CONSUMER FINANCIAL PROTECTION BUREAU | SEPTEMBER 2021

Data Point: Subprime Auto

Loan Outcomes by Lender

Type

Data Point No. 2021

-10

Jasper Clarkberg, Jack Gardner, and David Low

prepared this report.

Data points are an

occasional series of publications from the Consumer Financial Protection

Bureau’s Office of Research. These publications are intended to further the Bureau’s objective of

providing an evidence

-based perspective on consumer financial markets, consumer behavior,

and regulations to inform the public discourse.

1

1. Introduction and summary

Americans owe auto lenders well over $1 trillion, making the auto loan market the third-largest

debt market in the United States.

1

Consumers with subprime credit scores are especially likely

to need loans to purchase vehicles,

2

but they are also the most likely to default on their loans,

3

with potentially serious consequences.

4

Despite the importance of subprime auto loans for

consumer welfare, much remains unknown about them.

Borrowers with subprime auto loans typically pay high interest rates and frequently default on

their loans. Interest payments could compensate lenders for borrowers’ default risk, and so the

high interest rates paid by borrowers with subprime loans could be explained by their higher

default rates.

5

But interest rates can vary across consumers for a variety of other reasons, too. A

focus of this report is on how much of the variation of interest rates among subprime loans can

be explained by differences in default rates, and how much is left unexplained.

6

This report

should help the Bureau, other regulators, consumers, and private market participants better

understand the market for subprime auto loans.

7

1

See

https://www.newyorkfed.org/medialibrary/interactives/householdcredit/data/pdf/HHDC_2020Q4.pdf.

2

For evidence that many potential subprime auto loan borrowers cannot buy cars without large loans, see

Liran Einav, Mark Jenkins, and Jonathan Levin, 2012, “Contract Pricing in Consumer Credit Markets”,

Econometrica, Vol. 80, No. 4, p. 1387–1432.

3

In our data (described later), 15.9 percent of subprime loans end in default roughly three years after

origination, while 3 percent of other auto loans do.

4

For an empirical study of the effects of vehicle repossession on auto loan borrowers, see Elizabeth

Berger, Alexander W. Butler, and Erik J. Mayer, “Credit Where Credit Is Due: Drivers of Subprime

Credit”, 2018, available at http://dx.doi.org/10.2139/ssrn.2989380.

5

Lenders should care about a borrower’s default risk (i.e. her probability of defaulting on a loan in the

future, evaluated at the time the loan is originated) when pricing loans. We only observe borrowers’

actual default rates. Other researchers, as well as lenders themselves, often use default rates to study

default risk as we do. See Section 5 for more discussion.

6

The term “default” does not have one specific definition in the auto loan market, and it can be used to

refer to loan delinquency that ranges from 60-day delinquency to vehicle repossession. In this report, we

use two specific definitions of “default” given in Section 5.

7

This report is part of the Bureau’s broader mission to educate consumers and to anticipate and monitor

risks across credit markets. See the “Bureauof Consumer Financial Protection Strategic Plan: FY 2018-

2022” at https://files.consumerfinance.gov/f/documents/cfpb_strategic-plan_fy2018-fy2022.pdf

2

Several different types of auto lenders provide loans to borrowers with subprime credit scores.

Some borrowers obtain loans from banks or credit unions, while others obtain loans from

specialty finance companies or “buy-here-pay-here” car dealerships.

There is little existing research examining differences in auto loans provided by different types

of lenders.

8

In this report, we use detailed loan-level data to study differences across these

lender types to better understand the auto financing options available to borrowers with

subprime credit scores. As discussed further below, our data show that interest rates and

default rates vary significantly across lenders of different types. An important caveat is that this

report examines empirical correlations only, and none of its conclusions should be interpreted

as causal.

Our main findings are:

• There are notable average differences across lender types in the borrowers they serve

and the types of vehicles they finance. For example, banks and credit unions making

subprime auto loans tend to lend to borrowers with higher credit scores, and to finance

more valuable vehicles, when compared to finance companies and buy-here-pay-here

dealerships.

• Perhaps not surprisingly in light of these average differences, there are large differences

in average interest rates across different types of lender. For example, for subprime auto

loans in our sample, average interest rates at banks are approximately 10 percent,

compared to 15 percent to 20 percent at finance companies and buy-here-pay-here

dealerships.

• As expected, we find higher default rates at lender types that charge higher interest rates.

For example, we find that the likelihood of a subprime auto loan becoming at least 60

days delinquent within three years is approximately 15 percent for bank borrowers and

between 25 percent and 40 percent for finance company and buy-here-pay-here

borrowers.

• Using regression analysis, we find that differences in default rates could explain some of

the average differences in interest rates across lender types, but cannot explain all of the

average differences. This finding remains true after controlling for other information in

our data, such as credit score and whether the borrower has a mortgage. For example,

we estimate that the average borrower in our data with a “shallow subprime” credit score

8

One exception is Jordan van Rijn, Shuwei Zeng, and Paul Hellman, 2021, “Financial institution

objectives and auto loan pricing: Evidence from the survey of consumer finances”, Journal of Consumer

Affairs, p. 1-45.

3

would have the same default rate with a loan from a bank as with a loan from a small

buy-here-pay-here lender.

9

But her estimated interest rate would be 13 percent with a

loan from a small buy-here-pay here lender, while it would be nine percent with a loan

from a bank. This is a large difference; a borrower with the median loan term and loan

amount for small buy-here-pay-here borrowers in our data would save roughly $894

over the life of a loan if she could reduce her interest rate from 13 percent to nine

percent.

• These results mean that differences in default risk alone are unlikely to fully explain

differences in interest rates charged by different types of auto lenders. We discuss many

other reasons that interest rates could vary across lender types besides default risk; such

factors include (but are not limited to) variation in borrowers’ down payments, vehicle

values, access to information, and financial sophistication and variation in lenders’

practices and incentives when originating and servicing loans. Our data do not allow us

to confidently distinguish between these reasons. We present some preliminary

evidence from our data on these issues and suggest directions for future research.

9

We discuss finance companies and other auto lender types in Section 2 and define “small” and “large” for

the purposes of this Data Point in Section 3.

4

2. Background

2.1. Types of auto lenders

Auto lenders are typically placed into five distinct categories, each with a distinct business

model. The first two, banks and credit unions, obtain funding in part through accepting deposits

from consumers, and use that funding to provide many different kinds of loans including auto

loans. Their market share is higher among prime consumers than subprime consumers.

“Finance companies” obtain funding through other means, often through securitization of the

loans they originate, and typically focus narrowly on auto loans. The market share of finance

companies is higher for subprime consumers than prime consumers. In funding structure,

“captives” are similar to finance companies, but captives are typically owned by or work closely

with auto manufacturers to extend loans specifically to fund purchases of vehicles made by that

manufacturer. Captive business models vary, but their general goal is to increase demand for

specific vehicles, and so they often provide loans at particularly competitive rates (often for

prime consumers) and loans for deals that otherwise would not be funded at all (often for

subprime consumers.) Captives have a high market share among both prime and subprime

consumers. The four lender types described above provide loans for vehicles purchased from

other entities. The fifth lender type, “Buy-Here-Pay-Here” (“BHPH”) car dealerships, provide

loans themselves for vehicles they sell. BHPH dealerships focus heavily on the subprime market.

Auto loans can further be divided into two types: direct and indirect. As in most credit markets,

consumers can obtain auto loans themselves (“directly”) by applying for credit from a lender.

However, most auto loans are “indirect,” i.e. intermediated by car dealerships, who arrange

loans for consumers to purchase their vehicles and are compensated by lenders for doing so. In

this way, the auto loan market is unique among large credit markets in the U.S. Banks and credit

unions originate loans both directly and indirectly, though some specific lenders exclusively do

one or the other. Finance companies and captives typically originate only indirect loans. BHPH

dealerships typically originate direct loans for the vehicles they sell, and typically do not arrange

loans for consumers from other lenders.

5

2.2. “Search frictions” and interest rates

Auto loan prices and terms are not standardized and often depend on the lender, the borrower,

the dealer, and the specific vehicle purchase to be financed. As a result, potential borrowers

often do not know the kinds of loans they can qualify for or where they can obtain the best terms

or rates. In order to learn about relevant loan prices, consumers can try to obtain information on

offers other comparable consumers have received or to obtain actual loan offers themselves, but

these options can be difficult and time-consuming and provide only an incomplete picture of the

best loan offers a specific consumer could qualify for. Economists refer to markets that operate

in this way as characterized by “search frictions,” because consumers must search for prices and

may not find the best prices they could in theory obtain.

10

Identical consumers buying identical

products can pay different prices in markets with search frictions.

11

Search frictions can be exacerbated when product prices and terms are complex. For example,

for a specific auto loan borrower, potential auto loan offers can vary along several important

dimensions: e.g. down payment requirements, monthly payment, loan term, financing fees, and

interest rates. Auto loans that are obtained indirectly, or directly from BHPH dealerships, are

bundled together with the auto purchase they finance; these bundles can vary along several

more important dimensions, such as the quality of the vehicle, its price and vehicle add-ons.

This complexity can make it especially difficult for potential borrowers to understand the loan

offers they have received or to compare them to other loan offers. Dealers or lenders may exploit

this complexity by making a loan offer attractive in one dimension consumers pay particular

attention to, such as the monthly payment or the price of a vehicle, while still increasing the

10

Other markets characterized by search frictions include the labor market (a worker and an employer

must find each other), the housing market (a buyer and seller must find each other), and even the

marriage market (the two spouses must find each other). For an in-depth study of the effect of search

frictions in the auto loan market, see Bronson Argyle, Taylor Nadauld, and Christopher Palmer, 2020,

“Real Effects of Search Frictions in Consumer Credit Markets” available at

http://web.mit.edu/cjpalmer/www/ANP-Search.pdf.

11

For evidence that price differences are often quite large between similar consumers obtaining similar

products in another large credit market –the mortgage market - see Neil Bhutta, Andreas Fuster, and

Aurel Hizmo, 2020, “Paying Too Much? Price Dispersion in the U.S. Mortgage Market”, available at

https://www.federalreserve.gov/econres/feds/files/2020062pap.pdf. See also Alexei Alexandrov and

Sergei Koulayev, 2018, “No Shopping in the U.S. Mortgage Market: Direct and Strategic Effects of

Providing Information”, available at https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2948491 and

Jason Allen, Robert Clark, and Jean-François Houde, 2014, “Price Dispersion in Mortgage Markets”,

available at https://onlinelibrary.wiley.com/doi/full/10.1111/joie.12046.

6

total price of a transaction.

12

Exploiting complexity in this way is particularly effective for

consumers with low financial sophistication.

13

This report examines differences in borrowers’ interest rates across lender types. Auto loan

borrowers face many other potentially important prices, such as quality-adjusted vehicle prices

and financing fees, but we do not observe them and so we cannot study them. If different lender

types extract similar amounts of revenue from consumers but extract this revenue in different

ways (e.g. some charge high interest rates while others charge high financing fees), then

differences in interest rates across lender types will overstate differences in total prices across

lender types. Conversely, if different lender types extract revenue in similar ways from

consumers, but some lender types extract more than others on average, then differences in

interest rates across lender types will understate differences in total prices across lender types.

2.3. Might interest rates vary across lender types?

There are reasons to expect similar consumers to obtain different interest rates from different

kinds of auto lenders. Because they profit directly or indirectly from vehicle sales, both captives

and BHPH dealerships have financial incentives to provide loans beyond profit on the loan

itself, and so they may provide loans at particularly competitive terms for some consumers.

BHPH dealerships and many finance companies specialize in the subprime (often deep

subprime) market, and so often adopt technologies and practices that reduce the cost to lenders

of defaulted loans. These include GPS tracking devices, starter-interrupt devices, and a focus on

funding loans for vehicles with high resale value. Banks and credit unions adopt these practices

less often and so may have different incentives when they originate loans.

There are also reasons to expect similar consumers to obtain similar interest rates from different

kinds of auto lenders. The auto loan market is competitive, and at least in theory many

borrowers have many lenders to choose from. If search frictions in the auto loan market are not

substantial (so obtaining information on auto loan terms and rates is not difficult), and if

12

For evidence that many auto borrowers focus not on total costs but on monthly payments, and that auto

dealers can use this focus on monthly payments to extract extra revenue from consumers, see Bronson

Argyle, Taylor Nadauld, and Christopher Palmer, 2019, “Monthly Payment Targeting and the Demand for

Maturity”, available at https://academic.oup.com/rfs/article-

abstract/doi/10.1093/rfs/hhaa004/5713526.

13

For evidence that auto dealers mark up interest rates on indirect auto loans because consumers pay less

attention to loan prices than to vehicle prices, and that they are particularly likely to do this for consumers

who are less financially sophisticated, see Andreas Grunewald, Jonathan Lanning, David Low, and Tobias

Salz, 2020, “Auto Dealer Loan Intermediation: Consumer Behavior and Competitive Effects”, available at

http://www.nber.org/papers/w28136.

7

consumers actively consider auto loan terms and rates when searching for an auto loan, then

lenders who offered comparatively poor rates or terms would obtain little business and so rates

and terms should be comparable across lenders. Even if search frictions are substantial in the

auto loan market, they may not necessarily imply that differences across lender types should be

large. The type of an auto lender is much easier for a borrower to observe than other potentially

relevant lender characteristics (such as the best interest rate that lender will offer), so borrowers

may readily find the best lender type for them even if they do not find the best lender of that

type. The extent to which interest rates vary across lender types is an open empirical question

addressed in part by this Data Point.

8

3. Data and sample selection

This section discusses the data we use for our analysis, which as described below come from

Experian (one of the three nationwide consumer reporting agencies (NCRAs)) and from one of

the three NCRAs. First, however, there is an important caveat. The NCRAs obtain their

information on auto loans directly from lenders, who “furnish” it. Lenders are not required to

furnish data on loans and decide for themselves whether do so.

14

Some lenders do not furnish

information for some or all loans in their portfolio. Lenders who furnish information to any

NCRA typically furnish to all three NCRAs, but they may also choose to furnish to just one or

two NCRAs. If auto lenders do not furnish loan information for the data we are using, it will not

be in our data. While most auto lenders generally furnish information on most loans to the

NCRAs, there is anecdotal evidence that many BHPH dealerships and small finance companies

frequently do not furnish information on their loans.

15

Thus our NCRA data are likely missing

information on many loans from BHPH dealers and small finance companies. As described

below, our data do allow us to study this issue in Section 4 to a limited extent.

3.1. AutoCount

®

data on loans at origination

We begin our analysis by studying loans at the time they are originated using 2015 data from

Experian AutoCount

®

. We use data from 2015 so that it is comparable to the CCP data we use

from this time, discussed below in Section 3.2. Experian AutoCount

®

is a vehicle statistics

database that collects monthly deidentified title and registration data. In 46 states, title and

registration information includes the finance source on record. Additionally, AutoCount

®

includes estimates of the value of the vehicle securing the loan, as well as information on

whether the car was purchased used or new.

Experian has data on individual loans, but it provides the CFPB only data that are aggregated to

higher levels. The AutoCount

®

data used for this report are aggregated at the dealer-lender-

14

See https://files.consumerfinance.gov/f/201212_cfpb_credit-reporting-white-paper.pdf for more

information on credit records, the credit reporting agencies, and furnishing. Creditors may choose to

furnish in part to provide borrowers an additional incentive to repay loans on time and in partto attract

consumers who wish to improve their credit score. Creditors may choose not to furnish in part because

doing so is costly and because doing so may provide information to potential competitors.

15

In one survey of BHPH dealerships, 64 percent of respondents reported that they furnished information

on their loans to the NCRAs. See

https://www.niada.com/uploads/dynamic_areas/hsS0Fy3eBfivoyCWHvwG/34/EquifaxPresentation_Cr

editReportingBestPractices.pdf.

9

month-(new or used vehicle)-(credit score bin) level.

16

They include many useful variables we

analyze below, including within-bin means of loan amount, vehicle value, loan term, interest

rate, monthly payment, and LTV. Within a bin, values drawn from vehicle registration

information, such as the vehicle value, represent all observations in that bin. In general, values

drawn from credit record information, such as the loan term or amount, represent only

observations in that bin that were furnished. For example, if a bin has ten loans, of which five

were furnished, then information on the vehicle values in that bin will reflect the values for all

ten loans in that bin, while information on the loan amount in that bin will reflect only loan

amounts for the five loans furnished. Importantly however, because credit scores are drawn

from credit record data at the consumer level, not the loan level, they are also available even for

loans that are not furnished. This is important because it means in Section 4 we can compare the

credit scores of consumers whose loans are not furnished to those of consumers whose loans are

furnished.

The data also include information on lender type, placing auto lenders into one of the five

generally used categories: banks, credit unions, captives, other finance companies, and BHPH

dealerships. However, the data also include an “Other” category of lenders that Experian could

not categorize in more detail. We manually categorized the lenders in this category ourselves.

17

Most were BHPH dealerships, and many of the rest fell into the four other traditional categories.

However, some were alternative lenders placing liens on a vehicle (and therefore appearing in

the data) for loans not used to purchase that vehicle. This alternative category includes auto title

lenders, pawnshops, bail bonds companies, and auto repair shops.

18

Loans from these kinds of

lenders were dropped from the data. We did not have sufficient information to categorize a

small number of lenders in the “Other” category. More importantly, the data do not include

information on the lender or lender type for bins with less than three observations. Thus, there

is a fairly large category of observations in the AutoCount

®

data with missing lender type.

16

Credit score bins have left endpoints divisible by 20, so there is one bin for borrowers with a credit score

from 580-599, another for borrowers with a credit score between 600-619, etc.

17

The main rules we used to do so are (1) to label a lender as a BHPH dealership if its name is similar

enough to the dealer name, (2) to label a lender as a BHPH dealership if its website makes clear that it

sells vehicles, and (3) to label a lender as a finance company if it is not a bank, credit union, or captive,

and its website makes clear that it finances sales for a number of dealerships.

18

Auto repair shops will sometimes repair a vehicle for a consumer who cannot pay upfront and extend a

loan for the repairs secured by the vehicle.

10

3.2. CCP data on loans at origination and after

The other data source used for this report is the Consumer Financial Protection Bureau’s

Consumer Credit Panel (CCP). The CCP is a longitudinal 1-in-48 sample of de-identified credit

records from one of the three NCRAs. Importantly, because the CCP is longitudinal, it allows us

to study loan performance over time. The sample includes approximately six million credit

records representing the universe of approximately 300 million credit records. Historically, the

CFPB has received updated credit records for all sampled credit records on a quarterly basis.

The records include information about the credit accounts included in each consumer’s credit

record (such as auto loans, mortgages, credit cards, student loans, and other bank installment

loans) as well as the borrower’s geography (census tract), credit score, and birth year. Note that

data from the CCP are not and cannot be matched to data from AutoCount

®

; we analyze the two

datasets separately.

We begin by taking auto loans originated from 2014 through 2016. We focus on this time period

so that we can track loan performance for three years after loan origination without using data

from 2020, i.e. when auto loan performance was heavily affected by the COVID-19 pandemic.

Data on the loan at origination are taken from the CCP records from the quarter in which the

loan is originated, which may reflect the status of the loan several weeks after it is actually

opened. For many variables that do not change, such as the original loan amount, loan term, and

inferred interest rate, this small timing gap is not a concern.

19

However, soon after the loan is

originated, credit scores may reflect the effects of shopping for or obtaining a car loan or even

early loan delinquency. Therefore, to proxy for a borrower’s credit score at origination, we use

the borrower’s credit score from the quarter before the loan is originated. So that data on credit

scores is as close to origination as possible, and because new auto loans can take several weeks

to appear in the data for reasons that may be correlated with the variables we study, we use data

on originations only from the first month of every quarter.

20

Therefore our data cover auto loans

originated in January, April, July, and October of 2014, 2015, and 2016. Performance data are

taken 12 quarters after the originations data. Therefore, for auto loans originated in January

2014, we use performance data reported in Q1 2017, which reflects the status of the loan around

19

We do not directly observe interest rates on auto loans in the CCP. However, we can impute them using

data we do observe on monthly payments, loan amounts, and loan terms.

20

In Appendix A, we show that loans for consumers with lower credit scores do indeed take longer to

appear in the data, but that using data only from the first month of every quarter allows enough time for

nearly all loans to appear in the data and so largely addresses this issue.

11

March 2017. Unless otherwise noted, in this report we restrict our attention to consumers with

credit scores at origination of 620 or less, which is one common definition of “subprime”.

21

An important limitation of the CCP for the purposes of this study is that, while it has very rich

information on the auto loans themselves, it has no information on the vehicles securing the

loans. For example, it is possible that BHPH loans are used for cars that are less valuable than

loans from banks that otherwise appear comparable. To a limited extent we can study this issue

in the AutoCount

®

data in Section 4, since the AutoCount

®

data include information on vehicle

values and whether they are new or used.

21

The non-subprime market is fundamentally different from the subprime market in many ways and so

we do not compare outcomes across lender types for non-subprime consumers. For example, in our data

the combined market share of finance companies and BHPH dealerships is nearly 40% in the subprime

market but is less than 5% in the non-subprime market.

12

4. Market overview

In this section, we study subprime auto loans at the time of origination in both the Experian

AutoCount® data and in the CCP. We separately analyze “small” and “large” finance companies

and “small” and “large” BHPH dealerships.

22

We do this because, as shown later in this section,

furnishing rates for small finance (BHPH) companies are much lower than those for large

finance (BHPH) companies. Analysis using NCRA data and combining all finance (BHPH)

companies into one group would place artificially high weight on large finance (BHPH) lenders,

which could lead to incorrect conclusions. Also, for the sake of clarity, the rest of this report

capitalizes lender types. For example, later in this report we compare Bank borrowers to Small

BHPH borrowers.

4.1. Market overview with AutoCount®

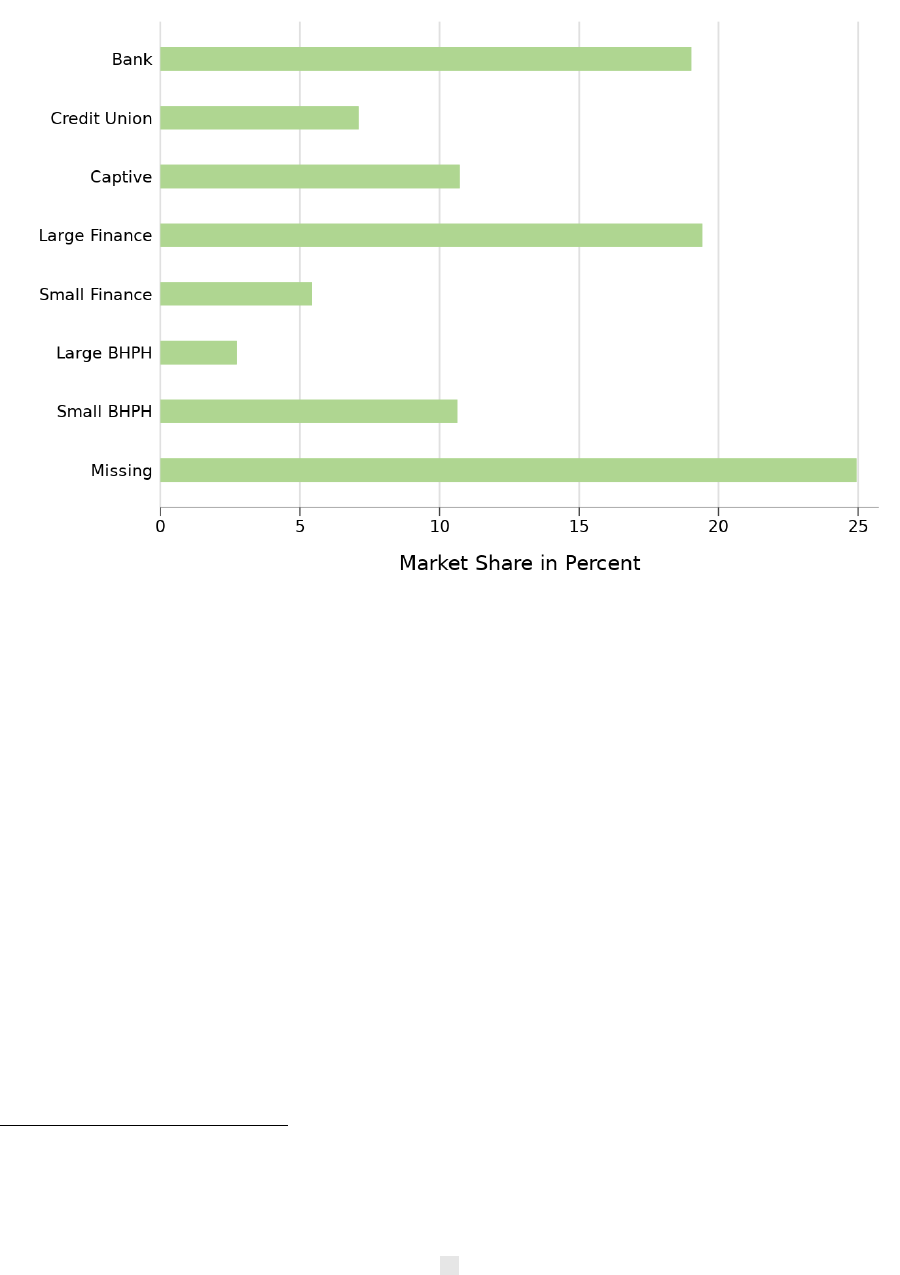

We begin with the Experian AutoCount® data. Figure 1 displays the subprime market shares of

the various lender types in the AutoCount® data. 24.9 percent of subprime loans are missing

lender type. This is because 0.1 percent of loans are from lenders that could not be categorized,

and 24.8 percent of loans are in bins with fewer than three observations.

22

For both finance companies and BHPH dealerships, a few lenders have substantial market share, but

most do not. We call a finance company “large” if it is in the top 80 of finance companies by market share,

and small otherwise. We define a BHPH lender as large if it is in the top 30 of BHPH lenders by market

share, and small otherwise. Both of these cutoff values are roughly where the marginal “large” lender has 1

percent of the market share of all the smaller lenders combined (and much less than 1 percent of the

market share of all the larger lenders combined). In other words, the smallest “large” lender is small

relative to both the smaller lenders combined and the larger lenders combined. This means the results are

robust to reasonable changes in the cutoff values.

13

FIGURE 1: SUBPRIME MARKET SHARE BY LENDER TYPE

Next, we study, to the extent possible, how borrowers, loans, and vehicles differ across lender

types in the AutoCount® data. Recall that the AutoCount® data are not at the individual-loan

level, but instead are aggregated to the dealer-lender-month-(new or used vehicle)-(credit score

bin) level. Out of necessity, for every variable we treat every observation in a bin as having the

observed mean of that variable in that bin. For example, one bin with ten loans may have five

loans securing a vehicle worth $7,500 and five loans securing a vehicle worth $12,500. We only

observe that the average vehicle value in that bin is $10,000, and so the analysis below will treat

the data as if every vehicle in that bin is worth $10,000.

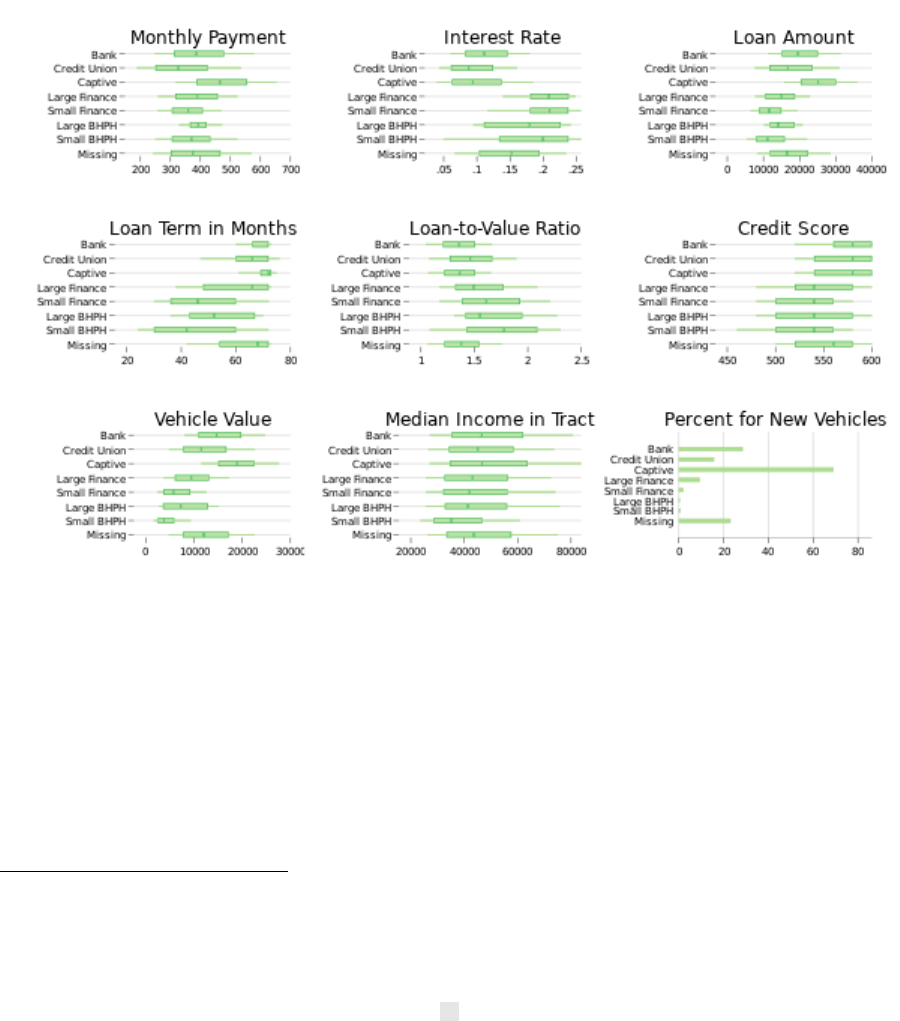

We begin with AutoCount® data that are available for all observations whether information on

the loans is furnished or not: bin-level observations of credit score, vehicle value, and the

percent of loans for new vehicles, as well as the median household income in the dealer’s (not

borrower’s) census tract.

23

For most variables, Figure 2 shows the 25

th

to 75

th

percentiles (thick

23

AutoCount® has data on the dealer’s zip code, which is matched to data on income by census tract from

the American Community Survey. Our AutoCount® data do not have information on borrowers’ income

or locations.

14

boxes) as well as the 10

th

and 90

th

percentiles (thin boxes)and the median (dark green line).

24

The figure also shows the percent of loans that are for new vehicles at each type of lender.

FIGURE 2: SUBPRIME LOAN OBSERVABLES BY LENDER TYPE

Figure 2 shows that there are substantial differences in borrowers and vehicles across lender

type. Vehicles securing subprime loans from Captives are notably different from other vehicles:

they are typically more valuable and are much more likely to be new. Bank and Credit Union

borrowers typically have higher credit scores than Finance and BHPH borrowers, and their

loans are for more valuable vehicles. Small Finance and Small BHPH borrowers have even lower

credit scores and buy less valuable cars than Large Finance and Large BHPH borrowers. Data on

income in dealers’ census tracts are a noisy measure of borrowers’ creditworthiness, but they

also indicate that Small Finance and Small BHPH borrowers are in general less creditworthy

than other borrowers.

24

Recall that credit scores are in bins of 20: 600-619, 580-559, etc. The figure shows the lower bound for

a bin, and consumers with credit scores above 619 are not considered subprime and so are not included in

the figure. Therefore 600 is the highest value in the data for subprime consumers. This is why it is the

highest value shown in Figure 2 as well as why so many Bank, Credit Union, and Captive borrowers have

that value in the data.

15

However, there is also some overlap in the distributions. For example, the 90

th

percentile of

Small Finance and Small BHPH borrowers have significantly higher credit scoresthan the 10

th

percentile of Bank and Credit Union borrowers. This may indicate that some Finance and BHPH

borrowers could have obtained loans instead from a Bank or a Credit Union. It may also indicate

that some Finance and BHPH borrowers are genuinely comparable to some Bank and Credit

Union borrowers, which is important for interpreting results presented later.

4.2. Comparing furnished and non-furnished loans

As already discussed, the AutoCount® data have several other informative variables, but these

are only available for furnished loans. The CCP, used later, also only has data for furnished

loans. Therefore, we now turn towards understanding, to the extent possible, how furnished

loans differ from loans that are not furnished, and how this varies across lender types.

In the AutoCount® data we observe the number of auto loans in each bin as well as the number

of auto loans successfully matched to an auto loan on a credit record. The ratio of the latter to

the former should be a good proxy for the fraction of auto loans that were furnished.

25

Figure 3

below shows the percent of subprime loans “furnished” by lender type, where “furnished” is

defined using the proxy.

25

A match could be unsuccessful, even if the data are furnished, if the data are not furnished by the time

the match is attempted or if the data are not furnished correctly (e.g. the loan is reported as an installment

loan and not an auto loan). Appendix A examines furnishing delays and how they may affect successful

match rates.

16

FIGURE 3: PERCENT OF SUBPRIME LOANS “FURNISHED” BY LENDER TYPE

Consistent with conventional wisdom, Banks, Credit Unions, and Captives all furnish data at

very high rates. As discussed in Appendix A, for these lender types furnishing delays appear able

to explain nearly all of the failed matches in our proxy, meaning that for these lender types

furnishing rates are nearly 100 percent. However, again consistent with conventional wisdom,

Small Finance and Small BHPH lenders furnish at far lower rates.

The very low furnishing rates of Small Finance and Small BHPH lenders means that loans

furnished by those lender types may differ in important ways from all loans originated by those

lender types. To understand how furnished loans differ from all loans for Small Finance and

Small BHPH borrowers, Figure 4 shows the 25

th

to 75

th

percentiles (thick boxes) as well as the

10

th

and 90

th

percentiles(thin boxes)and the median (dark green line) of the same variables as

in Figure 2.

26

Because Figure 3 showed that loans from Large Finance (BHPH) lenders are far

more likely to be furnished than loans from Small Finance (BHPH), Figure 4 also shows this

26

Figure 4 does not show the percent of loans for new vehicles because very few loans from Small Finance

and Small BHPH lenders are for new vehicles, whether they are furnished or not. Only roughly 2 percent

and .6 percent of furnished loans for Small Finance and Small BHPH lenders, respectively, are for new

cars. For all loans from Small Finance and Small BHPH lenders, the numbers are .7 percent and .1

percent, respectively.

17

information for lender size in annual loan volume. Again, recall that the AutoCount® data are

not at the individual loan level, but instead are aggregated to the dealer-lender-month-(new or

used vehicle)-(credit score bin) level. This means that Figure 4 examines differences in

observable characteristics across bins, but not within them.

FIGURE 4: SUBPRIME LOAN OBSERVABLES BY FURNISHED STATUS

Figure 4 shows that furnished loans tend to be for higher credit score consumers and for more

valuable cars. Therefore, in the analysis that follows using furnished loans, our sample of Small

Finance and Small BHPH borrowers is likely to be more creditworthy than Small Finance and

Small BHPH borrowers overall. Perhaps surprisingly, while as shown in Figure 3 loans from

Large Finance (BHPH) lenders are far more likely to be furnished than loans from Small

Finance (BHPH) lenders, within Small Finance and Small BHPH loans it does not appear to be

the case that furnished loans are from larger lenders than non-furnished loans.

18

4.3. Studying furnished loans in AutoCount®

Next, we study how all variables available in the AutoCount® data vary by lender type,

weighting bins by the number of furnished loans they contain. For most variables, Figure 5

shows the 25

th

to 75

th

percentiles (thick boxes) as well as the 10

th

and 90

th

percentiles (thin

boxes) and the median (dark green line).

27

The figure also shows the percent of loans that are for

new vehicles at each type of lender.

FIGURE 5: SUBPRIME LOAN OBSERVABLES FOR FURNISHED LOANS BY LENDER TYPE

Figure 5 shows that, even focusing on borrowers with loans that are furnished, Bank and Credit

Union borrowers in general appear more creditworthy than Finance and BHPH borrowers. For

example, they have higher credit scores and lower LTVs. However, there is also overlap in the

distributions. For example, the 90

th

percentile of Small Finance and Small BHPH borrowers

have credit scores about 60 points higher than the 10

th

percentile of Bank borrowers. There are

27

Recall that credit scores are in bins of 20: 600-620, 580-600, etc. The figure shows the lower bound for

a bin, and consumers with credit scores above 620 are not considered subprime and so are not included in

the figure. Therefore 600 is the highest value in the data for subprime consumers.

19

also substantial differences in interest rates across lender types. Later we will explore the extent

to which these differences in interest rates can be explained by differences in default risk.

4.4. Studying furnished loans in the CCP

Finally, we examine how observables differ across lender types in the CCP. Recall that the CCP is

constructed from information furnished by lenders and so includes only furnished loans.

28

Unlike AutoCount®, data in the CCP are available at the individual-loan level. Figure 6 shows

the 25

th

to 75

th

percentiles (thick boxes) as well as the 10

th

and 90

th

percentiles (thin boxes) and

the median (dark green line) of selected variables. The figure also shows the percent of

borrowers at each type of lender that have mortgages, as well as the percent of borrowers with a

co-borrower or co-signer.

28

The CCP does not separately identify captives from other finance companies. Captives are notable for

being large and for offering a large number of loans at very low interest rates. Therefore, we define

captives in the CCP as finance companies that are in the top 100 by market share and with at least 5

percent of loans with an interest rate of less than 1 percent.

20

FIGURE 6: SUBPRIME LOAN OBSERVABLES BY LENDER TYPE IN THE CCP

Figure 6 shows again that Bank and Credit Union subprime borrowers are generally more

creditworthy than Small Finance and Small BHPH subprime borrowers. However, again there is

overlap in the distributions. A large number of Small BHPH borrowers are measured to have

very low interest rates, which may be a data or credit reporting issue.

29

However, it may also in

part reflect that BHPH dealerships, unlike other lender types, control the price of the vehicle as

well as the interest rate on their loan. In many cases BHPH dealerships may be indifferent

between charging consumers for the car or the loan and so may charge a below-market interest

rate in exchange for an above-market vehicle price.

30

29

The interest rate issue appears to exist in the AutoCount® data too. In that data, the 5

th

percentile of

interest rates for Banks, Small Finance, and Small BHPH loans is .05, .04, and .01, respectively. However,

the AutoCount data are aggregated into bins while the CCP data are not, which may explain why the CCP

data include more surprisingly low interest rates.

30

For evidence that BHPH dealerships do sometimes charge a comparatively low interest rate in exchange

for a high vehicle price, see Brian Melzer and Aaron Schroeder, 2017, “Loan Contracting in the Presence of

Usury Limits: Evidence from Automobile Lending”, available at

https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2919070.

21

5. Are interest rates explained

by default risk?

Section 4 showed that there are large differences in the interest rates charged by different types

of auto lenders. Since interest payments might compensate lenders for default risk, one

hypothesis is that these differences can be entirely explained by differences in the default risk of

loans across lender types. This section examines this hypothesis. Other possibilities, such as

that different lender types evaluate risk in different ways or that different lender types suffer

different losses from default, are discussed in Section 6. Since borrowers’ ex-ante default risk is

unobservable, we use borrowers’ ex-post default outcomes to proxy for it.

31

As described in

Section 3, delinquency is measured roughly 38 months after origination.

5.1. Defining “default risk” in our data

In the CCP an auto loan may be delinquent in many ways, ranging from 30-day delinquency to

terminated with a repossession. Borrowers who become 30-days delinquent typically make up

their delinquent payment and get current again with almost no loss to the lender, and so 30-day

delinquency may not be useful for studying the effects of default risk on interest rates. More

serious measures of delinquency could imply greater expected losses for the lender and so likely

have a greater impact on interest rates, but they have the disadvantage that they reflect not only

the probability that a borrower becomes delinquent but also the lender’s behavior in response to

that delinquency. For example, one lender may prefer to cooperate with delinquent borrowers to

maximize the chance they become current on their own. Another lender may prefer to repossess

vehicles quickly. Even if these two lenders have borrowers that are otherwise identical, loans

from the latter lender are likely to ultimately end in repossessions at a higher rate if

repossessions have a causal negative effect on the probability a delinquent borrower becomes

31

For a discussion of how one large subprime auto lender uses default outcomes to predict default risk,

see Mark Jansen, Hieu Nguyen, and Amin Shams, 2021, “Rise of the Machines: The Impact of Automated

Underwriting”, available at https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3664708. For a recent

discussion of how economists use default outcomes to proxy for default risk when studying discrimination

in lending markets, see Alexander W. Butler, Erik J. Mayer, and James Weston, 2021, “Racial

Discrimination in the Auto Loan Market”, available at

https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3301009.

22

and stays current.

32

In Section 6, we present suggestive evidence that different lender types

respond to borrower default in different ways, and so this is an important issue.

To balance these concerns, we investigate two specific definitions of default. We define “60-day+

delinquency” as a borrower everexperiencing 60-day delinquency or anything worse, i.e.

including voluntary and involuntary vehicle repossessions, chargeoffs, collections, and

bankruptcies.

33

This definition of default is useful because lenders rarely initiate vehicle

repossessions before a borrower becomes at least 60 days delinquent. Therefore, 60+ day

delinquency is a useful outcome measure that is determined mostly by borrower behavior. The

other definition of default we consider is 90-day+ delinquency, which we define as a borrower

everexperiencing 90-day delinquency or anything worse. This definition is useful because most

lenders will consider a loan that is 90 days delinquent to be in serious trouble and likely not to

be paid in full. The choice whether to work with the borrower and hope they can become current

on the loan, to repossess the vehicle, to initiate collections, etc. will vary from lender to lender as

well as from borrower to borrower. Therefore, the disadvantage of 90-day+ delinquency is that

it is in part a measure of lender behavior as well as borrower’s creditworthiness.

34

However, the

advantage of 90-day+ delinquency is that it is likely more useful from the lender’s underwriting

perspective. Many loans that become 60 days delinquent are ultimately paid in full.

In this section we study auto loan default rates (an ex-post measure of loan performance that we

observe) to learn about auto loan default risk (an ex-ante measure of expected loan performance

that we do not observe). However, if the macroeconomic environment deteriorates rapidly and

unexpectedly (as it did at the beginning of the COVID-19 crisis), then borrowers will likely

default at higher rates than their default risk, evaluated ex-ante, would indicate. This is the

main reason that in this report we only study auto loans originated between 2014 and 2016; this

restriction ensures we study auto loan performance between 2014 and 2019, a generally stable

macroeconomic period in which actual macroeconomic performance did not deviate

substantially from expectations. During this period auto loan default rates are likely a very good

proxy for auto loan default risk, but this caveat should be kept in mind.

32

For evidence that repossessions after delinquency have a negative causal effect on borrowers’ future

credit outcomes, see Elizabeth Berger, Alexander W. Butler, andE rik J. Mayer, “Credit Where Credit Is

Due: Drivers of Subprime Credit”, 2018, available at http://dx.doi.org/10.2139/ssrn.2989380.

33

A “voluntary repossession” occurs when the borrower returns the vehicle to the lender, perhaps in

response to communications from the lender. An “involuntary repossession” occurs when the lender,

possibly through a third party, repossesses the vehicle without the permission of the borrower.

34

This is also why we include e.g. a borrower who becomes 60-days delinquent and becomes current in

our measure of 60-day+ delinquency. For example, if borrowers A and B in that group have identical

probabilities of becoming current on their own, but borrower A’s vehicle is repossessed quickly by the

lender and B’s is not, it would otherwise appear that borrower A was riskier.

23

5.2. How does default risk vary across lender types?

Subprime auto loans carry substantial default risk; roughly 27 percent of our subprime CCP

sample is 60-day+ delinquent. Different lender types specialize in different amounts of default

risk. Finance companies and BHPH dealerships typically specialize in the riskiest loans, while

Banks and Credit Unions generally specialize in the least risky loans. Therefore, we would expect

delinquency rates to vary across lender type.

First, we examine how 60-day+ delinquency risk varies across lender type. We are interested in

understanding whether delinquency risk varies across characteristics we can observe in the CCP

(such as credit score), as well as across characteristics we cannot observe (such as income).

Therefore, Figure 7 plots 60-day+ delinquency risk by lender type, in three ways.

The green dots plot unconditional default rates by lender type. The figure shows that there is

considerable variation in default rates across lender types, and that this variation is mostly as

expected. For example, the figure shows that the 60-day+ delinquency rate for Small Finance

borrowers in the sample is very high, nearly 40 percent. For bank borrowers, it is only slightly

more than 15 percent. Large BHPH borrowers and Small Finance borrowers are comparable in

default risk to each other and are substantially riskier than Small BHPH borrowers and Large

Finance borrowers, who are comparable in risk to each other and to Captive borrowers. It is

likely that the comparatively low default rate of Small BHPH borrowers is at least partly due to

the fact that Small BHPH borrowers whose loans are furnished are less risky than Small BHPH

borrowers overall (see Figure 4). However, Small Finance borrowers whose loans are furnished

are also less risky than Small Finance borrowers overall (again, see Figure 4), making their

comparatively high default rate more of a puzzle. Bank and Credit Union borrowers have the

lowest default rates.

The orange dots plot our average predicted 60-day+ delinquency rates after accounting for

differences in control variables by lender type.

35

For example, the decline in 60+ day

delinquency rates for Small Finance borrowers from roughly 40 percent without controls to

roughly 30 percent with controls means that the regression predicts that the default rates for

Small Finance borrowers would fall by roughly 10 percentage points, if instead of having the

observables that Small Finance borrowers have in the data (such as credit score), Small Finance

35

We used a logit regression to predict delinquency rates. The logit model is described in Appendix B. The

controls in the regression include credit score, age, whether the borrower has a mortgage on their credit

report, whether there is a co-borrower or co-signer on the loan, and lender type fixed effects. We also

considered including credit scores from previous years, the logarithm of median household income in the

borrower’s census tract, the percent of people in the borrower’s census tract with high school and college

degrees, and local market shares of the various lender types in the regressions, but these controls are not

available for all observations so we do not include them.

24

borrowers had the observables that all borrowers have in the data. Our controls explain some

but not most of the variation in default risk across lender types in the data. Potential

explanations for the remaining variation in default risk across lender types include (but are not

limited to) differences in income levels, income variation, down payments, access to liquid

assets, access to other forms of credit, financial sophistication and defaults costs across

borrowers, differences in business practices when originating and servicing loans across lenders,

and differences in quality and depreciation rates across financed vehicles.

The blue dots are the same as the orange dots, except restricting both the regression and the

sample to consumers with credit scores of at least 560 (“shallow subprime”). For example, the

regression predicts that the 60-day+ delinquency rate for the Small Finance borrowers in our

shallow subprime sample would be around 28 percent if they had the observables of all shallow

subprime borrowers in the data and not of shallow subprime Small Finance borrowers.

Restricting the sample to shallow subprime borrowers, and including control variables, explains

enough of the variation for comparisons across lender types to be meaningful. With controls,

shallow subprime Small BHPH borrowers appear comparable in default risk to shallow

subprime Bank and Credit Union borrowers, while shallow subprime Small Finance and Large

BHPH borrowers appear comparable in default risk to shallow subprime Large Finance

borrowers. However, even in the shallow subprime market, borrowers from Captives, Large

Finance, Small Finance, and Large BHPH lenders appear to be significantly riskier than Bank

and Credit Union borrowers for reasons we cannot observe in the CCP.

Our regressions account for uncertainty in our findings. In the figures, the bands around the

dots indicate 95 percent confidence intervals. For example, roughly speaking, our regression is

95 percent confident that the 60-day+ delinquency rate for the Small Finance borrowers in our

shallow subprime sample would be between about 25-31 percent if they had the observables of

all shallow subprime borrowers in the data and not of shallow subprime Small Finance

borrowers.

36

36

A more formal definition of these confidence intervals is as follows. Suppose we were to repeat the

procedure in Figure 7 N times, where N is a natural number, each time usinga different dataset that is

equivalent in size and quality to the one we use. For each estimate shown (e.g. the 60-day+ delinquency

rate for shallow subprime Small Finance borrowers if they had the observables of all shallow subprime

borrowers in our data), each repetition of the procedure would yield a different confidence interval,

because of the different data used. Then, under the assumptions used in the logit model (described in

Appendix B), asN grew larger and larger the percent of confidence intervals calculated in this way that

included the true, unknown value being estimated would approach 95 percent.

25

FIGURE 7: 60-DAY+ DELINQUENCY RISK BY LENDER TYPE

Figure 7 suggests that, when compared to the raw data, default risk does not vary as much

across lender types when we condition on the variables we can observe. However, they do not

show whether observationally similar borrowers do indeed obtain loans from different lender

types. For example, it could be the case that all Small BHPH borrowers are observably riskier

than all Bank borrowers. Next, we investigate whether this is true.

Figure 8 plots the cumulative density functions of estimated 60-day+ delinquency risk by lender

type.

37

For a given level of default risk (on the x-axis), the cumulative density (on the y-axis)

shows the estimated fraction of borrowers at that lender type with lower default risk. For

example, the figure shows that over 90 percent of Credit Union borrowers are estimated to have

less than a 20 percent chance of 60+ day delinquency, while fewer than 5 percent of Small

Finance borrowers do.

37

We use a logit regression with the same controls as before to predict 60+ day delinquency. The logit

model is described in Appendix B. Note that these controls include lender fixed effects, which should

effectively control for delinquency risk that varies across lender types for reasons we do not observe.

26

FIGURE 8: DISTRIBUTION OF PREDICTED DEFAULT RISK, BY LENDER TYPE

There are large and predictable differences in the distributions. Bank and Credit Union

customers on average have the lowest default risk. All of the other lender types appear to

provide loans to many consumers with a default risk greater than 20%, who would likely have

difficulty obtaining a loan from a Bank or Credit Union. Small Finance and Large BHPH

customers are the highest risk. Large Finance companies appear to have large numbers of

customers with both fairly low and fairly high risk. However, there is also substantial overlap in

the distributions. For example, roughly 30 percent of Small BHPH borrowers have estimated

default risk less than 20 percent; roughly 20 percent of Bank borrowers have estimated default

risk above this number. This may indicate that many of these less risky Small BHPH borrowers

could have obtained a loan from a Bank. Similarly, many Large BHPH and Small Finance

borrowers appear less risky than many Large Finance borrowers.

5.3. How do interest rates vary across lender types?

As shown in Figures 5 and 6, subprime auto loans vary substantially in their interest rates. High

interest rates may compensate lenders for bearing risk, and so higher-risk consumers should be

27

expected to pay higher interest rates. Figures 7 and 8 show that there are large differences in

consumers’ default risk across lender type. Lenders with higher-risk borrowers should be

expected to charge those borrowers higher interest rates, and so interest rates should vary with

default risk across lender types. However, interest rates may also vary across lender type for

reasons besides default risk. Potential reasons for this variation include (but are not limited to)

other prices relevant to borrowers (such as the price of the vehicle), borrowers’ bargaining

power and financial sophistication, lenders’ losses from delinquency, underwriting ability, and

willingness and ability to extract revenue from borrowers, and (for indirect loans) dealers’

willingness and ability to mark up loan interest rates over and above what the lender is willing to

offer.

Next, we investigate how interest rates vary across lender types. Figure 9 performs the same

analysis as Figure 7, but with interest rates as the outcome of interest rather than default rates.

38

Because default is not the outcome variable, we can now also include actual default outcomes in

the regression. Here we are most interested in the default risk that lenders use for underwriting,

so we use 90-day+ delinquency risk rather than 60-day+ delinquency risk. Controlling for actual

default outcomes provides evidence on whether variation in 90-day+ delinquency risk that

cannot be explained by the default regression, which could for example arise from unobserved

differences in borrower incomes or vehicle values, can explain variation in interest rates. The

fourth set of points, colored brown, does this for the shallow subprime sample.

38

Since interest rates (a continuous variable) are the outcome of interest, rather than delinquency (a

binary variable), we run an Ordinary Least Squares (OLS) regression rather than a logit regression to

predict interest rates. The OLS model is described in Appendix C.

28

FIGURE 9: INTEREST RATES BY LENDER TYPE

Interest rates vary with default risk across lender types in some ways that are intuitive. Bank

and Credit Union borrowers, who are the least risky, pay the lowest interest rates. However,

some differences in interest rates across lender types do not seem to be fully explained by

default risk. Captive borrowers pay interest rates comparable to those of Bank and Credit Union

borrowers, despite having default risk comparable to those of Large and Small Finance

borrowers. This may be because their loans are often secured by newer and more valuable

vehicles, or because the business model of captives is, in part, to subsidize loans in order to

increase vehicle demand.

39

Even though shallow subprime Small BHPH borrowers have similar

risk to observationally comparable Bank and Credit Union borrowers, they pay notably higher

interest rates. Similarly, shallow subprime Small Finance and Large BHPH borrowers pay

substantially higher interest rates than observationally similar Large Finance borrowers, even

though their default risk is comparable. These statements are true even after controlling for

actual default outcomes, as the brown points do. In general, variables we can observe in the data

39

We showed in Section 4 that vehicles securing loans from captives are in general more valuable than

vehicles securing loans from other lender types at the time the vehicle is purchased. What matters for the

pricing of delinquency risk is vehicle value at the time of default, not at the time of purchase, because this

is what affects the lenders’ losses from delinquency. It seems likely that vehicles securing loans from

Captives are also more valuable than other vehicles at the time of default, though we cannot test this.

29

explain less of the variation in interest rates than the variation they explain in default rates. This

suggests that interest rates may vary across lender types for reasons beyond default risk.

The differences in interest rates shown in Figure 9 are quantitatively large. A borrower with the

median loan term and loan amount for Small BHPH borrowers in AutoCount® would save

roughly $894 over the life of a loan if she could reduce her interest rate from 13 percent (roughly

the brown point for Small BHPH borrowers) to nine percent (roughly the brown point for Bank

borrowers). A borrower with the median loan term and loan amount for Small Finance

borrowers in AutoCount® would save roughly $1,348 over the life of a loan if she could reduce

her interest rate from 18 percent (roughly the brown point for Small Finance borrowers) to 13

percent(roughly the brownpoint for Large Finance borrowers.)

40

40

As noted in the introduction, this estimate does not necessarily imply that a specific borrower could

save $1,348 by switching lender types because these estimates are not causal and there are variables we do

not observe and so cannot control for (such as financing fees).

30

6. Discussion and suggestions

for future research

The previous section provided evidence that there is variation in interest rates across lender

types that cannot be explained by default risk. This raises a critical question: why else do

interest rates vary across lender types? The limitations of our data mean we must leave a

definitive answer to this question to future research. But this section discusses potential

explanations for our results and provides some useful clues to distinguish between them.

6.1. Some potential explanations for variation in

interest rates

An important possibility for why interest rates vary across lender types is that a given level of

default risk poses a greater risk to, for example, the profits of Small BHPH lenders than it does

for Banks. For example, more Bank borrowers that are 90+ days delinquent could still become

current than otherwise comparable 90+ day delinquent Small Other borrowers. Moreover, in

Section 4 we showed in the AutoCount® data that the vehicles securing Small BHPH loans are

in general less valuable at loan origination than the vehicles securing Bank loans. This may

mean that vehicle repossessions may recover less of the loan amount for Small BHPH lenders

than for Banks.

41

Small BHPH lenders may also recover less from consumers in collections than

Banks do. Repossessions or collections could be more expensive for Small BHPH lenders to

initiate than Banks, perhaps because their borrowers are more difficult to find after default or

because of local regulations. If any of the above are true, the loss given default for Small BHPH

lenders could be higher than it is for Banks. Therefore, a given level of delinquency would pose

more of a risk to Small BHPH lenders than to Banks, which in turn could explain why Small

BHPH borrowers pay higher interest rates than Bank borrowers with similar default risk. If this

kind of explanation is true, then it would have an empirical implication we can test in our data:

the difference between the interest rates paid by risky and less risky borrowers should be greater

for Small BHPH lenders than it is for Bank lenders.

A different set of explanations come from underwriting practices and funding structure. As

shown in Section 4, Banks and Credit Unions typically focus on the higher end of the subprime

41

Note in the previous section we could not control for vehicle value because it is not in the CCP data.

31

credit spectrum, which could mean they have the underwriting ability to separate risky

borrowers from less risky borrowers. Moreover, they typically hold the loans they originate, and

so may place greater value on low-risk loans. Conversely, as noted above, many Finance and

BHPH lenders explicitly advertise their willingness to lend to borrowers who appear quite risky.

This could give them less incentive to invest in underwriting to separate risky borrowers from

less risky borrowers, since they will lend to risky borrowers anyway, and so they may not be able

to offer lower interest rates to less risky consumers because they cannot identify them. BHPH

lenders profit from selling vehicles as well as financing them, so if a delinquency results in a

repossession, this gives them another chance to sell the vehicle which in turn may lower the loss

given default. Moreover, Finance and BHPH lenders often adopt technologies such as GPS

tracking devices and starter-interrupt devices that lower their costs when consumers default,

42

and these lenders may optimize their funding structure for the deep subprime market they

specialize in. These factors could raise the cost of issuing and servicing loans for consumers that

are not particularly risky but reduce the cost of issuing and servicing loans for especially risky

consumers. Finance and BHPH lenders may also have little incentive to offer their less risky

customers lower interest rates, since they may assume that if the consumer has approached

them that means they will be willing to pay the interest rates associated with riskier borrowers.

If this kind of explanation is true, then for example the difference between the interest rates paid

by risky and less risky borrowers should be smaller for Small BHPH lenders than it is for Banks.

Finally, interest rates may vary across lender types for reasons that have nothing to do with

delinquency risk. As depository institutions, Banks and Credit Unions have may have access to

cheaper funding than Finance or BHPH lenders, and so may be able to provide all customers

lower interest rates. If there are returns to scale in auto lending, then larger institutions may be

able to provide loans more efficiently and thus at lower interest rates than smaller institutions.

43

Captives and BHPH dealerships have financial incentives to originate loans beyond the interest

payments they generate, so they may simply offer more competitive interest rates for all

consumers in order to sell more vehicles. If this kind of explanation is true, then for example the

difference between the interest rates paid by risky and less risky borrowers should be roughly

the same for Small BHPH lenders as it is for Banks.

42

For example, see https://www.forbes.com/sites/kashmirhill/2014/09/25/starter-interrupt-

devices/#5466b0b07733.

43

For some evidence that this may be the case, see Constantine Yannelis and Anthony Lee Zhang, 2021,

“Competition and Selection in Credit Markets”, available at

https://anthonyleezhang.github.io/pdfs/competitionselection.pdf.

32

6.2. Delinquency risk premia by lender type

Section 6.1 provided a long, but not exhaustive, list of potential explanations for differences in

interest rates across lender types. Definitively distinguishing between these explanations is well

beyond what is possible in our data. However, as discussed in Section 6.1, these various

explanations can be placed into categories based on whether they predict that the difference in

interest rates paid by risky borrowers and less risky borrowers should be larger, smaller, or the

same across lender types. This is something we can investigate in our data.

To investigate which kind of explanation more closely fits the data, Figure 10 plots average

predicted interest rates, assuming borrowers have the lender type and ultimate delinquency

status shown, but the other observable characteristics of borrowers in the shallow subprime

sample.

44

For example, the figure shows that the average predicted interest rate for shallow

subprime Bank borrowers, if they had the observable characteristics of borrowers in the shallow

subprime sample and would not ultimately become delinquent, is roughly nine percent. The

figure also shows that the average predicted interest rate for shallow subprime Bank borrowers,

if they had the observable characteristics of borrowers in the shallow subprime sample and

would ultimately become delinquent, is roughly 11 percent. This is an indication that Banks

charge borrowers higher interest rates if they are riskier for reasons that are not observable in

our data. Captives and Large Finance companies also appear to charge borrowers higher interest

rates if they are riskier for reasons that are not observable in our data. By contrast, the interest

rate premium paid by borrowers at Credit Unions, Small Finance companies and BHPH lenders

(especially Small BHPH lenders) who ultimately become delinquent, relative to those who do

not ultimately become delinquent, is smaller. However, because Small BHPH lenders furnish at

very low rates as shown in Figure 3, the sample of Small BHPH loans in the data is not large and

so there is some uncertainty around this result for Small BHPH borrowers.

44

The OLS regressionis exactly the same as that used for the brown dots in Figure 8, except it does not

have separate fixed effects for lender type and delinquency status, but instead has fixed effects for lender

type interacted with delinquency status. The OLS model is described in Appendix C.

33

FIGURE 10: INTEREST RATES BY LENDER TYPE AND DEL

Figure 10 shows that the interest rate premium paid by borrowers who became delinquent,

relative to borrowers who did not become delinquent, is smaller (or at least not larger) at Small

Finance, Large BHPH, and Small BHPH lenders than at other lenders. This is suggestive

evidence in favor of the second and third category of explanations discussed in Section 6.1 for

the interest rates charged by these lender types, and against the first category of explanations

which predict that default is particularly costly for these kinds of lenders.

6.3. Servicing after delinquency by lender type

Next, we investigate how different lender types service delinquent loans. This may provide

another useful, if imperfect, method for distinguishing between the categories of explanations

discussed in Section 6.1. For example, if repossessions are more (less) difficult or expensive for

some lender types, then those lender types may be slower (faster) to repossess a vehicle after a

borrower becomes delinquent.

34

For this purpose, we restrict our attention to borrowers who ever become at least 30-days

delinquent on a loan, and we focus on the first time they do so. The goal is to examine whether,

two months after this delinquency, different lender types have either repossessed the vehicle or

started collections at different rates. We drop borrowers who are less than 90-days delinquent

two months after becoming 30-days delinquent, and place the remaining loans into one of four

categories: (1) still delinquent, (2) terminated by the borrower (through bankruptcy or a

voluntary repossession), (3) terminated by the lender through chargeoff or collections, and (4)

terminated by the lender through involuntary repossession of the vehicle.

45

Figure 11 shows the

percent of loans in each category by lender type.

FIGURE 11: LOAN STATUS TWO MONTHS AFTER FIRST DELINQUENCY

Figure 11 shows that Captives, Small Finance and Small BHPH lenders appear to terminate

delinquent loans more quickly than Banks or Credit Unions. For example, of loans that were at

least 90-days delinquent two months after becoming 30-days delinquent, nearly 30 percent of

45

Accounts can transition from bankruptcy or repossession to chargeoff or collections, if the lender

recovers less than the total loan amount outstanding. However, few accounts transition from 30-days

delinquent to bankruptcy or repossession, which means that this kind of transition rarely affects account

status two months after an account first becomes 30-days delinquent.

35

Small BHPH loans were terminated through an involuntary repossession while less than 20

percent of Bank loans were. Broadly, Figure 11 supports the same conclusion as Figure 10: loans

terminating in default do not appear to be more costly for lender types that charge higher

interest rates. Clearly, however, much more research on this topic is necessary.

36

7. Conclusion

This report shows that there are large differences in the auto loan borrowers served by different

lender types. For example, Banks and Credit Union customers are on average notably more

creditworthy, and pay lower interest rates, than Small Finance and Small BHPH borrowers.

However, there is also overlap in the distribution of observables across lender types. There are

Small Finance borrowers and Small BHPH borrowers that appear comparable to many Bank

and Credit Union borrowers.

We investigated the extent to which differences in borrower creditworthiness across lender

types could explain the differences in borrowers’ interest rates across lender types. After

controlling for the borrower characteristics that we observe, we found that Small BHPH

borrowers appeared comparable in default rates to Bank and Credit Union borrowers, while

Small Finance and Large BHPH borrowers appeared comparable in default rates to Large

Finance borrowers. However, Small BHPH borrowers still paid substantially higher interest

rates than observationally similar Bank and Credit Union borrowers. Small Finance and Large

BHPH borrowers paid substantially higher interest rates than observationally similar Large

Finance borrowers.

There are many potential explanations for these findings. While we cannot definitively

distinguish between them with our data, we described three classes of explanations for our

findings. First, a given amount of default risk could be more costly for one kind of lender than

another. Second, some lender types may differentiate between comparatively low-risk and high-

risk borrowers more than other lender types. Third, some lender types may be able to provide

better interest rates for their borrowers, regardless of default risk, than other lender types. We

present some suggestive evidence that provides more support for the latter two classes of

explanations.

This report sheds valuable light on an important market, but it has several limitations.

Addressing these could be a valuable path for future research. One limitation is that the results

we find are descriptive and do not establish a causal relationship. For example, we found that

Small BHPH borrowers pay higher interest rates than observationally similar Bank borrowers.

This could mean that these Small BHPH borrowers would have paid lower interest rates had

they obtained their loans from Banks. However, this relationship might also arise if, for

example, Small BHPH lenders attract borrowers who are not focused primarily on interest rates

and that Banks would also charge these borrowers relatively high rates.

Another important limitation is that, while we do observe interest rates and delinquency

outcomes, we do not observe many other factors that may be relevant for auto loan borrowers.

37

For example, borrowers often must pay substantial fees to obtain auto loans, and we cannot

study how fees vary across lender types. There are many other loan characteristics we cannot