© 2013 Fannie Mae. Trademarks of Fannie Mae. SVC-2013-20 Page 1

Servicing Guide Announcement SVC-2013-20

October 11, 2013

Delinquency Management and Default Prevention Updates Related to the Consumer

Financial Protection Bureau Mortgage Servicing Rules and Other Servicing

Responsibilities

Fannie Mae is updating delinquency management and default prevention servicing policies impacted by certain

Consumer Financial Protection Bureau (CFPB) rules and regulations that implement the mortgage servicing

provisions of the Dodd-Frank Wall Street Reform and Consumer Protection Act (Dodd-Frank Act). This

Announcement is not, however, intended to address all CFPB servicing requirements adopted in response to

the Dodd-Frank Act. Servicers are expected to comply with all applicable laws including any CFPB-related

mortgage servicing requirements not covered below. Unless stated otherwise, the requirements detailed below

apply to all mortgage loans secured by all property types (i.e., principal residences, second homes, and

investment properties) that are

held in Fannie Mae’s portfolio,

sold to Fannie Mae for cash and subsequently securitized into Mortgage-Backed Security (MBS)

pools (known as Pooled from Portfolio or PFP mortgage loans), or

sold to Fannie Mae in exchange for MBS that are part of an MBS pool serviced under the special

servicing option or a shared-risk MBS pool for which Fannie Mae markets the acquired property.

This Announcement describes policy changes related to the following:

Borrower Inquiries and Error Resolutions Process

Borrower Delinquency Management Model

Payment Change Notification

Borrower Solicitation Letter – 31 Days Delinquent (Form 731)

Acknowledgement of Borrower Response Package (BRP) and Incomplete Information Notice

Evaluation Notice

Appeals Process for the Denials of Mortgage Loan Modifications

Documentation Required for Forbearance

Requesting Approval for a Forbearance Extension

Prereferral to Foreclosure Review

Referral to Foreclosure

Delay in Legal Action

Effective Date

The effective date for this Announcement is January 10, 2014, unless stated otherwise.

© 2013 Fannie Mae. Trademarks of Fannie Mae. SVC-2013-20 Page 2

Borrower Inquiries and Error Resolutions Process

Servicing Guide, Part I, Section 202: Servicer’s Basic Duties and Responsibilities; Section 312:

Borrower Inquiries; Part VII, Section 102: Quality Assurance Program for Delinquency and Default

Prevention; Section 104: Escalated Cases; Section 104.01: Staffing Requirements for Escalated Cases;

Section 104.02: Escalation Resolution Process; Section 104.03: Case Resolution; Section 205.08:

Evaluation Notices; Chapter 3: Delinquency Prevention; Part VIII, Section 102: Prereferral to

Foreclosure Review; Section 103.04: Conventional and RD First-Lien Mortgage Loans; Section

107.01.05: Postponement of Escalated Cases; Section 107.03.01: Certification Prior to Foreclosure Sale

Fannie Mae is eliminating all the requirements for escalated cases in the Servicing Guide.

As a reminder, servicers must have sufficient properly trained staff and adequate controls and quality control

policies and procedures in place to carry out all aspects of their servicing duties and responsibilities under the

Servicing Guide including promptly addressing borrower inquiries and disputes.

In addition to the Servicing Guide requirements (in Part I, Section 202: Servicer’s Basic Duties and

Responsibilities and Section 312: Borrower Inquiries), servicers must ensure that all processes to respond to

borrower inquiries and resolve allegations of servicer errors asserted by borrowers are compliant with

applicable law, including timelines for responding to borrowers and any applicable prohibitions on foreclosure

referral or foreclosure sale.

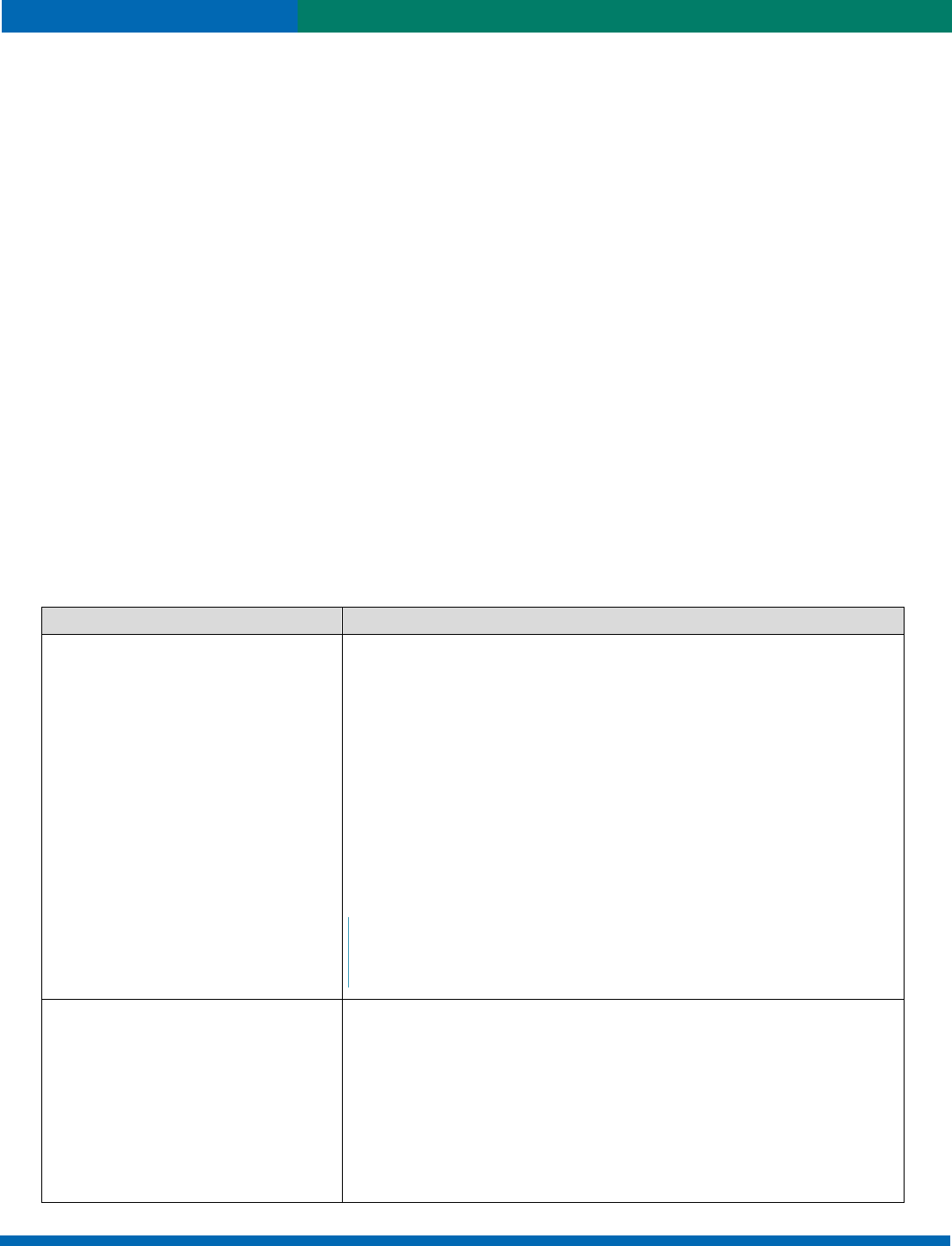

The following table describes the information the servicer must provide the borrower when the borrower makes

an inquiry to determine the owner or assignee of his or her mortgage loan.

If the mortgage loan is…

Then, the servicer must …

a mortgage loan securitized into

a Fannie Mae MBS pool,

indicate the owner of the mortgage loan as “Fannie

Mae in its capacity as Trustee”;

provide the owner contact address of 3900

Wisconsin Ave, NW, Washington, DC, 20016-2892;

provide the contact number of the owner as 1-800-

7FANNIE (1-800-732-6643); and

provide the six-digit pool number as the Trust

identifier. The Fannie Mae Trust identifier for

structured deals is the designated trust name (e.g.,

Fannie Mae REMIC Trust 2005-W2).

NOTE: The six-digit MBS pool number appears in the

Servicer's Reconciliation Facility (SURF

™

) application under

the “VIEW LOAN” screen.

a mortgage loan held in Fannie

Mae’s portfolio,

indicate the owner of the mortgage loan as “Fannie

Mae”;

provide the owner contact address of 3900

Wisconsin Ave, NW, Washington, DC, 20016-2892;

and

provide the contact number of the owner as 1-800-

7FANNIE (1-800-732-6643).

© 2013 Fannie Mae. Trademarks of Fannie Mae. SVC-2013-20 Page 3

Servicers must indicate in their communication to borrowers that the owner status of their loan is based upon

the servicer’s review of its records as of a date certain and that loan ownership status may change from time to

time.

Borrower Delinquency Management Model

Servicing Guide, Part VII, Section 103: Staffing and Training

Fannie Mae is requiring servicers to develop an approach to managing delinquent borrowers that provides

continuity of contact with the borrower and allows a borrower to contact one individual or a dedicated team of

individuals in the servicer’s organization to obtain accurate information on the various workout options

available to the borrower.

When using a team approach, servicers must provide the borrower with the ability to request and speak to, or

leave a message for, a specific person from the assigned team.

Payment Change Notification

Servicing Guide, Part IV, Chapter 4: Notices to the Borrower; Part VII, Section 207: Payment Change

Notification, and the Payment Change Notification Guidelines exhibit

The servicer of an adjustable-rate mortgage (ARM) loan must adhere to the notification timeframes in the

Payment Change Notification Guidelines exhibit (available on Fannie Mae’s website), in addition to any

requirements under applicable law or the security instrument, which may have different notice requirements.

Furthermore, all servicers must abide by the Payment Change Notification Guidelines for all payment changes

(not just for dramatic payment increases, as previously required).

Fannie Mae is removing language in Part IV, Chapter 4: Notices to the Borrower of the Servicing Guide that

states that the notification be mailed in time to reach the borrower at least 60 days before the new monthly

payment becomes effective.

Borrower Solicitation Letter – 31 Days Delinquent (Form 731)

Servicing Guide, Part VII, Section 203: Outbound Call Attempts; Section 204: Behavioral Model Tool;

Section 205.01 Borrower Solicitation Letters; Collection Call Guidelines Exhibit and Letters and

Notices Guidelines Exhibit

Servicers using a Behavioral Model Tool are now required to mail the first Borrower Solicitation Letter – 31

Days Delinquent (Form 731) between days 31 to 35 of delinquency, regardless of the results of the Behavioral

Model Tool. Servicers can still use the results of a Behavioral Model Tool to manage their collection call

campaigns as permitted by the Servicing Guide.

Servicers are reminded that if the borrower does not respond to the first Borrower Solicitation Letter or the

servicer has been unable to achieve Quality Right Party Contact (QRPC), the servicer must send the second

Borrower Solicitation Letter – 61 Days Delinquent (

Form 761) between days 61 to 65 of delinquency. All

Borrower Solicitation Letters must comply with applicable law.

© 2013 Fannie Mae. Trademarks of Fannie Mae. SVC-2013-20 Page 4

Acknowledgement of Borrower Response Package (BRP) and Incomplete Information

Notice

Servicing Guide, Part VII, Section 205.06: Acknowledgement of Borrower Response Package; Section

205.07: Incomplete Information Notices

Fannie Mae is eliminating the option for servicers to provide verbal acknowledgement of receipt of a BRP.

Servicers must provide written, rather than verbal, acknowledgement of the receipt of a BRP within five

business days of its receipt. If the BRP is incomplete, the servicer has the discretion to combine the Incomplete

Information Notice with the acknowledgement of the BRP. The acknowledgment of the BRP and Incomplete

Information Notice must also include any other disclosures and information required by applicable law.

Evaluation Notice

Servicing Guide, Part VII, Section 205.08: Evaluation Notices

In addition to the existing requirements in the Servicing Guide, if the Evaluation Notice is provided to the

borrower in response to the first complete BRP relating to a mortgage loan secured by the borrower’s principal

residence and received by the servicer on or after January 10, 2014, the Evaluation Notice must also:

include a denial reason for any mortgage loan modification trial period plan(s) that is not offered to

the borrower; and

inform the borrower of the right to appeal the denial of any mortgage loan modification trial period

plan(s) within 14 days of the date of the Evaluation Notice if the complete BRP is received 90 or

more days prior to a scheduled foreclosure sale (or if the foreclosure sale date is unknown). The

Evaluation Notice must also include the requirements for the borrower to appeal the denial of any

mortgage loan modification trial period plan(s).

The Evaluation Notice Model Clauses posted on

Fannie Mae’s website have been updated (except those

related to short sale and Mortgage Release

™

transactions) to include servicer instructions and related

provisions to cover the above requirements. Servicers are reminded that use of the model clauses is optional;

however, the model clauses reflect a minimum level of information that the servicer must communicate and

illustrate a level of specificity that complies with the requirements of the Servicing Guide. A servicer that elects

to use the model clauses must revise its letter as necessary to comply with applicable law.

The list of possible outcomes provided to the borrower in the Evaluation Notice will no longer include:

Offer Fannie Mae HAFA preforeclosure sale, and

Offer Fannie Mae HAFA deed-in-lieu.

The following outcome will be added:

Non-approval — not eligible for alternative to foreclosure.

Appeals Process for the Denials of Mortgage Loan Modifications

Servicing Guide, Part VII, Chapter 1: Servicing Standards

In addition to existing requirements in the Servicing Guide, servicers are required to develop comprehensive

processes and written policies and procedures to respond to a borrower’s appeal of the denial of any mortgage

loan modification trial period plan solely in connection with a borrower’s first complete BRP that is received

on or after January 10, 2014,

© 2013 Fannie Mae. Trademarks of Fannie Mae. SVC-2013-20 Page 5

90 days or more before a scheduled foreclosure sale or if a foreclosure sale date is unknown, and

with respect to a mortgage loan secured by a principal residence.

The appeal process applies only to a denial of any mortgage loan modification trial period plan(s) if it relates to

the first complete BRP and meets all of the above requirements.

NOTE: A servicer’s appeal decision is final and not subject to further appeal. Foreclosure prevention

alternatives (workout options) that do not require a complete BRP do not have the right to an appeal.

Borrower Requirements Relating to an Appeal

Servicers must confirm that the borrower properly exercised an appeal in connection with a BRP that satisfies

the above requirements by ensuring that the borrower, within 14 days of the date of the servicer’s Evaluation

Notice, provides the servicer with a written request for an appeal that includes the borrower’s name, property

address, and mortgage loan number.

The servicer must inform the borrower that any supporting documentation and specific appeal reason may be

submitted at the time the servicer is notified of the appeal.

Servicer Requirements Relating to an Appeal

Servicers must complete the review of a borrower’s appeal using personnel different from those responsible for

the initial evaluation of and decision on the complete BRP. Servicers must provide written notice of the appeal

decision within 30 days of receipt of the borrower’s appeal.

If the borrower’s appeal is received within the 14-day appeal period,

• the servicer must evaluate the appeal and must accept any new information submitted by the borrower

within this timeframe as part of the independent appeal review (whether the information relates to the

appeal, i.e., modification denial, or a material change of circumstances unrelated to the appeal).

If any new information or documentation submitted by the borrower is received after the 14-day

appeal period in connection with a borrower’s timely appeal but before the appeal decision, or if the

borrower’s appeal is received after the 14-day appeal period,

• the servicer must provide written notice of the appeal decision within 30 days of receipt of the borrower’s

appeal. In these cases, the servicer has the discretion to

o

complete the review with any new information or documentation provided by the borrower as part of

the appeals process; or

o

treat the request along with any additional information as part of a new BRP and review the BRP in

accordance with existing requirements in Part VII, Section 205: Letters and Part VIII, Section 107:

Conduct of Foreclosure Proceedings of the Servicing Guide.

If the borrower elects to appeal, the borrower does not have to accept the initial offer for a workout option until

resolution of the appeal. If, after review of an appeal, the servicer determines that the borrower was eligible for

a loan modification trial period plan for which the borrower had been denied, the servicer must send the

borrower an offer for such loan modification trial period plan. In that case, the borrower may choose to accept

the initial offer, provided that the borrower continues to be eligible for such offer, or the new loan modification

trial period plan offer, and must be given 14 calendar days from the date of the servicer’s appeal decision

notice to indicate their intent to accept either offer. The borrower’s intent to accept an offer may be indicated by

verbal or written notification or by making the first trial period plan payment within 14 days, in accordance with

the Servicing Guide.

If the borrower waits to accept the initial offer until after receiving the appeal decision, the servicer must

© 2013 Fannie Mae. Trademarks of Fannie Mae. SVC-2013-20 Page 6

inform the borrower that the mortgage loan will become more delinquent and that any unpaid

interest and other unpaid amounts, such as escrows for taxes and insurance, will continue to

accrue during the appeal process; and

adjust the payment amounts and due dates of the initial offer accordingly.

If the borrower waits to accept the initial offer until after receiving the appeal decision, the first payment due

date of any new mortgage loan modification trial period plan offer, and the revised first payment due date for

the initial offer, is based on when the appeals decision is sent by the servicer to the borrower, and will follow

the timelines established for loan modification trial period plans in the Servicing Guide, as follows:

If the servicer sends the appeal decision on or before the 15th of the month, then the trial period

plan effective date and the due date of the first trial period payment is the first day of the next

month.

If the servicer sends the appeal decision after the 15th of the month, then the trial period plan

effective date and the due date of the first trial period payment is the first day of the month after the

next month.

The servicer must track and document all information related to appeals in the mortgage servicing file.

Information related to the appeals process must be made available to Fannie Mae upon request.

Documentation Required for Forbearance

Servicing Guide, Part VII, Section 403: Forbearance; Announcement SVC-2013-16: Updates to

Assistance in Disasters

Servicers must obtain and evaluate a complete BRP if the borrower is offered any forbearance plan with a term

greater than six months or if consecutive forbearance extensions exceed six months as measured from the

start of the initial forbearance to the projected end of the forbearance extension.

If the borrower is impacted by a disaster and meets the requirements as outlined in Announcement SVC-2013-

16 that would have made him or her eligible to receive forbearance for a period of longer than six months, the

servicer must initially offer forbearance for six months. If the borrower is unable to provide a complete BRP at

the end of the initial six months of disaster-related forbearance, servicers are allowed to offer successive

disaster-related forbearance plans up to six months in length, but not to exceed 12 months of disaster-related

forbearance in aggregate, without obtaining a complete BRP. Servicers are reminded that any other

forbearance arrangement longer than six months, inclusive of any extension, must receive prior written

approval from Fannie Mae.

Requesting Approval for a Forbearance Extension

Servicing Guide, Part VII, Section 403: Forbearance, and Section 403.02.04: Forbearance Extension;

Announcement SVC-2012-01: Introduction to Unemployment Forbearance

Effective immediately, requests for forbearance extensions will now be reviewed by Fannie Mae’s Loss

Mitigation Department. Servicers must no longer send forbearance extension requests to Portfolio Managers,

Servicing Consultants, or the National Servicing Organization’s Servicer Solutions Center. All new forbearance

extension requests must be submitted to the following mailbox:

forbearance_ext_req[email protected].

The Loss Mitigation Department will notify servicers of decisions on forbearance extension requests via email.

Fannie Mae is also introducing a new form titled, Forbearance Extension Request Form, which is located on

Fannie Mae’s website. For all forbearance extension requests, servicers must complete and submit a

Forbearance Extension Request Form with supporting documentation to Fannie Mae. (This form replaces the

© 2013 Fannie Mae. Trademarks of Fannie Mae. SVC-2013-20 Page 7

Unemployment Forbearance Policy Form formerly used to request extensions for an Unemployment

Forbearance.)

Prereferral to Foreclosure Review

Servicing Guide, Part VIII, Section 102: Prereferral to Foreclosure Review; Section 107.03.01:

Certification Prior to Foreclosure Sale; and Chapter 1, Exhibit 2: Expected Servicer/Attorney (or

Trustee) Interaction

Currently, servicers must perform a prereferral to foreclosure review at least 7 days prior to the date by which

the servicer is required to refer the mortgage loan to foreclosure. Fannie Mae is changing this timeframe.

Servicers must now perform a prereferral to foreclosure review within 15 days prior to the date by which the

servicer is required to refer the mortgage loan to foreclosure.

Referral to Foreclosure

Servicing Guide, Part VII, Section 205.09: Breach or Acceleration Letters; Part VIII, Section 102:

Prereferral to Foreclosure Review; Section 103.04: Conventional and RD First-Lien Mortgage Loans;

Section 107.03.01: Certification Prior to Foreclosure Sale

The following updated requirements for referral to foreclosure are only applicable to mortgage loans secured

by a principal residence.

Servicers must refer the mortgage loan to foreclosure no earlier than day 121 of delinquency but no later than

5 business days after day 121 of delinquency, unless applicable law permits earlier referral. If the servicer

determines, in accordance with applicable law, that the property securing the mortgage loan is not or is no

longer the borrower’s principal residence, the servicer must refer the mortgage loan to foreclosure prior to day

121 of delinquency as stated in the Servicing Guide.

During any prereferral to foreclosure review period or before the servicer has made the first notice or filing

required by applicable law for any judicial or non-judicial foreclosure process, the servicer must not refer the

mortgage loan to foreclosure under any of the following circumstances:

there is an approved payment arrangement for a workout option;

a complete BRP is received and the servicer is within the 30-day time period for evaluating the

BRP;

the servicer has extended an offer for a workout option and the borrower’s response time period

has not expired;

the borrower is conditionally approved for mortgage payment assistance under the federal Hardest

Hit Fund program;

the borrower has accepted an offer for a workout option and is performing in accordance with its

terms; or

the time period for the borrower to exercise any right of appeal as described above has not expired,

the servicer is evaluating the borrower’s appeal, or the time period following the servicer’s appeal

decision for the borrower to accept any offer for a workout option has not expired.

© 2013 Fannie Mae. Trademarks of Fannie Mae. SVC-2013-20 Page 8

Delay in Legal Action

Servicing Guide, Part VIII, Section 103.04: Conventional and RD First-Lien Mortgage Loans; Section

107.01: Servicer-Initiated Temporary Suspension of Proceedings; Section 107.01.01: Borrower

Response Package Received Within 30 Days of Post Referral to Foreclosure Solicitation Letter; Section

107.01.02: Borrower Response Package Received After 30-Day Response Period But Before 37 Days

Prior to the Foreclosure Sale Date; Section 107.01.05: Postponement of Escalated Cases;

Announcement SVC-2012-19: Standard Short Sale/HAFA II and Deed-in-Lieu of Foreclosure

Requirements; Announcement SVC-2012-25: Mortgage Release™ (Standard Deed-in-Lieu of

Foreclosure and Deed for Lease) Requirements and Updates to Standard Short Sale/HAFA II

Requirements

The following updated requirements for delay in legal action are only applicable to the first complete BRP

submitted by the borrower that is

related to a mortgage loan secured by a principal residence, and

received by the servicer on or after January 10, 2014.

If the borrower’s first complete BRP is received after referral to foreclosure and more than 37 days prior to the

foreclosure sale date, then the servicer must delay filing the motion for foreclosure judgment or order of sale,

or if the motion for foreclosure judgment or order of sale has been filed, the servicer must request the court to

delay a hearing or ruling as permitted under state or local law unless

the servicer has reviewed the first complete BRP and delivered an Evaluation Notice to the

borrower stating that the borrower is not eligible for a workout option and, if applicable, the borrower

has not requested an appeal or the borrower’s appeal has been denied in accordance with the

requirements of this Announcement; or

the borrower rejects all workout options offered by the servicer; or

the borrower fails to perform under an agreement on a workout option.

These requirements are applicable to all workout options including short sale and Mortgage Release.

Additional guidance related to short sale and Mortgage Release transactions (including updated Evaluation

Notice Model Clauses) will be published at a later date.

*****

Servicers should contact their Servicing Consultant, Portfolio Manager, or Fannie Mae’s National Servicing

Organization’s Servicer Support Center at 1-888-FANNIE5 (1-888-326-6435) with any questions regarding this

Announcement.

Gwen Muse-Evans

Senior Vice President

Chief Risk Officer for Credit Portfolio Management