Grant Thornton July 2020

Viewpoint

Accounting for software costs

2

This publication was created for general information purposes, and does not constitute professional

advice on facts and circumstances specific to any person or entity. You should not act upon the

information contained in this publication without obtaining specific professional advice. No representation

or warranty (express or implied) is given as to the accuracy or completeness of the information contained

in this publication. Grant Thornton LLP (Grant Thornton) shall not be responsible for any loss sustained

by any person or entity that relies on the information contained in this publication. This publication is not a

substitute for human judgment and analysis, and it should not be relied upon to provide specific answers.

The conclusions reached on the examples included in this publication are based on the specific facts and

circumstances outlined. Entities with slightly different facts and circumstances may reach different

conclusions, based on considering all of the available information.

The content in this publication is based on information available as of June 30, 2020. We may update this

publication for evolving views and as we continue to monitor the standard-setting process and

implementation of any ASC amendment. For the latest version, please visit grantthornton.com.

Portions of FASB Accounting Standards Codification® material included in this work are copyrighted by

the Financial Accounting Foundation, 401 Merritt 7, Norwalk, CT 06856, and are reproduced with

permission.

3

Contents

Introduction ............................................................................................................................... 5

1. Scope................................................................................................................................. 7

1.1 Internal-use software ................................................................................................ 10

1.1.1 Substantive plan to market software externally ......................................................10

1.1.2 Identifying internal-use software ..........................................................................13

1.2 Software to be used in research and development ........................................................ 15

1.3 Software to be sold, leased, or marketed ..................................................................... 16

1.4 Hosting arrangements .............................................................................................. 16

1.4.1 Hosting arrangement as a cloud computing transaction ..........................................17

1.4.2 Hosting arrangement as software as a service transaction ......................................19

1.5 Other costs of technology.......................................................................................... 21

1.5.1 Business process reengineering and technology transformation...............................21

1.5.2 Website development costs ................................................................................21

2. Internal-use software ...........................................................................................................22

2.1 Preliminary project stage........................................................................................... 24

2.2 Application development stage................................................................................... 25

2.2.1 Acquiring a software license for internal use..........................................................29

2.2.2 Multiple elements included in purchase price.........................................................29

2.2.3 Impact of new software development activities on existing software ..........................31

2.3 Post-implementation operation stage .......................................................................... 32

2.3.1 Training and maintenance ..................................................................................32

2.3.2 Upgrades and enhancements .............................................................................33

2.4 Amortization of capitalized internal-use software costs................................................... 37

2.5 Impairment of capitalized internal-use software cost ...................................................... 38

2.5.1 Abandoned or suspended projects.......................................................................39

2.6 Presentation and disclosure....................................................................................... 41

3. Research and development software .....................................................................................42

3.1 Software that is purchased or leased .......................................................................... 42

3.2 Software that is developed internally ........................................................................... 43

3.3 Disclosure............................................................................................................... 44

4. Software to be sold..............................................................................................................45

4.1 Technological feasibility ............................................................................................ 46

4.1.1 A detail program design exists ............................................................................48

4.1.2 A detail program design does not exist .................................................................49

4.1.3 Development issues after technological feasibility is established ..............................50

4.2 Production costs and post-production costs of computer software ................................... 51

4.2.1 Costs of customer support and maintenance ........................................................52

4.2.2 Costs of product enhancements ..........................................................................54

4.3 Purchased software.................................................................................................. 55

4.4 Funded software-development arrangements ............................................................... 57

4.5 Costs of producing inventory...................................................................................... 58

4.6 Amortization of capitalized amounts ............................................................................ 58

4.6.1 Amortization of product enhancements.................................................................61

4.7 Impairment of capitalized amounts.............................................................................. 62

4.8 Presentation and disclosure....................................................................................... 63

4

5. Costs to implement a cloud computing arrangement .................................................................67

5.1 Costs to implement a cloud computing arrangement that is a service contract ................... 67

5.1.1 Multiple element arrangements in a hosted arrangement ........................................69

5.2 Amortization of implementation costs of cloud computing arrangement ............................ 69

5.3 Impairment ............................................................................................................. 71

5.4 Presentation and disclosure for costs of a cloud computing arrangement.......................... 72

6. Internal-use software subsequently marketed ..........................................................................74

6.1 Decision to market made before software is complete ................................................... 75

Introduction

Companies today rely on software in countless ways to help forge a competitive edge, whether it’s using

basic email and smartphones or pioneering new ways to harness artificial intelligence. Savvy businesses

routinely use software to streamline operations like payroll, manufacturing, or financial reporting, while a

growing number of executives are deploying data analytics to grow sales and inform smart business

decisions.

The myriad ways that companies currently leverage software are matched by the number of ways that

software can be developed or otherwise obtained. Companies can develop software internally, externally,

or jointly with a third party. Software can be purchased off-the-shelf and used directly as a stand-alone

product or customized to meet a company’s specific needs. Software can also be embedded into an

existing product or process, or it can be accessed directly online via a hosting arrangement that is

provided by a third party.

While this variety bodes well for growing a business, accounting for the costs of software can be

somewhat of a challenge. The FASB’s Codification features no fewer than five Topics that offer guidance

on how to account for the costs of developing, purchasing, and implementing software. This guidance is

nuanced depending on how a company either obtains or develops, and how it ultimately uses, the

software.

For example, software that is used exclusively for internal purposes, whether it is developed internally or

acquired from an outside party, is accounted for using the guidance in ASC 350-40, Internal-Use

Software—except for certain costs that are incurred when internal software is used in research and

development, which are accounted for under ASC 730, Research and Development.

In contrast, software that is sold, leased, or marketed as a stand-alone product, or as an integral

component of another product or process, is accounted for using the guidance in ASC 985-20, Software –

Costs of Software to Be Sold, Leased or Marketed, regardless of whether it is developed internally or

purchased from a third party.

Determining which guidance applies to a hosting arrangement depends not only on whether the company

is a customer or a vendor, but also on whether the customer ultimately takes control of the software or

can only access it. Hosting arrangements are generally treated as service contracts unless the customer

takes or can take possession of the software. Some of a customer’s costs to implement such an

arrangement may be capitalized under the guidance in ASC 350-40.

This publication unravels the FASB’s guidance on accounting for software costs in ASC 350-40,

ASC 730, and ASC 985-20, by using direct citations from the Codification, examples created to illustrate

the FASB’s guidance, and insights based on our experience with clients and conversations with

colleagues and standard-setters.

This publication will be updated periodically to reflect new guidance and practice issues that develop, and

is written to reflect the adoption of the following recently issued Accounting Standards Updates that

impact the accounting for software costs:

6

• ASU 2018-15, Customer’s Accounting for Implementation Costs Incurred in a Cloud Computing

Arrangement That Is a Service Contract (a consensus of the FASB Emerging Issues Task Force)

• ASC 606, Revenue from Contracts with Customers

Scope 7

1. Scope

Entities today obtain software in many ways. Sometimes, software is a standard off-the-shelf product with

broad applicability that can be easily purchased and is ready to use without any customization or complex

installation. Other times, an entity might engage a third-party specialist or use its own internal specialist

to develop customized software designed to meet its specific needs. Somewhere between these two

options, an entity might purchase base software from a third party and then customize it internally or with

the help of a third party for its own purposes. Finally, an entity may enter into a hosting arrangement

whereby a third party makes software available for the entity to access online as needed.

Entities also use software in many different ways. An entity may use software internally to run its

business, or it may sell or provide access to software in contracts with customers. Some entities purchase

or develop software to use as part of research and development activities that are focused on developing

new products or services.

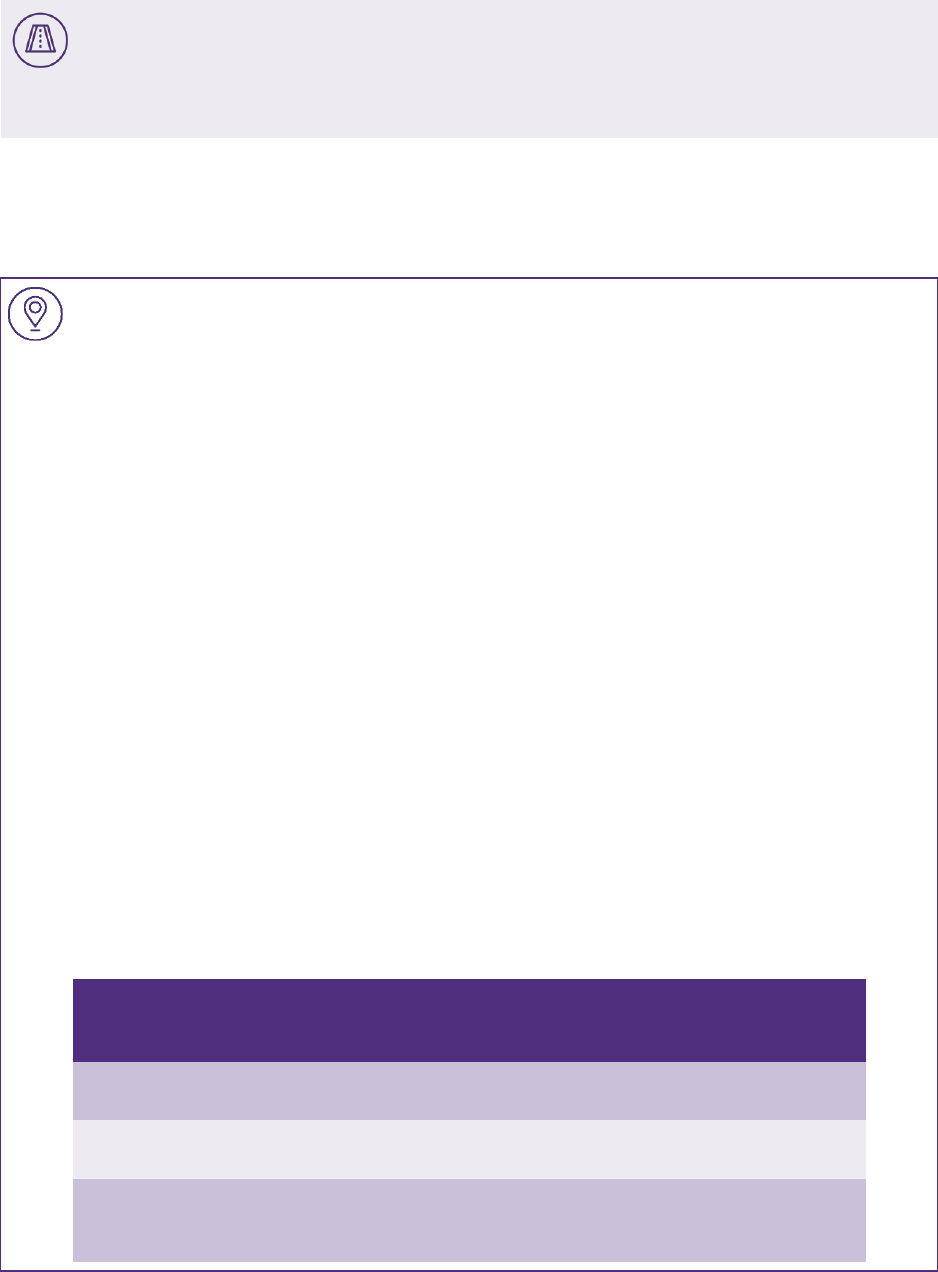

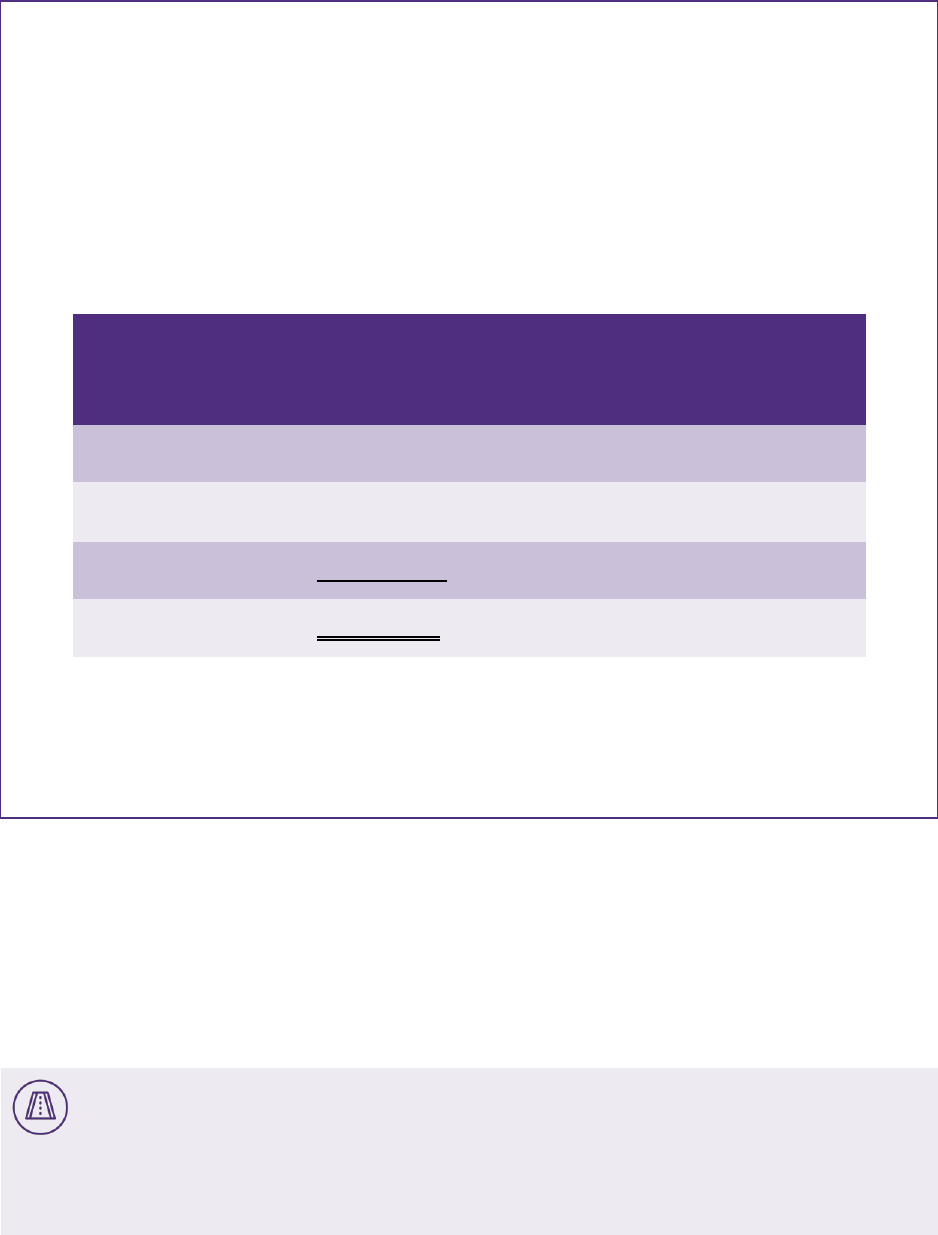

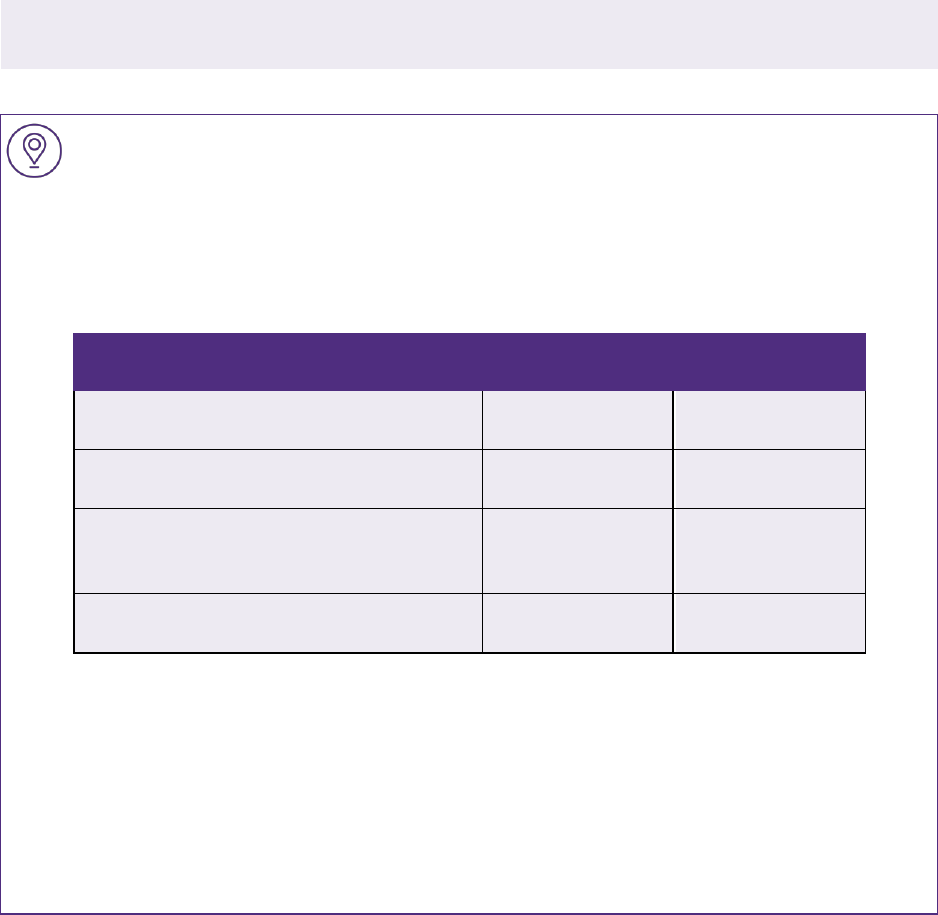

How the entity obtains and uses software will impact the accounting for a particular software product. The

following table outlines the various FASB guidance that might apply to accounting for software costs and

indicates when that guidance should be applied.

Figure 1.1 Summary of guidance for software development costs

Guidance

Applicability

ASC 350-40, Intangibles – Goodwill and

Other: Internal-Use Software

Applies when there is no intention to sell the software;

rather, it will be used solely in operating an entity’s

business, including

• For a vendor – When the software will be used by the

vendor in providing a cloud computing service

arrangement where the customer does not take

possession of the software and cannot host it on its

own.

• For a customer – When the customer can take

possession of the software and host it on its own.

ASC 985-20, Software: Costs of

Software to Be Sold, Leased, or

Marketed

Applies to software development costs for a software

product that will either be sold or embedded in a product

that will subsequently be sold, leased, or otherwise

marketed.

ASC 730, Research and Development

Applies to costs incurred to internally develop software to

be used in research and development.

Scope 8

Guidance

Applicability

ASC 720-45, Other Expenses: Business

and Technology

Reengineering

Provides guidance on the costs associated with business

process reengineering and information technology

transformation projects.

ASC 350-50, Website Development

Costs

Discusses the accounting for costs incurred in the five

stages of website development, which are outlined in this

guidance.

Determining which guidance applies to the costs of developing, purchasing, or implementing software

requires an understanding of the intended use of the software product, the types of costs involved, and

the product’s stage of development. Broadly, the first step is for an entity to determine if the software

being developed or implemented is only for internal use, such as a customized inventory tracking system,

or if it is being designed to sell to customers either as a stand-alone product or as an integral component

of another product. An entity must also determine if the arrangement is a hosting arrangement and, if so,

whether the customer can take possession of the software underlying the hosting arrangement and is

able to host the software on its own or with another third party.

The guidance in this Viewpoint is written from the perspective of an entity that has adopted ASU 2018-15,

Customer’s Accounting for Implementation Costs Incurred in a Cloud Computing Arrangement That I s a

Service Contract, which is effective for public business entities for fiscal years beginning after December

15, 2019, and interim periods within those fiscal years, and for all other entities in annual reporting

periods beginning after December 15, 2020, and interim periods beginning after December 15, 2021. An

entity may elect to early adopt the guidance, including in interim periods, and may apply the guidance

prospectively or retrospectively.

This Viewpoint is also written from the perspective of an entity that has adopted ASC 606, Revenue from

Contracts with Customers.

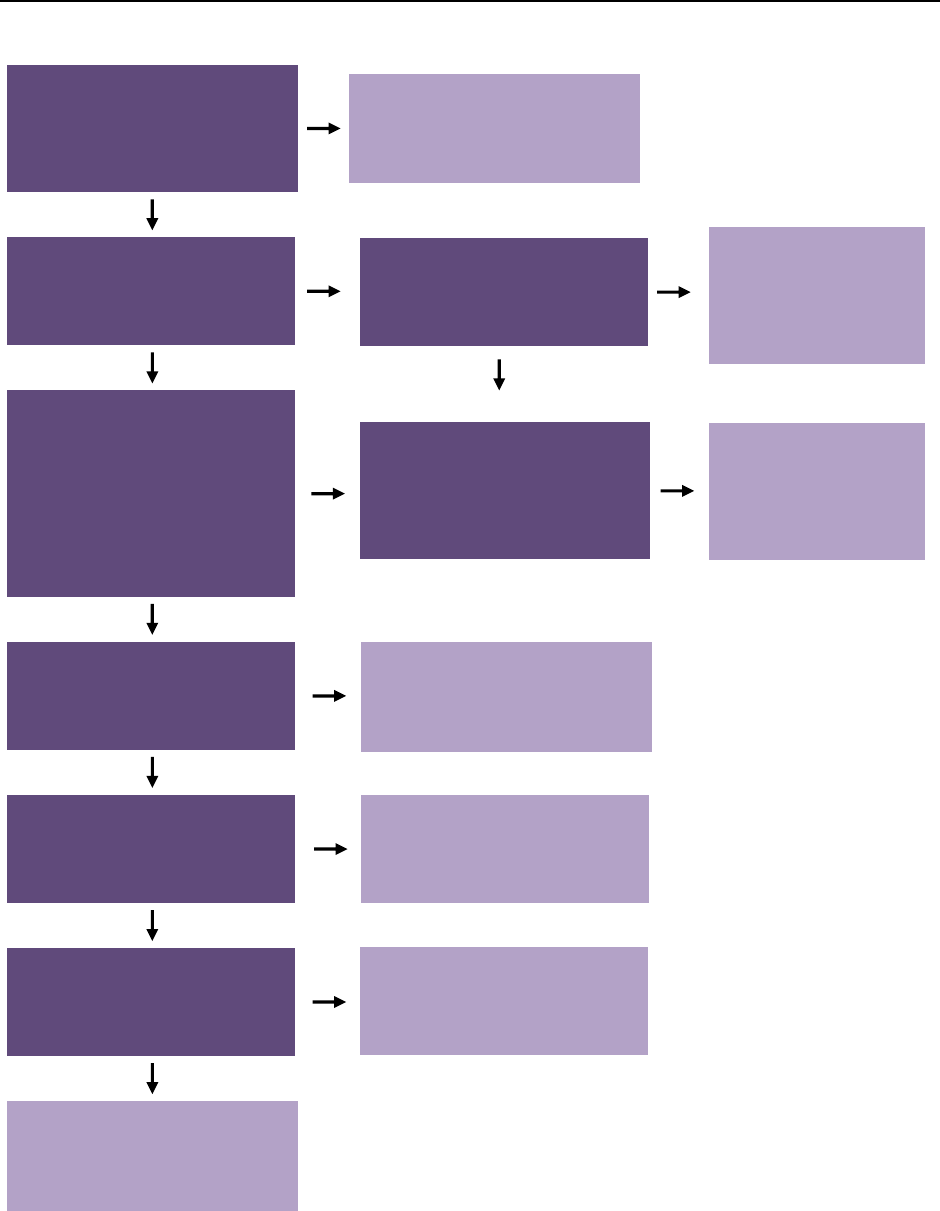

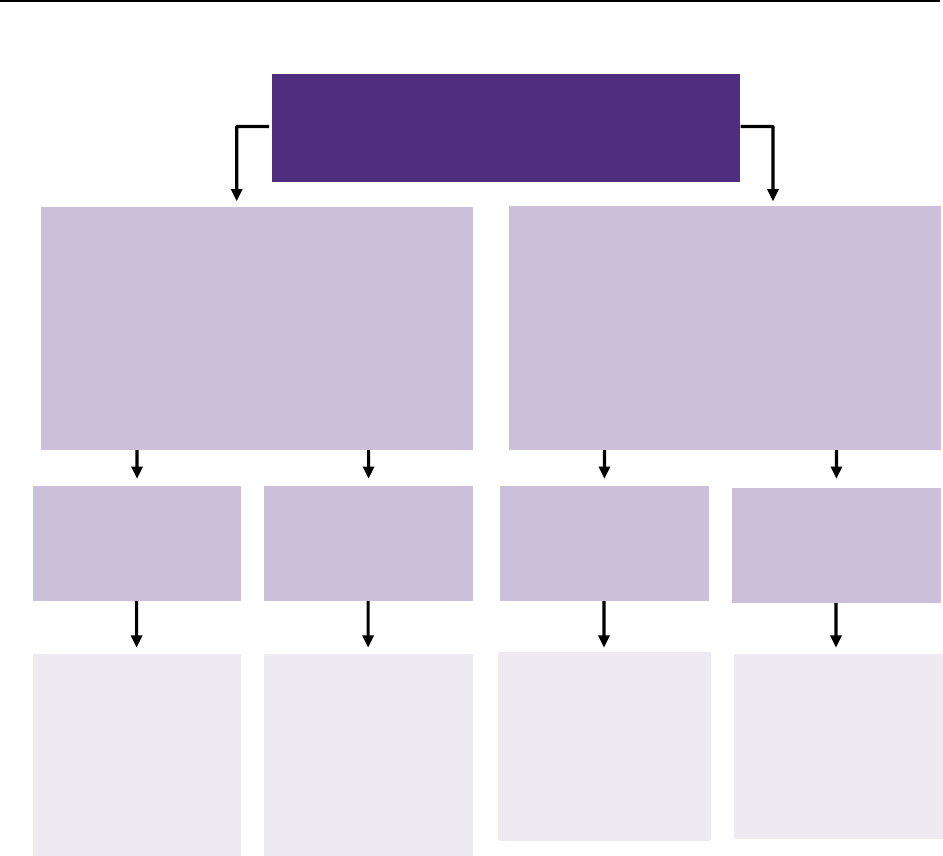

The following figure illustrates how an entity should evaluate which guidance to apply to particular

software-related costs. The scope of each type of software-development accounting guidance in the

figure is discussed in the rest of this section.

Scope 9

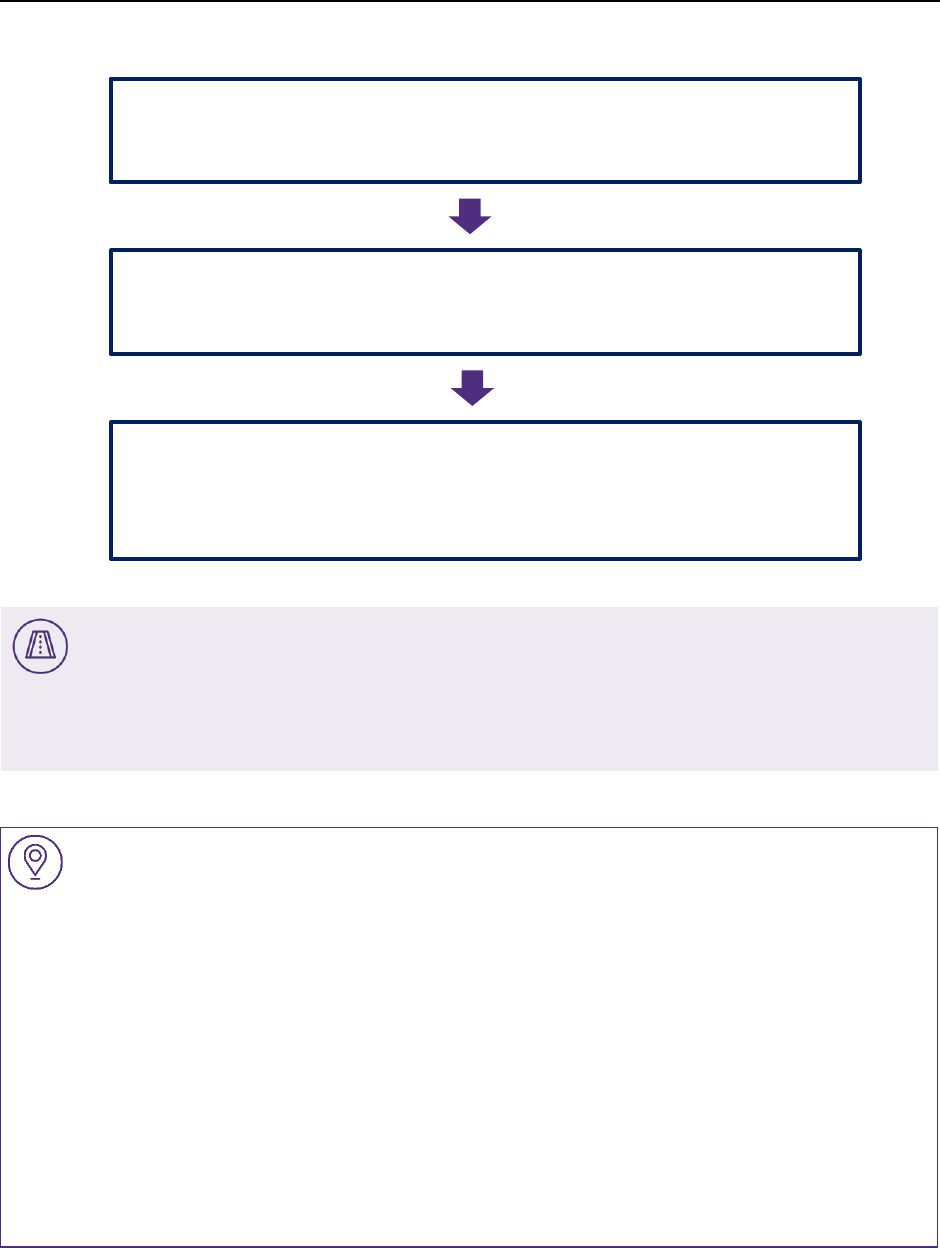

Figure 1.2: Determining the appropriate accounting to apply to software related costs

Y

Y

Y

During the internal-use

software’s development,

modification, or life cycle,

has the plan to use the

software changed so that the

plan is now to sell, lease, or

otherwise market the

software externally?

Was the software acquired,

internally developed, or

modified solely to meet the

entity’s internal needs?

Is the software being

produced as part of a

contract with a customer

under ASC 606?

Is there a plan to sell, lease,

or otherwise market the

software as a separate

product or as part of a

product or process?

Apply ASC 340-40,

Other Assets and

Deferred Costs:

Contracts with

Customers.

Is the software to be used

internally for research and

development purposes only?

Apply ASC 730-10,

Research and Development.

Are the costs being incurred

for reengineering activities

(such as evaluating and

updating business

processes)?

Apply ASC 720-45, Other

Expenses: Business and

Technology Reengineering.

Are the costs being incurred

for website development

(other than costs for

software)?

Apply ASC 350-50, Website

Development Costs.

Apply ASC 350-40,

Intangibles – Goodwill and

Other: Internal-Use

Software.

Apply ASC 985-20,

Software: Costs of

Software to Be Sold,

Leased, or

Marketed.

Is the underlying

arrangement a hosting

arrangement from either the

customer’s or vendor’s

perspective?

Use Figure 1.3 to

determine the appropriate

accounting guidance.

N

Y

N

Y

Y

Y

Y

N

N

N

N

N

Scope 10

1.1 Internal-use software

Although internal-use software is generally considered to be an intangible asset, it has characteristics

that are similar to property, plant, and equipment: it is specifically identifiable, it may have a useful life

of several years or more, it is not intended for sale in the ordinary course of business, and it is either

acquired or developed with the intention of being used by the entity. The guidance used to account for

internal-use software under ASC 350-40 is likewise similar to the guidance in ASC 360 Property, Plant,

and Equipment, in that it accounts for internal-use software using a cost accumulation model and

amortizes the asset over its useful life.

However, the guidance on accounting for internal-use software in ASC 350-40, which includes software

that is used as all or a part of a service offering (see Section 1.1), differs from the guidance on accounting

for software that an entity intends to sell during the ordinary course of business, which falls under

ASC 985-20, Software: Costs of Software to Be Sold, Leased, or Marketed. For software to be

considered internal-use software, it must be used solely to meet an entity’s internal needs, and the entity

must not have a substantive plan to market the software externally. Internal-use software may either be

developed internally or acquired from a third party. If there is a substantive plan to market the software

externally, regardless of whether it already exists or is being developed, the software does not qualify as

internal-use software. In other words, if the initial primary purpose of a specific software product is for the

entity’s own use but its secondary purpose is to be sold or marketed to outside parties, the software does

not meet the definition of internal-use software. The software must be created and intended solely for

internal use to qualify as internal-use software under ASC 350-40.

Internal-use software is accounted for using the guidance in ASC 350-40, as discussed in Section 2.

Software that is developed to be marketed, sold, or leased is accounted for using the guidance in

ASC 985-20, as discussed in Section 1.3 and Section 4.

ASC 350-40-15-2A

Internal-use software has both of the following characteristics:

a. The software is acquired, internally developed, or modified solely to meet the entity’s internal

needs.

b. During the software’s development or modification, no substantive plan exists or is being

developed to market the software externally.

1.1.1 Substantive plan to market software externally

ASC 350-40 includes a list of conditions that an entity should consider when determining whether it has a

“substantive” plan to market software externally. First, implementation of the plan must be “reasonably

possible” in order for a plan to be considered “substantive.” The implementation would be considered

reasonably possible if the chance of it occurring is greater than remote. However, the chance that the

implementation would occur does not need to be likely in order for it to be considered reasonably

possible. Therefore, activities like engaging in a market feasibility study, or entering into a joint

arrangement to share costs with another entity to develop software that both entities plan to use

Scope 11

internally, would not qualify as a substantive plan to market the software externally. On the other hand,

any one of the following conditions might indicate that a plan to market software externally is substantive:

• Selecting a marketing channel,

• Identifying specific promotional activities.

• Developing a plan for delivery, billing, and support of the software product.

ASC 350-40-15-2B

A substantive plan to market software externally could include the selection of a marketing channel

or channels with identified promotional, delivery, billing, and support activities. To be considered a

substantive plan, implementation of the plan should be reasonably possible. Arrangements providing

for the joint development of software for mutual internal use (for example, cost-sharing arrangements)

and routine market feasibility studies are not substantive plans to market software for purposes of this

Subtopic. Both characteristics in paragraph 350-40-15-2A must be met for software to be considered

for internal use.

Determining whether a marketing plan is ‘substantive’ under ASC 350-40

The following examples illustrate how an entity might determine whether it has a substantive plan to

market software externally.

Substantive marketing plan

A bank develops software that allows customers to transfer cash from their account to another

individual’s account using a mobile application. The software is initially developed as a feature to be

accessed only by the bank’s customers as software as a service (SaaS). While development of the app

is still in the “preliminary project stage,” as discussed in Section 2.1, the bank conducts exploratory

market research and discovers there is a market to sell the software to other banks. The bank decides

to pursue this option but does not intend to market the software to other banks immediately after

completing the app, because it expects that offering the application exclusively to its own retail banking

customers might grow its customer base. The bank establishes a committee of individuals comprising

software developers, marketing personnel, and finance staff to identify other banks as potential

customers and to develop the infrastructure necessary to support the product when it is released for

sale to other banks in the future.

The bank concludes that it has a substantive plan to market the software externally because

implementation of the plan is reasonably possible, and accounts for the costs incurred to develop the

software in accordance with ASC 985-20.

No substantive marketing plan

Assume the same facts in the previous example, except that, as the outcome of the exploratory market

research, the bank instead decides that the benefits of offering the SaaS software exclusively to its

customers outweigh the marketing costs and potential profit from selling the software to its competitors.

Scope 12

The bank therefore decides not to move forward with a plan to market the software externally to other

banks and accounts for the software under the internal-use guidance in ASC 350-40.

The guidance in ASC 350-40 also requires entities to consider their past practices when evaluating

whether a software product is designed only for internal use. If an entity has both used software internally

and sold the same software externally in the past, then there is a rebuttable presumption that any

software the entity develops is intended for sale, as explained in ASC 350-40-15-2C.

ASC 350-40-15-2C

An entity’s past practices related to selling software may help determine whether the software is for

internal use or is subject to a plan to be marketed externally. For example, an entity in the business

of selling computer software often both uses and sells its own software products. Such a past practice

of both using and selling computer software creates a rebuttable presumption that any software

developed by that entity is intended for sale, lease, or other marketing.

Grant Thornton insights: Considering an entity’s past practices

An entity with a history of subsequently marketing and selling software products initially developed for

internal use must carefully consider whether any newly developed software may subsequently be

leased or sold in determining how to account for software development costs. The FASB has stated

that a past practice of selling internally used software creates a rebuttable presumption that any

software developed by the entity will be marketed, sold, or leased. Under ASC 350-40, an entity is

required to present a preponderance of evidence to overcome this presumption.

Drawing on the previous example in “Determining whether a marketing plan is substantive under

ASC 350-40” with no substantive marketing plan above, if the bank reverses its decision not to market

or sell the software and subsequently markets the internal-use software to other banks, management

should evaluate whether it has established a practice of both using and selling computer software. If

so, a rebuttable presumption that the bank intends to market or sell future software projects would then

exist. The bank could overcome the rebuttable presumption if a preponderance of the evidence

indicates that the software will not be marketed or sold.

For example, assume management determined that a rebuttable presumption exists. The bank begins

developing a new software product to provide to its customers as part of its services, similar to the

cash transfer software from the previous example. The software is an app that the customers can

download to assist in splitting a check among patrons at a restaurant. The bank does not have plans

to sell or market the app to other banks. However, because of the bank’s history of selling software

initially intended to be solely for its customers, it might conclude that it is unable to overcome the

rebuttable presumption that it would sell this software. In that case it would be required to account

for the development of this software in accordance with the guidance in ASC 985-20, unless a

preponderance of evidence exists to overcome the presumption that the software is intended for sale.

On the other hand, if the bank begins developing a customized software product to interface with its

highly customized financial reporting software by pulling data for strategic analysis, it might be able to

Scope 13

provide sufficient evidence that the software will not be transferred to other entities in the future, since

the software could not feasibly interface with other entities’ financial reporting software. Additionally,

the type of financial analysis conducted by the software may be key to the bank’s overall strategy

for generating profit, in which case, sharing the strategy could significantly impair the bank’s ability

to remain competitive in the marketplace. If the bank can provide compelling evidence that the

software will never be sold, leased, or otherwise marketed, it may be able to overcome the rebuttable

presumption that the software will be sold, leased, or marketed externally. If so, the bank should

account for the software under the guidance for internal-use software in ASC 350-40.

1.1.2 Identifying internal-use software

To help entities correctly identify internal-use software, the FASB has provided lists of examples that both

would and would not qualify as internal-use software accounted for under ASC 350-40. While the lists

provide specific examples, there are common elements among the items on the lists that may be helpful

for an entity trying to determine whether its software is internal-use.

Common elements of internal-use software include software that will be used:

• As part of a manufacturing process. This could include software that runs machines or equipment

used by the entity to produce its goods, or software used to control other operations within a

manufacturing plant or distribution center.

• By the entity’s employees to provide services to customers.

• By the entity in its internal operations, such as in the accounting, finance, or payroll departments, for

storage of information, or internal communications.

Common elements of software that is not intended for internal use include software that:

• Is integrated into or operates a good manufactured or sold by the entity.

• Creates a digital version of an analog item that is then sold to customers.

• Meets any of the previously discussed scope exceptions (software that an entity has a plan to sell,

software developed under a contract with a customer, software to be used for research and

development).

ASC 350-40-55-1

The following is a list of examples illustrating when computer software is for internal use:

a. A manufacturing entity purchases robots and customizes the software that the robots use to

function. The robots are used in a manufacturing process that results in finished goods.

b. An entity develops software that helps it improve its cash management, which may allow the entity

to earn more revenue.

c. An entity purchases or develops software to process payroll, accounts payable, and accounts

receivable.

Scope 14

d. An entity purchases software related to the installation of an online system used to keep

membership data.

e. A travel agency purchases a software system to price vacation packages and obtain airfares.

f. A bank develops software that allows a customer to withdraw cash, inquire about balances, make

loan payments, and execute wire transfers.

g. A mortgage loan servicing entity develops or purchases computer software to enhance the speed

of services provided to customers.

h. A telecommunications entity develops software to run its switches that are necessary for various

telephone services such as voice mail and call forwarding.

i. An entity is in the process of developing an accounts receivable system. The software

specifications meet the entity’s internal needs and the entity did not have a marketing plan before

or during the development of the software. In addition, the entity has not sold any of its internal-use

software in the past. Two years after completion of the project, the entity decided to market the

product to recoup some or all of its costs.

j. A broker-dealer entity develops a software database and charges for financial information

distributed through the database.

k. An entity develops software to be used to create components of music videos (for example, the

software used to blend and change the faces of models in music videos). The entity then sells the

final music videos, which do not contain the software, to another entity.

l. An entity purchases software to computerize a manual catalog and then sells the manual catalog to

the public.

m. A law firm develops an intranet research tool that allows firm members to locate and search the

firm’s databases for information relevant to their cases. The system provides users with the ability

to print cases, search for related topics, and annotate their personal copies of the database.

ASC 350-40-55-2

The following list provides examples of computer software that is not for internal use:

a. An entity sells software required to operate its products, such as robots, electronic game systems,

video cassette recorders, automobiles, voice-mail systems, satellites, and cash registers.

b. A pharmaceutical entity buys machines and writes all of the software that allows the machines to

function. The pharmaceutical entity then sells the machines, which help control the dispensation of

medication to patients and help control inventory, to hospitals.

c. A semiconductor entity develops software embedded in a microcomputer chip used in automobile

electronic systems.

d. An entity purchases software to computerize a manual catalog and then sells the computer version

and the related software to the public.

e. A software entity develops an operating system for sale and for internal use. Though the

specifications of the software meet the entity’s internal needs, the entity had a marketing plan

Scope 15

before the project was complete. In addition, the entity has a history of selling software that it also

uses internally and the plan has a reasonable possibility of being implemented.

f. An entity is developing software for a point-of-sale system. The system is for internal use; however,

a marketing plan is being developed concurrently with the software development. The plan has a

reasonable possibility of being implemented.

g. A telecommunications entity purchases computer software to be used in research and

development activities.

h. An entity incurs costs to develop computer software for another entity under a contract with that

other entity.

1.2 Software to be used in research and development

Certain costs associated with software developed for internal research and development activities are

within the scope of ASC 730, Research and Development, rather than ASC 350-40. The accounting for

software used in research and development differs, depending on whether the entity purchases, leases,

or internally develops the software.

When an entity purchases or leases software from a third party to use in research and development

activities, it should consider whether the software could have an alternative future use beyond the existing

research and development project. If the software has a future internal use, an entity should account

for the costs in accordance with the guidance in ASC 350-40. Otherwise, the costs associated with

purchasing or leasing the software should be expensed in accordance with ASC 730.

If the software is developed internally for a specific research and development project, an entity should

account for the costs under ASC 730, regardless of whether the software has an alternative future use.

Furthermore, any costs associated with developing software for a “pilot project,” meaning a project that is

not executed on a scale that is economically feasible for commercial production, should also be

accounted for as research and development under ASC 730.

The accounting for software costs under ASC 730 is discussed in more detail in Section 3.

ASC 350-40-15-7

The following costs of internal-use computer software are included in research and development and

shall be accounted for in accordance with the provisions of Subtopic 730-10:

a. Purchased or leased computer software used in research and development activities where the

software does not have alternative future uses

b. All internally developed internal-use computer software (including software developed by third

parties, for example, programmer consultants) in either of the following circumstances:

1. The software is a pilot project (that is, software of a nature similar to a pilot plant as noted in

paragraph 730-10-55-1(h)).

2. The software is used in a particular research and development project, regardless of whether

the software has alternative future uses.

Scope 16

1.3 Software to be sold, leased, or marketed

Software that is developed or purchased by an entity that will be sold, leased, or marketed is accounted

for under ASC 985-20. This guidance applies to software that will be sold as a stand-alone product as

well as to software that will be sold as part of another product or process, regardless of whether it is

internally developed or purchased from a third party. An entity that has a substantive plan to externally

market software that has been developed internally should account for the software as a product to be

sold under ASC 985-20. (Refer to Sections 1.1.1. and 1.1.2 for a discussion of the criteria to consider

when determining whether software will be sold externally or is designed solely for internal use.)

Software that is developed for internal use or for research and development purposes, along with

software that is produced, modified or customized as part of a contract with a customer, does not fall

within the scope of ASC 985-20. Accounting for software that will be sold, leased, or marketed is

discussed in more detail in Section 4.

ASC 985-20-15-2

The guidance in this Subtopic applies to the costs, including costs incurred after the date of a business

combination or a combination accounted for by a not-for-profit entity, of computer software to be sold,

leased, or otherwise marketed as a separate product or as part of a product or process, whether

internally developed and produced or purchased.

ASC 985-20-15-3

The guidance in this Subtopic does not apply to the following transactions and activities:

a.

Software developed or obtained for internal use (see Subtopic 350-40).

b.

Research and development assets acquired in a business combination or an acquisition by a

not-for-profit entity. If tangible and intangible assets acquired in those combinations are used in

research and development activities, they are recognized and measured at fair value in accordance

with Subtopic 805-20.

c.

Arrangements to deliver software or a software system, either alone or together with other products

or services, requiring significant production, modification, or customization of software (see the

guidance on costs to fulfill a contract in Subtopic 340-40).

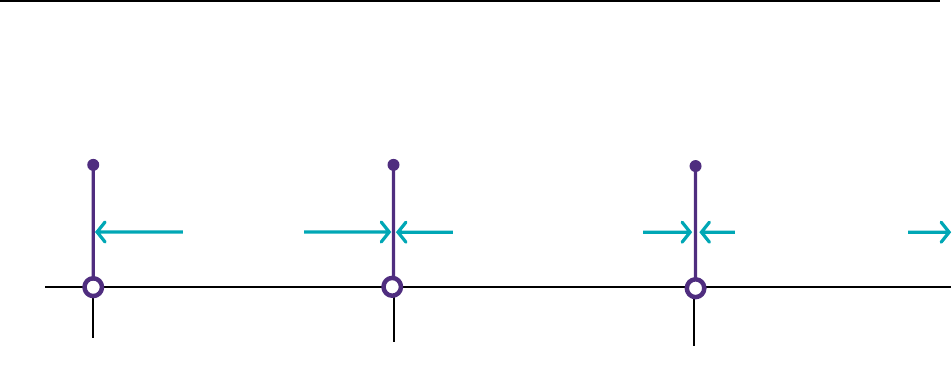

1.4 Hosting arrangements

According to the Codification’s Master Glossary, the term “hosting arrangement” refers to a transaction

entered into by a vendor to provide a customer with access to software that the customer can use, but

does not own or possess.

Hosting Arrangement: In connection with accessing and using software products, an arrangement in

which the customer of the software does not currently have possession of the software; rather, the

customer accesses and uses the software on an as-needed basis.

Scope 17

The phrase “hosting arrangement” can describe the overall transaction from either the customer’s or the

vendor’s perspective. In this publication, however, the term “cloud computing arrangement” describes a

hosting arrangement from the customer’s perspective, whereas the term “software as a service” describes

the same transaction from the vendor’s perspective. See Figure 1.3 below for a summary of the

accounting for a hosting arrangement.

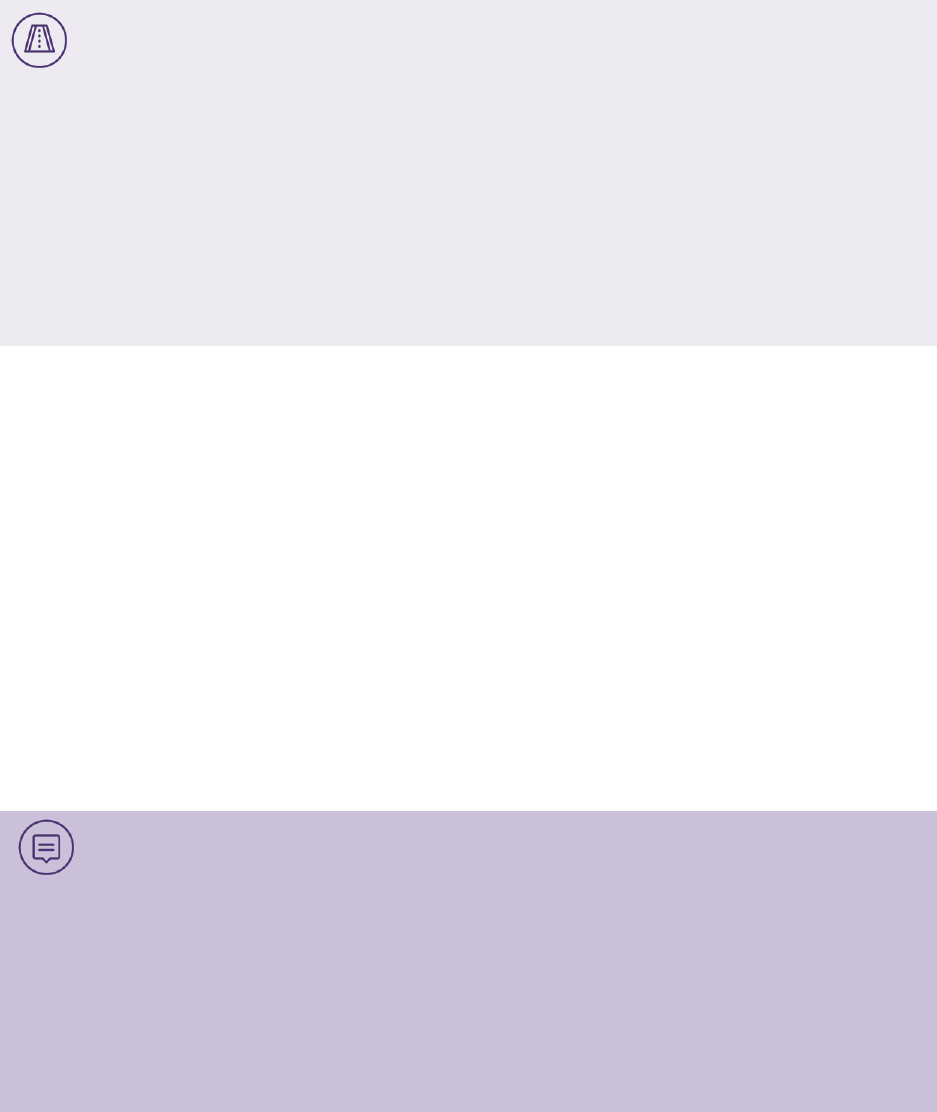

Figure 1.3: Accounting for a hosting arrangement

1.4.1 Hosting arrangement as a cloud computing transaction

In this publication, a “cloud computing arrangement” is a hosting arrangement from a customer’s

perspective in which the customer cannot take possession of the hosted software. If the customer can

take possession of the hosted software, the contract both the service of hosting and a license. If the

customer cannot take possession, the contract is accounted for as a service only contract, that is, a cloud

computing arrangement. The customer can take possession of the software only if both of the following

criteria in ASC 350-40 are met:

Is the entity the vendor or the customer in

the hosting arrangement?

Account for the

arrangement as

a service contract

and the costs of

implementation under

ASC 350-40-35.

Does the customer take possession of the

software by meeting both of the criteria in ASC

985-20-15-5?

• Customer has the right to take possession of

the software at any time without incurring a

significant penalty.

• It is feasible for customer to run the software

on its own hardware or to contract with

another party to run it.

Account for

the software

as internal-use

software under ASC

350-40.

Vendor

Customer

Does the customer take possession of the

software by meeting both the criteria in ASC 350-

40-15-4A?

• Customer has the right to take possession of

the software at any time without incurring a

significant penalty.

• It is feasible for customer to run the software

on its own hardware or to contract with

another party to run it.

•

Account for

the software

as internal-use,

research and

development, or

software to be sold

or marketed, as

appropriate.

Account for

the software as

software to be

sold or marketed

under ASC 985-20.

N N Y Y

The arrangement is a

cloud computing

arrangement.

The arrangement

is a software

as a service

arrangement.

The arrangement

includes a software

license.

The arrangement

is a sale of a

software license.

Scope 18

a. It has the right to take possession of the software at any time during the hosting period without

incurring a significant penalty.

b. It can feasibly run the software on its own hardware or contract with a third party unrelated to the

software vendor to host the software.

If one or both of these criteria are not met, the customer does not take possession of the software.

Under the guidance in ASC 350-40, two factors must be considered when evaluating whether a customer

would incur a significant penalty if it takes possession of software in a hosting arrangement:

• Will the customer incur a significant cost when it takes possession of the software?

• Will the software become significantly less useful or valuable if it were used separately from the

hosting service?

ASC 350-40-15-4A

The guidance in the General Subsections of this Subtopic applies only to internal-use software that

a customer obtains access to in a hosting arrangement if both of the following criteria are met:

a. The customer has the contractual right to take possession of the software at any time during the

hosting period without significant penalty.

b. It is feasible for the customer to either run the software on its own hardware or contract with

another party unrelated to the vendor to host the software.

ASC 350-40-15-4B

For purposes of the guidance in paragraph 350-40-15-4A(a) the term without significant penalty

contains two distinct concepts:

a. The ability to take delivery of the software without incurring significant cost

b.

The ability to use the software separately without a significant diminution in utility or value.

If the customer does not have the right to take possession of the software, it must account for the contract

as a cloud computing arrangement. Because the vendor is only allowing the customer to access the

software as needed, the arrangement is a service contract rather than a contract to purchase or license

software. Therefore, the customer actually accounts for the service it receives from the vendor hosting

the software, and not the software itself. However, it must also account for the costs of implementing the

cloud computing arrangement, as outlined in ASC 350-40. These set-up and implementation costs are

capitalized or expensed, and then subsequently accounted for, as discussed in Section 5.

If the customer has the ability to take possession of software under a hosting arrangement, it should

account for the arrangement as internal-use software, as discussed in Section 2, and not as a cloud

computing arrangement.

Scope 19

ASC 350-40-15-4C

Hosting arrangements that do not meet both criteria in paragraph 350-40-15-4A are service contracts

and do not constitute a purchase of, or convey a license to, software.

ASC 350-40-15-4D

Implementation costs of a hosting arrangement that does not meet both criteria in paragraph 350-40-

15-4A shall be accounted for in accordance with the Implementation Costs of a Hosting Arrangement

That Is a Service Contract Subsections of this Subtopic.

ASC 350-40-25-18

An entity shall apply the General Subsection of this Section as though the hosting arrangement that is

a service contract were an internal-use computer software project to determine when implementation

costs of a hosting arrangement that is a service contract are and are not capitalized.

At the crossroads: Accounting for implementation costs in a cloud computing

arrangement that is a service contract

In August 2018, the FASB issued ASU 2018-15, Customer’s Accounting for Implementation Costs

Incurred in a Cloud Computing Arrangement That Is a Service Contract (a consensus of the FASB

Emerging Issues Task Force), which provides guidance on accounting for costs incurred by a customer

when implementing a cloud computing arrangement that is considered a service contract. Prior to the

amendments in the ASU, there was diversity in practice because no explicit GAAP existed on how a

customer should account for these implementation costs. The amendments require an entity that incurs

costs to implement a cloud computing arrangement to account for those costs in a manner similar to

costs for internal-use software.

Public business entities should apply the amendments in ASU 2018-15 in fiscal years beginning after

December 15, 2019, including interim periods within those fiscal years. All other entities should apply

the amendments in fiscal years beginning after December 15, 2020 and in interim periods within fiscal

years beginning after December 15, 2021. Early adoption is permitted for all entities in any annual or

interim period if the financial statements have not already been issued or made available for issuance.

Entities should apply the amendments either (1) retrospectively, recognizing the cumulative effect of

applying the amendments in the financial statements in the opening retained earnings of the earliest

period presented, or (2) prospectively to costs for activities performed on or after the adoption date of

the ASU.

1.4.2 Hosting arrangement as software as a service transaction

In this publication, a “software as a service (SaaS) arrangement” is a hosting arrangement from a

vendor’s perspective in which the customer cannot take possession of the hosted software. When an

entity develops software to be used in a SaaS arrangement, it must determine whether to account for the

software as internal-use software or as software that will be sold or marketed externally. An entity should

Scope 20

account for software used in a SaaS arrangement as software that will be sold if both of the following two

criteria are met:

• The customer has a contractual right to take possession of the software at any time during the

hosting period without incurring a significant penalty.

• The customer can either run the software on its own hardware or can contract with a party unrelated

to the vendor to host the software.

In determining whether a penalty that would be incurred to take possession of hosted software is

“significant,” an entity must consider if the customer can both (1) take possession of the software without

incurring significant costs, and (2) use the software separately from the hosting arrangement without

significantly decreasing the software’s value or usefulness.

If the criteria are expected to be met at any time during the arrangement, the costs of developing the

software are accounted for as software that will be sold, leased, or marketed under ASC 985-20, as

discussed in Section 4.

If both of these criteria are not expected to be met during the arrangement, the software is used to

provide a service (SaaS) rather than being sold, leased, or marketed. The costs to develop the software

used in the SaaS contract are accounted for as internal-use software in ASC 350-40, as discussed in

Section 2.

ASC 985-20-15-5

The software subject to a hosting arrangement is within the scope of this Subtopic only if both of the

following criteria are met:

a. The customer has the contractual right to take possession of the software at any time during the

hosting period without significant penalty.

b. It is feasible for the customer to either run the software on its own hardware or contract with

another party unrelated to the vendor to host the software.

ASC 985-20-15-6

For purposes of criterion (a) in paragraph 985-20-15-5, the term significant penalty contains two

distinct concepts:

a.

The ability to take delivery of the software without incurring significant cost

b.

The ability to use the software separately without a significant diminution in utility or value

ASC 985-20-15-7

If the software subject to a hosting arrangement never meets the criteria in paragraph 985-20-15-5,

then the software is utilized in providing services and is not within the scope of this Subtopic and,

therefore, the development costs of the software should be accounted for in accordance with

Subtopic 350-40 on internal-use software (see also paragraph 985-20-55-2).

Scope 21

1.5 Other costs of technology

U.S. GAAP also includes specific guidance for two other types of technology-related costs that entities

might incur: business and technology reengineering costs, and website development costs. While neither

of these types of costs is directly related to software, they are connected with the entity’s technology

environment and may include software-related costs that should be accounted for under other

ASC Topics.

1.5.1 Business process reengineering and technology transformation

Entities often perform information technology transformation projects as well as business process

reengineering projects to better align their businesses with their existing technology or to update both

their business processes and their existing technology. An entity may either hire a consultant with

specialized skills in the area being transformed or reengineered or perform these projects in-house if the

expertise exists. A consultant may provide services that are limited to business process reengineering,

or may provide services that encompass an entire project, including internally developing or purchasing

software as well as updating hardware and other fixed assets. When a consultant assumes an entire

project, an entity must track and differentiate between reengineering costs and costs incurred during

other phases of the project.

Examples of activities that may be involved in a business process reengineering or an information

technology transformation project include

• Preparing a request for proposal

• Assessing and documenting the current state of business processes and information technology,

including mapping, developing an “as-is” baseline, flow charting, and determining the current

business process structure

• Reengineering the entity’s business processes to increase their efficiency or effectiveness

• Restructuring the workforce to determine the number and types of employees that will be necessary

for the reengineered business processes

Costs of the reengineering process itself are accounted for under ASC 720-45 and are generally

expensed as incurred, regardless of whether they are provided by a third party or internally. The guidance

on accounting for these costs is outside of the scope of this publication.

1.5.2 Website development costs

An entity might incur a variety of costs to develop a website. Costs relating to developing or obtaining

software as a part of website development are accounted for as software costs, following the guidance

for internal-use software or software to be sold or marketed, as appropriate (see Section 1.1 and 1.3 for

more information).

Other costs of developing a website, including costs for registering an internet domain, developing

graphics and content, and operating the website, are accounted for under ASC 350-50. These costs are

capitalized or expensed based on the purpose of the activity and the stage of development of the website,

as outlined in the guidance in ASC 350-50. Website development costs are outside of the scope of this

publication.

Internal-use software 22

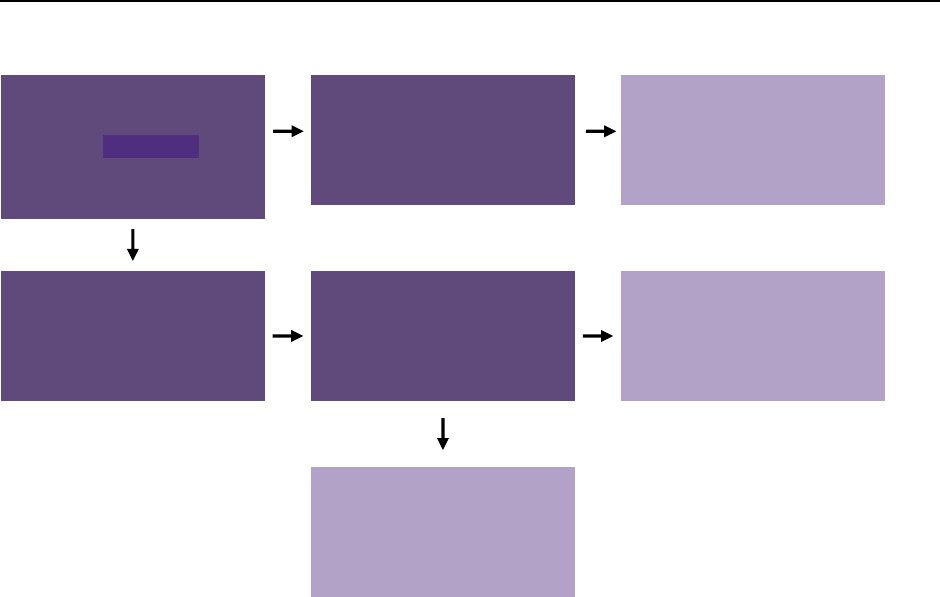

2. Internal-use software

Costs incurred in developing internal-use software are either capitalized or expensed, depending on both

the nature of the costs and the phase of development in which they are incurred (Figure 2.1 outlines the

stages of internal-use software development and the accounting for each phase, as defined in ASC 350-

40.) Costs incurred for implementation activities during the preliminary and post-implementation

phases of a project, for instance, are expensed as incurred, while costs incurred during the application

development phase are generally capitalized. Entities that incur costs to upgrade or enhance existing

software are required to capitalize these costs if the changes result in additional functionality, but to

expense costs if the software’s functionality is not improved.

When it is no longer probable that software being developed will be used, capitalization should cease and

the asset should be evaluated for impairment as discussed in Section 2.5.

Capitalization of development costs should cease, and amortization of those costs should begin, when

the software is ready for its intended use. The costs are amortized over the estimated useful life of the

software as discussed in Section 2.4.

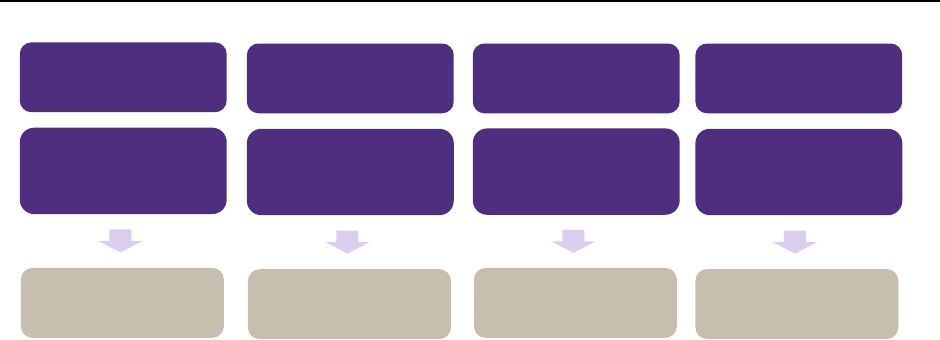

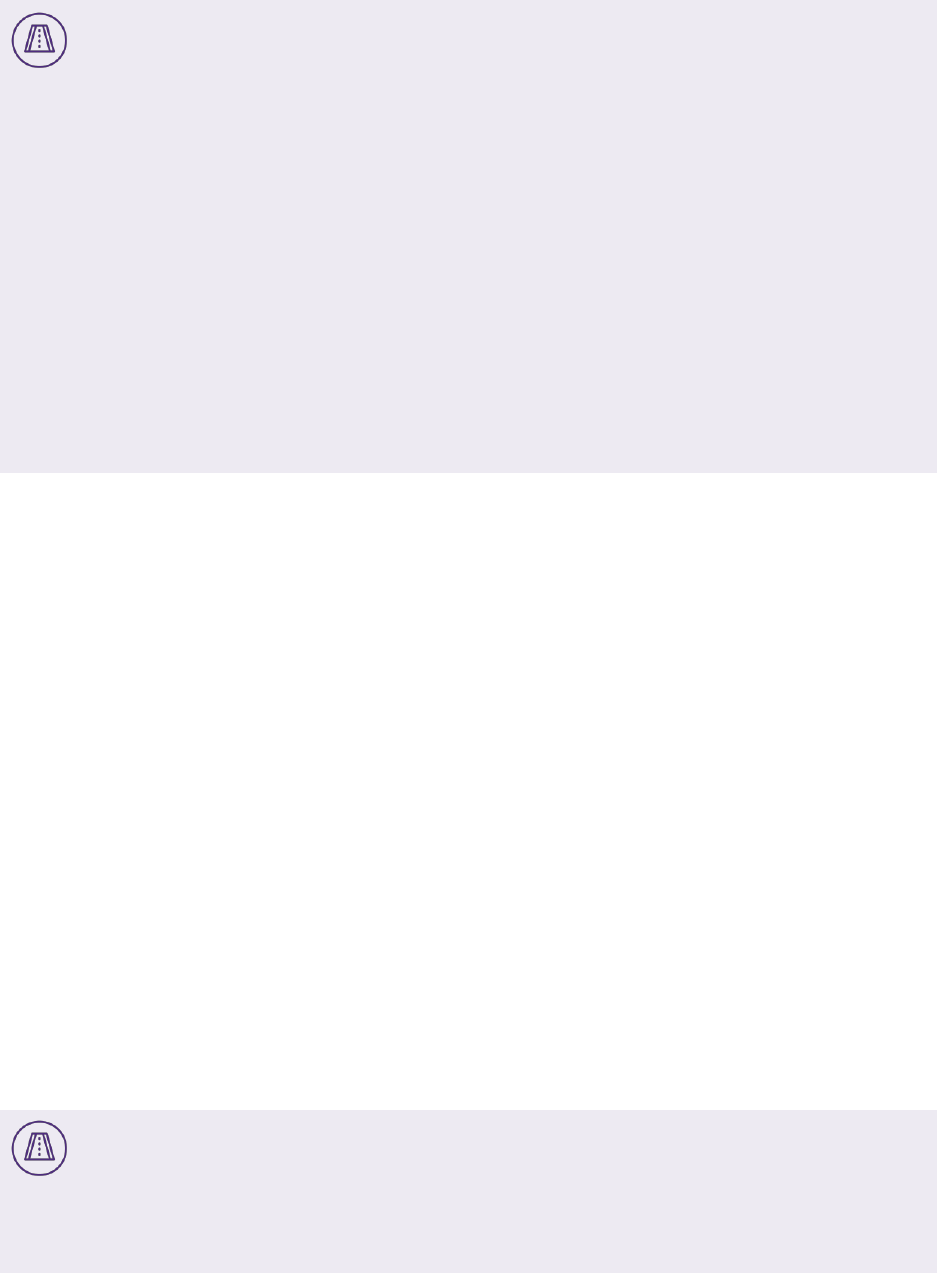

Figure 2.1: Accounting for costs incurred to develop internal-use software

Entities should consider the activities being performed when determining the software project’s stage of

development. The guidance in ASC 350-40-55-3 outlines activities and processes that fall into each stage

of development. For example, a software development project would be in the preliminary phase while

the entity determines the performance and system requirements for the software as well as evaluates

potential methods for meeting those identified requirements.

Define system

requirements,

formulate a plan

Expense

Design, coding,

hardware installation,

testing

Capitalize

Training, routine

maintenance

Expense

Changes beyond

routine maintenance

Capitalize or

expense

Preliminary project

phase

Application

development phase

Post-implementation

phase

Upgrades and

enhancements

Internal-use software 23

ASC 350-40-55-3

The following list illustrates the various stages and related processes of computer software

development:

a. Preliminary project stage:

1. Conceptual formulation of alternatives

2. Evaluation of alternatives

3. Determination of existence of needed technology

4. Final selection of alternatives.

b. Application development stage:

1. Design of chosen path, including software configuration and software interfaces

2. Coding

3. Installation to hardware

4. Testing, including parallel processing phase.

c. Postimplementation−operation stage:

1. Training

2. Application maintenance.

ASC 350-40-55-4

This Subtopic recognizes that the development of internal-use computer software may not follow the

order shown in the preceding list. For example, coding and testing are often performed simultaneously.

Regardless, for costs incurred subsequent to completion of the preliminary project stage, the guidance

shall be applied based on the nature of the costs incurred, not the timing of their incurrence. For

example, while some training may occur in the application development stage, it should be expensed

as incurred as required in paragraphs 350-40-25-2 through 25-6.

Grant Thornton insights: Evaluating costs when project stages are unclear

Many entities conduct multiple project stages simultaneously when developing internal-use software.

For instance, a software project might revert back to a previous stage due to various developmental

issues, which creates complexities when applying the guidance in ASC 350-40.

ASC 350-40-55-3 outlines which processes fall into each stage of product development, but the

FASB has acknowledged that these stages and processes do not always occur linearly in the order

presented in the guidance. When project stages fluctuate or are not clearly distinguishable, we believe

that entities should focus on the type of activity being conducted rather than on the project stage.

For example, an entity that commits to funding a software project from start to finish and selects

a specific project from among alternatives would consider the project to be in the application

Internal-use software 24

development stage, and would capitalize development costs incurred after that point. In contrast, an

entity that commits to funding a project before evaluating project alternatives and selecting a specific

solution would account for the costs incurred during the selection phase as part of the preliminary

project stage, based on the nature of those costs, even though the entity had already committed to

the project.

2.1 Preliminary project stage

The preliminary project stage is the period during which an entity determines the performance and system

requirements for the proposed internal-use software and evaluates potential methods for meeting the

project’s requirements with the resources available. In general, an entity is assessing its needs and

evaluating various alternatives in the preliminary project stage. This stage includes defining and creating

a plan to develop and / or implement the proposed internal-use software, as well as selecting vendors if

the software will be purchased or consultants will assist with implementing the plan. Activities undertaken

in the preliminary project stage are analogous to research and development activities. Entities should

expense all costs incurred during this stage.

The ASC Master Glossary outlines the types of activities an entity may perform during the preliminary

project stage.

Preliminary Project Stage

When a computer software project is in the preliminary project stage, entities will likely do the following:

a. Make strategic decisions to allocate resources between alternative projects at a given point in time.

For example, should programmers develop a new payroll system or direct their efforts toward

correcting existing problems in an operating payroll system?

b. Determine the performance requirements (that is, what it is that they need the software to do) and

systems requirements for the computer software project it has proposed to undertake.

c. Invite vendors to perform demonstrations of how their software will fulfill an entity’s needs.

d. Explore alternative means of achieving specified performance requirements. For example, should

an entity make or buy the software? Should the software run on a mainframe or a client server

system?

e. Determine that the technology needed to achieve performance requirements exists.

f. Select a vendor if an entity chooses to obtain software.

g. Select a consultant to assist in the development or installation of the software.

The following example shows the types of costs incurred during the preliminary stage of a project.

Internal-use software 25

2.2 Application development stage

Typically, when the preliminary project stage is completed and an entity decides to move forward with a

software project and commits to funding the project through completion, the project enters the application

development stage. The application development stage includes (1) designing the development path,

including software configuration and software interfaces, (2) coding, (3) installation and (4) testing,

including parallel processing.

During this stage, the entity is required to capitalize internal and external costs to develop internal-use

software. Costs to develop or obtain software that provides access to or conversion of old data by new

systems should also be capitalized. In order to capitalize costs, management must authorize the project

and be sufficiently committed to the point that it is probable that the software will be fully developed and

used to perform its intended function. Authorization to develop the software may be explicit, as in the

case of an executed contract with a third party, or it may be implicit, such as budgeting for expenses that

will be incurred to develop the software.

ASC 350-40-25-12

Capitalization of costs shall begin when both of the following occur:

a. Preliminary project stage is completed.

b. Management, with the relevant authority, implicitly or explicitly authorizes and commits to funding a

computer software project and it is probable that the project will be completed and the software will

be used to perform the function intended.

Accounting for costs incurred during the preliminary project stage

A trade association tracks membership data using a database stored on its internal network. While this

system is functional, the association determines that members would benefit greatly from online access

to the data. The association performs initial outreach to obtain information about the cost of providing its

members online access. Based on the initial data collected, the association decides to move forward

with the project and allocates money for the project in its annual budget.

The association sets up a committee comprising certain members of management as well as members

of the association to develop a list of requirements and desired functionality for the proposed online

membership system. The committee evaluates existing off-the-shelf products as well as proposals to

develop a customized solution from outside vendors. After several months, the committee selects a

vendor that specializes in online membership software programs to provide a customized interface for

members to access the system.

All expenses incurred during this preliminary project period would be expensed as incurred. Even

after the association committed to the project and allocated a portion of its budget to the changes,

the nature of the expenses incurred by the committee related to determining the performance and

system requirements for the proposed software and to evaluating potential methods for meeting those

requirements. As a result, all costs incurred in this example are considered preliminary-project-stage

costs and are expensed as incurred.

Internal-use software 26

Examples of authorization include the execution of a contract with a third party to develop the software,

approval of expenditures related to internal development, or a commitment to obtain the software from

a third party.

As previously noted, in determining whether to capitalize or expense costs for developing internal-use

software, an entity must consider not only the project phase, but also the nature of the expenses incurred

and whether they relate to developing the software. Entities should capitalize any costs that directly relate

to the development of the software, including direct costs of materials or services provided externally, and

payroll and payroll-related costs for employees’ time spent directly on the development of the software.

The amounts capitalized should include interest costs incurred while developing the software in

accordance with ASC 835-20, Interest: Capitalization of Interest.

ASC 350-40-25-2

Internal and external costs incurred to develop internal-use computer software during the application

development stage shall be capitalized.

ASC 350-40-25-3

Costs to develop or obtain software that allows for access to or conversion of old data by new systems

shall also be capitalized.

ASC 350-40-25-4

Training costs are not internal-use software development costs and, if incurred during this stage, shall

be expensed as incurred.

ASC 350-40-25-5

Data conversion costs, except as noted in paragraph 350-40-25-3, shall be expensed as incurred. The

process of data conversion from old to new systems may include purging or cleansing of existing data,

reconciliation or balancing of the old data and the data in the new system, creation of new or additional

data, and conversion of old data to the new system.

While a project is in the application development stage, the entity should carefully review the nature of the

costs incurred, as costs that do not directly relate to the development of the software are not capitalizable.

For example, entities should expense all costs to train employees on how to use the software, even if the

costs are incurred during the application development stage.

Transferring data from existing software to newly developed or purchased software is an activity that

usually happens during the application development phase. If the data is converted between systems

using manual processes, the cost to do so should be expensed as incurred. However, if the data will be

converted using software, the cost of developing or purchasing software to perform the conversion should

be capitalized as software development costs. All costs to manually convert data from the old system,

including purging existing data, reconciling data between the systems, or importing old data into the new

system are expensed as incurred.

Internal-use software 27

Costs of converting software

Entity A and Entity B are both developing internal-use software to replace existing software. Both

projects are in the application development phase. Both entities need to convert data from their

existing software to the software being developed.

Entity A needs to convert data from its existing inventory tracking system to the new software it has

developed. Entity A tasks some of its inventory management staff to manually type the data from the

old system into the new system. The cost of the employees who manually enter the data, as well as the

employees who review the data once input, is an expense in the period incurred. Although the project is

in the application development phase, the activity of manually converting data is not a captializable cost.

Entity B needs to convert data from its existing customer data management system to the new software

it is developing. Entity B tasks its project team to build a software program that will automatically extract

the data from the existing system, reformat it, and import it into the new system. The cost to develop

the conversion software would be capitalized subject to the guidance in ASC 350-40. Any manual

processes performed in addition to the development of the software, such as reconciling between the

old and new system once the software has completed the conversion, are expensed as incurred.

ASC 350-40-30-1

Costs of computer software developed or obtained for internal use that shall be capitalized include only

the following:

a. External direct costs of materials and services consumed in developing or obtaining internal-use

computer software. Examples of those costs include but are not limited to the following:

1. Fees paid to third parties for services provided to develop the software during the application

development stage

2. Costs incurred to obtain computer software from third parties

3. Travel expenses incurred by employees in their duties directly associated with developing

software.

b. Payroll and payroll-related costs (for example, costs of employee benefits) for employees who are

directly associated with and who devote time to the internal-use computer software project, to the

extent of the time spent directly on the project. Examples of employee activities include but are not

limited to coding and testing during the application development stage.

c. Interest costs incurred while developing internal-use computer software. Interest shall be

capitalized in accordance with the provisions of Subtopic 835-20.

Only direct costs of the internal-use software are eligible for capitalization. General and administrative or

overhead costs are expensed as incurred. Examples of such costs include depreciation of the computers

or an allocation of rent to the space used by the computer programmers.

Internal-use software 28

ASC 350-40-30-3

General and administrative costs and overhead costs shall not be capitalized as costs of internal-use

software.

The following example illustrates how an entity would account for costs incurred during the application

development stage in an internal-use software project.

Accounting for costs incurred during the application development stage

A manufacturing entity purchases equipment to use in its manufacturing process and authorizes an

internal team of engineers to customize the software embedded in the equipment.

The entity has previously expensed the costs incurred to determine the performance and system

requirements for the project, as well as costs involved in evaluating whether to customize the software

in-house or hire a third-party consultant. Management commits to moving forward with the project using

the internal team by including the associated costs in its budget.

During the current year, the entity incurs $1 million in total payroll and benefits costs for the software

engineers, but only 25 percent, or $250,000, of that amount is directly related to working on the software

project. The entity incurs $50,000 in costs to train employees on how to operate the customized

equipment. The entity has also allocated a portion of overhead for rent and utilities, totaling $100,000,

to the software engineering group based on the square footage of the engineering space divided by the

total square footage of the leased property. Of that amount, the entity allocates the same proportion as

payroll and benefits for the engineers (25%) to the application development stage.

The entity capitalizes payroll and benefits related to the employees’ time spent directly working on

the project. In other words, the software engineers are required to track their time, and their salary is

allocated proportionately to this development stage based on the time spent coding and testing the

software. The entity expenses training and overhead costs, including the allocated rent and utilities, as

incurred.

The table below summarizes the costs incurred in the application development phase during the year,

as well as the accounting treatment for each type of cost.

Type of cost

Amount

allocated

Capitalize

or expense?

Engineering payroll

$250,000

Capitalize

Training

$ 50,000

Expense

Allocated overhead for rent

and utilities

$ 25,000

Expense

Internal-use software 29

2.2.1 Acquiring a software license for internal use

An entity may license software for internal use from a third party. When this happens, an entity should

first look to the guidance in Section 1.4 for identifying hosted software to determine if the license is an

asset or a service. If it is not a service (not hosted software), the software license is recognized at cost

as an intangible asset that is amortized over its useful life. If the entire license fee is not paid at license

inception, for example, if it will be paid over the license term, the asset should be recorded at total

contractual cost (or allocated cost in a multiple-element arrangement, see Section 2.2.2), and a liability

is recognized for future payments under the license agreement. The initial measurement guidance in

ASC 350-40-25 refers to the general intangible assets guidance in ASC 350-30, Intangibles: General

Intangibles Other Than Goodwill, for recognition and measurement of software licensed from third parties.

The intangible assets guidance then refers to the asset acquisition guidance in ASC 805, Business

Combinations, specifically 805-50-15-3 and 805-50-30-1 to 30-4, which requires an acquired intangible

asset to be recognized at cost.

ASC 350-40-25-17

Entities often license internal-use software from third parties. A software license within the scope of this

Subtopic (see paragraphs 350-40-15-1 through 15-4C) shall be accounted for as the acquisition of an

intangible asset and the incurrence of a liability (that is, to the extent that all or a portion of the software

licensing fees are not paid on or before the acquisition date of the license) by the licensee. The

intangible asset acquired shall be recognized and measured in accordance with paragraphs 350-30-

25-1 and 350-30-30-1, respectively.

2.2.2 Multiple elements included in purchase price

An arrangement to purchase internal-use software or a cloud computing arrangement may include

multiple elements, such as a license, implementation services, training, and maintenance. An entity

that purchases software or hosting services from a third party in a multiple-element arrangement should

Licensing software for internal use

An entity purchases a two-year software license from a vendor for inventory tracking software for

$120,000. The entity pays $60,000 when it enters into the license and will pay the remaining $60,000

at the end of the first year. At inception of the license term the entity records the following entry to

recognize the license and the liability for payment:

DR: Software license $120,000

CR: Cash $60,000

CR: Software license payable $60,000

Each month the entity records entries to amortize the software license:

DR: Amortization of software license $10,000

CR: Software license $10,000

Internal-use software 30

allocate the consideration paid to the various elements based on their relative stand-alone selling price.

The entity should capitalize only the costs that meet the capitalization criteria in ASC 350-40. An entity

should not default to allocating the total cost to the various elements based on each element’s stated

price within the multiple-element contract.

ASC 350-40-30-4

Entities may purchase internal-use computer software from a third party or may enter into a hosting

arrangement. In some cases, the price includes multiple elements, such as the license or hosting,

training for the software, maintenance fees for routine maintenance work to be performed by the third

party, data conversion costs, reengineering costs, and rights to future upgrades and enhancements.

Entities shall allocate the cost among all individual elements. The allocation shall be based on the

relative standalone price of the elements in the contract, not necessarily separate prices stated

within the contract for each element. Those elements included in the scope of this Subtopic shall be

accounted for in accordance with the provisions of this Subtopic.

Grant Thornton insights: Estimating stand-alone selling price