nor predictable over the next few

quarters; yet, we believe that all of the key drivers of Chipotle’s powerful economic moat and long-term

success remain intact. These drivers include:

1. A strong and relevant brand built by visionary leadership

2. A differentiated product offering with a highly attractive value proposition

3. Substantial scale in the fast casual industry and first-mover advantage in real estate

4. Strong unit economics and extremely high returns on capital, driven by a well-honed model that

facilitates best-in-class throughput

5. Enormous growth opportunities including new units and operating enhancements such as mobile

ordering and catering

… Today, we believe that Chipotle is one of the most compelling and authentic large-scale food brands in

the U.S.

The number one driver that Ackman cites pertains to Chipotle’s, “strong and relevant

brand.” In reality though, Chipotle’s brand is neither strong . The company’s brand reputation

has become extremely blemished, probably beyond repair. As Bloomberg News asserts, the

primary affliction for Chipotle is that the freshness of its food, which was centric to the success

of the brand, has become the company’s biggest weakness. Locally sourced food, free of

genetically modified organisms (GMOs), hormones, and antibiotics becomes much less

appealing if it causes sickness. Brand consultant, Allen Adamson, said that the food catastrophe

“strikes deeper at their brand because so much of their story is based on the quality of their

ingredients. This can clearly do long-term damage.

11

” A brief review of the company’s

operations through fiscal 2016 reveals this taking shape, and analysts at Raymond James suggest

that the sharp decline in sales “could prove to be more permanent in nature.

12

”. Not only have

customers lost trust in the quality and safety of Chipotle’s food, but they have also grown tired of

the chain’s stagnant and limited menu. Consumer preferences are a very important determinant

of performance in the restaurant space. Ackman might see “a differentiated product offering with

a highly attractive value proposition.” I see the opposite. Indeed, Deutsche Bank analysts cite a

!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!

10

http://www.valuewalk.com/2016/12/pershing-square-capital-management-3q16-letter/?all=1

11

https://www.bloomberg.com/news/articles/2015-12-08/chipotle-s-greatest-strength-is-now-its-greatest-weakness-

too

12

http://www.cnbc.com/2016/10/18/sell-chipotle-on-permanent-lost-sales-raymond-james-says.html

Investment Thesis for Chipotle Mexican Grill Inc. (NYSE:CMG) by Alexander Mabie!

!

lack of innovation, overall complacency, and the resulting “menu fatigue” as a contributing to

factor to lost sales

13

.

Catalysts and Risks

• TV advertising proves an effective method of advertising, reflected through increased

same-store sales trends.

• Menu expansion, such as the two dessert items currently in testing, garners revitalized

consumer interest in Chipotle stores.

• Improvements in digital selling facilitate a more convenient customer experience and

therefore increase restaurant traffic and sales.

• The presence of activist investor Bill Ackman whips corporate governance into shape.

• Ackman’s involvement could, however, disrupt the company’s restoration efforts and

cause more distress (read: Valeant, Target).

• In absence of amendments under Ackman, the clubby board and management resist

change.

• Another food safety incident occurs, further damaging Chipotle’s brand reputation.

• Softer-than-expected comparable restaurant sales for 4Q16, which management expects

to be in the negative single digits.

• Higher-than-expected food cost safety protocols and procedures resulting in margin

compression.

• The overall restaurant space continues to struggle given weak traffic due to food deflation

(cheaper groceries) and rising rent, and drags Chipotle sales down with it.

• A weakening consumer would hurt the company even if Chipotle can replenish its brand.

Historical Performance

Chipotle shareholders have experienced somewhat muted returns over the past five years,

with a cumulative average growth rate (CAGR) of 3.34% and a cumulative total return of

23.25%

14

. Most equity market participants would view these returns as disappointing. Figure 1

demonstrates Chipotle’s historical stock price versus the S&P 500 Index.

!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!

13

http://www.fool.com/investing/2016/05/30/is-menu-fatigue-chipotles-newest-problem.aspx

14

Bloomberg Terminal, Function <HP>

Investment Thesis for Chipotle Mexican Grill Inc. (NYSE:CMG) by Alexander Mabie!

!

Figure 1: Chipotle versus S&P 500 Five Year Historical Performance

Source: Bloomberg Terminal. Command <GP>. Accessed 12/18/2016

Of the 37 analysts covering the stock, 11 assign a buy rating, 18 have a hold rating, and 8

assign a sell rating. The average target price is $410.50, implying a 3.6% upside to the current

price

15

.

A Long Term Asset Turnover (LTAT; i.e. revenue divided by average long-term assets

per fiscal year) analysis of a company’s historical financial results can yield fruitful insights. The

chart in Figure 2 below plots Chipotle’s LTAT and Useful Life (UL; i.e. long-term assets divided

by depreciation and amortization expense) over a ten-year period (2005-2015). LTAT increased

to 2.73 in FY 2014 as the company grew its top line healthily. In fourth quarter 2015 the decline

in revenue that came along with the food-borne illness outbreaks was enough to slow overall

revenue growth and, by extension, reduce LTAT.

Through 2010, UL fell steadily as the increase in depreciation and amortization outpaced

that of long-term assets. In 2011, however, Chipotle began engaging in long-term investments.

This boosted overall-long term assets and reversed the trend. UL increased each year until FY

2015, when Chipotle opened fewer new locations than in previous years, which caused long-term

assets to decelerate.

!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!

15

Bloomberg Terminal, Function <ANR>

Investment Thesis for Chipotle Mexican Grill Inc. (NYSE:CMG) by Alexander Mabie!

!

Figure 2: Chipotle 10 Year Historical LTAT versus UL

Source: Company filings. Accessed 12/15/2016

10

11

12

13

14

15

16

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

1.5

1.7

1.9

2.1

2.3

2.5

2.7

2.9

Useful Life (Years)

LTAT

Chipotle 10 Year Long Term Asset Turnover Analysis

LTAT

Avg LTAT

Useful Life

Avg UL

Model Assumptions

The P-DCF model for Chipotle was built as discussed in course lectures. In a typical

“buy” stock pitch, conservative assumptions might mean projecting revenue at a growth rate

below its historical mean and contracting margins over the forecast period. Thus, in the case of a

short sale pitch, conservative model inputs are those that will put upward pressure on the

obtained model output.

Balance Sheet and Income Statement Trends

The results are contained in the ‘Balance Sheet’ and ‘Income Statement’ worksheets of the accompanying

Excel workbook.

On the balance sheet, the first notable line item fluctuation occurs with cash and cash

equivalents. I observe that the cash balance generally declines in periods that treasury stock

increases. Put simply, the company is buying back shares (it spent over $1B on repurchases from

mid 2015 to mid 2016

16

). A brief glance of the balance sheet also reveals a debt-free capital

structure. Upon inspection of the assets, it is clear that Chipotle exited a significant number of

positions in investments and short-term investments between the end of FY15 and the third

!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!

16

https://www.bloomberg.com/news/articles/2016-05-11/chipotle-spends-1-billion-on-stock-buybacks-as-recovery-

lags

Investment Thesis for Chipotle Mexican Grill Inc. (NYSE:CMG) by Alexander Mabie!

!

quarter of 2016. Liquidation of these stakes was likely part of an effort to free up cash given the

financial pressure resulting from the food-borne illness incidents.

Chipotle’s income statement highlights the deceleration and the decline in revenue that

began in FY15 and persisted into the current fiscal year. The prorated estimate for FY16 of

$3.83B represents a 15% contraction in revenue. Margins on expenses are relatively constant

throughout the historical period of interest.

Value Drivers

The results are contained in the ‘Value Drivers’ worksheet of the accompanying Excel workbook.

The value drivers worksheet provides substantial insight into the past five years of

Chipotle’s operational health. First and foremost, fiscal years 2011 through 2014 clearly display

the telltale signs of an explosive growth period. The top line grows at impressive rates, averaging

21.9% over the period. Moving to FY15, this figure drops slightly to 9.6%, reflecting the weak

fourth quarter performance that followed the food-borne illness crises. The increase in revenue

was almost exclusively driven by new store openings. Specifically, of the $392.9 million

increase in revenue, revenue from restaurants not yet in the comparable base contributed $390.4

million, or 99.36%, of the increase in sales in FY15. Of this $390.4 million, $183.6 million was

attributable to restaurants opened during FY15. Comparable restaurant sales increased 0.2% on

the year and declined 14.6% for the fourth quarter of 2015, including a 30% decline in December

2015

17

.

When considering fixed costs (the sum of labor, occupancy, other operating costs, and

general and administrative expenses), the trend as a percentage of revenue from FY11through

FY14 was downwards. The reason behind this is that Chipotle reported positive comparable

restaurant sales growth over this period, allowing the company to earn more revenue on the same

fixed costs. However, I see fixed costs as a percentage of revenue increase in FY15 due to the

food illness incidents. I can expect a significant increase in FY16 given the crises’ dampening

effects on revenue, as well as the significant uptick in advertising and marketing efforts

attempting to regain customers. Shareholders should therefore expect margin contraction in

2016.

P-DCF

The results are contained in the ‘P-DCF’ worksheet of the accompanying Excel workbook.

Revenue was projected based on the single reportable business segment. It was predicted

to contract 15% in FY16 to $3.826B, which is the approximate value obtained when prorating

the first three quarters of FY16evenue. It’s worth noting that this decline is slightly more

pessimistic when compared to street estimates. For example, JP Morgan models a 12.5% decline

in FY16 revenue. However, JP Morgan made this assumption before December 6, 2016. On this

date, Chipotle co-CEO Steve Ells expressed his concern about the company’s ability to meet its

guidance for the year

18

at a Barclays retail conference in New York. I feel that this comment

supports our decision to contract FY16 revenue slightly more than Street analysts.

!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!

17

https://www.sec.gov/Archives/edgar/data/1058090/000105809016000058/cmg-20151231x10k.htm

18

http://www.businessinsider.com/chipotle-says-its-nervous-about-guidance-for-the-year-2016-12

Investment Thesis for Chipotle Mexican Grill Inc. (NYSE:CMG) by Alexander Mabie!

!

For FY17, revenue is projected at a growth rate of 20%, factoring in any recovery in sales

to pre-crisis levels that might occur. For the remainder of the forecast period – FY18 to FY25 –

our model assumes a 12% revenue growth rate for each year. These assumptions may seem

overly optimistic compared to street estimates of roughly 18% revenue growth for FY17 and

then 10% thereafter (FY18 to FY25). However, as mentioned above, these generous revenue

projections are chosen intentionally to help convey the degree to which Chipotle stock is

overvalued. At these rates, our output implies that the current market price trades at premium of

roughly 30%. Put another way, holding all else equal, total revenue would have to grow at a

CAGR of 19% from FY18 to FY25 in order to justify the current stock price of $382.48. This

scenario is highly unlikely considering the pervasive trends damaging Chipotle’s brand and

dragging down its top line.

With the exception of two line items, cost margins are held constant at their historical

averages. The first divergence is with the food, beverage and packaging expenses line item. It is

fairly clear, based on its sequential historical margins on revenue [32.5%, 32.6%, 33.4%, 34.6%,

33.4%] that this item has not illustrated signs of operating leverage. Since Chipotle is likely

transitioning into more the mature stage of its life cycle, however, I assume that it will achieve

operating leverage through economies of scale in future periods. Thus, I apply a 0.1% step

decline, as is common practice, over the ten year forecast period. The potential for expansion to

temporarily increase food expenses might bring into question this assumption, but I choose to

omit this consideration for the sake of yielding a conservative model output. J apply this same

step decline to general and administrative expenses for the similar reason of obtaining a

conservative result and due to the fact that this line item has generally declined over the

historical period of focus.

With regard to the cash flow drivers, capital expenditures and depreciation and

amortization are each equated to three percent of revenue, the idea being that the firm invests an

amount that is roughly equivalent to that which it expends. During Chipotle’s growth phase, it

made sense that capital expenditures outpaced depreciation and amortization. However, moving

forward these items should converge to a one-to-one ratio as the company matures. Changes in

working capital, along with another immaterial item, are zeroed out in the model due to lack of

predictability. Remaining items such as interest and taxes were held at their historical averages.

Model Results

These assumptions lead to free cash flow per share of $264.80 versus the current price of

$392.07, implying 33% potential downside. According to the Monte-Carlo results shown in

Figure 3 below, the current price falls in the 99

th

percentile of the simulation. This essentially

indicates that there is a 1% probability that Chipotle’s long-term free cash flow per share will

exceed today’s market price (Figure 3).

Investment Thesis for Chipotle Mexican Grill Inc. (NYSE:CMG) by Alexander Mabie!

!

Figure 3: Monte Carlo Simulation Output

Qualitative and Other Analyses

Competitor Analysis

To gain an understanding of Chipotle’s competitive positioning among industry peers, I

conduct a competitor analysis. This analysis includes three components: valuation multiples,

operating metrics, and profitability metrics. These methodologies can pose useful implications

when viewed in tandem. Namely, they can point to any instances of variability in the multiples.

If Chipotle has the best growth and strongest margins, for example, then high valuation multiples

could be justified.

The valuation multiple columns in the Figure 4 exhibit a comparison of Chipotle’s price

to earnings (P/E) and enterprise value (EV) to earnings before interest, depreciation, and

amortization (EBITDA). The P/E ratio essentially reflects the dollar amount a market participant

will invest in a company to receive one dollar of that company’s earnings. Chipotle’s trailing

twelve-month P/E ratio is 125.31x, while the peer universe average and median P/E is 31.59x

and 29.27x respectively. The EV/EBITDA ratio is another valuation multiple that takes into

account a firm’s debt, which the P/E ratio does not. By this measure as well, Chipotle’s multiples

sizably exceed the industry mean and median.

Investment Thesis for Chipotle Mexican Grill Inc. (NYSE:CMG) by Alexander Mabie!

!

Name Mkt Cap P/E EV EV/EBITDA EV/Sales Sales Growth Yoy (%) Y- SSS (%) EBITDA Margin

POTBELLY CORP 360.21 36.39

7.96

8.46 0.77 14.03 4.40 9.80

PANERA BREAD COMPANY 4882.62 31.43

12.01

12.77 1.77 6.03 1.90 14.84

SHAKE SHACK INC 1388.72 83.24

25.44

33.92 5.14 60.80 13.30 16.41

DOMINO'S PIZZA INC 7781.56 39.55

18.74

20.91 3.85 11.17 N/A 19.94

PAPA JOHN'S INTL INC 3241.11 35.29

17.13

18.38 1.97 2.45 N/A 11.44

STARBUCKS CORP 85490.20 30.44

15.08

16.51 3.77 11.24 5.00 24.67

JACK IN THE BOX INC 3602.41 28.25

12.37

13.68 2.56 3.83 N/A 20.94

WENDY'S CO/THE 3544.42 24.06

14.65

13.99 3.15 -6.42 3.10 25.87

POPEYES 1272.18 29.60

15.22

16.40 4.73 9.93 5.90 32.48

YUM! BRANDS INC 23431.47 17.61

14.42

9.95 3.15 -1.31 N/A 23.22

MCDONALD'S CORP 101853.91 21.66

13.09

13.06 4.79 -7.39 1.50 38.56

SONIC CORP 1265.06 20.75

11.45

10.59 3.08 0.04 2.60 27.90

DUNKIN' BRANDS GROUP INC 4890.37 29.85

14.84

15.96 8.28 8.31 N/A 54.14

DARDEN RESTAURANTS INC 9400.91 20.59

9.77

10.14 1.13 2.51 3.30 13.78

TEXAS ROADHOUSE INC 3442.86 27.88

11.67

12.89 1.46 14.24 7.20 13.54

BUFFALO WILD WINGS INC 3037.93 28.93

9.62

10.20 1.48 19.56 4.20 15.44

Average 16180.37 31.59 13.97 14.86 3.19 9.31 4.76 22.69

Median 3573.42 29.27 13.76 13.37 3.11 7.17 4.20 20.44

CHIPOTLE MEXICAN GRILL

INC

10873.59 125.31

20.48

37.88 3.08 9.56 0.20 7.18

Figure 4: Chipotle Competitor Analysis

Source: Bloomberg Terminal. Command <RV>. Accessed 12/15/16

Valuation Multiples and Operating Metrics

Therefore, we might expect to see that Chipotle has superior operating and profitability

metrics, but this is not the case. Chipotle’s FY15 revenue growth slightly edges over the industry

average and median. Further apparent weakness lies in same-store sales growth and the EBITDA

margin.

In summary, it seems that there is a significant discrepancy between Chipotle’s

staggeringly high valuation and its underwhelming operating and profit performance. While this

analysis is not a surefire method to craft an investment thesis, it is a useful ancillary stress test.

Investors ought to be wary of overpaying for a company that cannot outperform its competitors

throughout the income statement. Chipotle fits this description to a tee.

What Say the Bulls?

I briefly addressed bullish sentiments on Chipotle earlier in this paper when discussing

Ackman’s thesis. However, to properly identify a short candidate, it is prudent to extensively

evaluate the arguments of those most positive on the stock. Ackman, of course, is not the only

investor who sees a bright future for the beleaguered restaurant chain. The famous Jim Cramer of

CNBC cites the experience of Jack-in-the-Box after its 1993 food borne illness incident as

evidence that Chipotle’s “ballgame will change

19

.” However, there are several reasons why I

disagree with this comparison.

1. The Jack-in-the-Box food borne illness outbreak only had one occurrence, while

Chipotle had five consecutive major incidents in less than six months.

2. The Jack-in-the-Box food borne illness outbreak was traced to a single batch of

tainted meat that was cooked to the federal-standard temperature. The sources of

the Chipotle pathogens have yet to be determined.

!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!

19

http://realmoney.thestreet.com/articles/12/06/2016/cramer-wait-few-months-longer-buy-chipotle

Investment Thesis for Chipotle Mexican Grill Inc. (NYSE:CMG) by Alexander Mabie!

!

3. Jack-in-the-Box management was extremely upfront about their outbreak,

apologizing immediately. Chipotle’s team waited months and arrogantly

dismissed public concern over the outbreaks as “hype” concocted by the media

and by the Center of Disease Control

20

.

4. Jack-in-the-Box had a very simple supply chain, but Chipotle’s produce items and

other ingredients are at much higher risk food borne illness.

5. Lastly, Jack’s outbreak occurred in an era when news was still being delivered to

Americans mainly through TV and newspapers. Chipotle’s incidents have been

viral across dozens of news outlets and all over social media.

Management Compensation

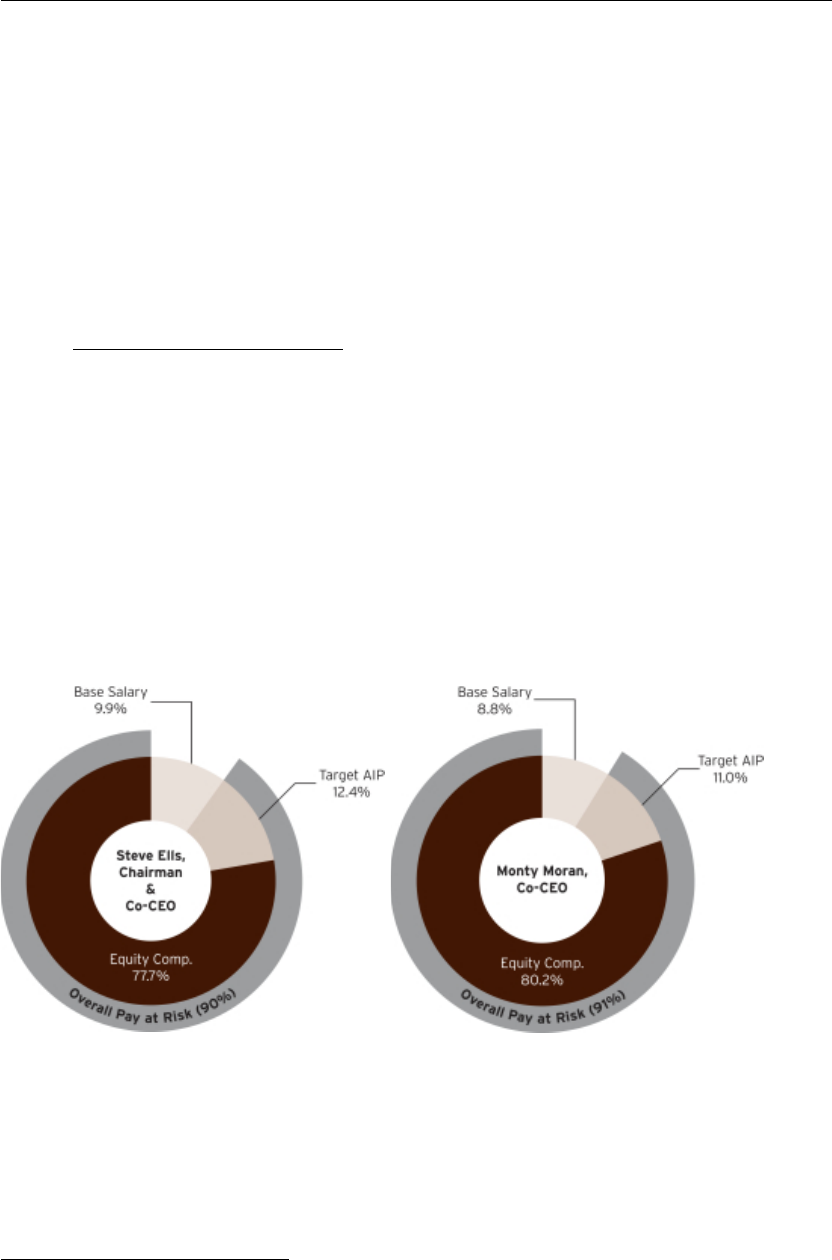

According to Chipotle’s FY15 proxy statement, the company’s executives are

compensated in three ways: base salaries, annual bonuses, and equity-based compensation

21

.

Base salaries are determined each year depending on each executive’s contributions, individual

performance, and level of experience. Annual bonuses are determined under the company-wide

Annual Incentive Plan (AIP). This plan gives variable payouts based on operating and financial

performance goals approved by the compensation committee each year, as well as subjective

measures of individual performance. Equity compensation is designed to align the incentives of

executive officers with shareholder interests and to reward the creation of shareholder value. The

following charts, taken from the company's proxy report, illustrate the breakdown of

compensation structure for various executive officers.

!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!

20

http://seekingalpha.com/article/3987378-chipotles-third-strike-anecdotal-stories-illnesses-highlight-risk-corporate-

shortcomings!

21

https://www.sec.gov/Archives/edgar/data/1058090/000119312516516433/d101839ddef14a.htm

Investment Thesis for Chipotle Mexican Grill Inc. (NYSE:CMG) by Alexander Mabie!

!

To determine various aspects of its compensation policies, Chipotle uses the following

restaurant industry peer group:

COMPANY

2015 ANNUAL REVENUES

(1)(2)

MARKET CAPITALIZATION

(1)(3)

Biglari Holdings, Inc.

$

861

$

673

BJ’s Restaurants, Inc.

$

920

$

1,096

Bloomin’ Brands, Inc.

$

4,378

$

2,024

Bob Evans Farms, Inc.

$

1,336

$

811

Brinker International, Inc.

$

3,100

$

2,856

Buffalo Wild Wings, Inc.

$

1,813

$

3,040

Carrols Restaurant Group, Inc.

$

823

$

411

The Cheesecake Factory Incorporated

$

2,101

$

2,181

Cracker Barrel Old Country Store, Inc.

$

2,861

$

3,036

Darden Restaurants, Inc.

$

6,905

$

8,155

DineEquity Inc.

$

681

$

1,578

Domino’s Pizza Inc.

$

811

$

3,945

Dunkin Brands Group, Inc.

$

2,118

$

6,079

Fiesta Restaurant Group, Inc.

$

664

$

893

Ignite Restaurant Group, Inc.

$

830

$

110

Jack In The Box Inc.

$

1,540

$

2,746

McDonald’s Corp.

$

25,413

$

108,480

Panera Bread Company

$

2,682

$

5,206

Papa John’s International Inc.

$

1,637

$

2,180

Red Robin Gourmet Burgers, Inc.

$

1,258

$

860

Ruby Tuesday, Inc.

$

1,123

$

341

Sonic Corp.

$

612

$

1,594

Starbucks Corporation

$

19,733

$

89,132

Texas Roadhouse Inc.

$

1,807

$

2,509

The Wendy’s Company

$

1,956

$

2,945

Yum! Brands, Inc.

$

13,105

$

31,502

Chipotle’s compensation committee administers base salaries in the range around the 50

th

percentile of the market (determined by the above peer group). The committee also takes into

account other factors such as individual performance, experience, development, and potential.

Therefore, the overall may range from the 25

th

percentile and below for newer executives to the

90

th

percentile or higher for “truly exceptional performers in critical roles who consistently

exceed expectations.” The current base salaries of Chipotle’s executives are at the high end of

Investment Thesis for Chipotle Mexican Grill Inc. (NYSE:CMG) by Alexander Mabie!

!

the range. While no discretionary bonuses were paid in 2015, base salaries were increased for all

executives.

In general, four measures are used to determine the company and team performance

factors. The fiscal 2015 targets for each of the metrics are shown in the table below.

Performance Measure

Target

Operating Income (before AIP and stock compensation expense)

$

1,067.9 million

New Rest. Avg. Daily Sales

$5,278

Comparable Rest. Sales Increase

7.0

%

New Weeks of Operations

5,188

Of the above measures, operating income is weighted most heavily, as the company

believes profitability is the most important measure of its financial success and driver of

shareholder value. Due to the food-borne illness incidents that negatively affected 2015 results,

Chipotle’s company performance factor was 0 percent, resulting in no AIP payouts to executives.

For FY15, the compensation committee made long-term incentive awards to each

executive officer in the form of new performance share awards. These awards incorporate a

three-year performance-contingent vesting period based on Chipotle’s relative performance

return versus the restaurant industry peer group. The following three measures are weighted

equally: averaged revenue growth, net income growth, and total shareholders’ return. The

following illustrates the specifics of payouts and contingencies.

OFFICER NAME

SHARES

EARNED FOR

PERFORMANCE

BELOW

THRESHOLD

THRESHOLD:

SHARES

EARNED AT

35

TH

PERCENTILE

TARGET:

SHARES

EARNED AT

65

TH

PERCENTILE

MAXIMUM:

SHARES

EARNED AT

90

TH

PERCENTILE

% REDUCTION

FROM 2014

LTI

VALUE

Steve Ells

0

7,444

14,887

29,774

49.2

%

Monty Moran

0

7,444

14,887

29,774

49.2

%

Jack Hartung

0

3,126

6,252

12,504

37.8

%

Mark Crumpacker

0

2,233

4,466

8,932

11.2

%

Finally, the summary compensation below effectively communicates the composition of

Chipotle’s executive compensation.

NAME AND

PRINCIPAL POSITION

YEAR

SALARY

STOCK

AWARDS

(1)

OPTION

AWARDS

(2)

NON-EQUITY

INCENTIVE PLAN

COMPENSATION

(3)

ALL OTHER

COMPENSATION

(4)

TOTAL

STEVE ELLS

2015

$

1,526,000

$

12,030,036

—

—

$

281,858

$

13,837,894

Chairman and Co-Chief Executive

Officer

2014

$

1,400,000

—

$

23,698,500

$

3,570,000

$

255,770

$

28,924,270

2013

$

1,400,000

$

7,961,250

$

12,304,500

$

3,196,816

$

254,305

$

25,116,871

MONTY MORAN

2015

$

1,308,000

$

12,030,036

—

—

$

223,041

$

13,561,077

Co-Chief Executive Officer

2014

$

1,200,000

—

$

23,698,500

$

3,060,000

$

194,702

$

28,153,203

2013

$

1,200,000

$

7,961,250

$

12,304,500

$

2,740,128

$

191,176

$

24,397,054

JACK HARTUNG

2015

$

745,769

$

5,052,179

—

—

$

235,361

$

6,033,309

Chief Financial Officer

2014

$

700,000

—

$

8,125,200

$

1,213,800

$

206,842

$

10,245,842

2013

$

645,719

$

3,980,625

$

4,101,500

$

975,501

$

179,004

$

9,882,349

MARK CRUMPACKER

2015

$

532,077

$

3,608,930

—

—

$

141,581

$

4,282,588

Chief Creative and Development Officer

2014

$

500,000

—

$

4,062,600

$

663,000

$

109,591

$

5,335,191

2013

$

402,580

$

3,184,500

$

1,692,400

$

506,328

$

107,054

$

5,892,862

Overall, the company’s management compensation plan is mediocre. The first red flag is

the fact that base salaries were increased in 2015. Even though no annual bonuses were paid out

Investment Thesis for Chipotle Mexican Grill Inc. (NYSE:CMG) by Alexander Mabie!

!

last year (and rightfully so), the compensation committee’s decision to increase base salaries

after the food-borne illness incidents is questionable. One are of strength is the compensation

structure.. Roughly 90% of each executive’s overall pay is at risk, and within this at-risk section,

there is a favorable split between annual bonuses and long-term incentives. Regarding the long-

term incentives, however, there are a couple minor blips. First, a three-year period is really not

“long-term.” Something in the range of five years would be more optimal for aligning interests

with shareholders who have a truly long time horizon. Second, one of the measures involved in

calculating new performance shares granted is annual revenue growth (over the same three year

period). An analysis that also includes a comparison of revenue growth for each of the three

years over this period would be valuable as well. Without such a provision, there is more

likelihood that egregious years such as FY16 fall between the cracks and do not truly implicate

management, as they should.

Share Ownership and Insider Trading

Figure 5 shows a list of Chipotle’s largest shareholders. After Pershing Square Capital

Management, Bill Ackman’s hedge fund, several other big institutional players have invested

considerable stakes in Chipotle’s equity. These firms include exchange-traded fund managers

like BlackRock, Vanguard, State Street, as well as the more traditional mutual fund managers

such as Fidelity and Goldman Sachs Asset Management. The screenshot also reveals that

Chipotle’s short interest is 17.3% of the float, a fairly high value.

Figure 5: All Holders of Chipotle Stock, Sorted by Size

Source: Bloomberg Terminal. Command <HDS>. Accessed 12/19/2016

Investment Thesis for Chipotle Mexican Grill Inc. (NYSE:CMG) by Alexander Mabie!

!

Figure 6 tracks management’s open market buys and sells of the stock over the past

calendar year. It highlights one sale transaction executed by co-CEO Steve Ells on May 31,

2016. Actual insider positions can be seen in Figure 7, which sorts them by size. In aggregate,

insiders hold 1.65% of outstanding stock. Steve Ells owns .68% of the company’s outstanding

shares. Clearly, insiders do not own a significant portion of Chipotle’s equity. While not

necessarily a warning sign itself, low insider ownership should prompt investors to take another

look at company executives. It is important to understand the degree to which these individuals

are financially incentivized to cultivate positive company performance.

Figure 6: Chipotle Insider Transactions

Source: Bloomberg Terminal. Command <GPTR>. Accessed 12/19/2016

Investment Thesis for Chipotle Mexican Grill Inc. (NYSE:CMG) by Alexander Mabie!

!

Figure 7: Insider Holdings of Chipotle Stock, Sorted by Size

Source: Bloomberg Terminal. Command <HDS>. Accessed 12/19/2016

Conclusion

Based on the disappointing output of the P-DCF, a slew of food-borne illnesses that

induced a reversal in popularity, the structure of Chipotle’s management compensation, and a

rich relative valuation, it appears that there is significant potential downside given the current

stock price of $392.07. While management has optimistic views on the company’s ability to right

its course in the wake of its 2015 public relations nightmare, this remains to be seen. Regarding

management, I believe that their allocation of capital with an emphasis on share repurchase

programs is ill informed given Chipotle’s lofty valuation. Furthermore, I perceive the presence of

activist investor William Ackman in the stock as an overall negative, as I do not share his views

on the health of the company’s brand reputation and the brand reputation. Lastly, I think that a

sustained difficult macro backdrop and the potential for consumer spending to weaken in the

near-term pose significant risks. Again, all of these factors, when considered in conjunction,

point to a sell.