1620 Eye Street, NW, Suite 200 | Washington, DC 20006 | (202) 387-6121 | ConsumerFed.org

The One Hundred Percent Penalty:

How Auto Insurers’ Use of Credit Information

Increases Premiums for Safe Drivers and Perpetuates

Racial Inequality

Douglas Heller

Director of Insurance

Michael DeLong

Research and Advocacy Associate

July 31, 2023

The Credit Score Penalty in Auto Insurance Premiums | CFA 2

Executive Summary

Auto insurance must, by law, be purchased by drivers in every state except New

Hampshire. Therefore, policymakers and regulators have a special responsibility to ensure that

coverage is available and affordable and that consumers do not experience unfair discrimination.

Since the 1990s, auto insurance companies have used consumer credit information as a factor in

setting insurance premiums. The use of credit information in insurance pricing results in

significant differences in the cost of auto insurance, even when comparing otherwise similar

customers with clean driving records and no history of claims. For consumers with fair and poor

credit, insurance premiums are often unaffordable due to the heavy emphasis most insurers place

on the reported credit history of their customers.

This study focuses on the impact of the use of credit on the prices charged to Americans

with safe driving histories. While Consumer Federation of America (CFA) maintains that the

results of our evaluation of the pricing data should lead to legislative and regulatory reform of

the auto insurance industry, the central finding of the report lies with the numbers themselves.

Namely:

• American consumers with clean driving records and excellent credit pay an average

annual auto insurance premium of $470 for state-mandated coverages. If those same

consumers instead have fair credit, their average premium increases to $701, even if

their driving records are perfect. Good drivers with poor credit face even higher

premiums, averaging $1,012 for basic coverage across the country.

• In percentage terms, consumers with fair credit pay premiums that average 49% higher

than the premiums paid by consumers with excellent credit. Consumers with poor credit

pay 115% more than consumers with excellent credit and 44% more than those with

fair credit.

• As credit impacts are generally uniform statewide but in-state territorial rates vary

widely, often by ZIP code or census tract, drivers with fair and poor credit in higher

priced urban communities face minimum limits insurance premiums that are often more

than a thousand dollars higher than their neighbors with excellent credit.

Because credit history correlates to race and income, raising premiums on drivers with lower

credit disproportionately harms low-income consumers and people of color. In our conclusion,

we argue that state policymakers should prohibit insurers from using credit information in setting

auto insurance rates as California, Hawaii, and Massachusetts do currently. This ban, however,

must be accompanied by additional protections that test for and minimize unfair discrimination

to ensure that the disparities driven by the use of credit are not maintained by the replacement of

credit information with other underwriting and pricing tools that lead to similar results.

The Credit Score Penalty in Auto Insurance Premiums | CFA 3

I. Introduction

Mandatory auto insurance is intended to ensure that drivers can take financial

responsibility for the bodily injury and property damage that results from traffic collisions. In

2022, the American auto insurance market’s size totaled $270 billion.

1

Individual policyholders’

auto insurance premiums depend upon a variety of factors that differ from state to state and from

company to company such that customer premiums vary widely from the average premiums

found in the market.

While most Americans believe that their driving record and annual mileage are—and

should be—the primary determinants of the premium they are charged, companies use several

other factors for determining the premium different customers pay. Firms often explain their

pricing strategy as “risk segmentation,”

2

but several of the factors in their premium-setting

algorithms do not relate at all to their driving and, instead, reflect customers’ socio-economic

status. Most drivers are unaware these social status factors are used for pricing their policies;

according to one survey, 66% of Americans are unaware that credit information is used in

calculating auto insurance rates.

3

When made aware of the use of these non-driving factors, a

substantial majority believe that it is unfair for insurance companies to use socio-economic

factors in setting auto insurance rates, according to surveys of the public.

4

,

5

Among those factors

having the largest impact on price are where a driver lives (typically based on their ZIP code or,

more recently, census tract) and their credit history, which is incorporated into their premium by

means of a “credit-based insurance score.” These scores are often provided by the same credit

reporting agencies that create the credit scores used by banks and other lenders for underwriting

loans.

Insurers’ use of both territory and credit information contribute to the disproportionately

high premiums faced by communities of color. While this study focuses on the impact of the use

of credit, we will make note of the cumulative pressure that the interaction of credit information

1

“Property/Casualty Market Share report.” National Association of Insurance Commissioners. March 1, 2023.

Available at https://content.naic.org/sites/default/files/research-actuarial-property-casualty-market-share.pdf.

2

Insurance industry vendor Verisk, for example, presents marketing material to help insurers “Refine your personal

auto risk segmentation with granular data and advanced analytics.”

https://www.verisk.com/siteassets/media/downloads/predictive-analytics/iso-risk-analyzer-personal-auto.pdf

3

“Credit Scores and Car Insurance: How Unfair Pricing Practices Discriminate Against Millions of Drivers.” Root

Inc. Available at

https://cdn.brandfolder.io/5S4BNCY2/as/7m788tfps556f7fzm4q5gj/RootInc_DroptheScore_ConsumerReport.pdf.

4

“Major Auto Insurers Raise Rates Based on Economic Factors: Low-and-Moderate Income Drivers Charged

Higher Premiums.” By Douglas Heller and Michelle Styczynski. June 2016. Available at

https://consumerfed.org/wp-content/uploads/2016/06/6-27-16-Auto-Insurance-and-Economic-Status_Report.pdf.

5

“Which Data Fairly Differentiate? American Views on the Use of Personal Data in Two Market Settings.” By

Barbara Kiviat. Sociological Science. January 13, 2021. Available at https://sociologicalscience.com/articles-v8-2-

26/.

The Credit Score Penalty in Auto Insurance Premiums | CFA 4

and territory places on many low-income drivers and people of color and how that interaction

reinforces and amplifies structural racism in the United States.

For decades the auto insurance market has been opaque and lacking in transparency.

6

In

order to investigate the impact of certain aspects of pricing algorithms, in fall 2020 CFA

purchased data from Quadrant Information Services, LLC for auto insurance premiums charged

by many of the largest auto insurers in every ZIP code in the United States. CFA analyzed these

data and found that the use of credit information in auto insurance pricing has an enormous

impact on the premium charged to otherwise similar drivers with clean driving records. In this

report we detail the results of a comparison of premiums charged to drivers with “excellent,”

“fair,” and “poor” credit-based insurance scores. The report concludes with suggestions for

reforming the auto insurance market in response to the problems created by the use and

significant impact of credit information in pricing.

II. Background

Every state except New Hampshire requires drivers to purchase auto insurance that

provides liability protection in case someone is injured or killed in a crash or there is property

damage arising from the incident.

7

Therefore, state governors, legislators, and regulators have a

responsibility to ensure that this government mandated product is available to residents,

affordable, and that drivers are not subject to unfair discrimination.

The national average annual expenditure on auto insurance in 2020

8

was $1,047,

according to the most recent National Association of Insurance Commissioner (NAIC) report on

auto insurance costs.

9

Residents of ten states faced an average annual expenditure of more than

$1,362, according to the NAIC.

10

These costs impose significant monthly expenses on many

consumers and make compliance with state coverage requirements difficult for millions of

drivers, who either suffer the economic consequences of not being allowed to drive or who opt to

drive uninsured and risk legal consequences in order to get to work, run errands, get children to

school, and generally get around. While states strictly regulate consumer behavior and enforce

6

A notable exception is the California insurance market, which is governed by a consumer protection law that

requires public access to all aspects of insurance ratemaking and premium setting.

7

Some states allow vehicle owners to meet the financial responsibility requirements by other means (including

surety bonds or certificates of deposit, for example) and certain states require that motorists maintain first-party

personal injury protection (no-fault) coverage in addition to or rather than coverage to pay the costs of associated

with another person’s injuries.

8

Large rate increases by major insurers in 2021 and, particularly, 2022 and 2023, make it reasonable to assume that

the 2020 averages – which were lowered modestly by insurance refunds provided early in the pandemic --understate

the actual prices charged to consumers in 2023.

9

NAIC, 2023. “2019/2020 Auto Insurance Database Report.” Table 4. These are the most recent data available from

NAIC.

10

These states are Delaware, District of Columbia, Florida, Georgia, Louisiana, Michigan, Nevada, New Jersey,

New York, and Rhode Island.

The Credit Score Penalty in Auto Insurance Premiums | CFA 5

the purchase of auto insurance through hefty fines, impounded cars, and even jail time, states

have done little to address affordability, including curbing the use of pricing models that increase

costs for consumers because of imperfect credit histories and other characteristics not related to

the driving safety of policyholders.

Three states—California, Hawaii, and Massachusetts—prohibit credit information from

being used in auto insurance pricing; the other 47 states and the District of Columbia allow its

use, with very few limitations.

11

Most consumers are aware that information related to their credit history is collected by

credit bureaus (Equifax, Experian, and TransUnion) and converted to a credit score (e.g., FICO

Score and Vantage Score). Or, at least, they are aware that they have something called a credit

score that will determine whether or not they can get a loan and how much interest they might

have to pay. Credit-based scores, which were originally developed to determine someone’s

creditworthiness, have become tools for other purposes as well, including landlords evaluating

prospective tenants, employers assessing job candidates, and various uses by insurance

companies. The scores have also received public policy attention over the years for a range of

concerns, including issues with accuracy,

12

lack of transparency,

13

and creating substantial

financial burdens for lower-income people and people of color.

14

With the growing use of credit scores has also come more scrutiny of the accuracy of the

consumer credit reports that underlie the scoring. A 2012 Federal Trade Commission (FTC)

study found that a quarter of consumers identified at least one error on their credit reports, with

five percent of consumers finding errors on their credit reports that were costing them at least 25

points on their credit score.

15

A 2021 Consumer Financial Protection Bureau (CFPB) report

11

In late 2020 and early 2021 Nevada and Washington State enacted regulations temporarily banning the use of

credit information during the COVID-19 pandemic. Nevada’s regulation was upheld by the state’s Supreme Court

and will expire in 2024; the Washington regulation was struck down by a state court.

12

“A Broken System: How the Credit Reporting System Fails Consumers and What to Do About It.” By Syed Ejaz.

Consumer Reports. June 10, 2021. Available at https://advocacy.consumerreports.org/wp-

content/uploads/2021/06/A-Broken-System-How-the-Credit-Reporting-System-Fails-Consumers-and-What-to-Do-

About-It.pdf.

13

“Equifax, TransUnion, Experian Have Spent Decades Avoiding Transparency, Regulation.” By Teresa Dixon

Murray. The Cleveland Plain Dealer. October 6, 2017. Available at

https://www.cleveland.com/business/2017/10/equifax_transunion_experian_ha_1.html.

14

Ratcliffe, C. and Brown, S., November 2017. Credit scores perpetuate racial disparities, even in America’s most

prosperous cities. Urban Institute. Retrieved from https://www.urban.org/urban-wire/credit-scores-perpetuate-racial-

disparities-even-americas-most-prosperous-cities See also, Leonhardt, M., January 28, 2021. Black and Hispanic

Americans often have lower credit scores—here’s why they’re hit harder. CNBC. Retrieved from

https://www.cnbc.com/2021/01/28/black-and-hispanic-americans-often-have-lower-credit-scores.html ; Cornfield, J.

September 19, 2018. “Low-Income Americans Get Double Squeeze from Poor Credit and High Fees.” CNBC.

Retrieved from https://www.cnbc.com/2018/09/19/poor-credit-keeps-low-income-people-paying-higher-fees-and-

stiff-interest-rates.html.

15

“In FTC Study, Five Percent of Consumers Had Errors on Their Credit Reports That Could Result in Less

Favorable Terms for Loans.” Federal Trade Commission. February 11, 2013. Available at

The Credit Score Penalty in Auto Insurance Premiums | CFA 6

found that residents of majority African American and Hispanic neighborhoods had significantly

more incidence of disputed items on their credit reports than residents of majority white

neighborhoods.

16

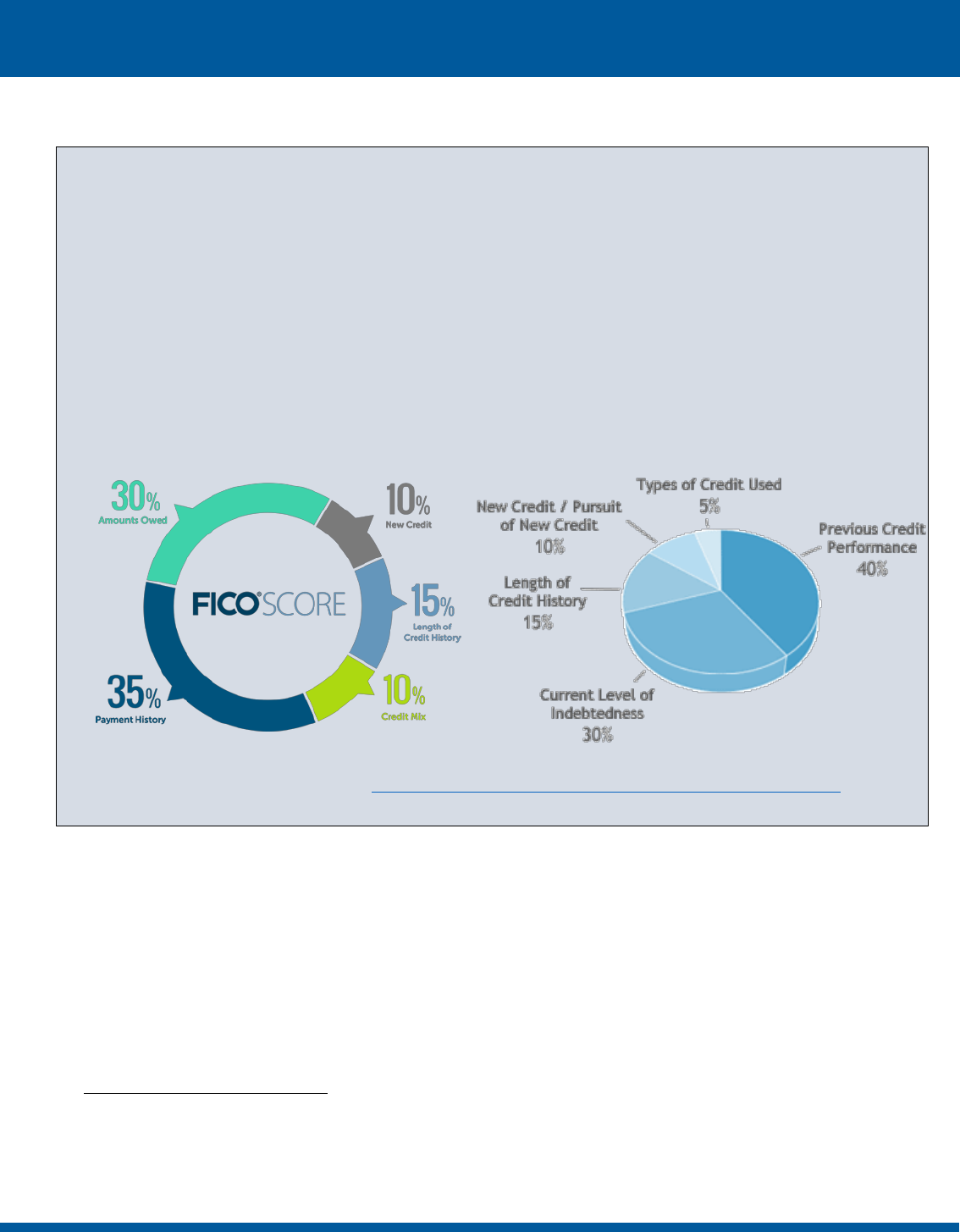

The exact formulas for calculating a credit score are proprietary, but FICO has released

the following information about the elements from which a credit score is calculated:

17

• Payment history (35%)—the presence or lack of derogatory information, such as late

payments, bankruptcy, liens, settlements, judgments, repossessions, foreclosures;

• Debt burden/amounts owed (30%)—debt specific measurements like debt-to-limit

ratio, number of accounts with balances, amount owed across different kinds of

accounts, amount paid on installment loans;

• Length of credit history (15%)—average age of the accounts in a credit report, and

the age of the oldest account;

• Types of credit (10%)—consumer finance, mortgage, installment, credit cards, etc.;

and

• New credit and recent searches for credit (10%)—hard credit inquiries or “pulls.”

For insurance underwriting and rating, companies use “credit-based insurance scores,”

which are ratings based in whole or in part on a consumer’s credit information. As the charts

below indicate, these credit-based insurance scores are built using algorithms very similar to

those crafted for credit scores, though the score vendors generally keep the details of these

models confidential as well.

https://www.ftc.gov/news-events/press-releases/2013/02/ftc-study-five-percent-consumers-had-errors-their-credit-

reports.

16

“Disputes on Consumer Credit Reports.” Consumer Financial Protection Bureau. October 2021. Available at

https://files.consumerfinance.gov/f/documents/cfpb_disputes-on-consumer-credit-reports_report_2021-11.pdf.

17

“What’s In My FICO Scores?” FICO.com. Accessed on November 1, 2022. Available at

https://www.myfico.com/credit-education/whats-in-your-credit-score.

The Credit Score Penalty in Auto Insurance Premiums | CFA 7

III. Measuring the Impact of Credit Information and Auto

Insurance Premiums

Using auto insurance premium data from August 2020 for ten large insurers in every ZIP

code in the United States,

18

CFA found that in all states plus the District of Columbia that allow

the use of credit-based insurance scores, consumers pay significantly higher auto insurance

premiums if they have fair or poor credit, even if their driving records are perfect, than those

18

The data, purchased by CFA from Quadrant Information Services, used insurers’ rate plans filed with each state to

calculate the premium for a 35-year-old unmarried driver with no accidents, moving violations, license suspensions,

or lapses in coverage, and who has a high school diploma and rents their home. They drive a 2011 Honda Civic LX

and have a 12-mile commute, five days a week, for 12,000 miles driven annually. Finally, the drivers purchase the

state minimum insurance coverage. The companies reviewed vary by state in order to include several of the largest

carriers in each state.

Credit Scores vs. Credit-based Insurance Scores

Insurers distinguish between credit scores and credit-based insurance scores, claiming that the latter

assess insurance risk rather than credit risk. However, as Figures 1 and 2 illustrate, the components of

the FICO* Credit Score model and the FICO Insurance Score model are virtually identical, with only

slightly less emphasis on “Types of Credit/Credit Mix” and slightly more emphasis on “Previous Credit

Performance/Payment History” in the insurance score model. Despite small differences, the insurance

scores and credit scores are closely related. For the purpose of this report, credit scores and credit-based

insurance scores are considered equivalent, as the differences are nominal.

*

FICO is one of several firms that provide credit-based insurance scores to insurers.

Figure 1. Components of a FICO Credit Score Figure 2. Components of a FICO Insurance Score

FICO Credit Score chart was retrieved from https://www.myfico.com/credit-education/whats-in-your-credit-score

FICO Insurance Score chart was retrieved from https://insurancescores.fico.com/InScore

The Credit Score Penalty in Auto Insurance Premiums | CFA 8

who have excellent credit. As shown in Figure 4, American consumers with excellent credit pay

an average annual countrywide premium of $470. But if those very same consumers instead have

fair credit, their average premium increases to $701, even if their driving records are perfect. If

those customers have poor credit, their average premium rises further, to $1,012, or more than

double what is charged to customers with the same driving history but excellent credit.

The use of the terms excellent, fair, and poor credit are imprecise and will vary in

meaning based on the particular credit-based insurance score model used by each company

(some of which, for example, do not follow a 300-850 point scale). For our analysis, Figure 3

provides a rough guideline of what each category represents within the structure of a standard

300-850 scale.

Figure 3: Definitions of Credit-Based Insurance Scores

Excellent Credit-Based Insurance Score

Approximately 823 and above

Fair Credit-Based Insurance Score

Approximately 710-740

Poor Credit-Based Insurance Score

Approximately 524-577

Figure 4. Average Premium Nationwide by Credit History

Figures 5 and 6 below present the weighted average premiums for basic (minimum

limits) auto insurance coverage from 10 large auto insurers and the percentage change by score,

respectively, in each state.

19

,

20

These are the premiums offered to drivers with spotless driving

records and other characteristics held constant.

19

The average statewide premium data are weighted in each state based on the statewide market share of each

company in our database.

20

A minimum limits auto insurance policy is the amount of coverage required by the state to be legally insured. The

minimum coverage amounts vary by state, but all states require property damage liability insurance, which pays for

any injuries or damages a consumer causes in an accident. Every state except Florida requires bodily injury liability

insurance, which pays for the medical costs for someone if a consumer causes a car accident. A number of states

$470

$701

$1,012

Excellent Credit

Safe Driver

Fair Credit

Poor Credit

Safe Driver

Safe Driver

The Credit Score Penalty in Auto Insurance Premiums | CFA 9

Figure 5: Average State Auto Insurance Premiums by Credit Information

State

Premiums for

Consumers with

Excellent Credit

Premiums for

Consumers with

Fair Credit

Premiums for

Consumers with

Poor Credit

Alabama

$392

$625

$1,003

Alaska

$333

$455

$632

Arizona

$460

$714

$1,138

Arkansas

$340

$495

$678

California

$590

$590

$590

Colorado

$588

$786

$1,028

Connecticut

$653

$977

$1,351

Delaware

$773

$1,154

$1,695

District of

Columbia

$557

$854

$1,306

Florida

$822

$1,346

$2,000

Georgia

$535

$789

$1,047

Hawaii

$368

$368

$368

Idaho

$310

$444

$608

Illinois

$424

$607

$915

Indiana

$362

$531

$738

Iowa

$236

$386

$663

Kansas

$373

$570

$812

Kentucky

$555

$916

$1,451

Louisiana

$713

$1,093

$1,505

Maine

$282

$471

$755

Maryland

$805

$1,116

$1,422

Massachusetts

$451

$451

$451

Michigan

$734

$1,439

$2,667

Minnesota

$560

$960

$1,522

Mississippi

$356

$535

$755

Missouri

$472

$743

$1,095

Montana

$342

$487

$672

Nebraska

$296

$530

$911

Nevada

$667

$960

$1,267

New Hampshire

$343

$492

$682

New Jersey

$660

$1,087

$1,663

New Mexico

$412

$560

$733

New York

$730

$1,148

$2,097

North Carolina

$398

$525

$698

also require uninsured/underinsured motorist insurance, which protects consumers if they are in an accident with

someone who lacks insurance or is underinsured. Finally, several states, including Florida, require personal injury

protection insurance, which covers medical expense regardless of who is at fault.

The Credit Score Penalty in Auto Insurance Premiums | CFA 10

94%

112%

0%

100%

107%

152%

134%

77%

AK – 90%

HI - 0%

97%

90%

96%

72%

107%

75%

148%

78%

136%

117%

208%

117%

126%

78%

172%

181%

132%

100%

111%

154%

116%

104%

105%

263%

162%

93%

112%

156%

96%

143%

75%

90%

113%

187%

112%

98%

168%

120%

99%

North Dakota

$361

$599

$851

Ohio

$310

$462

$635

Oklahoma

$388

$538

$692

Oregon

$600

$911

$1,271

Pennsylvania

$377

$550

$805

Rhode Island

$789

$1,167

$1,580

South Carolina

$519

$775

$1,103

South Dakota

$264

$403

$573

Tennessee

$329

$475

$635

Texas

$399

$641

$904

Utah

$564

$813

$1,167

Vermont

$362

$567

$796

Virginia

$378

$544

$718

Washington

$397

$572

$768

West Virginia

$448

$636

$889

Wisconsin

$347

$542

$881

Wyoming

$255

$340

$438

National Average

$470

$701

$1,012

California, Hawaii, and Massachusetts ban the use of credit information in auto insurance pricing, so premiums are

the same for good drivers irrespective of credit status and the data are not included in our national average. Nevada

has a temporary, pandemic-related ban on credit penalties, but these data pre-date the implementation of that rule.

Figure 6: Premium Increase for Safe Drivers with Poor Credit Compared to Safe Drivers

with Excellent Credit, by State

The Credit Score Penalty in Auto Insurance Premiums | CFA 11

Similar results are apparent in every state that allows credit information to be used—auto

insurers severely penalize safe drivers who have poor credit. People in some states face more

credit-driven disparities than others; the price hikes are especially severe in Florida (where

people with poor credit pay 143% higher average premium), Minnesota (172% higher average

premium), and Michigan (263% higher average premium).

Translated into percentages for the entire United States, if drivers have a perfect driving

record (with no tickets, car crashes, or insurance claims) but fair credit, auto insurers charge

them premiums that are 49% higher, solely because they don’t have an excellent credit history. If

consumers have poor credit, their premiums rise 44% over the premiums paid by their fair credit

peers. Drivers with a perfect driving record but poor credit face 115% higher auto insurance

premiums than those with excellent credit, exclusively because of their credit-based insurance

score.

The overwhelming majority of auto insurers practice this price discrimination and charge

consumers more based on their credit information; however, some companies place greater

emphasis on credit data than others. Figure 7 below shows a number of the largest insurers in the

United States and the average premiums they charge in the states for which CFA reviewed their

pricing data. (See Appendix B for the list of states included for each of these large insurers.)

Figure 7: Premiums Charged By Largest Auto Insurers Based on Credit Information

Company

Average

Annual

Premium-

Excellent

Credit

Average

Annual

Premium-Fair

Credit

Average

Annual

Premium-Poor

Credit

Number of

States Included

in Average

Premium

Allstate

$737

$1,045

$1,392

48

American

Family

$582

$838

$1,219

16

Auto Owners

Group

$284

$477

$797

18

GEICO

$443

$621

$846

27

Farmers

$712

$1,035

$1,485

45

Nationwide

$503

$678

$789

21

Progressive

$528

$867

$1,309

49

State Farm

$338

$604

$1,098

49

Travelers

$586

$964

$1,505

24

USAA

$317

$414

$608

40

Data for Liberty Mutual were not available.

The Credit Score Penalty in Auto Insurance Premiums | CFA 12

Among the nation’s largest insurers, the carriers with the steepest penalties are State

Farm, Auto Owners Group, Travelers, and Progressive. Our research found that:

• State Farm charges people with fair credit a 78% surcharge over the premiums charged to

excellent credit drivers, and it charges poor credit customers a 224% surcharge on

average.

• Auto Owners Group imposes a 68% increase on fair credit customers and a 181%

increase on poor credit customers.

• Travelers adds 64% to the premium of fair credit customers and 157% to those with poor

credit.

• Progressive charges customers with fair credit 64% more and customers with poor credit

148% more.

IV. State and Local Examples of Discrimination Based on Credit

Information

An examination of auto insurance premiums and credit information at the state and local

level reveals even more dramatic examples of discrimination and excessive premiums. Pricing

on the basis of credit history varies depending on state, but in many communities, due to the

strong influence that a customer’s ZIP code already has on their premium, the dollar impact of

credit-based premiums is especially egregious.

In New Jersey, a 35-year-old person with excellent credit pays an average annual

premium of $660. But the same individual with fair credit pays a premium of $1,087, and if they

have poor credit their premium increases to $1,663. When the data are viewed at the ZIP-code

level, the credit score penalty meted out by insurers can prove significantly more intense than the

statewide averages suggest. Figure 8 below looks at several ZIP codes in various locations

around New Jersey—Princeton, West Orange, Trenton, and Newark—and the various premiums

charged by insurers to consumers based on their credit.

In each of these ZIP codes, consumers pay the lowest premiums if they have excellent

credit, suffer a significant penalty if they have fair credit, and face the largest increases if they

have poor credit. But lower-credit consumers in Trenton and Newark pay the highest premiums.

When the territorial and credit differences are combined, the price disparities are staggering. A

safe driver with poor credit living in Newark pays more than three times the premium charged to

a safe driver with excellent credit living eight miles away in West Orange. A poor-credit but safe

driver in Trenton pays more than four times the amount charged to an excellent credit driver 13

miles north in Princeton.

The Credit Score Penalty in Auto Insurance Premiums | CFA 13

Figure 8: Average Premiums Charged By Insurers Based on Credit History in Various

New Jersey ZIP Codes

The results are similar across all states where credit information is permitted in auto

insurance pricing. Only California, Hawaii, and Massachusetts permanently ban its use; in those

states there was no difference in premium between consumers who have excellent, fair, or poor

credit, and financially vulnerable safe drivers are protected from the punishing surcharges that

poor or fair credit brings to their insurance premiums.

Some of the most severe penalties are found in Michigan. The data capture premiums

charged after the legislature declared the use of credit scores for insurance illegal in 2019. But,

in an act of brazen deception, even as the legislature prohibited the use of an “individual’s credit

score” in the Michigan Insurance Code (Section 500.2162), it allowed insurers to use “credit

information or a credit-based insurance score” (Section 500.2153) for pricing customers. Of

course, as noted in the opening of this report, insurers do not use “credit scores” but a nominally

different “credit-based insurance score” to wield credit history against safe drivers. Ironically,

after the purported reform, Michigan is among the states with the worst penalties associated with

consumer credit history. The average auto insurance premium in our Michigan dataset

21

for

21

Due to data quality concerns related to one Michigan insurer, the average premiums in this state reflect the rating

systems of nine insurers. By excluding the tenth insurer in our dataset, the average premium charged to drivers and

the percentage impact of credit history is lower than it would have been if that insurer had been included in the

analysis.

$0 $500 $1,000 $1,500 $2,000 $2,500 $3,000 $3,500 $4,000

Statewide

Princeton-08542

West Orange-07052

Trenton-08618

Newark-07106

Average Premiums Charged by Insurers Based on Credit

Score in Various New Jersey ZIP Codes

Poor Credit Fair Credit Excellent Credit

$3,538

$2,145

$1,268

$3,146

$1,901

$1,123

$2,846

$1,756

$1,062

$1,925

$1,225

$775

$1,663

$1,087

$660

The Credit Score Penalty in Auto Insurance Premiums | CFA 14

someone with poor credit is $2,667, compared to $1,439 for someone with fair credit and $734

for someone with excellent credit. That is a 263% average premium increase for consumers with

poor credit compared to those who have excellent credit.

V. Insurers Value Credit More Than Driving Safety

The problem of emphasizing credit for pricing is made even worse by the scale of its role

in pricing. Evidence shows that insurers, on average, consider credit information a more

important rating factor than how safe a driver has been. In 2015, Consumer Reports tested the

impact of credit history on auto insurance premiums and found that “your credit score could have

more of an impact on your premium price than any other factor.” In fact, the research showed

that in the vast majority of states, customers with pristine driving records but poor credit paid

higher auto insurance premiums than excellent credit drivers who had a drunk driving conviction

on their motor vehicle record.

22

Using information from that study, Figure 9 below shows the state-by-state difference in

average premium for a full coverage

23

policy between safe drivers with poor credit and excellent

credit drivers with a DWI (driving while intoxicated) conviction. Other than in California,

Hawaii, and Massachusetts where credit scoring is impermissible, there were only five states in

which drunk driving leads to a higher insurance penalty than poor credit at the time of the

Consumer Reports study.

Figure 9. Auto Insurance Premiums by State-For Consumers With a DWI Conviction Vs.

Consumers With Poor Credit

State

Premium for Driver

With DWI and

Excellent Credit

Premium for Good

Driver With Poor

Credit

How Much More

Drivers With Poor

Credit Pay

Alabama

$1,483

$2,555

$1,072

Alaska

$2,204

$2,001

-$203

Arizona

$2,055

$3,032

$977

Arkansas

$2,233

$2,278

$45

California

$4,746

$1,747

-$2,999

Colorado

$1,632

$2,773

$1,141

Connecticut

$2,895

$3,453

$558

Delaware

$2,790

$3,723

$933

District of Columbia

$2,215

$2,957

$742

Florida

$2,274

$3,826

$1,552

Georgia

$2,133

$2,415

$282

22

“The Secret Score Behind Your Rates.” Consumer Reports. July 30, 2015. Available at

https://www.consumerreports.org/cro/car-insurance/credit-scores-affect-auto-insurance-rates/index.htm.

23

Note that Consumer Reports data are for full coverage policies (including comprehensive and collision) while the

Consumer Federation of America premium quotes are only for state minimum limits policies, which is why the

premium quote from CFA research are much lower than the CR research.

The Credit Score Penalty in Auto Insurance Premiums | CFA 15

Hawaii

$3,460

$993

-$2,467

Idaho

$1,355

$2,429

$1,074

Illinois

$1,677

$2,539

$862

Indiana

$1,675

$1,996

$321

Iowa

$1,489

$1,837

$348

Kansas

$1,367

$2,266

$899

Kentucky

$2,749

$3,694

$945

Louisiana

$2,643

$3,548

$905

Maine

$1,413

$1,760

$347

Maryland

$1,268

$2,904

$1,636

Massachusetts

$4,112

$2,207

-$1,905

Michigan

$5,744

$5,725

-$19

Minnesota

$1,582

$2,487

$905

Mississippi

$1,920

$2,378

$458

Missouri

$1,262

$2,135

$873

Montana

$1,410

$2,589

$1,179

Nebraska

$1,586

$2,061

$475

Nevada

$2,052

$3,323

$1,271

New Hampshire

$1,694

$2,590

$896

New Jersey

$3,043

$3,080

$37

New Mexico

$1,859

$2,248

$389

New York

$2,573

$3,162

$589

North Carolina

$4,015

$1,221

-$2,794

North Dakota

$1,510

$2,302

$792

Ohio

$1,097

$1,521

$424

Oklahoma

$2,198

$3,872

$1,674

Oregon

$1,777

$2,302

$525

Pennsylvania

$1,893

$2,258

$365

Rhode Island

$3,163

$2,762

-$401

South Carolina

$2,210

$3,339

$1,129

South Dakota

$1,663

$2,250

$587

Tennessee

$1,974

$2,102

$128

Texas

$2,435

$3,426

$991

Utah

$1,507

$1,995

$488

Vermont

$1,902

$2,364

$462

Virginia

$2,038

$2,566

$528

Washington

$1,873

$2,563

$690

West Virginia

$2,153

$2,848

$695

Wisconsin

$1,126

$1,722

$596

Wyoming

$1,615

$2,070

$455

Nationwide Average

$2,171

$2,592

$421

Nationwide Average

Excluding CA, MA,

& HI

$2,051

$2,651

$600

The Credit Score Penalty in Auto Insurance Premiums | CFA 16

Consumer Reports did not publish comparable data for California, Hawaii, and Massachusetts as those states do

not allow the use of credit. The data for these three states come from a similar, non-public data-set reviewed by the

authors. The premiums are not precisely comparable with the other states, (they are more recent among other slight

differences) but they accurately reflect difference in those states relative to other states.

Negative numbers mean that drivers with poor credit pay less than drivers with a DWI conviction.

VI. Modern Day Redlining: How Credit Information in Auto

Insurance Perpetuates Racial Discrimination

When auto insurers use credit information in insurance underwriting and pricing, data

show that people of color face a disproportionate share of higher priced policies. For example,

the 2019 study “The Geography of Subprime Credit” published by the Federal Reserve Bank of

Chicago, found that “[p]laces with lower credit scores show more signs of economic adversity

and reflect patterns of segregation.” The authors also reported a “disproportionate representation

of black households in the most subprime neighborhoods.”

24

In 2021, the Urban Institute found that median credit scores reveal persistent racial

disparities, with scores for white Americans significantly higher than credit scores for Black,

Hispanic, and Native American consumers.

25

Figure 10 below shows median credit scores for

consumers by demographics in August 2021.

Figure 10: Median Credit Scores By ZIP Code Demographics in August 2021

Community

Median Credit Score In August 2021

White Communities

727

Hispanic Communities

667

Native American Communities

612

Black Communities

627

All Communities

709

Per Urban Institute analysis, “credit scores are Vantage scores that range from 300 to 850. The communities listed

in the key refer to zip codes where more than 60 percent of residents are Native American or in the respective racial

or ethnic group.”

A 2013 Federal Reserve Bulletin illustrated that among home buyers, only 5.4% of white

Americans had a credit score below 620, while 21.4% of Black Americans purchasing homes

had a credit score below 620.

26

24

“The Geography of Subprime Credit.” By Taz George, Robin Newberger, and Mark O’Dell. ProfitWise News and

Views, No. 6, 2019. Available at https://www.chicagofed.org/publications/profitwise-news-and-views/2019/the-

geography-of-subprime-credit.

25

“Credit Health During the COVID-19 Pandemic.” Urban Institute. February 25, 2021. Available at

https://apps.urban.org/features/credit-health-during-pandemic/.

26

“Mortgage Market Conditions and Borrower Outcomes: Evidence from the 2012 HMDA Data and Matched

HMDA–Credit Record Data.” By Neil Bhutta and Glenn Canner. Federal Reserve BULLETIN Vol. 99, No. 4.

(Table 14a). November 2013. Available at https://www.federalreserve.gov/pubs/bulletin/2013/pdf/2012_hmda.pdf.

The Credit Score Penalty in Auto Insurance Premiums | CFA 17

A 2007 Federal Trade Commission study illustrated the problem clearly. As Figure 11

(the graph was Figure 18 in the FTC study) reveals, African American and Hispanic insurance

customers have disproportionately low credit-based insurance scores. Even after controlling for

income, age, and gender, the study found “that large differences remain in the distributions of

scores across racial and ethnic groups.”

27

These credit disparities are

connected to systemic biases against Black,

Latino, and Indigenous communities and

long-standing structural hurdles to

achieving financial stability for

communities of color. When credit

information is used to construct credit-

based insurance scores for underwriting and

rating auto insurance, the result is higher

auto insurance premiums for drivers of

color.

VII. Credit Information, Income and Auto Insurance Premiums:

The Poor Pay More

The use of credit information in auto insurance especially harms low-income consumers;

a number of studies have found that consumers who earn lower salaries disproportionately have

worse credit information and lower credit scores.

28

,

29

Several state insurance departments have conducted or commissioned studies of credit

scores, as has the Federal Trade Commission. All of these studies have used different datasets,

but virtually all have found a positive relationship between household income and these scores –

27

“Credit-Based Insurance Scores: Impacts on Consumers of Automobile Insurance.” Federal Trade Commission.

July 2007. Pg. 57. Available at https://www.ftc.gov/sites/default/files/documents/reports/credit-based-insurance-

scores-impacts-consumers-automobile-insurance-report-congress-federal-trade/p044804facta_report_credit-

based_insurance_scores.pdf.

28

“Average Credit Score in America: 2021 Report.” By Joe Resendiz. Value Penguin. January 27, 2021. Available

at https://www.valuepenguin.com/average-credit-score#income.

29

“Why the South Has Such Low Credit Scores.” By Andrew Van Dam. Washington Post. February 17, 2023.

Available at https://www.washingtonpost.com/business/2023/02/17/bad-southern-credit-scores/.

Figure 11: Scores by Race and Ethnicity

The Credit Score Penalty in Auto Insurance Premiums | CFA 18

as income declines, scores tend to decline.

30

A Missouri study of scores by ZIP Codes from 1991

to 2001 found that credit scores appear to be positively and significantly correlated with family

income.

31

Washington State’s 2003 study uncovered a “statistically significant association

between credit scores and income,” with lower incomes being correlated with lower scores.

32

Research by the Texas Insurance Department submitted to the Texas State Legislature in 2004

found that “in general, average and median credit scores tend to get better as income rises.”

33

Low-income consumers are also more likely to have little or no credit history; consumers

with limited credit histories have worse credit-based insurance scores and face higher rates. In

recent years, the CFPB has reported on the number of primarily lower-income Americans who

are “credit invisible” (26 million) or whose credit has “gone stale” (19 million), which creates

barriers to and higher costs for products and services that use credit history in underwriting and

pricing.

34

Research has shown that “almost 30 percent of adults in low-income Census tracts

were credit invisible, a rate about 8 times higher than that in upper-income Census tracts.”

35

In 2017, the CFPB also found that the way consumers establish their credit history often

differs greatly based on economic background. Consumers in lower-income areas are far more

likely to become credit visible (meaning they begin their credit history) based on negative

records such as having a debt sent to collectors. By contrast, consumers in wealthy areas are

more likely to begin their credit history by opening a credit card or by getting someone else to

help them establish their credit.

36

As much research and reporting have revealed, low and moderate-income families who

make prudent financial decisions often face far more severe financial challenges than higher-

income families. They have less discretionary income, less income security, less savings, and are

more likely to face sudden financial demands that cannot be easily met. The application of credit

30

A 1999 Virginia State Corporation Commission’s Bureau of Insurance report assessing the relationship between

scores and income, according to the Federal Trade Commission, “left unclear the relationship between scores and

race and income.”

31

“Insurance-Based Credit Scores: Impact on Minority and Low Income Populations in Missouri.” By Brent Kabler.

Missouri Department of Insurance. January 2004. Available at https://insurance.mo.gov/reports/credscore.pdf.

32

“A Report to the Legislature: Effect of Credit Scoring on Auto Insurance Underwriting and Pricing.” State of

Washington, Office of the Insurance Commissioner. 2003.

33

“Report to the 79th Legislature: Use of Credit Information by Insurers in Texas.” Texas Department of Insurance.

Pg. 16. December 30, 2004. Available at https://www.tdi.texas.gov/reports/documents/creditrpt04.pdf.

34

“CFPB Explores Impact of Alternative Data on Credit Access for Consumers Who Are Credit Invisible.”

Consumer Financial Protection Bureau. February 16, 2017. Available at https://www.consumerfinance.gov/about-

us/newsroom/cfpb-explores-impact-alternative-data-credit-access-consumers-who-are-credit-invisible/.

35

“The Geography of Credit Invisibility.” By Kenneth Brevoort, Jasper Clarkberg, Michelle Kambara, and

Benjamin Litwin. Consumer Financial Protection Bureau Office of Research Reports Series No. 18-6. September 1,

2018. Available at SSRN: https://ssrn.com/abstract=3288848.

36

“Consumer Financial Protection Bureau Study Finds Consumers in Lower-Income Areas are More Likely to

Become Credit Visible Due to Negative Records.” Consumer Financial Protection Bureau. June 7, 2017. Available

at https://www.consumerfinance.gov/about-us/newsroom/consumer-financial-protection-bureau-study-finds-

consumers-lower-income-areas-are-more-likely-become-credit-visible-due-negative-records/.

The Credit Score Penalty in Auto Insurance Premiums | CFA 19

history to insurance prices only amplifies those challenges by raising the cost of required

insurance products for the many millions of low-income residents with sub-prime credit histories

or none at all. Therefore, when insurers determine rates and eligibility based on credit, low-

income Americans are harmed to a greater extent than wealthy consumers, meaning they pay

more for auto insurance even though they can afford less.

VIII. Recent and Current State Reform Efforts

For decades, consumer advocates and civil rights groups have pressed insurers,

regulators, and policymakers to end the use of credit-based insurance scoring. While for years

the use of credit has been prohibited by three states, the practice has mostly persisted unabated.

However, in recent years there has been increased concern about the use of credit-based

insurance scoring generally and the way in which credit history reinforces and exacerbates

structural racism in particular. Below are some of the reform efforts around the country that have

focused on the impact of credit history on auto insurance premiums:

• Nevada. In 2020 the Nevada insurance commissioner promulgated regulation R087-20,

temporarily blocking the use of credit scoring for two years after the end of Nevada’s

COVID-19 emergency declaration, until May 2024. The rule was issued in response to

the impact of the COVID pandemic on the validity of credit scoring models as well as its

impact on the credit history of individual consumers. The regulation was upheld by the

Nevada Supreme Court.

• Washington State. The insurance commissioner promulgated regulations that

temporarily block the use of credit scoring for three years in response to the impact of the

COVID pandemic on the validity of credit scoring models, as well as its impact on the

credit history of individual consumers. A state court struck down this regulation in 2022.

In 2021, a bill permanently banning credit was introduced in the Washington legislature,

but it did not pass.

• New Jersey. An auto insurance reform bill, supported by a coalition of consumer and

civil rights groups along with some insurance companies, would ban the use of credit

history in auto insurance, as well as education, occupation, marital status, and

homeownership status. In the 2020-2021 legislative session it was passed by the New

Jersey Senate but failed in the General Assembly.

• Maryland. In recent years the legislature failed to enact bills which would have banned

the use of credit informed in auto insurance.

• Oregon. In 2023, the legislature considered a bill that would ban the use of credit scores

in insurance, as well as the use of other socioeconomic factors, but it did not pass.

• Colorado. In 2021 the Colorado legislature enacted SB 21-169, supported by the

Colorado Insurance Commissioner and consumer and civil rights advocates. This law

bans unfair discrimination in insurance pricing and other aspects of the insurance

The Credit Score Penalty in Auto Insurance Premiums | CFA 20

transaction, including marketing and claims settlement, and requires the application of a

governance and testing regime for the use of external data and data models or algorithms

that could result in unfair discrimination. While the law does not directly mention credit

scores, consumer groups expect that it will be subject to the unfair discrimination testing

requirements that are adopted pursuant to this law. The Colorado Division of Insurance is

currently conducting a series of stakeholder meetings to reduce unfair discrimination in

auto insurance.

• In 2023, Representative Bonnie Watson Coleman (NJ) and original co-sponsors Rep.

Rashida Tlaib (MI) and Rep. Mark Takano (CA) introduced the Prohibit Auto Insurance

Discrimination Act” or “PAID Act” in Congress, which would prevent the use of various

socioeconomic rating factors, including credit history, by auto insurers.

IX. Some Insurers Suggest a Readiness to Move Beyond Credit

Information

While the major auto insurers all use credit information to underwrite and rate customers,

there have been some cracks in industry unanimity concerning this factor.

The New Jersey-based insurer CURE has been arguing against the use of credit scoring in

insurance for much longer. Its Chief Operating Officer Eric Poe testified before Congress in

2008 that “[w]ithout these fundamental changes to our industry [including a prohibition on credit

scoring] it is clear that the highest rates for car insurance will be charged to the segment of the

population that can least afford it regardless if they commit themselves to responsible driving.”

37

The start-up insurer Loop does not use credit in its pricing model, explaining:

The use of credit scores in insurance pricing is clearly an issue that has to be

fixed. These scores don't accurately predict a driver’s risk as a policyholder and

disproportionately affect low-income individuals and communities of color.

38

In August 2020, Root Insurance, another recent entrant in the auto insurance market,

which relies on driving data it captures from customers’ vehicles, announced it would stop using

credit scores to set rates. The company explained its decision by announcing that “by basing

37

“Written Testimony of Eric S. Poe, Esquire CPA and Chief Operating Officer of CURE Auto Insurance Before

the Subcommittee on Oversight and Investigations, House Committee on Financial Services.” May 21, 2008.

Available at https://archives-financialservices.house.gov/hearing110/poe052108.pdf.

38

“ How Does Your Credit Score Affect Your Car Insurance?” Loop. January 30, 2023. Available at

https://www.ridewithloop.com/blog/how-does-your-credit-score-affect-your-car-insurance-2.

The Credit Score Penalty in Auto Insurance Premiums | CFA 21

rates on demographic factors like credit score, the traditional car insurance industry has long

relied on unfair, discriminatory biases in its insurance pricing.”

39

Sigo Seguros, a new auto insurer serving the Spanish speaking community, launched its

own insurance product in Texas that removes what it describes as biased rating factors like credit

score, education level, and employment history from its underwriting process.

40

Insurance giant Allstate has begun to speak publicly about moving away from non-

driving rating factors such as credit scores and toward driving data captured through telematics

41

to determine rates.

42

But even as some insurers large and small begin to acknowledge the deep

seated problems that are associated with the use of credit based insurance, it will almost certainly

require regulatory and legislative pressure on carriers before consumers have many options to

buy a reasonably priced policy irrespective of their credit score.

X. Conclusion: Decisive Reforms Are Needed to Reduce Auto

Insurance Costs and Eliminate Unfair Discrimination

Consumer credit information, when used in auto insurance pricing, has a significant and

negative impact that is particularly acute for the most financially vulnerable consumers. It

increases costs for millions of drivers, disproportionately penalizes low income-consumers and

people of color, and contributes to higher levels of uninsured motorists, which in turn raises

premiums on insured drivers. Policymakers should enact reforms to end this practice. CFA

makes the following recommendations:

• State lawmakers should prohibit the use of credit information in setting auto insurance

rates or determining eligibility for a policy.

• Until credit-based insurance scoring is prohibited, state insurance departments should

devote more resources to analyzing insurer rate and rule filings and reject company plans

that unfairly discriminate based on their use of credit-based insurance scores. Regulators

should also report to the public the premium impact of credit scoring for each company

39

“Root Car Insurance Will Stop Using Credit Scores to Set Rates, Calling It Discriminatory.” By Sebastian Blanco.

Car and Driver. August 14, 2020. Available at https://www.caranddriver.com/news/a33555840/root-auto-insurance-

credit-scores-racism/.

40

“Sigo Seguros Launches Spanish-First Auto Insurance Product in Texas.” Insurance Journal. August 4, 2021.

Available at https://www.insurancejournal.com/news/southcentral/2021/08/04/625622.htm.

41

For a discussion of the pros and cons and consumer concerns regarding telematics, or “usage based insurance,”

see Consumer Federation of America’s white paper “Watch Where You’re Going: What’s Needed to Make Auto

Insurance Telematics Work for Consumers.” Available at https://consumerfed.org/press_release/new-white-paper-

released-auto-insurance-telematics-programs-require-new-consumer-and-privacy-protection-standards-to-achieve-

safety-and-pricing-promises/.

42

“Allstate Wants to Track Your Driving to Determine Your Car Insurance Rate.” By Leslie Scism. Wall Street

Journal. October 8, 2021. Available at https://www.wsj.com/articles/allstate-wants-to-track-your-driving-to-

determine-your-car-insurance-rate-11633685400.

The Credit Score Penalty in Auto Insurance Premiums | CFA 22

licensed to sell auto insurance in their state. This report should include a comparison of

the premium for a poor-credit driver with a clean driving record and an excellent credit

driver with a drunk driving conviction.

• States should enact reforms modeled on Colorado law SB 21-169 to combat unfair

discrimination and bias in insurance and in information, data models, and algorithms that

insurers use. Even if the use of credit information is prohibited in insurance pricing and

underwriting, regulators will need testing and oversight to ensure the unfairness of the

use of credit is not simply replaced with other factors that also tend to unfairly

discriminate.

For too long auto insurers have used consumer credit information to charge higher rates

to financially vulnerable consumers and unfairly discriminate against safe drivers due to their

reported credit history. It is long overdue for lawmakers and insurance regulators to put a stop to

this practice and fulfill their duty of ensuring a fairly priced auto insurance market.

The Consumer Federation of America is an association of more than 250 nonprofit consumer

organizations that was established in 1968 to advance the consumer interest through research,

advocacy, and education.

The Credit Score Penalty in Auto Insurance Premiums | CFA 23

Appendix A: Base Profile for Auto Insurance Premium Data Acquired from Quadrant

Information Services, LLC

Base Profile

About Our Driver

Vehicle and Coverage

35-year-old, unmarried driver

2011 Honda Civic LX

Licensed for 19 years

12 mile daily commute, 5 days/week

No accidents, moving violations, or license

suspensions

12,000 miles driven annually

No lapse in coverage

Coverage quoted: state minimum

High school diploma

Rents home

The Credit Score Penalty in Auto Insurance Premiums | CFA 24

Appendix B: List of States With Premium Data Reviewed for Each of the Largest Insurers

in Dataset

Allstate: Alabama, Alaska, Arizona, Arkansas, California, Colorado, Connecticut, Delaware,

District of Columbia, Florida, Georgia, Hawaii, Idaho, Illinois, Indiana, Kansas, Kentucky,

Louisiana, Maine, Maryland, Massachusetts, Minnesota, Mississippi, Missouri, Montana,

Nebraska, Nevada, New Hampshire, New Jersey, New Mexico, New York, North Carolina,

North Dakota, Ohio, Oklahoma, Oregon, Pennsylvania, Rhode Island, South Carolina,

Tennessee, Texas, Utah, Vermont, Virginia, Washington, West Virginia, Wisconsin, Wyoming.

American Family: Arizona, Colorado, Idaho, Illinois, Indiana, Iowa, Kansas, Minnesota,

Missouri, Nevada, North Dakota, Oregon, South Dakota, Utah, Washington, Wisconsin.

Auto Owners Group: Alabama, Arizona, Colorado, Georgia, Idaho, Indiana, Iowa, Kentucky,

Minnesota, Nebraska, North Carolina, North Dakota, Ohio, South Carolina, South Dakota,

Tennessee, Utah, Wisconsin.

Farmers: Alabama, Arizona, Arkansas, California, Colorado, Florida, Hawaii, Idaho, Illinois,

Kansas, Michigan, Missouri, Montana, Nebraska, Nevada, New Jersey, New Mexico, North

Dakota, New Jersey, New Mexico, Oklahoma, Oregon, South Dakota, Tennessee, Texas, Utah,

Washington, Wisconsin, Wyoming.

GEICO: Alabama, Alaska, Arizona, California, Colorado, Connecticut, Delaware, District of

Columbia, Florida, Georgia, Hawaii, Illinois, Indiana, Iowa, Kentucky, Louisiana, Maine,

Maryland, Michigan, Minnesota, Mississippi, Missouri, Montana, Nevada, New Hampshire,

New Jersey, New Mexico, New York, North Carolina, Ohio, Oklahoma, Oregon, Pennsylvania,

Rhode Island, South Carolina, Tennessee, Texas, Utah, Vermont, Virginia, Washington, West

Virginia, Wisconsin, Wyoming.

Nationwide: Arkansas, Colorado, Connecticut, Delaware, District of Columbia, Iowa, Kansas,

Maryland, Mississippi, Montana, Nebraska, New Mexico, Ohio, Pennsylvania, Rhode Island,

South Carolina, South Dakota, Texas, Vermont, Virginia, West Virginia.

Progressive: Alabama, Alaska, Arizona, Arkansas, California, Colorado, Connecticut,

Delaware, District of Columbia, Florida, Georgia, Hawaii, Idaho, Illinois, Indiana, Iowa, Kansas,

Kentucky, Louisiana, Maine, Maryland, Massachusetts, Michigan, Minnesota, Mississippi,

Missouri, Montana, Nebraska, Nevada, New Hampshire, New Jersey, New Mexico, New York,

North Carolina, North Dakota, Ohio, Oklahoma, Oregon, Pennsylvania, Rhode Island, South

Carolina, South Dakota, Tennessee, Utah, Vermont, Virginia, Washington, West Virginia,

Wisconsin.

State Farm: Alabama, Alaska, Arizona, Arkansas, California, Colorado, Connecticut, Delaware,

District of Columbia, Florida, Georgia, Hawaii, Idaho, Illinois, Indiana, Iowa, Kansas, Kentucky,

Louisiana, Maine, Maryland, Michigan, Minnesota, Mississippi, Missouri, Montana, Nebraska,

Nevada, New Hampshire, New Jersey, New Mexico, New York, North Carolina, North Dakota,

The Credit Score Penalty in Auto Insurance Premiums | CFA 25

Ohio, Oklahoma, Oregon, Pennsylvania, South Carolina, South Dakota, Tennessee, Texas, Utah,

Vermont, Virginia, Washington, West Virginia, Wisconsin, Wyoming.

Travelers: Alabama, Arizona, Connecticut, Delaware, Florida, Idaho, Illinois, Indiana, Kansas,

Kentucky, Maine, Maryland, Massachusetts, Minnesota, Missouri, Nevada, New Jersey, New

York, Oregon, Pennsylvania, Rhode Island, South Carolina, Tennessee, Virginia, Washington.

USAA: Alabama, Alaska, Arizona, Arkansas, California, Colorado, Connecticut, Delaware,

District of Columbia, Florida, Georgia, Hawaii, Idaho, Kansas, Kentucky, Louisiana, Maine,

Maryland, Michigan, Mississippi, Montana, Nebraska, Nevada, New Hampshire, New Mexico,

New York, Oklahoma, Oregon, Pennsylvania, Rhode Island, South Carolina, South Dakota,

Tennessee, Texas, Utah, Vermont, Virginia, Washington, West Virginia, Wyoming.