2BDoD 7000.14-R Financial Management Regulation Volume 2B, Chapter 9

* August 2022

9-1

VOLUME 2B, CHAPTER 9: “DEFENSE WORKING CAPITAL FUND BUDGET

JUSTIFICATION ANALYSIS”

SUMMARY OF MAJOR CHANGES

All changes are denoted by blue font.

Substantive revisions are denoted by an * symbol preceding the section, paragraph,

table, or figure that includes the revision.

Unless otherwise noted, chapters referenced are contained in this volume.

Hyperlinks are denoted by bold, italic, blue, and underlined font.

The previous version dated December 2014 is archived.

PARAGRAPH

EXPLANATION OF CHANGE/REVISION

PURPOSE

All

Changed the term “Budgetary Depreciation” to “Capital

Investment Recovery”

Revision

All

Updated hyperlinks and formatting to comply with current

administrative instructions

Revision

1.1

Identified other Revolving Funds separate from the DWCF.

Revision

1.2

Added Authoritative Guidance Section in compliance with

administrative guidance.

Addition

Policy Memo

Incorporated DWCF cash policy and cancelled “Cash

Management Policy for the Defense Working Capital Fund

Activities (FPM21-03)” published June 25, 2021.

Cancellation

1.5

Clarified CIP using reimbursable authority. Clarified Fund-

9c requirements. Updated

Minor Construction Thresholds.

Added ne

w DBMSC certification requirement for CIP

carryover.

Revision

1.6

Updated that budgeted rates are aggregate composite rates.

Incorporated cash policy revision. Clarified CIP for software

in dual funded organizations. Clarified

unusual and

infrequently occurring losses

not affecting budgetary

resources.

Revision

1.9.7

Updated that Direct Reimbursable Work is work performed

outside the rate structure.

Revision

2.4.8

Updated the CIS database input requirements.

Revision

2.6.2

Updated the definitions of the terms “Replenishment Cost,”

“Provisioning Item” and “Variability Target.”

Revision

2.7.1

Added the terms and definitions for “Mission Cost” and “Non-

mission Cost.”

Addition

Exhibit SM-16a

Added the SM-16a exhibit.

Addition

Exhibit Fund-1

Updated the term “CIS obligations”.

Revision

2BDoD 7000.14-R Financial Management Regulation Volume 2B, Chapter 9

* August 2022

9-2

PARAGRAPH

EXPLANATION OF CHANGE/REVISION

PURPOSE

Exhibit

Fund 1a

Updated definition that “All entries are obligations” to “All

entries are expenses.”

Revision

Exhibit

Fund-11a

Updated the display for each approved carryover waiver

separately. Updated the Carryover Calculation methodology.

Revision

Exhibit

Fund-12

Added the Fund-12 exhibit. Addition

Exhibit

Fund-13b

Added the Fund-13b exhibit. Addition

Exhibit

Fund-14

Clarified that NOR may be retained to ensure availability of

budgetary resources.

Revision

Exhibit PB-32

Added the PB-32 exhibit.

Addition

2BDoD 7000.14-R Financial Management Regulation Volume 2B, Chapter 9

* August 2022

9-3

Table of Contents

VOLUME 2B, CHAPTER 9: “DEFENSE WORKING CAPITAL FUND BUDGET

JUSTIFICATION ANALYSIS” ..................................................................................................... 1

1.0 GENERAL ........................................................................................................................ 6

*1.1 Purpose ........................................................................................................................... 6

*1.2 Authoritative Guidance .................................................................................................. 6

1.3 Background .................................................................................................................... 6

*1.4 Cash Management Policy ............................................................................................... 7

*1.5 Capital Investment Program (CIP) Policy .................................................................... 11

1.6 Mobilization/Surge Costs and War Reserve Materiel .................................................. 20

1.7 Military Personnel ........................................................................................................ 21

*1.8 Full Recovery of Costs and the Setting of Prices ......................................................... 21

1.9 Rate Setting for DWCF Activities ................................................................................ 28

1.10 Public-Private Partnerships at Depot Maintenance Activities ..................................... 31

1.11 Military Clothing Items and Individual Equipment ..................................................... 32

*2.0 BUDGET JUSTIFICATION PRESENTATION ......................................................... 32

2.1 Purpose ......................................................................................................................... 32

2.2 Preparation of Materials ............................................................................................... 33

2.3 References .................................................................................................................... 33

2.4 General ......................................................................................................................... 33

2.5 DWCF Application of Commonly Used Financial Management Terms ..................... 37

2.6 Supply Management DWCF Activity Definitions ....................................................... 38

2.7 Non-Supply Definitions ............................................................................................... 44

*3.0 DWCF ACTIVITY EXHIBIT FORMATS ................................................................. 46

3.1 Purpose ......................................................................................................................... 46

3.2 Defense Working Capital Fund Exhibits ...................................................................... 46

Exhibit SM-1 Supply Management Summary .......................................................................... 48

Exhibit SM-3a Requirements to Budget .................................................................................... 50

Exhibit SM-3b By Weapon System Requirements ................................................................... 52

Exhibit SM-4 Inventory Status .................................................................................................. 54

Exhibit SM-5a Markup on Materiel Cost .................................................................................. 57

Exhibit SM-5b OP-32 Price Change to Customers ................................................................... 60

Exhibit SM-6 War Reserve Materiel ......................................................................................... 62

2BDoD 7000.14-R Financial Management Regulation Volume 2B, Chapter 9

* August 2022

9-4

Table of Contents (Continued)

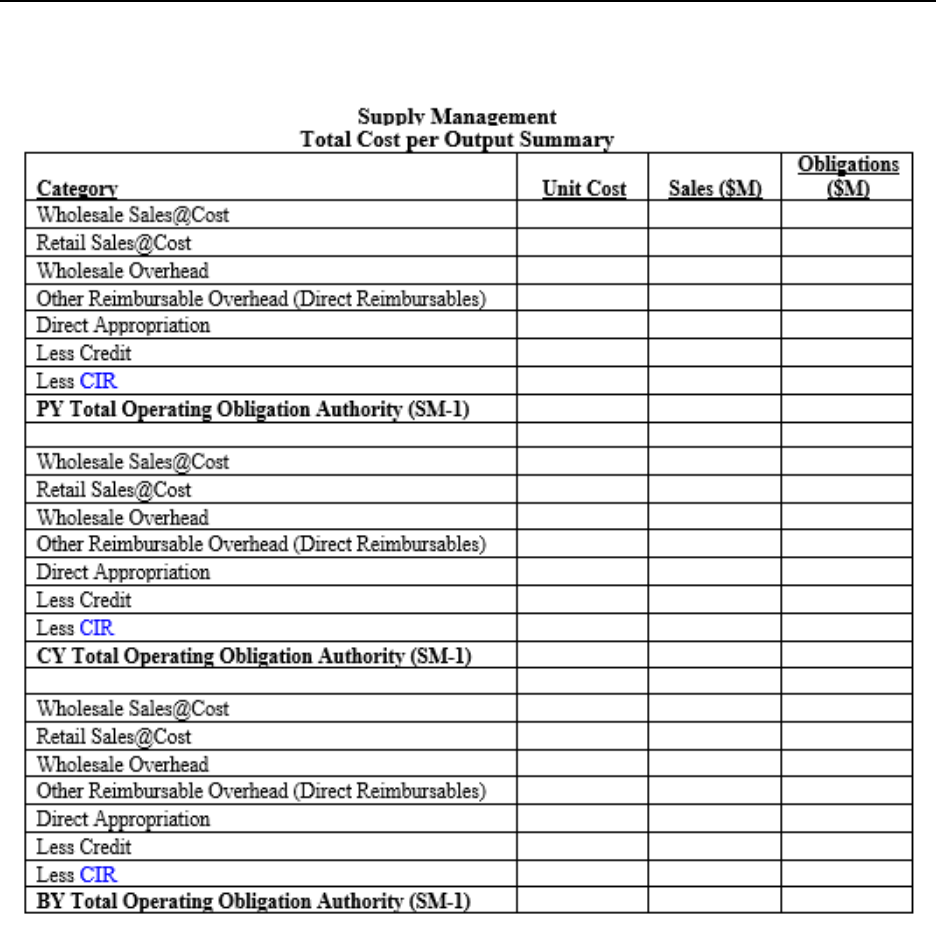

Exhibit SM-16 Total Cost Per Unit Summary .......................................................................... 64

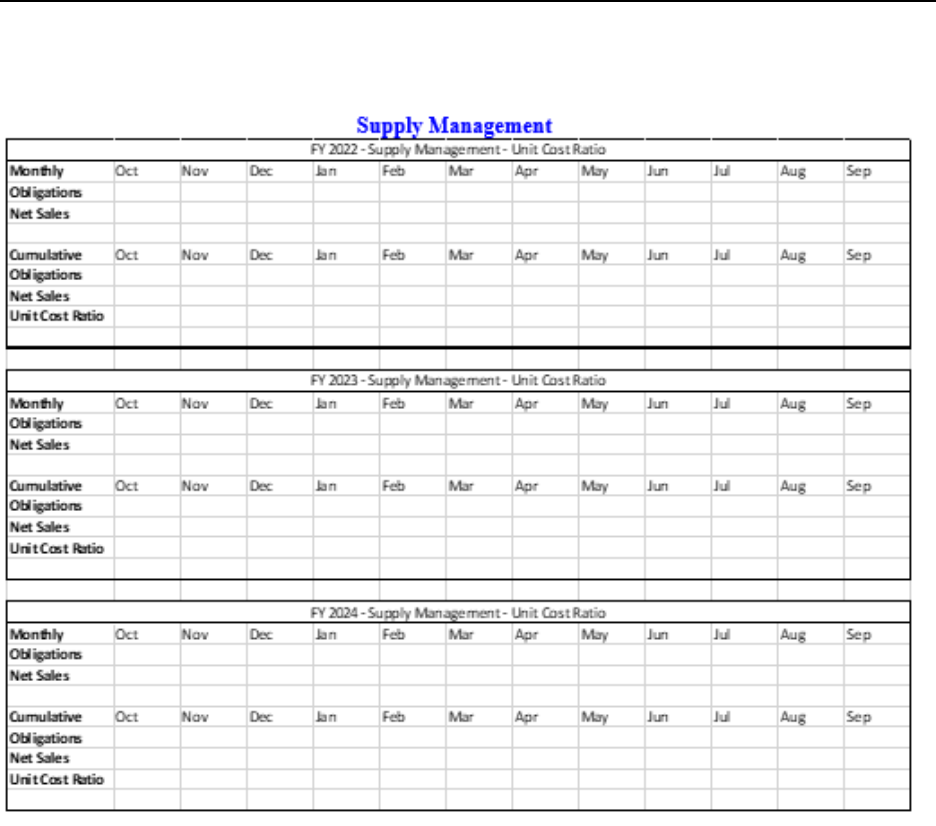

*Exhibit SM-16a Unit Cost Ratio by Month and Fiscal Year ................................................... 65

*Exhibit Fund-1 Summary of Price and Program Changes – Costs ......................................... 66

*Exhibit Fund-1a Details of Price and Program Changes – Costs ............................................ 68

Exhibit Fund-2 Changes in Costs of Operations ....................................................................... 77

Exhibit Fund-3 Labor and Manpower Breakdown .................................................................... 79

Exhibit Fund-5 Total Cost Per Output Summary ...................................................................... 81

Exhibit Fund-6 Depot Maintenance-6 Percent Capital Investment Plan ................................... 83

Exhibit Fund-7 Customer Rate Computations .......................................................................... 86

Exhibit Fund-8 Air Mobility Command Common User Services ............................................. 88

Exhibit Fund-9a Activity Capital Investment Summary ........................................................... 90

Exhibit Fund-9b Activity Capital Purchase Justification .......................................................... 94

Exhibit Fund-9c Capital Budget Execution ............................................................................... 97

Exhibit Fund-11 Source of New Orders & Revenue ................................................................. 98

*Exhibit Fund-11a Carryover Reconciliation ......................................................................... 100

*Exhibit Fund-12 Customer Orders to Customer Funding Reconciliation ............................. 102

Exhibit Fund-13 Cash Management Plan ................................................................................ 107

*Exhibit Fund-13b Cash Requirements ................................................................................... 108

*Exhibit Fund-14 Revenue and Expenses ............................................................................... 111

Exhibit Fund-15 Fuel Data ...................................................................................................... 114

Exhibit Fund-16 Materiel Inventory Data ............................................................................... 116

Exhibit Fund-19 Military Personnel Strength ......................................................................... 117

Exhibit Fund-22 Summary of Base Support ........................................................................... 118

Exhibit Fund-24 Summary of Personnel Data ......................................................................... 119

2BDoD 7000.14-R Financial Management Regulation Volume 2B, Chapter 9

* August 2022

9-5

Table of Contents (Continued)

Exhibit Fund-28 Execution Performance Analysis ................................................................. 120

Exhibit Fund-30 Underutilized Plant Capacity ....................................................................... 123

*Exhibit PB-32 Summary of Price and Program Changes ...................................................... 125

2BDoD 7000.14-R Financial Management Regulation Volume 2B, Chapter 9

* August 2022

9-6

CHAPTER 9

DEFENSE WORKING CAPITAL FUND BUDGET JUSTIFICATION ANALYSIS

1.0 GENERAL

*1.1 Purpose

This chapter describes and documents the policies and procedures for budget formulation

and justification of the Department of Defense (DoD) Working Capital Funds (WCFs), the

Defense Working Capital Fund (DWCF), Building Maintenance Fund (BMF), and the Defense

Counterintelligence and Security Agency (DCSA) WCF. In addition, this chapter provides

guidance for the National Defense Stockpile Fund and Pentagon Reservation Maintenance

Revolving Fund (PRMRF), where applicable. The DWCF is also referred to as the “Fund” in this

chapter.

*1.2 Authoritative Guidance

The National Security Act of 1947, as amended Title 10 United States Code, section 2208

(10 U.S.C. § 2208), and other provisions of 10 U.S.C. § 131 provide the Department’s revolving

fund authority. The BMF, and DCSA WCF were also established under 10 U.S.C. § 2208 as

separate and distinct revolving funds and therefore are not part of the DWCF. The PRMRF was

established by the 1991 National Defense Authorization Act (NDAA) and codified in

10 U.S.C. § 2674.

1.3 Background

1.3.1. The DWCF was established to satisfy recurring DoD requirements using a buyer-

and-seller approach. The customers of the DWCF are the generators of requirements. Federal

customers which operate using appropriated funds justify their budget requests to the Congress.

The requiring activities (i.e. customers) place orders with DoD WCF organizations that have

expertise in the service or product required, and operate under business management principles.

Unlike profit-oriented commercial businesses, the WCF goal is to break even over the long term.

The WCF establishes selling prices in the budget that are normally stabilized or fixed during

execution to mitigate the impact of unforeseen fluctuations that would impact on customers’ ability

to execute the programs approved by the Congress. Exceptions to stabilized prices are listed in

section 1.8 of this document.

1.3.2. The intent of the WCF is to operate as a self-supporting entity to fund business-like

activities. The basic principle of the WCF structure is to create a customer-provider relationship

between military operating units and other federal and non-federal customers and support

organizations. This relationship is designed to make managers of support organizations funded

through WCF and decision-makers at all levels more cost conscious.

1.3.3. Prior to the establishment of an activity as a WCF, the Secretary or Assistant

Secretary of the Military Department or the Director for a Defense Agency, as applicable, must

2BDoD 7000.14-R Financial Management Regulation Volume 2B, Chapter 9

* August 2022

9-7

prepare, sign, and submit a charter that sets forth the scope of the activity to the Under Secretary

of Defense (Comptroller) (USD(C)) for approval. Four criteria are used in evaluating potential

activities for inclusion into the Fund. The four criteria are: 1) identification of outputs that relate

to products or services provided by the business to customers; 2) establishment of a cost accounting

system to collect costs of producing outputs; 3) identification of customers so that resources can

be aligned with the requirements; and 4) evaluation of buyer-seller advantages and disadvantages

to include assessment of the customers’ ability to influence cost by changing demand.

1.3.4. The DWCF evolved from two distinct types of activities. The first type, the Stock

Funds that procured materiel from commercial sources and held an inventory, are now known as

Supply activities. These activities sell the materiel to authorized customers who need the materiel

to achieve weapon systems readiness or provide required personnel support items. The second

type, known then and now as Industrial Funds, provide industrial and commercial goods and

services such as depot maintenance, transportation, and research and development. Although both

types of revolving funds are financed primarily by reimbursements from customers’ appropriated

accounts, Supply activities use contract authority (CA) and Industrial Funds use reimbursable

authority.

1.3.5. The DoD expanded the use of business-like financial management practices through

the establishment of the Defense Business Operations Fund (DBOF) on October 1, 1991. Building

on Stock and Industrial Fund principles, cost and performance are linked and the Fund’s managers

are expected to operate within cost goals established in operating and capital budgets.

1.3.6. The DBOF combined existing operations that were previously managed as

individual funds into a single Treasury account. On December 11, 1996, the USD(C) reorganized

the DBOF, retaining the numerous benefits and improvements resulting from the implementation

of DBOF while clearly establishing each DoD Component’s responsibility for managing the

functional and financial aspects of their respective WCF activities, by creating four DoD

Component WCFs: Army, Navy, Air Force, and Defense-Wide. On December 16, 1997, a

separate DoD Component WCF was established to consolidate the separate Military Departments’

commissaries into the Defense Commissary Agency effective in FY 1999.

1.3.7. Prior to FY 1992, industrially-funded activities did not receive Annual Operating

Budget (AOB) funding documents. All funding authority was provided through customer orders.

With the implementation of the DBOF, the Office of the Under Secretary of Defense (Comptroller)

(OUSD(C)) began to issue AOBs that provide official and administrative management cost goals

and contract authority for the Capital Investment Program (CIP) for each WCF activity within a

DoD Component. The Department has retained this process for the WCFs.

*1.4 Cash Management Policy

1.4.1. The Components will maintain a positive, daily cash balance at levels exceeding the

minimum necessary to meet operating, capital investment, and other justified requirements

throughout the year and to support continuing requirements into the subsequent year. Cash

generated from operations is the primary means of maintaining adequate cash levels. The ability

to maintain sufficient, appropriate cash levels is dependent on setting rates to recover full costs to

2BDoD 7000.14-R Financial Management Regulation Volume 2B, Chapter 9

* August 2022

9-8

include prior year losses, projecting workload accurately, and meeting established operational

goals.

1.4.2. Cash management and accountability are integral parts of operational and cost

management. Each DoD Component is responsible for managing its cash at the activity group

level and in compliance with applicable laws and guidelines. Components must manage cash at

each subordinate DWCF sub-account, organization, and activity, since most cash transactions

occur and cash is most effectively controlled at these levels. Components must submit budget

exhibits (Fund-13, and Fund-13b) for each activity group that displays plans to maintain cash

balances within the lower and upper operating range. The ending cash balance must be above the

lower operating range at the end of each budget year. Decentralizing cash management to the

activity group level provides the DoD Components with additional control, because each level of

management becomes an accountable participant in the execution of the cash plan or policy.

1.4.3. In addition to proper rate setting, cash managers at all levels should employ the

management mitigation strategies available to control cash flows and cash balances to the full

extent possible. These cash management tools include, but are not limited to:

1.4.3.1. Negotiating the timing of customer order receipt, completion and the

related collections;

1.4.3.2. Controlling the timing of delivered goods/services from the

supplier/service provider and the related disbursements;

1.4.3.3. Requesting policy waivers when necessary from the OUSD(C)

Program/Budget (P/B) Director or Deputy Director for Revolving Funds, for example: an approval

for an out-of-cycle rate adjustment, or non-recoverable costs to maintain/reduce cash.

1.4.4. The DoD Components and cash managers at all levels should consider the following

when determining appropriate levels of cash to budget and maintain.

1.4.4.1. Effective cash management is dependent on the availability of accurate

and timely data on cash activity, demand planning, rate setting, and operational results.

1.4.4.2. Activities must budget to achieve an operating cash level that will maintain

a positive cash balance throughout the year within the upper and lower operating range, and an

adequate ending balance to support continuing operations into the subsequent year. In determining

required cash levels, activities will document average disbursements and the expected range of

cash balances, adjusted to accommodate seasonality, known changes in the business environment,

and the inherent risk associated with estimation error and unplanned events outside management’s

control.

1.4.4.3. Each DoD Component and subordinate activity, command, or business

line must establish a cash requirement based on business events, trends, activities, and risks

relevant to its operations. The cash requirement will be developed based on four primary elements:

1) the rate of disbursements, 2) the range of operations, 3) risk mitigation, and 4) reserves. The

2BDoD 7000.14-R Financial Management Regulation Volume 2B, Chapter 9

* August 2022

9-9

amount of cash needed for each of the four cash requirement elements will be determined by the

DoD Component and presented by activity in the exhibit, Fund-13b, Cash Requirements, which

will be reviewed and approved by Revolving Funds Directorate during the Program and Budget

Review (PBR). The four cash requirement elements are explained further in the instructions to the

Fund 13b and also in the following four paragraphs.

1.4.4.4. Rate of Disbursement. The rate of disbursement is the average amount

disbursed between collection cycles. It is calculated by dividing the total amount of disbursements

planned for the year by the number of collection cycles planned for the year. The rate describes

the average amount of cash needed to cover disbursements from one collection cycle to the next.

Changing the number of collection cycles can influence the amount of cash needed to cover the

volatility created by cyclical collections. Both the average disbursements and the number of

collection cycles will be based on authoritative, auditable data.

1.4.4.5. Range of Operations. The range of operations is the difference between

the highest and lowest cash level required based on budget assumptions and past experience. Cash

balances are not static and volatility can be expected due to annual, quarterly, and more frequent

seasonal trends and significant one-time events. Historical trends should be normalized for such

factors as Annual Operating Result (AOR) return/recovery, capital investments, the amount of

work, and changes in operations, and used to estimate future fluctuations in cash flows and

balances. Studying the causes of cash volatility enables the development of strategies for reducing

the range of operation and the amount of cash required for normal operations.

1.4.4.6. Risk Mitigation. Some amount of cash is required, beyond the range of

operation, to mitigate the inherent risk of unplanned and uncontrollable events. Examples of these

risks are budget estimation error, commodity price fluctuation, and other contingency or response

missions. The amount of cash held for risk mitigation will depend on the activity’s sensitivity to

anticipated types of risk, the effectiveness of other cash management and risk mitigation tools, and

management’s level of risk tolerance.

1.4.4.7. Reserves. Cash reserves are funds held for known future requirements.

This element identifies cash on hand that must be kept for specific requirements that are not

expected to disburse until subsequent fiscal years. Examples of reserve requirements include

return of AOR, advances/pre-payments received, liquidation of unexpended appropriations,

liquidation of unpaid obligations, and planned capital investments. Since reserves are only for

specific known requirements, they may not be needed every year.

2BDoD 7000.14-R Financial Management Regulation Volume 2B, Chapter 9

* August 2022

9-10

1.4.4.8. The following figure depicts how the four elements (rate, range, risk

mitigation, and reserves) come together to build the complete cash requirement.

1.4.4.9. Components will develop monthly phased cash plans, incorporating

collections, disbursements, appropriations, and other cash transactions based on Component

estimates, to facilitate the cash management process. The plans will be initially developed during

the budget process and will be an integral part of the budget document (Fund-13).

1.4.4.10. Components will monitor and control to the extent possible execution of

collections and disbursements to ensure a sufficient cash balance is maintained throughout the

year. Components will also monitor execution against monthly phased plans to increase

management attention on reducing costs, emphasizing timely billing, collecting revenue, and

disbursing. Components should consider leveraging the aforementioned available cash

management tools when cash execution is trending below/above plan for more than three

consecutive months of execution.

1.4.4.11. Components must be able to reconcile and explain variances between

cash balances and AOR. In addition to explaining variances based on operations, components

must also explain events that affect cash but not revenues and expenses.

1.4.5. Transfers of cash between DWCF activities, whether directed internally by the

Components or as the result of audit, Departmental guidance, or Congressional direction, will be

included in all the affected activities’ budgets (Fund-13). Transfers between DoD Component

WCFs (e.g., Army to Air Force) or between the DWCF and appropriation-funded activities require

Congressional approval.

1.4.6. Advance Billings.

1.4.6.1. The term “advance billing” means a billing to a customer by the fund, or a

requirement for a customer to reimburse or otherwise credit the fund, for the cost of goods or

services provided (or for other expenses incurred) on behalf of the customer. The term “customer”

means a requisitioning component or agency.

2BDoD 7000.14-R Financial Management Regulation Volume 2B, Chapter 9

* August 2022

9-11

1.4.6.2. Except as provided in paragraph f, the total amount of advance billings

executed by the Department for a fiscal year may not exceed the amount specified in

10 U.S.C. § 2208 (l) or as amended by public law.

1.4.6.3. Components may use advance billings of customers as a cash mitigation

strategy. The OUSD(C) or the Military Department, as applicable, must submit written

notification to Congress within 30 days after the end of the month in which the advance billing is

made. The notification must include the reasons for the advance billing, an analysis of the effects

of the advance billing on military readiness, and an analysis of the effects of the advance billing

on the customer. Military Departments must provide the Revolving Fund Directorate copies of all

advance billing notification letters provided to Congress. Defense agencies will submit their

requests to the Revolving Fund Directorate, who will notify Congress on their behalf.

1.4.6.4. Advance billing requires authorization within the activity’s Annual

Operating Budget (AOB). Components will request this authority and, if approved, the Advanced

Billing Authority will be added to their AOB.

1.4.6.5. Advance payments received from non-federal entities are not subject to

10 U.S.C. § 2208, advance billing limitations, and are required by Volume 11B, Chapter 11. The

billing of customers by Supply Management Activities upon shipment rather than delivery also is

not subject to paragraph (l) advance billing limitations.

1.4.6.5.1. 10 U.S.C. § 2208, paragraph (l)(4) provides that advance billing

for background investigations and related services performed by the Defense Counterintelligence

and Security Agency is not subject to section 2208’s congressional notification requirements and

dollar limitations.

*1.5 Capital Investment Program (CIP) Policy

These policy statements address preparation of the PBR submission.

1.5.1. The legal requirements related to the CIP are found in 10 U.S.C. § 2208, paragraphs

(k), (m), and (o). The legal requirements for unspecified minor military construction projects are

found in 10 U.S.C. § 2805.

1.5.2. The CIP may be used by WCF activities to purchase capital assets meeting the

criteria in 10 U.S.C. § 2208, paragraph (k).

1.5.3. With the exception of major military construction and items listed in paragraphs

1.5.6 and 1.5.9 below, acquisition of all capital assets for use by activities within the Fund will be

financed through the Fund using contract authority. Components may not use the CIP to establish

a new or expand an existing organic capability except as specifically justified in the President’s

Budget Request (Exhibit Fund-9b, “Capital Investment Justification”).

2BDoD 7000.14-R Financial Management Regulation Volume 2B, Chapter 9

* August 2022

9-12

1.5.4. Revolving Fund activities outside the DWCF that are not authorized contract

authority (e.g. the PRMRF) must build the full cost of capital investments into their rate structure

to ensure funds are available prior to obligation.

1.5.5. The CIP consists of the following four major categories of assets: 1) Automated

Data Processing Equipment (ADPE); 2) Non-ADPE Equipment; 3) Software Development,

whether internally or externally developed; and 4) Minor Construction.

1.5.6. The WCF Capital Budget specifically excludes the following items, which must be

financed by appropriated funds.

1.5.6.1. Major Range and Test Facility (MRTF) installations (equipment and

minor construction) that meet the DoD Investment capitalization criteria in accordance with

10 U.S.C. § 2208, paragraph (k).

1.5.6.2. Military and tenant support functions

1.5.6.3. Major weapons systems (such as aircraft, ships, tanks, barges, etc.), and

general-purpose passenger type vehicles

1.5.6.4. Equipment and minor construction projects for mobilization requirements,

but not used during peacetime operations

1.5.6.5. Equipment initially procured and usually furnished as part of a weapons

system and/or support system including modifications (includes initial common support equipment

for depot maintenance support of new weapons systems)

1.5.6.6. Materiel normally funded by appropriated funds and provided to

contractors as Government-Furnished Materiel (GFM). The GFM is incorporated into, used in

conjunction with, or consumed in the production of an end product. The customer must use

appropriated funds to purchase the GFM and provide it at no cost to the WCF

1.5.6.7. Minor construction projects for non-WCF activity or military support

functions

1.5.6.8. Construction and facility investment projects that exceed the amount

specified in 10 U.S.C. § 2805 for funding under Operation and Maintenance appropriations

1.5.6.9. Environmental projects financed or submitted for funding by the

applicable Environmental Restoration Transfer appropriation

1.5.6.10. Capital Investments for morale, welfare, and recreation activities

1.5.6.11. Such other exclusions as may be approved by the USD(C).

1.5.7. The AOB permits a WCF activity to obligate contract authority to purchase capital

assets prior to receiving funded customer orders and collecting cash from customers. Those

2BDoD 7000.14-R Financial Management Regulation Volume 2B, Chapter 9

* August 2022

9-13

obligations must be funded by offsetting collections since cash does not come with contract

authority.

1.5.8. As an administrative control of resources subject to the rules of 31 U.S.C. § 1517,

the Anti-Deficiency Act, the AOBs provide a specific amount of CIP contract authority.

Therefore, obligations may not exceed the amount provided on the AOB.

1.5.9. The WCF customers may procure capital assets through direct appropriations for

use by a WCF activity. However, these assets remain the property of the customer and will not be

recorded as Property, Plant and Equipment assets on revolving fund financial statements unless

the asset is transferred to WCF ownership.

1.5.9.1. At the time of transfer, the WCF activity will record the asset at its net

book value and depreciate it for accounting purposes over the remaining useful life. Depreciation

does not have to be incorporated into the WCF rate structure if the WCF did not outlay any cash

resources. If the asset is expected to be replaced at the end of its useful life, then a capital surcharge

may be collected prior to the acquisition of the replacement asset.

1.5.9.2. The appropriate procurement account will continue to fund the purchase

and installation costs for the initial procurement of depot maintenance capital equipment unique

to newly introduced platforms or weapon systems (this includes modifications). The capital

equipment becomes the property of the depot when it is transferred to or otherwise capitalized by

the depot. The depot will treat the equipment as a capital asset and depreciate it for accounting

purposes. Funding of subsequent replacement and maintenance of the equipment in the DWCF

should be included in the DWCF capital and operating budgets.

1.5.10. WCF activities must recover costs to purchase capital assets by including a Capital

Investment Recovery (CIR) factor in rates billed to customers. The CIR factor is the amount added

to the rate to substitute and then liquidate contract authority obligated to purchase capital assets.

To do this, the Component will allocate a portion of the collections from revenue on customer

orders to liquidate the contract authority. This process allocates cash (i.e. FBwT) from the

operating program to the capital program. The amount of collections used to liquidate contract

authority will equal the amount of obligated contract authority at the end of each FY, net of any

decreases to contract authority or contract authority withdrawn. If there are insufficient budgetary

resources to liquidate the full amount of contract authority obligated, then at a minimum, the

Activities must liquidate enough to cover outlays associated with CIP. This will ensure there is

sufficient cash in the capital program to fund outlays associated with the obligated contract

authority. The CIR factor will differ from the depreciation expense. Collections associated with

the CIR fund capital outlays while depreciation expense is an allocation of costs over an asset’s

useful life.

1.5.10.1. In addition to the CIR, a capital surcharge may be used to collect cash for

the capital outlay if minimum balances are not sufficient to provide adequate budgetary resources

to offset budgetary claims (See Volume 3, Chapter 19).

2BDoD 7000.14-R Financial Management Regulation Volume 2B, Chapter 9

* August 2022

9-14

1.5.11. Guidance on accounting for capital assets is contained in Volume 4, Chapter 24,

Chapter 25, Chapter 26, and Chapter 27.

1.5.12. The following budget exhibits are required to document an activity’s capital budget

request.

1.5.12.1. Exhibit Fund-9a, “Capital Investment Summary,” represents the

summary data of the four asset categories (ADPE, Non-ADPE, Software, and Minor Construction)

at the approved DoD Component aggregate project line item level. The exhibit displays data on

annual capital obligations, cash outlays, and budgeted CIR. The prior-year column on the Exhibit

Fund-9a will show all amounts approved in the most recent President’s Budget, adjusted for actual

project year obligations, additional authorizations and all reprogramming (as depicted on the

Exhibit Fund-9c, “Capital Budget Execution”).

1.5.12.2. Exhibit Fund-9b, “Capital Investment Justification,” provides detailed

cost data and narrative justification for each approved DoD Component aggregate project line item

level. Components will provide a corresponding Exhibit Fund-9b for each aggregate project line

item on the Fund-9a exhibit. The exhibit displays the Benefit to Investment Ratio, Savings to

Investment Ratio and/or the Payback period. Exhibits Fund-9a and Fund-9b data should agree

with, and also should be used for cross-referencing, Exhibit 53 of the Information Technology

budget.

1.5.12.3. Exhibit Fund-9c, “Capital Budget Execution” compares and explains the

differences between the most recent President’s Budget and the current submission by the DWCF

activity for the four asset categories (ADPE, Non-ADPE, Software, and Minor Construction). This

includes prior year (PY) execution adjustments and adjustments to the current year (CY) due to

unexecuted programs or new emerging requirements. Adjustments to project years not displayed

in the budget submission are not recorded on the Fund-9c.

1.5.13. Each proposed CIP project must be reviewed to ensure that it satisfies the

following criteria for justification and backup:

1.5.13.1. The acquisition of a capital asset meets the Department’s long-range

planning and programming objectives and satisfies a documented need for capability to perform

valid operations, functions, or services that cannot be performed as effectively or economically by

the use of existing equipment and facilities or by contract.

1.5.13.2. The acquisition of a capital asset complies with policies and regulations

governing the acquisition and management of facilities, special tooling, and special test equipment

as established by DoD Directive 4275.5, “Acquisition and Management of Industrial Resources,”

as well as other applicable policies and regulations governing the lease and acquisition of

equipment and facilities.

1.5.13.3. The workload projections used to justify capital purchases take into

account the results of inter-service decisions, workload posture planning decisions, readily

2BDoD 7000.14-R Financial Management Regulation Volume 2B, Chapter 9

* August 2022

9-15

available commercial alternatives, and other reasonable options available for accomplishing

applicable work load.

1.5.13.4. The acquisition of a capital asset efficiently and effectively accomplishes

the objective for which it is justified. The criteria are: improved efficiency (savings) or

effectiveness of operations; replacement of unsafe (locally determined by an authorized safety

representative), beyond economical repair, or inoperative and unusable assets; and environmental,

hazardous waste reduction, or regulatory agency (state, local, or Federal) mandated requirements.

1.5.14. A formal pre investment analysis or a cost comparison is required to justify

investment projects for capital budget submissions in the four investment categories (ADPE, Non-

ADPE, Software, and Minor Construction).

1.5.14.1. Either an economic analysis or cost comparison will be used to support a

project substitution or accomplish a reprogramming request. An economic analysis will be used

for all projects with a cost of $5,000,000 or more. A cost analysis will be used for projects under

$5,000,000.

1.5.14.2. Activities must complete this pre-investment analysis prior to including

the capital asset in the capital budget submission, a reprogramming action, or a project substitution.

The originating office of the DoD Component will maintain these analyses as project

documentation support for the capital budget submission and program execution.

1.5.14.3. A cost comparison for investment projects under $5,000,000 will be

prepared in constant base year dollars and present a differential cost display by year for up to a 6-

year evaluation period, beginning with the budget year for which investment funds are requested.

1.5.14.3.1. Documentation for a cost comparison should describe the

functional process performed; define the need/requirement/objective; identify workload

projections; address feasible alternatives; present total costs attributed to each alternative and the

differential costs/monetary benefits expected in constant and current dollars over the 6-year

evaluation period; and provide significant assumptions, constraints, estimating methods, rationale,

data sources.

1.5.14.3.2. The payback period should be the primary economic indicator

used for cost comparisons to rank order within the investment categories of each activity.

1.5.14.4. A pre-investment economic analysis should be prepared to justify capital

investment projects of $5,000,000 or more. The economic analysis should be prepared on a net

present value (NPV) basis and must comply with applicable DoD or Component guidance and

functional program guidance. The economic analysis initially should be prepared in constant base

year dollars and should present a differential cost display by year over the project’s expected

economic life, beginning with the budget year of the investment fund request.

1.5.14.4.1. Documentation should describe the functional process

performed; define the need/requirement/objective; present and explain workload projections;

2BDoD 7000.14-R Financial Management Regulation Volume 2B, Chapter 9

* August 2022

9-16

identify feasible alternatives; present total costs and the differential costs/monetary benefits in

constant, discounted, and current dollars over the expected economic life of the project; present

estimating methods/relationships, and data sources; identify significant constraints, assumptions,

and variables; treat sensitivity and uncertainty of key parameters; and address all other quantifiable

benefits as well as any intangible benefits influencing the recommended course of action.

1.5.14.4.2. Quantifiable benefits are all outputs/results achieved in return

for investment dollars associated with an alternative.

1.5.14.4.3. Benefit-to-Investment Ratio (BIR) should be the primary

indicator used to rank order projects of $5,000,000 or more within the investment categories of

each activity. Also consider the payback period in the ranking process.

1.5.14.4.4. Automated economic analysis programs and reports may be

used if the programs provide comparable information to that of standard economic analysis reports.

1.5.14.5. Compute the payback period to compare the period of time, in years,

necessary for an alternative to repay its investment cost based on the monetary benefits expected.

Present this metric in tenths of years (for example, 7.2 years.)

1.5.14.6. Use the BIR to compare project alternatives in terms of all expected

monetary benefits, inclusive of whole and partial manpower productivity savings resulting from

increased efficiency and other cost avoidance achieved over the total project life under evaluation.

Calculate the BIR using discounted constant dollars, as an index value and rounded to two decimal

places. A BIR of greater than one indicates the project is cost-beneficial; the larger the ratio, the

greater the advantage of the project.

1.5.14.7. Calculate the Savings-to-Investment Ratio (SIR) between actual savings

in terms of funds no longer required and the investment cost for Automated Information Systems,

using discounted dollars.

1.5.14.8. A post-investment analysis should also be done after project completion

to assess the actual costs and benefits and inform future investments.

1.5.14.9. Exemptions to the investment analysis include environmental, hazardous

waste reduction, or regulatory agency (state, local, or Federal) mandated requirements. This

includes action directed by a higher DoD or Component authority that precludes a choice among

alternatives, and DoD instruction or other directive that waives the requirement (e.g., equipment

age or condition replacement criteria).

1.5.15. Internal Use Software as defined in DoDI 5000.76 is: Acquired or developed to

meet the entity’s internal or operational needs (intended purpose); A standalone application, or the

combined software components of an IT system that can consist of multiple applications, modules,

or other software components integrated and used to fulfill the entity’s internal or operational

needs (software type); Used to operate an entity’s programs (e.g. financial and administrative

software, including that used for project management); Used to produce the entity’s goods and to

2BDoD 7000.14-R Financial Management Regulation Volume 2B, Chapter 9

* August 2022

9-17

provide services (e.g., maintenance work order management, loan servicing); or Developed or

obtained for internal use and subsequently provided to other federal entities with or without

reimbursement. This excludes software that is integrated into and necessary to operate general

property, plant, and equipment.

1.5.15.1. Software that is integrated into hardware and is necessary to operate the

hardware, rather than to perform an application, should be budgeted with and capitalized as part

of the hardware. Systems application software, however, should be budgeted separately as either

an expense or a capital investment, depending on whether it meets the criteria for a capital asset.

1.5.15.2. Budget for new acquisitions of and improvements to software by project.

The full scope of a software development project may consist of costs incurred in: 1) Preliminary

Design, 2) Software Development, and 3) Post Implementation. While all of these costs are part

of the project, only the software development phase is capitalized. Refer to Volume 4, Chapter 27

for more information on the accounting requirements.

1.5.15.2.1. The preliminary design phase consists of conceptual

formulation of alternatives, evaluation and testing of alternatives, determining the existence of

needed technology, and final selection of an alternative. This phase consists of all functional

actions, including source selection for COTS and all actions prior to Systems Requirements

Specification for internally developed software. Expense the preliminary design phase costs as

part of the operating budget and identify them on the Exhibit Fund-1a, “Details of Price and

Program Changes - Costs

1.5.15.2.2. Capitalize the software development phase consisting of the

design of a chosen alternative including software configuration and interfaces, coding, installation

of software and related hardware, and testing, which may include parallel processing development

of user manuals and training.

1.5.15.2.3. Expense the post implementation/operational phase costs of

data conversion and application maintenance, including functional training and documentation,

operational testing, and evaluations conducted after technical acceptance of the software.

1.5.15.3. Exclude from the capital budget all costs incurred prior to Milestone 0,

Concept Exploration and Definition. Expense costs such as basic research, study, exploratory

development establishing feasibility and practicality of proposed solutions and rough order of

magnitude estimates. Also expense costs for technical software support and maintenance software

support occurring after system installation.

1.5.15.4. Only include those software development or acquisition efforts for the

benefit of the activity in the DWCF capital budget submissions. Software developed or acquired

for a specific customer order should be charged to and reimbursed by the requesting customer.

Types of cost to be included in a software development project include total labor and non-labor

costs such as: 1) all direct costs for civilian and military personnel; 2) contractor labor; 3) supplies;

4) travel; 5) processing support for testing; 6) indirect production costs; and 7) general and

2BDoD 7000.14-R Financial Management Regulation Volume 2B, Chapter 9

* August 2022

9-18

administrative (overhead) costs (e.g., base operations support, higher headquarters, and costs for

central design activity-owned assets).

1.5.15.5. Software projects may be accomplished in modules. A module is an

application that may be operated or used independent of other modules within a system. Where

an entire system consists of more than one severable module, request funding for each severable

module in the year that the module is started. Funding requests must be sufficient to complete the

module. If several modules make up a complete ADP system, show the cost of all modules related

to the system.

1.5.15.6. Separately identify ADP equipment and ADP software in the capital

budget.

1.5.15.7. In accordance with 10 U.S.C. § 2222, paragraph (c) and DoDI 5000.75,

current services (CS), development and modernization (DevMod) to a business system with budget

authority and/or spending of $250 million or more over the Future Years Defense Program (FYDP)

for Priority Defense Business Systems or $25 million or more for Fourth Estate Defense Business

Systems over the FYDP must be approved by the Defense Business Council (DBC) , tri-chaired

by the Director, Administration and Management (DA&M), OUSD (C), and DoD CIO for

certification prior to obligating funds.

1.5.16. Unspecified minor military construction projects costing more than the threshold

established in 10 U.S.C. § 2805 must be funded within the DoD Component’s Military

Construction appropriation. Exceptions to this limitation are noted below in 1.5.16.1.

1.5.16.1. Authority provided by 10 U.S.C. § 2805, paragraph (c) to use funds

available for operation and maintenance for unspecified minor construction projects costing not

more than the threshold established therein is available for DWCF-funded unspecified minor

construction. However, projects that have an estimated cost that exceed the thresholds established

in 10 U.S.C. § 2208 that have not been documented in a corresponding budget exhibit (Exhibit

Fund-9b, “Activity Capital Investment Summary”) must be approved through the Congressional

notification process or in a subsequent budget and displayed as an adjustment on the Exhibit

Fund-9c, “Capital Budget Execution.” The approval will be reflected in the Component’s Annual

Operating Budget.

1.5.16.2. In 10 U.S.C. § 2805, paragraph (d), Congress authorized a DoD

Laboratory Revitalization Program that increases to the upper ceiling threshold for certain minor

construction projects at DoD laboratories. The authority is not permanent, but is subject to periodic

congressional extension. Laboratory Revitalization Program projects must be for the revitalization

and recapitalization of Defense laboratories owned by the U.S. and under the jurisdiction of the

Secretary of Defense or a Military Department. In accordance with 10 U.S.C. § 2805, paragraph

(d)(3) any projects using the Laboratory Revitalization Program requires the concerned Secretary

to provide the appropriate Congressional committees a 14 day notification prior to obligation of

funds. Fund activities designated to participate in the DoD Laboratory Revitalization Program

must obtain prior approval from the Director or Deputy Director for Revolving Funds for all

2BDoD 7000.14-R Financial Management Regulation Volume 2B, Chapter 9

* August 2022

9-19

projects estimated to exceed the thresholds established in 10 U.S.C. § 2208 so that those projects

can be specifically identified in the capital program within the AOB prior to project execution.

1.5.16.3. Capital investment costs financed in the minor construction portion of the

capital budget include project planning and design costs associated with minor construction

projects. Planning and design costs are not included as part of the statutory threshold for minor

construction projects.

1.5.17. DoD Components may reprogram capital funds between DWCF activities, or

categories or projects within a DWCF activity. There is no minimum or maximum limit on this

type of reprogramming. Except as noted below, capital reprogramming does not require the

written approval of the Director or Deputy Director for Revolving Funds in the form of a signed

AOB. The following approval levels and dollar threshold apply to changes to projects approved

in the capital budget including reprogramming, substitutions, cancellations, and additions:

1.5.17.1. Obtain certification from the approval authority as directed in the

guidance displayed in DoDI 5000.75. All transfers between information technology capital

projects (ADP Equipment and Software) must be documented in the Activity’s next AOB, but will

not require a new AOB solely for such documentation.

1.5.17.2. Fund managers may approve transfers between the Non-ADP Equipment

and Minor Construction categories or among their individual projects. Components are required

to document the transfers in the activity’s next AOB, but will not require a new AOB solely for

such documentation. CIP transfers between DWCF activities within a DoD Component (e.g.,

supply to non-supply) must be approved by the Director or Deputy Director for Revolving Funds,

in the form of a signed AOB, before the transfer is executed.

1.5.17.3. Components must charge capital obligation adjustments to the program

year cited in the President’s Budget for the original project. The prior year capital investment

program limitation is equal to actual obligations on September 30 of that fiscal year plus

adjustments approved by the Director or Deputy Director for Revolving Funds to the prior year

program. Fund managers may request approval to carry over authority for any unobligated capital

projects before the end of the fiscal year.

1.5.17.4. Capital obligation authority may be adjusted for prior year within-scope

increases provided that there is contract authority available to finance the increase. Before making

such increases, the Component must have equal off reductions (deobligations) of current year

capital authority to finance the prior year increase. Prior approval from the Director or Deputy

Director for Revolving Funds is only required if cumulative adjustments exceed 20 percent of the

total CIP budget of the current fiscal year. All adjustments should be documented in the activity’s

next AOB, but will not require a new AOB solely for such documentation.

1.5.17.5. For current fiscal year capital projects that will not obligate by

September 30, components must request in writing permission to carry over these projects via a

memo to the Director or Deputy Director for Revolving Funds. If the Director or Deputy Director

for Revolving Funds approves the request in a signed memorandum, the approved carry over

2BDoD 7000.14-R Financial Management Regulation Volume 2B, Chapter 9

* August 2022

9-20

amounts for projects not obligated by the end of the fiscal year will be carried forward to the next

fiscal year’s AOB.

1.6 Mobilization/Surge Costs and War Reserve Materiel

1.6.1. Mobilization capability costs include the costs to maintain a surge capacity; procure

and maintain approved war reserve materiel levels; and/or maintain other assets, functions, or

capabilities required to meet an operational contingency as documented in Defense planning

guidance or operational plans.

1.6.2. The DWCF activities should identify all costs related to maintaining a capacity to

meet mobilization requirements. These costs are not considered normal operating costs and may

be reimbursed by direct appropriations so that customer rates are not burdened by contingency

requirements.

1.6.2.1. War Reserve Materiel. Obligations for the procurement of war reserve

materiel must be funded by a direct appropriation to the Fund with one exception; if Congress is

notified, and a cost recovery rate is included in the rates, contract authority may be used. Such

appropriated amounts for secondary items must be reflected as a separate goal within the applicable

Supply Management or Commissary Resale activity AOB. Use the SM-6 “War Reserve Materiel”

exhibit to justify War Reserve Materiel Requirements.

1.6.2.2. Unutilized and Underutilized Plant Capacity.

1.6.2.2.1. Unutilized/Underutilized Plant Capacity (UPC) represents costs

associated with maintaining facilities to meet surge capacity needed for mobilization or war. The

UPC is a mobilization requirement budgeted in and funded by Operation and Maintenance

appropriated funds of the DoD Component responsible for the activity’s management. Do not

include UPC costs in the DWCF rate structure. As a general rule, UPC funding includes the pro-

rata facilities support costs for any month in which 1) mobilization facilities are not used or

2) facilities are used 20 percent or less of available work days.

1.6.2.2.2. Mobilization expenses related to UPC may include both

maintenance and labor costs related to mobilization.

1.6.2.2.3. Each non-supply DWCF activity should prepare a UPC Budget

Exhibit (Fund-30). This exhibit documents total capacity, Unutilized Capacity Index, justification,

and cost used in developing the request for UPC. All non-supply DWCF activities should

complete the three capacity-index metrics found in Part I of the exhibit. Any non-supply activity

requesting UPC funding will also complete the funded UPC line in Part I and the UPC justification

in Part II of the exhibit.

1.6.3. Industrial Mobilization Costs. The Army established a category of costs that

includes both UPC and underutilized facilities cost called “Industrial Mobilization Cost.” The

Army will use the Exhibit Fund-30, “Underutilized Plant Capacity” to justify their IMC costs.

2BDoD 7000.14-R Financial Management Regulation Volume 2B, Chapter 9

* August 2022

9-21

1.6.4. Airlift Readiness Account (ARA). The U.S. Transportation Command

(USTRANSCOM) must maintain sufficient airlift capability to respond to transportation

requirements for a wide variety of mobilization conditions. This requirement exists in both

peacetime and contingency environments. To the extent customer revenue is insufficient to

support the costs of maintaining this capability; the Air Force must provide appropriated funds

from the ARA. USTRANSCOM will coordinate with military services and Combatant

Commanders to understand airlift workload requirements and adjustments to workload projections

on a routine basis. USTRANSCOM must provide the Air Force with the budgeted ARA amount

that will be part of the Transportation Working Capital Fund Budget Estimate Submission (BES)

and President’s Budget with enough lead time for the Air Force to incorporate in its budget

submissions. The Air Force must submit a matching amount in its BES and President’s Budget

submission within its Operation & Maintenance account. USTRANSCOM must submit the

Fund-8, “Air Mobility Command Common User Services” exhibit to justify the ARA requirement.

The USTRANSCOM will record as a funded order and revenue.

1.7 Military Personnel

1.7.1. Components will use the civilian-equivalent rates provided by the OUSD(C) to price

military labor at DWCF activities. The difference between the civilian-equivalent costs, included

in the DWCF budget, and the actual military personnel cost will be budgeted directly in the

appropriate military personnel appropriation. The number of military included in the budget

should be the average strength of military assigned to the DWCF business, using the average fill

rate for the 3 prior fiscal years, unless there is a significant change projected in the budget year.

The fill rate is calculated by dividing actual average strength by the authorized strength for each

grade. The budget amount will equal the average strength for each grade multiplied by the

applicable civilian-equivalency rate.

1.7.2. The amount expensed for military personnel by DWCF activities and the amount

reimbursed to the appropriate military personnel appropriation will equal the amount budgeted.

No adjustments will be made to the DWCF cost of operations to reflect the actual cost of military

personnel employed by DWCF activities. Military Departments having military personnel

assigned to other Components will provide to each Component the number of work years that

should be included in the DWCF budget submission. The DWCF activities that augment their

manpower requirements with National Guard or Reserve personnel, to include those participating

in the Personnel Force Innovation (PFI) program, will reimburse the appropriate military personnel

appropriation at the DWCF civilian-equivalency rates.

1.7.3. The civilian-equivalent costs are provided by the OUSD(C) and are calculated in

accordance with Volume 11A, Chapter 6.

1.7.4. See Volume 2A, Chapter 1 for active duty military personnel pricing policy.

*1.8 Full Recovery of Costs and the Setting of Prices

1.8.1. Managers of DWCF activities within each Component will set their prices based on

full cost recovery, including all general and administrative support. Prices are established by the

2BDoD 7000.14-R Financial Management Regulation Volume 2B, Chapter 9

* August 2022

9-22

budget process and are represented at the aggregate level in the form of a composite rate. Prices

and corresponding rates should remain fixed during the year of execution (exceptions are listed in

Volume 11B, Chapter 15). This stabilized price policy serves to protect customers from

unforeseen inflationary increases and other cost uncertainties and better assures customers that

they will not have to reduce programs to pay for potentially higher-than-anticipated prices. In

turn, this policy allows activities to execute the budgeted program level and permits a more

effective use of DWCF resources.

1.8.2. Except in unusual circumstances, prices for the budget year will be set to break even

over the long run at the activity level. This means that prices will be set to achieve an AOR of

zero in the budget year, provided that cash and budgetary resources are available to support AOR

returns. In budget execution, activities will incur either a positive or negative operating result.

Accordingly, activities will increase their budget year prices to make up actual or projected losses

of budgetary resources or reduce their budget year prices to return actual excess cash resources or

projected budgetary gains to customers.

1.8.3. An activity may request recovery of AOR outside the budget year. This request

must be included in the budget submission, and must demonstrate that the alternative recovery

period will not adversely affect the cash balance of the activity. A phased recovery schedule must

be provided with the budget.

1.8.4. Special Circumstances: DWCF rules for pricing and operating loss recovery or gain

distribution may be waived or deferred if one or more of the following conditions exist.

1.8.4.1. Fund Liquidity: Component fund managers must maintain a positive cash

balance throughout the year. The cash requirement developed on the exhibit, Fund 13b, Cash

Requirements, provides a management guide for maintaining cash sufficiency. Several factors,

however, could cause activities to operate outside the requirement range. To prevent the buildup

of excess cash balances, or to ensure fund solvency, the Director or Deputy Director for Revolving

Funds may direct out-of-cycle rate adjustments at any time during the fiscal year.

1.8.4.2. Depot Maintenance Additional Requirements: If Component cash

balances are projected to be sufficient (see paragraph 1.4) by the end of the budget year, depot

maintenance activities will recoup losses and return gains in the budget year. However, if cash

balances will be outside the cash requirement range, an out-of-cycle rate adjustment or surcharges

may be directed, to restore cash to appropriate levels, at any time in accordance with paragraph 1

above. Also, unplanned depot losses recouped in subsequent years may be financed with prior

year resources, provided all other criteria associated with prior year upward obligations are met.

1.8.4.3. Contingency or Emergency Operations: Fund managers may waive

DWCF pricing and financing requirements to facilitate Department operations during times of war

or other national emergencies. The DWCF activity must notify the Director and Deputy Director

for Revolving Funds in writing within 30 days of this action.

2BDoD 7000.14-R Financial Management Regulation Volume 2B, Chapter 9

* August 2022

9-23

1.8.4.4. Impact of Foreign Currency Exchange Rates: A DWCF activity operating

overseas may experience significant operating losses or gains due to changes in foreign currency

exchange rates.

1.8.4.4.1. While these operating losses and gains are normally recovered or

returned through stabilized rate adjustments in budget years, fund managers may propose out-of-

cycle rate adjustments to the Director and Deputy Director for Revolving Funds to address such

losses and gains in execution. In calculating any gain or loss from foreign currency fluctuations,

the DWCF must use the foreign currency exchange rates published as part of the Department’s

budget justification materials submitted to Congress in support of the President’s budget request

and follow applicable procedures in Volume 6A, Chapter 7.

1.8.4.4.2. The DWCF activities are not eligible to participate directly in the

Foreign Currency Fluctuations, Defense (FCF,D) (97-X-0803) and the Foreign Currency

Fluctuations – Construction, Defense (FCF-C,D) (97-X-0801) accounts.

1.8.4.5. In addition to spreading contract costs when developing rates for all

customers, the DWCF activities may incur and recover costs for contracts awarded specifically to

fill the requirements of one customer by charging that customer an amount equivalent to the

DWCF activity’s expense in funding, awarding, and administering the contract.

1.8.4.6. Unbillable costs and operational losses that cannot be billed to an

identifiable customer or that were generated from unforeseen cost overruns are to be treated as

costs in the fiscal year in which the costs were incurred. The resulting operating losses must be

included in calculating net and accumulated operating results.

1.8.4.7. Unless approved in writing by the Director or Deputy Director for

Revolving Funds as an out-of-cycle rate adjustment, the prices must be consistent with the rates

set for all activity products, goods, or services approved during the budget review and documented

in a memorandum signed by the USD(C), or designated representative.

1.8.4.8. Reimbursement procedures humanitarian efforts are as follows:

1.8.4.8.1. Users must pay for the goods and services provided by all DWCF

activities, including deployment or other emergency response for military or humanitarian

assistance.

1.8.4.8.2. See Volume 11B, Chapter 11, Section 2.7 for guidance.

1.8.4.8.3. Consistent with this policy, third party collections for

transportation provided in response to a Request-for-Assistance (RFA) from another government

agency are prohibited. The Military Department that controls the equipment or personnel is

responsible for reimbursing USTRANSCOM. It is then the responsibility of the Military

Department that accepted the RFA to collect any required reimbursements due that Military

Department by the requesting government agency.

2BDoD 7000.14-R Financial Management Regulation Volume 2B, Chapter 9

* August 2022

9-24

1.8.4.8.4. The sole exception to this policy occurs when the

USTRANSCOM receives an order from the Joint Chiefs of Staff requiring transportation of non-

U.S. owned equipment and/or non-U.S. personnel such as non-reimbursed efforts in support of the

United Nations. In those instances, the Army will pay Surface Deployment and Distribution

Command (SDDC) costs, the Navy will pay Military Sealift Command (MSC) costs, and the Air

Force will pay Air Mobility Command (AMC) costs. Bills may be centralized for more convenient

processing if appropriate; however, billings must be forwarded to the appropriate Military

Department within 30 days from the commencement of service or humanitarian effort. The

Military Departments must pay these bills, including transportation bills, in a timely manner.

1.8.4.8.5. This guidance does not address any contingency operation

designated by the Secretary of Defense as a “National Contingency Operation” under the provision

of the 10 U.S.C. § 127. Special rules apply for such an operation and those rules should be

promulgated separately in conjunction with any designation by the Secretary under the provisions

of that section.

1.8.4.9. Base Realignment and Closure (BRAC) cost reimbursement policies are

as follows:

1.8.4.9.1. BRAC-Related Costs. Costs incurred in implementing the

recommendations of the BRAC Commissions will be funded by the appropriate BRAC account

and are not to be included in the rates and costs of businesses within the Fund. The DWCF

activities may incur BRAC expenses prior to receiving an allocation of BRAC funding; however,

all costs properly charged against the BRAC account must be reimbursed with BRAC funds. The

DWCF activities may not expend funds prior to complying with the notification requirements

imposed by law with respect to the obligation of BRAC funds. The BRAC account must reimburse

all costs incurred by DWCF activities to carry out BRAC prior to the end of the fiscal year in

which costs were incurred. Prior year, current year, or budget year operating losses in DWCF are

not to be budgeted in the base closure accounts. Costs attributable to base closure actions at DWCF

activities to be budgeted in BRAC may include:

1.8.4.9.1.1. BRAC directed reductions-in-force, separation

incentives, plant closures, plant layaway or custody costs, or other BRAC-related expenses, such

as all costs not associated with a valid work order during the year of closure

1.8.4.9.1.2. Environmental restoration and mitigation, to include

reducing, removing, and recycling hazardous waste, and removing unsafe building debris

1.8.4.9.1.3. Planning, to include conducting such advance planning

and design as may be required to transfer from an activity being closed to another military

installation

1.8.4.9.1.4. Outplacement assistance in relocating, training, or

providing other necessary assistance to civilian employees employed by the Department at

installations being closed

2BDoD 7000.14-R Financial Management Regulation Volume 2B, Chapter 9

* August 2022

9-25

1.8.4.9.1.5. Community programs, to include economic adjustment

assistance to a community in which the closed base is located, or community planning assistance

to the community to which functions will be transferred as a result of closure of a military

installation.

1.8.4.9.2. BRAC and DWCF Rates. Overhead, not specific to BRAC and

not in support of producing goods or services for customers, will be financed in the year the costs

are incurred with the Components’ Operation and Maintenance (O&M) appropriations. The

DWCF losses occurring in years prior to closure will be recovered through the rate structure to the

extent that there are new customer orders. When there are no new customer orders in the budget

year, the Component responsible for the activity incurring the loss will finance, as a pass through

from O&M appropriations to the DWCF, all overhead not included in rates supported by ongoing

work or prior year losses to be recovered in the budget year. All costs at a closing activity in the

year of closure that are not associated with a valid work order or are not valid BRAC costs are

O&M costs and must be budgeted in the fiscal year when they will be incurred.

1.8.4.9.3. BRAC-Related Permanent Change of Station (PCS) Moves for

DWCF Activities. Costs incurred to recruit and hire civilian personnel (including associated PCS

costs) to fill vacant positions at an activity that is being transferred from a closing or realigning

installation to another military installation in accordance with a BRAC recommendation may

properly be considered BRAC costs under the Base Closure and Realignment Act of 1990. As a

matter of Department policy, however, BRAC funds will not be used for such costs except in the

case of DWCF activities, which may temporarily charge such costs against the DWCF, provided

the DWCF is reimbursed with BRAC or O&M funds by the end of the fiscal year in which the

costs are incurred.

1.8.4.10. Funding of Civilian Voluntary Separation Incentive Program will be

financed and included in stabilized rates for civilian separation incentive requirements of assigned

employees unless they must be offered as a result of directed BRAC action, in which case the

appropriate BRAC account will fund the civilian separation incentive.

1.8.4.11. Any DWCF activities that use any of the services as listed in Exhibit

Fund-22, “Summary of Base Support” as tenants must reimburse installation host activities in

accordance with DoDI 4000.19 (Support Agreements) to the extent that the specified support for

the DWCF activity increases the host activity’s direct costs. Costs for DWCF mission products

and services (e.g., depot supply, depot maintenance, facility engineering services, information

processing, communications, and software development) should be based on the approved

stabilized rate. Other support incidental to the DWCF activity’s primary mission or purpose must

be budgeted based on direct costs measurable and directly attributable to the DWCF activity

(e.g., incremental direct cost). Only the incremental direct cost attributable to the DWCF activity

may be chargeable to the DWCF activity. Overhead costs are not to be included as a cost to the

DWCF activity. The cost of operations budgeted for these services either as a host or tenant

activity should be noted on Exhibit Fund-22, “Summary of Base Support” in the fall budget

submission.

2BDoD 7000.14-R Financial Management Regulation Volume 2B, Chapter 9

* August 2022

9-26

1.8.4.12. First line supervision is that position level immediately over non-

supervisory workers. First line supervisors and above occupy an official supervisory designated

position, and when acting in a supervisory capacity, should have their labor costs charged by the

DWCF activity as an indirect production cost of the cost center supervised, unless all the

supervisor’s time is in direct support of a single project. First line supervisors may be borrowed

and when used as direct labor, DWCF activities must classify the time of the first line supervisor

as direct labor and charge it to the applicable job order rather than as an indirect production cost.

“Crew chiefs,” “snappers,” “team leaders,” and other subordinate job leaders are not first line

supervisors. Volume 11B, Chapter 13 contains additional information related to charging labor

costs.

1.8.4.13. Management Headquarters Costs for DWCF activities may be allocated

using the following guidance:

1.8.4.13.1. A management headquarters is a discrete organization or part of

an organization that has authority over the management of the DWCF activity. The OSD and

Service Departmental activities normally do not have this direct responsibility. All the major

systems/logistics organizations in the Services include headquarters elements directly supporting

DWCF activities that should be funded or reimbursed by the DWCF activities.

1.8.4.13.2. Costs for discrete DWCF management headquarters

organizations and parts of organizations that perform direct DWCF management headquarters

functions can be financed directly in the DWCF or reimbursed by the DWCF activity (whichever

is more practical). In addition, Components may allocate significant costs for common support

functions, such as counsel or personnel services, at DWCF management headquarters to other

users based on workload percentages in those functions.

1.8.4.14. Dual-Funded Organizations are organizations that are funded (including

reimbursable funding) by both the DWCF and other appropriations or accounts.

1.8.4.14.1. Functions. In instances where a non-management headquarters

function is funded with a combination of WCF and General Funds, the function initially will be

funded in its entirety by either the DWCF or General Funds, based on the preponderance of

definable units of measure for the function (e.g., workload, productive hours, outputs, or ultimate

use).

1.8.4.14.1.1. The part of the organization (or funding source