A1

Final Submission to the

Productivity Commission’s

Inquiry into Competition in the

Australian Financial System

20 MARCH 2018

This document should be read in conjunction with the

Commonwealth Bank of Australia’s Initial Submission

(dated 15 September 2017)

| CommBank of Australia |

1

This page intentionally

left blank

| CommBank of Australia |

2

Contents

Executive summary ........................................................................................................................................................... 5

Chapter 1: Industry context ............................................................................................................................................. 9

1.1 Competition and regulation in the Australian financial system are healthy ................................... 9

1.2 Australia’s economic prosperity relies on a strong and stable financial system .......................... 17

1.3 The performance of the industry reflects the operating context ..................................................... 25

Chapter 2: Balancing competition and stability for economic prosperity ....................................................... 29

2.1 Change in regulators' roles and responsibilities .................................................................................. 29

2.2 Balancing macro-prudential regulation ................................................................................................... 33

2.3 Balancing non-macro-prudential regulation ......................................................................................... 37

2.4 Access to data and switching ..................................................................................................................... 41

Chapter 3. Examining industry practices for better customer outcomes ........................................................ 47

3.1 An effective and efficient payments system ......................................................................................... 47

3.2 Improving customer choice and outcomes in residential home lending ....................................... 51

3.3 Improving customer choice and outcomes in insurance .................................................................... 61

3.4 Improving customer choice and outcomes in financial advice ........................................................ 65

Cross reference of Draft Recommendations ........................................................................................................... 69

Cross reference of Draft Findings ............................................................................................................................... 70

Cross reference of Information Requests .................................................................................................................. 71

Glossary ..............................................................................................................................................................................72

| CommBank of Australia |

3

This page intentionally

left blank

| CommBank of Australia |

4

Executive summary

The Commonwealth Bank of Australia (CommBank) welcomes the Productivity Commission’s

(Commission) Inquiry into Competition in the Australian Financial System (Inquiry) on behalf of the

Australian Government (Government) and the Inquiry’s Draft Report (Draft Report).

CommBank believes a highly competitive banking system that is stable, fair, efficient and safe through

the economic cycle is good for customers, shareholders and the Australian economy. It is working hard

to create a better, stronger bank that focuses on customers’ wellbeing, leads on operational standards

and compliance, drives industry innovation, and contributes to communities and the economy in ways

that reflect its size and heritage.

CommBank also believes it is important to deliver a highly competitive proposition to customers whilst

ensuring responsible management of Australia’s largest financial institution.

Over the last decade, the level of competition in the Australian financial system has increased.

Innovations and regulatory changes have enabled new entrants and smaller competitors to compete

effectively, including relative to Australia’s four largest banks (collectively referred to as Australia’s

Major Banks).

For example, there is a long term declining market share trend for Australia’s Major Banks collectively

in home loan approvals and furthermore, there is significant volatility in underlying month on month

market share movements between competitors which highlights vigorous levels of competition.

Despite Australia being a relatively small economy, Australian financial services customers have access

to world-leading propositions with high levels of choice, innovation, accessibility and service quality.

Nonetheless, CommBank recognises that there will always be opportunities for the industry to

continue improving customer outcomes.

The intensity of competition in the Australian financial system is on par with other advanced

economies

1

and the industry is also highly productive by comparison

2

. These competitive dynamics

have delivered high customer satisfaction levels, reflected in the long term trend of increasing

customer satisfaction that has risen to over 80%

3

. It is also important to note that there is a decreasing

trend in customer dissatisfaction which is now less than 5%. CommBank is continually striving to better

understand the needs of all customers’ views, in particular by focusing on the individual concerns of

dissatisfied customers.

Australia has enjoyed over 26 years of uninterrupted economic growth

4

. This is globally

unprecedented. Given the procyclical nature of banking, it has naturally led to strong performance for

Australian banks. This has flowed through to support the broader economy; almost 80% of Australian

1 Bullock, M., 2017, Big banks and financial stability, delivered 21 July, www.rba.gov.au/speeches/2017/sp-ag-2017-07-21.html.

2 Boston Consulting Group, 2016, Retail Banking Excellence Benchmark (Australia’s Major Banks have lower operating expenses

per customer compared to the global median).

3 Roy Morgan Research, Retail MFI Customer Satisfaction, Australian population 14 years+, 6 month rolling average to January

2018. Includes ANZ, CommBank excluding Bankwest, NAB and WBC excluding St George Bank. Satisfaction includes percent

“very satisfied” or “fairly satisfied” with relationship with MFI and Dissatisfaction includes percent “very dissatisfied” or “fairly

dissatisfied” with relationship with MFI.

4 OECD, Main Economic Indicators Publication, available from OECD. Stat online: http://stats.oecd.org

| CommBank of Australia |

5

banks’ profits are returned to shareholders as dividends

5

and Australia’s Major Banks are amongst the

nation’s largest taxpayers

6

.

CommBank reiterates the importance of maintaining the stability and resilience of the Australian

financial system as the primary aim of policy, whilst also ensuring customers are protected and

competition is promoted for the benefit of customers. Systemic failures in banking typically result in

catastrophic fiscal and socio-economic outcomes, as recently demonstrated by the impact of the

Global Financial Crisis (GFC) on many advanced economies.

Financial system strength and stability, including perceptions of strength and stability, are particularly

important given the Australian financial system’s strong reliance on offshore wholesale funding in

supporting economic growth. To put this in perspective, Australia’s Major Banks alone raised almost

$100bn of long term wholesale funding in offshore markets in FY17

7

. During this period CommBank

raised $27bn offshore in long term wholesale funding, and renewed approximately $32bn offshore in

short term wholesale funding on average each month. The reliance of the Australian economy on the

strong credit ratings of Australia’s Major Banks and their ability to access offshore markets at scale was

critical in enabling CommBank to provide $135bn in new lending to Australian customers during this

period.

At some point in the future, Australia is likely to experience a recession. Australia’s regulatory settings

must ensure that the financial system has the strength and stability to absorb losses and support

economic recovery in this event. Whilst Australia’s financial system was not as impacted by the GFC as

many others, the factors that helped protect Australia’s economy then (such as persistent demand for

commodity exports and interest rates that were sufficiently high to enable expansionary monetary

policy) are unlikely to exist, at least to the same extent, entering into the next downturn.

CommBank believes that Australia’s regulatory framework is robust, comprehensive and appropriately

balanced to promote innovation and competition, protect customers, and maintain the stability and

resilience of the Australian financial system. Indeed, in November 2017 the international ratings

agency S&P Global Ratings said that the existing laws and regulations governing Australia's banks are

amongst the strongest in the world

8

.

Any regulation designed to stimulate competition should give consideration to “through the cycle”

implications, in particular the potential risks to customer protection, market integrity and/or financial

system stability in the event of an economic downturn or period of economic volatility. CommBank

continues to stress this view.

Whilst CommBank accepts many of the Draft Findings in the Draft Report, it rejects several of them

and in particular those relating to the state of competition in the financial system, consumers’ ability to

apply competition pressure, implications of oligopolistic market structure, perceptions of ‘too big to

fail’ and the Four Pillars policy. In CommBank’s view the conclusions drawn in these Draft Findings do

not give an appropriate and balanced assessment of the range of considerations that are relevant to

each of the respective topics.

5 ABA, https://www.banksbelongtoyou.com.au/

6 ATO, 2015-16 Report of Entity Tax Information, available online at:

https://data.gov.au/dataset/corporate-transparency

7 Australia’s Major Banks’ annual reports. Note: CommBank has a 30 Jun-17 year end. WBC, NAB and ANZ have a 30 Sep-17 year

end.

8 S&P, refer to AFR’s article “Australian banks the best regulated in the world: S&P” (29/11/2017)

| CommBank of Australia |

6

CommBank supports in principle or is unopposed to the majority of the Commission’s Draft

Recommendations. However, CommBank does not support the Commission’s Draft Recommendations

with regard to three matters:

The proposal to abolish interchange fees. The payments system is critical infrastructure for the

nation. Investment is necessary to provide security, stability and continuous innovation. There have

been successive reforms that have aimed to optimise interchange. Australia’s interchange fees are low

by global standards. There should be no further changes to these regulations until the Reserve Bank of

Australia (RBA) has had the opportunity to evaluate the effects of the most recent reforms introduced

last year.

The proposal for the Australian Prudential Regulation Authority (APRA) to develop an online tool

to report median interest rates on home loans. CommBank’s concern is this will likely have a number

of significant unintended consequences. Mortgage pricing is determined by a number of factors,

including a risk assessment of individual customers and external factors such as wholesale funding

costs. Publishing historical median interest rates without the relevant personal context is likely to

mislead customers and distort the decisions of lenders.

The proposal related to a duty of care for mortgage aggregators and brokers. CommBank supports

recommendations that aim to protect customers and puts their interests first. However CommBank

does not support the recommendation as currently expressed, as it applies only to aggregators owned

by lenders. This would cause confusion for consumers as different brokers would have different service

level obligations, and creates an unnecessarily uneven playing field for industry participants. Further, it

would be important to ensure that any duty of care obligations allow for brokers to consider price

together with the full range of product features that may be of value to customers, for example

physical branch networks, access to digital banking, product flexibility (redraw, offset, etc.).

CommBank looks forward to working constructively with the Commission, the Government and

regulators to address important design considerations to promote competition, protect customers and

maintain the stability and resilience of the Australian financial system.

| CommBank of Australia |

7

This page intentionally

left blank

| CommBank of Australia |

8

Chapter 1: Industry context

1.1 Competition and regulation in the Australian financial system are healthy

Key Points

• A highly competitive banking system that is stable, fair, efficient and safe through the

economic cycle is good for customers, shareholders and the Australian economy.

• There is vigorous competition between banks, demonstrated by high levels of customer

satisfaction, material monthly volatility in market share of flows; high levels of investment in

innovation; and high spend on marketing.

• Barriers to entry and expansion are low and falling and there is ongoing entry of new players

across all parts of the value chain.

• Australian banks are among the most efficient banks in the world, having a lower cost-to-

income ratio, lower cost-to-asset ratio and lower operating expenses per customer than in

most comparable countries.

• ROEs in banking are comparable to other industries in Australia, and lower in many

instances.

• Australia’s regulatory framework is superior to most mature markets and CommBank

supports the clear division of accountability between the RBA, APRA and the Australian

Securities and Investments Commission (ASIC) to ensure system stability, prudential

supervision, and customer protection and competition respectively. CommBank also

supports the role of the Council of Financial Regulators (CFR) to balance these objectives to

ensure Australia’s economic prosperity and the financial wellbeing of customers.

• In addition, CommBank supports the role and mandate of the Australian Competition and

Consumer Commission’s (ACCC) new Financial Services Unit.

Summary of Response to Draft Recommendations

• CommBank is unopposed to

Draft Recommendation 7.2 (Building an evidence base on

integration

).

Summary of Response to Draft Findings

• CommBank accepts

Draft Finding 2.1 (Key features of workable competition in the

financial system).

A highly competitive banking system that is stable, fair, efficient and safe through the economic cycle

is good for customers, shareholders and the Australian economy.

CommBank accepts

Draft Finding 2.1 (Key features of workable competition in the financial

system).

CommBank supports the Commission’s assessment of key features of workable competition and

believe these already exist in the Australian financial system today or, as in the case of Open Banking,

| CommBank of Australia |

9

will be implemented shortly. These features and how they apply to the Australian financial system are

discussed in detail throughout this submission.

CommBank supports competition and the ability for all Australians to choose a financial institution

which best suits their needs. CommBank has supported the industry's advancements in enhancing the

customer switching experience, while spearheading a number of initiatives to support customers to

switch banks easily.

As a result of vigorous competition for customers, customer satisfaction is high, and has been

increasing (refer Figure 1). As the figure shows, this has corresponded with declining customer

dissatisfaction.

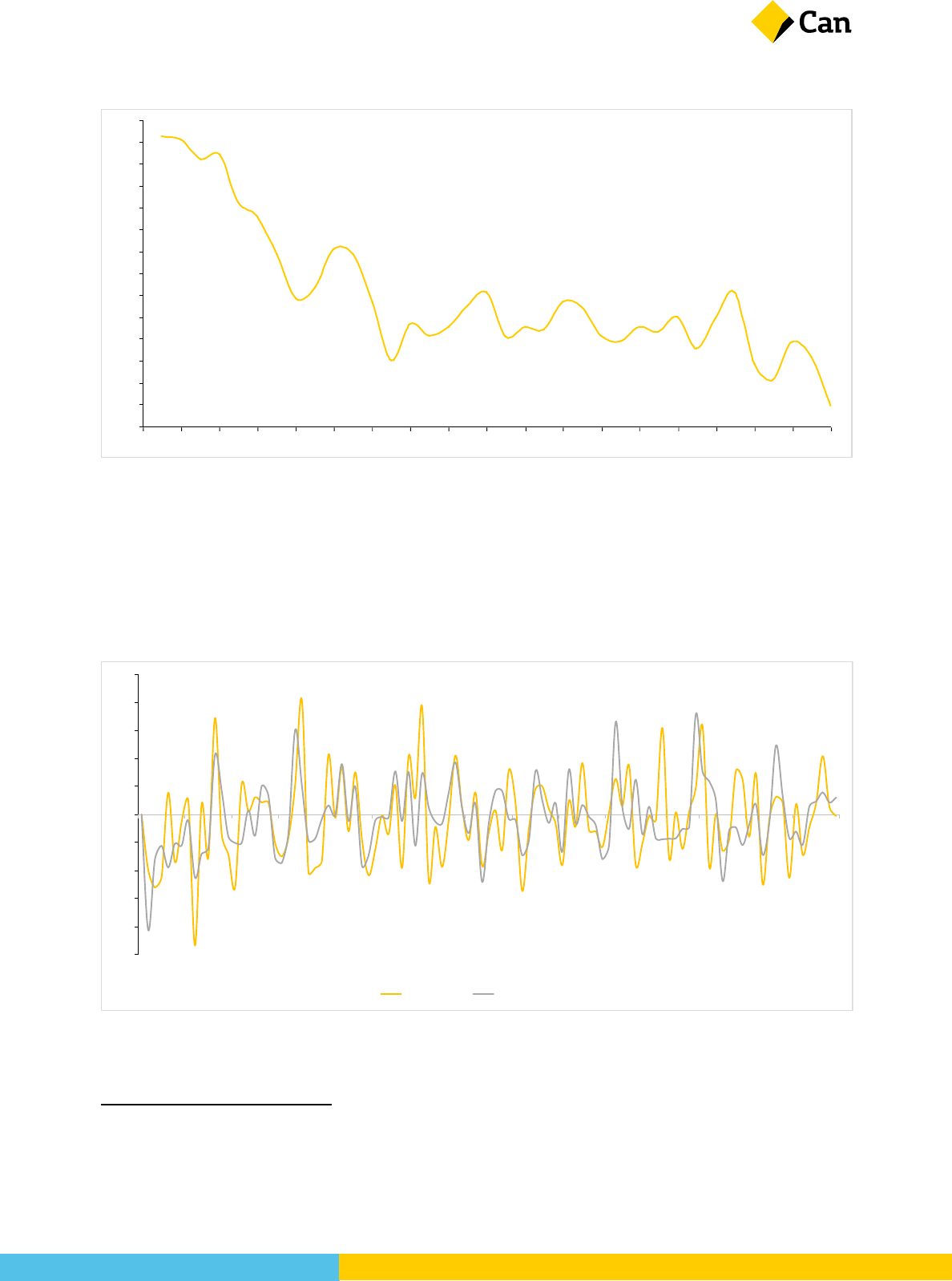

For example, from 2002 to 2018, the proportion of respondents in Roy Morgan’s Retail Main Financial

Institution (“MFI”) Customer Satisfaction survey who said they were “Very Satisfied” or “Fairly

Satisfied” with their MFI has increased from 61.2% to 81.1%, with the proportion of dissatisfied

respondents decreasing from 16.0% to 4.6%.

Similarly, in the seven years to January 2018, the proportion of business customers satisfied with their

MFI increased by 2.7 percentage points (from 76.5% to 79.2%) with the proportion of dissatisfied

customers decreasing by 2.9 percentage points (from 13.5% to 10.6%)

9

.

CommBank is continually striving to better understand the needs of all customers’ views, in particular

by focusing on the individual concerns of dissatisfied customers.

Figure 1: Retail MFI customer satisfaction for Australia’s Major Banks

10

9 DBM Business Financial Services Monitor, Jan 2018, Satisfaction with MFI, percentage of respondents who scored 0-4 and

6-10. Selected MFIs comprise only of ANZ, NAB, WBC, and CommBank excluding Bankwest, and Regional Banks including

Bendigo Bank, Bank of Queensland, Suncorp

10 Roy Morgan Research, Retail MFI Customer Satisfaction, Australian population 14 years+, 6 month rolling average to January

2018. Includes ANZ, CommBank excluding Bankwest, NAB and WBC excluding St, George Group. Satisfaction includes percent

“very satisfied” or “fairly satisfied” with relationship with MFI and Dissatisfaction includes percent “very dissatisfied” or “fairly

dissatisfied” with relationship with MFI

2007

0

100%

60

40

80

20

20082001 2002 2003 2005 20062004 201320102009 2012 2014 201720162011 20182015

Very Dissatisfied’ or ’Fairly Dissatisfied’Very Satisfied’ or ’Fairly Satisfied’

| CommBank of Australia |

10

High levels of technological innovation are a key indicator of a highly competitive banking system. In

addition to the world-leading digital banking solutions offered by Australian banks and the many other

leading innovations by Australian banks, such as Lock, Block and Limit or Cardless Cash (refer to

CommBank’s initial submission to the Inquiry (Initial Submission) for detail), Australian customers

have also benefited from global firsts in system innovation. Some world leading system innovations

include BPAY, which was launched in 1997 as a single bill payment service across the industry, PEXA,

the world's first digital settlement platform enabling digital registration and lodgement of property

titles and real-time financial settlement, and the New Payments Platform (NPP), one of the world’s

first real time payments settlement platforms.

Further evidence of vigorous competition in the Australian financial system is the direct marketing

spend per customer of Australia’s Major Banks which is on par with global peers

11

, and the substantial

investment made each year by participants to maintain and improve their businesses. CommBank

alone has invested over $1.2bn per annum on average over the last five years to improve and maintain

its franchise.

The intensity of competition is also further evidenced by trends in the market shares of Australia’s

Major Banks in home loans. In this context it is important to recognise that (a) there is a long term

declining market share trend for Australia’s Major Banks; and (b) there is significant volatility in

underlying month on month market share movements between competitors.

As noted by APRA in its initial submission to the Inquiry “In some cases, particularly for residential

mortgage lending, the four major banks have lost market share to smaller entities. […] the four major

banks’ share of mortgage approvals peaked at 86.3% in March 2009. By June 2017 this share had

fallen to 76.9%, reflecting a gradual but consistent downward trend”. This downward trend has since

continued and the share of mortgage approvals of Australia’s Major Banks was 74.0% in December

2017 (refer Figure 2 below).

11 Boston Consulting Group, 2016, Retail Banking Excellence Benchmark, Australia’s Major Banks median spend compared to

global median spend

| CommBank of Australia |

11

Figure 2: Market share of residential mortgage loans approved – Australia’s Major Banks (%)

12

Notwithstanding the long term declining market share trend for Australia’s Major Banks in key

products, of greater significance is the significant volatility in underlying month on month market

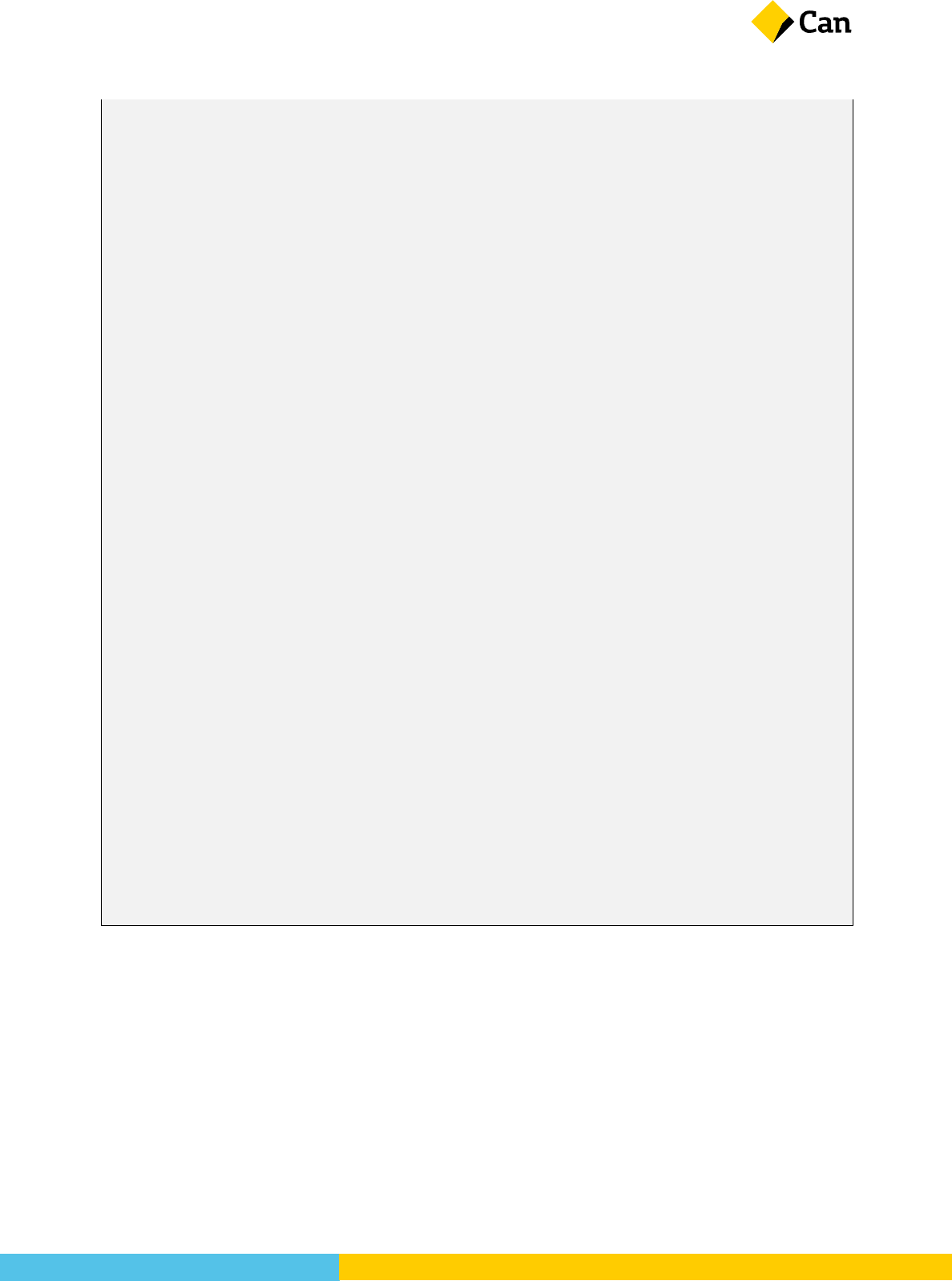

share movements between competitors. CommBank’s share of residential mortgage loans approved

varies significantly month on month, demonstrating intense competition to win customers (refer

Figure 3 below).

Figure 3: CommBank’s share of residential mortgage loans approved – percentage point change

month-to-month

13

12 APRA, Quarterly Authorised Deposit-taking Institution Property Exposures -December 2017 (released 13 March 2018)

www.apra.gov.au/adi/Publications/Pages/Quarterly-ADI-Property-Exposures-statistics.aspx

13 ABS for market data (5609 / 5671, November 2017), CommBank data

73%

74%

75%

76%

77%

78%

79%

80%

81%

82%

83%

84%

85%

86%

87%

Jan-15Jul-13 Jul-14Jul-12 Jan-18Jan-13 Jul-17Jul-15 Jan-17Jul-16Jan-16Jan-14Jul-09 Jan-11Jan-10 Jan-12Jul-10Jan-09 Jul-11

-5%

-4%

-3%

-2%

-1%

0%

1%

2%

3%

4%

5%

Mar-09 Oct-09 May-10 Dec-10 Jul-11 Feb-12 Sep-12 Apr-13 Nov-13 Jun-14 Jan-15 Aug-15 Mar-16 Oct-16 May-17

Investment Owner Occupied

| CommBank of Australia |

12

New market entrants and emerging business models have contributed to today’s highly competitive

financial services sector with numerous, diverse providers. In addition to Australia’s Major Banks,

customers can choose to meet their financial service needs through regional banks, credit unions and

mutuals, non-bank lenders, non-financial consumer brands (for example, Qantas, Coles) as well as a

growing range of global technology businesses (for example, PayPal, AliPay) and FinTechs.

In addition there is growing fragmentation of value chains and new entrants are building scale

businesses in areas such as payments and home loan distribution.

The intensity of competition in Australia’s financial system is also evidenced through the focus that

Australian banks have had on being highly productive.

Australian banks are among the most efficient banks in the world, having a lower cost-to-income ratio,

lower cost-to-asset ratio and lower operating expenses per customer

14

than in most comparable

countries (refer Figures 4 and 5). This reflects ongoing investment in technology which boosts

productivity as well as improving customer service levels and outcomes.

Figure 4: Large banks’ cost-to-income ratios (%)

15

14 Boston Consulting Group, 2016, Retail Banking Excellence Benchmark (Australia’s Major Banks have lower operating

expenses per customer compared to the global median)

15 Bullock, M., 2017, Big banks and financial stability, delivered 21 July, available online:

https://www.rba.gov.au/speeches/2017/sp-ag-2017-07-21.html (underlying source of graph: RBA; S&P Global Market Intelligence)

Market share of the five largest banks

79.1

69.3

61.2

61.0

45.0

Canada UKEuro area USAAustralia

| CommBank of Australia |

13

Figure 5: Banks’ cost-to-asset ratios (%)

16

As noted in CommBank’s Initial Submission, Australian banks have generally outperformed global

peers as the Australian economy has performed strongly, against a backdrop of global volatility and

off-shore banks operating in challenging economic conditions. Despite this, it is worth noting that the

ROE of the Australian banking industry is below the weighted average of ASX200 companies (refer

Figure 6).

Figure 6: ROE across industry sectors in Australia (%)

17

16 Cost-to-Assets calculated as sum of Total Non-Interest Expenses divided by sum of Total Assets for Primary Banks in each

country (Diversified Financials excluded). S&P Capital IQ, PwC Analysis

17 Credit Suisse

1.8

1.7

1.6

1.5

1.5

1.4

1.2

1.1

Italy USASpain CanadaUKGermanyNetherlandsAustralia

7.8

8.8

8.9

11.5

12.1

13.8

13.8

14.3

15.2

15.6

17.1

17.4

19.6

21.8

23.2

24.6

35.9

Health care

Information Technology

Telecoms

Utilities

Banks

Insurance

REITs

Energy

Materials

Staples

ASX 200

Retailing

Consumer Discretionary

Financials

Industrials

Media

Metals & Mining

Industry median

excluding banks 15.2%

| CommBank of Australia |

14

Australia’s regulatory framework is superior to most mature markets. CommBank supports the clear

division of accountability between the RBA, APRA and ASIC to ensure system stability, prudential

supervision and customer protection respectively. CommBank also supports the role of the CFR to

balance these objectives to ensure Australia’s economic prosperity and the financial wellbeing of

customers. The strength of this system has contributed greatly to the prosperity of the country as was

evidenced by the strength of the Australian banks relative to banks in the USA, UK and other European

countries when the GFC occurred. Unlike Australia, banking systems in those countries had been more

highly deregulated to drive competition which led to unfavourable competitive activity and ultimately

facilitated the GFC.

The strength of Australia’s financial system regulation was recognised externally in November 2017 by

the CEO of Standard & Poor’s who noted that the regulations governing Australia's banks are amongst

the strongest in the world

18

.

Notwithstanding this, there have been a number of financial system policy developments in recent

years, including new capital adequacy requirements for Authorised Deposit-taking Institutions (ADIs),

the extension of APRA’s powers with respect to provision of credit by non-ADI lenders, the

development of a phased licensing approach for ADIs, ASIC’s regulatory ‘sandbox’ and Future of

Financial Advice (FOFA).

‘Competition vs regulation’ in the financial services industry and the role of capital have been debated

across the globe. The Basel III and accounting standard reforms were a sweeping set of reforms

designed to prevent bailing out of banks by governments and their taxpayers in the event of financial

crises like the GFC.

In this regard, APRA’s Chairman, Wayne Byres has often referred to the ‘regulatory pendulum’. In his

speech titled “Achieving a stable and competitive financial system”, he mentioned the positive mutual

reinforcement of competition and stability, rather than the opposition

19

:

“To borrow a phrase, we don’t want ‘the stability of a graveyard’. But we have all seen

instances of excessive, or reckless, competition too. Eliminating the excess, and finding the

optimum level of both, is a matter of careful balance. And, if we get the balance right, they

will be mutually reinforcing: competition will support stability, and stability will support a

competitive environment.” […] “Much of the policy debate over recent years has been cast in

terms of a trade-off between stability and competition in the financial system. We have never

seen it that way, and were pleased that the FSI reached the same conclusion. Good regulatory

settings can deliver financially strong competitors, creating both financial stability and a

dynamic and innovative marketplace for financial services.”

CommBank reiterates that over the last decade, the level of competition in the Australian financial

system has increased, as innovations in technology and changes to regulation have enabled new

entrants and smaller competitors to compete effectively. Despite Australia being a relatively small

economy, Australian financial services customers have access to world-leading propositions with high

levels of choice, innovation, accessibility and service quality. Nonetheless, CommBank recognises that

there will always be opportunities for the industry to continue improving customer outcomes.

18 S&P, refer to AFR’s article “Australian banks the best regulated in the world: S&P” (29/11/2017)

19 Wayne Byres, “Achieving a stable and competitive financial system”, AFR Banking & Wealth Summit, Sydney, 29 April 2015

| CommBank of Australia |

15

The intensity of competition in the Australian financial system is on par with other advanced

economies and the industry is also highly productive by comparison. These competitive dynamics have

delivered high customer satisfaction levels. CommBank supports measures that promote vigorous

competition and is unopposed to

Draft Recommendation 7.2 (Building an evidence base on

integration)

.

| CommBank of Australia |

16

1.2 Australia’s economic prosperity relies on a strong and stable financial system

Key Points

• Economies of scale are a primary driver of the profitability of Australia’s Major Banks relative

to other Australian banks.

• Although Australia’s Major Banks experience a lower cost of funding, the relativity between

their cost of funding and that of other Australian banks has been contracting over time.

• The sophistication in risk systems from banks investing to attain internal ratings-based (IRB)

accreditation provides a benefit for financial system stability, investors and deposit holders.

• The structure of Australia’s financial system in terms of market concentration is similar to

other countries which are comparable to Australia.

• Australia’s reliance on offshore funding to fund the current account deficit means that

Australia needs large, strong banks with good credit ratings to access global wholesale

funding markets at scale.

• Systemic failures stemming from weakened prudential regulation / absence of

“unquestionably strong” banks typically result in catastrophic fiscal and socio-economic

outcomes.

Summary of Response to Draft Findings

• CommBank rejects

Draft Finding 5.1 (Cost of funds for different size banks

).

• CommBank rejects

Draft Finding 3.1 (The major banks’ oligopoly power)

.

• CommBank accepts

Draft Finding 4.1 (A consolidation in banking).

• CommBank rejects

Draft Finding 16.1 (Ratings agencies exacerbate the perception of ‘too

big to fail’)

.

• CommBank rejects

Draft Finding 16.2 (The Four Pillars policy is redundant

).

A primary driver of profitability of Australia’s Major Banks compared to other Australian banks is

economies of scale. As outlined later in this chapter, Australia’s reliance on offshore funding means

that Australia needs large, strong banks with good credit ratings to access global wholesale funding

markets at scale.

CommBank rejects

Draft Finding 5.1 (Cost of funds for different size banks

). It is important that

Australian banks are profitable and that they have a positive outlook when competing for the lowest

cost, and potentially scarce, funding. Australia’s Major Banks have traditionally experienced a lower

cost of funding compared to the other Australian banks. The lower cost of funding is function of the

following key factors:

• Strong credit ratings (a function of diversity of income, scale of operations, confidence of

investors, history of successful execution of business strategy, prudent liquidity, funding and

capital management, and external conditions such as system stability);

• Ability to access diverse sources of funds, including international capital markets; and

• Competitive deposit pricing.

| CommBank of Australia |

17

However, it should be noted that whilst Australia’s Major Banks experience a lower level cost of

funding, the relativity between Australia’s Major Banks and the other Australian banks cost of funding

has been contracting since the shock of the GFC (refer Figure 7).

Figure 7: Banks’ Debt Funding Costs

20

In general, Australia’s Major Banks proportionally hold less capital for the same assets compared to the

smaller banks. This capital efficiency is partly due to the fact that Australia’s Major Banks (and

Macquarie Bank, as well as ING Bank (Australia) from 1 April 2018) are permitted to use the IRB

approach to credit risk to determine their capital requirements. The IRB approach allows banks to use

their own internal assessment of risk to determine the risk-weighting for loans and is a more risk

sensitive measure than the standardised approach that is used by the smaller banks. The resultant

impact of this is that Australia’s Major Banks have been able to operate with a proportionally lower

level of capital (refer Figure 8).

Figure 8: Australian Banks’ Profitability and Leverage

21

20 APRA, RBA. Quarterly, by type. *Selected non-major banks.

21 APRA. Leverage Ratio denotes Tier 1 capital as a share of total assets. Break in March 2008 due to the introduction of Basel II;

break in March 2013 due to introduction of Basel III.

Major banks

Other Australian Banks*

Major banks

Other Australian Banks*

| CommBank of Australia |

18

The IRB approach is available to all banks but in order to use it, a bank must be accredited by APRA. To

obtain accreditation, a bank must demonstrate that its internal models can produce reliable, risk-

sensitive, and comparable estimates of the capital required at the predetermined soundness

standards. Significant investments have been made and are required on an on-going basis for

Australia’s Major Banks to achieve and maintain their IRB accreditation.

The reduced capital required by the IRB accreditation is regarded as a strong incentive for banks to

continue increasing the sophistication of risk systems. Such sophistication in risk systems provides a

benefit for institutional financial stability, investors and deposit holders.

However, the relative benefit from IRB accreditation has reduced in recent years given the recent

regulatory changes imposed by APRA have required Australia’s Major Banks to materially increase

their capital levels

22

. In addition, ING Bank (Australia) received IRB accreditation from APRA on 19

March 2018

23

, and CommBank understands that several other non-IRB accredited banks are currently

going through the accreditation process with APRA.

CommBank rejects

Draft Finding 3.1 (The major banks’ oligopoly power)

and would note that

concentration with a given market is not, per se, an indication of the degree of competition in a

market.

Notwithstanding this, concentration levels in Australia are comparable to other relevant countries,

particularly when compared to the size of the economy. As the RBA has noted, Australia is by no

means unique when it comes to the concentration of the banking sector. Among advanced economies,

the market share of Australia’s largest five banks is comparable to that of the Netherlands, Sweden

and Canada

24

. By global standards, the level of concentration is consistent with the size of the

population (refer Figure 9).

22 APRA, 2017, Information Paper: Strengthening banking system resilience – establishing unquestionably strong capital ratios,

available online at:

www.apra.gov.au/adi/Documents/Unquestionably%20Strong%20Information%20Paper.pdf

23 APRA announcement 19 March 2018

24 RBA, “Big Banks and Financial Stability”, July 2017, https://www.rba.gov.au/speeches/2017/sp-ag-2017-07-21.html

| CommBank of Australia |

19

Figure 9: Relationship between financial system concentration and population size

25

In addition, Australian consumers have a similar number of banking relationships as consumers in peer

markets, even in markets which have a significantly higher number of banks (refer Figure 10).

Figure 10: Number of Banking Relationships per consumer

26

CommBank accepts

Draft Finding 4.1 (A consolidation in banking)

however would note that

although the GFC led to a significant rationalisation of ADIs, with the number declining by 80 over the

10 years to 2016

27

, much of this change was a result of credit unions and building societies merging

and/or becoming banks. This corresponded with a rise in the number of banks, with banks now the

most common type of ADI.

If Australia’s banks (particularly Australia’s Major Banks) were to operate at a lower level of

profitability, this could negatively affect their credit ratings as profitability and capital generation is one

of the key factors considered by rating agencies in their assessment of credit ratings. A lower credit

25 The World Bank, 2016, https://data.worldbank.org/indicator/SP.POP.TOTL /

26 McKinsey, 2016, Retail Banking Consumer Survey; Australia Personal Financial Services Survey 2014

27 APRA, Quarterly Authorised Deposit-taking Institution performance, available online at:

www.apra.gov.au/adi/Publications/Pages/adi-quarterly-performance-statistics.aspx

0.1 1.0

10.0

75

25

100

50

Canada

France

UK

US

Japan

Italy

Germany

Sweden

Netherlands

Australia

Spain

Market share of

the largest five banks (%)

Share of

world population (%)

(log scale)

2.1

2.0

1.9

Australia Core EuropeCanada and USA

| CommBank of Australia |

20

rating would result in either an increase in the cost of funding and/or a reduction in the level of capital

imported into the Australian economy by banks.

This is an important consideration for Australia because the contribution of banks to facilitating private

sector growth in the economy is higher than most other mature markets

28

. To put this in context,

Australia’s Major Banks alone raised almost $100bn of long term wholesale funding in offshore

markets in FY17

29

. During this period, to enable it to provide $135bn in new lending to Australian

customers, CommBank raised $27bn offshore in long term wholesale funding and renewed

approximately $32bn offshore in short term wholesale funding on average each month.

This ability to access offshore markets at scale and to fund Australia’s current account deficit, both in

normal and stressed macro-economic conditions, is critical to the prosperity of the Australian

economy. This takes on greater importance as regulators increase focus on net stable funding ratios.

It is also critical that Australia’s Major Banks are sufficiently profitable in order to generate capital

(through retained earnings) to absorb losses. A consequence of insufficient profitability is lower

organic capital generation, which in turn results in a possible constraint on the growth of balance

sheets and limits the ability to absorb losses.

To bring this to point to life, industry Loan Impairment Expenses (LIE) are currently at historical lows

which is reflective of this point in the economic cycle. If all other things remained equal and

CommBank’s LIE was to increase to a level experienced by the UK banks during the GFC, it would likely

result in a negative Return on Equity (ROE) for CommBank

30

.

Systemic failures stemming from weakened prudential regulation or the absence of “unquestionably

strong” banks typically result in catastrophic fiscal and socio-economic outcomes, as recently

demonstrated by the impact of the GFC on many advanced economies. While bank bail-outs by

governments represent a direct fiscal cost, disruption of the banking sector typically also results in

indirect costs such as a reduction in the availability of credit to consumers and businesses and

weakening demand in the economy

31

. As banking crises may not occur in isolation, it is difficult to

separate indirect costs attributable to bank failure from the impact of economic conditions that

resulted in bank failure, for example a reduction in export demand. Regardless, the size of such costs

may be considerable compared to the direct bail-out costs (refer Figure 11).

28 Bank for International Settlements, June 2017, Database: Credit to the non-financial sector, available online at:

www.bis.org/statistics/totcredit.htm

29 Australian Major Banks’ annual reports. Note: CommBank has a Jun-17 year end. WBC, NAB and ANZ have a Sep-17 year end.

30 High level internal estimate based on LIE levels experienced in UK market during GFC (UK FY09 Peak average 258 bps)

31 Frontier Economics

| CommBank of Australia |

21

Figure 11: Direct and indirect costs of banking crises during the GFC

32

Banking failures in the Republic of Ireland and the Netherlands resulted in large direct fiscal costs,

owing to the cost of government support for failing banks, in addition to substantial increases in public

debt and output loss that may be attributed to the bank failures (and the GFC in general). The

systemic failures in the USA and UK also resulted in significant direct and indirect costs to these

economies.

CommBank rejects

Draft Finding 16.1 (Ratings agencies exacerbate the perception of ‘too big to

fail’)

. Australia’s Major Banks have an advantage in accessing capital markets by virtue of their credit

ratings relative to smaller banks. This reflects the fundamental characteristics, such as size, ability to

manage risk and balance sheet strength, and the probability of Government support in times of stress.

General Government support for the whole banking industry is important, and is critical in periods of

stress. It is worth noting that there is a difference between an implicit Government guarantee for

particular banks and general Government support for all banks. As demonstrated during the GFC, the

Government provided support to all banks.

Governments and central banks have long been recognised as lenders of last resort to the banking

sector. Guaranteeing the debt of banks to enable them continued access to capital markets is an

indirect way of fulfilling this role, and the precise nature of the guarantee does not need to be

determined until the time it is needed, when the risk can be better judged. While ratings agencies each

hold similar expectations of Government support, they differ in their assessment of the associated

ratings uplift from the expected support. The views of ratings agencies and capital markets persist

despite the absence of direct policies or statements from the Government on the matter. However, the

Government’s conduct in the wake of the GFC demonstrated that it has an appetite to support all

banks.

Quantifying the extent of any funding advantage from the uplift in credit ratings is complex

33

. The size

of a bank can affect perceptions of its creditworthiness but size is also part of the ratings agencies’

belief that Government support will be provided in a crisis. The RBA indicates that the funding

advantage rises and falls over time. For example, the funding advantage for Australia’s Major Banks

32 Laeven and Valencia, “Systemic Banking Crises Database: An Update”, International Monetary Fund Working Paper 12/163,

2012

33 RBA – implicit guarantee for banks, available online at: https://www.rba.gov.au/information/foi/disclosure-log/pdf/151609.pdf

0%

20%

40%

60%

80%

100%

120%

United States United Kingdom Netherlands

Ireland

% of pre-crisis GDP

Fiscal costs (direct)

Increase in public debt (indirect)

Output loss (indirect)

| CommBank of Australia |

22

was estimated to have fallen to around 10 basis points in late 2014 (a time of relative stability for

financial markets and the financial system) whereas there are estimates of a 120 basis point advantage

in 2009 (a time of heightened instability for financial markets and the financial system).

CommBank acknowledges that the funding advantage for Domestic Systemically Important Banks

(versus smaller banks) can become material in times of heightened instability for financial markets.

However, from a competition perspective it is not wise to attempt to nullify advantages that derive

from good business practices and fundamental differences in risk to the stability of the financial

system.

If the Government is to address the effects of a perceived "implicit guarantee" for Australia's Major

Banks, the best way to minimise the impact would be to continue to increase the resilience of the

financial system, as recommended by the Financial System Inquiry (FSI).

CommBank rejects

Draft Finding 16.2 (The Four Pillars policy is redundant

). As indicated in

CommBank’s FSI response, it continues to support the Four Pillars policy, which operates to prevent a

merger between any of the large banks, reflecting a decision by the Government to prevent further

consolidation in the market.

| CommBank of Australia |

23

This page intentionally

left blank

| CommBank of Australia |

24

1.3 The performance of the industry reflects the operating context

Key Points

• Australia’s unprecedented period of economic prosperity has underpinned the strong

performance of the Australian financial system relative to the UK, USA and Europe.

• Australia will experience a recession at some point in the future and this will have a negative

impact on the profitability of Australia’s banks and test the resilience of Australia’s financial

system.

• While Australia’s Major Banks have better economies of scale than other Australian banks,

the difference in ROE has been steadily declining since the GFC.

• Any evaluation of the state of competition must recognise the complex nature of

interdependencies that govern the economics, stability, and safety of the financial system.

Summary of Response to Draft Findings

• CommBank rejects Draft Finding II.1 (State of competition in the financial system).

When compared to international peers in the USA, UK and Europe since the GFC, Australia’s banks

have been relatively more profitable, partly reflecting the unprecedented period of uninterrupted

economic growth in Australia and the continued strength of the housing sector in Australia.

One of the drivers of Australia’s outperformance is the simpler asset mix of the Australian banks.

Returns for Australian and Canadian banks, which have comparatively simple structures, or lower

exposure to trading and institutional banking, have been higher than most other jurisdictions since the

crisis

34

.

The GFC severely damaged major economies across the world, yet Australia proved resilient. Despite

higher unemployment and slow economic growth, Australia did not suffer a large financial crisis. There

were several reasons for the resilience of the Australian economy during the GFC. The RBA typically

refers to the following

35

:

• Australian banks had limited exposure to the USA housing market and USA banks;

• Australian banks had pursued limited high risk / subprime lending in Australia;

• The resource boom, including exports to China whose economy rebounded quickly from the

GFC; and

• Policy response: the RBA lowered the cash rate substantially, and the Government undertook

expansionary policy while providing support for deposits and bonds issues by the banking

sector.

At some point in the future, Australia will experience a recession. When this happens, Australia’s

regulatory settings must ensure that the financial system has the strength and stability to absorb

losses and support economic recovery. Whilst Australia’s financial system was not as impacted by the

34 RBA, initial submission, page 11

35 https://www.rba.gov.au/education/resources/explainers/pdf/the-global-financial-crisis.pdf?v=2018-03-15-20-14-42

| CommBank of Australia |

25

GFC as many other countries’ financial systems, the factors that helped protect Australia’s economy

then (such as persistent demand for commodity exports and interest rates that were sufficiently high

to enable expansionary monetary policy) are unlikely to exist, at least to the same extent, entering into

the next downturn.

As a result of the financial system shock created by the GFC, the ROE of Australia’s Major Banks was

higher than other Australian banks for a period of time however, this gap has narrowed significantly

over the period and is now approximately 4% (refer Figure 12). This has been primarily due to an

increase in capital requirements for Australia’s Major Banks and, as credit spreads for the non-major

banks have decreased over time, an improvement in the Net Interest Margin (NIM) of the other

Australian banks.

Figure 12: ROE gap - Majors vs. other Australian-owned Banks

36

As APRA has pointed out in its initial submission to the Inquiry, average ADI ROE for the 12 months to

30 June 2017 was 11.7%, below the 10 year average of 13.4% (which itself has declined in recent years).

This should be considered in the context of Australia’s unprecedented period of economic prosperity

and industry LIE being at historically low levels. As noted earlier, if all other things remained equal and

CommBank’s LIE was to increase to a level experienced by the UK banks during the GFC, it would likely

result in a negative ROE for CommBank.

In response to the Commission’s assertions presented during the Inquiry’s public hearings that the

NIM of Australia’s Major Banks has remained stable for several years, and that “major banks have the

ability to pass on cost increases and set prices that maintain high levels of profitability”, CommBank

notes the following for consideration:

• The NIMs of Australia’s Major Banks has been trending down consistently for over 20 years

(refer Figure 13).

• NIM measures only a subset of profitability. A more comprehensive measure of profitability is

ROE as this accounts for NIM and all other costs and incomes, for example, operating

expenses, LIE, other (non-interest) income, etc. One example of this is the relative decline in

36 APRA Quarterly Authorised Deposit-taking Institution Performance, December 2017 (released 13 March 2018)

-9%

-6%

-3%

0%

3%

6%

9%

12%

15%

18%

Mar

2008

Sep

2008

Mar

2009

Sep

2009

Mar

2010

Sep

2010

Mar

2011

Sep

2011

Mar

2012

Sep

2012

Mar

2013

Sep

2013

Mar

2014

Sep

2014

Mar

2015

Sep

2015

Mar

2016

Sep

2016

Mar

2017

Sep

2017

ROE gap - Majors vs. other Australian-owned Banks

Linear (ROE gap - Majors vs. other Australian-owned Banks)

Linear trend

| CommBank of Australia |

26

fees which have benefited customers in recent years that would not be reflected in NIM (refer

Figure 14).

• As noted earlier, industry ROEs, particularly the ROEs of Australia’s Major Banks, have declined

in recent years. This fall in profitability is evidence that Australia’s Major Banks cannot simply

“pass on cost increases and set prices that maintain high levels of profitability” and that

competition is vigorous.

• Cost of funding is not determined only by the RBA’s Official Cash Rate. Whilst there is some

correlation, off-shore funding markets also have a significant influence on cost of funding.

Figure 15 shows the cost of funding spread for CommBank and how this is not highly

correlated to the RBA’s Official Cash Rate. This chart also shows how CommBank’s spread has

declined since the GFC.

• Larger banks benefit from the economies of scale in operating costs and funding costs and

thus, all other things being equal, one would expect Australia’s Major Banks to be more

profitable than the other Australian banks in an effective and competitive market.

Figure 13: Australia’s Major Banks’ Net Interest Margin

37

37 RBA, Bank financial reports, domestic, half yearly. From 2006 data on IFRS basis; prior years on AGAAP. Excludes St George

Bank and Bankwest prior to the first half of 2009.

| CommBank of Australia |

27

Figure 14: Banking Fees in Australia

38

Figure 15: CommBank’s funding costs vs RBA Cash Rate

39

An evaluation of the state of competition in the industry must recognise the complex

interdependencies between all the considerations raised in this chapter. On balance, CommBank

rejects

Draft Finding II.1 (State of competition in the financial system)

.

38 RBA, June 2017, Domestic banking fee income, available online at:

https://www.rba.gov.au/publications/bulletin/2017/jun/pdf/bu-0617-4-banking-fees-in-australia.pdf. Adjusted for breaks in series

in 2002 due to a change in banks’ reporting; financial-year average assets and deposits have been used.

39 RBA, Cash Rate available online at:

https://www.rba.gov.au/statistics/cash-rate/

Deposit fee income

Other non-deposit fee income

Lending fee income

0%

1%

2%

3%

4%

5%

6%

7%

8%

Interest revenue from assets

Interest expense from liabilities

Dec 04 Dec 06 Dec 08 Dec 10 Dec 12 Dec 14 Dec 16

RBA Cash Rate

FY05:

Spread = 2.08%

1H18:

Spread =

1.92%

Dec 17

| CommBank of Australia |

28

Chapter 2: Balancing competition and stability for

economic prosperity

2.1 Change in regulators' roles and responsibilities

Key Points

• Australia has a robust regulatory framework.

• Financial system stability should be a primary aim of policy, whilst also ensuring customers

are protected, and promoting competition. Design of regulation must be guided by “through

the cycle” implications.

• CommBank supports in principle the need for a regulator to be mindful of competition

outcomes and notes the Minister for Revenue and Financial Services’ announcement of

ASIC’s new competition mandate (19 March 2018).

Summary of Response to Draft Recommendations

• CommBank supports in principle

Draft Recommendation 15.1 (Statements of expectations

for regulators)

.

• CommBank supports in principle

Draft Recommendation 17.1 (New competition functions

for a regulator)

, however urges caution and further consultation with regulators in relation

to a number of features of the proposal.

• CommBank supports in principle

Draft Recommendation 17.2 (Transparency of regulatory

decision making)

, but urges caution and has concerns regarding the delays to regulatory

decisions and/or confidentiality considerations.

• CommBank supports in principle

Draft Recommendation 17.3 (Robust and transparent

analysis of macro-prudential policies)

, but urges caution and has concerns regarding the

delays to regulatory decisions and/or confidentiality considerations.

Summary of Response to Draft Findings

• CommBank notes

Draft Finding 2.2 (Competition and stability must co-exist).

• CommBank rejects

Draft Finding 6.1 (Cost of APRA interventions on home loans

).

• CommBank notes

Draft Finding 15.1 (APRA not well placed to consider competition in the

financial system)

. CommBank notes that the Commission's draft report proposes the CFR to

assess the competition related implications of regulation. As a member of CFR, APRA would

be involved in this process.

CommBank supports the current regulatory framework and believes that it is robust, comprehensive

and appropriately balanced to promote competition, preserve financial system stability and protect

customers. Indeed, in November last year the international ratings agency S&P Global Ratings said

| CommBank of Australia |

29

that the existing laws and regulations governing Australia's banks are the amongst strongest in the

world

40

.

CommBank reiterates Recommendation 4 of its Initial Submission that any regulation designed to

stimulate competition should give consideration to “through the cycle” implications, in particular the

potential risks to customer protection, market integrity and/or financial system stability in the event of

an economic downturn or period of economic volatility.

CommBank also takes this opportunity to reiterate the importance of maintaining financial system

stability as the primary aim of policy, whilst also ensuring customers are protected and competition is

promoted for the benefit of customers. Systemic failures have led to materially adverse outcomes for

the broader economy in other countries such as Ireland and the UK, with broad fiscal and socio-

economic impacts.

As such, CommBank notes

Draft Finding 2.2 (Competition and stability must co-exist)

, but notes

that financial system stability, and the perception thereof, should remain of primary importance for

policy and supervision in financial services. Where there is a conflict or any doubt between financial

stability and other considerations such as competition, it is critical that stability should prevail in those

circumstances.

CommBank supports in principle

Draft Recommendation 15.1 (Statements of expectations for

regulators)

. As stated in its submission to the FSI, CommBank has already supported the use of these

statements to establish principles or boundaries around which regulation is formed. CommBank also

notes that the Minister for Revenue and Financial Services announced that the Government has settled

on the new statement of expectations for ASIC (19 March 2018).

CommBank believes a regulator’s statement of expectations should ensure that future regulation

should be guided by its “through the cycle” implications. CommBank also supports Statements of

Intent to be published by regulators as a matter of good practice (however further consideration

should be given to the proposed three month time period). CommBank supports in principle the need

for regulators to provide in their annual reports the actions they are taking in line with Statements of

Intent. However, CommBank also recognises that there might be some specific decisions / actions

taken by regulators that might need to remain confidential for an extended period of time. CommBank

believes that regulators are in a better position to comment on such circumstances.

CommBank supports in principle

Draft Recommendation 17.1 (New competition functions for a

regulator)

.

As noted above, CommBank supports in principle the recommendation that regulator

Statements of Expectations are updated and Statements of Intent are published by regulators.

CommBank supports in principle the need for regulators to be more mindful of competition outcomes.

However, CommBank urges caution and further consultation with the regulators in relation to the

following proposal raised by the Commission: “[including] transparent analysis of competition impacts

to be tabled in advance of measures proposed by regulators” - some regulatory decisions need to be

made quickly in order to preserve financial stability, consumer outcomes or market integrity. Examples

could include recovery and resolution interventions, bailouts, and short selling prohibitions.

CommBank also does not support the creation of any significant regulatory uncertainty where industry

may be required to immediately respond to regulatory measures only to subsequently be asked to

unwind this response after a competitive assessment requiring transparency (such as in Draft

40 S&P, refer to AFR’s article “Australian banks the best regulated in the world: S&P” (29/11/2017)

| CommBank of Australia |

30

Recommendation 17.2) over all regulatory decisions. As mentioned above, CommBank recognises that

there might be some specific decisions / actions taken by regulators that might need to remain

confidential and for an extended period of time.

CommBank supports in principle

Draft Recommendation 17.2 (Transparency of regulatory decision

making)

, but urges caution. Indeed, some additional transparency around the CFR’s deliberations and

decision making process would provide industry with useful insights into regulators’ expectations and

intentions. However, as noted above, CommBank has concerns regarding the delays to regulatory

decisions and/or confidentiality considerations. CommBank believes that its regulators are in a better

position to provide a more comprehensive view on the specific considerations of such challenges.

CommBank supports in principle

Draft Recommendation 17.3 (Robust and transparent analysis of

macro-prudential policies)

. However, CommBank would welcome clarity as to which prudential

regulatory decisions / actions the Commission considers to be potential areas of ‘macro-prudential

policies’ and thereby subject to the Commission’s proposal to ensure ‘robust and transparent analysis’.

As stated above, CommBank has some concerns regarding delays to regulatory decisions and/or

confidentiality considerations. For example, the future requirement to review a decision annually and

publicly may result in the regulators taking a slower approach to their decision making in situations

where a swifter approach is necessary.

Provided this concern is addressed, CommBank welcomes

Draft Recommendation 17.3

(

Robust and

transparent analysis of macro-prudential policies)

in principle. More generally, it is important that

APRA continues to clearly articulate the intent of proposed macro-prudential policies, consults widely

and evaluates the outcomes.

CommBank rejects

Draft Finding 6.1 (Cost of APRA interventions on home loans

) (i.e. assertion that

“competition between lenders was restricted, and there was limited competitive variation in lenders’

responses to the regulatory intervention). These changes were made to help meet CommBank’s

regulatory requirements, specifically APRA's requirement that interest only lending not be more than

30% of total new business. CommBank’s first step in response to the APRA limit was to change its

lending policies and to reduce discretionary discounts on new interest only lending. CommBank

reduced these to the lowest level possible, while leaving its headline rates unchanged. Subsequently,

CommBank’s competitors announced increases in their headline interest only rates. Consequently,

CommBank’s interest only product was the cheapest of all of Australia’s Major Banks. If this situation

had continued, CommBank anticipated breaching the APRA cap as CommBank would have attracted

more volume. Because CommBank had already reduced its discretionary discounts, the only option left

was to change its headline interest only rates to avoid breaching the APRA 30% limit. As the headline

rate is the same 'reference rate' for both new and existing customers, raising CommBank’s headline

rate impacted both new and existing customers.

CommBank notes

Draft Finding 15.1 (APRA not well placed to consider competition in the financial

system)

. CommBank notes that the Commission's draft report proposes the CFR to assess the

competition related implications of regulation. As a member of CFR, APRA would be involved in this

process.

| CommBank of Australia |

31

Response to Information Requests

Information Request 17.1 Which regulator should advance competition in the financial system?

• CommBank notes the Minister for Revenue and Financial Services’ announcement of ASIC’s

new competition mandate (19 March 2018).

| CommBank of Australia |

32

2.2 Balancing macro-prudential regulation

Key Points

• CommBank is supportive of more finely calibrating the risk weights to better reflect the risk

inherent to specific segments, as long as these calibrations are in line with the Basel

Framework and are appropriate in the context of the Australian financial system.

• There is currently a level playing field for all ADIs as the IRB approach is currently available

to all banks, subject to demonstrated ability to meet the appropriate risk evaluation

standards set by APRA.

• Removing the incentive for banks to attain IRB accreditation could result in less sensitive risk

measurement and poor pricing outcomes for customers.

Summary of Response to Draft Recommendations

• CommBank is unopposed to

Draft Recommendation 7.1 (A proportionate approach to

risks non-ADIs pose)

.

• CommBank supports in principle

Draft Recommendation 9.1 (Standardised risk weightings

for SME lending)

.

• CommBank supports in principle

Draft Recommendation 16.1 (Review standardised risk

weights for residential mortgages)

.

Summary of Response to Draft Findings

• CommBank accepts

Draft Finding 7.2 (New rules costly for non-ADIs)

.

Risk weights

Australia’s Major Banks, Macquarie Bank and ING Bank (Australia) (from 1 April 2018) have had their

IRB models approved by APRA, allowing them to utilise a greater degree of granularity in risk weights

than ADIs using the standardised approach. While it is true that risk weights for IRB residential

mortgage lending are lower than that of standardised ADIs, it is also true that IRB risk lending for

riskier IRB lending (such as unsecured personal loans) require higher risk weights than that of

standardised ADIs.

CommBank's view is that there is currently a level playing field for all ADIs. The IRB approach is

currently available to all banks, subject to accreditation by APRA i.e. a bank must demonstrate that the

bank's internal models can produce reliable, risk-sensitive, and comparable estimates of the capital

required at the predetermined soundness standards.

This incentivises all ADIs to invest in these capabilities as it provides ADIs a greater risk-sensitivity and

in general allows these ADIs to operate with a more efficient capital structure.

Australia’s Major Banks have made, and continue to make, significant investments on an on-going

basis to achieve and maintain their IRB accreditation. Removing the incentive for banks to use the IRB

approach could result in reduced risk measurement and poor risk and price outcomes for all

stakeholders (including customers).

| CommBank of Australia |

33

On 14 February 2018, APRA released a discussion paper on its proposed revisions to the existing capital

framework. The papers include revisions to the capital framework resulting from the Basel Committee

finalising the Basel III reforms (also referred to as 'Basel IV') in December 2017, and also includes

proposals to address the systemic concentration of bank portfolios in residential mortgage lending by

seeking to target higher risk residential mortgage lending (for example investment and interest only

loans).

In general, the proposed revisions to the standardised approach are intended to provide a more risk-

sensitive approach. One of the changes that is proposed by APRA is a revision to the current risk-

weighting applied to mortgages calculated on a standardised approach, where there is more granular

risk-weighting for mortgages with a Loan to Value Ratio (LVR) <80% (current framework applies a flat

35% risk-weighting).

The review also contains a proposal to introduce a risk-weighted asset floor for banks using internal

models of at least 72.5% of standardised risk-weighted assets. The capital floor will limit the variation

in capital requirements between banks that are IRB accredited and those utilising the standardised

approach.

CommBank is in favour of more finely calibrating risk weights to better reflect the risk inherent to

specific segments, as long as these calibrations are in line with the Basel Committee’s minimum risk

weight and credit conversion factor recommendations. As such, CommBank supports in principle

Draft

Recommendation 9.1 (Standardised risk weightings for SME lending)

and

Draft Recommendation

16.1 (Review standardised risk weights for residential mortgages)

. In APRA’s discussion paper

“Revisions to the Capital framework for ADIs” dated 14 February 2018, it is noted that different

treatments than those recommended by the Basel Committee are being proposed for SME lending not

secured by property. I.e. APRA is proposing a 85% risk weight instead of the Basel Committees

recommended 75% risk weight. In addition, it is noted that different risk weights are being proposed

that take into account LVR, if a loan meets APRA’s operational requirements and/or if loan is owner

occupied and principal and interest; or not. This appears to meet the Commission’s requirements.

Warehouse lending

It should be noted that CommBank provides mortgage warehouses to a range of predominantly non-

ADI mortgage lenders. As such, CommBank is unopposed to

Draft Recommendation 7.1 (A

proportionate approach to risks non-ADIs pose)

. CommBank notes the suggestion to review the

scope of APRA’s Prudential Standard APS 120 Securitisation (APS 120). CommBank believes that any

such assessment should consider the risk-sensitivity of underlying assets and counterparties, and not

lead to ADIs artificially being considered more risky than non-ADIs. CommBank notes that the recent

changes to APS 120 not only impact the cost of warehouse provision, but also the cost of mortgage

securitisation more broadly.

As a result, CommBank accepts

Draft Finding 7.2 (New rules costly for non-ADIs)

.

| CommBank of Australia |

34

Response to Information Requests

Information Request 16.1 Where can IRB accreditation processes be improved?

• IRB modelling would be assisted by allowing more flexible modelling and simpler reporting

approaches. The challenge for many banks is historical data, and the expertise to support the

risk modelling. In APRA’s discussion paper “Revisions to the Capital framework for ADIs”

dated 14 February 2018, it is noted that a different / simpler approach for small ADIs is being

proposed. ADIs and Australian Banking Association (ABA) should work with APRA to

determine the best approach available to achieve part or full IRB accreditation.

Information Request 7.1 How will prudential standard APS 120 affect you?

• APS 120 amended regulatory capital risk weights across all securitisation exposures:

warehouses, term securitisations, hedging & support facilities. The regulatory capital

allocation under APS 120 applies equally to standard and advanced ADIs for all securitisation

exposures whether originated by ADIs or non- ADIs. Foreign banks, which are not bound by

APS 120 are actively competing to provide securitisation financing in the Australian market.

Global neutrality on securitisation risk weights would provide for more balanced competition

between Australian and foreign warehouse providers.

• The impact of costs due to APS 120 changes for standard ADIs and non-ADIs varies and is

difficult to quantify. Each warehouse provided by CommBank was assessed and the outcome

was negotiated with each client having regard to client requirements, market conditions,

funding costs, changes in general capital requirements and changes in APS 120. Different

warehouses were priced and restructured in different ways reflecting these different factors.

In some instances warehouse pricing reduced because clients provided or sourced additional

credit support, however the cost of the additional credit support is unknown to CommBank

so the overall impact is difficult to quantify. In some instances warehouse pricing increased

but this was driven by the multiple factors outlined and it is difficult to quantify the change

solely due to APS 120.

• CommBank was able to reach mutually agreeable outcomes for all warehouses and some

non-ADI clients have requested increased warehouse limits.

• The Commission is also seeking estimates of the costs of obtaining similar levels of finance

to that obtained through warehousing, such as through commercial loans in retail markets.

• Securitisation pools assets to obtain a rating / credit quality uplift from the underlying

individual asset and originator. Pricing on any securitisation facility is dependent on the risk

profile of the asset, transaction structure, risk profile of the securitisation tranche, volume,

tenor and capability of transaction parties. Securitisation provides for cost effective funding

across a range of assets and issuer types. In many cases, particularly for unrated, or lower

rated entities, the volume, pricing and tenor of securitisation facilities could not be matched

in un-securitised format via other funding channels.

| CommBank of Australia |

35

This page intentionally

left blank

| CommBank of Australia |

36

2.3 Balancing non-macro-prudential regulation

Key Points

• Before further regulatory intervention is considered, recent policy changes should be given

time to work.

• CommBank supports recent regulatory initiatives and reforms that lower hurdles for

innovation in the financial system insofar as they continue to ensure financial system

stability and the protection of customers.

• FinTechs and global technology companies are already successfully becoming part of

everyday experiences in a range of customer relationships.

Summary of Response to Draft Recommendations

• CommBank supports in principle Draft Recommendation

4.1 (Reducing regulatory barriers

to entry and expansion)

but before further regulatory intervention is considered, recent

policy changes should be given time to work.

• CommBank supports in principle

Draft Recommendation 10.2 (Making the ePayments

code mandatory)

.

• CommBank supports in principle

Draft Recommendation 10.1 (Review regulation of

purchased payment facilities).

Summary of Response to Draft Findings

• CommBank rejects

Draft Finding 4.3 (Most FinTechs are focusing on less regulated

services)

.

• CommBank rejects

Draft Finding 4.4 (FinTech collaboration and competition)

.

• CommBank rejects

Draft Finding 4.2 (Foreign banks remain predominantly niche

operators).

CommBank supports in principle the Commission’s draft recommendations related to balancing non-

macro-prudential regulation.

Reducing regulatory barriers to entry and expansion

CommBank takes this opportunity to reiterate Recommendation 3 of its Initial Submission that the

anticipated impact of the breadth of statutory and regulatory changes currently being planned or