Report to Congressional Requesters

United States Government Accountabilit

y

Office

GA

O

August 2005

PRESCRIPTION

DRUGS

Price Trends for

Frequently Used

Brand and Generic

Drugs from 2000

through 2004

GAO-05-779

What GAO Found

United States Government Accountability Office

Why GAO Did This Study

Highlights

Accountability Integrity Reliability

www.gao.gov/cgi-bin/getrpt?GAO-05-779.

To view the full product, including the scope

and methodology, click on the link above.

For more information, contact Marjorie Kanof

at (202) 512-7114 or [email protected].

Highlights of GAO-05-779, a report to

congressional requesters

Au

g

ust 2005

PRESCRIPTION DRUGS

Price Trends for Frequently Used Brand

and Generic Drugs from 2000 through

2004

We found the average U&C prices at retail pharmacies reported by two state

pharmacy assistance programs for a 30-day supply of 96 drugs frequently

used by BCBS FEP Medicare and non-Medicare enrollees increased

24.5 percent from January 2000 through December 2004. Of the 96 drugs:

• Twenty drugs accounted for nearly two-thirds of the increase in the U&C

price index.

• The increase in average U&C prices for 75 prescription drugs frequently

used by Medicare beneficiaries was similar to the increase for 76

prescription drugs frequently used by non-Medicare enrollees.

• The average U&C prices for 50 frequently used brand prescription drugs

increased three times as much as the average for 46 generic frequently

used prescription drugs.

A

WPs increased at a faster rate than AMPs and U&C prices for the 50

frequently used brand drugs from first quarter 2000 through fourth quarter

2004. Ten drugs in each index accounted for almost 50 percent of the

increase for AMP, AWP, and U&C prices. Eight of these 10 drugs were

consistent across the three price indexes.

The Centers for Medicare & Medicaid Services (CMS), two state pharmacy

assistance programs, and BCBS FEP reviewed a draft of this report. While

CMS noted that U&C and AWP do not reflect discounts in a drug’s price, this

report’s focus was to examine price trends rather than price levels.

Technical comments were incorporated as appropriate.

Average Annual Percentage Change of AMP, AWP, and U&C Price Indexes for 50 Brand

Drugs Frequently Used by Enrollees in BCBS FEP, from First Quarter 2000 through Last

Quarter 2004

Percentage change

Source: GAO analysis of data from CMS, First DataBank, New York’s Elderly Pharmaceutical Insurance Coverage

program, Pennsylvania’s Pharmaceutical Assistance Contract for the Elderly program, and BCBS FEP.

0

1

2

3

4

5

6

5.4

6.0

5.2

AMP

AWP

U&C

Prescription drug spending has

been the fastest growing segment

of national health expenditures. As

the federal government assumes

greater financial responsibility for

prescription drug expenditures

with the introduction of Medicare

part D, federal policymakers are

increasingly concerned about

prescription drug prices. GAO was

asked to examine the change in

retail prices and other pricing

benchmarks for drugs frequently

used by Medicare beneficiaries and

other individuals with health

insurance from 2000 through 2004.

To examine the change in retail

prices from 2000 through 2004, we

obtained usual and customary

(U&C) prices from two state

pharmacy assistance programs for

drugs frequently used by Medicare

beneficiaries and non-Medicare

enrollees in the 2003 Blue Cross

and Blue Shield (BCBS) Federal

Employee Program (FEP). The

U&C price is the price an individual

without prescription drug coverage

would pay at a retail pharmacy.

Additionally, we compared the

change in U&C prices for brand

drugs from 2000 through 2004 to

the change in two pricing

benchmarks: average

manufacturer price (AMP), which

is the average of prices paid to

manufacturers by wholesalers for

drugs distributed to the retail

pharmacy class of trade, and

average wholesale price (AWP),

which represents the average of list

prices that a manufacturer suggests

wholesalers charge pharmacies.

Page i GAO-05-779 Prescription Drug Price Trends

Letter 1

Results in Brief 4

Background 5

Retail Prices Increased from 2000 through 2004, with Larger

Increases for Brand Than Generic Drugs 6

AWPs Increased at a Faster Rate Than AMPs and U&C Prices for

50 Brand Drugs from 2000 through 2004 11

Concluding Observations 13

Agency and Other External Comments 14

Appendix I Scope and Methodology 16

Appendix II Drugs Included in Analyses 20

Appendix III GAO Contact and Staff Acknowledgments 24

Table

Table 1: Ninety-Six Drugs Included in U&C Price Indexes, by

Month, January 2000 through December 2004 20

Figures

Figure 1: Drug Prices for Different Buyers and Sellers 6

Figure 2: Index of Average U&C Prices for 96 Drugs Frequently

Used by BCBS FEP Enrollees, by Month, 2000 through

2004 7

Figure 3: Annual Change in U&C Price Index for 96 Drugs

Frequently Used by BCBS FEP Enrollees, 2000 through

2004 8

Figure 4: Indexes of Average U&C Prices for Drugs Frequently

Used by BCBS FEP Medicare and Non-Medicare

Enrollees, by Month, 2000 through 2004 10

Figure 5: Indexes of Average U&C Prices for 50 Brand and 46

Generic Drugs Frequently Used by BCBS FEP Enrollees,

by Month, 2000 through 2004 11

Contents

Page ii GAO-05-779 Prescription Drug Price Trends

Figure 6: Indexes of AMPs, AWPs, and Average U&C Prices for 50

Brand Drugs Frequently Used by BCBS FEP Enrollees, by

Quarter, 2000 through 2004 12

Figure 7: Comparison of 10 Drugs Accounting for the Largest

Portions of Changes in AMP, AWP, and U&C Price

Indexes for 50 Brand Drugs Frequently Used by BCBS

FEP Enrollees, by Quarter, 2000 through 2004 13

Abbreviations

AMP average manufacturer price

AWP average wholesale price

BCBS Blue Cross and Blue Shield

BLS Bureau of Labor Statistics

CMS Centers for Medicare & Medicaid Services

EPIC Elderly Pharmaceutical Insurance Coverage

FEP Federal Employee Program

NDC National Drug Code

PACE Pharmaceutical Assistance Contract for the Elderly

U&C usual and customary

This is a work of the U.S. government and is not subject to copyright protection in the

United States. It may be reproduced and distributed in its entirety without further

permission from GAO. However, because this work may contain copyrighted images or

other material, permission from the copyright holder may be necessary if you wish to

reproduce this material separately.

Page 1 GAO-05-779 Prescription Drug Price Trends

August 15, 2005

The Honorable Olympia J. Snowe

Chair

Committee on Small Business and Entrepreneurship

United States Senate

The Honorable Ron Wyden

United States Senate

Prescription drug spending as a share of national health expenditures

increased from 5.8 percent in 1993 to 10.7 percent in 2003 and was the

fastest growing segment of health care expenditures.

1

In addition to

increasing utilization and the introduction of newer drugs, rising

prescription drug prices are a key component of increasing drug

expenditures. Increasing drug prices can affect consumers, employers, and

federal and state governments. Policymakers are increasingly concerned

about drug prices as the federal government will assume greater financial

responsibility for prescription drug expenditures with the introduction of a

prescription drug benefit to Medicare beneficiaries in January 2006,

known as Medicare part D. Medicare beneficiaries also will continue to be

responsible for a large share of drug costs under Medicare part D.

Tracking prescription drug prices can be complicated by the different

prices that different purchasers, such as consumers, insurers and other

third-party payers, and wholesalers, pay for the same drug. Several price

benchmarks represent these differing amounts paid by different

purchasers. For example, individuals without prescription drug coverage,

including Medicare beneficiaries who do not currently have drug coverage,

may pay the full retail price at the pharmacy, known as the usual and

customary (U&C) price. Insurers and other third-party payers, including

state Medicaid programs, typically pay negotiated prices with retail

pharmacies, often receiving discounts from the average wholesale price

(AWP), commonly referred to as a list price.

2

Retail pharmacies may obtain

1

Our calculations are based on data from the national health accounts prepared by the

Centers for Medicare & Medicaid Services, Office of the Actuary, National Health Statistics

Group.

2

The AWP is the average of the list prices that a manufacturer suggests wholesalers charge

pharmacies.

United States Government Accountability Office

Washington, DC 20548

Page 2 GAO-05-779 Prescription Drug Price Trends

drugs directly from pharmaceutical manufacturers or through wholesalers.

The average manufacturer price (AMP) represents the average of prices

paid to manufacturers by wholesalers for drugs distributed to the retail

pharmacy class of trade, and is used by the Centers for Medicare &

Medicaid Services (CMS) to determine rebates due by law to Medicaid

programs. Prices also substantially vary depending on whether drugs are

marketed as brand or generic, with some third-party payers encouraging

the use of less expensive generic drugs through lower cost sharing for

consumers and other strategies.

To provide a baseline of prescription drug prices before the

implementation of the Medicare part D drug benefit, you asked GAO to

review drug price changes from 2000 through 2004, including drugs

frequently used by seniors. Specifically, we examined the following

questions.

1. How have retail prices for prescription drugs frequently used by

Medicare beneficiaries and other individuals with health insurance

changed from 2000 through 2004?

2. How does the change in retail prices for brand drugs frequently used

by Medicare beneficiaries and other individuals compare to other drug

pricing benchmarks from 2000 through 2004?

To examine the change in retail prices for prescription drugs frequently

used by Medicare beneficiaries and other individuals with health

insurance, we selected the 100 most frequently dispensed retail

prescriptions in 2003 for Medicare beneficiaries and for non-Medicare

enrollees in the Blue Cross and Blue Shield (BCBS) Federal Employee

Program (FEP).

3

Combined, these two lists of 100 frequently used drugs

represented a total of 133 unique drugs. Of these 133 drugs, we analyzed 96

drugs (50 brand and 46 generic) for which we were able to obtain U&C

prices at retail pharmacies for every month from January 2000 through

3

We used data of frequently dispensed prescriptions from BCBS FEP because they

represent a large number of retail prescriptions dispensed and could provide data for drugs

used by FEP enrollees who were Medicare beneficiaries and those who were not Medicare

eligible. Of the nearly 55 million retail prescriptions dispensed to BCBS FEP enrollees in

2003, 21 million were for FEP enrollees who were also Medicare beneficiaries.

Page 3 GAO-05-779 Prescription Drug Price Trends

December 2004.

4

These 96 drugs included 75 drugs that were frequently

used by BCBS FEP Medicare enrollees and 76 drugs that were frequently

used by BCBS FEP non-Medicare enrollees, with 55 of these drugs

overlapping the Medicare and non-Medicare frequently used lists. To

calculate a price index, we weighted each drug using the number of

prescriptions dispensed to BCBS FEP enrollees in 2003. We collected the

average monthly U&C prices for a typical 30-day supply from two large

state programs that assist low-income Medicare beneficiaries in

purchasing prescription drugs: Pennsylvania’s Pharmaceutical Assistance

Contract for the Elderly (PACE) program from January 2000 through

December 2004, and New York’s Elderly Pharmaceutical Insurance

Coverage (EPIC) program from August 2000 through December 2004.

5

To compare the change in U&C prices at retail pharmacies with other

drug-pricing benchmarks, we examined changes in the AMP and AWP for

the 50 brand drugs frequently used by BCBS FEP enrollees. We calculated

a quarterly AMP index for a 30-day supply for the 50 brand drugs based on

data we collected from CMS from the first quarter of 2000 through the

fourth quarter of 2004. We calculated a quarterly AWP index for a 30-day

supply for the same 50 brand drugs based on data we collected from First

DataBank for the same period. We determined that the data from BCBS

FEP, PACE, EPIC, CMS, and First DataBank were sufficiently reliable for

our purposes. Our analyses are limited to drugs most frequently used by

Medicare beneficiaries and non-Medicare enrollees in the 2003 BCBS FEP,

and our analyses using U&C prices are limited to prices reported by retail

pharmacies in Pennsylvania to the PACE program and by retail

pharmacies in New York to the EPIC program. See appendix I for more

information about our selected drugs and detailed information on our

4

For the purpose of this report, we refer to single-source and multisource drugs that are

marketed under a proprietary, trademark-protected name as brand drugs. Single-source

drugs include those brand drugs that have no generic equivalent on the market and are

generally available from only one manufacturer. Brand multisource drugs include those

brand drugs that have generic equivalents available from multiple manufacturers and are

marketed under their brand name. Generic drugs include multisource drugs that are

chemically identical to their branded counterparts and are generally marketed by multiple

manufacturers under a non-proprietary name.

5

We used data from PACE and EPIC because they were two of the largest state

pharmaceutical assistance programs, collected data from pharmacies on U&C prices for

drugs, and had historical price data available from 2000.

Page 4 GAO-05-779 Prescription Drug Price Trends

methodology. We performed our work from April 2004 through July 2005

in accordance with generally accepted government auditing standards.

6

From January 2000 through December 2004, based on our analysis of data

from PACE and EPIC, the average monthly U&C prices for a 30-day supply

of 96 prescription drugs frequently used by BCBS FEP Medicare and non-

Medicare enrollees increased 24.5 percent. Twenty of the 96 drugs

accounted for nearly two-thirds of the increase in the U&C price index.

The average U&C prices for 75 prescription drugs frequently used by

BCBS FEP Medicare beneficiaries and the average U&C prices for 76

prescription drugs frequently used by BCBP FEP non-Medicare enrollees

increased at similar rates of 24.0 percent and 24.8 percent, respectively.

The average U&C prices for 50 brand prescription drugs increased

28.9 percent, three times as much as the average U&C price increase of

9.4 percent for 46 generic prescription drugs.

The AWP index increased by 31.6 percent for the 50 frequently used brand

drugs from the first quarter of 2000 through the fourth quarter of 2004—

about 3 to 4 percentage points more rapidly than the AMP and U&C price

indexes. Ten drugs in each index accounted for nearly 50 percent of the

increase for the AMP, AWP, and U&C indexes, with 8 of these top 10 drugs

consistent for all three prices. As a result of AWP’s faster rate of increase,

AWP as a percentage of U&C price increased from an average of about

91 percent in the first quarter of 2000 to about 94 percent in the last

quarter of 2004. AMP stayed about 72 percent of the U&C price during this

period.

We provided a draft of this report to CMS, PACE, EPIC, and BCBS FEP.

CMS noted that U&C and AWP do not reflect discounts in a drug’s price.

While our analysis does not reflect these discounts, our focus was to

examine price trends rather than price levels and U&C and AWP are

consistent measures used to examine price trends. CMS also suggested

that we examine the effect on prices when generic alternatives are

introduced, but such an analysis was beyond the scope of this report.

6

We also reported on trends in U&C prices for 99 drugs from January 2000 through June

2004 in GAO, Prescription Drugs: Trends in Usual and Customary Prices for Drugs

Frequently Used by Medicare and Non-Medicare Enrollees, GAO-05-104R (Washington,

D.C.: Oct. 6, 2004). This report includes 3 fewer drugs than our earlier analysis because

pricing data were not available for these 3 drugs through December 2004.

Results in Brief

Page 5 GAO-05-779 Prescription Drug Price Trends

PACE and BCBS provided technical comments that we incorporated as

appropriate; EPIC stated that it did not have any comments.

Several measures of price are commonly used within the health care

sector to measure the price of prescription drugs. These varying price

measures are due to the different prices that drug manufacturers and retail

pharmacies charge different purchasers, and drug prices can vary

substantially depending on the purchaser. (See fig. 1.)

• The U&C price, the retail price for a drug, is the price an individual

without prescription drug coverage would pay at a retail pharmacy. The

U&C price includes the acquisition cost of the drug paid by the retail

pharmacy and a markup charged by the pharmacy.

• AWP is the average of the list prices or sticker price that a manufacturer of

a drug suggests wholesalers charge pharmacies. AWP is typically less than

the U&C price, which includes the pharmacy’s own markup. AWP is not

the actual price that large purchasers normally pay. Nevertheless, AWP is

part of the formula used by many state Medicaid programs and private

third-party payers to reimburse retail pharmacies.

7

• AMP is the average of prices paid to a manufacturer by wholesalers for a

drug distributed to the retail pharmacy class of trade, after subtracting any

account cash discounts or other price reductions.

8

CMS uses AMP in

determining rebates drug manufacturers must provide, as required by the

Omnibus Budget Reconciliation Act of 1990, to state Medicaid programs as

a condition for the federal contribution to Medicaid spending for the

manufacturers’ outpatient prescription drugs.

9

For brand drugs, the

7

Before 2005, Medicare reimbursement for prescription drugs covered under Medicare part

B was based on AWP. The average sales price generally replaced AWP as the basis for

outpatient drug reimbursement under Medicare part B beginning in 2005. The average sales

price is defined for each drug as a manufacturer’s sales to all purchasers in a given quarter,

net of discounts and rebates and excluding certain government and other purchasers,

divided by the number of units of the drug sold by the manufacturer in that quarter.

Medicare Prescription Drug, Improvement, and Modernization Act of 2003, Pub. L. No. 108-

173, § 303(c), 117 Stat. 2066, 2239-2245 (to be codified at 42 U.S.C. § 1395w-3a).

8

AMP does not include prices to government purchasers based on the Federal Supply

Schedule, which are prices for prescription drugs negotiated with manufacturers by the

Department of Veterans Affairs. AMP also does not include prices from direct sales to

health maintenance organizations and hospitals or prices to wholesalers when they relabel

drugs they purchase under their own label.

9

Pub. L. No. 101-508, § 4401, 104 Stat. 1388, 1388-156 (codified as amended at 42 U.S.C. §

1396r-8(k) (2000)).

Background

Page 6 GAO-05-779 Prescription Drug Price Trends

minimum rebate amount is the number of units of the drug multiplied by

15.1 percent of the AMP.

Figure 1: Drug Prices for Different Buyers and Sellers

a

U&C is the price an individual without prescription drug coverage would pay at a retail pharmacy.

b

When an insured consumer purchases a drug at a retail pharmacy, the pharmacy collects from the

insured consumer the appropriate cost-sharing amount and then submits a claim to the third-party

payer for reimbursement.

c

Third-party payers often negotiate a discount off AWP, the average of the list prices that a

manufacturer suggests wholesalers charge pharmacies. However, third-party payers may pay other

negotiated rates not based on AWP.

d

Retail pharmacies can also purchase prescription drugs directly from manufacturers.

e

AMP represents the average of prices paid to manufacturers by wholesalers for drugs distributed to

the retail pharmacy class of trade.

From January 2000 through December 2004, the average U&C prices for a

typical 30-day supply of 96 prescription drugs frequently used by BCBS

FEP Medicare and non-Medicare enrollees increased 24.5 percent. The

average U&C prices for 75 prescription drugs frequently used by Medicare

beneficiaries and for 76 prescription drugs frequently used by non-

Medicare enrollees increased at similar rates. The average U&C prices for

50 frequently used brand drugs increased three times faster than the

average U&C prices for 46 frequently used generic drugs.

Retail Prices

Increased from 2000

through 2004, with

Larger Increases for

Brand Than Generic

Drugs

Source: GAO.

Retail pharmacy

Uninsured

consumer

Insured

consumer

Manufacturer

Wholesaler

U&C

a

$

AMP

e

$

Retail pharmacy

Retail pharmacy

d

Third-party

payer

c

Cost

share

b

AWP

- discount $

Buyer Buyer Buyer

Seller Seller Seller

Page 7 GAO-05-779 Prescription Drug Price Trends

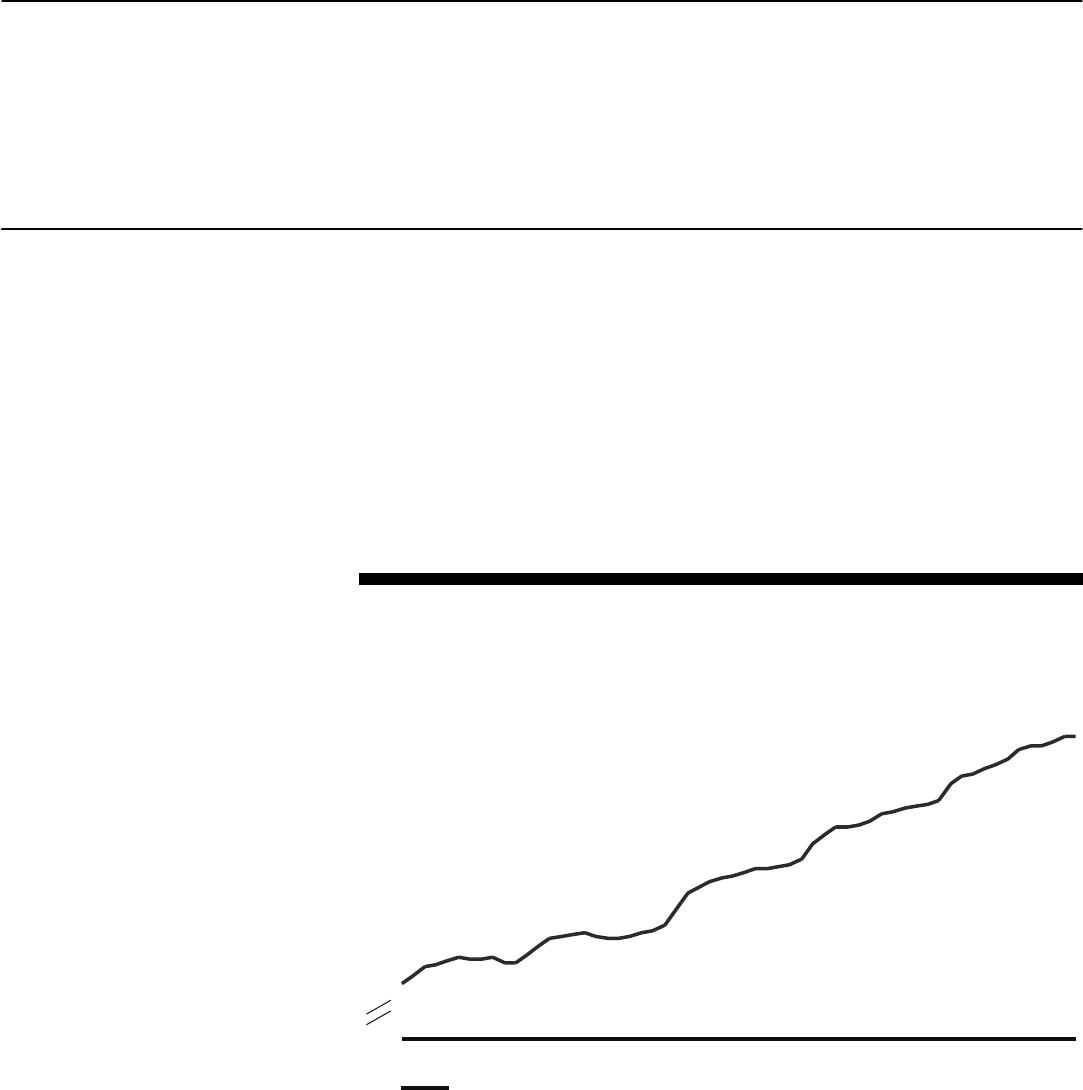

From January 2000 through December 2004, the average U&C price

collected from retail pharmacies by PACE and EPIC for a 30-day supply

for 96 prescription drugs frequently used by BCBS FEP Medicare

beneficiaries and non-Medicare enrollees increased 24.5 percent, a

4.6 percent average annual rate of increase. (See fig. 2.) During the same

period, using nationwide data from the Bureau of Labor Statistics (BLS),

prices for prescription drugs and medical supplies for all urban consumers

increased 21.3 percent, a 4.0 percent average annual rate of increase.

Additionally, using BLS data, prices for all consumer items for all urban

consumers—the Consumer Price Index—increased 12.7 percent, a

2.5 percent average annual rate of increase from January 2000 through

December 2004.

Figure 2: Index of Average U&C Prices for 96 Drugs Frequently Used by BCBS FEP

Enrollees, by Month, 2000 through 2004

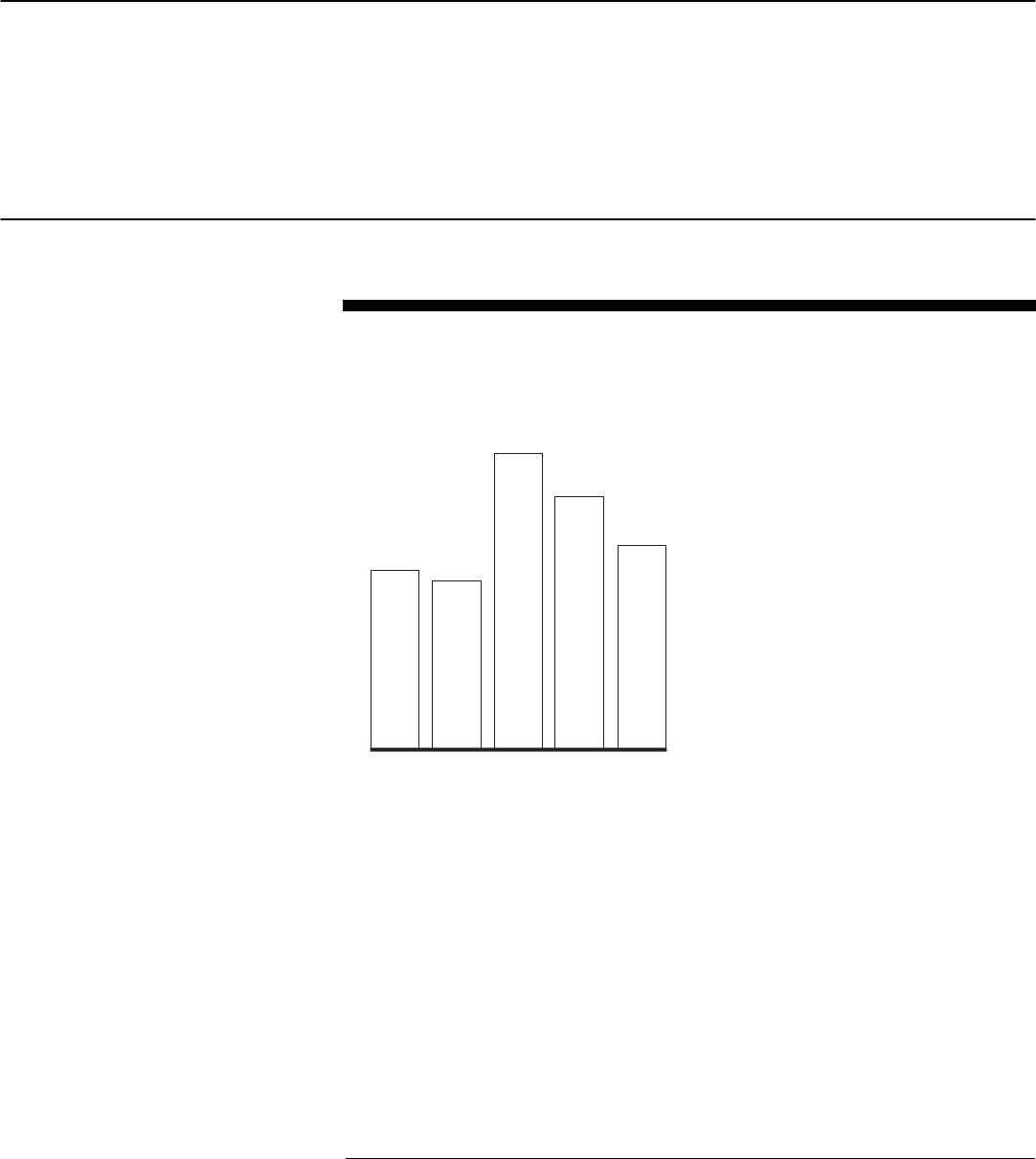

While U&C prices increased each year from 2000 through 2004, the

greatest annual rate of increase—6.1 percent—occurred from January

2002 to January 2003. (See fig. 3.) Since then, annual rates of increase have

U&C Prices for Frequently

Used Drugs Increased

24.5 Percent

124.5

100

105

0

110

115

120

125

130

1/2000 1/2001 1/2002 1/2003 1/2004

U&C

Index (Base = January 2000)

Source: GAO analysis of data from BCBS FEP, EPIC, and PACE.

Page 8 GAO-05-779 Prescription Drug Price Trends

been less, increasing 5.2 percent from January 2003 to January 2004 and

4.2 percent from January 2004 to December 2004.

10

Figure 3: Annual Change in U&C Price Index for 96 Drugs Frequently Used by BCBS

FEP Enrollees, 2000 through 2004

Note: The change in average U&C prices from January 2004 through December 2004 is expressed

as an annual percentage change.

Twenty drugs, representing 33 percent of BCBS FEP prescriptions for the

96 drugs we reviewed, accounted for 64 percent of the total increase in the

U&C price index from January 2000 through December 2004.

11

The drug

with the largest effect on the price index was Lipitor 10mg, which

accounted for 6.6 percent of the total increase. Nineteen of the 20 drugs

were brand drugs and 1 was a generic drug, Hydrocodone/Acetaminophen

5/500mg. The twenty drugs accounting for the largest changes in the U&C

price index are listed below.

10

The change in average U&C prices from January 2004 through December 2004 is

expressed as an annual percentage change.

11

We measured the share each drug contributed to the overall index by comparing the ratio

of (1) each drug’s price change from January 2000 through December 2004 multiplied by its

weight based on BCBS FEP prescriptions, to (2) the sum of all drugs’ price changes

multiplied by their associated weights.

3.7

3.5

6.1

5.2

4.2

0

1

2

3

4

5

6

7

1/2000-

1/2001

1/2001-

1/2002

1/2002-

1/2003

1/2003-

1/2004

1/2004-

12/2004

Percentage change

Source: GAO analysis of data from BCBS FEP, EPIC, and PACE.

Page 9 GAO-05-779 Prescription Drug Price Trends

• Lipitor 10mg

• Celebrex 200mg

• Plavix 75mg

• Prevacid 30mg

• Lipitor 20mg

• Ambien 10mg

• Zocor 20mg

• Levaquin 500mg

• Hydrocodone/Acetaminophen 5/500mg

• Flonase 0.05mg

• Zithromax 250mg

• Wellbutrin SR 150mg

• Singular 10mg

• Premarin 0.625mg

• Celexa 20mg

• Zoloft 50mg

• Evista 60mg

• Norvasc 5mg

• Neurontin 300mg

• Aciphex 20mg

From January 2000 through December 2004, the average U&C prices

collected by PACE and EPIC for 75 prescription drugs frequently used by

BCBS FEP Medicare beneficiaries increased at a similar rate as the

average U&C prices for 76 prescription drugs frequently used by BCBS

FEP non-Medicare enrollees.

12

(See fig. 4.) The prices of 75 Medicare drugs

increased 24.0 percent, a 4.5 percent average annual rate of increase. The

prices of 76 non-Medicare drugs increased 24.8 percent, a 4.6 percent

average annual rate of increase.

13

12

While 55 drugs were used in calculating both the Medicare and non-Medicare U&C price

indexes, each drug had a different weight in each index depending on the frequency of

prescriptions dispensed to BCBS FEP Medicare enrollees or BCBS FEP non-Medicare

enrollees.

13

We found the non-Medicare index rose slightly faster than the Medicare index, in part

because drugs that treat depression were present to a larger extent in the non-Medicare

index. The U&C prices for the eight drugs that treat depression increased at an average rate

of 31.1 percent from January 2000 through December 2004. Excluding the eight drugs that

treat depression from our analysis resulted in a 24.0 percent rate of increase for both the

Medicare and non-Medicare index.

U&C Prices for Drugs

Frequently Used by

Medicare Beneficiaries and

by Non-Medicare Enrollees

Increased at Similar Rates

Page 10 GAO-05-779 Prescription Drug Price Trends

Figure 4: Indexes of Average U&C Prices for Drugs Frequently Used by BCBS FEP

Medicare and Non-Medicare Enrollees, by Month, 2000 through 2004

From January 2000 through December 2004, the average U&C price (based

on PACE and EPIC data) for 50 frequently used brand drugs rose three

times faster than the average U&C price for 46 frequently used generic

drugs. (See fig. 5.) Specifically, the average U&C price for brand drugs

increased 28.9 percent, a 5.3 percent average annual rate of increase,

whereas U&C prices for generic drugs increased 9.4 percent, a 1.8 percent

average annual rate of increase.

U&C Prices Increased

Three Times Faster for

Brand Drugs Than for

Generic Drugs

Source: GAO analysis of data from BCBS FEP, EPIC, and PACE.

124.0

124.8

100

105

0

110

115

120

125

1/2000 1/2001

1/2002

1/2003

1/2004

Medicare

Non-Medicare

Index (base = January 2000)

Page 11 GAO-05-779 Prescription Drug Price Trends

Figure 5: Indexes of Average U&C Prices for 50 Brand and 46 Generic Drugs

Frequently Used by BCBS FEP Enrollees, by Month, 2000 through 2004

From the first quarter of 2000 through the fourth quarter of 2004, AMPs

and U&C prices for the 50 brand drugs increased at similar rates, but

AWPs increased at a faster rate. The quarterly AWPs for 50 brand

prescription drugs increased 31.6 percent, a 6.0 percent average annual

rate of increase. For these same 50 drugs, the quarterly AMPs increased

28.2 percent, a 5.4 percent average annual rate of increase, while the

average quarterly U&C prices increased 27.5 percent, a 5.2 percent average

annual rate of increase.

14

Over the entire period, the AWP index increased

about 3 to 4 percentage points more than the AMP or U&C price indexes.

(See fig. 6.)

14

The quarterly U&C price index increased at a slightly lower rate of increase than the

monthly U&C price index because the base and end periods differ. Whereas the base period

for the monthly U&C index is January 2000, the base period for the quarterly index is

January through March 2000. Similarly, the end period for the monthly index is December

2004 and for the quarterly index is October through December 2004.

AWPs Increased at a

Faster Rate Than

AMPs and U&C Prices

for 50 Brand Drugs

from 2000 through

2004

128.9

109.4

95

100

0

105

110

115

120

125

130

135

1/2000

1/2001 1/2002

1/2003 1/2004

Brand name

Generic

Index (base = January 2000)

Source: GAO analysis of data from BCBS FEP, EPIC, and PACE.

Page 12 GAO-05-779 Prescription Drug Price Trends

Figure 6: Indexes of AMPs, AWPs, and Average U&C Prices for 50 Brand Drugs

Frequently Used by BCBS FEP Enrollees, by Quarter, 2000 through 2004

The difference between the levels of AWP and U&C prices for brand drugs

narrowed slightly during the time period we analyzed. Whereas in the first

quarter of 2000 AWP was on average about 91 percent of the U&C price for

the same drug, by the fourth quarter of 2004 AWP was on average about

94 percent of the U&C price. In contrast, AMP stayed a similar portion of

U&C in first quarter 2000 and fourth quarter 2004, with the AMP on

average about 72 percent of the U&C price.

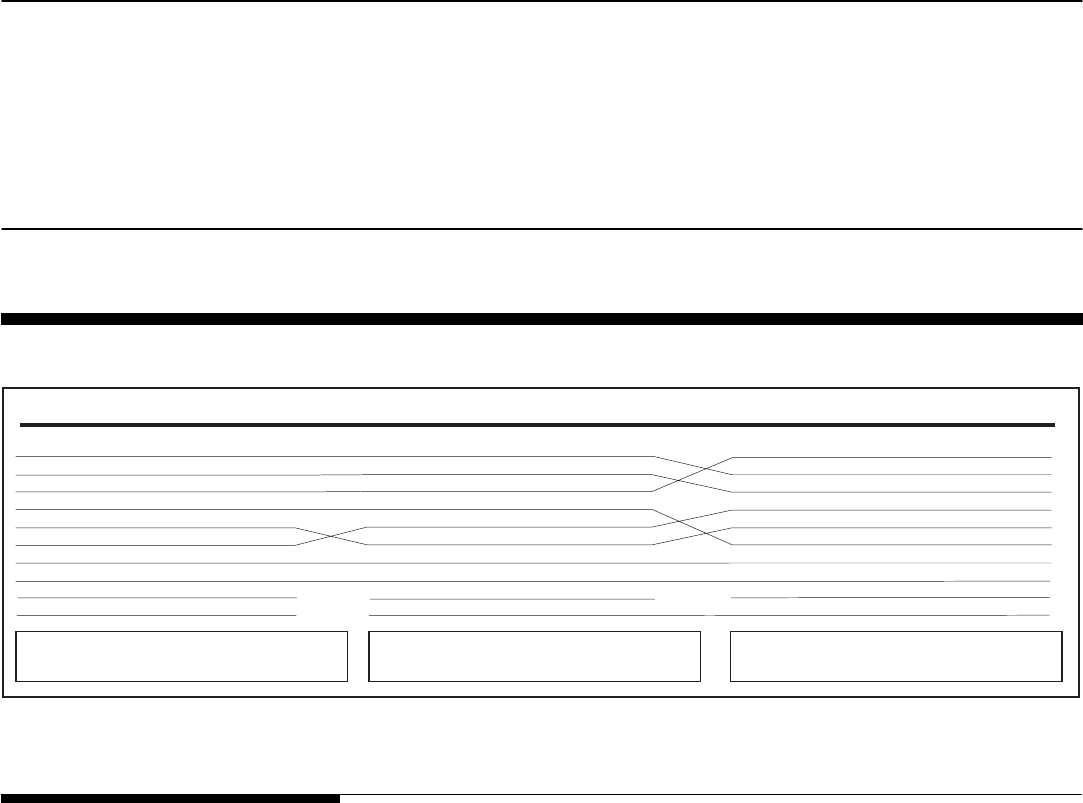

Ten brand drugs in each index, representing one-third or more of the

prescriptions for the 50 brand drugs, accounted for almost 50 percent of

the increase for the quarterly AMP, AWP, and U&C price indexes. Eight of

these 10 drugs were the same across all three price indexes. The drug

accounting for the largest portion of the change in the AMP and AWP

indexes was Celebrex 200mg, accounting for 8.6 percent of the increase

for AMP and 7.5 percent for AWP. Lipitor 10mg was the drug accounting

for the largest portion of the change in the quarterly U&C price index and

128.2

131.6

127.5

100

0

105

110

115

120

125

130

135

Q1/2000 Q1/2001 Q1/2002 Q1/2003 Q1/2004

AMP

AWP

U&C

Index (base = 1st Quarter 2000)

Source: GAO analysis of data from CMS, First DataBank, EPIC, PACE, and BCBS FEP.

Page 13 GAO-05-779 Prescription Drug Price Trends

accounted for 7.2 percent of the increase for the 50 brand drugs. (See fig.

7.)

Figure 7: Comparison of 10 Drugs Accounting for the Largest Portions of Changes in AMP, AWP, and U&C Price Indexes for

50 Brand Drugs Frequently Used by BCBS FEP Enrollees, by Quarter, 2000 through 2004

From 2000 through 2004, retail prices for drugs frequently used by

Medicare beneficiaries increased 24.0 percent—an average rate of

4.5 percent per year. In general, higher drug prices mean higher spending

by consumers and health insurance sponsors, including employers and

federal and state governments. With brand drug prices increasing three

times as fast as generic drug prices, public and private health insurance

sponsors will likely continue to focus on strategies to encourage increased

use of generic drugs when available. Starting in 2006, with the introduction

of the Medicare prescription drug benefit, Medicare will be paying claims

for a wider array of drugs and, as a result, the federal government will be

affected more than previously by rising drug prices.

We found that from 2000 through 2004, on average the AWPs for 50

frequently used brand drugs rose 0.8 percent per year faster than the retail

prices for these same drugs. A continuation of this difference between

AWP and retail prices increases could affect many Medicaid programs and

private third-party payers that base their reimbursement of drug claims on

AWPs.

Concluding

Observations

AMP

Celebrex 200mg

Plavix 75mg

Lipitor 10mg

Ambien 10mg

Lipitor 20mg

Prevacid 30mg

Levaquin 500mg

Zocor 20mg

Zithromax 250mg

Singulair 10mg

AWP

Celebrex 200mg

Plavix 75mg

Lipitor 10mg

Ambien 10mg

Prevacid 30mg

Lipitor 20mg

Levaquin 500mg

Zocor 20mg

Wellbutrin Sr 150mg

Flonase 0.05mg

U&C

Lipitor 10mg

Celebrex 200mg

Plavix 75mg

Prevacid 30mg

Lipitor 20mg

Ambien 10mg

Levaquin 500mg

Zocor 20mg

Zithromax 250mg

Flonase 0.05mg

Source: GAO analysis of data from CMS, First DataBank, EPIC, PACE, and BCBS FEP.

Percentage of 50 brand drug prescriptions: 36%

Percentage of price index’s increase: 49%

Percentage of 50 brand drug prescriptions: 33%

Percentage of price index’s increase: 48%

Percentage of 50 brand drug prescriptions: 37%

Percentage of price index’s increase: 46%

Page 14 GAO-05-779 Prescription Drug Price Trends

We provided a draft of this report to CMS, PACE, EPIC, and BCBS FEP. In

commenting on this report, CMS highlighted the discounts and price

information tools that will be available under the Medicare drug benefit.

CMS also stated that neither the U&C price nor AWP reflect discounts,

such as manufacturers’ discount programs, or other price concessions

affecting a drug’s price. We noted in the report that U&C represents the

retail pharmacy price paid by consumers without insurance. The U&C

does not reflect prices available from other sources, such as mail order

pharmacies. We also noted that AWP is a list price that is not the actual

price paid by large purchasers. We agree that consumers may be able to

obtain lower prices than reflected by the U&C and AWP. However, the

focus of our analysis was to examine price trends rather than price levels,

and U&C and AWP are consistent measures used to assess price trends.

Further, increases in the published AWP may increase what many public

or private third-party purchasers pay for prescription drugs because AWP

is often included in the formula to calculate payments to pharmacies.

Additionally, CMS suggested that we examine the effect on prices when

generic alternatives are introduced. We agree that the introduction of

generic drugs can reduce consumer payments for drugs. Examining

changes in consumer spending for drugs, which are also affected by

changes in utilization and the introduction of new drug alternatives, would

be useful, but was beyond the scope of this report in examining price

trends for frequently-used brand and generic drugs.

PACE and BCBS provided technical comments that we incorporated as

appropriate; EPIC stated that it did not have any comments.

As agreed with your offices, unless you publicly announce the contents

earlier, we plan no further distribution of this report until 30 days after its

date. We will then send copies of this report to the Administrator of CMS

and other interested parties. We will also provide copies to others upon

request. In addition, the report will be available at no charge on the GAO

Web site at http://www.gao.gov.

Agency and Other

External Comments

Page 15 GAO-05-779 Prescription Drug Price Trends

If you or your staffs have any questions about this report, please call me at

(202) 512-7114 or [email protected]. Contact points for our Offices of

Congressional Relations and Public Affairs may be found on the last page

of this report. GAO staff who made major contributions to this report are

listed in appendix III.

Marjorie Kanof

Managing Director, Health Care

Appendix I: Scope and Methodology

Page 16 GAO-05-779 Prescription Drug Price Trends

To examine the change in retail prices for prescription drugs frequently

used by Medicare beneficiaries and other individuals with health

insurance, we used data from the Blue Cross and Blue Shield (BCBS)

Federal Employee Program (FEP) to select the 100 prescription drugs

most frequently dispensed through retail pharmacies in 2003 for BCBS

FEP Medicare enrollees and the 100 most frequently dispensed for BCBS

FEP non-Medicare enrollees.

1

Combined, these two lists included 133

unique drugs.

2

We obtained average monthly usual and customary (U&C) prices reported

by retail pharmacies to Pennsylvania’s Pharmaceutical Assistance

Contract for the Elderly (PACE) program from January 2000 through

December 2004 and New York’s Elderly Pharmaceutical Insurance

Coverage (EPIC) program from August 2000 through December 2004.

3

,

4

We

collected prices based on a specific strength, dosage form, and common

number of units (such as pills), typically for a 30-day supply.

5

Based on

combined PACE and EPIC data, 96 of the 133 drugs we selected had prices

reported for every month from January 2000 through December 2004. We

1

BCBS FEP covered nearly 55 million prescriptions dispensed to enrolled federal

employees, retirees, and their dependents at retail pharmacies in 2003, including 21 million

prescriptions for FEP enrollees who were also Medicare beneficiaries. The 96 drugs that

we included in our analyses represented about 32 percent of total prescriptions dispensed

to BCBS FEP enrollees in 2003. Of these 96 drugs, 50 were brand drugs and represented

about 17 percent of total prescriptions dispensed to BCBS FEP enrollees in 2003.

2

Drugs with the same name but with different forms (such as capsules or tablets) or

number of units dispensed were counted separately as unique drugs.

3

PACE covered more than 9 million prescriptions and EPIC covered nearly 10 million

prescriptions dispensed to mostly low-income seniors in 2003. As of June 2005, PACE

officials reported that approximately 2,800 retail pharmacies—95 percent of pharmacies in

Pennsylvania—participated in PACE, while EPIC officials reported approximately 4,150

retail pharmacies—87 percent of pharmacies in New York—participated in EPIC.

4

We merged price data from PACE and EPIC for August 2000 through December 2004, but

report price data from PACE alone for January 2000 through July 2000. Because the

average of the U&C prices reported by PACE and by EPIC were nearly identical, we do not

believe that including the EPIC data beginning in August 2000 notably affected the price

trend.

5

The Department of Veterans Affairs Pharmacy Benefits Management Strategic Healthcare

Group provided the most common number of units for a retail prescription for a 30-day

supply.

Appendix I: Scope and Methodology

Appendix I: Scope and Methodology

Page 17 GAO-05-779 Prescription Drug Price Trends

analyzed price trends on a monthly basis from January 2000 through

December 2004 for these 96 drugs.

6

Of the 96 drugs, 75 were among those most frequently used by BCBS FEP

Medicare enrollees, and 76 were among those most frequently used by

BCBS FEP non-Medicare enrollees. Fifty-five of the 96 drugs were

frequently used by both BCBS Medicare enrollees and non-Medicare

enrollees.

7

We first determined the total number of prescriptions in 2003

for the drugs we selected dispensed to BCBS FEP Medicare enrollees and

the total number of prescriptions dispensed to BCBS FEP non-Medicare

enrollees. Separately for drugs frequently used by Medicare and by non-

Medicare enrollees, we calculated the share of the total number of BCBS

FEP prescriptions attributed to each drug. The price of each drug was then

weighted by its relative share of total Medicare or total non-Medicare

prescriptions in 2003 to calculate the average price for frequently used

Medicare drugs and the average price for frequently used non-Medicare

drugs for each month from January 2000 through December 2004.

8

,

9

We

standardized these averages to create a Medicare price index and a non-

Medicare price index, each with a value of 100 as of January 2000.

We also separately analyzed monthly trends in U&C prices for brand and

generic drugs frequently used by BCBS FEP enrollees. Of the 96 drugs, 50

were brand drugs and 46 were generic drugs. Similar to our calculation of

6

We also analyzed price trends for 117 drugs that had prices reported for every month from

January 2002 through December 2004, which had an average annual rate of increase of

5.2 percent. For the 96 drugs that had reported prices for every month from January 2000

through December 2004, the average annual rate of increase from January 2002 through

December 2004 was also 5.2 percent.

7

While these 55 drugs were used in calculating both the Medicare and non-Medicare U&C

price indexes, they had different weights in each index depending on the frequency of

prescriptions dispensed to BCBS FEP enrollees who were either Medicare beneficiaries or

not Medicare eligible.

8

BCBS FEP retail prescriptions represent various days supply (such as 34- or 90-day

supply), while PACE and EPIC price data we obtained are limited only to retail

prescriptions for a typical 30-day supply. Over half of BCBS FEP retail prescriptions are for

a 30-day supply.

9

The 2003 BCBS FEP retail prescription drug weights applied to PACE and EPIC retail

prices for 96 drugs from January 2000 through December 2004 were held constant

throughout the entire period of the analysis. We also obtained 2004 BCBS FEP retail

prescription data for 89 of the 96 drugs and found almost no difference in the change in the

U&C price index for the 89 drugs using constant 2003 or 2004 BCBS FEP drug weights

throughout the period of analysis.

Appendix I: Scope and Methodology

Page 18 GAO-05-779 Prescription Drug Price Trends

Medicare and non-Medicare price indexes, we calculated indexes for

brand drugs and generic drugs based on each drug’s share of the total

number of brand or generic prescriptions dispensed to BCBS FEP

enrollees in 2003.

To examine the change in retail prices for frequently used drugs compared

to other drug price benchmarks, we compared an index based on the U&C

prices reported by PACE and EPIC for 50 brand drugs to indexes based on

the average manufacturer prices (AMP) and average wholesale prices

(AWP) for these 50 drugs on a quarterly basis from the first quarter of 2000

through the fourth quarter of 2004.

10

The Centers for Medicare & Medicaid

Services (CMS) requires manufacturers to report AMP within 30 days of

the end of each calendar quarter. Manufacturers submit AWPs on a

periodic basis to publishers of drug-pricing data, such as First DataBank.

Using the National Drug Codes (NDC)

11

reported by PACE and EPIC for

the U&C prices for the 50 brand drugs, we obtained per unit AMPs from

CMS and per unit AWPs from First DataBank associated with each NDC.

12

For each drug, we calculated a quarterly AMP and a quarterly AWP by

multiplying the per unit price by the most common number of units for a

30-day supply.

13

We created an AMP and AWP index by weighting the 50

brand drugs by the number of prescriptions in 2003 from BCBS FEP.

10

These 50 brand drugs were frequently used by Medicare beneficiaries and non-Medicare

enrollees in the BCBS FEP in 2003 and had reported U&C prices to PACE and EPIC for

every month from January 2000 through December 2004.

11

NDCs are three segment numbers that are the universal product identifiers for drugs for

human use; the U.S. Food and Drug Administration assigns the first segment of the NDC,

which identifies the firm that manufacturers, repackages, or distributes a drug. The second

segment identifies a specific strength, dosage form, and formulation for a particular firm

and the third segment identifies package size. A single drug can have multiple NDCs

associated with it. For example, a drug made by one manufacturer, in one form or strength,

but in three package sizes would have three NDCs.

12

We obtained quarterly AMPs from CMS for each two-segment NDC, represented by 9

digits (not accounting for package size), associated with the 50 brand drugs from the first

quarter of 2000 through the fourth quarter of 2004. Similarly, we obtained monthly AWPs

from First DataBank for each three-segment NDC, represented by 11 digits, associated with

the 50 brand drugs from first quarter 2000 through fourth quarter 2004. Specifically, we

obtained the AWP effective on the last day of each month for each 11-digit NDC.

13

For brand drugs with multiple 9-digit NDCs, we calculated an average quarterly AMP for

the drug weighted by the number of PACE and EPIC prescriptions for each 9-digit NDC

during that quarter. For brand drugs with multiple 11-digit NDCs, we calculated an average

monthly AWP for the drug weighted by the number of PACE and EPIC prescriptions during

that month. We created a quarterly AWP by taking a simple average of the three monthly

prices in each quarter.

Appendix I: Scope and Methodology

Page 19 GAO-05-779 Prescription Drug Price Trends

Similarly, we recalculated the U&C price for the 50 brand drugs on a

quarterly basis to make comparisons to AMP and AWP.

We also determined how much each drug’s change in price contributed to

the overall change in price for the 50 brand drugs for AMPs, AWPs, and

U&C prices. We measured the share each drug contributed to the overall

index by comparing the ratio of (1) each drug’s price change from January

2000 through December 2004 multiplied by its weight based on BCBS FEP

prescriptions, to (2) the sum of all drugs price changes multiplied by their

associated weights.

Our analyses are limited to drugs most frequently used by Medicare

beneficiaries and by non-Medicare enrollees in the 2003 BCBS FEP.

Additionally, our analyses using U&C prices are limited to prices reported

by retail pharmacies in Pennsylvania to the PACE program and by retail

pharmacies in New York to the EPIC program. We reviewed the reliability

of data from BCBS FEP, CMS, First DataBank, EPIC, and PACE, including

screening for outlier prices in the PACE and EPIC data and ensuring that

the price trends and frequently used drugs were consistent with other data

sources. We determined that these data were sufficiently reliable for our

purposes. We performed our work from April 2004 through July 2005 in

accordance with generally accepted government auditing standards.

Appendix II: Drugs Included in Analyses

Page 20 GAO-05-779 Prescription Drug Price Trends

Table 1 lists the 96 drugs used in constructing monthly U&C price indexes

from January 2000 through December 2004. Fifty of the 96 drugs are brand

drugs and were also used in examining price changes in AMP, AWP, and

U&C on a quarterly basis from first quarter 2000 through fourth quarter

2004. Of the 96 drugs, 75 were frequently used by Medicare beneficiaries

and 76 were frequently used by non-Medicare enrollees, with 55 of these

drugs frequently used by both Medicare beneficiaries and non-Medicare

enrollees.

Table 1: Ninety-Six Drugs Included in U&C Price Indexes, by Month, January 2000 through December 2004

Drug name and strength

Units dispensed and

dosage form for a typical

30-day supply

Brand or

generic

Medicare or non-

Medicare

Acetaminophen/Codeine 30/300mg 60 tablets Generic Both

Aciphex 20mg 30 tablets

delayed release

Brand Both

Albuterol 90mcg 17gm aerosol Generic Both

Allegra-D 60-120 mg 60 tablets

extended release

Brand Non-Medicare

Allopurinol 300mg 30 tablets Generic Medicare

Alprazolam 0.25mg 60 tablets Generic Both

Alprazolam 0.5mg 60 tablets Generic Both

Ambien 5mg 30 tablets Brand Medicare

Ambien 10mg 30 tablets Brand Both

Amoxicillin 500mg 21 capsules Generic Both

Aricept 10mg 30 tablets Brand Medicare

Atenolol 25mg 30 tablets Generic Both

Atenolol 50mg 30 tablets Generic Both

Carisoprodol 350mg 90 tablets Generic Non-Medicare

Celebrex 200mg 60 capsules Brand Both

Celexa 20mg 30 tablets Brand Both

Cephalexin 500mg 30 capsules Generic Both

Cipro 500mg 20 tablets Brand Non-Medicare

Clonazepam 0.5mg 60 tablets Generic Non-Medicare

Combivent 103-18mcg 14.7gm aerosol Brand Medicare

Cosopt 2-0.5% 5mL solution Brand Medicare

Coumadin 5mg 30 tablets Brand Medicare

Cozaar 5mg 30 tablets Brand Medicare

Cyclobenzaprine HCl 10mg 60 tablets Generic Non-Medicare

Appendix II: Drugs Included in Analyses

Appendix II: Drugs Included in Analyses

Page 21 GAO-05-779 Prescription Drug Price Trends

Drug name and strength

Units dispensed and

dosage form for a typical

30-day supply

Brand or

generic

Medicare or non-

Medicare

Doxycycline Hyclate 100mg 30 capsules Generic Non-Medicare

Effexor XR 75mg 30 capsules

extended release

Brand Non-Medicare

Effexor XR 150mg 30 capsules

extended release

Brand Non-Medicare

Evista 60mg 30 tablets Brand Both

Flomax 0.4mg 30 capsules Brand Both

Flonase 0.05mg 16gm spray Brand Both

Folic Acid 1mg 30 tablets Generic Both

Furosemide 20mg 60 tablets Generic Both

Furosemide 40mg 60 tablets Generic Both

Hydrochlorothiazide 25mg 30 tablets Generic Both

Hydrocodone/Acetaminophen 5/500mg 90 tablets Generic Both

Hydrocodone/Acetaminophen 7.5/500mg 90 tablets Generic Both

Hydrocodone/Acetaminophen 7.5/750mg 90 tablets Generic Non-Medicare

Ibuprofen 800mg 90 tablets Generic Non-Medicare

Isosorbide Mononitrate 30mg 30 tablets

extended release

Generic Medicare

Isosorbide Mononitrate 60mg 30 tablets

extended release

Generic Medicare

Klor-Con 10 10mEq 30 tablets

extended release

Generic Medicare

Lanoxin 125mcg 30 tablets Brand Medicare

Lanoxin 250mcg 30 tablets Brand Medicare

Levaquin 500mg 10 tablets Brand Both

Lipitor 10mg 30 tablets Brand Both

Lipitor 20mg 30 tablets Brand Both

Lipitor 40mg 30 tablets Brand Non-Medicare

Lorazepam 0.5mg 60 tablets Generic Both

Lorazepam 1mg 60 tablets Generic Both

Meclizine HCl 125mg 90 tablets Generic Medicare

Methylprednisolone 4mg 30 tablets Generic Non-Medicare

Metoprolol Tartrate 50mg 60 tablets Generic Both

Miralax 17gm 255gm powder Brand Medicare

Naproxen 500mg 60 tablets Generic Non-Medicare

Nasacort AQ 55mcg 16.5gm spray Brand Non-Medicare

Nasonex 50mcg 17gm spray Brand Non-Medicare

Appendix II: Drugs Included in Analyses

Page 22 GAO-05-779 Prescription Drug Price Trends

Drug name and strength

Units dispensed and

dosage form for a typical

30-day supply

Brand or

generic

Medicare or non-

Medicare

Neurontin 300mg 90 capsules Brand Both

Norvasc 5mg 30 tablets Brand Both

Norvasc 10mg 30 tablets Brand Both

Oxycodone/Acetaminophen 5/325mg 90 tablets Generic Non-Medicare

Paxil 20mg 30 tablets Brand Both

Penicillin V Potassium 500mg 30 tablets Generic Non-Medicare

Plavix 75mg 30 tablets Brand Both

Potassium Chloride 10mEq 60 capsules

extended release

Generic Medicare

Potassium Chloride 10mEq 30 tablets

extended release

Generic Medicare

Pravachol 20mg 30 tablets Brand Medicare

Pravachol 40mg 30 tablets Brand Both

Prednisone 5mg 30 tablets Generic Medicare

Prednisone 10mg 35 tablets Generic Both

Prednisone 20mg 30 tablets Generic Non-Medicare

Premarin 0.625mg 30 tablets Brand Both

Prevacid 30mg 30 capsules

delayed release

Brand Both

Promethazine HCl 25mg 60 tablets Generic Non-Medicare

Propoxyphene Napsylate/Acetaminophen 100/650mg 90 tablets Generic Both

Ranitidine HCl 150mg 60 tablets Generic Both

Singulair 10mg 30 tablets Brand Both

Spironolactone 25mg 30 tablets Generic Medicare

Sulfamethoxazole/Trimethoprim 800/160mg 20 tablets Generic Both

Synthroid 50mcg 30 tablets Brand Both

Synthroid 75mcg 30 tablets Brand Both

Synthroid 100mcg 30 tablets Brand Both

Toprol XL 50mg 30 tablets

extended release

Brand Both

Toprol XL 100mg 30 tablets

extended release

Brand Both

Trazodone HCl 50mg 90 tablets Generic Both

Triamterene/Hydrochlorothiazide 37.5/25mg 30 capsules Generic Both

Triamterene/Hydrochlorothiazide 37.5/25mg 30 tablets Generic Both

Warfarin Sodium 5mg 30 tablets Generic Medicare

Wellbutrin SR 150mg 60 tablets

extended release

Brand Non-Medicare

Appendix II: Drugs Included in Analyses

Page 23 GAO-05-779 Prescription Drug Price Trends

Drug name and strength

Units dispensed and

dosage form for a typical

30-day supply

Brand or

generic

Medicare or non-

Medicare

Xalatan 0.005% 2.5mL solution Brand Both

Zithromax 200mg/5mL 30 suspension Brand Non-Medicare

Zithromax 250mg 6 tablets Brand Both

Zocor 20mg 30 tablets Brand Both

Zocor 40mg 30 tablets Brand Both

Zoloft 50mg 30 tablets Brand Both

Zoloft 100mg 30 tablets Brand Both

Zyrtec 10mg 30 tablets Brand Both

Source: GAO analysis of data from BCBS FEP, EPIC, and PACE.

Appendix III: GAO Contact and Staff

Acknowledgments

Page 24 GAO-05-779 Prescription Drug Price Trends

Marjorie Kanof (202) 512-7114 or kanof[email protected]

In addition to the contact named above, John E. Dicken, Director; Rashmi

Agarwal; Jessica L. Cobert; Martha Kelly, Matthew L. Puglisi; and Daniel S.

Ries made key contributions to this report.

Appendix III: GAO Contact and Staff

Acknowledgments

GAO Contact

Acknowledgments

(290356)

The Government Accountability Office, the audit, evaluation and

investigative arm of Congress, exists to support Congress in meeting its

constitutional responsibilities and to help improve the performance and

accountability of the federal government for the American people. GAO

examines the use of public funds; evaluates federal programs and policies;

and provides analyses, recommendations, and other assistance to help

Congress make informed oversight, policy, and funding decisions. GAO’s

commitment to good government is reflected in its core values of

accountability, integrity, and reliability.

The fastest and easiest way to obtain copies of GAO documents at no cost

is through GAO’s Web site (www.gao.gov). Each weekday, GAO posts

newly released reports, testimony, and correspondence on its Web site. To

have GAO e-mail you a list of newly posted products every afternoon, go

to www.gao.gov and select “Subscribe to Updates.”

The first copy of each printed report is free. Additional copies are $2 each.

A check or money order should be made out to the Superintendent of

Documents. GAO also accepts VISA and Mastercard. Orders for 100 or

more copies mailed to a single address are discounted 25 percent. Orders

should be sent to:

U.S. Government Accountability Office

441 G Street NW, Room LM

Washington, D.C. 20548

To order by Phone: Voice: (202) 512-6000

TDD: (202) 512-2537

Fax: (202) 512-6061

Contact:

Web site: www.gao.gov/fraudnet/fraudnet.htm

E-mail: [email protected]v

Automated answering system: (800) 424-5454 or (202) 512-7470

Gloria Jarmon, Managing Director, [email protected] (202) 512-4400

U.S. Government Accountability Office, 441 G Street NW, Room 7125

Washington, D.C. 20548

Paul Anderson, Managing Director, AndersonP1@gao.gov (202) 512-4800

U.S. Government Accountability Office, 441 G Street NW, Room 7149

Washington, D.C. 20548

GAO’s Mission

Obtaining Copies of

GAO Reports and

Testimony

Order by Mail or Phone

To Report Fraud,

Waste, and Abuse in

Federal Programs

Congressional

Relations

Public Affairs

PRINTED ON

RECYCLED PAPER