© 2022 Fannie Mae. Trademarks of Fannie Mae. 10.7.2022 1 of 35

Confidential‐InternalDistribution

DSCR Guidance Job Aid - Table of Contents

Lender Underwritten DSCR per Guide Requirements: Guidance and

Examples

Page 2 -4 Definitions and detailed explanation of calculation methodologies

Page 4 – 7 Scenarios and calculation examples

Actual DSCR and DSCR at Maximum Payment

**

Fields Retired/Disabled for Mortgage Loan deliveries on or after October 2022**

Page 8 Definitions and detailed explanation of calculation methodologies

Page 8 – 13 Scenarios and calculation examples

Target State DSCR Fields

Page 14 UW NCF DSCR, UW NCF DSCR IO, UW NCF DSCR at Cap and UW NCF DSCR

All In (new fields) - Definitions

Page 15 – 17 Scenarios and calculation examples for Fixed Rate Mortgage Loans

Page 18 – 21 Scenarios and calculation examples for ARM Loans

Page 23 – 28 Scenarios and calculation examples for SARM Loans

Page 29 Review of Credit Facilities - UW NCF DSCR at Facility Level and UW NCF

DSCR IO at Facility Level (new fields) - Definitions

Page 30 Deal 1: Scenario and calculation example for UW NCF DSCR at Facility Level

Page 31 Deal 1: Scenario and calculation example for UW NCF DSCR IO at Facility Level

Page 32 Deal 2: Scenario and calculation example for UW NCF DSCR at Facility Level

Page 33 UW NCF DSCR, UW NCF DSCR IO, UW NCF DSCR at Cap and UW NCF DSCR

All In, UW NCF DSCR at Facility Level and UW NCF DSCR IO at Facility Level -

Summary and Conclusions

© 2022 Fannie Mae. Trademarks of Fannie Mae. 10.7.2022 2 of 35

Confidential‐InternalDistribution

Job Aid: Lender Underwritten DSCR per Guide Requirements:

Guidance and Examples

Information Effective: October 24, 2022

This purpose of this document is strictly for guidance and examples only. This document is not

a replacement for the Multifamily Selling and Servicing Guide (the “Guide”). This guidance and

examples are effective as of October 6, 2017 and are subject to change. Refer to the most recent

Guide and Underwriting Standards (Form 4660) for complete details on the Lender

Underwritten DSCR per Guide Requirements field.

Lender Underwritten DSCR per Guide Requirements

The ratio of underwritten Net Cash Flow (“NCF”) and the underwritten annualized debt service (see below for

more guidance on how to calculate this debt service).

Underwritten Net Cash Flow (Underwritten NCF) = Underwritten Effective Gross Income less

underwritten Property operating expenses including Capital Expenditures (Replacement Reserves) as required

in the Multifamily Selling and Servicing Guide (the “Guide”).

However, for Cooperative Properties, Lender must calculate: (i) Cooperative Market Rental Basis

(“Underwritten NCF”), and (ii) Actual Cooperative Property Basis (“Actual Cooperative Property NCF”), as

follows:

Cooperative Market Rental Basis Net Cash Flow (“Underwritten NCF”): Underwritten NCF calculated

as described above, however, based on a Market Rental Basis as reflected in the Appraisal. The

Cooperative Market Rental Basis NCF must include minimum economic vacancy and Capital

Expenditures (Replacement Reserves) per unit, if any, as set forth in the Underwritten NCF calculation

detailed in Part IIIA, Chapter 3 or Part IIIB, as required in the Guide; and

Actual Cooperative Property Basis Net Cash Flow (“Actual Cooperative Property NCF”): calculated on

actual Cooperative Property operations as required in the Guide.

Underwritten Annualized Debt Service = the following calculations for full and partial interest only

Mortgage Loans:

For Fixed Rate Mortgage Loans:

The annual debt service must be based on a level debt service payment with an Amortization term

pursuant to the Multifamily Underwriting Standards, or other Amortization term approved by Fannie

Mae, and the higher of:

the Gross Note Rate; or

the required Underwriting Interest Rate Floor (as identified in the “Underwriting Standards (Form

4660)”.

© 2022 Fannie Mae. Trademarks of Fannie Mae. 10.7.2022 3 of 35

Confidential‐InternalDistribution

For Adjustable Rate Mortgage Loans (ARM Loans)

1

:

Structured ARM Loans (“SARM Loans”): Based on the underwritten annualized monthly payment

calculation using the overall Variable Underwriting Rate (as defined in Part IIIC Chapter 6 Section

605) of the “Guide”).

ARM 5-5 and ARM 7-6 Loans (i.e. “Embedded Cap ARM Loans”): Based on the annualized monthly

payment calculated using the Maximum Lifetime Interest Rate (as defined in Part IIIC Chapter 5 of

the “Guide”).

For Cooperative Property Mortgage Loans: the underwritten annual debt service must be

calculated as stated above, with the following caveat: Cooperative Market Rental Basis: Debt

service must be based on a level debt service payment with an Amortization term pursuant to

the Multifamily Underwriting Standards, or other Amortization term approved by Fannie Mae,

and the higher of:

the Gross Note Rate; or

the required Underwriting Interest Rate Floor; and

If Fannie Mae pre-approves subordinate debt as provided in the Guide, the annual debt

service must also include principal and interest to cover the maximum principal amount of

the subordinate debt outstanding.

Actual Cooperative Property Basis: Debt service must be based on a level debt service payment

at the actual Gross Note Rate with an Amortization term pursuant to the Multifamily

Underwriting Standards, or other Amortization term approved by Fannie Mae. If Fannie Mae

pre-approves subordinate debt as provided in the Guide, the annual debt service must also

include principal and interest to cover the actual loan balance of such subordinate debt

outstanding at the time of underwriting. Interest-only payments may only be used for a full

term interest-only Mortgage Loan.

For Supplemental Mortgage Loans:

Based on the combined annual debt service amount of all Pre-Existing Mortgage Loans and the

Supplemental Mortgage Loan based on the following:

Pre-Existing Mortgage Loans

Interest Rate Type Amortization Type Debt Service Amount

Fixed Rate Fully-amortizing

Partial-term Interest-Only

Amortizing debt service amount based

on the Gross Note Rate

Full Term Interest-Only Interest-Only debt service amount

based on the Gross Note Rate

Adjustable Rate

1

Fully-amortizing

Partial-term Interest-Only

Amortizing debt service amount based

on the origination loan amount,

amortization term, and variable

underwriting rate

1

In addition to meeting the Lender Underwritten DSCR per Guide requirements described above, in no event shall the Mortgage Loan amount exceed

the amount calculated in Part IIIA of the Guide for a fixed rate Mortgage Loan with equivalent term and Tier and using the Lender delegated pricing

published in the DUS Pricing Memo or, if applicable, the Fannie Mae approved fixed rate pricing for the Mortgage Loan in effect at the time of Rate Lock

© 2022 Fannie Mae. Trademarks of Fannie Mae. 10.7.2022 4 of 35

Confidential‐InternalDistribution

Pre-Existing Mortgage Loans

Full Term Interest-Only Interest-Only debt service amount

based on the origination loan amount,

amortization term, and variable

underwriting rate

Supplemental Mortgage Loan**

Interest Rate Type Amortization Type Underwritten Annualized Debt

Service Amount

Fixed Rate / Adjustable

Rate

2

All Amortization Types Amortizing debt service amount based

on the greater of the Gross Note Rate

or:

for fixed rate Supplemental

Mortgage Loans, the applicable

Underwriting Interest Rate Floor

in the applicable Multifamily

Underwriting Standards; or

for adjustable rate Supplemental

Mortgage Loans, the variable

underwriting rate determined in

accordance with Part IIIC

**Please note, Supplemental Mortgage Loans must comply with New Loan Test in the Guide, which may further restrict

proceeds. Please refer to Part IIIC – Chapter 2 for complete details on Supplemental Mortgage Loans and sizing requirements.

Sample Calculations

Example 1: $10,000,000 Fixed Rate Mortgage Loan (Fully Amortizing)

Conventional Mortgage Loan

Gross Note Rate: 4.00

Underwriting Interest Rate Floor = 5.00

Loan Term: 120 months

Interest Only Term: 0 months

Amortization: 360 months

Underwritten NCF: $1,000,000

Underwritten Debt Service (Amortizing @ 5.00% UW Interest Rate Floor): $53,682 (monthly), $644,186 (annualized)

Lender Underwritten DSCR per Guide Requirements:

1.55 = $1,000,000 / $644,186 (@ UW Interest Rate Floor)

Cooperative Property Mortgage Loan

Gross Note Rate: 4.00

Underwriting Interest Rate Floor = 5.00

Loan Term: 120 months

Interest Only Term: 0 months

Amortization: 360 months

2

In addition to meeting the Lender Underwritten DSCR per Guide requirements described above, in no event shall the Mortgage Loan amount exceed

the amount calculated in Part IIIA of the Guide for a fixed rate Mortgage Loan with equivalent term and Tier and using the Lender delegated pricing

published in the DUS Pricing Memo or, if applicable, the Fannie Mae approved fixed rate pricing for the Mortgage Loan in effect at the time of Rate Lock

© 2022 Fannie Mae. Trademarks of Fannie Mae. 10.7.2022 5 of 35

Confidential‐InternalDistribution

Underwritten NCF (Market Rental Basis): $1,000,000

Actual Cooperative Property NCF: $573,000

Underwritten Debt Service (Amortizing @ 5.00% UW Interest Rate Floor): $53,682 (monthly), $644,186 (annualized)

Debt Service (Amortizing @ 4.00%): $47,742 (monthly), $572,898 (annualized)

Lender Underwritten DSCR per Guide Requirements (Market Rental Basis):

1.55 = $1,000,000 (Market Rental Basis NCF) / $644,186 (@ UW Interest Rate Floor)

Actual Cooperative Property DSCR:

1.0 = $573,000 (Actual Cooperative Property NCF) / $572,898

Example 2: $10,000,000 Fixed Rate Mortgage Loan (Partial Interest Only)

Conventional Mortgage Loan

Gross Note Rate: 4.00

Underwriting Interest Rate Floor = 5.00

Loan Term: 120 months

Interest Only Term: 60 months

Amortization: 360 months

Underwritten NCF: $1,000,000

Underwritten Debt Service (Amortizing @ 5.00% *UW Interest Rate Floor): $53,682 (monthly), $644,186 (annualized)

Lender Underwritten DSCR per Guide Requirements:

1.55 = $1,000,000 / $644,186 (@UW Interest Rate Floor)

Cooperative Property Mortgage Loan

Gross Note Rate: 4.00

Underwriting Interest Rate Floor = 5.00

Loan Term: 120 months

Interest Only Term: 60 months

Amortization: 360 months

Underwritten NCF (Market Rental Basis): $1,000,000

Actual Cooperative Property NCF: $573,000

Underwritten Debt Service (Amortizing @ 5.00% UW Interest Rate Floor): $53,682 (monthly), $644,186 (annualized)

Debt Service (Amortizing @ 4.00%): $47,742 (monthly), $572,898 (annualized)

Lender Underwritten DSCR per Guide Requirements (Market Rental Basis):

1.55 = $1,000,000 (Market Rental Basis NCF) / $644,186 (@UW Interest Rate Floor)

Actual Cooperative Property DSCR:

1.00 = $573,000 (Actual Cooperative Property NCF) / $572,898

Example 3: $10,000,000 Fixed Rate Mortgage Loan (Full Interest Only)

Conventional Mortgage Loan

Gross Note Rate: 4.00

Underwriting Interest Rate Floor = 5.00

Loan Term: 120 months

Interest Only Term: 120 months

Amortization: 360 months

Underwritten NCF: $1,000,000

Underwritten Debt Service (Amortizing @ 5.00% UW Interest Rate Floor): $53,682 (monthly), $644,186 (annualized)

© 2022 Fannie Mae. Trademarks of Fannie Mae. 10.7.2022 6 of 35

Confidential‐InternalDistribution

Lender Underwritten DSCR per Guide Requirements:

1.55 = $1,000,000 / $644,186 (@UW Interest Rate Floor)

Cooperative Property Mortgage Loan

Gross Note Rate: 4.00

Underwriting Interest Rate Floor = 5.00

Loan Term: 120 months

Interest Only Term: 120 months

Amortization: 360 months

Underwritten NCF (Market Rental Basis): $1,000,000

Actual Cooperative Property NCF: $573,000

Underwritten Debt Service (Amortizing @ 5.00% UW Interest Rate Floor): $53,682 (monthly), $644,186 (annualized)

Debt Service (Interest Only @ 4.00%): $33,333 (monthly), $400,000 (annualized)

Lender Underwritten DSCR per Guide Requirements (Market Rental Basis):

1.55 = $1,000,000 (Market Rental Basis NCF) / $644,186 (@UW Interest Rate Floor)

Actual Cooperative Property DSCR:

1.43 = $573,000 (Actual Cooperative Property NCF) / $400,000

Example 4: $10,000,000 ARM Loans

3

:

Please note, ARM Loan examples do not reflect Fixed Rate Test which further may impact proceeds and DSCR calculation,

refer to Guide and Underwriting Standards (Form 4660) for further details.

ARM 7-6 Loan: ARM Loan with embedded interest rate caps

Initial Interest Rate: 2.00 (Guaranty Fee + Servicing Fee + 30 Day Average SOFR index)

Lifetime Max Interest Rate: 8.00 (Initial Interest Rate + 6% embedded interest rate cap)

Loan Term: 84 months

Interest Only Term: 36 months

Amortization: 360

Underwriting NCF: $1,000,000

Debt Service using Lifetime Max Interest Rate: $73,376 (monthly), $880,517 (annualized)

Lender Underwritten DSCR per Guide Requirements:

1.14 = $1,000,000 / $880,517

STRUCTURED ARM Loan

Initial Interest Rate: 2.77 (ex. Margin (Guaranty Fee, Servicing Fee plus Investor spread) + 30 Day Average SOFR index)

Variable Underwriting Rate (as defined in the Guide): 5.77 (Initial Interest Rate + Underwriting Spread (i.e., 3%) + Cap

Cost Factor)

Term: 120 months

Interest Only: 36 months

Amortization: 360 months

Underwriting NCF: $1,000,000

Underwritten Debt Service using Variable Underwriting Rate: $58,484 (monthly), $701,813 (annualized)

Lender Underwritten DSCR per Guide Requirements:

1.42 = $1,000,000 / $701,813

3

In addition to meeting the Lender Underwritten DSCR per Guide requirements described above, in no event shall the Mortgage Loan amount exceed

the amount calculated in Part IIIA of the Guide for a fixed rate Mortgage Loan with equivalent term and Tier and using the Lender delegated pricing

published in the DUS Pricing Memo or, if applicable, the Fannie Mae approved fixed rate pricing for the Mortgage Loan in effect at the time of Rate Lock

© 2022 Fannie Mae. Trademarks of Fannie Mae. 10.7.2022 7 of 35

Confidential‐InternalDistribution

Example 5: Hybrid ARM Loan:

A 5-Year Hybrid ARM Loan for $3,817,000.00 secured by a Property located in a Strong Market or Los Angeles-Long

Beach-Anaheim, CA MSA:

Initial Fixed Interest Rate: 4.11

Underwriting Interest Rate Floor = Not Applicable for Hybrid ARM Loans

Interest Only Term: 0 months

Loan Term: 360 months

Amortization: 360 months

Underwritten NCF: $277,000

Underwritten Debt Service (Amortizing @ 4.11%): $18,466 (monthly), $221,590 (annualized)

Lender Underwritten DSCR per Guide Requirements:

1.25 = $277,000 / $221,590 (@ Actual Interest Rate)

A 7-Year Hybrid ARM Loan for $1,720,000.00 secured by a Property located in a Nationwide Market:

Initial Fixed Interest Rate: 4.18

Minimum 1.00 DSCR Stress Test: 6.68 (Initial Fixed Interest Rate of 4.18 plus 2.50)

Underwriting Interest Rate Floor = Not Applicable for Hybrid ARM Loans

Underwritten Value: $2,150,000.00

Interest Only Term: 0 months

Loan Term: 360 months

Amortization: 360 months

Underwritten NCF: $142,140

Maximum Loan Amount per LTV at 80%: $1,720,000.00

Maximum Loan Amount minimum 1.00 DSCR Stress Test @ 6.68: $1,839,425

Underwritten Debt Service (Amortizing @ 4.18%) at maximum constrained loan proceeds $1,720,000.00: $8,391

(monthly), $100,692 (annualized)

Lender Underwritten DSCR per Guide Requirements:

1.41 = $142,140 / $100,692 (@ Actual Interest Rate)

Example 6: Supplemental Mortgage Loan:

Please note, Supplemental Mortgage Loans must comply with New Loan Test in the Guide, which may further restrict

proceeds. Please refer to Part IIIC – Chapter 2 for complete details on Supplemental Mortgage Loans and sizing

requirements.

Underwriting NCF = $1,400,000

Loan Amount and Loan Term Rate / Amortization / Interest Only Annualized Debt Service

Pre-Existing

Mortgage Loan

$10,000,000 Origination UPB; 5

years remaining

Gross Note Rate = 5.50%; Amortization

= 360 months; Interest Only = 0 months

$681,347

Supplemental

Mortgage Loan

$5,000,000; 5 years Gross Note Rate = 5.00%; UW Interest

Rate Floor = 6.75%; Interest Only = 0

months

$389,159 (@UW Interest

Rate Floor)

Total Combined Annualized Debt Service $1,070,506

© 2022 Fannie Mae. Trademarks of Fannie Mae. 10.7.2022 8 of 35

Confidential‐InternalDistribution

Lender Underwritten DSCR per Guide Requirements:

1.31 = $1,400,000 / $1,070,506

1

In addition to meeting the Lender Underwritten DSCR per Guide requirements described above, in no event shall the Mortgage Loan amount

exceed the amount calculated in Part IIIA of the Guide for a fixed rate Mortgage Loan with equivalent term and Tier and using the Lender delegated

pricing published in the DUS Pricing Memo or, if applicable, the Fannie Mae approved fixed rate pricing for the Mortgage Loan in effect at the time

of Rate Loc

k

© 2022 Fannie Mae. Trademarks of Fannie Mae. 10.7.2022 9 of 35

Confidential‐InternalDistribution

Job Aid: DSCR Training Aid for Currently Disclosed DSCR Fields

**Fields Retired/Disabled for Mortgage Loan deliveries on or after October

2022**

Actual DSCR

Actual DSCR is the ratio of underwritten Net Cash flow (“NCF”) and the annualized debt service.

UW NCF = Underwritten Effective Gross Income less underwritten Total Expenses.

Annualized Debt Service = For full and partial interest only Mortgage Loans use Initial Interest Rate

multiplied by Actual UPB at Acquisition. For amortizing 30/360 and Actual/360 Mortgage Loans use monthly

payment as stated in the Loan Documents multiplied by 12.

Product Variations:

Partial and Full Interest Only Mortgage Loans: this calculation will not include an amortization

factor.

ARM Loans/Hybrid ARM Loans: this calculation will be based on the initial interest rate.

Cooperative Properties: Actual cooperative NCF effective gross income less underwritten Total

Expenses.

Supplemental Mortgage Loans and Mortgage Loans with Subordinate Debt or Additional

Debt (Combined): The ratio of Underwritten Net Cash Flow (UW NCF) to the annualized combined

monthly payments of all Pre-Existing Mortgage Loans.

Combined monthly payments = the combined monthly payments for all supplemental, subordinate

debt, and first liens (does not include soft debt). If the additional debt is partial IO and is still in its IO

period, then the IO payment should be used. If the additional debt is partial IO and is in its

amortization period, then the amortizing payment should be used.

DSCR at Maximum Payment:

DSCR at Maximum Payment is the ratio of underwritten Net Cash Flow (“NCF”) and the debt service

calculated as described below.

UW NCF = Underwritten Effective Gross Income less underwritten Total Expenses.

Partial Interest Only Mortgage Loans

DSCR = Underwritten NCF/ annualized partial interest only amortizing payment.

ARM Loans/Hybrid ARM Loans

DSCR = Underwritten NCF/ annualized monthly payment calculated using, the Lifetime Maximum Interest

Rate, if applicable, for ARM Loans with an embedded cap or, the Variable Underwriting Rate for other ARM

Loans (e.g., SARM Loans) with an amortization factor (except in the case of a full interest only Mortgage Loan

– no amortization factor is used).

© 2022 Fannie Mae. Trademarks of Fannie Mae. 10.7.2022 10 of 35

Confidential‐InternalDistribution

Product Variations:

Interest Only Mortgage Loans: For Fixed and ARM Loans, Partial Interest Only Mortgage Loans,

DSCR at Maximum Payment will be different than Actual DSCR. For Fixed Rate, Full Interest Only

Mortgage Loans DSCR at Maximum Payment will be the same as Actual DSCR but will be different for

ARM Loans.

Amortizing Mortgage Loans: For Fixed Rate, Amortizing Mortgage Loans, DSCR at Maximum

Payment will be the same as Actual DSCR unless the Mortgage Loan is a Cooperative Property.

Cooperative Properties:

This calculation will use the UW NCF = Rental equivalent NCF Effective Gross Income less

underwritten Total Expenses.

The DSCR at Maximum Payment field will not contain the same figure as Actual DSCR field due

to different NCFs being used in the calculations.

Supplemental Mortgage Loans and Mortgage Loans with Subordinate Debt or Additional

Debt (Combined): The ratio of Underwritten Net Cash (UW NCF) to the annualized combined

monthly payments of all Pre-Existing Mortgage Loans.

Combined monthly payments = the combined monthly payments for all supplemental, subordinate

debt, and first liens (does not include soft debt). If the additional debt is partial IO and is in or out of its

IO period the amortizing payment should be used.

____________________________________________________________________________

Sample Calculations

Example 1 Amortizing Mortgage Loan

Loan $10,000,000

Interest Rate: 5.00

Fixed Rate

Term: 120

Amortization: 360

Underwritten NCF: $1,000,000

Debt Service: $53,682, annualized $644,186

Actual DSCR:

1.55 = $1,000,000 / $644,186

DSCR at Maximum Payment:

1.55

Cooperative Property

:

Loan $10,000,000

Interest Rate: 5.00

Fixed Rate

Term: 120

Amortization: 360

Actual Cooperative NCF: $750,000

Rental Equivalent NCF: $1,000,000

Debt Service: $53,682, annualized $644,186

Actual DSCR:

© 2022 Fannie Mae. Trademarks of Fannie Mae. 10.7.2022 11 of 35

Confidential‐InternalDistribution

1.16 = $750,000 (Actual Cooperative NCF) / $644,186

DSCR at Maximum Payment:

1.55 = $1,000,000 (Rental Equivalent NCF) / $644,186

© 2022 Fannie Mae. Trademarks of Fannie Mae. 10.7.2022 12 of 35

Confidential‐InternalDistribution

Interest Only Mortgage Loan

Loan $10,000,000

Interest Rate: 5.00

Fixed Rate

Term: 120

Amortization: 0

Underwritten NCF: $1,000,000

Debt Service: .0500 * $10,000,000 = $500,000

Actual DSCR:

2.00 = $1,000,000 / $500,000

DSCR at Maximum Payment:

2.00

Partial Interest Only Mortgage Loans:

Loan: $10,000,000

Interest Rate: 5.00

Fixed Rate

Term: 120

Actual 360

Partial IO: 12 months

Original Amortization: 0

Amortization: 360

Underwritten NCF: $1,000,000

Debt Service: .0500 * $10,000,000 = $500,000

Amortizing Debt Service: $53,682, annualized $644,186

Actual DSCR:

2.00 = $1,000,000 / $500,000

DSCR at Maximum Payment:

1.55 = $1,000,000 / $644,186

Example 2 - ARM Loans:

Amortizing

ARM 7-6 Loan: ARM Loan with embedded interest rate caps

Loan $10,000,000

Initial Interest Rate: 5.00 (Margin + 30 Day Average SOFR index)

Amortization: 360

Lifetime Max Interest Rate/Ceiling: 8.00

Underwriting NCF: $1,000,000

Debt Service using initial interest rate: $53,682, annualized $644,186

Debt Service using lifetime max interest rate: $73,377, annualized $880,518

Actual DSCR:

1.55 = $1,000,000 / $644,186

DSCR at Maximum Payment:

1.14 = $1,000,000 / $880,518

© 2022 Fannie Mae. Trademarks of Fannie Mae. 10.7.2022 13 of 35

Confidential‐InternalDistribution

Hybrid ARM Loans:

Amortizing

Hybrid ARM Loan

Loan $3,817,000.00

Initial Fixed Interest Rate: 4.11

Underwriting Interest Rate Floor = Not Applicable for Hybrid ARM Loans

Lifetime Max Interest Rate (Initial Fixed Interest Rate + 5%): 9.11

Interest Only Term: 0 months

Loan Term: 360 months

Amortization: 360 months

Underwritten NCF: $277,000

Debt Service using initial interest rate: $18,466, annualized $221,590

Debt Service using lifetime max interest rate: $31,015 , annualized $372,180

Actual DSCR:

1.25 = $277,000 / $221,590

DSCR at maximum Payment:

0.74 = $277,000 / $372,180 (@ Maximum Lifetime Interest Rate)

© 2022 Fannie Mae. Trademarks of Fannie Mae. 10.7.2022 14 of 35

Confidential‐InternalDistribution

Example 3 – Structured ARM Loans:

Loan: $12,500,000

Initial Interest Rate: 2.770 (ex. Margin (G Fee, S Fee and Investor spread) + 30 Day Average SOFR index)

Variable Underwriting Rate (As defined in the Guide): 5.77 (Initial Interest Rate + Underwriting Spread + Cap Cost)

Applicable Fixed Rate for same term mortgage: 4.95

Term: 120 months

Amortization: 360 months, using a straight line over loan term based on Applicable Fixed Rate

Fixed Principal Payment: $18,655

Lifetime Max Interest Rate/Ceiling: None

Underwriting NCF: $1,000,000

Debt Service using initial interest rate: Interest ($12,500,000*.02770/12=$28,854) plus Fixed Principal ($18,655) equals

$47,510, annualized $570,118

Debt Service using variable underwriting rate: Interest (12,500,000*.0577/12=$60,104) plus Fixed Principal ($18,655)

equals $78,760, annualized $945,118

Actual DSCR:

1.75 = $1,000,000 / $570,118

DSCR at Maximum Payment:

1.06 * = $1,000,000 / $945,118

It is possible for the DSCR at Maximum Payment to be less than 1.0 due to differences in interest rates used to calculate the

principal payment and the interest due.

___________________________________________________________________________

PARTIAL IO

Loan: $12,500,000

Initial Interest Rate: 2.770 (ex. Margin (G Fee, S Fee and Investor spread) + 30 Day Average SOFR index)

Variable Underwriting Rate (As defined in the Guide): 5.77 (Initial Interest Rate + Underwriting Spread + Cap Cost)

Applicable Fixed Rate for same term mortgage: 4.95

Term: 120 months

Amortization: 360 months, using a straight line over loan term based on Applicable Fixed Rate

Fixed Principal Payment: $18,655

Lifetime Max Interest Rate/Ceiling: None

Underwriting NCF: $1,000,000

Debt Service using initial interest rate: Interest $12,500,000*.0277=$346,250

Debt Service using variable underwriting rate: Interest ($12,500,000*.0577/12=$60,104) plus Fixed Principal ($18,655)

equals $78,760, annualized $945,118

Actual DSCR:

2.89=$1,000,000 / $346,250

DSCR at Maximum Payment:

1.06 * = $1,000,000 / $945,118

It is possible for the DSCR at Maximum Payment to be less than 1.0 due to differences in interest rates used to calculate the

principal payment and the interest due.

____________________________________________________________________________

© 2022 Fannie Mae. Trademarks of Fannie Mae. 10.7.2022 15 of 35

Confidential‐InternalDistribution

FULL IO

Loan: $12,500,000

Initial Interest Rate: 2.770 (ex. Margin (G Fee, S Fee and Investor spread) + 30 Day Average SOFR index)

Variable Underwriting Rate (As defined in the Guide): 5.77 (Initial Interest Rate + Underwriting Spread + Cap Cost)

Applicable Fixed Rate for same term mortgage: 4.95

Term: 120 months

Amortization: 360 months, using a straight line over loan term based on applicable Fixed Rate

Fixed Principal Payment: None

Lifetime Max Interest Rate/Ceiling: None

Underwriting NCF: $1,000,000

Debt Service using initial interest rate: Interest $12,500,000*.0277=$346,250

Debt Service using variable underwriting rate: Interest $12,500,000*.0577=$721,250

Actual DSCR:

2.89 = $1,000,000 / $346,250

DSCR at Maximum Payment:

1.39 = $1,000,000 / $721,250

© 2022 Fannie Mae. Trademarks of Fannie Mae. 10.7.2022 16 of 35

Confidential‐InternalDistribution

Job Aid: DSCR Training for Target State DSCR Fields

Review of DUS and Bulk Deliveries Fields

© 2022 Fannie Mae. Trademarks of Fannie Mae. 10.7.2022 17 of 35

Confidential‐InternalDistribution

Fixed Rate Mortgage Loan Scenarios

Scenario Review: Fixed Rate Amortizing Mortgage Loans

© 2022 Fannie Mae. Trademarks of Fannie Mae. 10.7.2022 18 of 35

Confidential‐InternalDistribution

Scenario Review: Fixed Rate Interest Only Mortgage Loans

© 2022 Fannie Mae. Trademarks of Fannie Mae. 10.7.2022 19 of 35

Confidential‐InternalDistribution

Scenario Review: Fixed Rate Partial Interest Only Mortgage Loans

© 2022 Fannie Mae. Trademarks of Fannie Mae. 10.7.2022 20 of 35

Confidential‐InternalDistribution

ARM Loan Scenarios

Scenario Review: Amortizing ARM Loans

© 2022 Fannie Mae. Trademarks of Fannie Mae. 10.7.2022 21 of 35

Confidential‐InternalDistribution

Scenario Review: Full Interest Only ARM Loans

© 2022 Fannie Mae. Trademarks of Fannie Mae. 10.7.2022 22 of 35

Confidential‐InternalDistribution

Scenario Review: Full Interest Only ARM Loans cont.

© 2022 Fannie Mae. Trademarks of Fannie Mae. 10.7.2022 23 of 35

Confidential‐InternalDistribution

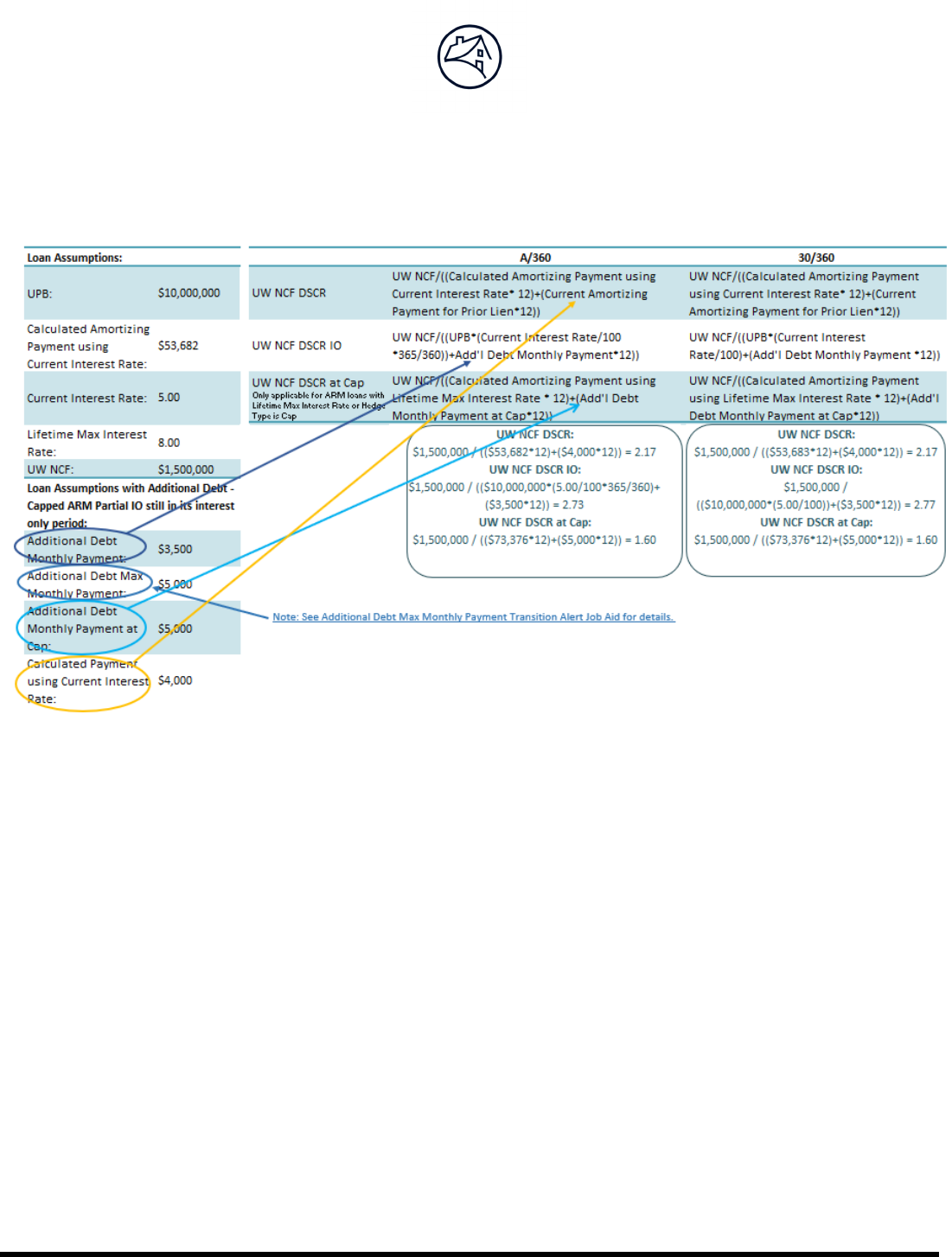

Scenario Review: Partial Interest Only ARM Loans

© 2022 Fannie Mae. Trademarks of Fannie Mae. 10.7.2022 24 of 35

Confidential‐InternalDistribution

Scenario Review: Partial Interest Only ARM Loans cont.

© 2022 Fannie Mae. Trademarks of Fannie Mae. 10.7.2022 25 of 35

Confidential‐InternalDistribution

SARM Loan Scenarios

Scenario Review: Amortizing SARM Loans

© 2022 Fannie Mae. Trademarks of Fannie Mae. 10.7.2022 26 of 35

Confidential‐InternalDistribution

Scenario Review: Amortizing SARM Loans cont.

© 2022 Fannie Mae. Trademarks of Fannie Mae. 10.7.2022 27 of 35

Confidential‐InternalDistribution

Scenario Review: Full Interest Only SARM Loans

© 2022 Fannie Mae. Trademarks of Fannie Mae. 10.7.2022 28 of 35

Confidential‐InternalDistribution

Scenario Review: Full Interest Only SARM Loans cont.

© 2022 Fannie Mae. Trademarks of Fannie Mae. 10.7.2022 29 of 35

Confidential‐InternalDistribution

Scenario Review: Partial Interest Only SARM Loans

© 2022 Fannie Mae. Trademarks of Fannie Mae. 10.7.2022 30 of 35

Confidential‐InternalDistribution

Scenario Review: Partial Interest Only SARM Loans cont.

© 2022 Fannie Mae. Trademarks of Fannie Mae. 10.7.2022 31 of 35

Confidential‐InternalDistribution

Credit Facilities

Review of Credit Facilities DSCR Fields

© 2022 Fannie Mae. Trademarks of Fannie Mae. 10.7.2022 32 of 35

Confidential‐InternalDistribution

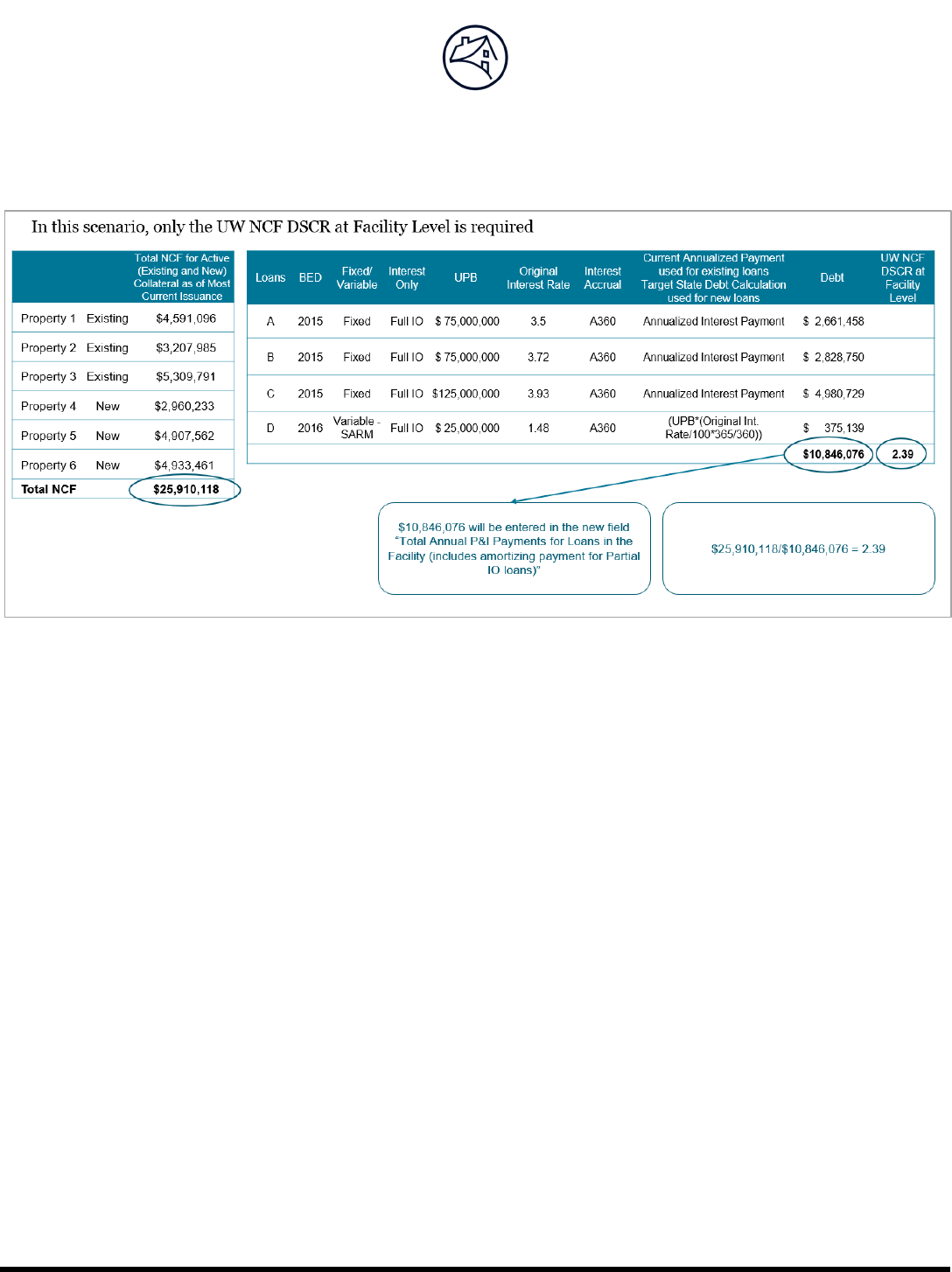

UW NCF DSCR at Facility Level – Example Deal 1

© 2022 Fannie Mae. Trademarks of Fannie Mae. 10.7.2022 33 of 35

Confidential‐InternalDistribution

UW NCF DSCR IO at Facility Level – Example Deal 1

© 2022 Fannie Mae. Trademarks of Fannie Mae. 10.7.2022 34 of 35

Confidential‐InternalDistribution

UW NCF DSCR at Facility Level – Example Deal 2

© 2022 Fannie Mae. Trademarks of Fannie Mae. 10.7.2022 35 of 35

Confidential‐InternalDistribution

Debt Service Coverage Ratio Summary and Conclusion