AnnualReport 2021

Corporate Prole

Since 1972, Credit Acceptance has offered nancing programs that enable automobile dealers

to sell vehicles to consumers, regardless of their credit history. Our nancing programs are offered

through a nationwide network of automobile dealers who benet from sales of vehicles to

consumers who otherwise could not obtain nancing; from repeat and referral sales generated

by these same customers; and from sales to customers responding to advertisements for our

nancing programs, but who actually end up qualifying for traditional nancing.

Without our nancing programs, consumers are often unable to purchase vehicles or they

purchase unreliable ones. Further, as we report to the three national credit reporting agencies,

an important ancillary benet of our programs is that we provide consumers with an opportunity

to improve their lives by improving their credit score and move on to more traditional sources of

nancing. Credit Acceptance is publicly traded on the Nasdaq stock market under the symbol

CACC. For more information, visit CreditAcceptance.com.

When I got my rst car, I was in an accident that caused me

to le bankruptcy. I had no reliable transportation, and I knew

I needed to get things turned around quickly for my family.

My brother-in-law reached out to me and said, “I think you

should try Credit Acceptance.” I was able to nd a car within

my budget and same day drove off the lot with the car. Having

reliable transportation was a big relief. I’m thankful because

Credit Acceptance allowed me to do that.

– Jaleise

(

Detroit, MI

)

1

2021 ANNUAL REPORT

|

SHAREHOLDER LETTER2021 ANNUAL REPORT

|

SHAREHOLDER LETTER

To Our Shareholders:

BACKGROUND

Credit Acceptance has been in business for 50 years. Don Foss founded the business in

1972 and held the role of CEO until 2002 and Chairman of the Board until 2017 when he

retired. Our core product has remained essentially unchanged under his leadership and

since: we provide auto loans

1

to consumers regardless of their credit history through a

nationwide network of automobile dealers.

One reason for our longevity is simple—we oer a product of immense value to our

dealers and customers. Our customers have a problem. They need a vehicle. And

because they have a credit history—or no credit history—that banks and other lending

sources view as high risk, they have typically been turned away by other lenders. We

oer a solution. Not only do we help them obtain a vehicle, but we provide them with an

opportunity to establish a positive credit record, an opportunity they can use to reenter

the nancial mainstream and move their lives in a positive direction.

Our customers are people like Kyle C. from Bualo, New York. Kyle had recently

graduated from high school and needed a vehicle to get back and forth to college.

He was driving an unreliable vehicle that broke down on the side of the road. The

vehicle was old, and it was cost prohibitive to repair it. Kyle was 18 at the time, with

no credit history and no one to cosign. He tried and failed to nd a lender that would

take a chance on him. We were able to nance Kyle’s purchase of a reliable vehicle.

He returned our faith in him by making all his payments. Not only did he pay but with

our encouragement he paid on time, which he said had a dramatic impact on his credit

score. He ended up trading in the vehicle he nanced with us for a newer vehicle

nanced at a lower interest rate. A short time later he bought his rst home at the age of

20.

Our potential customer market is large. Approximately 40% of adults in the United

States have a credit prole that is considered less than prime. That’s roughly 100 million

adults. We believe each of them deserve a chance for a better nancial future and that,

if given an opportunity to establish or reestablish a positive credit history, many will take

advantage of it. As a result of this belief, we have given millions of people the opportunity

to change their lives.

We also have a compelling value proposition for dealers. We work with independent

and franchise auto dealers nationwide to enable them to sell vehicles to customers who

wish to nance their purchase. We allow the dealer to nance customers, regardless of

their credit history. This gives the dealer the ability to sell a vehicle to a customer whom,

without us, the dealer may otherwise have to turn away.

1

Our company, like most of our competitors, is an indirect auto nance company, which means the nancing contract is originated by the

auto dealer and immediately assigned to us in exchange for compensation. The transaction between the dealer and the consumer is not

a loan, but instead something called a retail installment contract. However, for simplicity and to conform to the language commonly used

in the industry and used in our disclosures, I will refer in this letter to retail installment contracts as “loans” and to indirect auto nance

companies as “lenders”.

2

2021 ANNUAL REPORT

|

SHAREHOLDER LETTER

The impact our program can have on dealers is signicant. As an example, here is the

story of a dealer in Batesburg-Leesville, South Carolina. The general manager and

founder, Dupree C., started out selling cars at a franchise dealership. He dreamed of

starting his own business, which he did in 2014, You’re Approved Auto Sales. Initially,

it was very small, with a leased building and 6-10 cars in inventory. The dealership had

no nancing source, so customers either had to pay cash or obtain their own nancing.

After six months, they had an opportunity to join the Credit Acceptance program. While

there was a learning curve at rst, soon they ramped up to selling around 20 cars a

month, with a high of 44 cars! Things were going well until the pandemic hit, which

reduced customer ow signicantly. However, their payments from us for their share of

the collections on their previous deals provided them with enough cash ow to bridge the

tough months and continue to be successful. Today, they own their buildings and have

sold over 5,000 cars since they started.

The incremental sale creates incremental prot for the dealer, and the potential

for incremental repeat and referral business. Through our product, we have given

thousands of dealers the opportunity to change their lives.

The auto nance market is large and fragmented, with $1.3 trillion in outstanding loan

balances as of December 31, 2021. We compete with banks, credit unions, auto nance

companies aliated with auto manufacturers, independent auto nance companies

and buy here, pay here dealers. Our approach to the market is unique for two reasons.

First, as I have stated, customers are not denied the opportunity to purchase a vehicle

on the basis of their credit history. Second, for most of the vehicle sales we nance, the

dealer shares in the cash ows from the loan, as they receive 80% of net collections

throughout the life of the loan. This is a critical element of our success as it creates

an alignment of interests. The dealer benets if the loan is repaid and the customer’s

credit is reestablished. Therefore, the dealer has an incentive to sell a vehicle at a price

the customer can aord and a vehicle that will last the term of the loan. In addition, the

dealer has an incentive to help the customer after the sale if there are issues with the

vehicle.

HISTORY

Our business model has been quite successful throughout our history. For the rst 20

years, we had limited competition and wrote highly protable business. After we became

a public company in 1992, competition intensied, and we struggled for several years

in the mid to late 1990s. We were able to weather the storm and began focusing on a

nancial measure called Economic Prot. This led to an increased focus on our core

business, and we exited several business lines and geographic locations. This focus has

since guided our success over the last 20 years.

3

2021 ANNUAL REPORT

|

SHAREHOLDER LETTER2021 ANNUAL REPORT

|

SHAREHOLDER LETTER

TODAY

The COVID-19 pandemic, however, created signicant new challenges including vehicle

price ination and shortages. Beginning in March 2020, we experienced a decline in the

demand for our product as government authorities placed limits on economic activity in

an eort to slow the spread of the virus. Those same restrictions hampered the ability

of our eld sales force to conduct in-person meetings with dealers, hindering their

eectiveness. Unit volume declined starting in Q1 2020 through Q1 2021 except during

periods of government stimulus payments, which had a signicant positive impact on

our business. Throughout the remainder of 2021, vehicle prices, which had risen sharply

beginning in 2020, remained elevated and dealer auto inventory shortages worsened,

which further reduced the demand for our product. Simultaneously, however, our

collections, like others in the industry, improved signicantly, which made our loans much

more protable than anticipated.

The pandemic also had a signicant impact on our work environment as more than 95%

of our team members began working remotely. Because our remote operations and

processes proved successful early on, we now pursue a “remote rst” strategy to take

advantage of the national talent pool and an increased rate of team member satisfaction.

While we have experienced higher than normal turnover in certain areas of the business

(principally among our hourly servicing team) amid the national labor shortage, I am

pleased that most of our teams have remained fairly stable. It is a testament to the great

culture we have created.

We have always believed that we owe our success to our great team and culture.

Building and enhancing our culture has been one of our key goals since 2001. The

importance of this was never more evident than during the challenging times in recent

years. Highlights of our team and culture include:

• We have a strong leadership team. Because we are successful at retaining our

leaders, they become stronger each year as they gain knowledge of our business.

Our senior leadership team, consisting of 27 individuals, averages 16 years of

experience with our company. While we add talent selectively, the experience of our

team is a key advantage. Our success in growing the business while simultaneously

improving our return on capital could not have occurred without the dedication and

energy of this talented group.

• Like our senior leadership team, our mid-level leaders are also strong and

experienced. This team of 156 individuals averages 10 years of experience with our

company. It’s their talents and knowledge that keep our operation executing well.

• We devote a large portion of our time to something we call organizational health.

Organizational health is about putting all our team members in position to produce

their best work. For that, we focus consistently on key elements of operational

eectiveness, including setting clear expectations, managing performance, providing

training, maintaining eective incentive compensation plans, establishing the right

environment and providing the technology and processes required for operational

excellence.

4

2021 ANNUAL REPORT

|

SHAREHOLDER LETTER

IMPACT OF BUSINESS CYCLES ON OUR PERFORMANCE

The competitive environment and economic environment presented challenges for us in

2021. We have weathered tough competitive and economic cycles in the past, and we

aimed to extend that track record in the face of the new challenges.

The auto nance market is sensitive to changes in access to capital. When access

to capital decreases, competition in our market decreases. We thrived in such times,

as demonstrated by our nancial results in late 2007 through 2011 (the nancial

crisis triggered by the collapse of the housing market). We withstood the challenges,

outperformed competitors, and maintained access to capital.

Conversely, when access to capital increases, competition in our market increases.

In such times, we have applied strategies leveraging past lessons learned and our

strengths (e.g., the ability to predict loan performance, deploy risk-adjusted pricing,

monitor loan performance, and execute key functions consistently), which has allowed

us to successfully grow our business despite the tougher competitive environment. This

is demonstrated by the results we achieved in 2003 through 2007 and 2012 through

early 2020, when access to capital was readily available and competition increased.

Our dealer compensation strategy has remained consistent regardless of the cost of

capital and the competitive environment. We have maintained a margin of safety in the

amount we advance to dealers. When volume per dealer has declined as a result, we

have found alternative methods to grow the business and maintain protability, such

as increasing our dealer base. 2020 introduced an unprecedented challenge to our

market: a global pandemic. Our company put its team members and customers rst and

weathered the initial storm.

The long-term ripple eect of the pandemic on the automotive industry and, in turn, the

auto nance market has been profound. Supply chain issues arising from the pandemic

created a lack of computer chips needed for new vehicles, which created vehicle

shortages, and drove up vehicle prices. These issues are ongoing with no clear end

date. As I stated earlier, our product allows dealers to make incremental sales. However,

they generally make higher prots on prime credit and cash customers. Given limited

vehicle inventory, dealers are more likely to sell to prime credit and cash customers

instead of those with subprime credit scores who are nancing their transactions. This

resulted in reduced demand for our product throughout 2021. The number of vehicles

nanced for customers with subprime credit scores (our primary customer) reached

record lows in 2021 according to industry data from Experian

®

. Despite these industry

challenges, competition in the market remained strong.

Consistent with how we addressed past macroeconomic challenges, we leveraged

our strengths to persevere in the face of the pandemic and its ripple eects. Our loan

performance remained strong. Loan performance improved markedly after stimulus

payments were distributed and consumer loans assigned 2018 through 2020 yielded

forecasted collection results signicantly better than our initial estimates. In 2020, we

began piloting enhancements to our nancing programs for consumers with higher

credit ratings. In the fourth quarter of 2021, we made the enhancements available to

5

2021 ANNUAL REPORT

|

SHAREHOLDER LETTER2021 ANNUAL REPORT

|

SHAREHOLDER LETTER

all dealers. Above all, through these dicult times, we have remained committed to

positively changing the lives of our dealers and consumers through our innovative

products and solutions.

OPERATING PRINCIPLES

Economic Profit

We use a nancial measure called Economic Prot to evaluate our nancial results and

determine certain incentive compensation. We also use Economic Prot as a framework

to evaluate business decisions and strategies, with an objective to maximize Economic

Prot over the long term. Economic Prot measures how eciently we utilize our total

capital, both debt and equity, and is a function of the return on capital in excess of the

cost of capital and the amount of capital invested in the business. Economic Prot diers

from net income in that it includes a cost for equity capital. In the Supplemental Financial

Results section following this letter, we detail our past Economic Prot performance.

Share Repurchases

To the extent we generate capital in excess of what’s needed to fund the business, we

will return that capital to shareholders through share repurchases as we have done in

the past. We have used excess capital to repurchase shares when prices are at or below

our estimate of intrinsic value (which is the discounted value of estimated future cash

ows). As long as the share price is at or below our estimate of intrinsic value, we prefer

share repurchases to dividends for several reasons. First, repurchasing shares below

intrinsic value increases the value of the remaining shares. Second, distributing capital

to shareholders through a share repurchase gives shareholders the option to defer taxes

by electing not to sell any of their holdings. A dividend does not allow shareholders to

defer taxes in this manner. Finally, share repurchases enable shareholders to increase

their ownership, receive cash or do both based on their individual circumstances and

view of the value of a Credit Acceptance share—they do both if the proportion of shares

they sell is smaller than the ownership stake they gain through the repurchase. A

dividend does not provide similar exibility.

Since beginning our share repurchase program in mid-1999, we have repurchased

approximately 39.4 million shares at a total cost of $4.5 billion. In 2021 we repurchased

approximately 2.9 million shares, representing 16.8% of the shares outstanding at the

beginning of the year, at a total cost of $1.5 billion.

At times, it may appear that we have excess capital, but we won’t be active in

repurchasing our shares. This can occur for several reasons. First, the assessment of

our capital position involves a high degree of judgment. We need to consider future

expected capital needs and the likelihood that this capital will be available. Simply put,

when our debt-to-equity ratio falls below the normal trend line, it doesn’t necessarily

mean we have concluded that we have excess capital. Our rst priority is always to

make sure we have enough capital to fund our business, and such assessments are

always made using what we believe are conservative assumptions. Second, we may

have excess capital but conclude our shares are overvalued relative to intrinsic value or

6

2021 ANNUAL REPORT

|

SHAREHOLDER LETTER

are trading at a level where we believe it’s likely they could be purchased at a lower price

at some point in the future. The assessment of intrinsic value is also highly judgmental.

The nal reason we may be inactive in repurchasing shares, when we have excess

capital at a time when the share price is attractive, is that we are in possession of what

we believe to be material information that has not yet been made public. During such

periods, we suspend our share repurchases until the information has been publicly

disclosed.

Unless we disclose a dierent intention, shareholders should assume we are following

the approach outlined in this section. Our priority is to fund the business. If we conclude

we have excess capital, we will return that capital to shareholders through share

repurchases. If we are inactive for a period, shareholders should not assume that we

believe our shares are overvalued.

THE FUTURE

While we expect vehicle availability and pricing to eventually return to normal, we do not

expect that to occur within the coming months. Until it does, growing our business will be

a challenge. Even when it does, the challenges that were present before the pandemic

are likely to exist after it ends. There are no easy answers to these challenges, but we

operate in a large market. There are still many dealers to enroll who would benet from

our program and we believe that we can make our product more valuable to the dealers

enrolled in our program.

Although the current environment is challenging and our unit volumes have declined, we

are investing in our business to make our product more valuable and prepare for future

growth when the market does return to a more normal environment. In particular, I would

like to highlight a couple changes that we believe will make a signicant impact.

First, we created three “Changing Lives” teams that are focused on the improving the

experience of dealers, consumers and team members. We believe these teams will help

us increase our ability to improve the experience of these three constituents, which will

lead to shareholder success.

Second, we are investing signicant resources into becoming more innovative at

meeting and exceeding the needs of our dealers and consumers. We added a new

member to our Board of Directors, Vinayak Hegde, who has an extensive background

in innovative technology and growth companies. We are also expanding our Product

and Technology teams. In addition to hiring more team members in both these areas,

we recently hired a new Chief Marketing and Product Ocer and are searching for

a new Chief Technology Ocer. All of this is in an eort to enhance our product and

transform our technology systems to be more dealer and customer focused. This will

be a signicant but necessary eort to enable us to continue to grow. By becoming a

“remote rst” organization, we can hire anywhere and compete for the best talent. The

impact of technology on our business cannot be overstated. Over half of our corporate

support team members work in our Analytics, Product and Technology organizations.

This group of over 400 engineers, product managers, designers and data scientists

builds technologies that power our business and provide life-changing opportunities for

our dealers and customers.

7

2021 ANNUAL REPORT

|

SHAREHOLDER LETTER2021 ANNUAL REPORT

|

SHAREHOLDER LETTER

A FINAL NOTE

In 2021, two of our long-standing executives retired.

Charlie Pearce, formerly our Chief Legal Ocer, was hired to start our Legal team in

1996 and he led the team until he announced his retirement. Charlie was incredibly

knowledgeable about our industry and the related issues. Under his leadership, we

created a culture of compliance that aims to be the gold standard in our industry. Thanks

to Charlie and his team, we believe we are well positioned for the challenging regulatory

environment we face today. Charlie built a strong team with talented leaders that were

capable to take over and continue our success in this area. We are grateful for all his

eorts and wish him the best in retirement.

Brett Roberts, our CEO for almost 20 years, started in 1991 as our Corporate Controller,

only a couple years removed from his college days. Brett helped us through our IPO

in 1992 and quickly worked his way up, becoming CFO in 1995 and then CEO in 2002

at the age of 35. Brett is incredibly talented and made a signicant impact on our

organization. Our stock price was under $9 per share when he became CEO, and it went

over $500 while he was here. I was fortunate to work for Brett from the time I started

at Credit Acceptance in 2004 until he retired 17 years later. He is a great teacher and I

learned so much from him. But Brett was more than just a super talented CEO, he was

a super incredible person. As an example of this, we created a virtual going away card

where all team members could write stories and wish him well. It ended up being 119

pages long! It was amazing to read the wonderful stories and memories and learn that

he had changed the lives of so many throughout all levels of our organization. We all

miss him. We know he is our biggest fan and we wish him the best in retirement.

Kenneth S. Booth

Chief Executive Ocer

April 8, 2022

Certain statements herein are forward-looking statements that are subject to certain risks. Please see “Forward-Looking Statements” on

page 42 of our Annual Report on Form 10-K for the year ended December 31, 2021.

8

2021 ANNUAL REPORT

|

SHAREHOLDER LETTER

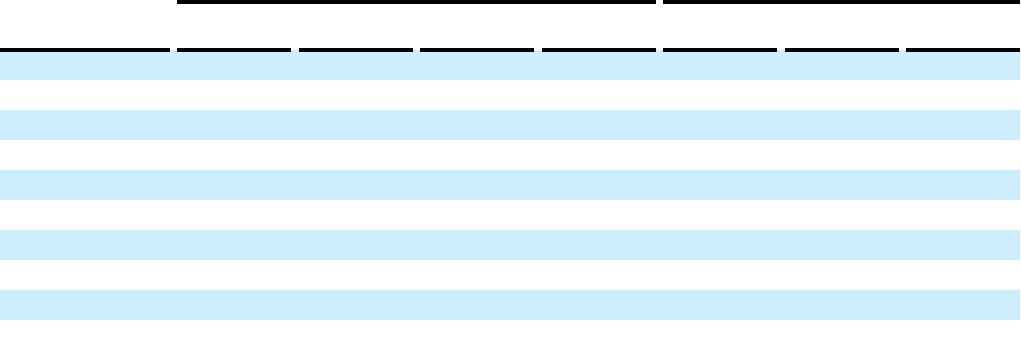

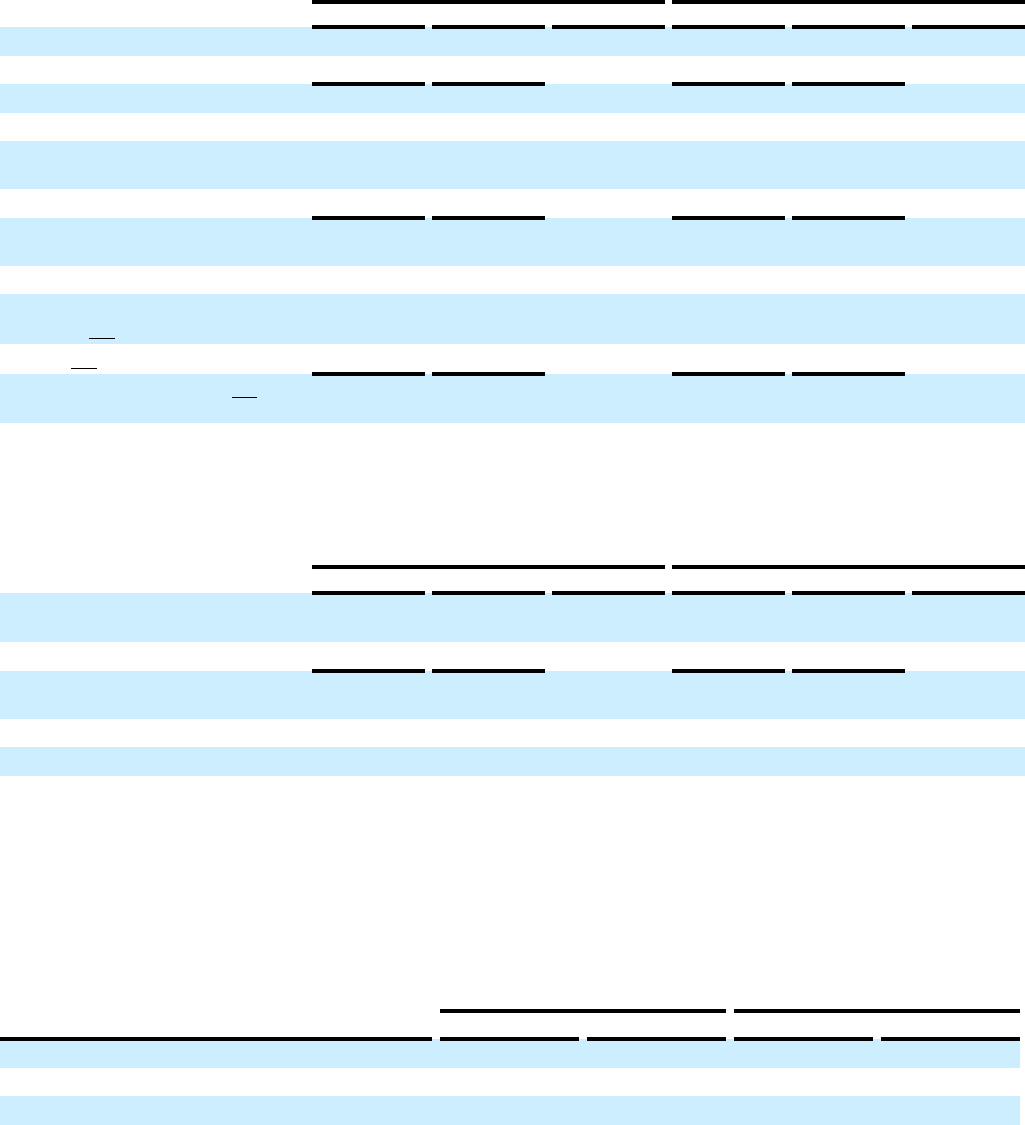

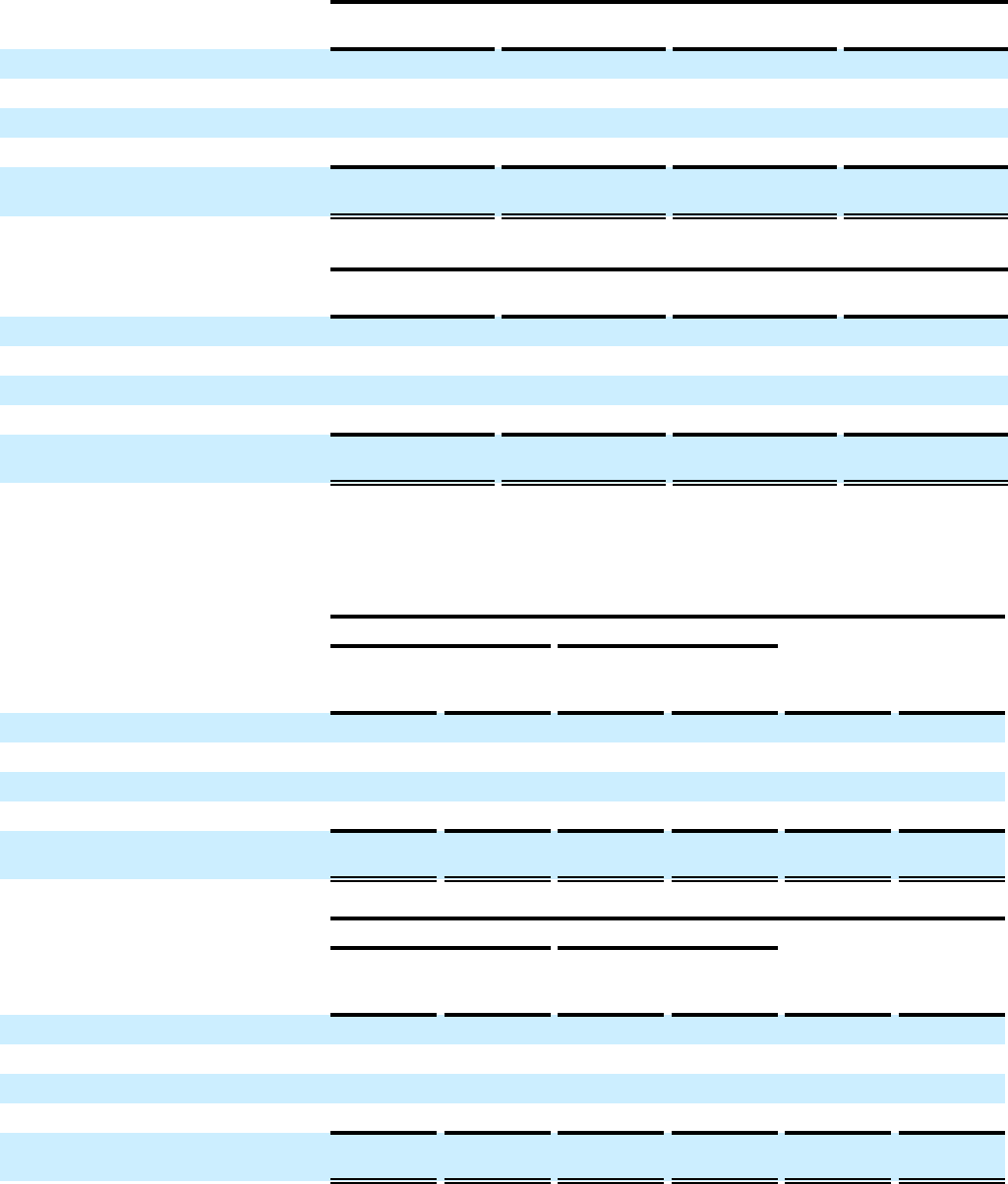

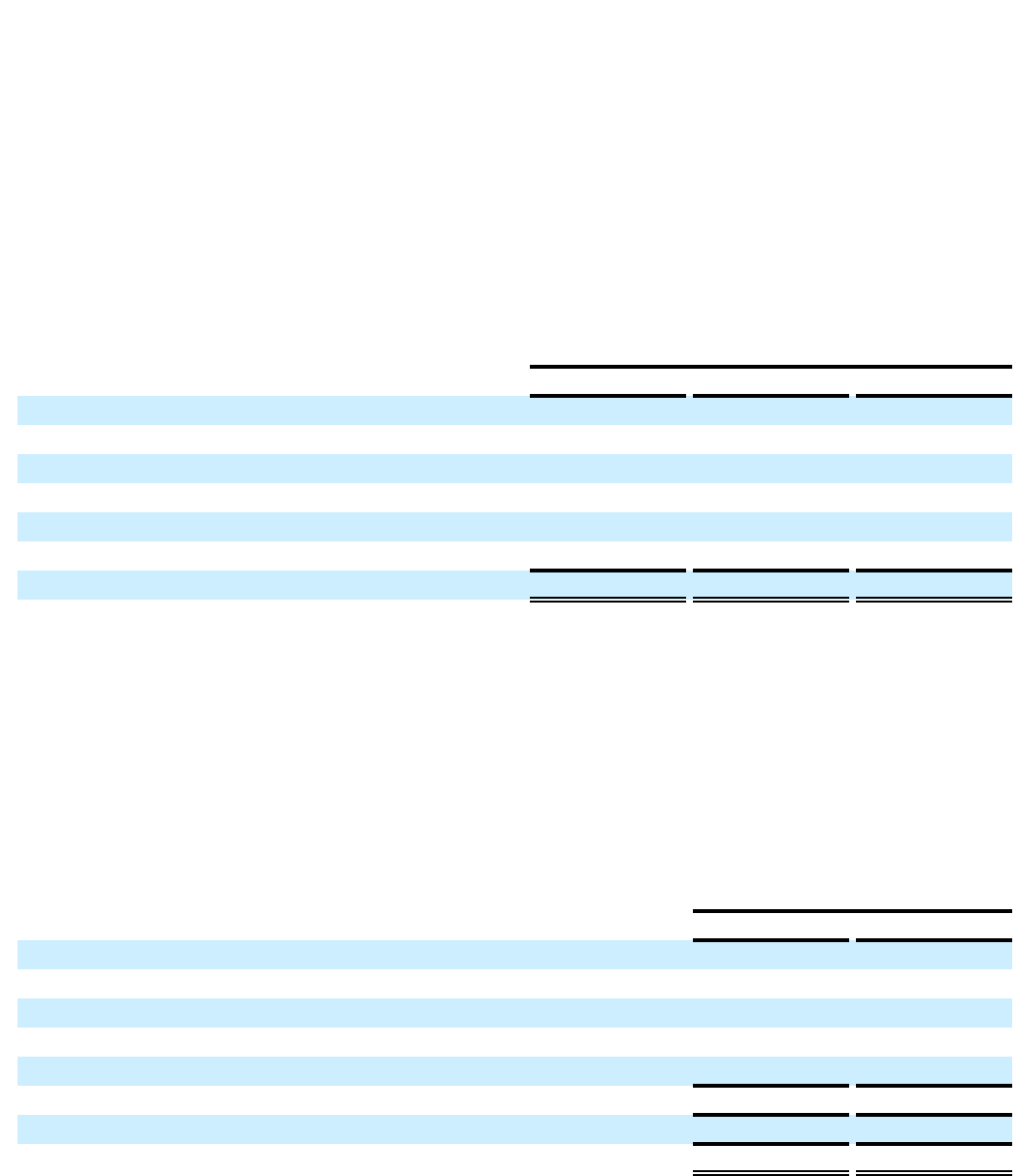

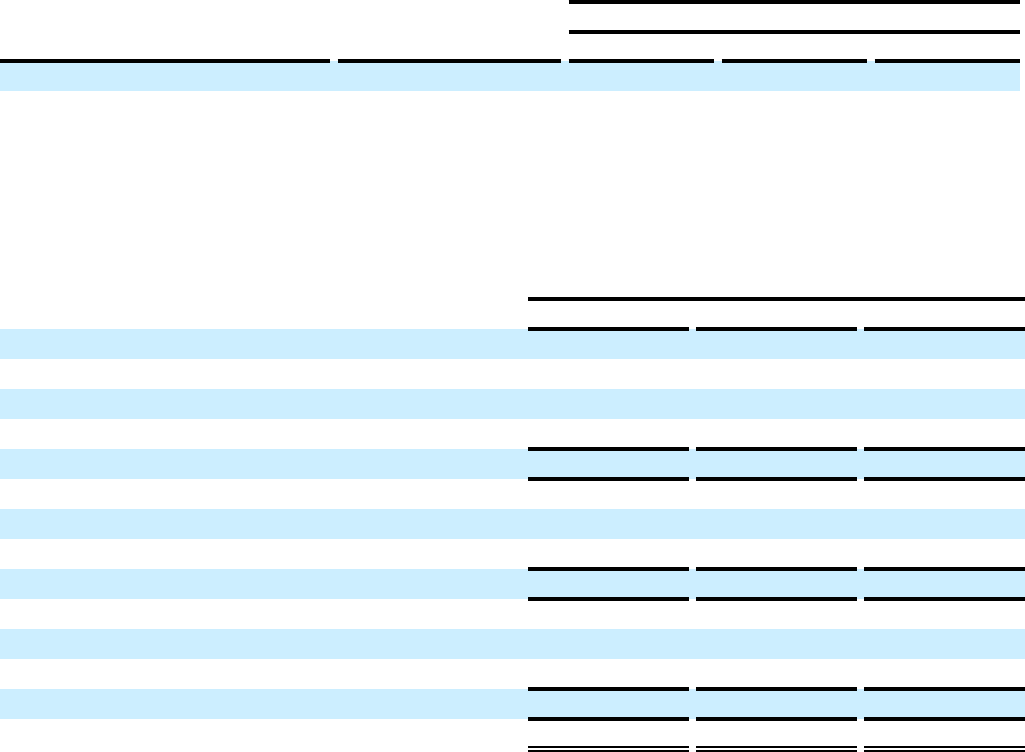

KEY OPERATING RESULTS

At the simplest level, our business success is largely determined by how many loans we

originate and how those loans perform.

Unit Volume

The following table summarizes the growth in number of loans, or unit volume, over the

last 20 years:

Unit volume Year-to-year change

2002 49,801

2003 61,445 23.4%

2004 74,154 20.7%

2005 81,184 9.5%

2006 91,344 12.5%

2007 106,693 16.8%

2008 121,282 13.7%

2009 111,029 −8.5%

2010 136,813 23.2%

2011 178,074 30.2%

2012 190,023 6.7%

2013 202,250 6.4%

2014 223,998 10.8%

2015 298,288 33.2%

2016 330,710 10.9%

2017 328,507 −0.7%

2018 373,329 13.6%

2019 369,805 −0.9%

2020 341,967 −7.5%

2021 268,730 −21.4%

Compound annual growth rate 2002 – 2021 9.3%

Since 2002, unit volume has grown at a compounded annual rate of 9.3%. However, unit

volume has declined the last three years.

9

2021 ANNUAL REPORT

|

SHAREHOLDER LETTER2021 ANNUAL REPORT

|

SHAREHOLDER LETTER

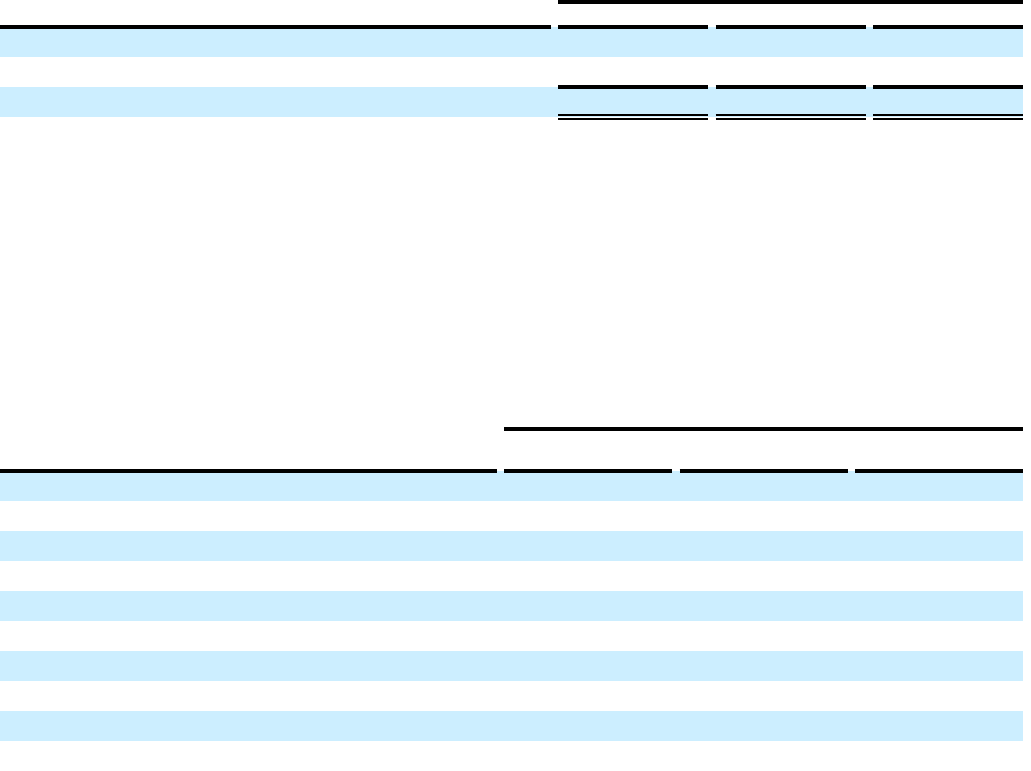

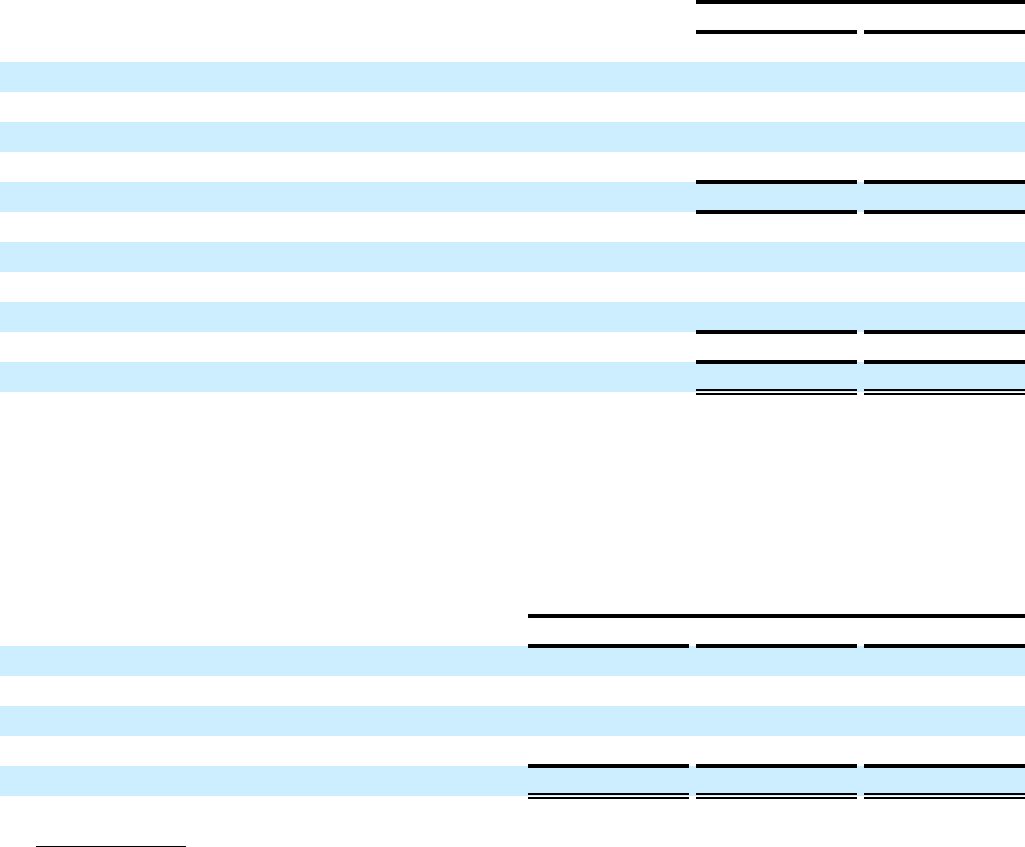

Unit volume is a function of the number of active dealers and the average volume per

dealer. The following table summarizes the trend in each of these variables over the last

20 years:

Active dealers Year-to-year change Unit volume per dealer Year-to-year change

2002 843 59.1

2003 950 12.7% 64.7 9.5%

2004 1,212 27.6% 61.2 −5.4%

2005 1,759 45.1% 46.2 −24.5%

2006 2,214 25.9% 41.3 −10.6%

2007 2,827 27.7% 37.7 −8.7%

2008 3,264 15.5% 37.2 −1.3%

2009 3,168 −2.9% 35.0 −5.9%

2010 3,206 1.2% 42.7 22.0%

2011 3,998 24.7% 44.5 4.2%

2012 5,319 33.0% 35.7 −19.8%

2013 6,394 20.2% 31.6 −11.5%

2014 7,247 13.3% 30.9 −2.2%

2015 9,064 25.1% 32.9 6.5%

2016 10,536 16.2% 31.4 −4.6%

2017 11,551 9.6% 28.4 −9.6%

2018 12,528 8.5% 29.8 4.9%

2019 13,399 7.0% 27.6 −7.4%

2020 12,690 −5.3% 26.9 −2.5%

2021 11,410 −10.1% 23.6 −12.3%

As the table shows, the gain in unit volume since 2002 has resulted, in most years, from

an increase in the number of active dealers partially oset by a reduction in volume per

dealer. Prior to the pandemic and resulting vehicle shortages, we faced two challenges

in growing unit volume. First, increased competition was making it more dicult to enroll

new dealers and more dicult to retain those who had already enrolled, since they

had more alternatives to choose from. In addition, increased competition was putting

downward pressure on volume per dealer. Second, as the number of active dealers

increased, it became harder to grow at the same rate. The impact of these challenges is

apparent starting in 2016. After rapid growth in 2015, active dealer growth slowed each

year from 2016 to 2019.

10

2021 ANNUAL REPORT

|

SHAREHOLDER LETTER

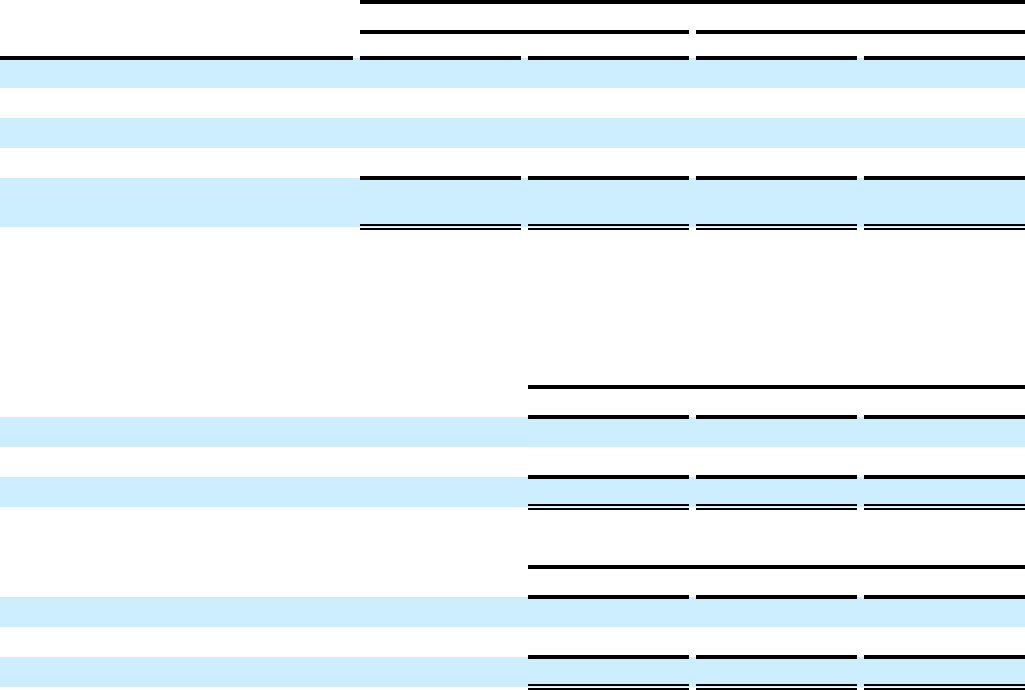

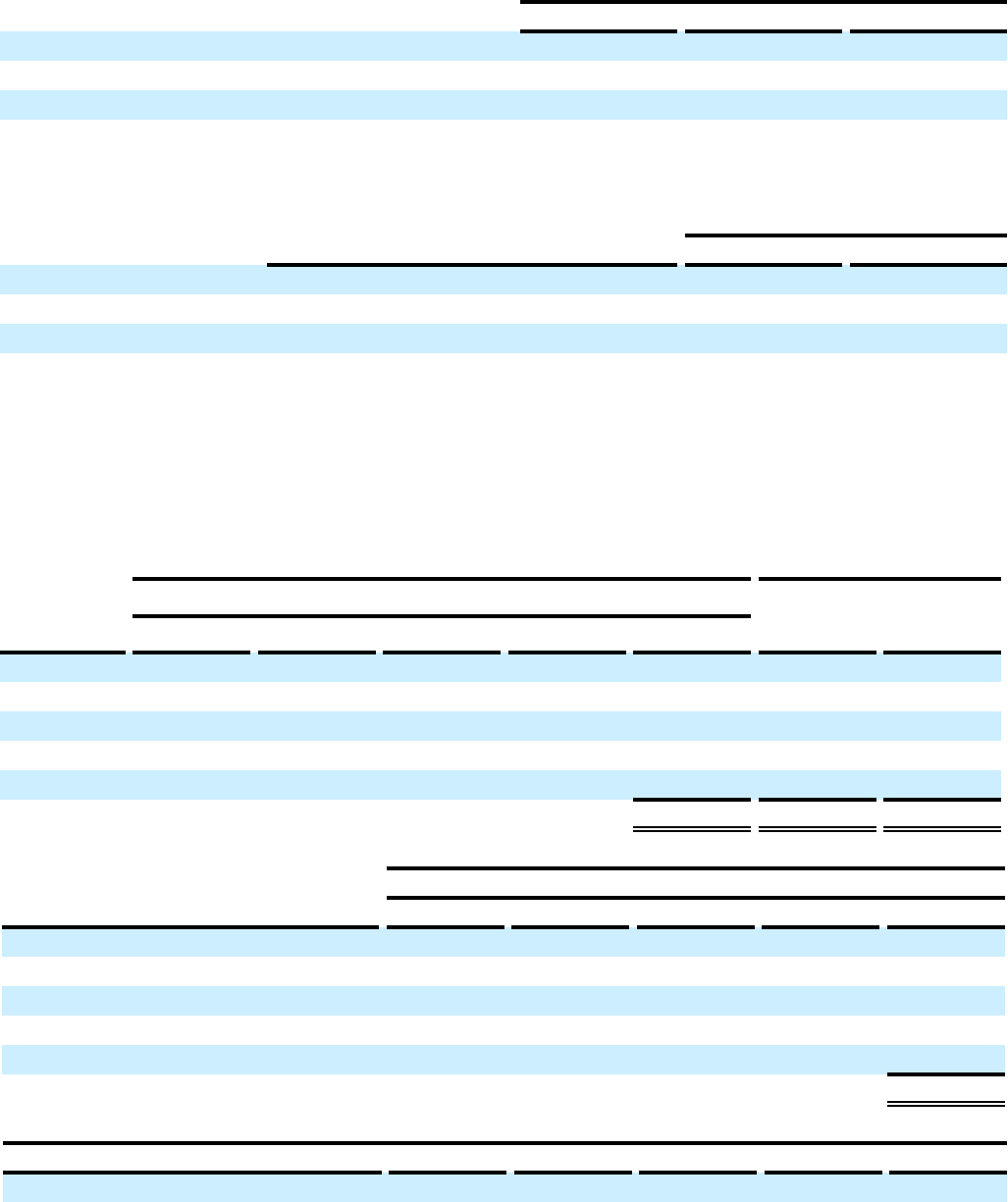

Loan Performance

The most critical time to correctly assess future loan performance is at loan inception,

since that is when we determine the amount we pay to the dealer.

At loan inception, we use a statistical model to estimate the expected collection rate

for that loan. The statistical model is called a credit scorecard. Most consumer nance

companies use such a tool to forecast the performance of the loans they originate.

Our credit scorecard combines credit bureau data, customer data supplied in the credit

application, vehicle data, dealer data, and data captured from the loan transaction such

as the initial loan term or the amount of the down payment received from the customer.

We developed our rst credit scorecard in 1998 and have revised it several times

since then. A credit scorecard that is accurate across a population of loans allows us to

properly price new loan originations, which improves the probability that we will realize

our expected returns on capital.

Subsequent to loan inception, we continue to evaluate the expected collection rate for

each loan. Our evaluation becomes more accurate as the loans age, since we use actual

loan performance data in our forecast. By comparing our current expected collection rate

for each loan with the rate we projected at the time of origination, we can assess the

accuracy of that initial forecast.

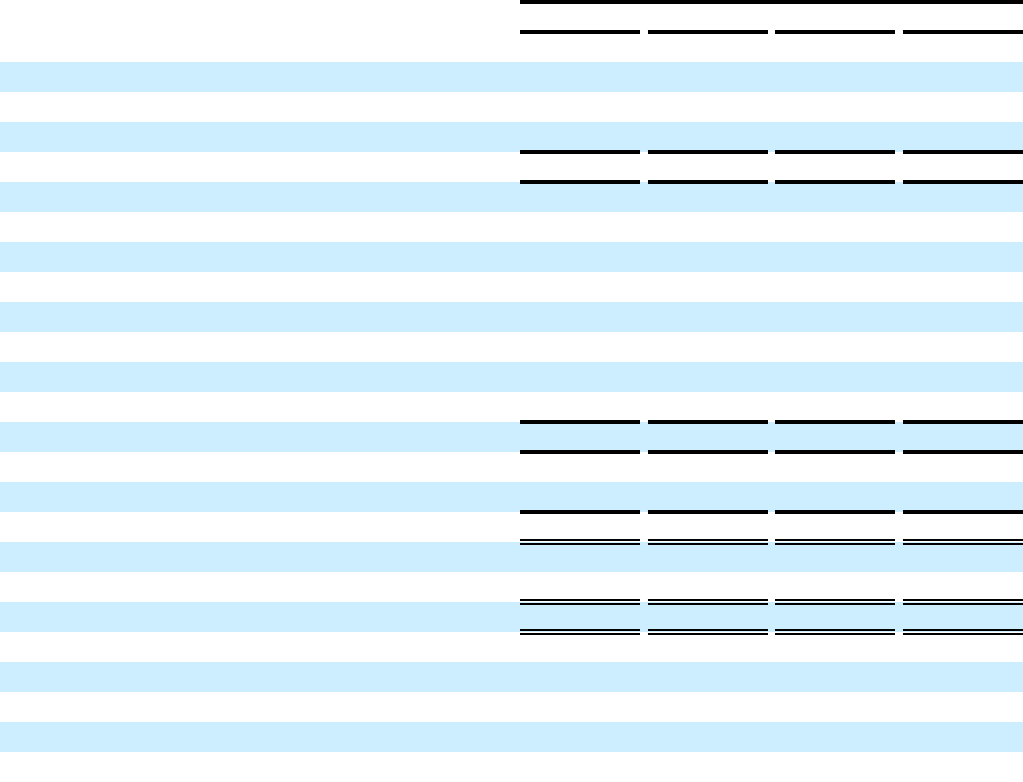

The following table compares, for each of the last 20 years, our December 31, 2021

forecast of loan performance with our initial forecast:

December 31, 2021 forecast Initial forecast Variance

2002 70.4% 67.9% 2.5%

2003 73.7% 72.0% 1.7%

2004 73.0% 73.0% 0.0%

2005 73.6% 74.0% −0.4%

2006 70.0% 71.4% −1.4%

2007 68.1% 70.7% −2.6%

2008 70.4% 69.7% 0.7%

2009 79.5% 71.9% 7.6%

2010 77.7% 73.6% 4.1%

2011 74.7% 72.5% 2.2%

2012 73.8% 71.4% 2.4%

2013 73.4% 72.0% 1.4%

2014 71.5% 71.8% −0.3%

2015 65.1% 67.7% −2.6%

2016 63.6% 65.4% −1.8%

2017 64.4% 64.0% 0.4%

2018 65.1% 63.6% 1.5%

2019 66.5% 64.0% 2.5%

2020 67.9% 63.4% 4.5%

2021 66.5% 66.3% 0.2%

Average

1

68.1% 67.0% 1.1%

1

Calculated using a weighted average based on loan origination dollars.

11

2021 ANNUAL REPORT

|

SHAREHOLDER LETTER2021 ANNUAL REPORT

|

SHAREHOLDER LETTER

Loan performance can be explained by a combination of internal and external factors.

Internal factors, among other things, include the quality of our origination and collection

processes, the quality of our credit scorecard, and changes in our policies governing

new loan originations. External factors, among other things, include the unemployment

rate, the retail price of gasoline, vehicle wholesale values, and the cost of other required

expenditures (such as for food and energy) that impact our customers. In addition, the

level of competition is thought to impact loan performance through something called

adverse selection.

Adverse selection, as it relates to our market, refers to an inverse correlation between

the number of lenders that are competing for the loan and the accuracy of an empirical

scorecard. Said another way, without any competition it is easier to build a scorecard

that accurately assesses expected collections across a population of loans based on

attributes collected at the time of loan origination. As competition increases, creating an

accurate scorecard becomes more challenging.

To illustrate adverse selection, we will give a simple example. Assume that the scorecard

we use to originate loans is based on a single variable, the amount of the customer’s

down payment, and that the higher the down payment, the higher the expected collection

rate. Assume that for many years, we have no competitors, and we accumulate

performance data indicating that loans with down payments above $1,000 consistently

produce the same average collection rate. Then assume that we begin to compete with

another lender whose scorecard ignores down payment and instead emphasizes the

amount of the customer’s weekly income.

As the new lender begins to originate loans, our mix of loans will be impacted as follows:

We will start to receive loans for borrowers with lower average weekly incomes as the

new lender originates loans for borrowers with higher weekly incomes—i.e., borrowers

whose loans we would have previously originated. Furthermore, since our scorecard

only focuses on down payment, the shift in our borrower mix will not be detected by

our scorecard, and our collection rate expectation will remain unchanged. It is easy

to see that this shift in borrower characteristics will have a negative impact on loan

performance, and that this impact will be missed by our scorecard.

Although the real world is more complex than this simple example—with hundreds

of lenders competing for loans and with each lender using many variables in its

scorecard—adverse selection is something that probably does impact loan performance.

12

2021 ANNUAL REPORT

|

SHAREHOLDER LETTER

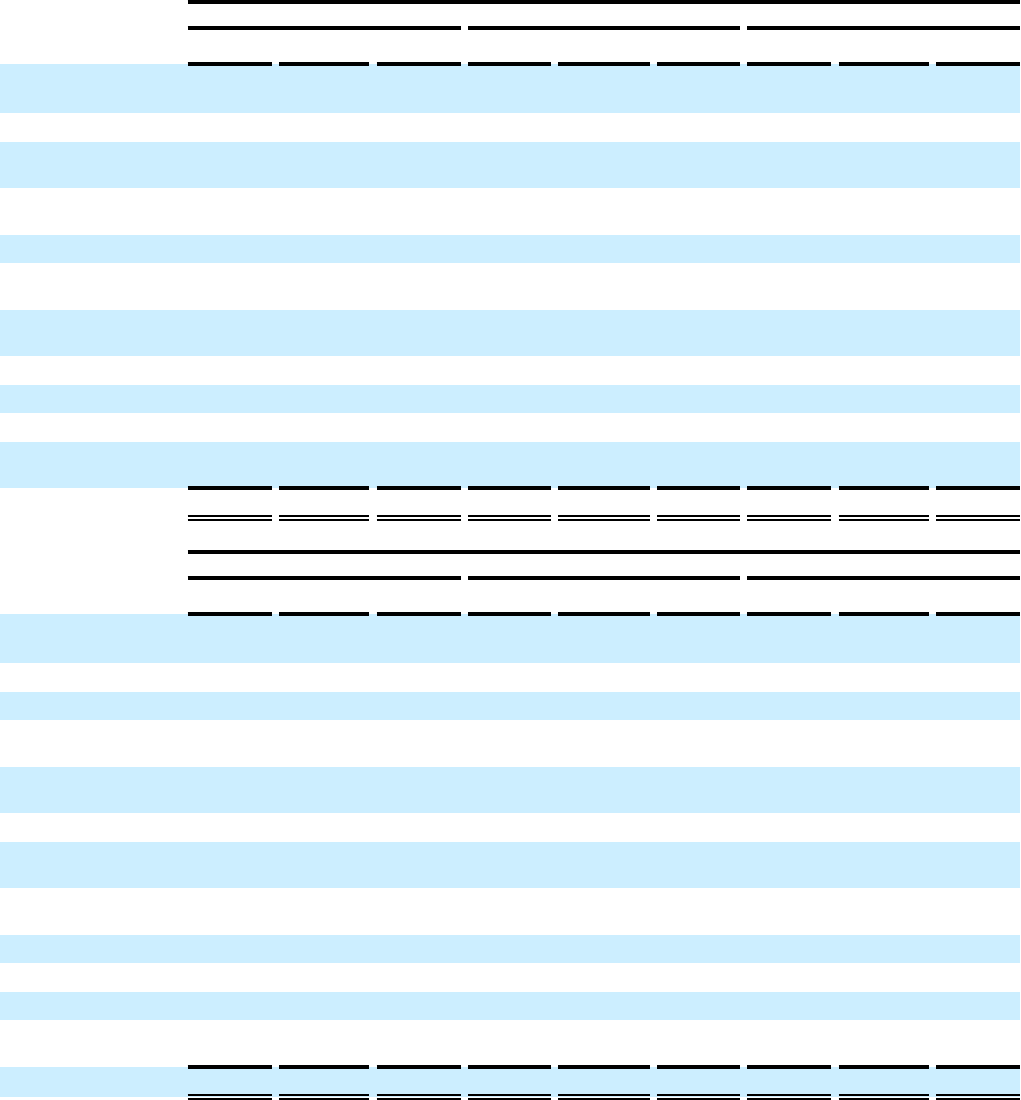

Over the 20-year period shown in the table above, our loans have performed on

average 110 basis points better than our initial forecasts. Loans originated in six of the

20 years have yielded actual collection results worse than our initial estimates. What

is noteworthy, however, is that the underperformance was modest. As a result, loans

originated in those six years were still protable, even though they performed worse than

we had forecast.

We have understood for many years that expecting to predict the performance of our

loans with exacting precision is not realistic. For this reason, we have made it a priority

to maintain a margin of safety so that, even if our forecasts prove to be optimistic, our

loans, on average, will still be protable. Because of this approach, we believe we can

withstand a signicant deterioration in loan performance and still have an opportunity to

move forward and create signicant value for our shareholders.

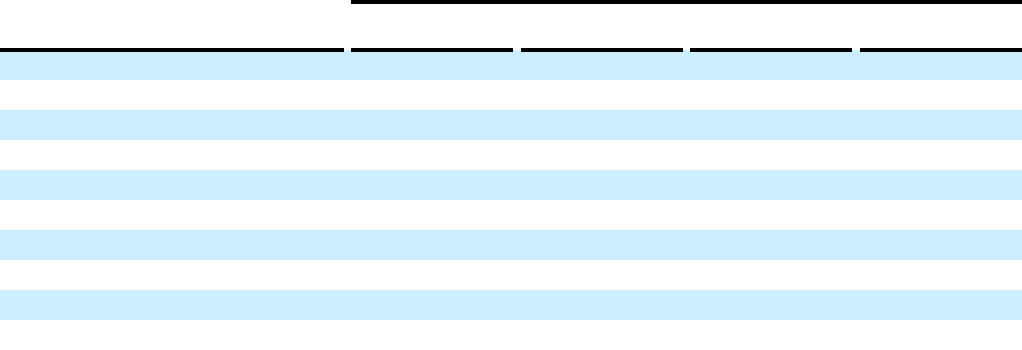

SUPPLEMENTAL FINANCIAL RESULTS

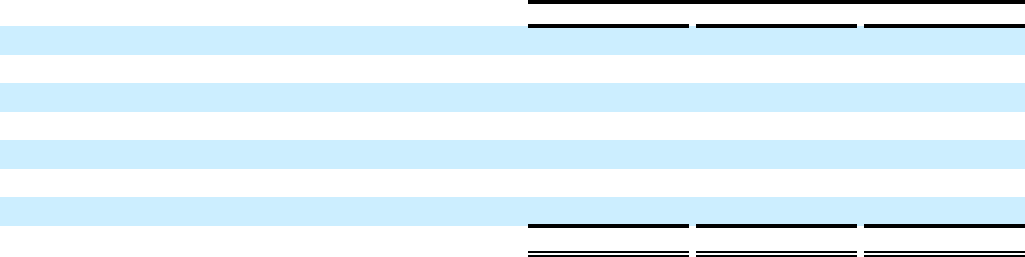

GAAP Results

The table below summarizes our results over the last 20 years under accounting

principles generally accepted in the United States of America (GAAP):

GAAP net income

per share (diluted)

Year-to-year change in

GAAP net income per share

Return

on equity

1

2002 $ 0.69 10.1

%

2003 $ 0.57 −17.4% 7.5

%

2004 $ 1.40 145.6% 18.4

%

2005 $ 1.85 32.1% 21.8

%

2006 $ 1.66 −10.3% 20.2

%

2007 $ 1.76 6.0% 23.1

%

2008 $ 2.16 22.7% 22.2

%

2009 $ 4.62 113.9% 35.6

%

2010 $ 5.67 22.7% 34.8

%

2011 $ 7.07 24.7% 40.0

%

2012 $ 8.58 21.4% 37.8

%

2013 $ 10.54 22.8% 38.0

%

2014 $ 11.92 13.1% 37.0

%

2015 $ 14.28 19.8% 35.4

%

2016 $ 16.31 14.2% 31.1

%

2017 $ 24.04 47.4% 36.9

%

2018 $ 29.39 22.3% 31.7

%

2019 $ 34.57 17.6% 29.8

%

2020 $ 23.47 −32.1% 19.2

%

2021 $ 59.52 153.6% 43.3

%

Compound annual growth rate 2002–2021 26.4%

Average annual return on equity 2002–2021 28.7 %

1

Return on equity is dened as GAAP net income for the applicable period divided by average shareholders’ equity for such period.

13

2021 ANNUAL REPORT

|

SHAREHOLDER LETTER2021 ANNUAL REPORT

|

SHAREHOLDER LETTER

Over the last 20 years, GAAP net income per share (diluted) has grown at a

compounded annual rate of 26.4%, with an average annual return on equity of 28.7%.

Last year, GAAP net income per share (diluted) increased 153.6% to $59.52, with a

return on equity of 43.3%. The increase was primarily due to stronger than expected

collections. The “Adjusted Results” section below explains our nancial results after

considering the impact of the current expected credit loss (CECL) accounting standard

and other accounting-related items.

Adjusted Results

Our business model is dierent from that of a typical lender and doesn’t t neatly into

GAAP. The adoption of CECL at the beginning of 2020 means we have now been

required to use three dierent GAAP accounting methods over the period we have been

public, even though our business hasn’t materially changed during that time. In 1992,

the year we became a public company, we accounted for our business as a lender to

consumers. In 2005, our external auditors decided we were a lender to dealers, which

required dierent accounting. CECL is now the latest new methodology we are required

to use. Unfortunately, none of the three GAAP methods results in nancial statements

that are consistent with how we think about our business. To solve this problem, we

began reporting adjusted results using an accounting method that we believe is simple

to understand, is consistently presented, and matches the economics of our business. To

explain this method, some additional background is needed.

Most of the automobile dealers we enroll receive two types of payments from us. The

rst payment is made at the time of origination. The remaining payments are remitted

over time based on the performance of the loan. The amount we pay at the time of

origination is called an advance; the portion paid over time is called dealer holdback.

The nance charge revenue we recognize over the life of a loan equals the cash we

collect from the loan (i.e., repayments by the consumer), less the amounts we pay to

the dealer (advance + dealer holdback). In other words, the nance charge revenue we

recognize over the life of the loan equals the cash inows from the loan less the cash

outows to acquire the loan. This amount, plus a modest amount of revenue from other

sources, less our operating expenses, interest and taxes, is the sum that will ultimately

be paid to shareholders or reinvested in new assets.

For our adjusted nancial results, we recognize nance charge revenue on a level-yield

basis. That is, the amount of nance charge revenue recognized in a given period,

divided by the loan asset, is a constant percentage. Since the future cash ows from

a loan are not known with certainty, we use statistical models to forecast the amount

of cash ows from each loan. Our nance charge revenue is recorded based on these

estimates. As the estimates change, we adjust the yield. This method produces nancial

results that we believe are a close approximation of the actual economics of our

business.

14

2021 ANNUAL REPORT

|

SHAREHOLDER LETTER

While our adjusted methodology is simple and closely represents the actual economics

of our business, we do not believe that our GAAP nancial results provide sucient

transparency into the economics of our business. To explain this, we will focus on the

current GAAP methodology as our two prior GAAP methodologies have been discussed

in previous years. As noted earlier, the current required GAAP methodology is called

CECL. Like the adjusted methodology described above, CECL requires a level-yield

approach for recognizing nance charge revenue. However, the yield under CECL is

not the yield that we expect to earn on the loan. Instead, the yield is what we would

earn if every payment were received according to the contractual terms of the loan, a

gure much higher than what we actually expect to earn. Based on this alone, you might

expect CECL to overstate our protability. But CECL, like any accounting standard,

doesn’t change the total amount of income recorded, it only changes the timing.

Eventually, the true cash prots and the accounting prots need to match.

To arrive at a result that eventually matches the cash prot, CECL requires us to oset

the additional revenue that it causes to be recorded over the life of the loan with an

additional expense in an equivalent amount. The expense is recorded as a provision for

credit losses at the time the loan is originated. Since no revenue has yet been recorded,

this means that under CECL, our nancial statements reect an initial loss on each loan

we originate, a result which does not match the economics of the transaction.

CECL also diers from our adjusted methodology in the way it treats changes in

expected cash ows. As mentioned above, for the adjusted results, we treat those

changes as yield adjustments. In contrast, CECL treats changes in expected cash

ows as a current-period expense (for unfavorable changes) or reversal of expense (for

favorable changes). The combination of the three CECL-required steps—(1) recording a

large expense at loan inception, (2) recording nance charge revenue at a yield higher

than the yield we expect to earn, and (3) recording forecast changes through the income

statement in the current period—can make it dicult to understand the performance of

our business using our GAAP-based nancial statements. The oating yield adjustment

in the tables below addresses all three of these issues by eliminating the provision for

credit losses recorded in our GAAP statements and modifying GAAP-based nance

charges so the yield is equal to the one we expect to earn on the loan.

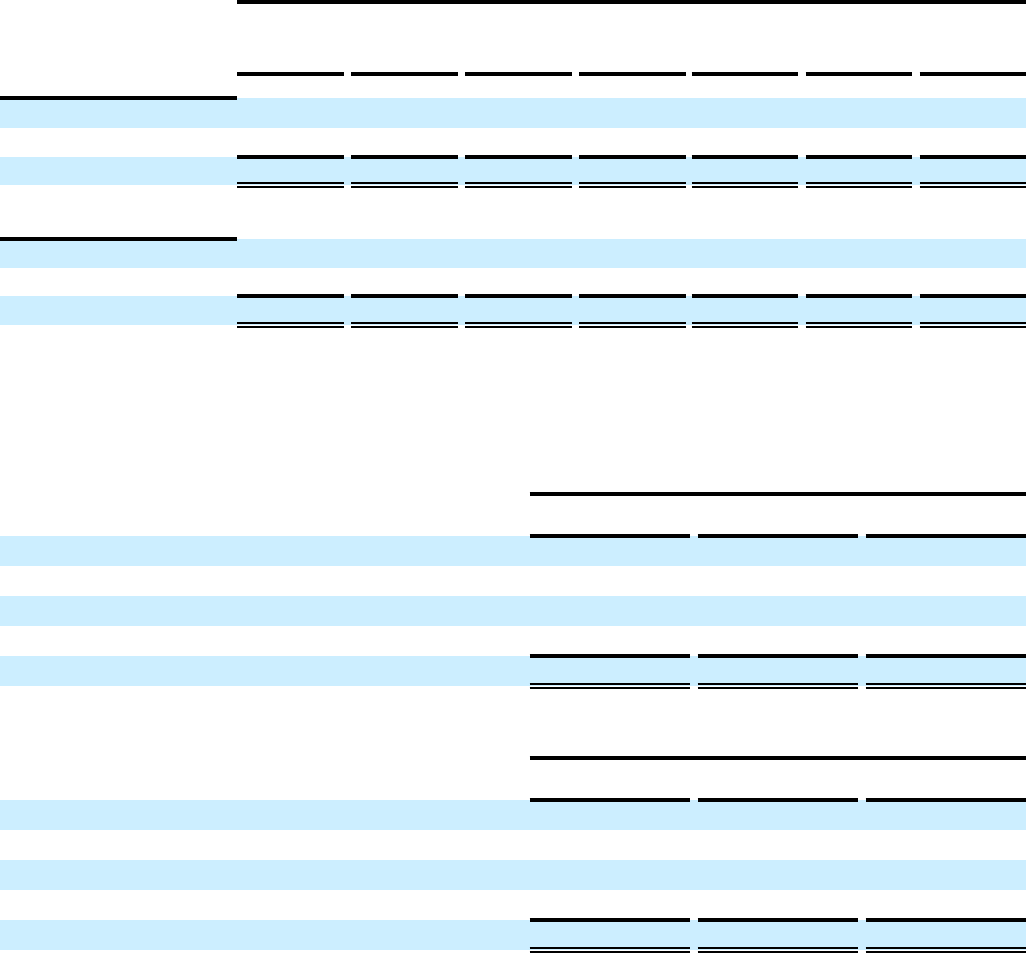

The tables below show net income and net income per share (diluted) for the last 20

years on both a GAAP and an adjusted basis. Besides the oating yield adjustment, the

tables include several other categories of adjustments that are generally less material.

The notable exception is the income tax adjustment in 2017, which reverses the one-

time benet arising from the 2017 Tax Cuts and Jobs Act. While the benet recorded

in 2017 represented a real cash savings due to the reduction in income tax rates, we

reversed it for adjusted net income as we prefer to measure the performance of the

business using consistent tax rates. To that end, we calculated adjusted net income

using a 37% tax rate for 2002–2017 and a 23% tax rate for 2018–2021. The other, less-

material adjustments are explained in prior-year CEO shareholder letters.

15

2021 ANNUAL REPORT

|

SHAREHOLDER LETTER2021 ANNUAL REPORT

|

SHAREHOLDER LETTER

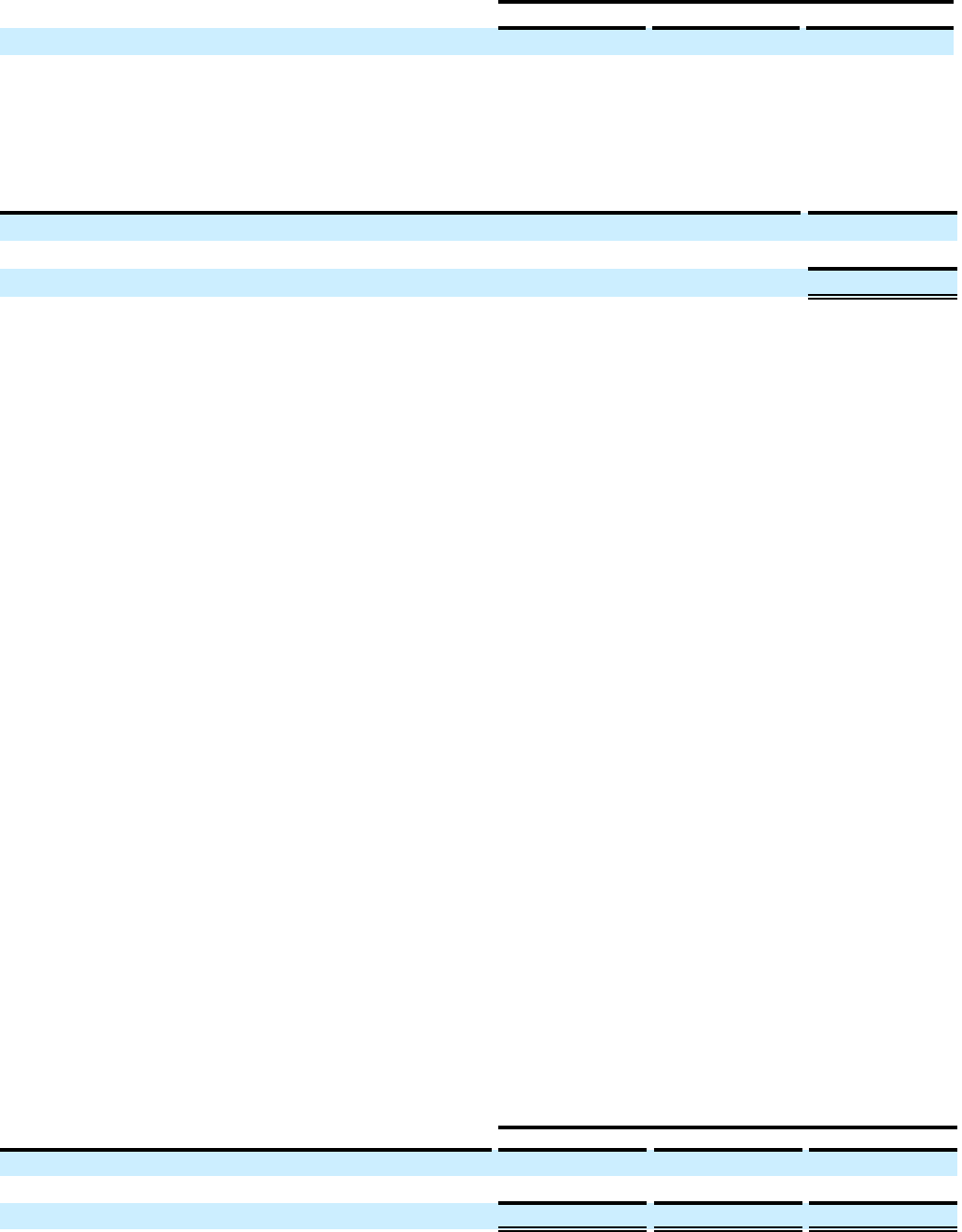

($ in millions)

GAAP net

income

Floating yield

adjustment

Senior notes

adjustment

Income tax

adjustment

Other

adjustments

Adjusted net

income

Year-to-year

change

2002 $ 29.8 $ 2.8 $ — $ 2.9 $ (4.5) $ 31.0

2003 $ 24.7 $ 1.4 $ — $ 5.7 $ 5.6 $ 37.4 20.6%

2004 $ 57.3 $ (0.1) $ — $ (1.8) $ (3.2) $ 52.2 39.6%

2005 $ 72.6 $ (2.2) $ — $ 0.1 $ (7.3) $ 63.2 21.1%

2006 $ 58.6 $ 0.4 $ — $ (1.7) $ 4.4 $ 61.7 -2.4%

2007 $ 54.9 $ 3.6 $ — $ (1.2) $ 4.4 $ 61.7 0.0%

2008 $ 67.2 $ 13.1 $ — $ 0.4 $ 2.1 $ 82.8 34.2%

2009 $ 146.3 $ (19.6) $ — $ (1.8) $ 0.1 $ 125.0 51.0%

2010 $ 170.1 $ 0.5 $ — $ (10.4) $ 0.3 $ 160.5 28.4%

2011 $ 188.0 $ 7.1 $ — $ (1.3) $ 0.3 $ 194.1 20.9%

2012 $ 219.7 $ — $ — $ (3.5) $ — $ 216.2 11.4%

2013 $ 253.1 $ (2.5) $ — $ (2.3) $ — $ 248.3 14.8%

2014 $ 266.2 $ (6.0) $

12.5

$

(1.0)

$

—

$ 271.7 9.4%

2015 $ 299.7 $ 12.9 $

(2.0)

$

(0.8)

$

—

$ 309.8 14.0%

2016 $ 332.8 $ 28.1 $

(2.1)

$

1.8

$

—

$ 360.6 16.4%

2017 $ 470.2 $ 34.1 $

(2.1)

$

(102.4)

$

—

$ 399.8 10.9%

2018 $ 574.0 $ (24.4) $

(2.5)

$

7.4

$

—

$ 554.5 38.7%

2019 $ 656.1 $ 0.2 $

(0.8)

$

2.9

$

—

$ 658.4 18.7%

2020 $ 421.0 $ 259.2 $

4.0

$

2.1

$

—

$ 686.3 4.2%

2021 $ 958.3 $ (142.0) $

(2.1)

$

12.6

$

—

$ 826.8 20.5%

Compound annual growth rate 2002 – 2021 18.9%

GAAP net

income

per share

(diluted)

Floating yield

adjustment

per share

(diluted)

Senior notes

adjustment

per share

(diluted)

Income tax

adjustment

per share

(diluted)

Other

adjustments

per share

(diluted)

Adjusted

net income

per share

(diluted)

Year-to-year

change

2002 $ 0.69 $ 0.06 $ — $ 0.07 $ (0.11) $ 0.71

2003 $ 0.57 $ 0.03 $ — $ 0.13 $ 0.13 $ 0.86 21.1%

2004 $ 1.40 $ — $ — $ (0.04) $ (0.09) $ 1.27 47.7%

2005 $ 1.85 $ (0.06) $ — $ — $ (0.18) $ 1.61 26.8%

2006 $ 1.66 $ 0.01 $ — $ (0.05) $ 0.13 $ 1.75 8.7%

2007 $ 1.76 $ 0.11 $ — $ (0.04) $ 0.15 $ 1.98 13.1%

2008 $ 2.16 $ 0.42 $ — $ 0.01 $ 0.07 $ 2.66 34.3%

2009 $ 4.62 $ (0.62) $ — $ (0.06) $ 0.01 $ 3.95 48.5%

2010 $ 5.67 $ 0.02 $ — $ (0.35) $ 0.01 $ 5.35 35.4%

2011 $ 7.07 $ 0.26 $ — $ (0.04) $ 0.01 $ 7.30 36.4%

2012 $ 8.58 $ — $ — $ (0.13) $ — $ 8.45 15.8%

2013 $ 10.54 $ (0.11) $ — $ (0.09) $ — $ 10.34 22.4%

2014 $ 11.92 $ (0.27) $ 0.56 $ (0.04) $ — $ 12.17 17.7%

2015 $ 14.28 $ 0.62 $ (0.10) $ (0.03) $ — $ 14.77 21.4%

2016 $ 16.31 $ 1.37 $ (0.10) $ 0.09 $ — $ 17.67 19.6%

2017 $ 24.04 $ 1.74 $ (0.11) $ (5.23) $ — $ 20.44 15.7%

2018 $ 29.39 $ (1.25) $ (0.13) $ 0.38 $ — $ 28.39 38.9%

2019 $ 34.57 $ 0.01 $ (0.04) $ 0.16 $ — $ 34.70 22.2%

2020 $ 23.47 $ 14.45 $ 0.22 $ 0.12 $ — $ 38.26 10.3%

2021 $ 59.52 $ (8.82) $ (0.13) $ 0.78 $ — $ 51.35 34.2%

Compound annual growth rate 2002 – 2021 25.3%

16

2021 ANNUAL REPORT

|

SHAREHOLDER LETTER

As the second table shows, adjusted net income per share (diluted) increased 34.2%

in 2021. Since 2002, adjusted net income per share (diluted) has increased at a

compounded annual rate of 25.3%. The strong growth in net income per share (diluted)

last year is attributable to the higher than expected collections received during 2021.

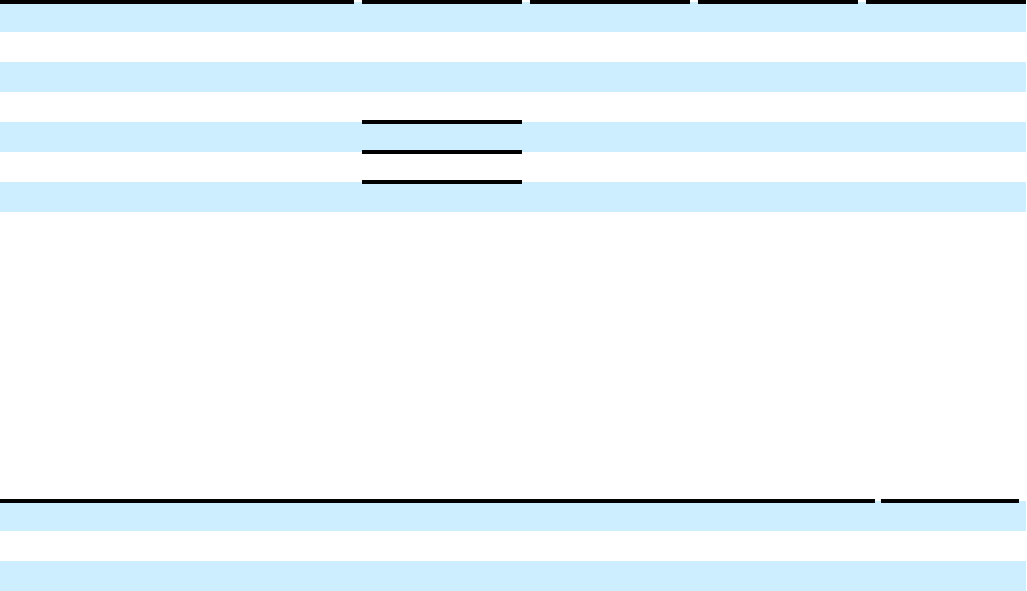

Economic Profit

We use a non-GAAP nancial measure called Economic Prot to evaluate our nancial

results and determine certain incentive compensation. We also use Economic Prot as a

framework to evaluate business decisions and strategies, with an objective to maximize

Economic Prot over the long term. Economic Prot measures how eciently we utilize

our total capital, both debt and equity, and is a function of the return on capital in excess

of the cost of capital and the amount of capital invested in the business. Economic Prot

diers from net income in that it includes a cost for equity capital.

The following table summarizes Economic Prot for 2002–2021:

1

($ in millions)

Adjusted net

income

Imputed cost

of equity

2

Economic

Prot

Year-

to-year

change

2002 $ 31.0 $ (35.6) $ (4.6)

2003 $ 37.4 $ (34.5) $ 2.9 —

2004 $ 52.2 $ (34.4) $ 17.8 513.8%

2005 $ 63.2 $ (34.5) $ 28.7 61.2%

2006 $ 61.7 $ (29.6) $ 32.1 11.8%

2007 $ 61.7 $ (27.2) $ 34.5 7.5%

2008 $ 82.8 $ (35.8) $ 47.0 36.2%

2009 $ 125.0 $ (45.9) $ 79.1 68.3%

2010 $ 160.5 $ (47.8) $ 112.7 42.5%

2011 $ 194.1 $ (51.0) $ 143.1 27.0%

2012 $ 216.2 $ (56.6) $ 159.6 11.5%

2013 $ 248.3 $ (75.1) $ 173.2 8.5%

2014 $ 271.7 $ (87.5) $ 184.2 6.4%

2015 $ 309.8 $ (93.2) $ 216.6 17.6%

2016 $ 360.6 $ (113.8) $ 246.8 13.9%

2017 $ 399.8 $ (142.8) $ 257.0 4.1%

2018 $ 554.5 $ (214.1) $ 340.4 32.5%

2019 $ 658.4 $ (225.7) $ 432.7 27.1%

2020 $ 686.3 $ (215.0) $ 471.3 8.9%

2021 $ 826.8 $ (252.7) $ 574.1 21.8%

Compound annual growth rate 2003 – 2021 34.1%

Economic Prot improved 21.8% in 2021, to $574.1 million from $471.3 million in 2020.

In 2002, Economic Prot had been a negative $4.6 million.

1

See Exhibit A for a reconciliation of the adjusted nancial measures to the most directly comparable GAAP nancial measures.

2

We determine the imputed cost of equity by using a formula that considers the risk of the business and the risk associated with our use

of debt. The formula is as follows: average equity x {(the average 30-year Treasury rate + 5%) + [(1 – tax rate) x (the average 30-year

Treasury rate + 5% – pre-tax average cost-of-debt rate) x average debt / (average equity + average debt x tax rate)]}.

17

2021 ANNUAL REPORT

|

SHAREHOLDER LETTER2021 ANNUAL REPORT

|

SHAREHOLDER LETTER

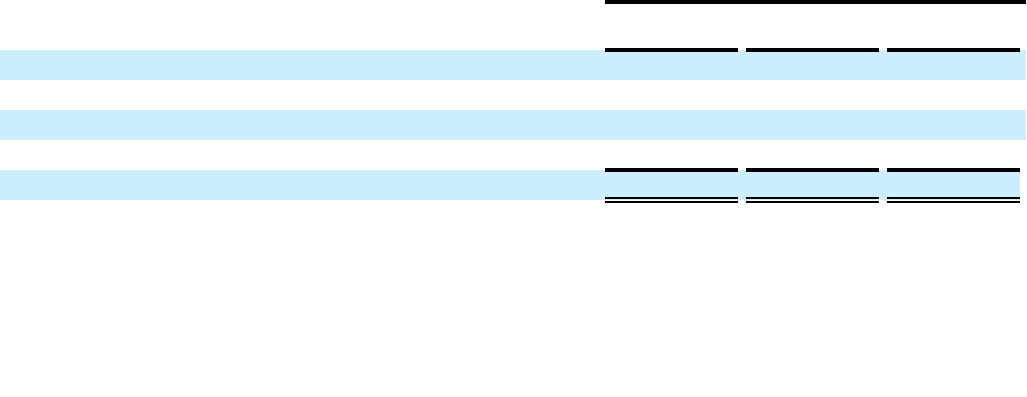

Economic Prot is a function of three variables: the adjusted average amount of capital

invested, the adjusted return on capital, and the adjusted weighted average cost of

capital. The following table summarizes our nancial performance in these areas over

the last 20 years:

1

($ in millions)

Adjusted average

capital invested

Adjusted return

on capital

Adjusted weighted

average cost of capital Spread

2002 $ 462.0 7.9% 8.9% −1.0%

2003 $ 437.5 9.7% 9.0% 0.7%

2004 $ 483.7 12.3% 8.6% 3.7%

2005 $ 523.4 13.7% 8.3% 5.4%

2006 $ 548.5 13.9% 8.1% 5.8%

2007 $ 710.1 11.9% 7.0% 4.9%

2008 $ 975.0 11.3% 6.4% 4.9%

2009 $ 998.7 14.6% 6.7% 7.9%

2010 $ 1,074.2 17.7% 7.2% 10.5%

2011 $ 1,371.1 16.8% 6.4% 10.4%

2012 $ 1,742.8 14.7% 5.5% 9.2%

2013 $ 2,049.2 14.1% 5.7% 8.4%

2014 $ 2,338.1 13.2% 5.3% 7.9%

2015 $ 2,831.9 12.7% 5.0% 7.7%

2016 $ 3,572.0 11.9% 5.0% 6.9%

2017 $ 4,276.4 11.2% 5.2% 6.0%

2018 $ 5,420.9 12.5% 6.2% 6.3%

2019 $ 6,372.2 12.7% 6.0% 6.7%

2020 $ 7,076.0 11.8% 5.2% 6.6%

2021 $ 7,078.4 13.5% 5.4% 8.1%

Compound annual growth rate 2002 – 2021 15.4%

1

See Exhibit A for a reconciliation of the adjusted nancial measures to the most directly comparable GAAP nancial measures.

As the table shows, we earned less than our cost of capital in 2002. From 2003 to 2011,

Economic Prot improved as a result of growth in average capital, higher returns on

capital and lower costs of capital. In 2003, our return on capital was 9.7%. In 2011, as

a result of a favorable competitive environment, it was 16.8%. Since 2011, almost all

of the growth in Economic Prot has occurred from increasing average capital. In each

year from 2011 through 2017, the return on capital declined as competition returned to

our market. The trend reversed in 2018 as our return on capital improved, by 130 basis

points, due to a change in the federal tax rate. In 2019, our return on capital increased

again, but by only 20 basis points.

In 2020, our return on capital declined by 90 basis points due to the impact of COVID-19

on loan performance. With hindsight, our downward forecast adjustment recorded in the

rst quarter of 2020 was too large. In 2021, much of the 170-basis point improvement in

our return on capital was due to increased collections and improvement in our forecast.

18

2021 ANNUAL REPORT

|

SHAREHOLDER LETTER

There are several additional points worth mentioning. First, we have grown adjusted

average capital each year starting in 2004. The growth is a direct result of our success

in growing the number of active dealers. While variables like volume per dealer and

contract size impact adjusted average capital growth as well, the trend in the number of

active dealers tells us much of what we need to know to understand the trajectory of our

business. Growing the number of active dealers makes future Economic Prot growth

likely. If we are unable to grow the number of active dealers, Economic Prot growth

will likely stall. This is important since in the last two years the number of active dealers

declined. While the pandemic and related vehicle shortages contributed to this decline,

the downturn follows a trend of decelerating growth which began in 2016.

Second, while the return on capital has been volatile, expenses as a percentage of

adjusted average capital have declined for 13 of the last 15 years, to 5.4% in 2021 from

15.1% in 2006. This underscores the importance of growing average capital. As long

as the return on incremental capital invested exceeds the cost of that capital, growing

average capital increases Economic Prot directly. In addition, growing average capital

improves the return on capital by reducing the impact of expenses, since a portion of our

expenses is xed. The volatility in the return on capital is due to the revenue component,

which moves up and down based on the competitive environment. When the competitive

environment is favorable, we reduce advance rates (the amount we pay the dealer

at loan origination), and that increases our return. When the competitive environment

worsens, the opposite occurs. But growing expenses more slowly than capital allows us

to achieve greater returns in both favorable and unfavorable environments.

19

2021 ANNUAL REPORT

|

SHAREHOLDER LETTER2021 ANNUAL REPORT

|

SHAREHOLDER LETTER

EXHIBIT A

Reconciliation of GAAP Financial Results to Non-GAAP Measures

($ in

millions)

GAAP

net

income

Floating

yield

adjustment

Senior

notes

adjustment

Income

tax

adjustment

Other

adjustments

Adjusted

net

income

Imputed

cost of

equity

Economic

Prot

2002 $ 29.8 $ 2.8 $ — $ 2.9 $ (4.5) $ 31.0 $ (35.6) $ (4.6)

2003 $ 24.7 $ 1.4 $ — $ 5.7 $ 5.6 $ 37.4 $ (34.5) $ 2.9

2004 $ 57.3 $ (0.1) $ — $ (1.8) $ (3.2) $ 52.2 $ (34.4) $ 17.8

2005 $ 72.6 $ (2.2) $ — $ 0.1 $ (7.3) $ 63.2 $ (34.5) $ 28.7

2006 $ 58.6 $ 0.4 $ — $ (1.7) $ 4.4 $ 61.7 $ (29.6) $ 32.1

2007 $ 54.9 $ 3.6 $ — $ (1.2) $ 4.4 $ 61.7 $ (27.2) $ 34.5

2008 $ 67.2 $ 13.1 $ — $ 0.4 $ 2.1 $ 82.8 $ (35.8) $ 47.0

2009 $ 146.3 $ (19.6) $ — $ (1.8) $ 0.1 $ 125.0 $ (45.9) $ 79.1

2010 $ 170.1 $ 0.5 $ — $ (10.4) $ 0.3 $ 160.5 $ (47.8) $ 112.7

2011 $ 188.0 $ 7.1 $ — $ (1.3) $ 0.3 $ 194.1 $ (51.0) $ 143.1

2012 $ 219.7 $ — $ — $ (3.5) $ — $ 216.2 $ (56.6) $ 159.6

2013 $ 253.1 $ (2.5) $ — $ (2.3) $ — $ 248.3 $ (75.1) $ 173.2

2014 $ 266.2 $ (6.0) $ 12.5 $ (1.0) $ — $ 271.7 $ (87.5) $ 184.2

2015 $ 299.7 $ 12.9 $ (2.0) $ (0.8) $ — $ 309.8 $ (93.2) $ 216.6

2016 $ 332.8 $ 28.1 $ (2.1) $ 1.8 $ — $ 360.6 $ (113.8) $ 246.8

2017 $ 470.2 $ 34.1 $ (2.1) $ (102.4) $ — $ 399.8 $ (142.8) $ 257.0

2018 $ 574.0 $ (24.4) $ (2.5) $ 7.4 $ — $ 554.5 $ (214.1) $ 340.4

2019 $ 656.1 $ 0.2 $ (0.8) $ 2.9 $ — $ 658.4 $ (225.7) $ 432.7

2020 $ 421.0 $ 259.2 $ 4.0 $ 2.1 $ — $ 686.3 $ (215.0) $ 471.3

2021 $ 958.3 $ (142.0) $ (2.1) $ 12.6 $ — $ 826.8 $ (252.7) $ 574.1

20

2021 ANNUAL REPORT

|

SHAREHOLDER LETTER

($ in

millions)

GAAP

average capital

invested

1

Floating

yield

adjustment

Senior

notes

adjustment

Deferred debt

issuance

adjustment

2

Income

tax

adjustment

Other

adjustments

Adjusted

average capital

invested

2002 $ 457.1 $ 5.8 $ — $ 0.5 $ — $ (1.4) $ 462.0

2003 $ 430.3 $ 7.9 $ — $ 1.7 $ — $ (2.4) $ 437.5

2004 $ 476.5 $ 8.7 $ — $ 1.8 $ — $ (3.3) $ 483.7

2005 $ 519.4 $ 7.5 $ — $ 1.0 $ — $ (4.5) $ 523.4

2006 $ 548.0 $ 5.5 $ — $ 2.0 $ — $ (7.0) $ 548.5

2007 $ 706.1 $ 8.2 $ — $ 1.7 $ — $ (5.9) $ 710.1

2008 $ 960.7 $ 13.8 $ — $ 2.9 $ — $ (2.4) $ 975.0

2009 $ 983.6 $ 13.2 $ — $ 2.9 $ — $ (1.0) $ 998.7

2010 $ 1,057.3 $ 5.2 $ — $ 12.2 $ — $ (0.5) $ 1,074.2

2011 $ 1,346.0 $ 9.4 $ — $ 16.0 $ — $ (0.3) $ 1,371.1

2012 $ 1,715.3 $ 11.1 $ — $ 16.4 $ — $ — $ 1,742.8

2013 $ 2,024.5 $ 9.9 $ — $ 14.8 $ — $ — $ 2,049.2

2014 $ 2,324.8 $ 6.7 $ (7.0) $ 13.6 $ — $ — $ 2,338.1

2015 $ 2,792.8 $ 7.0 $ 14.7 $ 17.4 $ — $ — $ 2,831.9

2016 $ 3,513.1 $ 29.6 $ 12.7 $ 16.6 $ — $ — $ 3,572.0

2017 $ 4,200.2 $ 51.6 $ 10.6 $ 18.1 $ (4.1) $ — $ 4,276.4

2018 $ 5,425.8 $ 80.8 $ 9.7 $ 22.4 $ (117.8) $ — $ 5,420.9

2019 $ 6,399.2 $ 66.2 $ 0.6 $ 24.7 $ (118.5) $ — $ 6,372.2

2020 $ 6,874.7 $ 287.6 $ 5.5 $ 26.7 $ (118.5) $ — $ 7,076.0

2021 $ 6,914.1 $ 243.0 $ 10.8 $ 29.0 $ (118.5) $ — $ 7,078.4

1

Average capital invested is dened as average debt plus average shareholders’ equity.

2

The deferred debt issuance adjustment reverses the impact of the reclassication of deferred debt issuance costs from other assets to GAAP average debt as a

result of the adoption by the Financial Accounting Standards Board of Accounting Standards Update (ASU) No. 2015-03, as amended by ASU No. 2015-05. The

net eect of this adjustment is to report adjusted average capital on the same basis as reported in historical shareholder letters.

21

2021 ANNUAL REPORT

|

SHAREHOLDER LETTER2021 ANNUAL REPORT

|

SHAREHOLDER LETTER

GAAP

return

on capital

1

Floating

yield

adjustment

Senior

notes

adjustment

Deferred debt

issuance

adjustment

2

Income

tax

adjustment

Other

adjustments

Adjusted

return

on capital

2002 7.7% 0.5% 0.0% 0.0% 0.6% −0.9% 7.9%

2003 6.9% 0.2% 0.0% 0.0% 1.3% 1.3% 9.7%

2004 13.5% −0.3% 0.0% 0.0% −0.3% −0.6% 12.3%

2005 15.6% −0.6% 0.0% 0.0% 0.0% −1.3% 13.7%

2006 13.3% −0.1% 0.0% 0.0% −0.3% 1.0% 13.9%

2007 11.0% 0.4% 0.0% 0.0% −0.2% 0.7% 11.9%

2008 9.8% 1.2% 0.0% 0.0% 0.0% 0.3% 11.3%

2009 17.0% −2.2% 0.0% 0.0% −0.2% 0.0% 14.6%

2010 18.9% 0.0% 0.0% −0.2% −1.0% 0.0% 17.7%

2011 16.7% 0.4% 0.0% −0.2% −0.1% 0.0% 16.8%

2012 15.1% −0.1% 0.0% −0.1% −0.2% 0.0% 14.7%

2013 14.5% −0.2% 0.0% −0.1% −0.1% 0.0% 14.1%

2014 13.1% −0.3% 0.5% −0.1% 0.0% 0.0% 13.2%

2015 12.5% 0.4% −0.1% −0.1% 0.0% 0.0% 12.7%

2016 11.3% 0.7% −0.1% 0.0% 0.0% 0.0% 11.9%

2017 13.0% 0.7% −0.1% −0.1% −2.3% 0.0% 11.2%

2018 12.8% −0.6% −0.1% 0.0% 0.4% 0.0% 12.5%

2019 12.6% −0.1% 0.0% 0.0% 0.2% 0.0% 12.7%

2020 8.3% 3.3% 0.0% 0.0% 0.2% 0.0% 11.8%

2021 15.7% −2.5% 0.0% −0.1% 0.4% 0.0% 13.5%

1

Return on capital is dened as net income plus after-tax interest expense divided by average capital.

2

The deferred debt issuance adjustment reverses the impact of the reclassication of deferred debt issuance costs from other assets to GAAP average debt as a

result of the adoption by the Financial Accounting Standards Board of Accounting Standards Update (ASU) No. 2015-03, as amended by ASU No. 2015-05. The

net eect of this adjustment is to report adjusted average capital on the same basis as reported in historical shareholder letters.

22

2021 ANNUAL REPORT

|

SHAREHOLDER LETTER

GAAP

weighted

average cost

of capital

1

Floating

yield

adjustment

Senior

notes

adjustment

Deferred debt

issuance

adjustment

2

Income

tax

adjustment

Other

adjustments

Adjusted

weighted average

cost of capital

3

2002 8.9% 0.0% 0.0% 0.0% 0.0% 0.0% 8.9%

2003 9.0% 0.0% 0.0% 0.0% 0.0% 0.0% 9.0%

2004 8.6% 0.0% 0.0% 0.0% 0.0% 0.0% 8.6%

2005 8.3% 0.0% 0.0% 0.0% 0.0% 0.0% 8.3%

2006 8.1% 0.0% 0.0% 0.0% 0.0% 0.0% 8.1%

2007 7.0% 0.0% 0.0% 0.0% 0.0% 0.0% 7.0%

2008 6.4% 0.0% 0.0% 0.0% 0.0% 0.0% 6.4%

2009 6.7% 0.0% 0.0% 0.0% 0.0% 0.0% 6.7%

2010 7.3% 0.0% 0.0% −0.1% 0.0% 0.0% 7.2%

2011 6.5% 0.0% 0.0% −0.1% 0.0% 0.0% 6.4%

2012 5.6% 0.0% 0.0% −0.1% 0.0% 0.0% 5.5%

2013 5.7% 0.0% 0.0% 0.0% 0.0% 0.0% 5.7%

2014 5.2% 0.1% 0.0% 0.0% 0.0% 0.0% 5.3%

2015 5.0% 0.0% 0.0% 0.0% 0.0% 0.0% 5.0%

2016 4.9% 0.1% 0.0% 0.0% 0.0% 0.0% 5.0%

2017 5.1% 0.1% 0.0% 0.0% 0.0% 0.0% 5.2%

2018 6.3% 0.1% 0.0% −0.1% −0.1% 0.0% 6.2%

2019 6.0% 0.1% 0.0% 0.0% −0.1% 0.0% 6.0%

2020 5.1% 0.2% 0.0% 0.0% −0.1% 0.0% 5.2%

2021 5.3% 0.2% 0.0% 0.0% −0.1% 0.0% 5.4%

1

The weighted average cost of capital includes both a cost of equity and a cost of debt. The cost of equity capital is determined based on

a formula that considers the risk of the business and the risk associated with our use of debt. The formula utilized for determining the cost

of equity capital is as follows: (the average 30-year Treasury rate + 5%) + [(1 – tax rate) x (the average 30-year Treasury rate + 5% – pre-

tax average cost-of-debt rate) x average debt / (average equity + average debt x tax rate)].

2

The deferred debt issuance adjustment reverses the impact of the reclassication of deferred debt issuance costs from other assets to

GAAP average debt as a result of the adoption by the Financial Accounting Standards Board of Accounting Standards Update (ASU) No.

2015-03, as amended by ASU No. 2015-05. The net eect of this adjustment is to report adjusted average capital on the same basis as

reported in historical shareholder letters.

3

The adjusted weighted average cost of capital includes both a cost of adjusted equity and a cost of debt. The cost of adjusted equity

capital is calculated using the same formula as above except that adjusted average equity is used in the calculation instead of average

equity.

_________________________________________________________________________________________________________________

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

FORM 10-K

(Mark One)

☑

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2021

OR

☐

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from ______ to ________

Commission file number 000-20202

CREDIT ACCEPTANCE CORPORATION

(Exact name of registrant as specified in its charter)

Michigan

38-1999511

(State or other jurisdiction of incorporation or organization)

(I.R.S. Employer Identification No.)

25505 W. Twelve Mile Road

Southfield,

Michigan

48034-8339

(Address of principal executive offices)

(Zip Code)

Registrant’s telephone number, including area code: (248) 353-2700

Securities registered pursuant to Section 12(b) of the Act:

Title of each class Trading symbol(s)

Name of each exchange on which registered

Common Stock, $.01 par value CACC

The Nasdaq Stock Market LLC

Securities registered pursuant to section 12(g) of the Act:

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes þ No o

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No þ

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12

months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No o

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T

(§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes þ No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth

company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer

☑

Accelerated filer

☐

Non-accelerated filer

☐

Smaller reporting company

☐

Emerging growth company

☐

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial

accounting standards provided pursuant to Section 13(a) of the Exchange Act. o

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial

reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☑

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No þ

The aggregate market value of 6,769,961 shares of the registrant's common stock held by non-affiliates on June 30, 2021 was approximately $3,074.3 million. For purposes of

this computation, all officers, directors and 10% beneficial owners of the registrant are assumed to be affiliates. Such determination should not be deemed an admission that

such officers, directors and beneficial owners are, in fact, affiliates of the registrant.

At February 3, 2022, there were 14,114,355 shares of the registrant's common stock issued and outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant's definitive proxy statement pertaining to the 2022 Annual Meeting of Shareholders (the “Proxy Statement”) filed pursuant to Regulation 14A are

incorporated herein by reference into Part III of this Annual Report on Form 10-K (this “Form 10-K”).

_________________________________________________________________________________________________________________

CREDIT ACCEPTANCE CORPORATION

YEAR ENDED DECEMBER 31, 2021

INDEX TO FORM 10-K

Item Description Page

PART I

1.

Business

3

1A.

Risk Factors

15

1B.

Unresolved Staff Comments

24

2.

Properties

24

3.

Legal Proceedings

25

4.

Mine Safety Disclosures

25

PART II

5.

Market for Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity

Securities

26

6.

[Reserved]

27

7.

Management's Discussion and Analysis of Financial Condition and Results of Operations

28

7A.

Quantitative and Qualitative Disclosures About Market Risk

42

8.

Financial Statements and Supplementary Data

43

9.

Changes in and Disagreements with Accountants on Accounting and Financial Disclosure

96

9A.

Controls and Procedures

96

9B.

Other Information

98

9C.

Disclosure Regarding Foreign Jurisdictions that Prevent Inspections

98

PART III

10.

Directors, Executive Officers and Corporate Governance

98

11.

Executive Compensation

98

12.

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters

98

13.

Certain Relationships and Related Transactions and Director Independence

98

14.

Principal Accounting Fees and Services

98

PART IV

15.

Exhibits, Financial Statement Schedules

99

16.

Form 10-K Summary

107

Signatures

108

2

PART I

ITEM 1. BUSINESS

General

Since 1972, Credit Acceptance Corporation (referred to as the “Company”, “Credit Acceptance”, “we”, “our” or “us”) has

offered financing programs that enable automobile dealers to sell vehicles to consumers, regardless of their credit history. Our

financing programs are offered through a nationwide network of automobile dealers who benefit from sales of vehicles to

consumers who otherwise could not obtain financing; from repeat and referral sales generated by these same customers; and

from sales to customers responding to advertisements for our financing programs, but who actually end up qualifying for

traditional financing.

Without our financing programs, consumers are often unable to purchase vehicles or they purchase unreliable

ones. Further, as we report to the three national credit reporting agencies, an important ancillary benefit of our programs is that

we provide consumers with an opportunity to improve their lives by improving their credit score and move on to more

traditional sources of financing.

Credit Acceptance was founded to collect retail installment contracts (referred to as “Consumer Loans”) originated by

automobile dealerships owned by Donald Foss, our founder. During the 1980s, we began to market this service to non-affiliated

dealers and, at the same time, began to offer dealers a non-recourse cash payment (referred to as an “advance”) against

anticipated future collections on Consumer Loans serviced for that dealer.

We refer to automobile dealers who participate in our programs and who share our commitment to changing consumers’

lives as “Dealers”. Upon enrollment in our financing programs, the Dealer enters into a Dealer servicing agreement with us that

defines the legal relationship between Credit Acceptance and the Dealer. The Dealer servicing agreement assigns the

responsibilities for administering, servicing, and collecting the amounts due on Consumer Loans from the Dealers to us. We

are an indirect lender from a legal perspective, meaning the Consumer Loan is originated by the Dealer and assigned to us.

Substantially all of the Consumer Loans assigned to us are made to consumers with impaired or limited credit histories.

The following table shows the percentage of Consumer Loans assigned to us with either FICO

®

scores below 650 or no FICO

®

scores:

For the Years Ended December 31,

Consumer Loan Assignment Volume 2021 2020 2019

Percentage of total unit volume with either FICO

®

scores

below 650 or no FICO

®

scores 91.0 % 94.9 % 95.9 %

In 2020, we began piloting an option that expanded our financing programs to consumers with higher credit ratings. In the

fourth quarter of 2021, we made this option available to all Dealers. A portion of the reduction in the percentage of total unit

volume with FICO

®

scores below 650 or no FICO

®

scores relates to Consumer Loans assigned under this option.

Business Segment Information

We currently operate in one reportable segment which represents our core business of offering Dealers financing programs

and related products and services that enable them to sell vehicles to consumers, regardless of their credit history. For

information regarding our one reportable segment and related entity-wide disclosures, see Note 15 to the consolidated financial

statements contained in Item 8 of this Form 10-K, which is incorporated herein by reference.

3

Principal Business

We offer our Dealers financing programs that enable them to sell vehicles to consumers, regardless of their credit history.

We have two programs: the Portfolio Program and the Purchase Program. Under the Portfolio Program, we advance money to

Dealers (referred to as a “Dealer Loan”) in exchange for the right to service the underlying Consumer Loans. Under the

Purchase Program, we buy the Consumer Loans from the Dealers (referred to as a “Purchased Loan”) and keep all amounts

collected from the consumer. Dealer Loans and Purchased Loans are collectively referred to as “Loans”. The following table

shows the percentage of Consumer Loans assigned to us under each of the programs for each of the last three years:

Unit Volume Dollar Volume (1)

For the Years Ended December 31, Portfolio Program Purchase Program Portfolio Program Purchase Program

2019 67.2 % 32.8 % 64.3 % 35.7 %

2020 64.1 % 35.9 % 60.6 % 39.4 %

2021 67.9 % 32.1 % 65.0 % 35.0 %

(1) Represents advances paid to Dealers on Consumer Loans assigned under our Portfolio Program and one-time payments made to Dealers to purchase

Consumer Loans assigned under our Purchase Program. Payments of Dealer Holdback (as defined below) and accelerated Dealer Holdback are not

included.

Portfolio Program

As payment for the vehicle, the Dealer generally receives the following:

• a down payment from the consumer;

• a cash advance from us; and

• after the advance balance (cash advance and related Dealer Loan fees and costs) has been recovered by us, the cash

from payments made on the Consumer Loan, net of certain collection costs and our servicing fee (“Dealer

Holdback”).

We record the amount advanced to the Dealer as a Dealer Loan, which is classified within Loans receivable in our

consolidated balance sheets. Cash advanced to the Dealer is automatically assigned to the Dealer’s open pool of advances. Prior

to August 5, 2019, we generally required Dealers to group advances into pools of at least 100 Consumer Loans. Beginning

August 5, 2019, Dealers may also elect to close a pool containing at least 50 Consumer Loans and assign subsequent advances

to a new pool. Unless we receive a request from the Dealer to keep a pool open, we automatically close each pool based on the

Dealer's election. All advances within a Dealer’s pool are secured by the future collections on the related Consumer Loans

assigned to the pool. For Dealers with more than one pool, the pools are cross-collateralized so the performance of other pools

is considered in determining eligibility for Dealer Holdback. We perfect our security interest with respect to the Dealer Loans

by obtaining control or taking possession of the Consumer Loans, which list us as lien holder on the vehicle title.

The Dealer servicing agreement provides that collections received by us during a calendar month on Consumer Loans

assigned by a Dealer are applied on a pool-by-pool basis as follows:

• first, to reimburse us for certain collection costs;

• second, to pay us our servicing fee, which generally equals 20% of collections;

• third, to reduce the aggregate advance balance and to pay any other amounts due from the Dealer to us; and

• fourth, to the Dealer as payment of Dealer Holdback.

If the collections on Consumer Loans from a Dealer’s pool are not sufficient to repay the advance balance and any other

amounts due to us, the Dealer will not receive Dealer Holdback. Certain events may also result in Dealers forfeiting their rights

to Dealer Holdback, including becoming inactive before assigning 100 Consumer Loans.

Dealers have an opportunity to receive an accelerated Dealer Holdback payment each time a pool of Consumer Loans is

closed. The amount paid to the Dealer is calculated using a formula that considers the number of Consumer Loans assigned to

the pool and the related forecasted collections and advance balance.

Since typically the combination of the advance and the consumer’s down payment provides the Dealer with a cash profit at

the time of sale, the Dealer’s risk in the Consumer Loan is limited. We cannot demand repayment of the advance from the

Dealer except in the event the Dealer is in default of the Dealer servicing agreement. Advances are made only after the

consumer and Dealer have signed a Consumer Loan contract, we have received the executed Consumer Loan contract and

supporting documentation in either physical or electronic form, and we have approved all of the related stipulations for

funding.

4

For accounting purposes, the transactions described under the Portfolio Program are not considered to be loans to

consumers. Instead, our accounting reflects that of a lender to the Dealer. The classification as a Dealer Loan for accounting

purposes is primarily a result of (1) the Dealer’s financial interest in the Consumer Loan and (2) certain elements of our legal

relationship with the Dealer.

Purchase Program

The Purchase Program differs from our Portfolio Program in that the Dealer receives a one-time payment from us at the

time of assignment to purchase the Consumer Loan instead of a cash advance at the time of assignment and future Dealer

Holdback payments. For accounting purposes, the transactions described under the Purchase Program are considered to be

originated by the Dealer and then purchased by us.

Program Enrollment

Beginning August 5, 2019, Dealers may enroll in our Portfolio Program without incurring an enrollment fee. Prior to

August 5, 2019, Dealers enrolled in our Portfolio Program by (1) paying an up-front, one-time fee of $9,850, or (2) agreeing to

allow us to retain 50% of their accelerated Dealer Holdback payment(s) on the first 100 Consumer Loan assignments.

Access to the Purchase Program is typically only granted to Dealers that meet one of the following:

• assigned at least 100 Consumer Loans under the Portfolio Program;

• franchise dealership; or

• independent dealership that meets certain criteria upon enrollment.

Revenue Sources

Credit Acceptance derives its revenues from the following principal sources: