LEGISLATIVE ANALYST’S OFFICE

CALIFORNIA’S TAX SYSTEM

California’s state and local governments rely on three main taxes. The personal

income tax is the state’s main revenue source, the property tax is the major

local tax, and the state and local governments both receive revenue from the

sales and use tax. In addition, many smaller taxes raise revenue for state and

local government operations. In 2015-16, taxes in California raised a total of

$220 billion—equal to nearly 10 percent of the state economy.

The chart to the right summarizes this tax system. The inner black pie chart shows

that roughly two-thirds of tax revenues in California go to the state government

with the other one-third collected by local governments. The middle ring shows

each tax as a share of the whole system. (Note that the line from the inner black

pie chart intersects with the sales and use tax segment to show the shares of

sales tax revenue that go to the state and to local governments.) The outer ring

breaks out each major tax by source. For example, the biggest source of personal

income tax revenue is wage and salary income.

In addition to taxes, the state and local governments rely on federal funds, fees,

and other sources of revenue to fund government operations. This publication,

however, focuses solely on taxes levied in California.

INTRODUCTION

2

LAO California’s Tax System | Overview

OVERVIEW OF CALIFORNIA’S TAX SYSTEM

3

LAO California’s Tax System | Overview

Wages and Salaries

Retirement Income

Dividends,

Interest, and Rent

Business Income

Capital Gains

Other

Corporations

Gasoline,

Diesel, and Other

Motor Vehicle

and Parts Dealers

Furniture, Home Furnishings, Electronics, and Appliance

Building Materials and Garden Supplies

Food and Beverage Stores

Gasoline Stations

Clothing and Accessories Stores

General

Merchandise Stores

Bars and

Restaurants

Other Retailers

Construction and Re

al Estate

Manufacturing

Wholesalers

Other Non-Retail

Businesses

Other

Commercial/Industrial

Residential Not

Owner-Occupied

Payroll

Property Transfer

Business

Utilities

Hotels

Vehicle License Fee

Tobacco Taxes

Insurance Tax

Personal

Income Tax

Corporation Tax

Fuel Taxes

Other State Taxes

Sales and

Use Tax

Other Local Taxes

Property Tax

State

Local

Residential

Owner-Occupied

Alcoholic Beverage Tax

Other Entities

2015-16

4

LAO California’s Tax System | Personal Income Tax (PIT)

1

CHAPTER

5

LAO California’s Tax System | Personal Income Tax (PIT)

The personal income tax (PIT) is a broad-based tax

that the state levies on most types of income, such

as wages and capital gains. The PIT is an important

revenue source for the state government, generating

over two-thirds of the revenue for the General Fund—

the state’s main operating account. In recent years,

the PIT has generated more revenue than any other

tax in California’s tax system.

PERSONAL

INCOME TAX

6

LAO California’s Tax System | Personal Income Tax (PIT)

ABOUT TWO-THIRDS OF INCOME

COMES FROM WAGES AND SALARIES

Business

Income

(Sole Owner)

$53 Billion

Dividends,

Interest,

and Rent

$56 Billion

Business

Income

(Multiple

Owners)

$88 Billion

Pensions,

Annuities,

and IRA

Distributions

$102 Billion

Capital Gains

$118 Billion

Wages and Salaries

$898 Billion

Personal income tax rates are marginal, meaning that higher income increments are taxed at

higher rates. For example, a single filer with taxable income of $300,000 is taxed at 1 percent on

the first $8,000 of their income, but 10.3 percent on the last $31,000 of their income. A taxpayer’s

highest marginal rate is higher than their effective rate (the average rate at which their income is

taxed). For example, a single filer with $100,000 in taxable income is taxed at 9.3 percent on their

last dollar of income but their effective tax rate (before tax credits) is 6.7 percent.

2015

Marginal Rate

Effective Rate

2

4

6

8

10

12

14%

100,000 200,000 300,000 400,000 500,000 600,000 700,000 $800,000

Marginal

Rate

1%

2%

4%

6%

Income

Between

$0K - $8K

$8K - $19K

$19K - $30K

$30K - $42K

8% $42K - $53K

9.3%

10.3%

11.3%

12.3%

$53K - $269K

$269K - $322K

$322K - $537K

$537K - $1M

13.3% $1M and Over

HOW DO PIT RATES WORK?

Marginal and Effective Tax Rates, Single Filer, 2017

7

LAO California’s Tax System | Personal Income Tax (PIT)

Do itemized

deductions exceed

$8,472 standard

deduction?

Step 1 Add up Income

$60K in Wages

$30K in Business Income

$90K

Adjusted Gross Income

Step 2 Add up Deductions

$8K in Mortgage Interest

$5K in Local Property Taxes

$2K in Student Loan Interest

$15K Itemized Deductions

Step 3

Calculate Taxable Income

$90K Adjusted Gross Income

$15K Itemized Deductions

$75K Taxable Income

Step 4

Apply Tax Rates in Table Above

First $16K Taxed at 1% = $164

Next $23K Taxed at 2% = $451

Next $23K Taxed at 4% = $902

Next $23K Taxed at 6% = $808

Tax Liability Before Credits $2,325

Step 5 Add up Tax Credits

$400 Child Care Tax Credit

$114 X 2

Personal Exemption Credit

$353 Dependent Exemption Credit

$981 Total Tax Credits

Step 6 Calculate Tax Liability

Tax Liability Before Credits $2,325

Minus Credits -$981

Final Tax Bill = $1,344

Yes: take

itemized

No: take

standard

25

50

75

100%

0-50K 50K-100K 100K-200K 200K-500K 500K-1M 1M-5M Over $5M

Standard Itemized

Filers Itemizing Deductions Tend to Be Higher-Income Taxpayers

Almost two-thirds of all filers take the standard deduction

Marignal

Rate

1%

2%

4%

6%

Income

Between

$0-$16K

$16K-$39K

$39K-$62K

$62K-$85K

CALCULATING THE

PERSONAL INCOME TAX BILL

Married Couple With One Dependent Filing Jointly, 2017

8

LAO California’s Tax System | Personal Income Tax (PIT)

BREAKDOWN OF DEDUCTIONS

In Billions, 2015

PIT deductions reduce taxpayers’ taxable incomes. In total, deductions reduced taxable income

by about $200 billion in 2015. About $7 billion of the deductions shown here went unused because

itemized deductions are phased out for high-income taxpayers.

$60.7

$52.9

$4.3

$30.1

$20.4

$10.6

Standard

Deduction

Mortgage

Interest

Property

Taxes

Business and

Other Expenses

Medical

Expenses

Other

$30.0

Charitable

Contributions

25

50%

$0K - $20K

$20K - $50K

$50K - $100K

$100K - $200K

$200K - $500K

$500K - $1M

$1M and Over

Standard Deduction

Medical Expenses

Mortgage Interest

Property Taxes

Charitable Contributions

Business and Other Expenses

WHO USES DEDUCTIONS?

Share of Deduction Value by Income Group, 2015

9

LAO California’s Tax System | Personal Income Tax (PIT)

BREAKDOWN OF CREDITS

In Billions, 2015

$4.0

$2.3

$0.4

$0.3

$0.2

$0.1

$1.1

Dependent Credit

Personal Credit

Blind and Senior

Credit

Enterprise Zones

EITC

Renter's Credit

Other

WHO USES CREDITS?

25

50%

Dependent Credit Personal Credit

Blind and Senior Credit

Renter’s Credit

EITC

Enterprise Zones

100

66

55

$0K - $20K

$20K - $50K

$50K - $100K

$100K - $200K

$200K - $500K

$500K - $1M

$1M and over

PIT credits reduce tax liabilities dollar for dollar, resulting in a dollar-for-dollar reduction in state

revenue. With the exception of the Earned Income Tax Credit (EITC), credits cannot reduce a

taxpayer’s liability below zero. For this reason, the amount of credits shown in the chart is about

double the amount of credits actually used by taxpayers to reduce liability.

Share of Credit Value by Income Group, 2015

10

LAO California’s Tax System | Personal Income Tax (PIT)

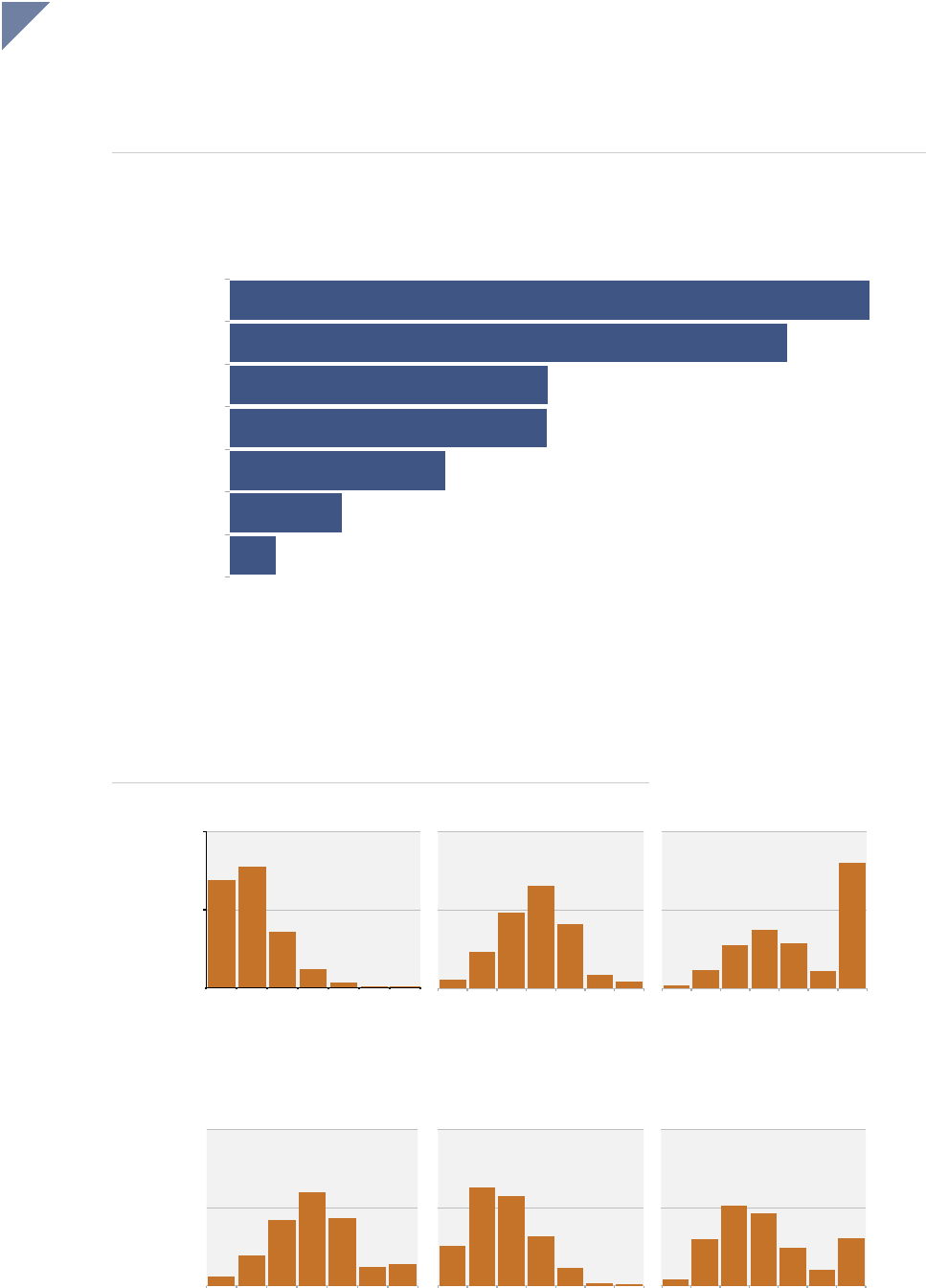

PIT LIABILITY CONCENTRATED AMONG TOP EARNERS

Tax Statistics by Income Group, 2015

$0 to $20K

$20K to $50K

$50K to $100K

$100K to $200K

$200K to $300K

$300K to $500K

$500K to $1M

Over $1M

27.7%

31.0%

21.2%

12.9%

3.2%

1.7%

0.8%

0.4%

3.7%

13.0%

19.1%

22.4%

9.8%

8.3%

6.9%

19.4%

0.1%

2.0%

8.6%

18.0%

10.7%

10.6%

10.3%

39.6%

Share of Tax Returns Share of Adjusted Gross Income Share of Tax Liability

$1M

to 2M

$2M

to 3M

$3M

to 4M

$4M

to 5M

Over

$5M

Over Half of PIT Liability for Over $1 Million Group

Paid by Filers With Adjusted Gross Income Over $5 Million

21% 10% 7% 5% 57%

11

LAO California’s Tax System | Personal Income Tax (PIT)

INCOME MAKEUP DIFFERENT

FOR LOW- AND HIGH-INCOME TAXPAYERS

2015

The graphic below shows how taxpayers in different income groups derive their income. Some types of

income, including wages and salaries and retirement income (pensions, annuities, and IRA distributions)

make up the majority of low- and middle-income taxpayers’ incomes. These sources, however, account

for a minority of the total incomes of the highest-income taxpayers, whose incomes are derived mostly

from capital gains, partnership income, and dividends, interest, and rent. (All other income—mostly

proprietors’ income—is shown in grey.)

25

50

75

100%

0-40K 40K-70K 70K-100K 100K-150K 150K-200K 200K-300K 300K-400K 400K-500K 500K-1M 1M-2M 2M-3M 3M-4M 4M-5M Over $5M

HIGH-INCOME TAXPAYERS RELY

MORE ON VOLATILE INCOME SOURCES

Total Percent Change, 2015 Dollars

50

100

150

200

250%

1996 2001 2006 2011

-50

Wages and Salaries

Capital Gains

Partnership

Income

Dividends, Interest, and Rent

Retirement Income

2015

50

100

150

200

250%

1996 2001 2006 2011

-50

2015

12

LAO California’s Tax System | Personal Income Tax (PIT)

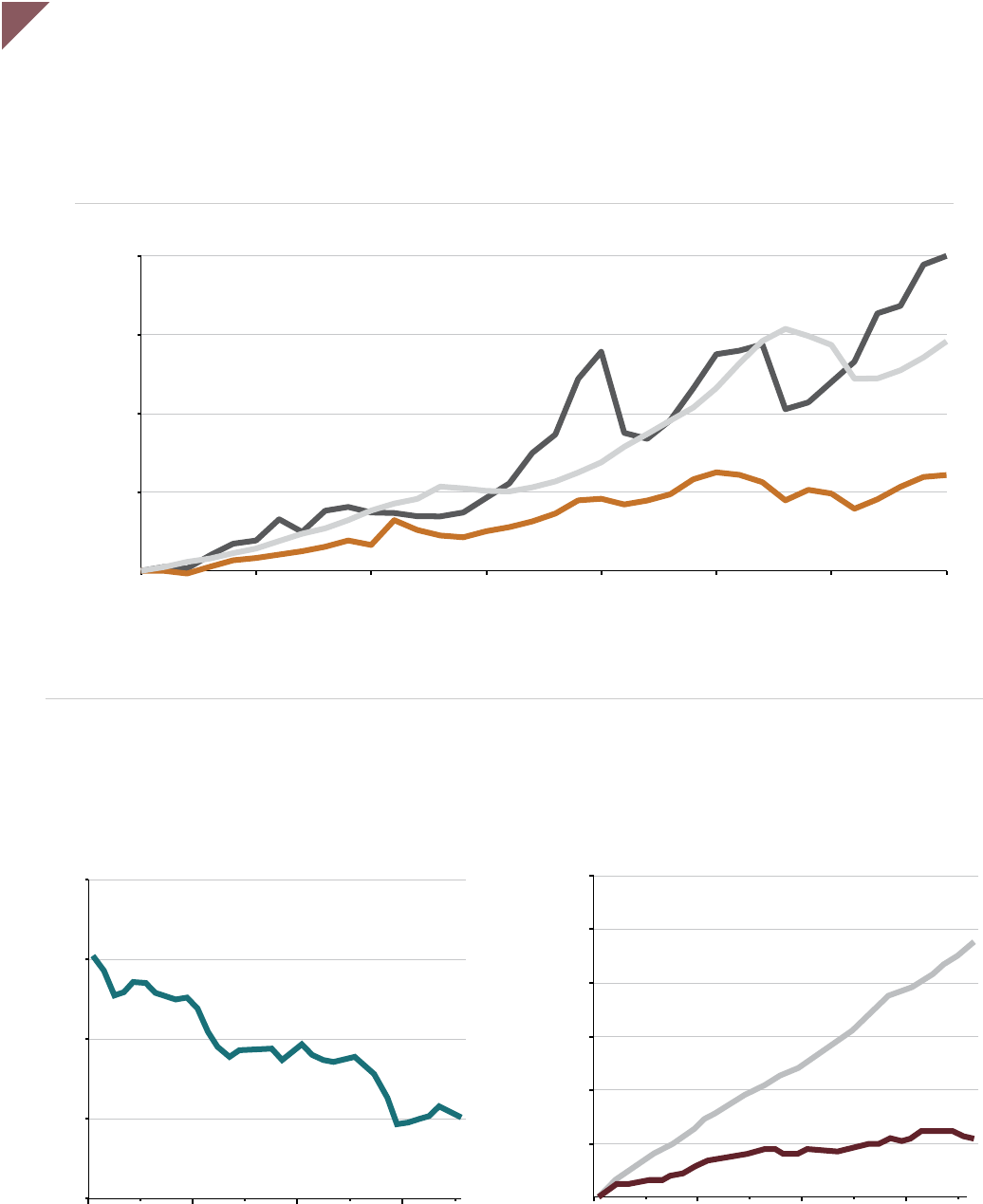

CAUSES OF PIT VOLATILITY

Average Deviation, 1990 to 2014

Average deviation (AD) is a measure of revenue volatility. With an AD of 12.2, the PIT is over five times more

volatile than personal income (2.3). About 40% of the higher volatility is due to the state’s choices about

which types of income to tax. Another 40% is due to taxing higher income at higher rates. The last 20%

comes from PIT credits and deductions, which mostly reduce the relatively stable part of the tax base.

PIT MORE VOLATILE THAN PERSONAL INCOME

Annual Percent Change

-30

-20

-10

10

20

30

40%

1997 2002 2007 2012

Personal Income Tax

Personal Income

5

10

15

Volatility of

Personal Income

Definition of

PIT Base

Graduated

Rate Structure

Credits

and Deductions

Volatility of PIT

As the state’s main revenue source, the highly volatile PIT results in revenue uncertainty, thus complicating

state budgeting. (Personal income is an overall measure of the economy that includes individuals’ wages,

business income, and various other types of income, but that excludes capital gains income.)

13

LAO California’s Tax System | Personal Income Tax (PIT)

WITH VOLATILITY COMES GREATER REVENUE GROWTH

Bulk of Income Growth Has Gone to High-Income Taxpayers...

Adjusted Gross Income Per Return by Income Range, Total Percent Change, 2015 Dollars

The top 1% of taxpayers typically pay between 40% and 50% of the PIT. Their incomes are highly volatile,

which has contributed to PIT volatility. On the other hand, their incomes also have grown more than any other

group of taxpayers. This has contributed to PIT growth.

...Which Has Contributed to PIT Revenues Growing Much Faster Than Revenues

From Other State Taxes

Total Percent Change, 2015-16 Dollars

95

th

to 99

th

90

th

to 95

th

-25

25

50

75

100

125%

1996 2001 2006 2011

Top 1 Percentile

Bottom Four Quintiles

80

th

to 90

th

2015

-25

25

50

75

100

125

150%

1996-97 2001-02 2006-07 2011-12

Personal Income Tax

Sales and Use Tax

Corporation Tax

2015-16

14

LAO California’s Tax System | Personal Income Tax (PIT)

VOLATILITY OF THE PIT BASE

State law specifies which types of income are subject to the

personal income tax. In general, California has chosen to tax

relatively volatile types of income, as illustrated by the chart

on the next page. The boxes are shaded by their volatility

measure (average deviation). An item with a measure of 6 is

twice as volatile as an item with a measure of 3.

Personal income is an economic statistic that includes most

types of income. Different portions of personal income are

subject to tax. Some portions of personal income are more

volatile than others. For example, the portion of dividends,

interest, and rent flowing to the PIT base is more volatile

(darker) than the portion not in the PIT base. California

also chooses to tax some types of income not included in

personal income. In particular, capital gains income, with a

volatility measure of 35, is more than twice as volatile as any

other part of the PIT base. Overall, the PIT base is almost

three times as volatile as personal income.

15

LAO California’s Tax System | Personal Income Tax (PIT)

PIT BASE MORE VOLATILE THAN PERSONAL INCOME

Average Deviation, 1990-2014

Wages and

Salaries

Dividends,

Interest,

and Rent

Proprietor and

Partnership

Transfer

Payments

Employer-Paid

Benefits

Components of

Personal Income

Pensions and IRA Distributions

Capital Gains

Items Not in

Personal Income

Personal Income

Tax Base

Pensions and IRA Distributions

Capital Gains

Wages and

Salaries

Dividends, Interest, and Rent

Proprietor and Partnership

Items Not

Included in

PIT Base

Wages and Salaries

Dividends, Interest, and Rent

Transfer Payments

Employer-Paid Benefits

Average Deviation

Under 3

3.1 - 6

6.1 - 9

9.1 - 12

Over 12

Proprietor and Partnership

Within these broad categories, some components of personal income are in the

tax base and others are untaxed. For example, interest earned from corporate

bonds is taxed but interest earned from municipal bonds is untaxed.

16

LAO California’s Tax System | Personal Income Tax (PIT)

HIGHER INCOMES CONCENTRATED IN BAY AREA

2013

The graphic below shows how incomes by county compare to the statewide average. A blue shade

indicates that a county has fewer taxpayers in that income range, a yellow shade indicates the county

is near the statewide average, and an orange shade indicates they have more taxpayers in that range.

Compared to the statewide average, Marin county has 4.6 times more taxpayers in the over $1 million

range, the most of any county.

Region County $500K to $1M Over $1M

Alameda

Contra Costa

Marin

Napa

San Benito

San Francisco

San Mateo

Santa Clara

Solano

Sonoma

Los Angeles

Orange

Ventura

San Diego

San Diego

Monterey

San Luis Obispo

Santa Cruz

Santa Barbara

El Dorado

Placer

Sacramento

Yolo

Fresno

Kern

Kings

Madera

Mariposa

Merced

San Joaquin

Stanislaus

Amador

Butte

Calaveras

Colusa

Del Norte

Glenn

Humboldt

Imperial

Inyo

Lake

Lassen

Mendocino

Modoc

Mono

Nevada

Plumas

Shasta

Sierra

Siskiyou

Sutter

Tehama

Trinity

Tulare

Tuolumne

Yuba

Riverside

San Bernardino

Rest of State

Inland

Empire

$300K to $500K

Bay Area

Los

Angeles

Central

Coast

Sacramento

San

Joaquin

Valley

$0 to $15K $15K to $30K $30K to $50K $50K to $80K $80K to $150K $150K to $300K

Legend

12.5 Times Less Frequent

Than Statewide Average

Equal to State Average 4.6 Times More Frequent

Than State Average

17

LAO California’s Tax System | Personal Income Tax (PIT)

Average deviation (AD) is a measure of revenue volatility. With an AD of 16.3, personal income tax paid by Bay

Area residents from 1996-2014 was over 40 percent more volatile than for tax paid statewide (11.4).

2014

BAY AREA CONTRIBUTES DISPROPORTIONATELY TO PIT

Average Deviation, 1996-2014

PIT PAID BY BAY AREA MORE VOLATILE THAN REST OF STATE

10

20

30

40

50%

10 20 30 40 50 60 70 80 90 100%

Percent of Personal Income Tax Paid

Percent of Population

Los Angeles

Sacramento

San

Diego

Central

Coast

San

Joaquin

Valley

Rest

of

State

Inland

Empire

Bay Area

The Bay Area pays nearly 40% of the

PIT but only makes up 20% of population.

By contrast, Los Angeles’ tax paid (34%)

is closer to its share of the population (36%).

500 1,500 2,500 $3,500

Bay Area

Los Angeles

San Diego

Central Coast

Sacramento

Central Valley

Rest of State

Inland Empire

Per Capita Taxes Paid by Region

16.3

12.0

11.4

10.0

9.2

7.5

7.4

7.0

6.9

Bay Area

Central Coast

Statewide

San Diego

Los Angeles

Rest of State

Sacramento

San Joaquin Valley

Inland Empire

2

18

LAO California’s Tax System | Property Tax

CHAPTER

19

LAO California’s Tax System | Property Tax

For many California taxpayers, the property tax bill is one

of the largest tax payments they make each year. For

thousands of California local governments—K–12 schools,

community colleges, cities, counties, and special districts—

revenue from property tax bills represents the foundation

of their budgets. Cities, counties, and special districts use

property tax revenues to support municipal services like

police, fire, and parks. Property tax revenue remains in the

county in which it is raised.

Property taxes are levied by local governments on real

property (principally land and buildings), as well as some

types of personal property, which includes business

property (like manufacturing equipment), aircrafts, and

vessels. Proposition 13 (1978) limits the property tax

on real property to 1 percent of assessed value. Under

Proposition 13, assessed value for real property is limited

to the price paid for the property increased each year by 2

percent or inflation, whichever is lower. In contrast, personal

property is taxed based on its market value. In 2016-17,

statewide property tax revenues were about $60 billion.

PROPERTY TAX

20

LAO California’s Tax System | Property Tax

This figure shows the assessed value of each type of property subject to the property tax.

In most cases, county assessors determine the value of property within the county. For

a subset of property—like natural gas pipelines—the state determines the value of the

property. Statewide, the assessed value of taxable property is over $5.7 trillion.

WHAT IS SUBJECT TO THE PROPERTY TAX?

2016-17

Vacant Land $115 Billion

Single Family Homes

$2.9 Trillion

Commercial

and Industrial

$1.1 Trillion

Multifamily

and Condos

$939 Billion

State Assessed $103 Billion

Agricultural and Rural Land $101 Billion

Oil, Minerals, and Gas $22 Billion

Aircraft $19 Billion

Watercraft $6 Billion

Personal Property $203 Billion

21

LAO California’s Tax System | Property Tax

SAMPLE ANNUAL PROPERTY TAX BILL

Property ID: 1234567

Mailing Address:

Doe, Jane

1234 ABC Street

Sacramento, CA 00000

2016-17 Roll

Land

Improvements

Total

Less Exemptions

Net Assessed Value

Assessed Value

$115,000.00

$242,000.00

$357,000.00

$7,000.00

$350,000.00

Secured Property Tax for Fiscal Year July 1, 2016 to June 30, 2017

Property Owner Information

Property Valuation on Jan 1, 2012

Detail of Taxes Due

Agency

General Tax Levy

Voter-Approved Debt Rates

City

Water District

School District

Community College District

Direct Levies

Sidewalk District Assessment

Flood Control District Assessment

Street Lighting District Assessment

Mello-Roos District

School District Parcel Tax

Total Taxes Due

1st Installment

2nd Installment

Rate

1.0000

0.0201

0.0018

0.1010

0.0102

Amount

$3,500.00

$70.35

6.30

353.50

35.70

$9.36

64.39

12.71

86.51

125.00

$4,263.82

$2,131.91

2,131.91

Taxable Value

Each year, county assessors determine

each property’s assessed value,

which includes the value of both land

and buildings. Assessed value typically

is based on a property’s purchase

price. In the year a property is

purchased, it is taxed at its purchase

price. Each year thereafter, its assessed

value is increased by inflation or

2 percent, whichever is lower. Upon

resale, it is again taxed at its purchase

price. If a property’s market value dips

below its inflation-adjusted purchase

price, it is typically taxed on its market

value instead.

Exemptions

Certain exemptions can reduce

a property’s assessed value. The

most common is the homeowner’s

exemption, which reduces an

owner-occupied home’s assessed

value by $7,000.

Ad Valorem Taxes

Taxes based on the value of

property are known as ad valorem

taxes. Proposition 13 capped the

ad valorem property tax rate at

1 percent plus voter-approved

add-on rates to for certain debt

repayments.

Other Taxes and Charges

Local governments may levy

other charges on property that

are not ad valorem taxes. Often,

these charges are based on

the benefits the propertyowner

receives from the service

or improvement.

Total Payment

County tax collectors divide

properties’ total tax bill into two

payments. The first payment is

due by December 10

th

and

the second payment is due by

April 10

th

. Many homeowners pay

their property taxes as part of their

monthly mortgage and their

mortgage servicer pays the county

on the homeowners’ behalf.

1970: Home Purchased

From 1970 to 1977 the

home is taxed based on

its market value.

1978: Proposition 13

Proposition 13 (1978) requires a

home's assessed value to be based

on its purchase price, increased by

up to 2 percent per year for inflation.

Whenever it is sold, it is again taxed

at its purchase price. Proposition 13

also rolled back assessed values to

their 1975 levels.

1985: Bedroom Added

The addition of a bedroom

increases the home's assessed

value to reflect the added market

value of the bedroom but not that

original home.

1988: Transfer to Child

A property transfer typically

triggers a reassessment. However,

Proposition 58 (1986) allows the

home to transfer from the owner to

the child without a reassessment

to market value.

SOLD

SOLD

2005: Home Sold

The home is sold and

reassessed to market value,

significantly increasing the

tax bill.

2008: Decline in Value

The home's market value dips below

its inflation-adjusted purchase price.

Proposition 8 (1978) allows the

home to be temporarily assessed

based on its market value instead.

2014: Recovery

The home's market value

recovers and it is again

taxed at its inflation-adjusted

purchase price.

Market Value

The price the home could be sold for.

Assessed Value

The basis of the property owner's tax bill.

22

LAO California’s Tax System | Property Tax

This graphic shows the value of a hypothetical

home over time to demonstrate how different

transactions and changes to a property affect a

property owner’s tax bill.

THE LIFE OF A HOUSE

23

LAO California’s Tax System | Property Tax

This map shows the property taxes paid per $100,000 of market value for homes in a Los Angeles zip code

in 2015. Property taxes are based on the assessed value, which typically grows more slowly than market

value. Because of this, significant differences arise among property owners solely because they purchased

their properties at different times.

NEIGHBORS OFTEN FACE DIFFERENT TAX BURDENS

Greater Than $800

$600 to $800

$400 to $600

$200 to $400

Less Than $200

Property Taxes Per $100,000

of Market Value

24

LAO California’s Tax System | Property Tax

TWO FACTORS DRIVE FUNDING FOR MUNICIPAL SERVICES

50,000 100,000 150,000 200,000 250,000 $300,000

Marin

San Mateo

Napa

San Francisco

Inyo

Santa Clara

Plumas

San Luis Obispo

Sierra

Placer

Nevada

Colusa

Santa Barbara

Orange

Contra Costa

Sonoma

El Dorado

Alameda

Santa Cruz

San Diego

Amador

Ventura

Monterey

Calaveras

Los Angeles

Tuolumne

San Benito

Mendocino

Mariposa

Yolo

Modoc

Solano

Trinity

Riverside

Glenn

Siskiyou

Lake

Kern

Sacramento

San Bernardino

Shasta

Sutter

Humboldt

San Joaquin

Butte

Lassen

Madera

Stanislaus

Merced

Tehama

Kings

Fres

no

Yuba

Imperial

Tulare

Del Norte

Assessed Value of Property

Municipal Services Schools

While Contra Costa and Orange have

similar property tax bases, Orange has

less available for municipal services.

Property tax funding for municipal services—

such as police, fire, and parks—generally is

higher in counties with higher assessed values.

Municipal services funding also depends on

the share of property tax revenue allocated to

municipal services relative to schools. While

schools’ shares vary across counties, the state

allocates funding to schools to equalize these

differences.

Per Capita Assessed Value, 2016-17

25

LAO California’s Tax System | Property Tax

REVENUE FOR MUNICIPAL SERVICES VARIES WIDELY

Los Angeles

Ventura

San Diego

San Bernardino

Santa Clara

Alameda

Sacramento

Contra

Costa

Kern

San

Francisco

San

Mateo

Monterey

San

Luis

Obispo

Marin

Yolo

Napa

Calaveras

1,000,000

250,000

50,000

Orange

Riverside

Fresno

San

Joaquin

Tulare

Merced

Butte

Shasta

Kings

Inyo

San Benito

Mono

Mariposa

Alpine

Tuolumne

Amador

Sierra

Plumas

Lassen

Modoc

Siskiyou

Glenn

Colusa

Trinity

Del Norte

Tehama

Nevada

North Counties

Los Angeles Area

San Diego Area

Inland Empire

Central Coast

San Joaquin Valley

Sacramento Area

Bay Area

Imperial

Santa

Cruz

Santa

Barbara

Madera

El Dorado

Placer

Stanislaus

Sonoma

Solano

Sutter

Yuba

Lake

Mendocino

Humoldt

Per-Capita Revenue

Less Than $410

$410 - $520

$520 - $640

$640 - $890

Over $890

Population

This graphic shows the per-person property

taxes available within each county in 2015-16

for counties, cities, and special districts. The

amount of funding available in each county

reflects the level of municipal services that

residents can expect to receive from their local

governments.

26

LAO California’s Tax System | Property Tax

Stable—or predictable—revenues allow governments to provide consistent levels of service. The property tax—

the largest single source of local government revenue—is a stable revenue source compared to the personal

income tax, which is the state’s largest single source of revenue.

PROPERTY TAX MORE STABLE THAN PERSONAL INCOME TAX

Annual Percent Change

Governments ideally rely on revenue sources that grow sufficiently to cover any increases in the costs of

providing services. Some argue that the property tax has not grown sufficiently to cover local government costs

since the passage of Proposition 13 in 1978. Others argue property tax revenues have grown substantially

since 1978. Below, we present two ways of measuring property tax revenue growth.

PROPERTY TAX HAS GROWN SINCE PROPOSITION 13

400

800

1,200

1,600

$2,000

1960 1970 1980 1990 2000 2010

1

2

3

4

5

6

7%

1960 1970 1980 1990 2000 2010

Proposition 13 Proposition 13

Per Person Inflation-Adjusted (2015-16) Dollars As Share of California Economy (Personal Income)

-30

-20

-10

10

20

30%

1980 1985 1990 1995 2000 2005 2010 2015

Personal Income Tax

Property Tax

DETERMINE VEHICLE'S VALUE

In the first year a vehicle is owned, its value is roughly the

purchase price. In subsequent years, this value is

depreciated based on the schedule to the right. For this

example, we assume a four year-old car with an initial

purchase price of $30,100.

The car's value in year four is: $30,100 x 70% = $21,070.

DETERMINE VEHICLE'S VALUE

In the first year a vehicle is owned, its value is roughly the

purchase price. In subsequent years, this value is

depreciated based on the schedule to the right. For this

example, we assume a four year-old car with an initial

purchase price of $30,100.

The car's value in year four is: $30,100 x 70% = $21,070.

START

START

TIF

Transportation

Improvement

Fee

Determine the TIF owed.

Find the fee in the chart to

the right that corresponds

to the vehicle value

($21,070) = $50

Apply the 0.65% VLF rate

$21,070 X 0.65 = $137

VLF

Vehicle

License Fee

Total Tax = $187

STOP

Depreciation Schedule

Years Owned

1

2

3

4

5

6

7

8

9

10

11 and After

Depreciation Rate

100

90

80

70

60

50

40

30

25

20

15

%

TIF Schedule

Value of Vehicle

$0 to $5k

$5k to $25k

$25k to $35k

$35k to $60k

Over $60k

Annual Fee

$25

$50

$100

$150

$175

27

LAO California’s Tax System | Property Tax

California levies a variety of charges on vehicles. Two of the

larger ones—the vehicle license fee (VLF) and the transportation

improvement fee (TIF)—effectively are property taxes on vehicles

(but exempt from Proposition 13). Both taxes are levied on the car’s

depreciated value. Revenue from the VLF ($2.6 billion in 2016-17)

goes to cities and counties for health and human services and law

enforcement programs. Revenue from the TIF ($1.5 billion projected in

2018-19) goes to state and local agencies for transportation programs.

PROPERTY TAXES ON VEHICLES

3

28

LAO California’s Tax System | Sales Tax

CHAPTER

29

LAO California’s Tax System | Sales Tax

California’s state and local governments

levy a tax on retail sales of tangible personal

property. This tax—called the sales and use

tax (hereafter, sales tax)—is a significant

source of state and local revenue. In this

chapter, we draw distinctions between the

products that are subject to this tax and those

that are not. We also provide information on

the variation in tax rates across the state and

the distribution of revenue among state and

local programs.

SALES AND

USE TAX

The sales tax is levied on the retail sale of tangible personal property. (“Tangible” refers to physical materials. “Personal

property” is movable from one place to another.) The graphic below compares the amount of taxable sales (spending

on items subject to the sales tax) in 2015 with the amount of taxable sales that would be subject to the tax if not for

exemptions. The icons show major categories of taxable sales and exemptions.

WHAT THE SALES TAX IS

Households and businesses spend money on many services and other items that are not subject to the sales tax,

generally because those items are not tangible personal property. Instead, these items are services (such as a hair

cut), intangible property (such as an e-book), and real property (such as land). For example, a consumer having their

car repaired would pay sales tax on parts like brake pads but would not pay sales tax on the labor associated with the

repair. Spending on these items is several times the size of the sales tax base.

WHAT THE SALES TAX IS NOT

30

LAO California’s Tax System | Sales Tax

Items Not Subject to Sales Tax

Clothing Furniture Vehicles

Personal Care Products Office Supplies Appliances Prepared Foods

Groceries Utilities

Prescription

Medicines

Educational Study Transportation Services

Telecommunications

Medical Services

Maintenance

and Repairs

Housing Personal Care Services

Clothing Furniture Vehicles

Personal Care Products Office Supplies Appliances Prepared Foods

Groceries Utilities

Prescription

Medicines

Educational Study Transportation Services

Telecommunications

Medical Services

Maintenance

and Repairs

Housing Personal Care Services

Exemptions:

$221 Billion

Taxable Sales: $636 Billion

WHERE IS SALES TAX COLLECTED?

31

LAO California’s Tax System | Sales Tax

Share of Statewide Taxable Sales by Business Type, 2015

2 4 6 8 10 12 14%

Other Non-Retail

Businesses

Other Retailers

Food and

Beverage

Stores

Furniture, Home

Furnishings, Electronics,

and Appliance Stores

Building Materials

and Garden Supplies

Rentals, Real Estate,

and Construction

Clothing and

Accessories Stores

Manufacturing

Gasoline Stations

General

Merchandise

Stores

Wholesalers

Bars and

Restaurants

Motor Vehicle

and Parts Dealers

California’s sales tax rates vary across cities and counties, ranging from

7.25 percent to 10.25 percent. These rate differences result from optional

sales taxes levied by local governments. (The minimum rate in the two

regions shown below is 7.75 percent.)

32

LAO California’s Tax System | Sales Tax

IN SOME REGIONS, CONSUMERS

FACE SEVERAL DIFFERENT RATES

Rates as of April 1, 2018

Richmond

Moraga

Pinole

Alameda County

Contra Costa County

Antioch

Concord

Pittsburg

Orinda

Martinez

Hercules

Pleasant Hill

San Pablo

Hayward

Union City

Newark

San Leandro

El Cerrito

Albany

Hawthorne

Orange County

Los Angeles County

La Habra

El Monte

Inglewood

Commerce

Culver City

South El Monte

Long Beach

Compton

Santa Monica

South Gate

Lynwood

Pico Rivera

Westminster

Fountain Valley

Stanton

La Palma

7.75%

8.25

8.75

9.25

9.5

9.75

10.0

10.25

Downey

33

LAO California’s Tax System | Sales Tax

SALES TAX RATES IN CALIFORNIA COUNTIES

Rates as of April 1, 2018

7.0 7.5 8.0 8.5 9.0 9.5 10.0 10.5%

Alpine

Calaveras

Lassen

Modoc

Plumas

Sierra

Sutter

Trinity

Placer

Shasta

Tuolumne

Butte

Tehama

El Dorado

Colusa

Glenn

Siskiyou

Kern

Kings

Yuba

Ventura

Del Norte

San Luis Obispo

Mono

Lake

Amador

Inyo

Mariposa

Napa

San Bernardino

Orange

San Diego

Nevada

San Benito

Sacramento

Yolo

Madera

Imperial

Santa Barbara

Fresno

Merced

Stanislaus

Humboldt

Riverside

Mendocino

Tulare

Solano

Sonoma

San Joaquin

San Francisco

Marin

Contra Costa

Monterey

Santa C

ruz

San Mateo

Santa Clara

Alameda

Los Angeles

Legend

Minimum Maximum

Population-Weighted

Average

10

20

30

40%

Below 7.75 7.75 7.75-9.5 9.5 Above 9.5%

Half of Californians Live Where Rate Is 7.75% or 9.5%

Percent of Population as of January 1, 2017

5

34

LAO California’s Tax System | Sales Tax

This graphic shows how sales and use tax revenues were distributed to the state,

state-funded local programs, and local governments in 2016-17.

DISTRIBUTION OF SALES TAX REVENUE

Behavioral health programs and child welfare services:

$3.6 Billion

Law enforcement activities:

$2 Billion

Mental health programs: $1.1 Billion

Social services programs:

$1.9 Billion

Cash assistance to participants

in the state's welfare-to-work program:

$1.2 Billion

Other programs:

$100 Million

Transactions

and Use Taxes:

$6.3 Billion

2011 Realignment: $6.7 Billion

Transportation programs:

$5.2 Billion

Other:

$1.1 Billion

Total sales and use tax revenue:

$53 Billion

State General Fund: $24.9 Billion

The General Fund—the state's main

operating account—provides funding

primarily for education, health and social

services, and criminal justice programs.

Bradley-Burns

Transportation:

$1.7 Billion

Local Public Safety:

$3.3 Billion

Bradley-Burns

General Purpose:

$6.6 Billion

General funding for city

and county programs.

1991 Realignment:

$3.2 Billion

35

LAO California’s Tax System | Sales Tax

2015-16

PER CAPITA SALES TAX COLLECTIONS BY COUNTY

INYO

KERN

SAN

BERNARDINO

SISKIYOU

FRESNO

LASSEN

RIVERSIDE

MODOC

TULARE

SHASTA

MONO

TRINITY

IMPERIAL

TEHAMA

SAN DIEGO

PLUMAS

MONTEREY

BUTTE

LAKE

LOS

ANGELES

MADERA

MERCED

KINGS

TUOLUMNE

GLENN

PLACER

YOLO

EL

DORADO

COLUSA

SIERRA

HUMBOLDT

MENDOCINO

SONOMA

SAN LUIS

OBISPO

VENTURA

NAPA

SANTA

BARBARA

MARIPOSA

NEVADA

YUBA

STANISLAUS

SAN

BENITO

SOLANO

ALPINE

SAN

JOAQUIN

DEL NORTE

SANTA

CLARA

MARIN

CALAVERAS

ALAMEDA

ORANGE

SUTTER

SACRAMENTO

AMADOR

CONTRA

COSTA

SAN MATEO

SANTA

CRUZ

SAN

FRANCISCO

8

13

19

8

10

Less Than $700

$700-1000

$1001-$1225

$1226-$1400

Over $1400

$433

$297

$338

$1,890

$1,834

$5,462

Sales and

Use Tax

Property

Tax

Personal

Income Tax

Number of Counties in Each Group

Range of Per Capita Tax Collections by County

For Major California Taxes

Excludes Alpine and Mono Counties

36

LAO California’s Tax System | Sales Tax

SALES TAX GROWTH SLOWER

THAN PROPERTY AND INCOME TAXES

Total Percent Change, 2015-16 Dollars

100

200

300

400%

1980-81 1990-91 2000-01 2010-11

Sales and Use Tax

Personal Income Tax

Property Tax

60%

50

40

30

20

1980 1990 2000 2010

One Reason: Taxable Sales Have Shrunk

as a Share of the Economy...

Taxable Sales as Share of Personal Income

300%

250

200

150

100

50

1980 1990 2000 2010

...Because Prices of Goods Have Grown

More Slowly Than Prices of Services

Total Percent Change

Prices of Services

Prices of Goods

2015-16

37

LAO California’s Tax System | Sales Tax

4

CHAPTER

38

LAO California’s Tax System | Other Taxes

39

LAO California’s Tax System | Other Taxes

Beyond the three main taxes covered earlier in this report, the

state and local governments levy a variety of smaller taxes

that collectively sum to just over 10 percent of all tax revenue

collected in the state. These include taxes on corporations,

tobacco, alcohol, diesel and gasoline, insurance, and hotels.

(Tobacco, alcohol, and fuels are also subject to the sales tax

covered in Chapter 3.)

OTHER TAXES

Manufacturing

Retail

Holding

Companies

Financial

Agriculture

and Mining

Construction

Professional,

Scientific, and

Technical Services

Hospitality

and Food

Services

Other

Services

Real Estate

Communication,

Transportation,

and Utilities

100k

50k

10k

5

10

15

20

25%

10 15 20 25%

Percent of Total California Corporate Income

Percent of Total Tax Liability

No Net Income

or Net Loss

Less Than

$1 Million

$1 Million to

$10 Million

$10 Million

or More

40.1%

57.9%

1.8%

0.2%

21.0%

19.7%

59.3%

2.8%

12.4%

13.5%

71.3%

Share of Tax Returns Share of Positive Corporate Income Share of Tax Liability

Number of Taxpayers

Companies in these four

industries make up 24%

of corporate taxpayers but

pay 68% of the tax.

A relatively large number of

corporations in this industry

had no net income or a net loss.

40

LAO California’s Tax System | Other Taxes

California levies a tax on net corporate income. For most corporations,

the tax rate is 8.84 percent. California only taxes the portion of income

that was earned in California.

WHO PAYS CORPORATION TAX?

2 Percent of Corporate Taxpayers Pay 85 Percent of the Tax

Tax Statistics by Income Group, 2015

Manufacturing

Retail

Holding

Companies

Financial

Agriculture

and Mining

Construction

Professional,

Scientific, and

Technical Services

Hospitality

and Food

Services

Other

Services

Real Estate

Communication,

Transportation,

and Utilities

100k

50k

10k

5

10

15

20

25%

10 15 20 25%

Percent of Total California Corporate Income

Percent of Total Tax Liability

No Net Income

or Net Loss

Less Than

$1 Million

$1 Million to

$10 Million

$10 Million

or More

40.1%

57.9%

1.8%

0.2%

21.0%

19.7%

59.3%

2.8%

12.4%

13.5%

71.3%

Share of Tax Returns Share of Positive Corporate Income Share of Tax Liability

Number of Taxpayers

Companies in these four

industries make up 24%

of corporate taxpayers but

pay 68% of the tax.

A relatively large number of

corporations in this industry

had no net income or a net loss.

2015

Net corporate income is all revenues less most of the costs of doing business. These deductions

may include the cost of raw materials, rent, interest payments, and employee compensation.

Many companies have more deductions than their gross revenue, resulting in a net loss.

41

LAO California’s Tax System | Other Taxes

Corporations may apply a credit against their taxes for investing money in ways that further

certain policy goals. In the figure below, the darker, inner pie shows a breakdown of credits in

2015. The lighter, outer segments show the distribution of the two largest credits among various

types of corporations.

CORPORATION TAX CREDITS BY INDUSTRY

-20

-10

10

20

30%

1998 2003 2008 2013

Research and

Development

$1.3 Billion

Enterprise Zones

$450 Million

Electrical and

Electronic Equipment

Pharmaceuticals

Food Products

Chemicals

Other

Manufacturing

Information

Sector

Other

Industrial Sectors

Motion Picture $53 Million

Low-Income Housing $36 Million

Other $57 Million

Transportation and Utilities

Professions and Technical

Finance

Holding Companies

Manufacturing

Other

Retail

The state began phasing out

enterprise zone credits in 2013.

Corporate Profits

Gross State Product

Corporate Profits More Volatile Than State Economy

Annual Percent Change

2015

-20

-10

10

20

30%

1998 2003 2008 2013

Research and

Development

$1.3 Billion

Enterprise Zones

$450 Million

Electrical and

Electronic Equipment

Pharmaceuticals

Food Products

Chemicals

Other

Manufacturing

Information

Sector

Other

Industrial Sectors

Motion Picture $53 Million

Low-Income Housing $36 Million

Other $57 Million

Transportation and Utilities

Professions and Technical

Finance

Holding Companies

Manufacturing

Other

Retail

The state began phasing out

enterprise zone credits in 2013.

Corporate Profits

Gross State Product

42

LAO California’s Tax System | Other Taxes

FUEL TAXES

California levies several taxes that specifically apply to transportation fuel. These taxes include

gasoline and diesel excise taxes, which are collected from distributors when they remove the fuel

from terminals or refineries. They also include diesel sales taxes, which are collected at the point of

retail sale, just like other sales taxes.

Fuel Taxes Raise About $9 Billion Annually

2018-19 Projections

$0.8

Billion

$1.2

Billion

$7.1

Billion

Diesel

Sales Tax

Diesel

Excise Tax

Gasoline

Excise Tax

Diesel

Over 18 Billion Gallons of Fuel Sold Annually

2018-19 Projections

2.8 Billion

Gallons

Gasoline

15.8 Billion Gallons

Over Half of Fuel Tax Revenues Spent on State Highways

2018-19 Projections

Other

Public

Transportation

Local Streets

and Roads

State Highways

43

LAO California’s Tax System | Other Taxes

INSURANCE TAX

Personal Auto

$25 Billion

Commercial Auto

$3 Billion

Marine

$3 Billion

Workers'

Compensation

$13 Billion

Earthquake

$1 Billion

Fire

$948 Million

Mortgage Guarantee

$459 Million

Medical Professional Liability

$450 Million

Other

$12 Billion

Life

$16 Billion

Annuity

$24 Billion

Accident and Health

$16 Billion

Other

$12 Billion

Title Insurers

Property and Casualty

Life Insurers

Homeowners

$8 Billion

$2 Billion

Insurance Tax Generates $2.3 Billion Trends in Insurance Tax Base

$1,518

Million

$802

Million

Property &

Casualty

Life

$1 Million

Ocean

Marine

$13 Million

Title

20

40

60

$80

1991 1996 2001 2006 2011 2016

Special rules apply

to title and ocean

marine insurers

Life

Property & Casualty

Title

Annual Premiums, In Billions State General Fund, 2016

The state levies a 2.35 percent tax on insurance premiums. Insurance companies pay the insurance

tax instead of the corporate income tax.

Insurance Tax Base: $137 Billion in Premiums

2016

44

LAO California’s Tax System | Other Taxes

ALCOHOLIC BEVERAGE TAX

$198 Million

$136 Million

$26 Million

$4 Million

Beer

Wine

50

100

150

200

250

300

1960 1970 1980 1990 2000 2010

Spirits

Alcohol Consumption Trends

Annual Drinks Per Capita

The state levies an excise tax on alcoholic beverages. The tax is levied on distributors (such as

wholesalers) based on the volume and type of beverage sold. Revenue from this tax is deposited into

the state General Fund, which provides funding primarily for education, health and social services, and

criminal justice programs. Revenues from the tax totaled $363 million in 2015-16.

45

LAO California’s Tax System | Other Taxes

The state levies excise taxes on tobacco products. The taxes are levied on distributors (such as

wholesalers). The tobacco tax is levied on cigarettes on a per-cigarette basis. Currently, the tax rate is

equivalent to $2.87 per pack. The tobacco tax on other tobacco products—such as chewing tobacco

and electronic cigarettes—is levied as a percent of the wholesale price. The current rate is equivalent to

$3.37 per pack of cigarettes.

TOBACCO TAXES

Breakdown of Tobacco Tax Rates and Spending

$2

$.50

$2

$0.87

$.50

Cigarettes

Other Tobacco Products

$0.25

Proposition 56 rate:

Medi-Cal and various other purposes

Proposition 10 rate: early childhood development programs

$0.02 for breast cancer research

Proposition 99 rate: tobacco-related programs,

other health programs, environmental protection,

and recreational purposes

$0.10 deposited into state General Fund

0.5

1.0

1.5

2.0

$2.5

1959-60 1979-80 1999-00

50

100

150

1959-60 1979-80 1999-00

Tobacco Tax Revenues Have Increased

Due to Rate Increases

2018-19 Dollars, In Billions

Annual Per Capita Consumption of Cigarettes

Has Decreased Dramatically

Packs Per Year

Legislative Increase

Proposition 99

Proposition 10

Proposition 56

2017-182018-19

46

LAO California’s Tax System | Other Taxes

HOTEL TAXES

10 20 30 40 50 60 70%

Mammoth Lakes

Yountville

Calistoga

Solvang

Avalon

Pismo Beach

Angels

Anaheim

Indian Wells

Big Bear Lake

Rancho Mirage

Burlingame

South Lake Tahoe

Bishop

Half Moon Bay

Ojai

Monterey

Dana Point

Morro Bay

Goleta

Millbrae

Fort Bragg

West Hollywood

Crescent City

Palm Springs

Carmel-by-the-Sea

Plymouth

Carpinteria

Westlake Village

Coronado

Pacific Grove

Point Arena

Needles

Sonoma

Palm Desert

Napa

Healdsburg

Garden Grove

Buell

ton

San Diego

San Francisco

Los Angeles

San Jose

Statewide Average

Hotel taxes make up

more than 25 percent

of general purpose

tax revenues in 39 cities.

By contrast, hotel tax

revenues in these four

cities make up a lower

share of city budgets,

but make up about

40 percent of all hotel

taxes collected in the state.

1

2

$3

2002-03 2015-16

Hotel Tax Revenues Have Doubled Since Great Recession

2015-16 Dollars, In Billions

Most Hotel Spending Is Where Rate is 10% or 14%

In Billions, 2015-16

1

2

3

4

5

6

7

$8

<7% 7-8 8-9 9-10 10-11 11-12 12-13 13-14 14-15 >15%

Cities

Counties

Transient occupancy taxes are imposed on stays at hotels, motels, and similar accommodations. As such, the

tax typically is paid by visitors from outside of the city or county in which the tax is levied. While some cities

rely heavily on the hotel tax, statewide the tax makes up less than 10 percent of city tax revenues.

Hotel Taxes as a Share of Total Tax Revenues

47

LAO California’s Tax System

GENERAL RESOURCES

LAO Economy & Taxes Blog (www.lao.ca.gov/LAOEconTax) and Twitter (@LAOEconTax)

PERSONAL INCOME TAX

Volatility of the Personal Income Tax Base (Report)

Volatility of California’s Personal Income Tax Structure (Report)

PROPERTY TAX

Understanding California’s Property Taxes (Report)

Understanding Your Property Tax Bill (Blog Series)

Calculating Your 1 Percent Tax (Video)

The 1 Percent Tax—Where Does Your Money Go? (Video)

Common Claims About Proposition 13 (Report)

The Property Tax Inheritance Exclusion (Report)

SALES AND USE TAX

Understanding California’s Sales Tax (Report)

Why Have Sales Taxes Grown Slower Than the Economy (Report)

TAX EXPENDITURES

Review of the California Competes Tax Credit (Report)

California’s First Film Tax Credit Program (Report)

Community Development Financial Institution Tax Credit (Report)

Options for Modifying the State Child Care Tax Credit (Report)

ADDITIONAL LAO RESOURCES

48

LAO California’s Tax System

This report was prepared by Ryan Miller and Vu Chu, with assistance from Carolyn Chu, Justin Garosi,

Seth Kerstein, Brian Uhler, and Brian Weatherford. The Legislative Analyst’s Office (LAO) is a nonpartisan

office that provides fiscal and policy information and advice to the Legislature. This report and others, as

well as an e-mail subscription service, are available on the LAO’s website at www.lao.ca.gov.

LAO PUBLICATIONS