12610429

1

Consumer Morsel

Gig work back in favor as wages slide

12 October 2023

Key takeaways

• Moderating wage growth has led to a small uptick in gig job participation over the past few months. Specifically, the percentage

of Bank of America customers who received income from gig platforms through direct deposits or debit cards reached 3% in

August 2023, up from 2.7% in April.

• This increase was driven particularly by ridesharing jobs and younger people, the former of which can be largely explained by

strong travel-related spending. We also found that ridesharing gig workers do not tend to also have a traditional job and an

increased supply of these workers has driven average monthly ridesharing gig pay down in recent months.

• Millennials and Gen Z have seen the biggest increase in gig work as they tend to be more exposed to the rising cost of living.

But it seems gig work may not provide enough support: younger generations' credit and debit card spending growth has

consistently lagged that of Baby Boomers since mid-March, according to Bank of America internal data.

Number of gig workers inches up again

Earlier this year, a Consumer Morsel discussed how workers were leaving the gig economy as a tight labor market and strong

wage growth attracted them to more traditional jobs. Now, six months later, things have shifted again. With wage growth for

traditional jobs moderating, we have seen a small uptick in gig jobs over the past few months. Specifically, the percentage of

Bank of America customers who received income from gig platforms through direct deposits or debit cards reached 3% in

August 2023, up from 2.7% in April this year, but still down from March 2022’s 3.3% (

Exhibit 1).

As Exhibit 2 shows, the recent increase was primarily driven by more ridesharing work, as well as “other” types of gig jobs. Note

that “other” gig jobs refer to those that are not categorized by delivery, ridesharing, social commerce or vacation rental and

include gig work such as caregiving or home repair services etc. Meanwhile, delivery jobs have stabilized since the start of the

year and the number of customers engaging with social commerce marketplaces continues to decline.

Exhibit 1: Percentage of Bank of America customers receiving gig

income (monthly, %)

The percentage of Bank of America customers who received income

from gig platforms reached 3% in August 2023

Source: Bank of America internal data

Exhibit 2: Percentage of Bank of America customers receiving

select types of gig income (monthly, %)

The recent increase in gig jobs was primarily driven by more ridesharing

work

Source: Bank of America internal data

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

2017 2018 2019 2020 2021 2022 2023

0.0%

0.2%

0.4%

0.6%

0.8%

1.0%

1.2%

1.4%

2019 2020 2021 2022 2023

Deliveries

Ridesharing

Social Commerce

Vacation Rental

Oth er

I NSTI TUTE

Accessible version

2

12 October 2023

I NSTITUTE

Not all gigs are equal

In our view, the strength of ridesharing gig jobs can likely be explained by resilient discretionary services spending, particularly in

travel-related categories (for more on travel spend, please see Unpacking summer travel

). According to monthly personal outlay

data from the Bureau of Economic Analysis, nominal consumer spending on cabs and ridesharing grew by an average rate of

27% year-over-year (YoY) during the June-August period, much higher than the overall growth rate for personal consumption

expenditure (PCE) (

Exhibit 3). Rebounding business travel as workers return to in-person meetings could also be driving demand

for ridesharing higher. Similarly, consumer spending on food services remains elevated, which helps to explain delivery jobs

being the most common type of gig work.

One interesting observation is that gig workers for ridesharing platforms are less likely to have a traditional job at the same

time. In August 2023, only 31% of customers who received gig-type income from ridesharing platforms also received a

traditional paycheck; this compares with 52% and 44% for those gig workers at social commerce marketplaces and delivery

platforms (Exhibit 4).

Exhibit 3: Personal consumption expenditure: total and select

categories

Nominal consumer spending on cabs and ridesharing grew by 27% YoY

on average during the June-August period

Source: Bureau of Economic Analysis

Exhibit 4: Share of gig workers who also received paychecks from

traditional jobs through direct deposit (%, Aug 2023 vs. Aug 2019)

In August 2023, only 31% of customers who received gig-type income

from ridesharing platforms also received a traditional paycheck

Source: Bank of America internal data

While more people are performing ridesharing work full-time, average monthly ridesharing gig income has gone down slightly.

Exhibit 5 shows the average monthly income by type of gig platform according to Bank of America internal data, and it suggests

that the average pay for ridesharing gig jobs has been on a downward trend over the last year. That said, compared with the

same month in 2019, average monthly pay for ridesharing gig jobs was still 14% higher in August 2023.

Outside of ridesharing, two types of gig jobs have seen a noticeable rise in average monthly pay over the last year: vacation

rental and deliveries. In our view, the former reflects overall inflation in the lodging sector while the latter can be partly

explained by minimum wage increases in multiple states this year.

Exhibit 5: Average monthly gig income by type of work, according to Bank of America deposit data (index, 2019 average =100)

The average pay for ridesharing gig jobs has been on a downward trend over the last year

Source: Bank of America internal data

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Feb-22 May-22 Aug-22 Nov-22 Feb-23 May-23 Aug-23

Taxi/Cab/Ridesharing

Food Services

Tota l PCE

20%

25%

30%

35%

40%

45%

50%

55%

60%

Social

Commerce

Deliveries Vacation

Rental

Ridesharing Oth er

Aug 2023 Aug 2019

40

60

80

100

120

140

160

180

200

220

240

Mar-19 Oct-19 May-20 Dec- 20 Jul-21 Feb-22 Sep-22 Apr-23

Deliveries Ridesharing Social Commerce

Vacation rental Oth er

12 October 2023

3

I NSTITUTE

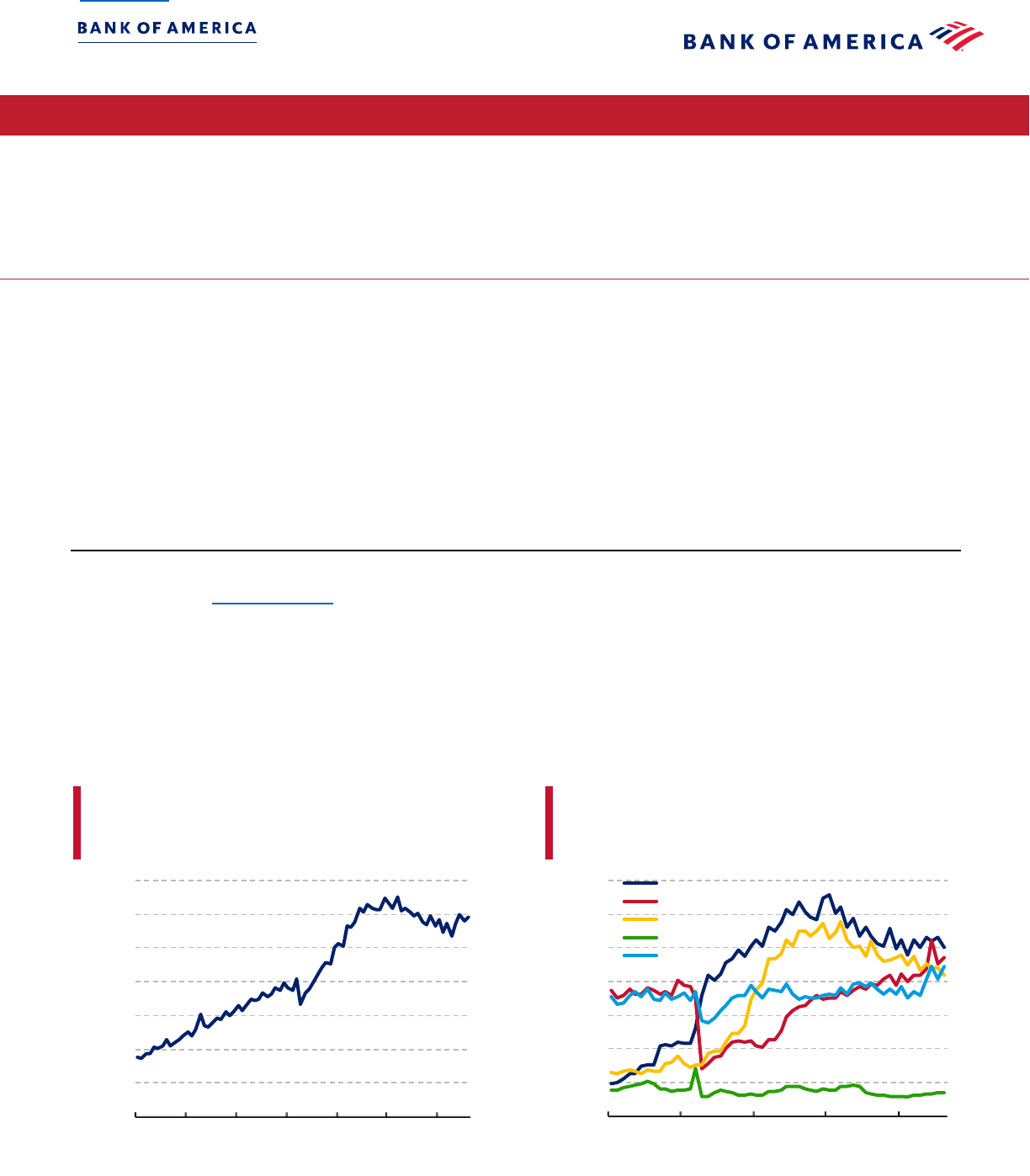

Gig income helps support younger generations

The recent increase in gig job participation seems to be driven by younger generations. Specifically, Millennials continue to

represent the biggest cohort. As of August 2023, 4.3% received income from gig platforms (Exhibit 6). Next was Gen Z, with

3.6% of customers seeing gig income inflows in August.

In our view, younger people tend to be less affluent than older generations and have greater need for supplemental income to

counter rising prices. According to data from the Federal Reserve, Baby Boomers hold the greatest wealth across generations at

$73 trillion in 4Q 2022, eight times that of Millennials.

In addition to different wealth levels, as we discussed in a previous Consumer Checkpoint

, younger generations are also more

exposed to the rising cost of living as they tend to move more frequently, either for work, to accommodate expanding families

or, more broadly, as they seek more space as they age. As such, they have been squeezed harder by the increase in rent and

mortgage payments compared with older generations.

As a result, not only are younger generations taking on more gig work, but they also have weaker spending trends. According to

Bank of America internal data, younger generations have consistently shown weaker credit and debit card spending growth than

Baby Boomers since mid-March this year (Exhibit 7).

Exhibit 6: Percentage of Bank of America customers receiving gig

income by generation (monthly, %)

As of August 2023, 4.3% of Millennial customers received income from

gig platforms

Source: Bank of America internal data

Exhibit 7: Total card spending excluding gas per household by

generation (%YoY, 14-day moving average, data through Sep 27)

Younger generations have shown weaker credit and debit card spending

growth than Baby Boomers since mid-March this year

Source: Bank of America internal data

Wage moderation could explain the rise in gig work

In a previous report, we found that for gig workers who also have traditional employment, they most commonly work in the re t ail

and restaurant industries. We therefore take a look at recent job creation and wage growth in these two industries.

Exhibit 8 shows the monthly change in nonfarm payrolls for the retail trade and leisure & hospitality sectors between October

2022 and September 2023 according to data from the Bureau of Labor Statistics. Even with a strong reading in September

2023, the six-month average of jobs added was at 45k, over 40% lower than the prior six-month average of 78k.

In addition, wage inflation is also easing. As of September, average hourly earnings for retail trade were up 4.2% YoY, down from

the high of 6.7% in early 2022 and only marginally above overall inflation, as measured by the Consumer Price Index. Wages for

leisure & hospitality were relatively higher at 4.7% YoY in September but the slowdown over the last year has been much

steeper (Exhibit 9). In short, lower wage growth in both of these sectors might mean more workers need to take on a side gig.

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

2017 2018 2019 2020 2021 2022 2023

Baby Boomer

Gen X

Millennials

Gen Z

-4%

-2%

0%

2%

4%

6%

8%

10%

Feb-23 Mar-23 Apr-23 May-23 Jun-23 Jul-23 Aug-23 Sep-23

Baby Boomers Gen X

Millennials Gen Z

4

12 October 2023

I NSTITUTE

Exhibit 8: Month over month change in payrolls for retail trade and

leisure & hospitality sectors (seasonally adjusted, thousands)

Change in nonfarm payrolls for the retail trade and leisure & hospitality

sectors has slowed over the last six months

Source: Bureau of Labor Statistics

Exhibit 9: Average hourly earnings for retail trade and leisure &

hospitality sectors (%YoY)

Wage growth for retail trade and leisure & hospitality sectors has

moderated from its peak in 2022

Source: Bureau of Labor Statistics

Methodology

Selected Bank of America transaction data is used to inform the macroeconomic views expressed in this report and should be

considered in the context of other economic indicators and publicly available information. In certain instances, the data may

provide directional and/or predictive value. The data used is not comprehensive; it is based on aggregated and anonymized

selections of Bank of America data and may reflect a degree of selection bias and limitations on the data available.

Bank of America credit/debit card spending per household includes spending from active US households only. Only consumer

card holders making a minimum of five transactions a month are included in the dataset. Spending from corporate cards is

excluded. Data regarding merchants who receive payments are identified and classified by the Merchant Categorization Code

(MCC) defined by financial services companies. The data are mapped using proprietary methods from the MCCs to the North

American Industry Classification System (NAICS), which is also used by the Census Bureau, in order to classify spending data by

subsector. Spending data may also be classified by other proprietary methods not using MCCs.

If applicable, the consumer deposit data based on Bank of America internal data is derived by anonymizing and aggregating data

from Bank of America consumer deposit accounts in the US and analyzing that data at a highly aggregated level.

Gig type of income referenced in this report is derived from aggregated inflows to consumer direct deposits or debit cards from

gig platforms.

Generations, if discussed, are defined as follows:

1. Gen Z, born after 1996

2. Younger Millennials: born between 1989-1995

3. Older Millennials: born between 1978-1988

4. Gen Xers: born between 1965-1977

5. Baby Boomer: 1946-1964

If applicable, any payments data represents aggregated spend from US Retail, Preferred, Small Business and Wealth

Management clients with a deposit account or credit card. Any reference to aggregated spend include total credit card, debit

card, ACH, wires, bill pay, business/peer-to-peer, cash and checks.

Unless otherwise stated, data is not adjusted for seasonality, processing days or portfolio changes, and may be subject to

periodic revisions.

Additional information about the methodology used to aggregate the data is available upon request.

0

20

40

60

80

100

120

140

160

Oct

'22

Nov

'22

Dec

'22

Jan

'23

Feb

'23

Mar

'23

Apr

'23

May

'23

Jun

'23

Jul

'23

Aug

'23

Sep

'23

MoM payroll change for retail trade and leisure & hospitality

Oct 2022 -Mar 2023 average

Apr 2023 - Aug 2 023 Average

-2%

0%

2%

4%

6%

8%

10%

12%

14%

16%

2018 2019 2020 2021 2022 2023

Retail Trade

Leisure & Hospitality

CPI inflation

12 October 2023

5

I NSTITUTE

Contributors

Anna Zhou

Economist, Bank of America Institute

Sources

Dale Lin

Senior Quantitative Finance Manager

Elaine Li

Quantitative Finance Analyst

6

12 October 2023

I NSTITUTE

Disclosures

These materials have been prepared by Bank of America Institute and are provided to you for general information purposes only. To the extent these materials reference Bank of

America data, such materials are not intended to be reflective or indicative of, and should not be relied upon as, the results of operations, financial conditions or performance of Bank

of America. Bank of America Institute is a think tank dedicated to uncovering powerful insights that move business and society forward. Drawing on data and resources from across

the bank and the world, the Institute delivers important, original perspectives on the economy, sustainability and global transformation. Unless otherwise specifically stated, any

views or opinions expressed herein are solely those of Bank of America Institute and any individual authors listed, and are not the product of the BofA Global Research department or

any other department of Bank of America Corporation or its affiliates and/or subsidiaries (collectively Bank of America). The views in these materials may differ from the views and

opinions expressed by the BofA Global Research department or other departments or divisions of Bank of America. Information has been obtained from sources believed to be

reliable, but Bank of America does not warrant its completeness or accuracy. Views and estimates constitute our judgment as of the date of these materials and are subject to change

without notice. The views expressed herein should not be construed as individual investment advice for any particular client and are not intended as recommendations of particular

securities, financial instruments, strategies or banking services for a particular client. This material does not constitute an offer or an invitation by or on behalf of Bank of America to

any person to buy or sell any security or financial instrument or engage in any banking service. Nothing in these materials constitutes investment, legal, accounting or tax advice.

Copyright 2023 Bank of America Corporation. All rights reserved.