“Are You Covered When Selling Fruits

and Vegetables? Be Informed About

Product Liability Risk”

Farmers Market Boot Camp Workshops

Hal Pepper

Financial Analysis Specialist

Cookeville, February 16, 2015

Alcoa, February 17, 2015

Greeneville, February 18, 2015

Covington, February 24, 2015

Clarksville, February 25, 2015

Franklin, February 26, 2015

Overview

Introduction to risk

Using liability insurance to manage risk

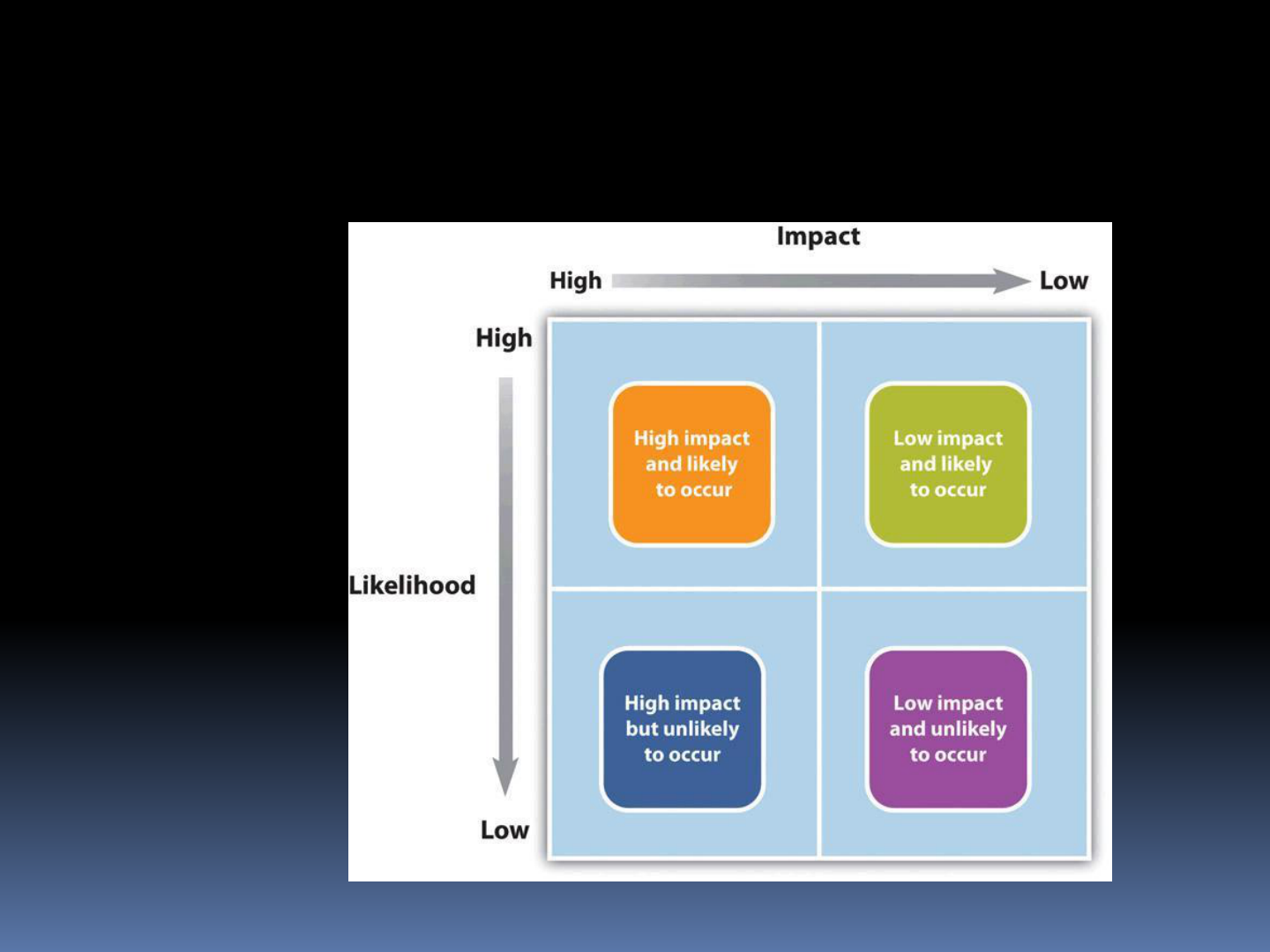

Risk is…

The uncertainty

regarding

likelihood or

magnitude of

loss, damage or

injury

Assessing Risk

Managing Risk

Avoid Risk

Reduce Risk

Transfer Risk Accept Risk

Even with local foods, food

safety is an issue!

Examples of Incidents of

Food-borne Illness

2011 Strawberries Oregon E. coli.

2011 Cantaloupes Colorado Listeria

2012 Cantaloupes Indiana Salmonella

2013 Mixed salad Mexico Cyclospora

2014 Caramel apples Listeria

Transferring Risk with

Insurance

Obtain insurance

Learn and follow

insurance

requirements and

claim procedures

Transferring Risk with Insurance

Start with a visit to a

qualified insurance

agent—preferably one

who is familiar with

how direct farm

businesses operate.

Transferring Risk with Insurance

Explain your operation in detail.

Request an insurance proposal that addresses

all your operation’s risks and potential

amount of loss.

Consider comparing policies from multiple

agents.

Can you add product liability insurance as a

rider to your existing policy?

Transferring Risk with Insurance

Some farmers markets

and vendors require

product liability

insurance.

Ask whether the policy

only covers product

liability arising from

raw/unprocessed farm-

grown products grown

on the farm.

Transferring Risk with Insurance

Does the policy cover

sales at:

Roadside stands?

Farmers markets?

Restaurants?

CSA’s?

Other vendors?

Transferring Risk with Insurance

Does the policy cover

“products and

completed

operations?”

Does the policy cover

sales of:

Products you purchased

for resale?

Processed products?

Are You Covered?

Many general farm liability insurance policies

are written to cover injuries that occur on the

farm premises or as a result of farm

operations. They may not consider direct

marketing activities as “farming” or necessary

operations.

Caution

Many farmers believe their general farm

liability policy provides them with coverage in

the situation where someone gets ill from

eating food the farmer sold them. In many

situations it may not!

Caution

The sale of farm

products you

purchased from

another farmer is likely

NOT covered under a

general farm liability

insurance policy.

Commercial General Liability

(CGL)

Covers activities that a farmer also

undertakes that are not considered “farming”

Written specifically for the business involved

May provide coverage for injuries excluded in

a general farm liability insurance policy

Some points to consider…

Insurance policies are contracts.

Know what you’re paying for.

Understand the exclusions (what the policy

does NOT cover).

Exclusions

Some policies limit the scope of bodily injury.

Example:

“Bodily injury does not include:

The transmission or exposure directly or indirectly

by any insured or by any other person or

instrumentality to any other person of any

communicable disease, bacteria, virus, parasite, or

other organism.”

Product Liability Insurance

Policy

Protects against claims

of injury from fresh or

processed food

products that cause

food-borne illness

Covers “products and

completed operations”

Excess/Umbrella/Surplus Lines

of Insurance

Provide catastrophic

loss protection when

the underlying

insurance is inadequate

Safe Haven???

“No need to worry… I

only sell to friends and

family.”

When you buy an insurance policy…

You are required to pay

the premium at the

time required or the

policy will no longer be

in force.

You are required to

report (in a timely

fashion) any

occurrences to the

agent and company.

When you buy an insurance policy…

You are required to

report any material

changes in the nature

of your activities or the

property which is

subject to insurance.

You are required to

cooperate with the

insurer in matters of

subrogration.

How Much Insurance?

Consider the value of your assets.

Consider the probability of a loss occurring

and the dollar value of potential claims.

What problems have others in farm direct

marketing or agritourism experienced?

What are you doing to reduce the chances of

loss to your business?

Buyers may require a minimum amount of

product liability insurance.

Points to Remember

Make sure the proper entity is insured.

Provide annual sales updates to your agent.

Premiums often are based largely on product

sales and hazards involved.

Reevaluate your coverage annually.

Take Home Messages

Product liability insurance is a vital legal risk

management tool for direct marketers.

Carefully consider needs for coverage.

Work closely with insurance agent and

communicate well and often.

“Thanks” to:

Tennessee Department of Agriculture

Contact Us

Center for Profitable Agriculture

https://ag.Tennessee.edu/cpa

Email [email protected]

(931) 486-2777