The Practical Lawyer | 39

Cindy J. Chernuchin

If you’ve never thought about it before, get

ready for a surprise: there is no such thing as

“boilerplate” in a security agreement.

A “SECURITY AGREEMENT” is an agreement that

creates or provides for an interest in personal property

that secures payment or performance of an obligation.

Uniform Commercial Code (§9-102(a)(73); §1-201(b)(35)).

(All section references used herein are to the Uniform

Commercial Code, as in effect on the date hereof.) “Boil-

erplate,” as dened by Bryan Garner, is “ready-made or

all-purpose language that will t a variety of contexts.”

Garner, Bryan, A Dictionary of Modern Legal Usage (Oxford,

1st ed., 1987). So given the highly technical nature of se-

curity agreements, it might seem that they would be fertile

soil for boilerplate language of all kinds. As with other

exercises in contract drafting there can be a temptation

to reach for ready-made language, if not for the sake of

relying on a tested model, for the sake of satisfying cli-

ents who keep reminding their attorneys not, as they often

put it, “to reinvent the wheel.” But security agreements

don’t really lend themselves to boilerplate. Although quite

a few provisions of security agreements fall under familiar

headings — just like other contracts — the security agree-

ments themselves are by necessity as different as every un-

Cindy J. Chernuchin

is special counsel in the Corporate and Financial

Services Department of Willkie Farr & Gallagher LLP

in New York. She specializes in banking and institu-

tional nance with an emphasis on issues regarding

Article 8 and Article 9 of the U.C.C. Ms. Chernuchin

represents borrowers, issuers, banks, institutional

lenders, hedge funds, and trustees in a wide ar-

ray of nancings, in cluding asset-based lending,

high-yield bonds, project nancing, acquisition

nancing, letter-of-credit facilities, debtor-in-pos-

session nancing, equipment nancing, industrial

development bonds, telecom nanc ing, mutual

fund nancing, and workouts. She has signicant

experience working with secured revolving credit

and term loan fa cilities for acquisition nancings, in-

cluding representation for the Bank of Nova Scotia;

portfolio companies of Warburg Pincus Equity Part-

ners, L.P. and its aliates; Loral Space & Communi-

cations, Inc. and other sponsors in connection with

a $3 billion acquisition nancing of Telesat Canada;

and an equity sponsor in connection with a $3.76

billion acquisition nancing of the Fairmont Hotel

chain. Ms. Chernuchin was recognized in 2010 as

a New York Super Lawyer. Ms. Chernuchin can be

reached at [email protected]. This article is

based on a paper the author prepared for a seminar

sponsored by the ABA’s Section of Business Law.

Understanding The Terms Of

Security Agreements

40 | The Practical Lawyer June 2011

derlying transaction — also like other contracts. So the purpose of this article isn’t to set forth off-the-shelf

language, but to discuss how each provision ts into the overall picture of the transaction. The examples are

for general reference only; as always, the transaction comes rst, and the best way to approach the agree-

ment is to make sure that both sides are perfectly clear about the terms of the deal.

RECITALS

a. Overview: Recitals explain the transaction, including naming parties thereto, their status, and why they

are entering into the security agreement. For attachment of a security interest to occur, the secured party

must give value (§9-203(b)(1)); the debtor must have an interest in or the power to transfer an interest in the

collateral to the secured party (§9-203(b)(3)(A)); and the debtor must authenticate a security agreement that

describes the collateral (§9-203(b)(2)). “Secured party” is dened as the person in whose favor the security

interest is granted (§9-102(a)(72)(A)). “Debtor” is dened as (A) a person having an interest, other than a se-

curity interest or other lien, in the collateral, whether or not the person is an obligor; (B) a seller of accounts,

chattel paper, payment intangibles or promissory notes; or (C) a cosignee. Note that there are exceptions to

the need to authenticate the security agreement: for example, if the collateral is a deposit account, and the

secured party has control under section 9-104 pursuant to a security agreement.

b. Example:

SECURITY AGREEMENT, dated as of ___________, between [name of Debtor] (“Debtor”), a

[State] [type of registered organization] and [name of Secured Party] (“Secured Party”);

WHEREAS, Debtor has entered into a Credit Agreement dated the date hereof (as amended from time

to time, the “Credit Agreement”) with the Secured Party, pursuant to which the Secured Party, subject

to the terms and conditions contained therein, is to make loans to the Debtor;

WHEREAS, it is a condition precedent to the Secured Party’s making any loans to Debtor under the

Credit Agreement that the Debtor execute and deliver a Security Agreement in substantially the form

hereof.

NOW, THEREFORE,

DEFINITIONS

a. Overview: A security agreement is frequently one of many “loan documents” executed in conjunction

with a loan. To the extent possible, it is best to keep the denitions in all the loan documents consistent. In

addition, the parties must choose which state’s U.C.C. governs, and to the extent terms are dened differ-

ently in various Articles of the U.C.C., which Article of the U.C.C. governs. For example, “instrument”

Security Agreements | 41

under Article 9 includes non-negotiable and negotiable instruments, while “instrument” under Article 3

includes only negotiable instruments (§9-102(a)(47); §3-102(1)(a); §3-104(b)).

Also, the Article 9 denition may not always be benecial. For example, the U.C.C. denition of a

commercial tort claim is “any claim,” thus making it difcult for a debtor to know when it has a claim and

difcult for a secured party to enforce a debtor default for failure to report the existence of such a claim.

Thus, both parties benet from inserting a clear standard into the U.C.C. denition of “Commercial Tort

Claim.”

Similarly, the U.C.C. denition of “Deposit Accounts” includes all deposit accounts, including payroll

accounts. For reputational and liability reasons, a secured party generally does not want to exercise control

over a payroll account and therefore is usually willing to exclude payroll accounts from the U.C.C. denition

of deposit accounts, or alternatively, to exclude payroll accounts from the perfection requirement.

It may make sense to exclude certain personal property from collateral, thereby creating a need for a

denition of “Excluded Collateral.” For example, a secured party may not want to spend time reading all of

the debtors’ contracts and therefore usually will include an exclusion for contracts that have an enforceable

anti-assignment provision. If a foreign subsidiary provides credit support of any type beyond a two-thirds

pledge of its stock, the foreign subsidiary is deemed to have paid a dividend to the U.S. parent equal to the

principal amount of the loan to the extent of the foreign subsidiary’s earnings and prots. Thus, any such

credit support beyond the two-thirds pledge can result in “phantom income” (i.e., taxable income without

corresponding cash) to the U.S. parent. See section 956 of the Internal Revenue Code. Secured parties do

not want their debtors to incur taxable phantom income and therefore will generally exclude from a U.S.

loan voting stock of foreign subsidiaries in excess of 65 percent. Similarly, it may not be worth the bor-

rower’s effort and expense to perfect a security interest in certain assets, including goods subject to a certi-

cate of title, if such personalty constitutes a minimal amount of the debtor’s assets, so secured parties are

frequently williing to exclude such personalty. A debtor does not want to lose the benet of its bargain in

the credit agreement and therefore will want to exclude capital leases, purchase money nancings and cash

to secure letter-of-credit rights, to the extent they prohibit other liens and are permitted under the credit

agreement.

Some states adopted non-uniform provisions of the U.C.C., so be cognizant of which state’s U.C.C. is

chosen to govern. For example, a question sometimes arises as to whether an annuity is a contract of insur-

ance that is excluded from the scope of Article 9 by section 9-109(d)(8), or whether it is a general intangible.

New York concluded that an annuity contract is a contract of insurance, and is therefore excluded from

the scope of Article 9. A secured party lending to a debtor that holds valuable annuity contracts may wish

to designate law other than the New York U.C.C. to govern. Also, some states (for example, New York) did

not adopt the Article 9 override of statutory anti-assignment clauses. Another non-uniform provision to be

aware of is whether the state’s U.C.C. is applicable to government debtors. Typically, the U.C.C. of the state

chosen will be the same state whose law governs the security agreement as a matter of contract between the

debtor and the secured party.

Moreover, certain terms must be dened. For there to be a security interest, the interest must secure

“payment or performance of an obligation.” For drafting simplicity and clarity, consider dening a term to

42 | The Practical Lawyer June 2011

refer collectively to the secured obligations. “Secured Obligations” can include future advances only if the

security agreement so states. However, beware of “dragnet” clauses because courts may not give effect to

these provisions (i.e., limit obligation to obligations arising out of the loan documents).

While remedies under Article 9 can only be enforced upon default, Article 9 does not dene default.

Thus, the security agreement must dene “Default” and/or “Event of Default.” Without such denition, it

is unclear when remedies can be exercised.

b. Negotiable Provisions: The denitions in a security agreement are negotiable. The parties may ne-

gotiate, for example, whether “Obligations” will cover existing obligations and hereafter arising obligations,

or obligations arising under the loan documents or at any time owing to the secured party. As noted, use

these dragnet clauses with caution, as courts may not enforce such provisions.

The parties may also negotiate, for example, whether “Excluded Deposit Accounts” will be “Excluded

Collateral” or “Unperfected Collateral”; whether “Commercial Tort Claims” must meet value thresholds

or must be asserted in a judicial proceeding; or whether “Commercially Reasonable Efforts” require the

making of payments or concessions.

c. Example:

All capitalized terms used herein without denition shall have the respective meanings provided there-

for in the Credit Agreement.

All terms dened in the U.C.C. of the State and used herein shall have the same denitions herein as

specied therein. However, if a term is dened in Article 9 of the U.C.C. of the State differently than in

another Article of the U.C.C. of the State, the term has the meaning specied in Article 9.

“Commercially Reasonable Efforts” means efforts that are commercially reasonable but in no event

require the making of payments or material concessions.

“Commercial Tort Claim” has the meaning provided in the U.C.C. except it shall refer only to such

claims that have been asserted in judicial proceedings.

“Deposit Accounts” has the meaning provided in the U.C.C. except it shall not include Excluded De-

posit Accounts.

“Excluded Collateral” means (1) any property in which the Debtor now or hereafter has rights, to the

extent in each case a security interest may not be granted by the Debtor in such property as a matter

of applicable law, or under the effective terms of the governing document applicable thereto, without

the consent of one or more parties thereto other than any [Loan Party] but only for so long as such

consent has not been obtained; (2) assets subject to capital leases, purchase money nancing, and cash

to secure letter-of-credit reimbursement obligations, to the extent such capital leases, purchase money

Security Agreements | 43

nancing, or letters of credit prohibit other liens and are permitted under the Credit Agreement; (3)

assets sold to a person who is not a [Loan Party] in compliance with the Credit Agreement; (4) assets

owned by a [Guarantor] after the release of the guaranty of such [Guarantor] pursuant to Section ___

of the Credit Agreement; (5) vehicles and other goods subject to a certicate of title; (6) any collateral

as to which the Secured Party has determined in its sole discretion that the collateral value is insufcient

to justify the difculty, time and/or expense of obtaining a perfected security interest therein; (7) any

application for registration of a [Trademark] led with the United States Patent and Trademark Ofce

(PTO) on an intent-to-use basis until such time (if any) as a statement of use or amendment to allege

use is accepted by the PTO, at which time such [Trademark] shall automatically become part of the

Collateral and subject to the security interest pledged; (8) any property to the extent that such grant of

a security interest is prohibited by any [Governmental Authority], or requires a consent not obtained

by any [Governmental Authority]; (9) the issued and outstanding voting capital stock of any rst-tier

[Foreign Subsidiary] in excess of sixty-ve percent (65%) thereof; [(10) any property to the extent that such

grant of a security interest would contravene the Agreed Security Principles, and (11) any subsidiary to the extent that Rule

3-10 or Rule 3-16 of Regulation S-X under the Securities Act requires separate nancial statements of such subsidiary to

be led with the SEC (or any other governmental agency).] Notwithstanding the foregoing, any and all proceeds

of Excluded Collateral, to the extent that the proceeds are not themselves Excluded Collateral, shall be

Collateral.

“Excluded Deposit Accounts” means (1) any deposit accounts specially and exclusively used for pay-

roll, payroll taxes, and other employee wage and benet payments to or for the benet of the Debtor’s

salaried employees; (2) escrow arrangements (e.g., environmental indemnity accounts); and (3) deposit

accounts not otherwise subject to the provisions of this paragraph, the aggregate average daily balance

of which for all Loan Parties does not exceed $_______ at any time.

“Quarterly Update Date” means the date of the delivery of the nancing statements pursuant to Sec-

tion ___ of the Credit Agreement.

“Secured Obligations” means all of the indebtedness, obligations, and liabilities of the Debtor to the

Secured Party, individually or collectively, whether direct or indirect, joint or several, absolute or con-

tingent, due or to become due, now existing or hereafter arising (and whether arising before or after the

ling of a petition in bankruptcy and including all interest accrued after the petition date) under or in

respect of the Credit Agreement, any promissory notes or other instruments or agreements executed

and delivered pursuant thereto or in connection therewith, or this Agreement.

“State” means the [State/Commonwealth of ____________________ ].

“Unperfected Collateral” means Excluded Deposit Accounts, goods subject to certicate of title laws,

and letter-of-credit rights, individually or in the aggregate not in excess of $_____.

44 | The Practical Lawyer June 2011

GRANTING LANGUAGE

a. Overview: No special language is required to create a security interest. The phrase “grant a security

interest” is sufcient. “Grant” and “pledge” can be used synonymously (§9-109; §9-203), but are frequently

used together. It is preferable not to use “assign” because that term can connote an outright transfer of

ownership when applied to certain intellectual property.

The security agreement must “provide a description of the collateral” (§9-203(b)(3)(A)), and that de-

scription of collateral is sufcient if it “reasonably identies” the collateral. See also §9-108(a). “Supergener-

ic” descriptions such as “all the debtor’s assets” and “all the debtor’s personal property” are not permitted.

Usually, the security agreement will simply use the categories of collateral established by the U.C.C.

An all asset lien can be described by naming each Article 9 category of collateral and then adding “and

all other personal property whether governed by Article 9 or other law.” See §9-108(b)(3) (see denition of

“general intangibles” for a list of the Article 9 categories of collateral). Nonetheless, one should be cogni-

zant of certain exceptions and limitations on language used to describe collateral, including:

1. “Commercial tort claims” must be described specically (for example, plaintiff ’s and defen-

dant’s names and a description of the claim) in order for a security interest to attach to such claim

(§9-108(e)(i); §9-204(b)(2)). Security agreements generally take this into account by requiring debtors to

give prompt notice to the secured party when any commercial tort claim arises and to supplement the

security agreement to describe the tort claim.

2. “Wherever located” (this makes clear, for example, that a secured party’s security interest will at-

tach to goods located outside of the United States).

3. “Whether now owned or hereafter acquired” will give the secured party a security interest

in personal property acquired after the effective date of the security agreement (§9-204(a)). However,

remember that the security interest cannot attach until the debtor has rights in the collateral or power

to transfer rights in the collateral. After-acquired property must be specically included in the granting

clause to be included in collateral.

4. “Proceeds” can be specically stated in the granting clause, but a security interest in collateral au-

tomatically extends to proceeds even if not mentioned (§9-102(a)(12)(A); §9-203(f); §9-315(a)(2)).

5. “Products” can be specically stated in the granting clause, but if goods become physically united

and identication is lost, the security interest automatically extends to products even if not mentioned

(§9-336).

6. “Insurance” is excluded by section 9-109(d)(8), so unless such claims are proceeds of collateral, Ar-

ticle 9 is not applicable. A security interest can be granted in insurance, but such security interest would

be governed by law other than Article 9 (e.g., common law).

Security Agreements | 45

b. Example:

The Debtor hereby grants and pledges to the Secured Party, to secure the payment and performance in

full of all of the Obligations, a security interest in all:

a. accounts;

b. chattel paper;

c. Commercial Tort Claims (described on Schedule I hereto);

d. Deposit Accounts;

e. documents;

f. general intangibles;

g. goods;

h. instruments;

i. investment property;

j. letter-of-credit rights;

k. money;

l. oil, gas, and other minerals before extraction;

m. insurance and insurance claims;

n. supporting obligations; and

o. all other personal and xture property, whether governed by Article 9 of the U.C.C. or other law

wherever located, whether now owned or hereafter acquired or arising, and all proceeds and prod-

ucts thereof (collectively, the “Collateral”).

Note: prior to extraction, oil, gas, and other minerals are treated as real property and as such lie outside the

scope of Article 9. It is only upon extraction that such minerals become goods and subject to Article 9. See

Ofcial Comment 4c to section 9-102.

PERFECTION

a. Overview: To ensure perfection, it is crucial to correctly classify the collateral. Classication frequently

depends on the debtor’s use of the collateral. For example, a titled vehicle can be consumer goods if it is

used primarily for personal, family, or household purposes; inventory if it is leased or held for sale or lease,

or equipment if it is held for use. Perfection of a security interest in titled vehicles held for consumer use or

as equipment is achieved by compliance with requirements administered by the governmental department

responsible for registration and licensing of such vehicles, which commonly requires a notation of the lien

on the certicate of title. If the titled vehicles are held for sale by a person in the business of selling goods of

that kind, it is inventory, and perfection of a security interest therein is achieved by a properly led nanc-

ing statement.

46 | The Practical Lawyer June 2011

b. Example:

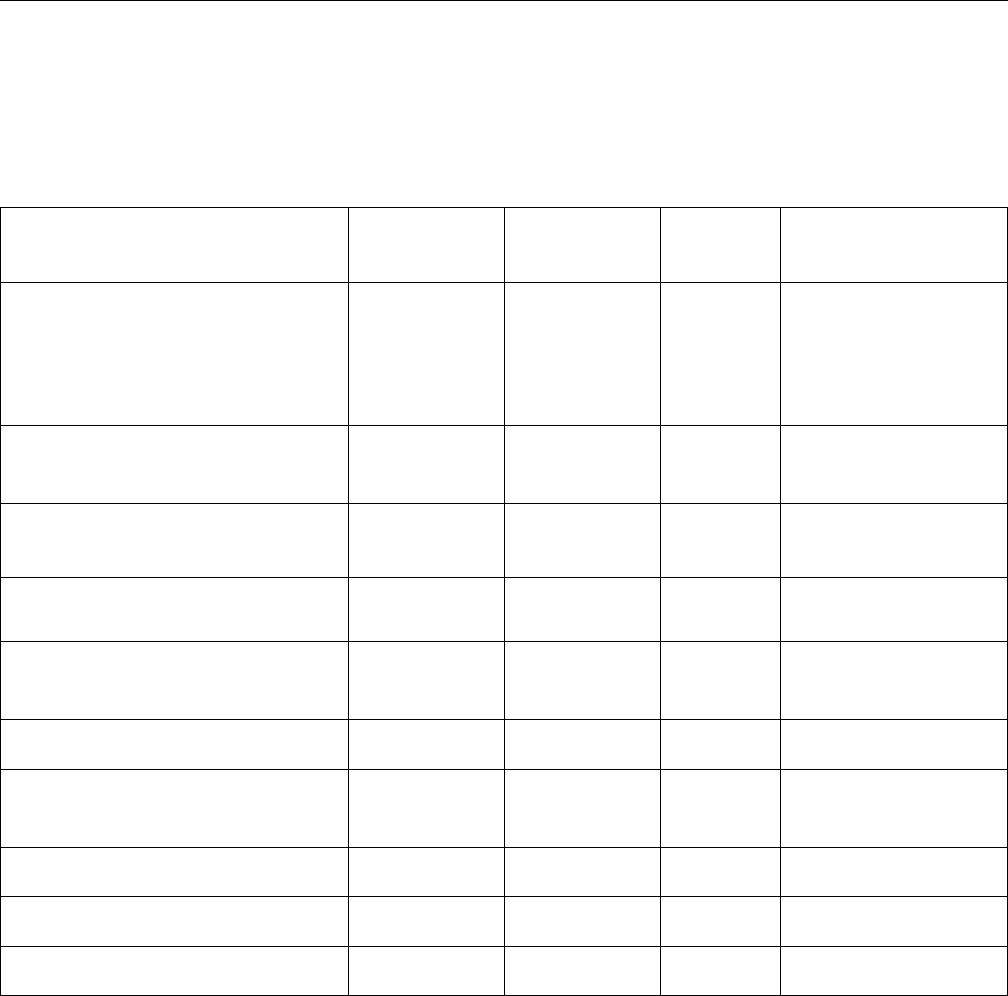

Following is a chart that indicates the various methods of perfection for most Article 9 collateral.

Type of Collateral

Automatic or

Temporary

Possession Control

Financing Statement

Accounts, general intangibles

(except for sales of payment

intangibles), described

commercial tort claims

x

Instruments (except sales of

promissory notes)

x x

x

Goods, negotiable documents x x

x

Tangible chattel paper x

x

Investment property, electronic

chattel paper

x

x

Certicated securities x x x

x

Deposit accounts, letter-of-credit

rights

x

Money x

Payment intangibles (sales) x

Promissory notes (sales) x

c. Filing — Overview: Other than a security interest in sales of payment intangibles and promissory

notes (where perfection is automatic), and deposit accounts, letter-of-credit rights and money, all security

interests in personal property subject to Article 9 can be perfected by a properly led nancing statement.

Authorization to le nancing statements is automatic if the collateral description used in the nancing

statement is the same description provided in the security agreement. Specic authorization is required to

le an “all assets” nancing statement if collateral is less than all assets.

1. Negotiable Provisions: Fixtures are goods, and are therefore perfected by properly ling a nanc-

ing statement centrally in the state where the debtor is located. However, the secured party may also

request a “xture ling” (§9-501(a)(2); Comment 4 to §9-501). Both lings perfect the security interest

in xtures. The signicance of a xture ling is that it will provide priority over any encumbrancer of

the underlying land. See §9-334. Note, a duly recorded mortgage can be effective as a xture ling if it

Security Agreements | 47

(among other things) indicates the goods, and the goods are, or are to become, xtures. See §9-502(c).

Since a xture ling gives additional priority in the real property records, it is a negotiable requirement

under a security agreement.

2. Example:

The Debtor hereby irrevocably authorizes the Secured Party at any time and from time to time to le in

any Uniform Commercial Code jurisdiction nancing statements (including amendments and continu-

ations thereto) that: (a) indicate the Collateral (i) as all assets of the Debtor or words of similar effect,

regardless of whether any particular asset comprised in the Collateral falls within the scope of Article 9

of the Uniform Commercial Code of the State or such jurisdiction, or (ii) as being of an equal or lesser

scope or with greater detail; and (b) contain any other information required for the sufciency or ling

ofce acceptance of any nancing statement or amendment, including (i) whether the Debtor is an or-

ganization, the type of organization, and any organization identication number issued to the Debtor

(if required by the applicable jurisdiction) and, (ii) in the case of a nancing statement led as a xture

ling or indicating Collateral as as-extracted collateral or timber to be cut, a sufcient description of

real property to which the Collateral relates. The Debtor agrees to furnish any such information to the

Secured Party promptly upon the Secured Party’s request. [The Debtor also raties its authorization for the

Secured Party to have led in any Uniform Commercial Code jurisdiction any like initial nancing statements or amend-

ments thereto if led prior to the date hereof.]

d. Possession — Overview: Even though a security interest can be perfected in certain collateral by the

proper ling of a nancing statement, greater priority is afforded by taking possession of certain collateral

(e.g., instruments, tangible chattel paper, certicated securities, negotiable documents).

1. Negotiable Provisions: The requirement for possession of such collateral is negotiable, and may

include thresholds for delivery (e.g., “value in excess of $____”) or requirements for time of delivery

(e.g., promptly, quarterly, upon default, after the continuance of an Event of Default).

2. Example:

If the Debtor shall at any time hold or acquire any promissory notes or tangible chattel paper in an

amount in excess of $______ individually or $ _____ in the aggregate, the Debtor shall endorse, assign,

and deliver the same to the Secured Party on or before the rst Quarterly Update Date following the

acquisition thereof, accompanied by such instruments of transfer or assignment duly executed in blank

as the Secured Party may from time to time specify.

e. Control — Overview: Whereas a security interest in letter-of-credit rights and deposit accounts can

only be perfected by control, a security interest in other collateral can be perfected by the proper ling of

a nancing statement or control, and priority is afforded by obtaining control of such collateral (e.g., elec-

tronic chattel paper, investment property (including uncerticated securities) where the secured party may

enter into a control agreement with the issuer or arrange for the uncerticated security to be registered

48 | The Practical Lawyer June 2011

on the books of the issuer in the secured party’s name), and certicated securities. Note that the secured

party’s security interest in nancial assets (or deposit accounts or commodity accounts) perfected by control

are superior to a security interest in nancial assets (or deposit accounts or commodity accounts) claimed

by another secured party as proceeds of other Article 9 collateral (§9-328(1)). However, the secured party’s

security interest will be junior to a security interest in favor of the securities intermediary (or depositary or

commodity intermediary), unless the securities intermediary (or depositary or commodity intermediary)

subordinates its security interest to the secured party’s security interest (§9-328(3)).

1. Negotiable Provisions: Requirements regarding control are negotiable and may include thresh-

olds for getting and exercising control, whether deposit accounts are excluded from the control require-

ment, timing to obtain control, and commercially reasonable efforts to obtain control. With respect to

the latter, extension of time should be at the sole discretion of the collateral agent (if more than one

secured party) to facilitate a quick response.

2. Example:

For each Deposit Account that the Debtor at any time opens or maintains, the Debtor shall, at the

Secured Party’s request and option, within 60 days of such request, such time to be extended in

Secured Party’s sole discretion, pursuant to an agreement in form and substance satisfactory to the

Secured Party, either: (a) cause the depositary bank to agree to comply without further consent of

the Debtor, with instructions from the Secured Party directing the disposition of funds from time to

time credited to such Deposit Account; or (b) arrange for the Secured Party to become the sole cus-

tomer of the depositary bank with respect to the Deposit Account, with the Debtor being permitted,

only with the consent of the Secured Party, to exercise rights to withdraw funds from such Deposit

Account. [The Secured Party agrees with the Debtor that the Secured Party shall not give any such instructions or

withhold any withdrawal rights from the Debtor, unless an Event of Default has occurred and is continuing.] The

provisions of this paragraph shall not apply to Excluded Deposit Accounts.

f. Collateral in the Possession of a Bailee — Overview: A security interest in possessory collateral

perfected by a properly led nancing statement will lose priority to another secured party that takes pos-

session of such collateral. See, e.g., §9-328 (certicated securities); §9-330 (tangible chattel paper); §9-331

(negotiable chattel paper generally). To avoid this loss of priority, secured parties often require that the

bailee acknowledge in an authenticated record that the bailee is holding such collateral for the benet of

the secured party. Such authenticated acknowledgment by the bailee will perfect the secured party’s security

interest by possession, thereby ensuring the priority of its security interest (§9-310(b)(6); §9-313).

1. Negotiable Provisions: A Debtor should never permit a third party to have the ability to put it

in default. Therefore, this requirement should be negotiated with respect to whether commercially rea-

sonable efforts are to be used to obtain bailee acknowledgement, the effects of failing to obtain such an

acknowledgement (e.g., Event of Default or decrease in borrowing base) or whether the requirement is

subject to a threshold based on the value of the collateral, individually or in the aggregate.

Security Agreements | 49

2. Example:

If any Possessory Collateral at any time is in the possession of a bailee, the Debtor shall promptly no-

tify the Secured Party thereof and, at the Secured Party’s request and option, shall promptly obtain

an acknowledgement from the bailee, in form and substance satisfactory to the Secured Party, that the

bailee holds such Collateral for the benet of the Secured Party and such bailee’s agreement to comply,

without further consent of the Debtor, at any time with instructions of the Secured Party as to such

Collateral. The Secured Party agrees with the Debtor that the Secured Party shall not give any such

instructions unless an Event of Default has occurred and is continuing.

g. Agreed Security Principles — Overview: Agreed Security Principles are applicable to debtors

organized under the laws of a jurisdiction outside of the United States, any state thereof, or the District of

Columbia. Under some foreign laws, a guaranty and/or grant of a security interest may cause nancial

assistance laws or capitalization rules to become applicable and non-compliance may result in civil or crimi-

nal liability of ofcers and directors of the guarantor and/or Grantor. It may also be difcult to create a

security interest in certain types of collateral, or it can take a long time and the documents may be different

from U.S. security agreements.

1. Negotiable Provisions: Even if the debtor does not have any foreign subsidiaries or collateral located

outside of the United States at the time of closing, the debtor could acquire a foreign subsidiary or move

collateral outside of the United States after closing. Therefore, the debtor should always request the grant

of a security interest be subject to the Agreed Security Principles.

2. Example:

(1) No lien or provision of a guarantee by any person organized outside the United States shall be

made that would result in any breach of corporate benet, nancial assistance, capital preserva-

tion, fraudulent preference, thin capitalization rules, or any other law or regulation (or analogous

restriction) of the jurisdiction of organization of such person, or result in any risk to the ofcers or

directors of such person of a civil or criminal liability; (2) it is expressly acknowledged that in certain

jurisdictions (a) it may be impossible or impractical (including for legal and regulatory reasons) to

grant guarantees or create security over certain categories of assets in which event such guarantees

will not be granted and security will not be taken over such assets or (b) it may take longer than

agreed upon to grant guarantees or create security over certain categories of assets in which event

the Collateral Agent will act reasonably in granting the necessary extension of timing for obtaining

such guarantees or security, provided that in each case, with respect to subclauses (a) and (b), the

relevant Guarantor has exercised due diligence and reasonable efforts in providing such guarantees

or security; and (3) it is expressly acknowledged that the form of the Security Documents may vary

from the forms attached to the Credit Agreement or Security Documents in order to conform to

local requirements and customs as well as potential impracticality of complying with local require-

ments in respect of every item of collateral.

50 | The Practical Lawyer June 2011

h. Other Actions — Overview: Article 9 generally precludes nancing statements from perfecting a

security interest in goods subject to state certicate of title statutes. Rather, perfection is achieved by com-

pliance with the state’s administering registration and licensing department, which commonly requires a

notation of the lien on the certicate of title.

Similarly, if perfection of collateral is governed by U.S. treaties, statutes, or regulations, the ling of a

nancing statement may not be effective to perfect a security interest in such personal property. Examples

of such collateral include registered copyrights, aircraft, rolling stock, and ship mortgages. Note that some

courts have held that security interests in registered trademarks, even though governed by a federal registra-

tion system, are not perfected by ling with the PTO. In re Together Development Corp., 227 B.R. 439 (Bankr. D.

Mass. 1998). However, secured parties frequently require such ling because it may be necessary to defeat

subsequent purchasers for value.

Security interests in personal property that are excluded from Article 9 (e.g., insurance policies) are per-

fected by complying with applicable state law other than Article 9.

Whereas perfection of a security interest in a government contract is achieved by a properly led -

nancing statement, enforcement of a security interest in such government contract can only be achieved if

the debtor complies with the Federal Assignment of Claims Act of 1940 (FAOCA), 31 U.S.C. §3727 and

41 U.S.C. §15. Further assurance clauses imply future performance and help parties to a contract achieve

their contractual purpose, even though not every required future action is identied therein. They are used

by the secured party to require acts that are not included in the security agreement, but are necessary to

achieve the objective of the security agreement (e.g., to grant and perfect a security interest in collateral and

provide remedies if there is an Event of Default).

1. Negotiable Provisions: The requirement for a debtor to comply with state and federal perfection

and enforcement laws is negotiable. It can be required, for example, only after the continuance of an

Event of Default or only if the value of the personal property exceeds a certain amount.

REPRESENTATIONS, WARRANTIES, AND COVENANTS CONCERNING THE DEBTOR

a. Overview: The representations and warranties conrm information that is necessary for the secured

party to perfect its security interest by ling and to determine whether any earlier lings covering the same

collateral exist. Perfection by ling is accomplished by ling a nancing statement in the state in which the

debtor is located, unless the collateral is timber to be cut or as-extracted collateral, or the nancing state-

ment is led as a xture ling and the applicable real estate is located in another state (§9-301). To le an

effective nancing statement and to search for other secured liens, among other things, the secured party

needs the debtor’s exact legal name and location. See §§9-503(a) and 9-506. For example, if the debtor is a

registered organization organized under state law, as dened in section 9-102, the debtor will be located,

for purposes of Article 9, in the state in which the debtor is organized. §9-307(e). If the debtor is a general

partnership, the debtor will be located in the state in which it has its chief executive ofce (§9-307(b)(2)-(3)).

That or like information (e.g., the debtor’s mailing address, if different from the address of its chief execu-

tive ofce) is also required to be contained on the nancing statement itself in order for the secured party

to avoid the risk of the ling ofce rejecting the ling, or the risk of the secured security interest being

Security Agreements | 51

subordinated to a later secured party or purchaser that relies upon incorrect or missing information in the

nancing statement (§9-338; §9-516(b)(5)).

The debtor should covenant to provide to the secured party notice of the debtor’s change of legal

name, place of business (or chief executive ofce, if the debtor’s location is so determined under section

9-307), type of organization (e.g., if the debtor’s limited partnership converts to a limited liability company)

or jurisdiction of organization (e.g., if the debtor reincorporates in another state). In these situations, the

secured party may need to amend its nancing statement or le a new nancing statement in order to avoid

the lapse of perfection or loss of priority of its security interest. See §9-316(a)(2) (change of debtor’s loca-

tion when the security interest had attached and was perfected at the time of the change); §9-316(a)(3) (a

transferee of the collateral becoming a debtor, or a new debtor becoming bound by the security agreement,

when the security interest had attached and was perfected at the time of the transfer of the new debtor

becoming bound); §9-507(c) (change of debtor’s name); and §9-508(a) (assets acquired by a new debtor after

the new debtor is bound by another debtor’s security agreement). A secured party generally has a minimum

of four months from the date such a change is effective to continue the perfection of its security interest.

Other changes in information reected on the led nancing statement may not need to be amended for

the secured party to preserve the perfection or priority of its security interest. See, e.g., §9-338 (“incorrect at

the time the nancing statement was led”) and §9-507(b). However, the secured party may wish to amend

that information out of caution.

b. Negotiable Provisions: The requirements regarding certain changes are negotiable, including when

the Perfection Certicate needs to be updated, whether a change in debtor’s name, location, or type of

organization is prohibited, or whether notice has to be given prior to such change or after such change. To

maintain its perfected status in any attached security interst, a secured party has a minimum of four months

to le or amend a nancing statement if required, due to a change in, for example, the name or location

of the debtor.

c. Example:

The Debtor has previously delivered to the Secured Party a certicate signed by the Debtor and en-

titled “Perfection Certicate” (the “Perfection Certicate”). The Debtor represents and warrants to

the Secured Party on the date hereof and on each Quarterly Update Date as follows: (a) the Debtor’s

exact legal name is that indicated on the Perfection Certicate and on the signature page hereof; (b) the

Debtor is an organization of the type, and is organized in the jurisdiction, set forth in the Perfection

Certicate; (c) the Perfection Certicate accurately sets forth the Debtor’s organizational identication

number or accurately states that the Debtor has none; (d) the Perfection Certicate accurately sets forth

the Debtor’s place of business or, if more than one, its chief executive ofce, as well as the Debtor’s

mailing address, if different; (e) all other information set forth on the Perfection Certicate pertaining

to the Debtor is materially accurate and complete; and (f) other than as disclosed from time to time as

required hereby, there has been no change in any of such information since the date on which the Per-

fection Certicate was signed by the Debtor.

The Debtor covenants with the Secured Party as follows: the Debtor shall provide notice to the Se-

cured Party (i) on or before the earlier of the rst Quarterly Update Date or 90 days after (a) changes to

52 | The Practical Lawyer June 2011

Debtor’s name and (b) changes to Debtor’s type of organization, jurisdiction of organization, or other

legal structure; and (ii) on or before the rst Quarterly Update Date following changes to Debtor’s orga-

nizational identication number (if it has one) or if it obtains an organizational identication number

(if it does not yet have one).

REPRESENTATIONS, WARRANTIES, AND COVENANTS

CONCERNING THE COLLATERAL

a. Overview: The debtor typically represents and warrants to the secured party that: the debtor has suf-

cient rights in, or power to transfer rights in, the collateral for the secured party’s security interest to attach

(§9-203(b)(2)); the collateral is either not encumbered or, if encumbered, the encumbrances are permitted

under the credit agreement (“Permitted Liens”); and the debtor will take all actions necessary to ensure

continued perfection of the secured party’s security interest in the collateral, including (if applicable) actions

necessary to perfect a security interest in after-acquired collateral.

If any of the collateral constitutes “farm products,” as dened in section 9-102(a)(34), the debtor should

inform the secured party, so that the secured party can decide whether to take appropriate steps to obtain

governmental consents under federal agricultural entitlement programs, to obtain waivers or subordina-

tions from suppliers whose claims for unpaid purchase prices for agricultural supplies may have priority un-

der federal law (e.g., the Packers and Stockyards Act of 1921, 7 U.S.C. §196, and the Perishable Agricultural

Commodities Act of 1930, 7 U.S.C. §499e(c)), or to preserve its security interest, or the proceeds thereof, fol-

lowing the disposition of the farm product collateral under the Food Security Act of 1985, 7 U.S.C. §1631.

If any of the accounts or other rights to payment comprised in the collateral are owned by governmental

account debtors, the debtor should inform the secured party, and the secured party may wish to take steps

under the FAOCA or any similar state statute to receive payments directly from the governmental account

debtors.

The secured party may request a representation and warranty that the debtor has complied with labor

and environmental laws where failure of the debtor to comply may result in a superior claim against, or

interest in, the collateral. There is often an analogous representation and warranty in the credit agreement

— the two should be drafted consistently. Similarly, other representations, warranties, and covenants may

be covered in both documents, including those relating to insurance, inspection, books and records, and

disposition of collateral. If covered in both the credit agreement and the security agreement, it is crucial

that the provisions be the same.

Some security agreements include a representation and covenant that all subsidiaries that are limited

partnerships and limited liability companies have opted into Article 8 of the U.C.C., so that all limited

partnership interests and the limited liability company interests are Article 8 securities rather than general

intangibles, thereby enabling the secured party to perfect by ling, possession and/or control, rather than

perfecting only by ling (i.e., general intangibles can only be perfected by ling) (§9-310; §9-313(a); §9-314).

This is because circumstances may change after closing that could affect the characterization of the collat-

eral. A limited liability company’s operating agreement may not, on the closing date, classify the member-

ship interests as “Article 8 securities.” If not so classied, the limited liability company will be a general in-

tangible, and a nancing statement ling is the only method of perfection. If, after the closing, the operating

agreement is amended to provide that the membership interests are Article 8 securities, the secured party

Security Agreements | 53

will be at risk that a subsequent secured party will take a security interest in the membership interests and

perfect the security interest by taking “control.” It is preferable to perfect by obtaining “control” because

a security interest perfected by control will have priority over a security interest perfected by ling (even

when the secured party perfecting by control is aware of the existing security interest perfected by ling)

(§9-328(1)). Perfection by control varies depending upon the type of security involved, but the three general

methods are: (a) becoming the registered owner of the security, (b) taking physical possession of the security

with all necessary endorsements (e.g., stock power, bond power), or (c) in the case of an uncerticated secu-

rity or an account at a brokerage rm, getting a “control” agreement signed by the owner of the security,

the issuer of the security (or, in the case of a brokerage rm, the brokerage rm) and the secured party in

which the issuer of the security (or the brokerage rm) agrees to follow the instructions of the secured party

with regard to the disposition of the security (or securities in the account) without further consent of the

owner of the security (or the securities in the account). See §9-106; §8-106.

b. Negotiable Provisions: Requirements regarding representations and warranties are negotiable and

may be negotiated with respect to whether they are always true, whether they are true on funding dates,

and when they need to be updated. Rather than opting into Article 8, the debtor can covenant not to opt

into it during the term of the loan. It is in debtor’s best interest to keep the representations, warranties,

and covenants limited to perfecting a security interest in the collateral and avoid provisions that deal with

the quality of the collateral and the maintenance of the collateral. Debtors will want quality of collateral

provisions limited by phrases such as “to the extent reasonably likely to cause a material adverse effect” and

maintenance of collateral provisions limited by phrases such as “in debtor’s prudent business judgment to

be decided in good faith.”

c. Example:

The Debtor further represents and warrants to the Secured Party as follows: (a) the Debtor is the owner

of [or has other rights in or power to transfer rights in] the Collateral, free from any right or claim of any per-

son or any adverse lien, security interest or other encumbrance, except for the security interest created

by this Agreement [and Permitted Liens]; (b) [other than as disclosed on the Quarterly Update Dates,] none of the

Collateral constitutes, or is the proceeds of, “farm products” as dened in §9-102(a) of the Uniform

Commercial Code of the State; (c) [except for (describe) and other than as disclosed on the Quarterly Update Dates,]

none of the account debtors or other persons obligated on any of the Collateral is a governmental

authority owing in excess of $_______ annually, covered by the FAOCA or like federal, state or local

statute or rule in respect of such Collateral; (d) the Debtor holds no Commercial Tort Claims except as

indicated on the Perfection Certicate and [other than as disclosed on the Quarterly Update Dates; (e) the Debtor

has at all times operated its business in compliance with laws to the extent required by Section __ of the Credit Agreement];

(f) all other information set forth on the Perfection Certicate pertaining to the Collateral is materially

accurate and complete; [and] (g) there has been no change in any of such information since the date on

which the Perfection Certicate was signed by the Debtor other than as disclosed [; and (h) the Memoran-

dum of Grant of Security Interest in Copyrights identies all now existing material registered copyrights and other rights

in and to all material registered copyrightable works of the Debtor, identied, where applicable, by title, author and/or

Copyright Ofce registration number and date].

54 | The Practical Lawyer June 2011

The Debtor further covenants with the Secured Party as follows: (a) other than in the ordinary

course of business, the Collateral, to the extent not delivered to the Lender pursuant to Section __, will

be kept at those locations listed on the Perfection Certicate and the Debtor will not remove a material

portion of the Collateral from such locations, without providing at least 30 days’ prior written notice to

the Secured Party; (b) except for the security interest herein granted [and Permitted Liens], the Debtor shall

be the owner of [or have other rights in] the Collateral free from any right or claim of any other person or

any lien, security interest, or other encumbrance, and the Debtor shall defend the Collateral against all

claims and demands of all persons at any time claiming the Collateral or any interests therein materi-

ally adverse to the Secured Party; (c) the Debtor shall not pledge, mortgage or create, or suffer to exist,

any right of any person in or claim by any person to the Collateral, or any security interest, lien, or

other encumbrance in the Collateral in favor of any person, or become bound (as provided in section

9-203(d) of the Uniform Commercial Code of the State or any other relevant jurisdiction or otherwise)

by a Security Agreement in favor of any person as Secured Party, other than the Secured Party [and

Permitted Liens]; (d) to the extent deemed prudent business conduct (to be determined by the Debtor in

its good faith discretion), the Debtor will keep the Collateral in good order and repair; (e) [as provided in

the Credit Agreement,] the Debtor will permit the Secured Party, or its designee, to inspect the Collateral at

any reasonable time, wherever located; (f) [except as otherwise provided in the Credit Agreement,] the Debtor will

pay promptly when due all taxes, assessments, governmental charges and levies upon the Collateral or

incurred in connection with the use or operation of such Collateral or incurred in connection with this

Agreement; (g) the Debtor will continue to operate its business in compliance with all laws as required

by Section __ of the Credit Agreement; (h) other than in the ordinary course of business, the Debtor

will not sell or otherwise dispose of, or offer to sell or otherwise dispose of, the Collateral or any interest

therein [except as permitted by the Credit Agreement][if an Event of Default has occurred and is continuing] [except

sales or other dispositions of equipment consistent with prudent business practices] [; and (i) on or before the rst Quarterly

Update Date following the Debtor’s acquisition thereof, to provide to the Secured Party like identications of all material

registered copyrights and other rights in and to all material registered copyrightable works hereafter acquired by the Debtor,

and to execute and deliver to the Secured Party a supplemental Memorandum of Grant of Security Interest in Copyrights,

in form and substance satisfactory to the Secured Party, modied to reect such subsequent acquisitions and registrations].

EXPENSES INCURRED BY THE SECURED PARTY

a. Overview: If the secured party incurs expenses to protect the collateral (e.g., cost of repairs, ling fees,

insurance premiums), such expenses usually are added to the debt and secured by the collateral. Interest

on these expenses usually is also included, because such expenses are considered an involuntary advance.

Reasonable expenses incurred by the secured party to protect the collateral are almost always paid for by

the debtor in secured transactions.

b. Negotiable Provisions: Parties frequently negotiate whether such expenses must be reasonable and

documented.

Security Agreements | 55

RIGHTS OF SECURED PARTY PURSUANT TO SECTION 9-207(c)(3)

a. Overview: The secured party has the right pursuant to section 9-207(c)(3) to create a security interest

for the benet of its lenders in any collateral in its possession or control pursuant to sections 9-104, 9-105,

9-106, or 9-107.

b. Negotiable Provisions: To avoid the risk of losing ownership of a debtor’s subsidiary (or other con-

sequences), the debtor should get the secured party to waive its rights under section 9-207(c)(3). Note that

if there is more than one secured party and a collateral agent has possession or control pursuant to sections

9-104, 9-105, 9-106 or 9-107, there is no need to get such a waiver because the collateral agent must hold

such collateral for the benet of the secured parties.

REMEDIES AND STANDARDS FOR EXERCISING REMEDIES

a. Overview: The secured party’s rights upon the debtor’s default are generally set forth in Part 6 of Ar-

ticle 9, which gives three types of rights:

• Rights provided for in the security agreement;

• Rights provided for in Part 6 of Article 9 (including collecting or obtaining performance from third par-

ties, foreclosure, and strict foreclosure); and

• Judicial procedures (but it is often helpful, especially in the case of non-Article 9 personal property col-

lateral, for the debtor to acknowledge in the security agreement the rights of the secured party).

The secured party, in turn, owes various duties to the debtor. See §9-602. Many of these duties may not be

waived by the debtor, in the security agreement or otherwise, or may be waived by the debtor only after

default.

Many security agreements set forth a period of time which the parties agree to be “reasonable” to

provide the debtor advance notice of the disposition of collateral by the secured party (§9-612(a)). Article

9 provides a “safe harbor” such that 10 days’ prior notice is per se reasonable in a transaction in which the

debtor is not a consumer (§9-612(b)).

Although many of the secured party’s duties to the debtor may not be waived by the debtor in the secu-

rity agreement or otherwise, or may be waived by the debtor only after default, there is no reason why the

parties may not agree in the security agreement to “not manifestly unreasonable” standards for the secured

party to fulll those duties. See §9-603. Such standards may include setting forth the publications in which

advertising of a public disposition of the collateral should be placed, the identity and bidders to be solicited

in a private sale, or particular markets in which collateral dispositions should be made. If the secured party

has determined a “reasonably convenient” location where, after default, the debtor should assemble the

collateral and make it available to the secured party, and that determination is not “manifestly unreason-

able,” the location may be set forth in the security agreement. See §9-603(a); §9-609(c). When reviewing such

provisions, debtor’s counsel needs to be cognizant of the enforceability opinion that the secured party will

likely require as a condition of closing.

56 | The Practical Lawyer June 2011

After default, there are three general remedies which may be exercised. It is best practice for the secured

party to accelerate the loan before exercising any remedies to ensure that the default covers all of the se-

cured obligations.

1. Sell the collateral.

Section 9-610 permits the secured party to sell, lease, license, or otherwise dispose of any or all of the

collateral in its present condition or following any commercially reasonable preparation or processing.

Every aspect of the sale must be commercially reasonable. Failure to sell the collateral in a commercially

reasonable manner will adversely affect the ability of the secured party to collect any deciency and will

expose the secured party to damages (§9-625; §9-626).

The sale can be accomplished through a public disposition or a private disposition. Article 9 does not

dene the term “public disposition,” but the Ofcial Comments indicate that it is one at which the price

is determined after the public has had a meaningful opportunity for competitive bidding. “Meaningful

opportunity,” according to the Comments, is meant to imply that some form of advertisement or public

notice must precede the sale or other disposition, and that the public must have access to the sale or

disposition (comment 7 to §9-6100).

The secured party cannot purchase the collateral at a private disposition unless the collateral is of a

kind that is customarily sold on a recognized market or the subject of widely distributed standard price

quotations. See Comment 7 to §9-610(c).

2. Negotiate a partial or full strict foreclosure with the debtor after default.

Section 9-620 provides a procedure in which the debtor and secured party can agree to transfer some

or all of the collateral to the secured party in satisfaction of some or all of the obligations secured by

the collateral.

There is a procedure that must be followed, and the rules are technical. The procedure requires an

agreement after default to accept the collateral and notice given of the transaction to persons having

a security interest in the collateral (who can block the transaction). If the transaction is completed, the

transaction transfers title to the secured party and discharges any subordinate liens. §9-622. However,

section 1-304 imposes an obligation of good faith on the secured party in enforcing its rights, and this

obligation cannot be disclaimed. See also §1-302. Comment 11 to section 9-620 states that a proposal

and acceptance made under section 9-620 in bad faith (e.g., accepting $1 million of collateral for a $10

debt) would not be effective.

Potential pitfalls when foreclosing on limited liability and partnership interests include:

• Transfer restrictions;

• Absence of the right to cause the admission of the purchaser as a partner/member;

• Capital contribution obligations that may be imposed on the new partner/member;

Security Agreements | 57

• Illiquidity (purchaser may not have a right to distributions or to resell);

• Securities law considerations in conducting a sale; and

• Lack of limited liability if this is a general partnership or general partnership interest as collateral

if formalities are not observed.

3. Collect from third parties after default.

If the collateral consists of rights to payment or performance by third parties, the secured party may

collect from, or obtain performance by, the third parties. Note that if the third party obligor is paying

the debtor in installments this can take a long time. Secured parties can exercise their control and sweep

all funds from controlled deposit accounts and nancial assets from controlled securities accounts. See

§9-607.

Typically, the security agreement will provide that after the occurrence and continuance of an Event of

Default, a secured party may:

• Accelerate the payment of the Obligations “without further notice or demand on the debtor”; and

• Have the right to take possession of the collateral in any jurisdiction in which enforcement is sought,

in addition to all rights and remedies of a secured party under the U.C.C. of the State or any other

relevant jurisdiction, and any additional rights and remedies as may be provided by applicable law.

As noted, Article 9 provides 10 days’ notice of sale as a safe harbor for notice requirements. Therefore,

the security agreement typically provides for 10 days’ notice. The security agreement may also indicate

what is agreed to be commercially reasonable (e.g., regarding advertising, notice, location of sale).

b. Negotiable Provisions: To the extent the Remedies section of the security agreement conforms to

Part 6 of Article 9, this section is minimally negotiated. However, make certain that all provisions are in

compliance with Article 9; for example, don’t permit the waiver of any rights that are not waivable under

Article 9. See §9-602.

c. Example:

After an Event of Default has occurred and is continuing, the Secured Party shall, without any other

notice to or demand upon the Debtor, thereafter have in any jurisdiction in which enforcement hereof is

sought, in addition to all other rights and remedies, the rights and remedies of a secured party under the

Uniform Commercial Code of the State or any other relevant jurisdiction and any additional rights and

remedies as may be provided by applicable law, including the right to take possession of the Collateral,

and for that purpose the Secured Party may, so far as the Debtor can give authority therefor, enter upon

any premises on which the Collateral may be situated and remove the same therefrom. The Secured

Party may in its discretion require the Debtor to assemble all or any part of the Collateral at such loca-

tion or locations within the jurisdiction(s) of the Debtor’s principal ofce(s) or at such other locations as

the Secured Party may reasonably designate. Unless the Collateral is perishable or threatens to decline

speedily in value or is of a type customarily sold on a recognized market, the Secured Party shall give

58 | The Practical Lawyer June 2011

to the Debtor at least ten (10) days’ prior written notice of the time and place of any public sale of

Collateral or of the time after which any private sale or any other intended disposition is to be made.

The Debtor hereby acknowledges that ten (10) days’ prior written notice of such sale or sales shall be

reasonable notice. In addition, the Debtor waives any and all rights that it may have to a judicial hearing

in advance of the enforcement of any of the Secured Party’s rights and remedies hereunder, including,

without limitation, the Secured Party’s right after an Event of Default has occurred and is continuing, to

take immediate possession of the Collateral and to exercise its rights and remedies with respect thereto.

To the extent that applicable law imposes duties on the Secured Party to exercise remedies in a com-

mercially reasonable manner, the Debtor acknowledges and agrees that it is not commercially unrea-

sonable for the Secured Party: (a) to fail to incur expenses reasonably deemed signicant by the Secured

Party to prepare Collateral for disposition or otherwise to complete raw material or work in process into

nished goods or other nished products for disposition; (b) to fail to obtain third-party consents for

access to Collateral to be disposed of, if not required by other law; (c) to fail to obtain governmental or

third-party consents for the collection or disposition of Collateral to be collected or disposed of; (d) to

fail to exercise collection remedies against account debtors or other persons obligated on Collateral or

to remove liens or encumbrances on or any adverse claims against Collateral; (e) to exercise collection

remedies against account debtors and other persons obligated on Collateral directly or through the use

of collection agencies and other collection specialists; (f) to advertise dispositions of Collateral through

publications or media of general circulation, whether or not the Collateral is of a specialized nature; (g)

to contact other persons, whether or not in the same business as the Debtor, for expressions of interest

in acquiring all or any portion of the Collateral; (h) to hire one or more professional auctioneers to as-

sist in the disposition of Collateral, whether or not the Collateral is of a specialized nature; (i) to dispose

of Collateral by utilizing Internet sites that provide for the auction of assets of the types included in

the Collateral or that have the reasonable capability of doing so, or that match buyers and sellers of

assets; (j) to dispose of assets in wholesale rather than retail markets; (k) to disclaim disposition warran-

ties; (l) to purchase insurance or credit enhancements to insure the Secured Party against risks of loss,

collection or disposition of Collateral or to provide to the Secured Party a guaranteed return from the

collection or disposition of Collateral; or (m) to the extent deemed appropriate by the Secured Party,

to obtain the services of brokers, investment bankers, consultants and other professionals to assist the

Secured Party in the collection or disposition of any of the Collateral. [Specify other standards appli-

cable to any specic type of Collateral.] The Debtor acknowledges that the purpose of this Section is

to provide nonexhaustive indications of what actions or omissions by the Secured Party would not be

commercially unreasonable in the Secured Party’s exercise of remedies against the Collateral and that

other actions or omissions by the Secured Party shall not be deemed commercially unreasonable solely

on account of not being indicated in this Section. Without limitation upon the foregoing, nothing con-

tained in this Section shall be construed to grant any rights to the Debtor or to impose any duties on the

Secured Party that would not have been granted or imposed by this Agreement or by applicable law in

the absence of this Section.

Security Agreements | 59

SURETYSHIP WAIVERS

Waiver of notice of loans made, extensions of due dates, failure to perfect, and release of collateral are

relevant only if the debtor is not the borrower (e.g., if debtor is granting a security interest in its assets to

secure a loan to its subsidiary).

NOTICES

The U.C.C. distinguishes the act of giving notice from the receipt of notice. Such notice provisions allocate

risks depending on whether the notice is deemed given upon delivery or upon receipt. Some of the provi-

sions to consider include whether notice has to be in writing or can be oral, whether notice must be signed

by a certain party, or received by a certain party, and how notice has to be delivered (email, fax, rst class

mail, registered mail, certied mail, overnight carrier), who must receive the notice, and whether the recipi-

ent must sign a receipt.

CONFLICTS

If there is an intercreditor agreement, it should always control if there is a conict between the security

agreement and the intercreditor agreement.

POST-CLOSING

a. Overview: Frequently, conditions precedent to closing, for example, requirements for delivery of con-

trol agreements and landlord waivers, are modied to become post-closing requirements to avoid extended

delays in closing.

b. Negotiable Provisions: Certain provisions are crucial for debtors, including giving the collateral

agent the sole discretion to extend such time period to satisfy such post-closing requirements if there is more

than one secured party. In addition, debtors do not want to risk allowing third parties the power to put them

in default. Thus, debtors should try to obtain a Commercially Reasonable Efforts standard for delivery of

post-closing requirements.

TERMINATION

a. Overview: Liens should automatically be released upon payment in full of the Obligations and termi-

nation of the commitment to extend credit. Exceptions include letters of credit that get cash collateralized

rather than terminated and indemnities that survive the termination of the credit agreement. Note that in

the case of consumer goods, a secured party has an afrmative duty to le a termination statement. In non-

consumer goods contexts, if the secured party does not terminate or authorize the termination of nancing

statements within 20 days after it receives an authenticated demand from the debtor, the debtor may le the

termination statement if the termination statement indicates the debtor authorized such ling. See Com-

ment 6 to §§9-509 and 9-513(c).

60 | The Practical Lawyer June 2011

b. Example:

Upon the indefeasible payment in full of the Obligations that are due and payable, including the cash

collateralization, expiration, or cancellation of all Obligations, if any, consisting of letters of credit,

and the full and nal termination of any commitment to extend any nancial accommodations under

the Credit Agreement, the security interests granted herein shall automatically terminate and all rights

to the Collateral shall revert to Debtor. Upon any such termination, Secured Party will, at Debtor’s

expense, execute and deliver to Debtor such documents as Debtor shall reasonably request to evidence

such termination. Such documents shall be prepared by Debtor and shall be in form and substance

reasonably satisfactory to Secured Party.

CHOICE OF LAW PROVISIONS

a. Overview:

1. Governing Law: Article 9 provides the rules for determining what law governs perfection because

third parties need certainty in where to look to obtain notice of a lien. The parties to a security agree-

ment (with certain exceptions) cannot pick the law that governs perfection.

2. General Rules for Law Governing Perfection: In general, the law of the jurisdiction in which

the debtor is “located” will govern the perfection of security interests by ling (§9-301). Section 9-307

outlines the determination of where a debtor is “located”:

• Individuals are located in the jurisdiction of the location of their principal residence (§9-307(b)

(1)). It may be difcult to determine a debtor’s principal residence if the debtor has more than

one residence. If representing the secured party, it is best to le in all jurisdictions where the

debtor has a residence, driver’s license, voting card, or state identication card;

• Registered organizations organized under state law are located in the state under the laws of

which they are organized (§9-307(e)). Not every entity organized under state law is a “registered

organization.” Generally, these entities include corporations, limited liability companies, limited

partnerships, and other entities that are organized solely under the law of a single state and for

which the state must maintain a public record showing that the entity has been organized (§9-

102(a)(70)). General partnerships typically do not meet this denition. Registered organizations

organized under federal law may be located, variously, in the state designated by federal law, in

the state designated as its location, or in the District of Columbia (§9-307(f));

• Foreign entities are located in the jurisdiction of the location of their place of business (or chief

executive ofce, if the entity has more than one place of business), if such location is in a juris-

diction whose law generally requires information concerning the existence of a nonpossessory

security interest to be made generally available in a ling, recording, or registration system as

a condition to the security interest obtaining priority over the rights of other lien creditors (a

notice ling system similar to Article 9). If the location is not in a jurisdiction with a notice ling

system similar to ours, the debtor is deemed located in the District of Columbia (§9-307(b)-(c)).

Security Agreements | 61

If the foreign jurisdiction has not adopted Article 9 or a previous version of Article 9 it is safest

to le with the District of Columbia and retain foreign counsel to perfect the security interest

under foreign law; and

• “Fallback Rule”/Other entities (e.g., general partnerships): Organizations are located in the ju-

risdiction of the location of their place of business; organizations with more than one place of

business are located in the location of their chief executive ofce.

3. Special Rules — Bank Accounts: The law of the depository institution’s “jurisdiction” governs

the perfection of a security interest in a deposit account maintained by the debtor with that bank (§9-

304(a)). Although there are several rules to determine this, the parties (i.e., the bank and the debtor)

can pick the “jurisdiction” for purposes of section 9-304(b). As noted below, the only method by which

to perfect a security interest in a bank deposit account is by obtaining “control” of that account.

Typically this will be accomplished through an “account control agreement” among the debtor, the

secured party and the depository institution or it is accomplished automatically if the secured party is

the depository institution. The account control agreement should state the law that governs perfection.

4. Perfection by Possession: The law of the jurisdiction where the collateral is located governs the

perfection of collateral that is perfected by possession.

GOVERNING LAW AND FORUM DESIGNATION CLAUSES

a. Overview: Most contracts designate a particular state’s law to govern the contractual relationship and

provide for application of such law in resolving disputes that arise out of such contracts, including whether

the security interest has attached and the rights of enforcement. Such governing law provisions provide

a degree of predictability of how the contract will be interpreted and how disputes will be resolved. The

designated state should bear some relationship to the contract (e.g., where parties conduct business, where

contract was negotiated, where performance occurs). If there is no such relationship, there is a risk that such

governing law provision will be unenforceable.

The forum designation clause works together with the governing law provision to maximize the predictabil-

ity of interpreting contractual provisions and resolving disputes. The forum does not need to be the same as

the state of the designated governing law (though it is preferable to ensure that a court is interpreting its own

state’s laws rather than the law of another state). The forum designation may be exclusive or non-exclusive:

• Exclusive — the action may be brought only in that jurisdiction. This must be expressed as clearly as

possible. In such circumstances a party can enjoin the opposing party from litigating elsewhere;

• Non-exclusive — serves only as a consent to jurisdiction in a particular forum. An action may be com-

menced elsewhere.

b. Examples:

Example 1: Exclusive Forum Designation

Forum Designation. Any action or proceeding against any of the parties hereto relating in any way to

this Agreement or the subject matter hereof shall be brought and enforced exclusively in the competent

62 | The Practical Lawyer June 2011

courts of New York, and the parties hereto consent to the exclusive jurisdiction of such courts in respect

of such action or proceeding.

Example 2: Exclusive Forum Designation

Designation of Forum. Any suit brought by either party against the other party for claims arising out of

this Agreement shall be brought in the United States District Court for the Southern District of New

York, or in the event that court lacks jurisdiction to hear the claim, in New York State Supreme Court

for New York County.

Example 3: Non-exclusive Forum Designation

Forum Designation; Submission to Jurisdiction. (i) The Debtor agrees that any legal action or proceed-

ing with respect to this Agreement or the transactions contemplated hereby may be brought in any

court of the State of New York, or in any court of the United States of America sitting in New York,

and the Debtor hereby submits to and accepts generally and unconditionally the jurisdiction of those

courts with respect to its respective person and property and irrevocably consents to the service of pro-

cess in connection with any such action or proceeding by personal delivery to the Debtor or by the mail-

ing thereof by registered or certied mail, postage prepaid to the Debtor, at the address for the Debtor.