July 2020July 2020

www.nrel.gov/usaid-partnership

Key Challenges and Potential Solutions

Distributed Solar Quality

and Safety in India

Authors

Arvind Karandikar, Nexus Energytech Pvt Ltd; Pune, Maharashtra, India

Ingrid Repins, Alexandra Aznar, and Carishma Gokhale-Welch, National Renewable Energy Laboratory;

Golden, CO USA

Ronnie Khanna and Devina Anand, Tetra Tech; Delhi, India

July 2020

A product of the USAID-NREL Partnership

Contract No. IAG-17-2050

Key Challenges and Potential Solutions

Distributed Solar Quality

and Safety in India

www.nrel.gov/usaid-partnership

NOTICE

This work was authored, in part, by the National Renewable Energy Laboratory (NREL), operated by Alliance for

Sustainable Energy, LLC, for the U.S. Department of Energy (DOE) under Contract No. DE-AC36-08GO28308. Funding

provided by the United States Agency for International Development (USAID) under Contract No. IAG-17-2050. The

views expressed in this report do not necessarily represent the views of the DOE or the U.S. Government, or any agency

thereof, including USAID.

This report is available at no cost from the National Renewable Energy Laboratory (NREL) at www.nrel.gov/publications.

U.S. Department of Energy (DOE) reports produced after 1991 and a growing number of pre-1991 documents are available

free via www.OSTI.gov.

Prepared by

Cover photo from iStock 956955560

NREL prints on paper that contains recycled content.

Acknowledgments

The authors thank Anurag Mishra from the U.S. Agency for International Development (USAID)-India

and Sarah Lawson from the USAID Office of Energy and Infrastructure for their support of this work. We

also wish to thank the following individuals for their detailed review comments, insights, and

contributions to this report: Andy Walker, Teresa Barnes, Andrea Watson, Adam Warren (National

Renewable Energy Laboratory [NREL]), Prakhar Goel, Rakesh Kumar Goyal, Ujjwal

Bhattacharjee (Tetra Tech), Akhilesh Magal (Gujarat Energy Management Institute [GERMI]), Omkar

Jani (Kanoda Energy Systems Pvt Ltd), Anjali Garg, and Brendon Mendonca (International Finance

Corporation).

The authors would also like to acknowledge and thank Britton Marchese, Isabel McCan, Terri Marshburn,

Liz Craig, Judy Powers, Liz Breazeale, Nathan Lee (NREL), Joginder Singh, and Yogeeta Sharma (Tetra

Tech) for their editorial and design support.

i

This report is available at no cost from the National Renewable Energy Laboratory (NREL) at www.nrel.gov/publications.

List of Acronyms

AC alternating current

BIS Bureau of Indian Standards

C&I commercial and industrial

CAPEX capital expenditure

CEA Central Electricity Authority of India

CEI Chief Electrical Inspectorate

CERC Central Electricity Regulatory Commission

CII Confederation of Indian Industry

DC direct current

Discom distribution company

DPV distributed photovoltaics

EL electroluminescence

EPC engineering, procurement, and construction

GERMI Gujarat Energy Research and Management Institute

IEC International Electrotechnical Commission

IECRE IEC System for Certification to Standards Relating to Equipment for Use in Renewable

Energy Applications

IEEE Institute of Electrical and Electronic Engineers

IIT Indian Institute of Technology

IP Intellectual Property

IP Ingress Protection

LID light induced degradation

LPS lightning protection system

MNRE Ministry of New and Renewable Energy, Government of India

MPPT maximum power point tracking

MQT module quality testing

NABCEP North American Board of Certified Energy Professionals

NEC National Electric Code

NGO nongovernmental organization

NISE National Institute of Solar Energy (India)

NREL National Renewable Energy Laboratory (U.S.A.)

NSM National Solar Mission

OD operational documents

OPEX operating expenditure

PID potential induced degradation

PPA power purchase agreement

PSU public sector unit

PV photovoltaic

QA quality assurance

QAF Quality Assurance Framework

R&D research and development

RESCO renewable energy service company

RTPV rooftop photovoltaic

SERC State Electricity Regulatory Commission

SLD single line diagram

SNA State Nodal Agency

SPD surge-protection device

TERI The Energy Resources Institute

TÜV TÜV Rhineland

ii

This report is available at no cost from the National Renewable Energy Laboratory (NREL) at www.nrel.gov/publications.

Executive Summary

In India, the quality and safety of solar photovoltaic (PV) systems—and their installation—have become a

concern for investors, regulators, consumers, and distribution companies (discoms). The lack of quality

standards and a push for low prices has led to the installation of poor-quality products and inferior system

design and execution on site (Devi et al. 2018). These low-quality systems deliver less energy than

expected and have a lower overall lifespan, which are serious issues for developers and investors whose

return on investment depends on the amount of power generated from these solar systems for the expected

life of the project. Equipment that does not conform to minimum quality standards also creates safety

risks for business and homeowners. Overall, both performance and safety concerns lower investor and

consumer confidence in solar products, threatening to slow market development, and are likely key

contributing factors in slowing rooftop photovoltaic (RTPV) installations in India, particularly small-

capacity systems (less than 100kW). Technical issues such as the absence of standards or monitoring

systems, and the penetration of inferior-quality products in the market hamper the performance of the

solar system and create a poor reputation for PV systems and the technology (Devi et al. 2018).

India is not alone; the solar quality and safety issues it faces mirror global experiences. Worldwide,

residential RTPV consumers are typically unable to distinguish between low- and high-quality systems.

RTPV system components vary in quality, and inadequate training leads to poor installation practices.

Many inspection checklists and certification procedures to rectify these issues are already available in

India, however, they are not always used because they are not mandatory, or the workforce is not aware

of them, or may not have the technical capacity to comply. Demonstrations of quality products and

installation practices are more effective if the information reaches the consumer in a clear way. A

successful approach to improving residential RTPV system quality is likely to include an assortment of

strategies by different stakeholders, as discussed later in this report.

This report provides solar quality and safety information and best practices that can help increase

confidence in RTPV in India, particularly for small-capacity systems, and thus accelerate the growth of

that sector. New data stemming from expert interviews and a stakeholder workshop shed light on

common quality and safety technical issues at various stages of an RTPV system’s life (Figure ES- 1) and

potential solutions for addressing them. To achieve the goal of a low-cost system with high energy yield,

best practices must be followed at each stage of system life.

iv

This report is available at no cost from the National Renewable Energy Laboratory (NREL) at www.nrel.gov/publications.

Figure ES- 1. Key RTPV quality and safety issues identified by stakeholders

Note: Common problems occur at all stages of an RTPV system’s life, as indicated by the vertical levels of the

pyramid. Issues that can result in a safety hazard or severe underproduction of energy are marked with colored

icons (see legend)

The new data and analysis are used to identify a prioritized approach to addressing the most common

RTPV issues. This approach takes the form of a quality-assurance framework comprising: 1) a Module

Quality Assurance program, 2) a Safety Quality Assurance program, and 3) a Vendor Rating Framework

(VRF) which are discussed further in Section 5 of the report. We propose that the development of a VRF

is likely the next best step to focus initial efforts to improve quality and safety of RTPV installations in

India. There are currently no mechanisms in place to monitor, evaluate, and rate vendors (engineering,

v

This report is available at no cost from the National Renewable Energy Laboratory (NREL) at www.nrel.gov/publications.

procurement, and construction contractors or installers) in India. Establishing a VRF would help measure

the quality of systems, as well as ensure compliance of those systems to established standards. As vendors

and suppliers are held accountable for component and installation quality using this framework, a VRF

would also provide an effective mechanism to link quality systems to market share by putting in place a

procedure to evaluate, rate, and certify vendors based on their track record of designing, developing, and

deploying systems.

vi

This report is available at no cost from the National Renewable Energy Laboratory (NREL) at www.nrel.gov/publications.

Table of Contents

Executive Summary.................................................................................................................................................. iv

1 Introduction ............................................................................................................................................................ 1

1.1 Solar Energy Targets and Growth in India .............................................................................2

1.2 Key Challenges of RTPV Deployment...................................................................................2

1.3 Key Stakeholders and Their Roles in Ensuring RTPV Quality and Safety ............................3

1.4 Rooftop Solar Implementation Models and their Impact on Quality and Safety....................4

1.5 Need for Quality and Safety Standards and Implementation Framework ..............................6

2 An International Perspective: U.S. and Other Global Experiences With Solar Quality and Safety Issues.... 7

2.1 Site Inspections.......................................................................................................................7

2.2 Standards for Systems—IECRE .............................................................................................9

2.3 Education and Developing Best Practices ............................................................................10

2.4 Industry-Wide Reports on Rooftop PV Quality....................................................................11

2.5 Looking Forward—Important Conclusions and Possible Paths ...........................................11

3 Research Methodology ......................................................................................................................................... 14

3.1 Literature Review..................................................................................................................14

3.2 Stakeholder Interviews: Methodology..................................................................................15

3.3 Stakeholder Workshop..........................................................................................................15

4 Key Findings: Quality and Safety Aspects of RTPV Systems in India ............................................................ 17

4.1 RTPV Project Development Cycle .......................................................................................17

4.2 Key Challenges in RTPV Quality and Safety.......................................................................18

4.2.1 System Design-Related Quality Issues .................................................................... 19

4.2.2 Component-Related Quality Issues.......................................................................... 20

4.2.3 Installation- and O&M-Related Quality Issues........................................................ 21

4.3 Key Drivers of Poor-Quality and Unsafe Systems ...............................................................23

4.3.1 Gaps in Existing Quality Standards ......................................................................... 23

4.3.2 Focus on Capital Cost Rather Than Cost per Electrical Unit .................................. 23

4.3.3 Competition in Pricing and Speed of Work............................................................. 23

4.3.4 Lack of Training for Installers—No Eligibility Criteria.......................................... 23

4.3.5 Lack of Customer Awareness .................................................................................. 24

4.3.6 Lack of Proper Inspection During and After Installation ........................................ 24

4.3.7 Absence of Mandatory Requirements for Supervision and Audit ........................... 24

5 Prioritized Solutions and Implementation Framework for Quality and Safety Issues in RTPV................... 25

5.1.1 Module Quality Assurance ...................................................................................... 27

5.1.2

Safety Quality Assurance......................................................................................... 29

5.1.3 Vendor Rating Framework ...................................................................................... 30

6 Next Steps .............................................................................................................................................................. 34

References ................................................................................................................................................................ 35

Appendix A – Referenced Published Reports ....................................................................................................... 38

Appendix B – MNRE Published List of Standards............................................................................................... 39

Appendix C – Schematic of Key Parameters for Vendor Rating Framework ................................................... 42

Appendix D – Summary List of Issues Analyzed by RTPV Project Development Stage .................................. 43

Appendix E – Complete List of Issues and Possible Corrective Actions............................................................. 45

vii

This report is available at no cost from the National Renewable Energy Laboratory (NREL) at www.nrel.gov/publications.

List of Figures

Figure ES- 1. Key RTPV quality and safety issues identified by stakeholders ............................................ v

Figure 3. Design, component procurement, and installation related quality challenges based on feedback

Figure 5. Opportunities and constraints for recommended solutions to quality and safety issues in India’s

Figure 1. Key institutions and their roles in quality and safety in solar rooftop systems in India................ 4

Figure 2. Stages in the development of a RTPV project............................................................................. 18

from stakeholders........................................................................................................................................ 19

Figure 4. Key quality and safety issues, and potential solutions. ............................................................... 26

RTPV systems............................................................................................................................................. 27

Figure 6. Implementation Framework for Module Quality Assurance....................................................... 29

Figure 7. Recommended safety quality assurance process. ........................................................................ 30

Figure 8. Process for developing and implementing a vendor rating framework....................................... 33

List of Tables

Table 1. Summary of Stages Relevant to PV-System Installation, Desired Characteristics at Each Stage,

and Standards that Describe How to Achieve these Characteristics........................................................... 10

Table 2. Desired Characteristics, Observed Problems, and Possible Solutions Based on Work at NREL

and in Literature.......................................................................................................................................... 13

Table 3. Common Findings at Various Stages of PV System Installation in India .................................... 14

Table 4. Key Quality and Safety Issues, Their Impact on Project Returns, and Potential Solutions.......... 22

Table B1. Published List of Standards........................................................................................................ 39

Table D1. Design, Component and Installation Related Quality and Safety Issues ................................... 43

Table E1. Complete List of Issues and Possible Corrective Actions.......................................................... 45

viii

This report is available at no cost from the National Renewable Energy Laboratory (NREL) at www.nrel.gov/publications.

1 Introduction

In India, the quality and safety of solar PV systems—and their installation—have become concerns for

investors, regulators, consumers, and distribution companies (discoms). Apart from some existing

component-related standards, design and installation standards are either lacking or not adopted by the

Indian market. The lack of quality standards and a push for low prices has led to the installation of poor-

quality products and inferior system design and execution on site (Devi et al. 2018). Existing literature,

reports from field studies that are later referred to in this report, and stakeholder interviews support this

claim. These inferior products deliver less energy than expected or have a lower overall lifespan than has

been reported in the literature—all of which are serious issues for developers and investors whose return

on investment depends on the amount of power generated from these solar systems for the expected life

of the project. Equipment that does not conform to minimum quality standards also creates safety risks for

the distribution network. Performance and safety concerns lower investor and consumer confidence in

solar products, threatening to slow market development. This is apparent in the slow growth of the

rooftop photovoltaic (RTPV)

1

segment in India despite being economically viable to many conventional

electricity consumers. These concerns are more prevalent with distributed solar systems where developers

and consumers have little awareness and technical competence to judge the quality of equipment and

installation, let alone the appropriateness of system design. Given the nature of these projects (small

capacity and large numbers), Indian states, discoms, and lenders have limited capacity to monitor and

enforce existing standards and guidelines for equipment and installation.

Against this backdrop, this report presents a series of best practices and priorities for use by concerned

authorities in India to improve the quality and safety of RTPV systems. Prepared under the USAID-

NREL Partnership, and in collaboration with USAID-India’s Partnership to Advance Clean Energy-

Development (PACE-D) 2.0, this report uses primary and secondary resources to help understand the

current state of solar quality and safety in India and to provide the basis for future recommendations. An

overview of issues and lessons learned about solar quality and safety issues from the United States and

other global experiences was also conducted. The report concludes with a series of potential solutions and

identify those parties that could most aptly lead change.

This report is organized into six sections:

1. Introduction—solar energy targets, key challenges of RTPV deployment, stakeholders involved,

and need for quality and safety standards

2. International Perspective—experiences from the United States and other places globally on solar

quality, safety issues, and solutions

3. Research Methodology—how information from key stakeholders was obtained and analyzed

4. Key Findings: Quality and Safety Aspects of RTPV Systems in India—key design, component,

and installation challenges, and key drivers of poor quality and safety standards

5. Prioritized Solutions and Implementation Framework—potential solutions for addressing issues

6. Next Steps

1

Throughout this report, we will use the term rooftop photovoltaic (RTPV) to denote small-scale PV systems

adopted primarily by residential and commercial customers and connected to the distribution system (also referred to

as distributed solar, or distributed PV in other contexts). RTPV is the term commonly used in India even though

these types of systems are not necessarily located on roof tops.

1

This report is available at no cost from the National Renewable Energy Laboratory (NREL) at www.nrel.gov/publications.

1.1 Solar Energy Targets and Growth in India

The Government of India launched the National Solar Mission (NSM) in January 2010 with the goal of

establishing India as a global leader in solar energy deployment. Its ambitious target is to deploy 20 GW

of grid-connected solar power by 2022. The NSM aimed to reduce the cost of solar and achieve grid

parity by 2022 through:

• Developing a long-term policy

• Deploying solar on a large scale

• Conducting aggressive research and development (R&D)

• Producing critical raw materials, components, and products domestically.

In 2014, India increased the target for the NSM fivefold, from 20 GW to 100 GW of grid-connected solar

power by 2022 (Ministry of New and Renewable Energy [MNRE] 2014). The government also

segregated this target into ground-mounted and rooftop segments, specifying a 60% versus 40% split for

ground-mounted and RTPV systems, respectively (MNRE 2019).

Though the NSM included targets for both ground-mounted MW-level systems and RTPV systems, the

initial emphasis from the market was on installations of the former; hence, growth in that sector has been

larger and currently exceeds that of RTPV deployment. According to the MNRE, as of May 2020,

installed capacity of ground-mounted systems was 32.2 GW

2

; installed capacity of RTPV systems in

December 2019 was 5.4 GW (Bridge to India 2019). In 2015, the MNRE developed state-specific targets

based on solar resource potential (MNRE 2015). In response, certain states developed road maps outlining

a framework for achieving these targets. In addition, many State Electricity Regulatory Commissions

(SERCs) announced regulations for net metering of RTPV systems based on technical specifications and

guidance provided by the central government. Despite these efforts, RTPV deployment has been slow in

India.

1.2 Key Challenges of RTPV Deployment

Several factors have contributed to the slow adoption of RTPV in India, including:

• Cost of generation: Solar rooftop deployment is accomplished by thousands of consumers installing

these systems on their property. These systems are typically small, with higher deployment costs

(compared to ground-mounted systems), and with higher transaction costs for financing and

installation. In the current regulatory framework, RTPV is economically viable mostly for high tariff-

paying consumer categories such as commercial and industrial (C&I) (Josey et al. 2018; Jaiswal et al.

2017). Residential consumers usually pay much lower tariffs, making RTPV less attractive to them

(Patel et al. forthcoming). Higher transaction costs coupled with limited understanding of the

technology and quality of the system, further act as deterrents to residential consumers who own a

significant portion of rooftop space. In some cases, capital subsidies (central financial assistance)

available as an incentive to residential consumers have exacerbated issues due to delayed

disbursement, complex procedures, intermittent availability and long pending overdues.

• Institutional financing: Most banks either do not want to fund such small transactions or lack

familiarity with the technology to feel comfortable financing RTPV systems. These systems are often

owned by third-party developers or financed through personal savings, making it challenging to

deploy RTPV at scale.

2

https://mnre.gov.in/the-ministry/physical-progress

2

This report is available at no cost from the National Renewable Energy Laboratory (NREL) at www.nrel.gov/publications.

• Utility caution and cumbersome deployment process: To date, most rooftop systems in India are

deployed by C&I consumers (Bridge to India 2019). These consumers also contribute to a high

percentage of the margins and revenues of the distribution utilities. Utilities perceive this as a

potential revenue loss and are not incentivized to develop a streamlined process (Jaiswal et al. 2017).

Utilities would benefit from additional PV technology capacity building and training, especially

regarding the safety requirements on the DC side.

• Complexity and lack of standards: The complexity of the installation process, the large number of

system components, the wide range in quality of available options, and the limitations in defining a

single national standard for these systems are barriers to the deployment of high-quality RTPV

installations. Most consumers are unable to effectively evaluate the quality of these installations to

make informed decisions.

• Quality and safety: Stakeholders have limited understanding of the quality and safety requirements

associated with RTPV and this further complicates the adoption process. Furthermore, quality and

safety considerations are particularly important to facilitate lender confidence in this investment-

intensive sector. For example, a significant portion of the overall life cycle costs come as an up-front

investment during the deployment of the systems. To recover the investment, it is critical that the

systems perform as expected. The success and sustainability of these investments, as well as the

achievement of national renewable energy targets, depend to a large extent on the performance of

these systems which, in turn, depends upon the quality of the systems, their components, the

workmanship during installation, operations and maintenance during the life of the system, and the

safety of the financed energy systems.

Over the past few years, the drastic reduction in the cost of solar coupled with a supply glut in the market

has led to a suppliers’ competition. This has forced engineering, procurement, and construction (EPC)

contractors, installers, and suppliers to cut prices to win orders—often sacrificing basic quality and safety

requirements. EPC contractors and installers may compromise on the quality of the components, the

systems, and the workmanship to keep costs low. This has created a certain amount of scepticism in the

market on the long-term performance and sustainability of the systems. To ensure the long-term health of

the sector, grow the market, and achieve India’s ambitious policy targets, there is a need for a system that

facilitates quality in these solar rooftop systems, especially for residential consumers who will make up

the bulk of the market in the future and who are most at risk.

1.3 Key Stakeholders and Their Roles in Ensuring RTPV Quality and

Safety

Ensuring quality and safety of RTPV systems falls under the domain of several central- and state-level

institutions that develop policies, regulations, rules, and guidelines for the power sector in general and for

the solar and RTPV sectors specifically. Figure 1 presents the key actors responsible for the development

of the RTPV sector in India and highlights some of the major quality and safety initiatives undertaken by

each of them.

3

This report is available at no cost from the National Renewable Energy Laboratory (NREL) at www.nrel.gov/publications.

Figure 1. Key institutions and their roles in quality and safety in solar rooftop systems in India.

The model regulations for net metering developed by the central Forum of Regulators, and informed by

guidelines and specifications developed by the Central Electricity Authority (CEA) and the MNRE, are

the basis on which SERCs have developed their net metering guidelines. State regulations are key drivers

for RTPV deployment, with states dictating technical, quality, and compliance requirements. This

includes the technical parameters and specifications for RTPV systems and for grid integration, as well as

identifying the various limits, checks, and approval timelines. Some state regulators provide detailed

technical specifications while others refer to those specifications published by the central authorities, such

as the MNRE and CEA. Ambiguous and loosely defined technical parameters related to design,

installation, and safety aspects, and the lack of standardization have an impact on the quality and safety of

systems being installed across states. The state-level Chief Electrical Inspectorate (CEI) and the state

electricity distribution utility are responsible for the implementation of these technical and safety

guidelines and ensuring that all systems conform to the standards laid down by the SERCs, MNRE, and

CEA.

1.4 Rooftop Solar Implementation Models and their Impact on Quality

and Safety

RTPV systems in India are primarily financed and developed in one of two ways: capital investments by

consumers (owners of rooftop) or capital investments by third-party RTPV developers, also known as

Renewable Energy Service Companies (RESCOs):

• Capital expenditures (CAPEX) model—the consumer purchases an RTPV system and either

consumes electricity through net metering or sells electricity to discoms through gross metering. Most

residential RTPV systems and most small-capacity systems (less than 100 kW) are built using this

model. Normally, the smaller residential customer hires an EPC agency to manage the project from

the beginning to the end, including design, supply, and installation. These systems are susceptible to

low quality and safety hazards

because of low-level customer awareness coupled with an emphasis on

reducing capital costs.

4

This report is available at no cost from the National Renewable Energy Laboratory (NREL) at www.nrel.gov/publications.

• RESCO or operational expenditures (OPEX) model—the RESCO invests in, operates, and maintains

the RTPV system, and the customer provides the rooftop and purchases energy generated from the

system. This model is common with C&I customers and public sector systems (for example,

government buildings) that have larger loads and rooftop area and higher system capacities (100 kW

and more). The quality and safety of such systems are better managed and maintained because the

developer is more experienced, has access to quality control and inspections, and directly benefits

from the higher revenue from better performing systems.

As of December 2019, total installed RTPV capacity in India was 5,440 MW (1,523 MW OPEX and

3,917 MW CAPEX), of which C&I customers represented 3,964 MW, public sector government

buildings represented 728 MW, and residential systems amounted to 750 MW (Bridge to India 2019).

Currently, the large C&I and public sector systems are developed under either of these models. These

consumer types and agencies have the wherewithal to develop quality systems that are safe and perform

per guidelines. However, small CAPEX-based systems and investments are likely to be the most

dominant investment model for residential consumers because RESCOs do not find it economical to

service this segment, or are prohibited from participating. Owing to improvements in technology,

economic incentives, and intermediate subsidies, it is likely that there will be an upward trend in the

deployment of RTPVs in the future. Therefore, it is critical to develop a framework and implement

solutions that address the quality and safety concerns currently prevalent with these solar PV systems.

Though limited in number, the larger solar developers in India, take measures to ensure that appropriate

quality and safety are built into the development of solar PV systems. For example, these developers

usually have a well-established team of quality-control personnel who work with component suppliers to

ensure the quality of the components. These developers also ensure that downstream work is carried out

according to their very strict quality and safety requirements.

These larger developers can implement quality measures because they have the financial resources to buy

in bulk (allowing them to dictate quality requirements to component suppliers), employ qualified

technical personnel to ensure quality of installations and components, and track quality throughout

operations to help them make future development decisions. However, most of these developers work

primarily on large grid-connected, ground-mounted systems (larger than 5 MW) and RESCO-based

distributed and solar rooftop installations. Acting as RESCOs, these developers assume performance risks

associated with their systems; this, in turn, creates an incentive to design and install high-quality systems.

In the RTPV space, these larger developers cater to either large C&I clients or participate in large RESCO

bids for institutional players (such as municipal corporations), public sector undertakings, and other

similar government establishments with high financial ratings. Small and medium establishments and the

residential sector are typically not covered by most developers under the RESCO model because of

contract security risks. These electricity consumers rely mostly on self-financed systems or on systems

developed through smaller, local RESCOs. This leads to the following issues:

• Consumers developing self-owned systems usually lack an understanding of the quality and safety

challenges associated with these systems; they tend to invest in the cheapest system available,

resulting in suboptimal performance, potential safety concerns, and impacted investment returns.

• Suboptimal performance of systems has downstream impacts on the industry and results in lower

adoption rates by other consumers because of negative word-of-mouth publicity; fewer banks are

willing to provide loans.

Price reductions and increased competition in the market will continue to make quality and safety

significant challenges for the industry. These challenges can stall the development of the distributed solar

and solar rooftop markets, especially for small and medium enterprises, and the residential sector.

5

This report is available at no cost from the National Renewable Energy Laboratory (NREL) at www.nrel.gov/publications.

1.5 Need for Quality and Safety Standards and Implementation

Framework

Implementing quality and safety measures requires adhering to international and national standards for

component manufacturing as well as design, installation, and workmanship. It also requires a framework

that allows stakeholders to examine whether these standards have been followed, which includes a

rigorous system of testing, monitoring, and performance mapping.

Policymakers and regulators in India have developed and prescribed standards for solar PV projects—for

both large grid-connected solar projects as well as RTPV projects (Appendix B). However, most of these

are component-level standards and do not address workmanship issues. Moreover, the adoptions and

enforcement of these standards have been left to stakeholders, such as the distribution utilities, banks,

project developers, or consumers. Project developers and EPC companies tend not to enforce these

standards under price pressures, while banks and consumers often lack the knowledge to implement these

standards. This is especially true for RTPV projects because of their large numbers, high transaction

costs, lack of knowledge among consumers and banks, and the small size of individual investments.

Therefore, to ensure quality through standards, implementing a framework is critical to enforcing

standards and associated services, such as testing, inspection, and calibration.

The key challenge lies in understanding and recognizing where quality compromises occur. For example,

during the design phase, it is critical to understand the nuances of designing strings to match the

maximum output current of strings, requirements for the design of strings to match inverters, or the use of

appropriate fasteners keeping in view the wind profile of the area to name a few. Similarly, compromises

may occur when the module manufacturers’ bill of material does not conform to prescribed standards, or

if specific standards are not adhered to during the manufacturing stage. In addition to prescribing

standards, there is also a need for on the ground support through inspections and audits.

Technical issues such as the gaps in standards or monitoring systems and the penetration of inferior

quality products in the market hamper the performance of the solar system and create a poor reputation

for PV systems and the technology (Devi et al. 2018). Developing a framework that will facilitate

developers (RESCOs and EPCs) to buy the right components, as well as ensure that the components have

been tested for quality and safety, is an urgent need. A framework will also provide developers standards

to conform to, and allow consumers to see that systems are installed in a manner prescribed by standards

and best practices.

6

This report is available at no cost from the National Renewable Energy Laboratory (NREL) at www.nrel.gov/publications.

2 An International Perspective: U.S. and Other Global

Experiences With Solar Quality and Safety Issues

India’s unique context influences how solar quality and safety issues manifest on the ground in terms of

their specific type, frequency, and prevalence. At the same time, India is not alone in facing such

challenges. Solar safety and quality issues have persisted worldwide from the technology’s early

deployment (1980s and earlier) to today. Over time, researchers have cataloged common solar quality and

safety issues and developed best practices for overcoming them—a process that is ongoing. Since its

inception, the U.S. Department of Energy’s National Renewable Energy Laboratory (NREL) has focused

on PV reliability and system performance research to improve these technologies. NREL’s PV Reliability

Group, in particular, has been involved in several efforts related to PV system quality; the group’s

experiences and lessons learned that are relevant to India are summarized below.

2.1 Site Inspections

NREL’s PV Reliability Group regularly performs PV site inspections to directly observe possible

reliability issues (or lack thereof) and help guide research. NREL also interviews system owners. The

majority of site inspections are performed on ground-mounted systems, but some are on residential

rooftop systems. Nevertheless, important commonalities have been observed. Major observed trends over

the years, and current issues with rooftop installations, are described below.

Failures in early PV systems were dominated by component failures, often in the modules and inverters.

Some examples of common failures in older PV systems include browning, cracked wires and connectors,

and compromised solder bonds. The incidents of such failures have decreased dramatically because of

improved PV component testing and standards. Programs such as the Jet Propulsion Lab block buys

between 1975 and 1985 provided guidance on which accelerated tests could reproduce observed failures.

Such tests were subsequently incorporated into component standards, such as International

Electrotechnical Commission (IEC) 61730 for module safety and IEC 61215 for module design

qualification. Qualification to international component standards has become a minimum requirement for

many large system procurements. In rare cases where modules are not designed to meet these standards,

NREL has observed a recurrence of these early problems. Based on discussions with stakeholders in India

(and outlined further in Section 4), a majority of the quality and safety issues was identified to be module

related. While standards have been developed and adopted for ensuring module quality, implementation is

lacking in India.

System downtime because of inverter failures and nuisance trips was also widespread in early systems.

Inverter issues have been slower to resolve than the majority of early module failures but are decreasing

in frequency with wider applications of revised or new inverter standards, such as IEC 62109 for safety

and 62093 for design qualification in natural environments. Benefiting from the newer inverter standards

developed and adopted, few survey respondents reported issues with inverters in India (Section 4).

Laws (codes) in the United States cover PV system safety quite thoroughly, but there are few

requirements for PV system performance: a system and components must be safe, but system energy

generation is not strictly mandated. For example, module certification to IEC 61730/UL 61730 (a safety

standard) is required via the national electric code (NEC). The NEC and building codes also govern

system wiring and grid connection, fire resistance requirements, and mechanical loads. Only within the

last year have governments started to require performance standards, such as the state of California

adding a requirement that modules meet IEC 61215/UL 61215 design qualification to receive state

incentives.

7

This report is available at no cost from the National Renewable Energy Laboratory (NREL) at www.nrel.gov/publications.

System energy generation can be compromised by poor choices in any aspect of the system construction.

Some system owners have cited an overemphasis on physical system completion rather than quality and

energy generation, which they believe was due to developers receiving tax incentives at physical system

completion. Thus, despite substantially improving module reliability, other factors may impact system

performance severely. An example is a system where the trackers were not certified or tested for PV

usage; most became stuck within a year of initial operation.

Some owners of large systems are more focused on return on investment through long-term energy

generation. These project owners and designers have become very technically savvy in the areas of

component certification, module degradation rates, and system construction requirements. The RTPV

consumer unknowingly benefits from this technical know-how because high-quality (certified) PV

components have become widely available.

Poor system design and installation are much more common in rooftop systems than in large ground-

mounted systems. For example, NREL has seen many rooftop systems inadvertently installed with

significant shading. Systems have been installed facing north (in the northern hemisphere) with the

designer seeing only that the location is not shaded. In other cases, installers have misinterpreted claims

about microinverters to mean that the modules can perform adequately in the shade if microinverters are

used. NREL has also seen multiple cases where installers flush-mounted modules to the roof, which

decreases performance and longevity because of hot temperatures, without discussing or explaining

higher-performance configurations to the homeowner.

These quality-related observations connected to system size are relevant for the Indian context, where

business models for RTPV deployment can further amplify these issues as discussed in Section 1.4.

A key stumbling block in U.S. rooftop system quality is that the consumer usually cannot distinguish

between a high- and low-quality system. While there are some quality marks that are discernible to a

subject-area expert (e.g., IEC component certification and North American Board of Certified Energy

Practitioners training of installers), these valid indications of quality are not well known. Instead, cost-

per-watt and customer recommendations are often used to select an installer. Even some government

websites that purport to compare installers only provide cost-per-watt information. Customer

recommendations may be misleading. Such recommendations are more likely to be based on the

installer’s personality or punctuality because most consumers cannot evaluate PV system quality. NREL

inspected a system with significant shading (using a string inverter), code violations, flush-mounted

modules, no warranty, and inoperable data transfer from the inverter, where the installer was highly

recommended by the homeowner’s friend.

When a homeowner suspects a problem with the PV system operation, it may be difficult to obtain

warranty benefits. While a part (such as a prematurely failed inverter) may be covered, the homeowner

may still be required to pay for shipping and labor. NREL encountered two cases where homeowners

were able to detect module performance problems and experienced a great deal of resistance from the

manufacturers in obtaining replacement modules (although they did eventually succeed).

Installers cite some challenges unique to rooftop installations. Some believe that they are shipped lower-

quality modules than those shipped to large sites because they cannot afford random-sample module

testing like the larger users. These installers believe that they may be shipped modules with cell cracks

and other flaws that are not visible to the eye. Some installers have also cited unhelpful inspections that

can delay the project by days. It is important to remain sensitive to these issues in thinking about quality

requirements.

8

This report is available at no cost from the National Renewable Energy Laboratory (NREL) at www.nrel.gov/publications.

2.2 Standards for Systems—IECRE

To improve system quality and provide solutions to the issues raised in the previous section, NREL

worked with teams of international experts to develop the PV portion of the IEC System for Certification

to Standards Relating to Equipment for Use in Renewable Energy Applications (IECRE) for PV system

certification

(https://www.iecre.org/about/what-it-is.htm, https://www.iecre.org/sectors/solarpvenergy/).

This effort involved identifying the characteristics and actions associated with high-quality PV systems,

coming to international consensus on these items, then updating or creating more than 30 standards,

technical specifications, and operational documents to reflect this content.

A general description of requirements for a high-quality system at each stage of its life is included in the

IECRE operational documents (ODs). The ODs reference standards for the details of various procedures.

For example, the OD describing system commissioning (OD-401) requires that components be of high

quality and that appropriate inspection of the installation occur before the system is considered to be

complete. The specifics of component testing and site inspection are not described in the ODs.

Component testing is accomplished via manufacturer certification of products to standards, such as IEC

61215 and 61730. Operational Document 401 describes which components must be certified to which

standards. For the details of system inspection at commissioning time, OD-401 references IEC 62446-1.

Where different requirements for different size systems are logical (e.g., onsite irradiance monitoring for

large systems versus use of online climate data for residential systems), the standards specify different

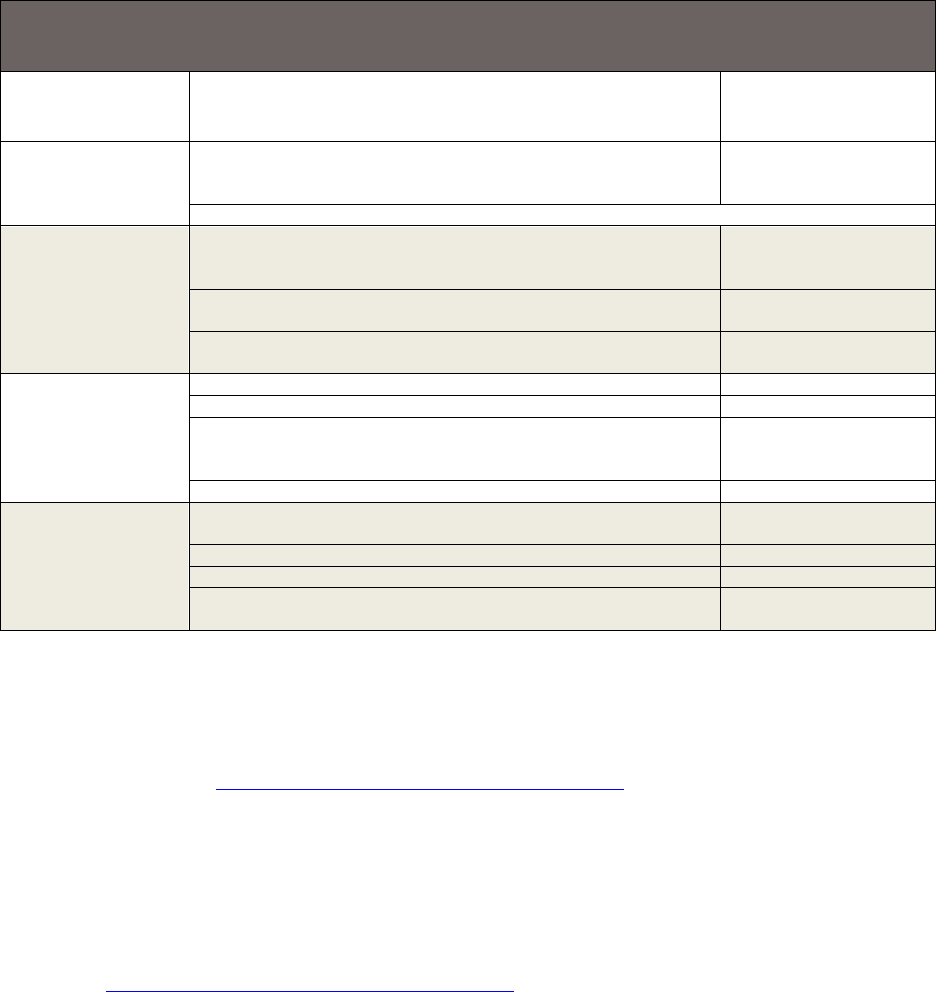

classes of systems. Table 1 summarizes the ODs used for different stages in PV installation, the desired

characteristics ensured by the OD, and the standards referenced to detail the procedures. ODs are

available free of charge at

https://www.iecre.org/documents/refdocs/

. The names of PV ODs begin with

OD-4. IEC standards may be purchased from the IEC website or through an institutional library

subscription.

The IECRE PV certification system, with certified inspection bodies and all necessary ODs and standards,

was first operational in 2017. Some aspects of the system were adopted quickly. In particular, module

manufacturers were eager to demonstrate their quality-management systems through certification to IEC

62941. Inspections and quality certificates were issued for some large PV systems. However, the

community has not yet begun to include IECRE system certifications regularly in procurement or

commissioning requirements.

9

This report is available at no cost from the National Renewable Energy Laboratory (NREL) at www.nrel.gov/publications.

-Table 1. Summary of Stages Relevant to PV System Installation, Desired Characteristics at Each

Stage, and Standards that Describe How to Achieve these Characteristics

Stage in PV

System Life

(Document #)

Desired Characteristic

Standard Where the

Requirements Are

Specified in Detail

Choosing a Module

Manufacturer

(OD 405-x)

The module manufacturer has a quality-management system in

place that covers product design, purchasing, customer

relations, monitoring, and measuring.

IEC TS 62941

Note: This step evaluates the manufacturer, not a specific product.

Choosing an

Installer

(OD 410-x)

The installer keeps records of projects and trains employees.

Training, continual improvement (including evaluating energy

production via 61724).

IEC TS 63049

The installer follows best practices for array design (including

shading, mechanical loads, etc.).

IEC 62548

IEC TS 62738

The installer follows best practices for commissioning (including

system documentation for customer, testing, and inspection).

IEC 62446-1

Commissioning—

PV System is

Complete (OD 401)

Modules are designed to be safe and durable.

IEC 61730, IEC 61215

Power electronics are safe.

IEC 62109, IEC 62093

Commissioning: System documentation is provided to

customer. Testing and inspections appropriate for residential

systems are performed.

IEC 62446-1

Performance and capacity are clearly understood.

IEC 61724-2

Checking System

Performance

(OD 402)

Compare predicted and actual irradiance this year with

accuracy appropriate to residential systems.

IEC 61724-1

Compare predicted versus actual energy production this year.

IEC 61724-3

Compare predicted versus actual system downtime this year.

IEC 61724-3

Compare predicted versus actual operations and maintenance

costs this year.

2.3 Education and Developing Best Practices

NREL has worked in industry-wide collaborations to develop best-practices guides for several topics

related to photovoltaics. Most relevant to India is a best-practices guide for PV system installation (Doyle

et al. 2015), available at https://www.nrel.gov/docs/fy15osti/63234.pdf

. This guide includes best practices

for several aspects of installation, including requirements for personnel training, company experience and

solvency, shading analysis, shading packages, and system production estimates. Requirements are

organized into a short checklist in each section of the guide. Some requirements in the guide (e.g., a

collection of roof dimensions and type) may be of only minor importance to Indian stakeholders.

NREL has also produced a best practices guide regarding how to plan and deliver effective O&M Best

Practices for Operations and Maintenance of Photovoltaic and Energy Storage Systems; 3rd Edition

available at https://www.nrel.gov/docs/fy19osti/73822.pdf

.

Also available online are best-practices guides for commercial and industrial PV installations (Doyle et al.

2015), operations and maintenance (Doyle et al. 2015; NREL et al. 2016), solar resource assessment

(Sengupta et al. 2015), and development of renewable portfolio standards (Heeter, Speer, and Glick

2019).

NREL promoted an education program for authorities having jurisdiction. These authorities are the state

and local officials responsible for inspections and enforcing codes related to PV system installations. The

goal of the program was to maintain high system quality but minimize costs to the installer that might be

associated with jurisdictional authorities that have not previously specialized in solar, or low-value

10

This report is available at no cost from the National Renewable Energy Laboratory (NREL) at www.nrel.gov/publications.

inspections. Authorities having jurisdiction were educated on important points and common failures and

how approvals are typically handled in high-volume solar areas. Installers reported a significant

improvement in how efficiently inspections and approvals were executed in areas where jurisdictional

authorities participated in an education program.

2.4 Industry-Wide Reports on Rooftop PV Quality

A number of papers and online reports document observations and recommendations for PV system

quality internationally (IRENA 2017) or in specific countries such as the United States and India (IRENA

2017; Chattopadhyay et al. 2017; N 2018), Australia (IRENA 2017; Arthur et al. 2017), and Kenya

(Jacobson and Kammen 2007; Mills et al. 2014; Duke, Jacobson, and Kammen 2002; Turman-Bryant et

al. 2015). These reports contain observations of quality issues (IRENA 2017; Jacobson and Kammen

2007; Mills et al. 2014; Duke, Jacobson, and Kammen 2002), recommendations to solve quality issues

(IRENA 2017; Arthur et al. 2017; Duke, Jacobson, and Kammen 2002; Jason S. Trager 2018),

instructions and checklists (Turman-Bryant et al. 2015; IBTS 2019.; Stanfield and Hughes 2018;

Interstate Renewable Energy Council (IREC) 2010; Brooks and James Dunlop 2016; Energy Market

Authority 2011; California Energy Commission 2001) for system design and construction, consumer

guides (Energy Market Authority 2011; California Energy Commission 2001; SEIA 2018; Chace and

Clay Mitchell 2018), and a study of successful quality improvement (Jacobson and Kammen 2007;

Turman-Bryant et al. 2015). The study of PV lighting quality in Kenya is particularly interesting because

strategies were effective, and considerable quality improvements were observed (Turman-Bryant et al.

2015).

2.5 Looking Forward—Important Conclusions and Possible Paths

Experience at NREL, and that described in the literature, is consistent in its recommendations regarding

best practices for improving quality and safety of RTPV systems in India and elsewhere. Table 2 shows a

brief summary of desired characteristics, observed problems, and possible solutions based on work at

NREL and in the literature.

Listed below are five key considerations for improving quality and safety of RTPV systems as identified

from the review of this broad collection of studies:

1. Most of the time, residential RTPV consumers are unable to distinguish between low- and high-

quality systems. The purchase of a PV system represents a complicated one-time occurrence for

many consumers, many of whom have no prior experience with this technology. System quality

contains many technical details, any of which can lead to a system failure or underperformance.

Even third-party information (including some consumer guides) tends to overemphasize the

importance of initial cost per watt, most likely because there is not a readily available

quantification of quality. Products change approximately every six months, so a useful guide

must be updated frequently. Even after the system is installed, consumers do not know if the

system is producing as expected because of the complexities of temperature, irradiance, inverter

functions, and data reporting. These situations make warranty claims particularly difficult.

2. Demonstrations of quality (installers or components) are only effective if the information reaches

the customer in a clear way.

3. Many inspection checklists and certification procedures are already available. Some checklists

focus on different aspects of the PV system (e.g., components, roofing and construction, safety,

and energy generation).

11

This report is available at no cost from the National Renewable Energy Laboratory (NREL) at www.nrel.gov/publications.

4. Residential systems often lack long-term monitoring or effective operational indicators. A

homeowner should be able to easily see if their system is operating properly or if it requires

attention.

5. A successful approach to improving residential PV system quality is likely to include an

assortment of strategies. Up-to-date and accessible communication to customers is very important

because customers drive the market. Also important are installer training and certification, use of

certified components, inspections, and incentives, warranties, and financing that encourages the

purchase of high-quality systems.

12

This report is available at no cost from the National Renewable Energy Laboratory (NREL) at www.nrel.gov/publications.

Table 2. Desired Characteristics, Observed Problems, and Possible Solutions Based on Work at

NREL and in Literature

Desired

Characteristic

Observed

Problems

Possible Solutions

High-quality

components

Early life component

failure

• IEC component certifications—minimal cost to consumer

because manufacturer performs test once per product

• Publicize components that meet requirements online to

customers

Counterfeit

components

• Import control and random testing of products at market with

consumer-accessible online publication of results

• Development of national certification labs when possible

Installers buy poor-

• Provide channels of communication between installers and

quality components

distributors or manufacturers so those up the supply chain

because they are

know about the problems and buyer preferences.

most readily

available

Competent

installation

professionals

Mistakes made

because of lack of

training or

experience

• Make relevant training programs more accessible

• Publicize system designers and installers who meet training

or certification requirements to consumers

• Require training or certification for installers to participate in

certain types of financing or incentive programs

• Require system inspections by third parties or government

agencies. A large investment is required to make sure all

inspectors are expert enough to add value and that a lack of

inspectors does not delay projects.

Highest-quality

systems are

purchased

Consumers purchase

a low-quality system

because the initial

cost was the lowest

• Educate consumers that initial cost is not the only important

metric. Life-cycle costs are also important

• Publicize from a trusted source, both online and in stores,

components and installers that demonstrate exceptional

quality—and those that have demonstrated poor quality

• Provide incentives to customers that participate in quality

programs

• Make available a good warranty that installers may use and

customers may look for online

• Make available financing options (e.g., system lease) that

provide incentives for both the customer and the installer to

consider quality.

Confident buyers

Consumers decide

not to buy a system

because they’ve

• A trusted third-party provider continuously updates

information online that allows consumers to know they are

selecting high-quality components and installers. The

information must be publicized so that consumers are aware

of the resource

heard about some

problems

• Make available a good warranty that installers may use and

customers may look for online

• Make available financing options (e.g., system lease) that

provide incentives for both the customer and the installer to

consider quality.

13

This report is available at no cost from the National Renewable Energy Laboratory (NREL) at www.nrel.gov/publications.

3 Research Methodology

To gain a better understanding of quality and safety issues in India, this research effort was conducted in

three stages, starting with a literature review of solar quality and safety in India, followed by interviews

with various stakeholders in the sector, and an in-person workshop.

3.1 Literature Review

Few reports are available from previous studies undertaken to evaluate quality and safety aspects of solar

PV deployment in India. Those available are based on actual field visits and tests conducted on installed

and commissioned plants in various regions in India. Similar to the global experience described in Section

2, the majority of these studies are based on ground-mounted, MW-scale systems, and only parts of some

of these studies include rooftop systems. Nevertheless, important similarities can be observed, and

recommendations for MW-scale systems are applicable to RTPV systems as well. Common findings from

these reports are corroborated by stakeholder interviews conducted for this research and are presented in

Table 3. A list of reports, including those from non-Indian regions studied for this project, is also

presented in Appendix A.

The most frequently mentioned issue in these reports is the solar module, which represents the major cost

component of the system and most affects system life and performance. These solar modules are reported

to be of varying quality from different suppliers.

Table 3. Common Findings at Various Stages of PV System Installation in India

Stage of RTPV Project Common Findings

Solar module issues Early degradation, microcracks, potential induced degradation (PID),

snail trails

Safety and protections Incorrect earthing, insufficient lightning protection systems (LPSs),

underrated fuses and surge-protection devices (SPDs), disregard for

fire-handling systems

Installation methods Partial shadows on array, long runs of direct current (DC) cables,

loose connections and wear and tear of cables, corrosion in structure

parts

Commissioning Absence of independent inspection, lack of commissioning tests

Performance Lower energy generation, intermittent monitoring of systems, slow or

no follow up on corrective actions prompted by monitoring

O&M Inadequate maintenance, no schedule for preventive maintenance

Documentation Absence of proper documents with customers, planning and design

documents not shared with customers, power purchase agreements

(PPAs) or contracts unclear in many aspects.

These findings are attributed to some common probable reasons as presented in these reports and

corroborated by stakeholder interviews:

• Lack of awareness of these module problems by all stakeholders involved in PV power projects

• Absence of independent supervision, inspection, and audit framework

14

This report is available at no cost from the National Renewable Energy Laboratory (NREL) at www.nrel.gov/publications.

• Lack of documentation and reporting framework

• Focus on initial cost of power plant rather than levelized cost of energy

• Cost pressures that result in low-quality and unsafe PV systems.

3.2 Stakeholder Interviews: Methodology

To gain a comprehensive understanding of quality and safety of rooftop PV systems in India and the

sector status in general, a series of interviews with different stakeholders was conducted, including EPC

companies, installers, developers, component manufacturers, and others. Authorities, financiers, and

consultants were also interviewed to provide insights from their experiences in the field. As the agencies

actually responsible for onsite quality and safety, the EPC companies and installers were included in

larger numbers as compared to others. This particular group of interviewees was selected by categorizing

them into large, medium, and small players because the issues, reasons, and possible solutions would

likely be different across such segments.

Next, a questionnaire was designed and used to conduct interviews with different stakeholders in person,

over the telephone, and via written responses. Questions focused on the role of the interviewee, reasons

for poor or high solar quality and safety, impacts of low-quality systems, strategies for improving quality,

and insight on specific categories (e.g., components and humanpower).

In-person interviews were conducted with 13 stakeholders and telephone interviews with three

stakeholders from June to September 2019. In November 2019, another 8 in-person interviews were

conducted. Both of these types of interviews lasted for an average of 1.5 hours each. Several other

respondents provided written responses. In keeping with the questions used in the interviews, these

stakeholders identified current issues based on their own experiences and provided suggestions for

addressing such issues and improving the quality and safety of RTPV systems.

Interview responses were compiled and summarized by categories used in the questionnaires, which

included component, manpower, commissioning, inspection, documentation, operations and maintenance,

tools, site, installation standards, and safety. Some of these categories, such as tools, humanpower, and

site did not receive substantial responses and, hence, were combined into an “other” category for this

report. A summary list of issues, along with frequency of occurrence and impact on project development

is listed in Appendix D; a complete list of issues and possible corrective actions is listed in Appendix E.

3.3 Stakeholder Workshop

The United States Agency for International Development (USAID) PACE-D 2.0

3

held a solar quality and

safety workshop on January 21, 2020, in New Delhi, India, to confirm issues raised by stakeholder

interviews and to get feedback on potential solutions. Participants included representatives from key

government agencies, technical institutions, quality monitoring centers, multilateral development

agencies, utilities and distribution companies, local and regional banks, solar PV vendors and developers,

EPC companies, O&M companies, and central- and state-level policymakers. The day-long workshop

included panel discussions and breakout sessions to review and discuss three potential solutions to

improve quality and safety of RTPV in India

• Module quality certification

• Electrical safety quality assurance

3

https://www.pace-d.com/

15

This report is available at no cost from the National Renewable Energy Laboratory (NREL) at www.nrel.gov/publications.

• Vendor rating framework.

Inputs and findings from these discussions were used to further refine the solutions proposed in Section 5

of this report. There was support and general agreement that the development of a vendor rating

framework as a mechanism to evaluate, monitor, and rate RTPV vendors based on certain established

standards was a timely next step for India.

16

This report is available at no cost from the National Renewable Energy Laboratory (NREL) at www.nrel.gov/publications.

4 Key Findings: Quality and Safety Aspects of RTPV

Systems in India

The stakeholders interviewed in the survey identified major and frequently observed issues related to the

quality and safety of grid connected RTPV systems in India, much of which corroborated existing

literature and the authors’ extensive field experience. Figure ES- 1 captures some of the most severe and

frequent solar quality and safety issues organized by category or stages of RTPV system life: site

analysis, system design, installation, commissioning, and operations and maintenance. While some issues

may have a relatively low impact on energy generation, their impact on safety can be high (denoted by the

colored icons).

4.1 RTPV Project Development Cycle

The development of a RTPV project can be divided into three broad stages: design, procurement and

installation (including O&M).

• Design: the design stage includes site assessment activities, system sizing and design, component

selection and procurement planning, and scheduling the installation.

• Component procurement: the component procurement process involves contracting for the

component, including putting in place performance guarantees, specifications and standards that the

components must conform to, specifying the particular tests that the components must go through

before being dispatched from the manufacturing facility, and the specific test results that the

developer or EPC contractor would like to see before finally receiving the components.

• Installation and O&M: The final installation stage involves receiving components at the site, site

preparation, storing material, installing the system, and completing the commissioning. This stage

usually lacks standards and is more dependent on the skills and training of the installers.

Figure 2 shows the three stages and the broad set of activities they encompass.

17

This report is available at no cost from the National Renewable Energy Laboratory (NREL) at www.nrel.gov/publications.

Figure 2. Stages in the development of a RTPV project.

4.2 Key Challenges in RTPV Quality and Safety

Stakeholders raised concerns with component-related quality issues that span several stages of RTPV

system life, including the system design and installation phases. Most of the quality and safety issues

occurred either at the component procurement stage (about 50% of quality and safety issues experienced)

or the installation stage (about 35% of quality and safety issues experienced); the design stage contributed

to the balance 15% of quality and safety issues experienced. Within the different stages, some specific

areas caused a high proportion of challenges (Figure 3). For example, in the case of system design quality,

almost half of the quality challenges stemmed from the wrong array layout, followed by string inverter

mismatch and site access. In the case of component quality, the major area of concern was the modules

and the module mounting structures, followed by junction boxes; in the installation phase, the main

quality issues were related to fasteners, handling of modules, and earthing. Given the emphasis on issues

related to system design, component procurement, and installation and O&M, this report expands on

those topics in Sections 4.2.1-4.2.3. A summary list of issues, along with frequency of occurrence and

impact on project development is listed in Appendix D; a complete list of issues and possible corrective

actions is listed in Appendix E.

18

This report is available at no cost from the National Renewable Energy Laboratory (NREL) at www.nrel.gov/publications.

Figure 3. Design, component procurement, and installation related quality challenges based on

feedback from stakeholders.

4.2.1 System Design-Related Quality Issues

The biggest challenge identified by respondents in the design phase of RTPV development is the

difference in array layout in the installed systems versus the design layout derived after conducting a

shadow analysis using software such as PV Syst or PV Sol. For some reason, installers or EPC

contractors change the array layout on the ground, resulting in loss of generation and, in some cases, hot

spots

4

due to shadows that fall on part of the array. Incorrect array layout is a major error during the

design phase and can result in lower performance, which can significantly impact lifetime returns. This

issue can either be corrected or can be identified in a post-installation inspection (i.e., by checking if the

array layout on the ground conforms to the array layout on the design drawings). Similarly, our analysis

found another significant design problem that arose from the designer not matching the string voltage

with the maximum power point tracking (MPPT) voltage range of the inverter. Here again this issue can

lead to a loss of the returns of the system and can be rectified by checking if the string voltage is beyond

the inverter’s MPPT voltage range.

Another key issue identified during the design phase was the site access issue, which impacts O&M and

the quality of installation. In a number of cases, the site was not easily accessible, and workers had to take

unnecessary risks to get to the site for installation, or the site was developed in such a way that although it

was aesthetically attractive, the installation experienced generation losses due to alignment issues. Simple

precautions, such as ensuring permanent and easy access to equipment, could be incorporated during the

design phase. This issue is more apparent with arrays on superstructures where module cleaning may be

more challenging, thereby affecting performance adversely. A planned stormwater run-off system

4

Defects characterized by local overheating of solar cells.

19

This report is available at no cost from the National Renewable Energy Laboratory (NREL) at www.nrel.gov/publications.

integrated into the surrounding stormwater run-off system is also essential to avoid flooding, erosion of

foundations, and muddy ground which can prevent access.

In addition to these key concerns, other design-related issues involved improper cleaning methods for

modules, inadequate earthing provisions, and inadequate structural considerations for withstanding

weather conditions. These can have a significant impact on the life cycle returns of the project; however,

most of these issues can be avoided with good quality control, timely feedback, better training, and

awareness. A summary list of issues, along with frequency of occurrence and impact on project

development is listed in Appendix D; a complete list of issues and possible corrective actions is listed in

Appendix E.

4.2.2 Component-Related Quality Issues

Specifications and standards during the design stage dictate the identification and procurement of

components for the RTPV system. Based on discussions with stakeholders, it was found that almost 50%

of all quality issues resulted from procuring faulty or substandard components. A majority of the quality

and safety issues occurred with the module and the structure, followed by junction boxes.

In the case of structures, respondents agreed that full energy loss or complete system damage was

possible if a faulty structure was not rectified. Respondents felt that structure quality was difficult to map

and ensure but was critical for the long-term viability and sustainability of the systems. Some of the

specific quality issues highlighted by stakeholders for structures were:

• Material damage and defects (of both galvanized iron and aluminum structures)

• Poorly installed fasteners and mismatched component sizes

• Improper anchoring on sloped roofs

• Poor practices and incorrect equipment used in fixing modules onto a structure

• Design errors that result in an inability to withstand estimated dead load and wind pressure

• Post-construction inadequate finishing/ cleaning-up and waterproofing