Presale:

Driver Australia Six Trust

September 17, 2019

Preliminary Ratings

Class

Preliminary

rating

Preliminary

amount (mil. A$)

Minimum credit

support* (%)

Credit support provided by

subordination and overcollateralization

(%)

A AAA (sf) 665.5 9.9 11.3

B A+ (sf) 37.5 6.0 6.3

Subordinated loan NR 39.8 N/A N/A

Note: This presale report is based on information as of Sept. 18, 2019. The ratings shown are preliminary. Subsequent information may result in

the assignment of final ratings that differ from the preliminary ratings. Accordingly, the preliminary ratings should not be construed as

evidence of final ratings. This report does not constitute a recommendation to buy, hold, or sell securities. *Minimum credit support for credit

losses. NR--Not rated. N/A--Not applicable.

Profile

Expected closing date Oct. 25, 2019

Final maturity date Dec. 21, 2027

Collateral Receivables generated by a pool of chattel mortgage, commercial hire-purchase,

and consumer loan contracts backed by passenger and light commercial motor

vehicles

Issuer Perpetual Corporate Trust Ltd. as trustee of the Driver Australia six Trust

Originator, servicer, subtrust manager,

and subordinated lender

Volkswagen Financial Services Australia Pty Ltd.

Trust manager Perpetual Nominees Ltd.

Security trustee P.T. Ltd.

Class A and class B interest-rate swap

provider

Appropriately rated financial institution (TBD)

Bank account provider Australia and New Zealand Banking Group Ltd.

Supporting Ratings

Bank account provider Australia and New Zealand Banking Group Ltd.

Interest-rate swap provider Appropriately rated financial institution (TBD)

Presale:

Driver Australia Six Trust

September 17, 2019

PRIMARY CREDIT ANALYST

Justin Rockman

Melbourne

(61) 3-9631-2183

justin.rockman

@spglobal.com

SECONDARY CONTACT

Elizabeth A Steenson

Melbourne

(61) 3-9631-2162

elizabeth.steenson

@spglobal.com

www.standardandpoors.com September 17, 2019 1

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimer

on the last page.

2301335

Rationale

This is the sixth closed-pool term transaction backed by collateral originated by Volkswagen

Financial Services Australia Pty Ltd. (VWFS Australia). The preliminary ratings assigned to the

notes to be issued by Perpetual Corporate Trust Ltd. as trustee of the Driver Australia six Trust

(the issuer) reflect the following factors.

The credit risk of the underlying collateral portfolio (discussed in more detail under "Collateral")

and the credit support available are commensurate with the preliminary ratings assigned. Credit

support for the class A notes comprises the subordination of the class B notes and the

subordinated loan, and overcollateralization. Credit support for the class B notes includes the

subordination of the subordinated loan and overcollateralization. In addition, any balance

remaining in the cash reserve on the maturity date of the notes or when the receivables pool

balance reaches zero may be applied toward redemption of the class A and class B notes,

providing additional support.

All contract payments, including the residual or balloon payments, are an obligation of the

borrower. As a result, the trust is not exposed to any market-value risk associated with the sale of

the motor vehicles (on performing receivables), which is a risk that may be associated with other

products, such as operating leases.

The issuer has the capacity to pay interest to the class A and class B note holders in full on each

interest payment date, and to repay principal in full no later than the final maturity date, under

rating stresses commensurate with the preliminary ratings assigned. All rating stresses are made

on the basis that the issuer does not call the notes on or beyond the call-option date, and that the

notes must be fully redeemed via the mechanisms under the transaction documents. Timely

payment of senior expenses and note interest is supported by the use of principal collections and

an amortizing cash reserve funded on the transaction closing date. The reserve is sized at 1.2% of

the discounted receivables balance, as well as being subject to a floor of the lesser of A$7.5

million and the outstanding amount of the class A and class B notes.

The legal structure of the issuer, which is established as a special-purpose entity, and meets our

criteria for insolvency remoteness.

Our preliminary ratings also take into account the counterparty support provided by Australia and

New Zealand Banking Group Ltd. (ANZ) as bank account provider and by the interest-rate swap

provider. Fixed-to-floating interest-rate swaps will be provided to hedge the mismatch between

the fixed-rate payments on the receivables and the floating-rate interest payable on the notes.

The transaction documents for the swap and bank accounts include downgrade language

consistent with our "Counterparty Risk Framework: Methodology And Assumptions" criteria,

published on March 8, 2019, that requires the replacement of the counterparty or other remedy,

should its rating fall below the applicable rating.

Notable Features

The receivables portfolios in Driver Australia transactions are purchased by the issuer at a single

fixed discount rate, which means the issuer could be acquiring the assets at a price that is, on

average, above the par value of the collateral pool. This could result in prepayment losses.

However, for this transaction, the collateral pool is not being purchased above par, and S&P

Global Ratings is satisfied that prepayment losses do not present an additional risk. The discount

rate is set by VWFS Australia at an amount that is intended to match the yield on the transaction

www.standardandpoors.com September 17, 2019 2

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimer

on the last page.

2301335

Presale: Driver Australia Six Trust

to the issuer's expenses. Consequently, there is no excess spread in the transaction.

The transaction has a single--rather than "income" and "principal"--cash-flow priority of

payments, and there is no concept of a principal deficiency ledger or invested/stated amounts of

the notes.

Under the transaction's payment structure, collections--after payment of senior expenses and

class A and class B note interest--initially will be allocated to the class A and class B notes on a

sequential-payment basis, until the class A notes reach a target balance. Thereafter, provided

certain performance triggers have not been breached, collections are to be allocated to the class A

and class B notes until they reach, or in order to maintain, target balances. The target balances

are determined using predefined minimum credit support (overcollateralization) levels for each

class of notes (refer to "Priority Of Payments").

Strengths And Weaknesses

Strengths

In S&P Global Ratings' opinion, the strengths of the transaction observed in the rating analysis

are:

- The pool is a closed pool, with no substitution of receivables.

- The entire portfolio comprises receivables that are backed by passenger and light commercial

motor vehicles. S&P Global Ratings has taken this into account in its assessment of the

minimum credit support at each rating level by giving credit to recoveries.

- About 58.5% of the discounted pool balance comprises contracts that are fully amortizing.

- The collateral pool is reasonably seasoned, with a weighted-average contract seasoning as of

the cut-off date of 11.9 months.

- Some 81.2% of the discounted pool balance represents contracts for the purpose of financing a

new motor vehicle. The historical losses when the motor vehicle financed was new are lower

than those when the motor vehicle was used. We have factored this performance into our

credit-support determination.

Weaknesses

In S&P Global Ratings' opinion, the weaknesses of the transaction observed in the rating analysis

are:

- About 41.5% of the discounted pool balance comprises contracts that are partly amortizing,

with balloon payments due at the end of the contracts, and aggregate balloons represent

17.5% of the discounted pool balance. However, the scheduled payment dates for the balloons

are diversified, and the maximum aggregate balloon payments due in any single month

represent 0.9% of the initial discounted pool balance.

- Under the terms of the servicing agreement, the servicer may extend, defer, amend, modify, or

adjust the receivable contracts in the collateral pool in accordance with its current practices.

- The transaction's principal payment structure is not fully sequential. Principal initially will be

paid to the class A and class B notes on a sequential basis, until the class A notes reach a

www.standardandpoors.com September 17, 2019 3

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimer

on the last page.

2301335

Presale: Driver Australia Six Trust

target balance. Thereafter, provided certain performance triggers have not been breached,

principal is to be allocated to the class A and class B notes until they reach, then maintain,

target balances based on predefined minimum credit support (overcollateralization) levels. In

addition, there is no documented lock-out period from transaction close before collections are

allocated to class B note principal. Nevertheless, S&P Global Ratings' cash-flow analysis of the

transaction suggests that principal would not be paid to the class B notes during the first 12

months of the transaction under rating stresses commensurate with the preliminary ratings

assigned to the notes. Also, the repayment structure will switch back to fully sequential

repayments after the collateral pool has reached 10% of its initial discounted balance, further

mitigating tail-end risk (refer to "Priority Of Payments").

- There is no excess spread in the transaction. Rather, the discount rate is set by VWFS Australia

at a rate intended to match the yield on the assets to the expenses of the transaction. S&P

Global Ratings' cash-flow analysis indicates that yield shortfalls would occur in the latter part

of the transaction under certain rating-stress assumptions. In this scenario, principal

collections that otherwise would be applied toward repayment of principal on the rated notes

would be instead directed toward meeting senior expenses. This is equivalent to the use of

principal draws to meet senior expenses in transactions that have separate "income" and

"principal" cash-flow waterfall priority of payments. Our cash-flow analysis indicates that the

risk that a portion of the principal collections required to repay the rated notes would be

diverted to meet senior expenses under rating-stress assumptions is fully mitigated by the

credit support provided to the class A and class B notes.

www.standardandpoors.com September 17, 2019 4

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimer

on the last page.

2301335

Presale: Driver Australia Six Trust

Transaction Structure

The structure of the transaction is shown in chart 1.

Chart 1

We understand that transaction counsel will lodge the relevant financing statements on the

Personal Property Securities Register in connection with the security interest.

Note Terms And Conditions

Interest payments and overcollateralization percentages

The notes are floating-rate, pass-through notes, paying a margin over the one-month bank-bill

www.standardandpoors.com September 17, 2019 5

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimer

on the last page.

2301335

Presale: Driver Australia Six Trust

swap rate (BBSW) on the principal amount of the notes. Interest payments on the class A notes

rank in priority to interest payments on the class B notes. The transaction does not have a

principal deficiency ledger mechanism. Consequently, the concepts of charge offs, note invested

amounts, and note stated amounts are not applicable in this transaction. Rather, credit support

for the class A and class B notes at any point in time is measured by its overcollateralization

percentage.

The overcollateralization percentage for the class A notes is determined by subtracting the

current balance of the class A notes from the current discounted balance of the collateral pool

and dividing the resultant figure by the current discounted balance of the collateral pool.

The overcollateralization percentage for the class B notes is determined by subtracting the

aggregate current balance of the class A and class B notes from the current discounted balance of

the collateral pool and dividing the resultant figure by the current discounted balance of the

collateral pool.

Principal payment structure

The transaction's principal payment structure is not fully sequential. Principal will be initially paid

to class A and class B notes on a sequential basis, until the class A notes reach a target balance,

determined by the applicable class A target overcollateralization percentage. Thereafter, provided

certain performance triggers have not been breached, principal is to be allocated to the class A

and class B notes until they reach--or maintain, as the case may be--their target balances,

determined by the applicable class A target overcollateralization percentage and class B target

overcollateralization percentage. Provided that the class A and class B target balances are

maintained, collections may be allocated to payments that rank below principal payments on the

rated notes (refer to "Priority Of Payments").

There is no documented lock-out period from transaction close before collections may be

allocated to paying class B note principal. Nevertheless, S&P Global Ratings' cash-flow analysis of

the transaction suggests that, under rating stresses commensurate with the preliminary ratings

assigned to the notes, collections would not be applied to pay class B note principal during the

first 12 months of the transaction.

In addition, the repayment structure will switch back to fully sequential principal repayments after

the collateral pool has reached 10% of its initial discounted balance, further mitigating tail-end

risk.

Call date

On any date on or after the discounted collateral pool balance reaches 10% of its initial amount,

VWFS Australia may notify the issuer and the trust manager that it is exercising a clean-up call.

The clean-up call may only be exercised if the principal outstanding and accrued interest on the

class A and class B notes will be repaid in full. Any balance remaining in the cash reserve at that

time may be applied--via payment of the reserve balance to VWFS Australia and, in turn, its

payment of the purchase price to the issuer--toward redemption of the class A and class B notes.

Priority Of Payments

The transaction has a combined interest and principal cash-flow waterfall priority of payments.

The pre-enforcement priority of payments is summarized in table 1.

www.standardandpoors.com September 17, 2019 6

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimer

on the last page.

2301335

Presale: Driver Australia Six Trust

Table 1

Priority Of Payments (Summarized)

1 A$1 to the beneficiary of the trust

2 Taxes (if any)

3 Trustee and security trustee fees and expenses; servicer, trust manager and sub-trust manager fees

4 Payments to the swap counterparty (except termination payments if the swap counterparty is the

defaulting party or, following a swap termination, due to an unremedied downgrade of the swap

counterparty)

5 Interest on the class A notes

6 Interest on the class B notes

7 Top up of the cash reserve up to its required level

8 Class A note principal (to reach or maintain its target balance)

9 Class B note principal (to reach or maintain its target balance)

10 Other indemnities, costs, and expenses

11 Payments to the swap counterparty not paid above

12 Interest on the subordinated loan

13 Subordinated loan principal

17 Any remaining amounts to the beneficiary of the trust

After the closing date, the notes will be amortized sequentially until the class A notes reach their

target balance, which is determined by the applicable class A note target overcollateralization

level. Following that, provided the class A target balance is maintained, the class B notes will be

amortized until they reach their target balance, which is determined by the applicable class B note

target overcollateralization level.

The target overcollateralization levels applied to determine the target balance of the notes depend

upon whether a credit enhancement trigger has been breached and, if so, whether it is a breach of

a level 1 or level 2 trigger. If a trigger has not been breached, the class A and class B notes would

continue to be amortized once they reach their initial target balances; however, there would be no

further build up in credit support because the target overcollateralization percentage would

remain unchanged. If a level 1 trigger is breached, the target overcollateralization levels for each

of the class A and class B notes would increase, and principal payments on the class B notes to

reach their target balance would not be made unless the class A notes have already reached, then

will maintain, their target balance.

The target overcollateralization level will be 100% for each class of notes, which equates to a fully

sequential principal amortization structure, if a level 2 trigger has been breached, a servicer

replacement event occurs, or the discounted collateral pool balance is less than 10% of its initial

balance.

The target overcollateralization levels would increase if one of the following performance triggers

were breached:

- Trigger level 1: The cumulative net loss ratio exceeds 0.4% for any payment date before or

during October 2020; 0.8% for any payment date from November 2020, but before or during

October 2021; or 1.2% for any payment date after October 2021.

- Trigger level 2: The cumulative net loss ratio exceeds 1.8% at any time.

www.standardandpoors.com September 17, 2019 7

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimer

on the last page.

2301335

Presale: Driver Australia Six Trust

There is no defined point in the transaction documents, such as a maximum number of days in

arrears, at which contracts must be recognized as a gross loss. In such circumstances, there is the

potential for contracts to sit in long-dated arrears buckets before being recognized as a loss. The

performance triggers in this transaction do not include an arrears test. In addition, VWFS

Australia's practice is to recognize a net loss at the time recovery proceeds are received, unless

the contract is fully written off earlier. As a result, there could be a timing lag in this transaction

between any significant deterioration in collateral performance and its recognition in cumulative

net losses, and, therefore, its measurement against the performance triggers. In addition, the

cumulative net loss triggers are set at levels higher than those sized by S&P Global Ratings at the

relevant points in time. However, the credit support provided at transaction close and the target

overcollateralization percentages are set at levels that largely mitigate this concern.

In addition, there is no documented lock-out period from transaction close before collections may

be allocated to class B note principal. Nevertheless, S&P Global Ratings' cash-flow analysis of the

transaction indicates that, under rating stresses commensurate with the preliminary ratings

assigned to the notes, principal would not be paid to the class B notes during the first 12 months

of the transaction in any case.

The target overcollateralization levels are set out in table 2.

Table 2

Overcollateralization Levels As A Percentage Of Discounted Collateral Pool Balance

Actual overcollateralization

Target overcollateralization levels

At closing No trigger breach

Level 1 trigger

breached

Level 2 trigger

breached

Class A notes 11.3 26.0 30.0 100.0

Class B notes 6.3 18.0 21.0 100.0

Before the call date, after the class A notes reach their initial targeted balance, the transaction

would only revert to a pure sequential principal payment structure if the cumulative net loss ratio

exceeds 1.8% or a servicer-replacement event occurs. Accordingly, we analyzed the effect of a

moderate stress on the transaction to determine whether the maximum expected rating transition

of the notes under such a scenario would be in line with those set out in our "Credit Stability

Criteria," published on May 3, 2010. The results of our analysis suggest that under a moderate

rating stress, the maximum expected rating transition on the class A and class B notes within time

horizons of one year and three years would fall within the bounds of those outlined in the criteria.

Originator/Servicer Overview

VWFS Australia is a 100% subsidiary of Volkswagen Financial Services AG (VWFSAG). VWFSAG has

undertaken many securitizations worldwide under its Driver ABS (asset-backed securities)

program. Driver Australia six Trust is VWFS Australia's sixth closed-pool term transaction.

VWFS Australia was incorporated in June 2001. It has around 150 employees, most of whom are

based at its head office in Chullora, New South Wales. Its management team has extensive

experience in either the automotive or finance industry, or both. Although VWFS Australia's

organizational structure includes its own risk and compliance function, VWFS Australia is subject

to VWFSAG's global risk-management framework, and therefore benefits from its parent's

support in risk management and the implementation of global policies.

VWFS Australia offers a range of financial products, including fleet leasing, and dealer floor plan

www.standardandpoors.com September 17, 2019 8

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimer

on the last page.

2301335

Presale: Driver Australia Six Trust

and business loans to dealerships that represent automotive brands within the Volkswagen (VW)

Group, including Audi, Bentley, Skoda, VW, and VW commercial. Its strategy also encompasses the

provision of finance and insurance products to the Australian business and consumer market via

such dealerships. Products offered include finance leases, novated leases, commercial hire

purchase, chattel mortgage, and consumer loans. These products are originated primarily through

about 170 dealerships across Australia. VWFS Australia's strategy includes increasing its

penetration rate (i.e., the percentage of VW Group-manufactured vehicles financed by VWFS

Australia). Its penetration rate is currently about 58%.

As a captive auto financier, VWFS Australia's primary target market is potential acquirers of a new

vehicle manufactured by the VW Group; however, VWFS Australia's origination channels include

dealerships that are "multimanufacturer." In addition, it has partnered with Jaguar and Land

Rover, which do not have finance arms in Australia. Accordingly, the collateral pool for this

transaction is diversified by the inclusion of about 48.5% (by discounted pool balance) of

contracts that are secured by motor vehicles manufactured by a company outside the VW Group.

Although the dealerships are incentivized with commissions and, in some cases, volume bonuses,

all credit decisions remain centralized at VWFS Australia's head office. In addition, such incentives

are clawed back in cases when, before the expiration of the preagreed time frames, contracts are

terminated early or the financed vehicle is repossessed. Dealership performance is also tracked

via hindsight reviews, month-end arrears performance, and quarterly reviews of relative dealer

performance.

The products being securitized in this transaction include VWFS Australia's "ABS Book," which

includes commercial hire purchase, chattel mortgage, and consumer loan contracts secured by

new or used passenger or light commercial motor vehicles. Although such vehicles may include

passenger vehicles used in businesses such as couriers and limousines, such vehicles are subject

to additional credit-assessment criteria. The types of motor vehicles that VWFS Australia will not

finance include trucks, buses, taxis, and commercial vehicles over 4.49T.

VWFS Australia may provide finance to borrowers for additional products such as comprehensive

insurance, gap insurance, extended warranty insurance, and vehicle servicing; however, each of

these is the subject of a separate contract to the vehicle finance contract.

VWFS Australia's credit function has a reporting line to senior management that is separate to its

sales function. While dealers may enter finance applications via the system's Access Catalyst

dealer interface, all credit decision-making is centralized with VWFS Australia's credit team.

Certain credit decisions are built into Access Catalyst and cannot be changed by the dealers, such

as the maximum contract terms of 60 months for commercial hire purchase and chattel mortgage,

and 84 months for consumer loans (provided that there is no balloon, otherwise a maximum

contract term of 60 months would apply).

Applications submitted are assessed via VWFS Australia's scorecard, introduced in 2012, where

they are also subject to checks against credit policy. Applications may be auto-approved or

declined, or referred to retail credit, where they are assessed by a credit officer who holds the

requisite delegated lending authority. Applications that are outside policy, such as vehicle age or

balloon policy, are referred. If an application is declined, then resubmitted with changes, the new

application would not be automatically referred. It could be auto-approved or referred to a

different credit analyst and potentially be approved. However, an application will be locked down

in the system if is resubmitted more than six times. Between January and December 2018, around

55% of applications were auto-approved, and of the 44.8% of applications that were referred,

around 86% were approved. Initially, when the scorecard utilized in the decision-making process

was implemented, VWFS Australia compared the arrears performance of contracts that were

auto-approved with manual approvals and observed that the auto-approved contract arrears were

www.standardandpoors.com September 17, 2019 9

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimer

on the last page.

2301335

Presale: Driver Australia Six Trust

only slightly higher. In addition, the scorecard is validated on a quarterly basis, with a full

validation process undertaken annually.

VWFS Australia's credit process includes an assessment against any adverse credit history listed

on the credit bureau, fraud checks, and other externally available databases such as Australian

post and electoral role listings. If it receives a new finance application for a previous or existing

borrower, it checks its own records of previous borrowers who have defaulted, and might also

undertake checks against its system to determine payment history.

The production of contract documentation is controlled by VWFS Australia systems. Documents

are printed by the dealer, signed by the borrower, and sent to VWFS Australia's settlements team.

System-generated, customized settlement checklists, which are produced for each contract and

include any approval conditions, assist the settlement team in its verification process. The

process must be completed before contracts may be uploaded to the system. All documentation is

scanned into VWFS Australia's document-management system.

VWFS Australia is responsible for servicing the receivables in the collateral pool. Its customer

service team and its collection department report to the front office. Both functions are

centralized at the head office in Chullora. The customer service team comprises a team leader, a

senior customer service officer, and six customer service officers. The collections team comprises

the team leader, five collections officers, one recovery officer and a hardship officer. VWFS

Australia offers a variety of payment methods, including direct debit and BPAY, but direct debit is

the initially elected payment method for more than 98% of the collateral pool, both by balance of

the discounted collateral pool and by number of contracts.

Contracts that fall into arrears are classified as either early or late-stage collections. Early stage

collections include contracts that are one to 21 days in arrears. During this phase, borrowers are

contacted by telephone and mail to attempt to make a payment arrangement. Automated SMS

contact is made at 10 days in arrears, and a behavioral scorecard helps to guide collections

strategy. A default notice will be issued if the borrower does not remedy the outstanding payment.

From August 2017, the management of arrears from one to 30 days has been outsourced to

Queensland-based Collection House, though any hardship cases are referred to VWFS Australia.

Late-stage collections, along with contracts in arrears that have an outstanding balance greater

than A$150,000 or an overdue balloon payment, are automatically sent to a separate work queue

that is managed by more experienced collections officers. Recovery action can commence when

the 30-day default notice period expires. This is usually between 51 and 90 days in arrears. About

60% of the accounts issued to a recovery agent are resolved by the borrower paying the arrears.

VWFS Australia generally recognizes contracts as a gross loss upon the earlier of 180 days in

arrears and repossession of the vehicle. Recognition of a net loss might not occur until the

contract is 270 days in arrears, following a lengthening of this period by VWFS Australia during

2016 to provide for potential financial ombudsman involvement and longer time to try to recover

on the contract. Auctioneers are used for the storage and sale of repossessed motor vehicles, with

prestige auctions selected for prestige vehicles to optimize sale proceeds. The average time from

repossession to sale fluctuates, though is generally 30-90 days.

www.standardandpoors.com September 17, 2019 10

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimer

on the last page.

2301335

Presale: Driver Australia Six Trust

VWFS Australia's historical arrears performance for its total retail book, of which the ABS

products are a subset, is reflected in chart 2.

Chart 2

Performance Of Previous Transactions

The arrears performance of Driver Australia One Trust, Driver Australia Two Trust, Driver Australia

Three Trust, Driver Australia four Trust, and Driver Australia five Trust is illustrated in chart 3. The

net loss performance of Driver Australia One Trust, Driver Australia Two Trust, Driver Australia

Three Trust, Driver Australia four Trust and Driver Australia five Trust is shown in chart 4.

We withdrew in December 2016 our ratings on the class A and class B notes issued by Driver

Australia One Trust and in October 2018 our ratings on the class A and class B notes issued by

Driver Australia Two Trust. Both transactions reached their 10% call option and the notes were

redeemed in full.

In May 2019, we raised the rating assigned to the class B notes of Driver Australia Four Trust to 'AA

(sf)' from 'A+ (sf)'. At the same time we affirmed our ratings on the class A and B notes notes of

Driver Australia Three Trust and the class A notes of Driver Australia Four Trust.

www.standardandpoors.com September 17, 2019 11

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimer

on the last page.

2301335

Presale: Driver Australia Six Trust

Chart 3

Chart 4

www.standardandpoors.com September 17, 2019 12

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimer

on the last page.

2301335

Presale: Driver Australia Six Trust

Collateral

The collateral pool contains 24,415 contracts, comprising chattel mortgage, commercial

hire-purchase, and consumer-loan contracts, secured by passenger and light commercial

vehicles. The aggregate discounted principal balance is about A$750 million. The receivables and

associated rights will be equitably assigned to the issuer by Perpetual Corporate Trust Ltd. as

trustee of the Driver Australia Master Trust. Title may be perfected if certain events occur, such as

the insolvency of VWFS Australia or the occurrence of a servicer replacement event (if VWFS

Australia is the servicer), including a failure of the servicer to remit collections to the issuer when

due or an unremedied breach of a material covenant that has a material adverse effect.

The receivables pool for Driver Australia six Trust as of July 31, 2019, is summarized and

compared with Driver Australia five Trust in table 3 and table 4.

Among Driver Australia six Trust's noticeable differences when compared with Driver Australia five

Trust are a higher percentage of chattel mortgage and a lower percentage of consumer loan, and a

higher proportion of non-VW manufactured vehicles. Consistent with the lower proportion of

consumer loans, the percentage of contracts with balloons and the total balloon payments have

increased.

Table 3

Summary Characteristics

Driver Australia six Driver Australia five

Total number of contracts 24,415 26,849

Total discounted principal balance of contracts (A$) 750,267,890 750,018,993

Maximum discounted principal balance of contracts (A$) 543,388 472,297

Average current discounted contract principal balance (A$) 30,730 27,935

Weighted-average contract rate (%) 6.5 6.8

Discount rate (%)* 8.9 8.9

Total balloon payments as a percentage of total pool balance (%) 17.5 15.2

Weighted-average contract seasoning (months) 11.9 13.1

Weighted-average remaining term to maturity (months) 45.4 46.0

*The discount rate includes a buffer (see "Buffer Release").

Table 4

Pool Characteristics (% Of Pool By Discounted Balance)

Driver Australia six Driver Australia five

Finance type

Chattel mortgage 45.9 37.6

Hire purchase 0.0 0.1

Consumer loan 54.1 62.3

Customer type

Retail 100.0 100.0

Corporate 0.0 0.0

www.standardandpoors.com September 17, 2019 13

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimer

on the last page.

2301335

Presale: Driver Australia Six Trust

Table 4

Pool Characteristics (% Of Pool By Discounted

Balance) (cont.)

Driver Australia six Driver Australia five

New and used

New 81.2 81.1

Used 18.8 18.9

Geographic distribution

New South Wales 39.2 38.7

Victoria 24.6 24.4

Queensland 21.4 19.1

Western Australia 6.0 7.4

Australian Capital Territory 3.0 4.1

South Australia 2.3 2.6

Tasmania 3.0 3.0

Northern Territory 0.5 0.5

Seasoning

Less than one year 52.9 51.9

1-2 years 38.0 38.0

2-3 years 6.9 7.8

3-4 years 1.5 1.5

4-5 years 0.5 0.7

Greater than five years 0.1 0.2

Remaining term to maturity

Less than one year 1.2 1.0

1-2 years 4.7 4.1

2-3 years 18.4 15.8

3-4 years 30.8 28.5

4-5 years 37.8 40.3

Greater than five years 7.1 10.4

Balloon payment

No balloon 58.5 62.7

Balloon 41.5 37.3

Outstanding discounted principal balance (A$)

Less than or equal to 20,000 14.5 18.7

20,000 to 40,000 40.8 43.9

40,000 to 60,000 25.7 23.1

60,000 to 80,000 8.6 7.0

80,000 to 100,000 4.0 3.3

www.standardandpoors.com September 17, 2019 14

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimer

on the last page.

2301335

Presale: Driver Australia Six Trust

Table 4

Pool Characteristics (% Of Pool By Discounted

Balance) (cont.)

Driver Australia six Driver Australia five

100,000 to 150,000 3.4 2.2

150,000 to 550,000 3.0 1.8

Greater than 550,000 0.0 0.0

Manufacturer

Volkswagen Group 51.5 57.4

Non-Volkswagen Group 48.5 42.6

Brand

Volkswagen 30.41 34.19

Audi 18.05 20.61

Land Rover 5.27 2.16

Mitsubishi 4.51 4.41

Ford 3.81 4.17

Holden 3.79 5.20

Subaru 3.43 3.22

Toyota 3.22 2.65

Mazda 2.80 3.58

Hyundai 2.46 2.35

Rover 2.17 0.70

Nissan 2.12 2.34

Honda 1.99 1.88

Skoda 1.85 1.75

Mercedes-Benz 1.72 1.10

KIA 1.51 1.23

Jaguar 1.31 0.50

BMW 1.10 1.55

Jeep 1.09 0.92

Isuzu 1.07 0.83

Maserati 0.87 0.62

Suzuki 0.54 0.67

Renault 0.54 0.62

Volvo 0.53 0.34

Other (29 brands) 3.84

The top 10 obligor concentrations for the collateral pool are set out in table 5.

VWFS Australia permits multiple borrowers for one contract. Examples include a couple jointly

purchasing a motor vehicle and a credit application by an initial borrower that requires secondary

www.standardandpoors.com September 17, 2019 15

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimer

on the last page.

2301335

Presale: Driver Australia Six Trust

support, such as when a young person's parents are supporting the application. VWFS Australia

counts each borrower as a separate obligor, even if the borrowers are parties to a single contract.

Its rationale is that a default by one obligor would only result in a default on the contract if the

joint or secondary borrower went into bankruptcy at the same time. VWFS Australia's

measurement methodology means that although each of the obligors listed in table 5 is a separate

borrower, there may be an overlap or duplication of contracts. This is different to the manner in

which obligor concentrations are measured and disclosed for other ABS originators. However, the

magnitude of the percentages below demonstrates that obligor concentration does not present an

additional risk for this transaction.

Table 5

Top 10 Obligor Concentrations (% Discounted Pool Balance)

Driver Australia six Driver Australia five

Obligor 1 0.08 0.06

Obligor 2 0.07 0.06

Obligor 3 0.07 0.06

Obligor 4 0.07 0.05

Obligor 5 0.07 0.05

Obligor 6 0.07 0.05

Obligor 7 0.07 0.05

Obligor 8 0.07 0.05

Obligor 9 0.06 0.05

Obligor 10 0.06 0.05

Eligibility Criteria

The receivables in the collateral pool are being equitably assigned to the issuer from the Driver

Australia Master Trust. Accordingly, the representations and warranties made on the cut-off date

in respect of the receivables are made by VWFS Australia rather than by the seller. They include,

but are not limited to:

- The obligations of the obligor being legal, valid, binding, and enforceable;

- The receivable being approved and originated by VWFS Australia in the ordinary course of its

business;

- The terms of the contract requiring the obligor to maintain insurance in respect of the financed

object;

- The terms of the contract requiring the obligor to make payments free of set-off;

- The receivable being governed by the laws of a state or territory of Australia;

- The obligor being either a corporation or registrable Australian body; an entity otherwise

established under Australian law; a permanent resident or citizen of Australia or a citizen of

New Zealand; or a person residing in Australia on a work visa whose work entitlements have

been verified and in respect of which the provision of credit has been assessed under internal

guidelines, including special consideration of the loan term relative to the visa term, the deposit

or trade and the inclusion of a residual or balloon payment;

www.standardandpoors.com September 17, 2019 16

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimer

on the last page.

2301335

Presale: Driver Australia Six Trust

- The scheduled maturity date of the receivable being no earlier than three months after the

cut-off date and no later than 84 months after its date of origination;

- The maximum obligor balance not exceeding A$750,000;

- The receivable being denominated and payable in Australian dollars in Australia;

- The receivable not being in arrears by more than one month;

- At least two payments having been received and the contract requiring substantially equal

monthly payments to be made within 84 months of origination and perhaps providing for a final

balloon payment; and

- The receivable being subject to VWFS Australia's standard terms and conditions and having

been serviced in all material respects in accordance with its servicing standards since

origination.

Commingling Risk

Bank accounts for this transaction will be opened in the name of the issuer and held with Australia

and New Zealand Banking Group Ltd. (ANZ) pursuant to the account agreement. The bank

accounts include the cash collateral account, in which the cash reserve is maintained; the

monthly collateral account; and the distribution account. The transaction documents require all

accounts to be held with or guaranteed by a bank that has a minimum long-term rating of 'A'.

If the servicer is VWFS Australia and it is rated at least 'BBB', then it can remit collections to the

issuer monthly. Otherwise, commingling risk is mitigated by the servicer's obligation to remit

expected collections to the monthly collateral account in advance (twice during each monthly

collection period), and transfer the actual amount of monthly collections to the distribution

account two business days after the end of each half-monthly collection prepayment period.

Set-Off Risk

There is no set-off risk for cash deposits in this transaction because VWFS Australia is not an

authorized deposit-taking institution. In addition, the representations and warranties provided by

VWFS Australia in respect of the collateral pool include that the terms of the contract require the

obligor to make payments free of set-off.

Liquidity And Yield

Liquidity is provided in the form of a cash reserve equal to 1.2% of the initial discounted collateral

balance funded on the transaction closing date. The required balance of the cash reserve is 1.2%

of the current discounted pool balance, subject to a floor which is the lesser of A$7.5 million and

the aggregate balance outstanding of the class A and class B notes. The cash reserve is to be

topped up to its required balance to the extent that funds are available for that purpose. If the

balance of the reserve exceeds its required amount, the excess is released to VWFS Australia via

repayments of interest and then principal on the subordinated loan. Any remaining balance of the

cash reserve also may be drawn and used toward repayment of principal on the class A and class

B notes on their final maturity date, or when the collateral pool balance is reduced to zero, which

provides additional support.

www.standardandpoors.com September 17, 2019 17

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimer

on the last page.

2301335

Presale: Driver Australia Six Trust

Interest-Rate Risk

The entire collateral pool comprises fixed-rate receivables. To hedge the mismatch between the

fixed-rate asset cash flows and the floating-rate interest payable on the notes, the issuer will

enter into class A and class B fixed-floating interest-rate swaps with an appropriately rated

counterparty (to be determined). The swap agreements include downgrade language consistent

with our "Counterparty Risk Framework: Methodology And Assumptions" criteria, published on

March 8, 2019, that requires the posting of collateral or the replacement of the swap counterparty

or other remedy if the swap counterparty rating falls below the applicable rating.

Buffer Release

There is no excess spread in this transaction. Rather, the receivables pool is discounted at a rate

intended to match the issuer's expenses during the life of the transaction. Each contract in the

collateral pool has already been discounted (in the Driver Australia Master Trust) at a rate of

8.8897%. This rate represents a considerable buffer over the discount rate required to meet the

issuer's expenses. On each payment date, however, provided VFWS Australia is not insolvent, the

buffer amount will be deducted from collections and paid to VWFS Australia before the remainder

of the collections is applied through the cash-flow waterfall.

Credit And Cash-Flow Analysis

S&P Global Ratings considers the principal rating transition risk for this transaction to be a

significant deterioration in the performance of the underlying receivables.

We have received monthly static gross and net loss data that show cumulative gross losses and

cumulative net losses between January 2006 and May 2019. VWFS Australia does not record a net

loss until the month when recovery proceeds from the sale of the vehicle have been received

(unless written off earlier if there was no expectation of a recovery; for example, if the vehicle is

deemed missing and the contract reaches 270 days in arrears). Accordingly, a loss will only be

recognized in VWFS Australia's cumulative net loss curve as a net loss, and after recovery

proceeds have been received. This is why there is an observable timing lag between the cumulative

gross loss curves and the cumulative net loss curves for VWFS Australia that is generally not seen

in the cumulative loss curves for other ABS originators in this region.

www.standardandpoors.com September 17, 2019 18

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimer

on the last page.

2301335

Presale: Driver Australia Six Trust

Charts 5 and 6 illustrate the cumulative gross default and cumulative net loss experience of VWFS

Australia's total ABS portfolio from January 2006 until May 2019.

Chart 5

Chart 6

www.standardandpoors.com September 17, 2019 19

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimer

on the last page.

2301335

Presale: Driver Australia Six Trust

Charts 7 and 8 illustrate the cumulative gross default and cumulative net loss experience of VWFS

Australia's ABS portfolio from January 2006 until May 2019 for instances in which the vehicle

financed was new.

Chart 7

Chart 8

www.standardandpoors.com September 17, 2019 20

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimer

on the last page.

2301335

Presale: Driver Australia Six Trust

Charts 9 and 10 illustrate the cumulative gross default and cumulative net loss experience of

VWFS Australia's ABS portfolio from January 2006 until May 2019 for instances in which the

vehicle financed was used.

Chart 9

Chart 10

www.standardandpoors.com September 17, 2019 21

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimer

on the last page.

2301335

Presale: Driver Australia Six Trust

Charts 11 and 12 illustrate the cumulative gross default and cumulative net loss experience of

VWFS Australia's ABS portfolio from January 2006 until May 2019 for instances in which the

contract type was chattel mortgage.

Chart 11

Chart 12

www.standardandpoors.com September 17, 2019 22

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimer

on the last page.

2301335

Presale: Driver Australia Six Trust

Charts 13 and 14 illustrate the cumulative gross default and cumulative net loss experience of

VWFS Australia's ABS portfolio from January 2006 until May 2019 for instances in which the

contract type was commercial hire purchase. The volume of commercial hire-purchase contracts

originated by VWFS Australia decreased substantially after mid-2012, consistent with the wider

industry. The loss curves from 2013 onward, in which losses appear to jump markedly at various

points in time, reflect the low origination volumes for those years, with relatively small loss

amounts appearing magnified in the curve.

Chart 13

Chart 14

www.standardandpoors.com September 17, 2019 23

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimer

on the last page.

2301335

Presale: Driver Australia Six Trust

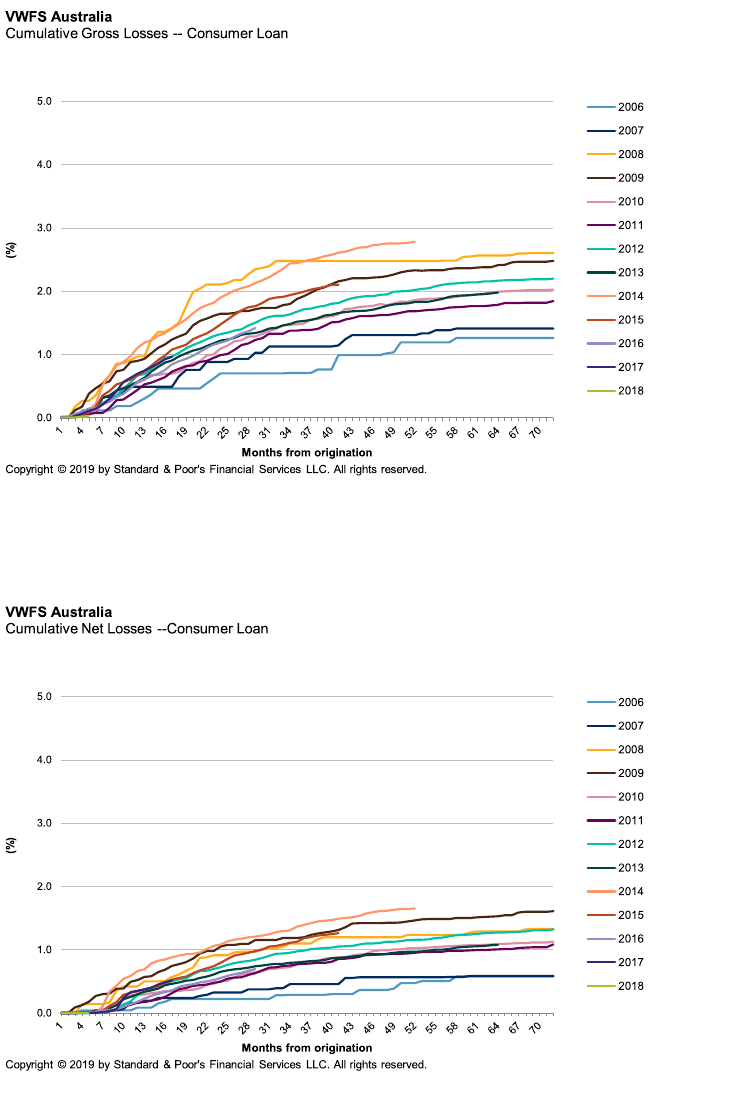

Charts 15 and 16 illustrate the cumulative gross default and cumulative net loss experience of

VWFS Australia's ABS portfolio from January 2006 until May 2019 for instances in which the

contract type was consumer loan.

Chart 15

Chart 16

www.standardandpoors.com September 17, 2019 24

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimer

on the last page.

2301335

Presale: Driver Australia Six Trust

In relation to the partially amortized pools, S&P Global Ratings has extrapolated the loss curves

based on the historical loss performance of VWFS Australia's fully amortized loss curves.

Historical gross loss and recovery data

For the purposes of our loss analysis, in addition to analyzing the total ABS book static loss data,

we separately analyzed each data subset provided by VWFS Australia: new vehicles, used

vehicles, chattel mortgage, commercial hire purchase, and consumer loans.

We adopted a similar approach to the analysis of VWFS Australia's net loss data.

In addition, we analyzed the proportion of total ABS originations during the loss-data period to

determine whether there had been material changes over time in the origination proportions of

new or used vehicles, or contract type. We considered all of these factors, in addition to the actual

composition of the collateral pool, in our determination of base-case gross loss and recovery

assumptions for this transaction.

Our base-case gross loss assumption for the collateral pool is 2.6%. We applied a stress multiple

to the base-case gross default percentage at each given ratings category. The magnitude of the

stress multiple applied depends on the rating level, whereby the higher rated notes are subject to

a higher stress multiple in the analysis.

Credit was given to recoveries. Our base-case recovery assumption for the collateral pool is

47.6%. The credit given to recovery at each ratings category is a percentage of base-case expected

recoveries. In our view, the base recovery rate we have assumed for this transaction, coupled with

the haircut applied, mitigates any possible deterioration in overall recoveries in connection with

the emissions-manipulation issue and vehicles equipped with E189 diesel engines.

Based on the above, our net loss expectation--also commonly referred to as "base-case loss

level"--for the underlying pool is 1.36%. The net loss expectation reflects our opinion of the

combination of the expected gross loss on the underlying pool of 2.6%, and the expected

recoveries of 47.6% from sales of the underlying motor vehicles upon a default.

Table 6 shows a summary of the credit assessment.

Table 6

Summary Credit Assessment

AAA A+

Stress multiple used (x) 5.0 3.0

Default frequency (%) 13.0 7.8

Loss severity (%) 76.2 76.2

Minimum credit support after credit to recovery (%) 9.9 6.0

Cash-flow analysis

We analyzed the capacity of the transaction's cash flow to support the rated notes by running

several different scenarios at each rating category. Our cash-flow analysis encompassed the

following factors:

- Level of gross defaults and recoveries commensurate with each rating level.

www.standardandpoors.com September 17, 2019 25

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimer

on the last page.

2301335

Presale: Driver Australia Six Trust

- Recovery period (assumed to be nine months).

Prepayment rates: We modeled two different prepayment curves. The prepayment stresses

assumed are shown in table 7, and include voluntary and involuntary (default) prepayments.

Timing of defaults: We modeled three different loss curves: a front-loaded, back-loaded, and

normal default curve. The curves employed were reflective of the loss timing observed in VWFS

Australia's static loss curves.

Table 7

Assumed Conditional Prepayment Rates

Months from transaction close Low CPR (% per year) High CPR (% per year)

0 to 3 0.0 12.0

4 to 6 0.0 14.0

7 to 9 0.5 16.0

10 to 12 0.5 18.0

13 to 18 1.0 20.0

19 to 24 1.5 22.0

25 to 30 2.0 24.0

31 onward 3.0 24.0

Note: Total CPR shown is inclusive of voluntary and involuntary (defaults) prepayments.

Our preliminary ratings address not only the availability of funds for full payment of interest and

principal, but also the timeliness of these payments in accordance with the terms of the rated

securities.

Sensitivity Analysis

We cash-flow modeled two additional scenarios to determine how vulnerable the notes would be

to a downgrade under each scenario:

- Scenario 1: Base-case gross losses are 1.25x higher than our expected level of 2.6%.

- Scenario 2: Base recoveries are only 75% of our expected base recovery rate of 47.6%.

The minimum credit support for credit losses under each scenario is set out in table 8.

Table 8

Minimum Credit Support After Credit To Recovery

Scenario AAA (%) A+ (%)

Expected 9.9 6.0

Scenario 1 12.4 7.6

Scenario 2 10.7 6.4

Table 9 sets out what the rating level of each class of notes would be at transaction close--after

incorporating cash flow modelling outcomes--under each scenario.

www.standardandpoors.com September 17, 2019 26

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimer

on the last page.

2301335

Presale: Driver Australia Six Trust

Table 9

Rating Transition

Scenario Class A notes Class B notes

Expected AAA (sf) A+ (sf)

Scenario 1 AA+ (sf) A- (sf)

Scenario 2 AAA (sf) A (sf)

Related Criteria

- Criteria | Structured Finance | General: Counterparty Risk Framework: Methodology And

Assumptions, March 8, 2019

- Legal Criteria: Structured Finance: Asset Isolation And Special-Purpose Entity Methodology,

March 29, 2017

- Criteria - Structured Finance - General: Global Framework For Cash Flow Analysis Of

Structured Finance Securities, Oct. 9, 2014

- Criteria | Structured Finance | ABS: Global Methodology And Assumptions For Assessing The

Credit Quality Of Securitized Consumer Receivables, Oct. 9, 2014

- Criteria | Structured Finance | General: Global Framework For Assessing Operational Risk In

Structured Finance Transactions, Oct. 9, 2014

- Criteria - Structured Finance - General: Global Derivative Agreement Criteria, June 24, 2013

- General Criteria: Global Investment Criteria For Temporary Investments In Transaction

Accounts, May 31, 2012

- General Criteria: Methodology: Credit Stability Criteria, May 3, 2010

- Criteria - Structured Finance - General: Standard & Poor's Revises Criteria Methodology For

Servicer Risk Assessment, May 28, 2009

Related Research

- Australia And New Zealand Structured Finance Scenario And Sensitivity Analysis:

Understanding The Effects Of Macroeconomic Factors On Credit Quality, published April 17,

2017

- Global Structured Finance Scenario And Sensitivity Analysis 2016: The Effects Of The Top Five

Macroeconomic Factors, published Dec. 16, 2016

- Yield Considerations In Standard & Poor's Cash-Flow Analysis Of Australian And New Zealand

ABS, Nov. 21, 2013

- Repayment Structures Of Australian RMBS and ABS Play An Important Role In Supporting

Ratings Stability, Aug. 16, 2010

- ABS Performance Watch: Australia and New Zealand, published quarterly

These articles are available on RatingsDirect, S&P Global Ratings' Web-based credit analysis

system, at

www.standardandpoors.com September 17, 2019 27

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimer

on the last page.

2301335

Presale: Driver Australia Six Trust

http://www.capitaliq.com

.

The issuer has not informed S&P Global Ratings whether the issuer is publicly disclosing all

relevant information about the structured finance instruments that are subject to this rating

report or whether relevant information remains non-public.

S&P Global Ratings Australia Pty Ltd holds Australian financial services license number 337565 under the Corporations

Act 2001. S&P Global Ratings' credit ratings and related research are not intended for and must not be distributed to any

person in Australia other than a wholesale client (as defined in Chapter 7 of the Corporations Act).

www.standardandpoors.com September 17, 2019 28

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimer

on the last page.

2301335

Presale: Driver Australia Six Trust

S&P may receive compensation for its ratings and certain credit-related analyses, normally from issuers or underwriters of securities or from obligors.

S&P reserves the right to disseminate its opinions and analyses. S&P's public ratings and analyses are made available on its Web sites,

www.standardandpoors.com (free of charge), and www.ratingsdirect.com and www.globalcreditportal.com (subscription), and may be distributed

through other means, including via S&P publications and third-party redistributors. Additional information about our ratings fees is available at

www.standardandpoors.com/usratingsfees.

S&P keeps certain activities of its business units separate from each other in order to preserve the independence and objectivity of their respective

activities. As a result, certain business units of S&P may have information that is not available to other S&P business units. S&P has established

policies and procedures to maintain the confidentiality of certain non-public information received in connection with each analytical process.

Credit-related and other analyses, including ratings, and statements in the Content are statements of opinion as of the date they are expressed and

not statements of fact. S&P's opinions, analyses and rating acknowledgment decisions (described below) are not recommendations to purchase,

hold, or sell any securities or to make any investment decisions, and do not address the suitability of any security. S&P assumes no obligation to

update the Content following publication in any form or format. The Content should not be relied on and is not a substitute for the skill, judgment and

experience of the user, its management, employees, advisors and/or clients when making investment and other business decisions. S&P does not act

as a fiduciary or an investment advisor except where registered as such. While S&P has obtained information from sources it believes to be reliable,

S&P does not perform an audit and undertakes no duty of due diligence or independent verification of any information it receives. Rating-related

publications may be published for a variety of reasons that are not necessarily dependent on action by rating committees, including, but not limited

to, the publication of a periodic update on a credit rating and related analyses.

To the extent that regulatory authorities allow a rating agency to acknowledge in one jurisdiction a rating issued in another jurisdiction for certain

regulatory purposes, S&P reserves the right to assign, withdraw or suspend such acknowledgment at any time and in its sole discretion. S&P Parties

disclaim any duty whatsoever arising out of the assignment, withdrawal or suspension of an acknowledgment as well as any liability for any damage

alleged to have been suffered on account thereof.

Copyright © 2019 Standard & Poor's Financial Services LLC. All rights reserved.

No content (including ratings, credit-related analyses and data, valuations, model, software or other application or output therefrom) or any part

thereof (Content) may be modified, reverse engineered, reproduced or distributed in any form by any means, or stored in a database or retrieval

system, without the prior written permission of Standard & Poor's Financial Services LLC or its affiliates (collectively, S&P). The Content shall not be

used for any unlawful or unauthorized purposes. S&P and any third-party providers, as well as their directors, officers, shareholders, employees or

agents (collectively S&P Parties) do not guarantee the accuracy, completeness, timeliness or availability of the Content. S&P Parties are not

responsible for any errors or omissions (negligent or otherwise), regardless of the cause, for the results obtained from the use of the Content, or for

the security or maintenance of any data input by the user. The Content is provided on an “as is” basis. S&P PARTIES DISCLAIM ANY AND ALL EXPRESS

OR IMPLIED WARRANTIES, INCLUDING, BUT NOT LIMITED TO, ANY WARRANTIES OF MERCHANTABILITY OR FITNESS FOR A PARTICULAR PURPOSE OR

USE, FREEDOM FROM BUGS, SOFTWARE ERRORS OR DEFECTS, THAT THE CONTENT'S FUNCTIONING WILL BE UNINTERRUPTED OR THAT THE

CONTENT WILL OPERATE WITH ANY SOFTWARE OR HARDWARE CONFIGURATION. In no event shall S&P Parties be liable to any party for any direct,

indirect, incidental, exemplary, compensatory, punitive, special or consequential damages, costs, expenses, legal fees, or losses (including, without

limitation, lost income or lost profits and opportunity costs or losses caused by negligence) in connection with any use of the Content even if advised

of the possibility of such damages.

Standard & Poor’s | Research | September 17, 2019 29

2301335

Presale: Driver Australia Six Trust