ACCOUNTING FOR INCOME TAXES -

INTERIM PERIOD TAX REPORTING

December 2023

OVERVIEW

This whitepaper is the fifth in a series of whitepapers to be used as a resource in understanding

and analyzing the accounting for income taxes under FASB Accounting Standards Codification

(ASC) 740, “Income Taxes”. This whitepaper addresses income tax reporting for interim periods

within an annual period. This requires an understanding of how to calculate an estimated annual

effective tax rate (AETR), as well as identifying discrete items, which are not reflected in the AETR,

but rather reflected in the period incurred. This whitepaper does not address every aspect of

accounting for income taxes and should therefore be read in conjunction with ASC 740.

For ease of use, definitions for acronyms and titles for ASC topics and subtopics and other

literature referred to in this whitepaper are included in Appendix A. In addition, several terms with

specific meaning are used throughout this whitepaper. Those terms and the corresponding

definition are provided in Appendix B.

Financial Reporting Insights

Page 2 of 21 © RSM US LLP

ACCOUNTING FOR INCOME TAXES - INTERIM PERIOD TAX REPORTING DECEMBER 2023

TABLE OF CONTENTS

1. Introduction ......................................................................................................................................... 3

2. Determining the AETR ........................................................................................................................ 5

2.1 AETR definition ........................................................................................................................... 5

2.2 Estimating annual ordinary income (loss) ................................................................................... 5

2.3 Losses incurred in interim periods within a fiscal year ............................................................... 6

2.4 Effect of multiple jurisdictions ................................................................................................... 10

2.5 Computation of the AETR ......................................................................................................... 14

3. Items treated outside of the AETR (discrete items) ....................................................................... 14

3.1 Change in tax laws and rates after adoption of ASU 2019-12 ................................................. 15

3.2 Change in tax status ................................................................................................................. 15

3.3 Change in accounting principle ................................................................................................. 15

3.4 Change in beginning of year valuation allowance .................................................................... 16

3.5 Investment tax credits ............................................................................................................... 16

3.6 Interest and penalties................................................................................................................ 16

3.7 Changes in the recognition of a deferred tax asset related to outside basis differences ......... 16

4. Balance sheet impact ........................................................................................................................ 16

Appendix A: Acronyms ............................................................................................................................ 18

Appendix B: Definitions ........................................................................................................................... 18

Page 3 of 21 © RSM US LLP

ACCOUNTING FOR INCOME TAXES - INTERIM PERIOD TAX REPORTING DECEMBER 2023

1. Introduction

ASC 740-270-25-1

This guidance addresses the issue of how and when income tax expense (or benefit) is recognized

in interim periods and distinguishes between elements that are recognized through the use of an

estimated annual effective tax rate applied to measures of year-to-date operating results, referred

to as ordinary income (or loss), and specific events that are discretely recognized as they occur.

ASC 740-270-25-2

The tax (or benefit) related to ordinary income (or loss) shall be computed at an estimated annual

effective tax rate and the tax (or benefit) related to all other items shall be individually computed

and recognized when the items occur.

Glossary Ordinary Income (or Loss) Ordinary income (or loss) refers to income (or loss) from

continuing operations before income taxes (or benefits) excluding significant unusual or

infrequently occurring items. Discontinued operations and cumulative effects of changes in

accounting principles are also excluded from this term. The term is not used in the income tax

context of ordinary income versus capital gain. The meaning of unusual or infrequently occurring

items is consistent with their use in the definitions of the terms unusual nature and infrequency

of occurrence.

ASC 740-270 establishes the accounting and disclosures for income taxes during interim periods. ASC

740-270-25-1 to 25-2 codifies the key concepts related to interim period tax provisions, which are:

• Using an estimated annual effective tax rate (AETR) as the basis for recognizing income tax expense

or benefit on ordinary income.

• Reflecting any discrete items in the interim period that they occur.

ASC 740-270-05-3 defines an interim period as a component period of the annual reporting period, rather

than merely a time-period of less than a full year. Therefore, ASC 740-270 does not apply to “short

years," since they are not a component part of a larger annual period. Applying the provisions of ASC

740-270 to interim periods would not change the year-end tax provision; it is the method of recognizing or

allocating the annual tax provision to interim periods within the year. Therefore, an entity’s annual tax

provision would be the same whether it prepares interim financial statements or not.

At the end of each interim period, and entity would estimate its AETR for the full year and apply that rate

to the year-to-date results of operations as of the end of that interim period. For interim periods after the

first interim period of the year, the entity would subtract the previously recognized interim period ordinary

income tax expense (benefit) from the year-to-date estimated income tax expense (benefit) provision to

calculate the current period income tax expense (benefit). Inputs to the entity’s AETR include forecasted

full-year ordinary income and forecasted full-year current and deferred tax expense.

Example 1-1: Accounting for Income Taxes Applicable to Ordinary Income at an

Interim Date if Ordinary Income Is Anticipated for the Fiscal Year- Case

A(ASC 740-270-55-2 to 55-4)

Case A has all of the following assumptions:

a. For the full fiscal year, an entity anticipates ordinary income of $100,000. All income is taxable in

one jurisdiction at a 50 percent rate. Anticipated tax credits for the fiscal year total $10,000. No

events that do not have tax consequences are anticipated. No changes in estimated ordinary

income, tax rates, or tax credits occur during the year.

Page 4 of 21 © RSM US LLP

ACCOUNTING FOR INCOME TAXES - INTERIM PERIOD TAX REPORTING DECEMBER 2023

b. Computation of the estimated annual effective tax rate applicable to ordinary income is as follows.

Tax at statutory rate

($100,000 at 50%)

$50,000

Less anticipated tax credits

(10,000)

Net tax to be provided

$40,000

Estimated annual effective tax rate ($40,000 ÷

$100,000)

40%

c. Tax credits are generally subject to limitations, usually based on the amount of tax payable before

the credits. In computing the estimated annual effective tax rate, anticipated tax credits are limited

to the amounts that are expected to be realized or are expected to be recognizable at the end of

the current year in accordance with the provisions of Subtopic 740-10.

Case A: Ordinary Income in All Interim Periods

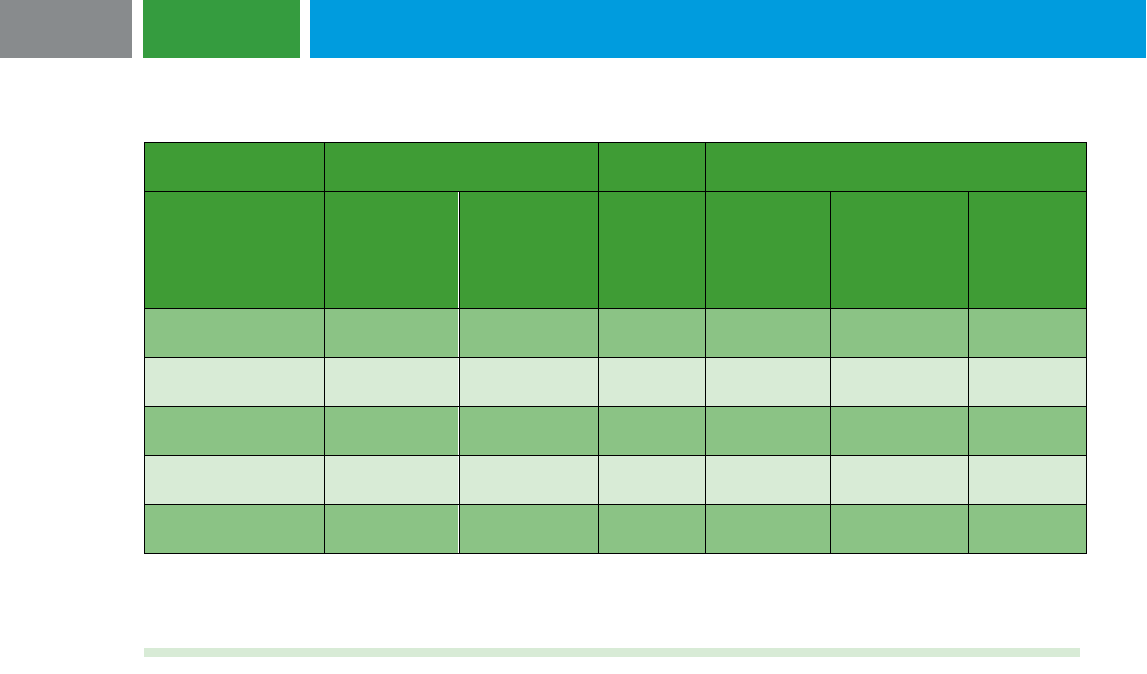

The entity has ordinary income in all interim periods. Quarterly tax computations are as follows:

Ordinary Income

Tax

Reporting Period

Reporting

Period

Year to

Date

Estimated

Annual

Effective

Tax Rate

Year to

Date

Less

Previously

Reported

Reporting

Period

First Quarter

$20,000

$20,000

40%

$8,000

$8,000

Second Quarter

20,000

40,000

40%

16,000

8,000

8,000

Third Quarter

20,000

60,000

40%

24,000

16,000

8,000

Fourth Quarter

40,000

100,000

40%

40,000

24,000

16,000

Fiscal year

$100,000

$40,000

Page 5 of 21 © RSM US LLP

ACCOUNTING FOR INCOME TAXES - INTERIM PERIOD TAX REPORTING DECEMBER 2023

2. Determining the AETR

2.1 AETR definition

ASC 740-270-30-5

The estimated annual effective tax rate, described in paragraphs 740-270-30-6 through 30-8,

shall be applied to the year-to-date ordinary income (or loss) at the end of each interim period to

compute the year-to-date tax (or benefit) applicable to ordinary income (or loss).

ASC 740-270-30-6

At the end of each interim period the entity shall make its best estimate of the effective tax rate

expected to be applicable for the full fiscal year. In some cases, the estimated annual effective

tax rate will be the statutory rate modified as may be appropriate in particular circumstances. In

other cases, the rate will be the entity’s estimate of the tax (or benefit) that will be provided for

the fiscal year, stated as a percentage of its estimated ordinary income (or loss) for the fiscal

year (see paragraphs 740-270-30-30 through 30-34 if an ordinary loss is anticipated for the fiscal

year).

The AETR is the result of the estimated annual income tax expense divided by the estimated pretax

ordinary income. The ratio is then applied to the year-to-date results as of that interim period to measure

the year-to-date income tax expense. The AETR requires a best estimate of the annual ordinary income

and annual income tax expense (i.e., current and deferred taxes), which generally includes all expected

events to occur in the fiscal year that may affect the income tax expense. There are certain exceptions in

creating this estimate, which will be covered in Chapter 3.

The first step in calculating the AETR is estimating the ordinary income (loss) for the year.

2.2 Estimating annual ordinary income (loss)

ASC 740-270-20

Ordinary income (or loss)

Ordinary income (or loss) refers to income (or loss) from continuing operations before

income taxes (or benefits) excluding significant unusual or infrequently occurring items.

Discontinued operations and cumulative effects of changes in accounting principles are

also excluded from this term. The term is not used in the income tax context of ordinary

income versus capital gain. The meaning of unusual or infrequently occurring items is

consistent with their use in the definitions of the terms unusual nature and infrequency of

occurrence.

Unusual Nature

The underlying event or transaction should possess a high degree of abnormality and be

of a type clearly unrelated to, or only incidentally related to, the ordinary and typical

activities of the entity, taking into account the environment in which the entity operates

Infrequency of Occurrence

The underlying event or transaction should be of a type that would not reasonably be

expected to recur in the foreseeable future, taking into account the environment in which

the entity operates

Page 6 of 21 © RSM US LLP

ACCOUNTING FOR INCOME TAXES - INTERIM PERIOD TAX REPORTING DECEMBER 2023

Ordinary income is defined in ASC 740-270-20 as income or loss from continuing operations before

income taxes or benefits, excluding significant unusual or infrequently occurring items. Ordinary income

also excludes discontinued operations and cumulative effects of changes in accounting principles. The

term “ordinary income” is not to be confused with the same phrase used in the income tax context of

“ordinary income versus capital gain.” To determine if an event or transaction would be considered

unusual or infrequent in nature may require judgment of the facts and circumstances, as well as the

entity’s history with similar types of situations. For instance, some non-operating transactions such as

gains or losses from the disposal of a fixed asset may be considered unusual depending on the entity’s

history of disposals and the type of fixed asset. If an entity is constantly replacing machinery in its

manufacturing facility, then disposals may not be unusual or infrequent. If, however, the entity rarely

replaces machinery and it replaces a significant amount of machinery as part of a manufacturing upgrade,

that action may be considered unusual and infrequent. Transactions or events that do not meet the

ordinary income definition would be evaluated as discrete items to be recognized as they occur and not in

the AETR calculation.

2.3 Losses incurred in interim periods within a fiscal year

ASC 740-270-25-9

The tax effects of losses that arise in the early portion of a fiscal year shall be recognized only

when the tax benefits are expected to be either:

a. Realized during the year:

b. Recognizable as a deferred tax asset at the end of the year in accordance with the provisions

of Subtopic 740-10.

ASC 740-270-25-10

An established seasonal pattern of loss in early interim periods offset by income in later interim

periods shall constitute evidence that realization is more likely than not unless other evidence

indicates the established seasonal pattern will not prevail.

ASC 740-270-25-11

The tax effects of losses incurred in early interim periods may be recognized in a later interim

period of a fiscal year if their realization, although initially uncertain, later becomes more likely than

not. When the tax effects of losses that arise in the early portions of a fiscal year are not

recognized in that interim period, no tax provision shall be made for income that arises in later

interim periods until the tax effects of the previous interim losses are utilized.

Entities often do not generate income ratably during the annual period. For example, a retailer may

generate a substantial portion of its income in the fourth quarter. Another example would be an

amusement park in a colder climate that may only open during the spring and summer. In such cases, the

relationship between the actual year-to-date ordinary income or loss and the estimated annual ordinary

income or loss may vary throughout the year. In these situations, specific considerations need to be

evaluated to appropriately recognize the interim income tax expense or benefit. ASC 740-270-25-9 to 25-

11 provides guidance on when to recognize benefits of losses incurred during earlier periods of a fiscal

year.

If an entity has incurred year-to-date losses or projects an estimated annual ordinary loss, the entity

needs to consider further when the estimated tax benefit should be included in the AETR. The tax effects

of losses that arise in early interim periods should be recognized only if the tax benefits are more likely

than not (MLTN) of being realized during the year (i.e., though ordinary income expected to be generated

in later interim periods) or in a future year (i.e., through recognition of a deferred tax asset with no

Page 7 of 21 © RSM US LLP

ACCOUNTING FOR INCOME TAXES - INTERIM PERIOD TAX REPORTING DECEMBER 2023

valuation allowance). The tax benefits of such losses would be considered when estimating the annual

effective tax rate. Such tax benefits arising from losses in earlier interim periods should only be

recognized in the interim reporting period and considered in the estimation of the AETR when the tax

benefits are meet the threshold of MLTN to be realized.

Further, adoption of ASU 2019-12, Simplifying the Accounting for Income Taxes, requires entities to

recognize the tax benefit of a year-to-date loss based on the AETR, regardless of whether the year-to-

date ordinary loss exceeds the anticipated ordinary loss for the fiscal year. ASU 2019-12 is effective no

later than fiscal years which began after December 15, 2021, and interim periods within fiscal years that

began after December 15, 2022.

The following table illustrates the treatment within the AETR when losses are expected in interim periods.

Considerations Related to Recognition within the AETR

Losses incurred in interim

periods–realization of tax

benefits is MLTN

The expected tax benefit for losses in the interim reporting periods

would be recognized in such periods, since the entity expects that

realization of the related tax benefits is MLTN. See Example 2-1.

Losses incurred in interim

periods–realization of tax

benefits is not MLTN

The expected tax benefit for losses in the interim reporting periods

would not be recognized in such periods, since the entity does not

expect the tax benefit to be realized either during the year or as a

deferred tax asset at the end of the year (i.e., realization is not

MLTN). See Example 2-2.

Losses incurred in interim

periods–partial realization of tax

benefits is MLTN

The AETR would consider the portion of the ordinary losses that

meet the MLTN criteria for realization. See Example 2-3.

The examples below highlight different scenarios for recognition of tax benefits, which depends on

whether the realization of the tax benefits is considered MLTN. Conclusions on realization of tax benefits

require judgement and are dependent on the specific facts and circumstances.

Example 2-1: Losses incurred in interim periods (Realization of tax benefits is MLTN)

ABC Company incurred ordinary losses in the first two quarters of the fiscal year ended December 31,

20X2. For the full fiscal year, ABC Company anticipates ordinary income of $100,000. ABC Company is a

retailer and earns most of its income during the last quarter of the year, and it has operated with a history

of profitability for over 15 years. Therefore, ABC Company’s seasonal earnings patterns provide evidence

that realization of tax benefits of year-to-date losses and anticipated tax credits is MLTN. ABC Company’s

income is taxable in one jurisdiction at a 25% rate which may be offset by anticipated tax credits of

$10,000. The estimated annual tax expense represents the tax at the statutory rate of $25,000 ($100,000

at 25%) less the anticipated tax credits of $10,000 for a total net estimated tax of $15,000. Therefore, the

AETR is 15%.

ABC Company recognizes the following income tax expense (benefit) in each of the fiscal quarters in the

year ended December 31, 20X2:

Page 8 of 21 © RSM US LLP

ACCOUNTING FOR INCOME TAXES - INTERIM PERIOD TAX REPORTING DECEMBER 2023

Ordinary Income

Income Tax Expense

Reporting

Period

Year to

Date

AETR

Year to

Date

Less

Previously

Provided

Reporting

Period

First Quarter

($10,000)

($10,000)

15%

($1,500)

$ -

($1,500)

Second Quarter

(10,000)

(20,000)

15%

(3,000)

(1,500)

(1,500)

Third Quarter

25,000

5,000

15%

750

(3,000)

3,750

Fourth Quarter

95,000

100,000

15%

15,000

750

14,250

Fiscal year

$100,000

$ -

15%

$ -

$ -

$15,000

ABC Company recognizes the tax benefits of the losses incurred in the first and second quarters of its

fiscal year because it believes that the evidence is MLTN that the tax benefits of the losses in such

quarters would l be realized.

Example 2-2: Losses incurred in interim periods (Realization of tax benefits is not

MLTN)

ABC Company incurred ordinary losses in first two quarters of the fiscal year ended December 31, 20X2.

For the full fiscal year, ABC Company anticipates ordinary income of $100,000. ABC Company is not in

an industry with established seasonal earning patterns, nor does it have a history of profitability.

Therefore, its earnings patterns do not provide evidence that realization of the tax benefit of the year-to-

date loss and of anticipated tax credits is MLTN. All income is taxable in one jurisdiction at a 25% rate

which may be offset by anticipated tax credits of $10,000. The estimated annual tax expense represents

the tax at the statutory rate of $25,000 ($100,000 at 25%) less the anticipated tax credits of $10,000 for a

total net estimated tax of $15,000. Therefore, the AETR is 15%.

Page 9 of 21 © RSM US LLP

ACCOUNTING FOR INCOME TAXES - INTERIM PERIOD TAX REPORTING DECEMBER 2023

ABC Company recognizes the following income tax expense (benefit) in each of the fiscal quarters in the

year ended December 31, 20X2:

Ordinary Income

Income Tax Expense

Reporting

Period

Year to

Date

AETR

Year to

Date

Less

Previously

Provided

Reporting

Period

First Quarter

($10,000)

(10,000)

15%

$

$ -

$-

Second Quarter

(10,000)

(20,000)

15%

-

-

-

Third Quarter

25,000

5,000

15%

750

-

750

Fourth Quarter

95,000

100,000

15%

15,000

750

14,250

Fiscal year

$100,000

$ -

15%

$ -

$ -

$15,000

ABC Company does not recognize the tax benefits of the losses incurred in the first and second quarters

of its fiscal year because it did not have sufficient evidence to conclude that the tax benefits of the losses

in such quarters would be realized. Thus, the entity recognizes income tax expense only in the third and

fourth quarter of its fiscal year.

Example 2-3: Losses incurred in interim periods (Partial realization of tax benefits is

MLTN)

ABC Company incurred losses in the first three quarters of its fiscal year ended December 31, 20X2. For

the full fiscal year, ABC Company anticipates an ordinary loss of $100,000. ABC Company operates

entirely in one jurisdiction where the tax rate is 25%. Thus, the anticipated tax benefit for the year would

be $25,000. However, ABC Company determined that the tax benefit for the projected loss for the year of

$100,000, is limited to $20,000, as the remainder would not meet the MLTN threshold for recognition as a

deferred tax asset at the end of the year. Therefore, the adjusted AETR is 20% ($20,000 tax benefit

divided by $100,000 estimated annual ordinary loss), and the benefit that can be recognized for the year

is limited to $20,000.

Page 10 of 21 © RSM US LLP

ACCOUNTING FOR INCOME TAXES - INTERIM PERIOD TAX REPORTING DECEMBER 2023

ABC Company recognizes the following income tax expense (benefit) in each of the quarters of the year

ended December 31, 20X2:

Ordinary Income

Income Tax Benefit

Reporting

Period

Year to

Date

AETR

Year to

Date

Less

Previously

Provided

Reporting

Period

First Quarter

($15,000)

($15,000)

20%

($3,000)

$-

($3,000)

Second Quarter

(25,000)

(40,000)

20%

(8,000)

(3,000)

(5,000)

Third Quarter

(25,000)

(65,000)

20%

(13,000)

(8,000)

(5,000)

Fourth Quarter

(35,000)

(100,000)

20%

(20,000)

(13,000)

(7,000)

Fiscal year

($100,000)

$ -

20%

$ -

$ -

($20,000)

ABC Company recognized tax benefit in each quarter based on its adjusted AETR of 20% since it had

determined that a benefit of $20,000 was MLTN to be realized on ABC Company’s expected loss for the

year of $100,000.

2.4 Effect of multiple jurisdictions

ASC 740-270-generally requires a single AETR which is equal to the entity’s expected global income tax

divided by the expected global ordinary income. ASC 740-270-30-36 provides two exceptions to

calculating a global AETR as follows.

1. The entity expects an ordinary loss for the year or has a year-to-date ordinary loss and no tax

benefit can be recognized (i.e., the tax benefit will not be used against current-year future interim

period income or in a future year) in a single jurisdiction. The expected and year-to-date ordinary

loss as well as unrecognized tax benefit for this jurisdiction would be excluded from the overall

AETR.

2. The entity is unable to estimate an AETR in a particular foreign jurisdiction. One reason for this

may be that the entity operates in a volatile economy and the foreign currency translation effects

make it difficult to estimate an AETR. The expected ordinary income or loss or related tax or

benefit for the foreign jurisdiction that is unable to make an estimate would be excluded from the

AETR and interim period tax or benefit. The related tax or benefit would be recognized once the

ordinary income or loss is reported in the interim period.

The following three-part example is sourced from Example 5 in ASC 740-270-55.

Page 11 of 21 © RSM US LLP

ACCOUNTING FOR INCOME TAXES - INTERIM PERIOD TAX REPORTING DECEMBER 2023

Example 2-4: Accounting for Income Taxes Applicable to Ordinary Income if an Entity

is Subject to Tax in Multiple Jurisdictions (ASC 740-270-55-37 to 55-43)

The following Cases illustrate the guidance in paragraph 740-270-30-36 for accounting for income taxes

applicable to ordinary income if an entity is subject to tax in multiple jurisdictions:

1. Ordinary income in all jurisdictions (Case A)

2. Ordinary loss in a jurisdiction; realization of the tax benefit not more likely than not (Case B)

3. Ordinary income or tax cannot be estimated in one jurisdiction (Case C).

Cases A, B, and C assume that an entity operates through separate corporate entities in two countries.

Applicable tax rates are 50 percent in the United States and 20 percent in Country A. The entity has no

unusual or infrequently occurring items during the fiscal year and anticipates no tax credits or events that

do not have tax consequences. (The effect of foreign tax credits and the necessity of providing tax on

undistributed earnings are ignored because of the wide range of tax planning alternatives available.). For

the full fiscal year, the entity anticipates ordinary income of $60,000 in the United States and $40,000 in

Country A. The entity is able to make a reliable estimate of its Country A ordinary income and tax for the

fiscal year in dollars. Computation of the overall estimated annual effective tax rate in Cases B and C is

based on additional assumptions stated in those Cases.

Case A: Ordinary Income in All Jurisdictions

Computation of the overall estimated annual effective tax rate is as follows:

Anticipated ordinary income for the fiscal year:

In the United States

$ 60,000

In Country A

40,000

Total

$ 100,000

Anticipated tax for the fiscal year:

In the United States ($60,000 at 50% statutory rate)

$ 30,000

In Country A ($40,000 at 20% statutory rate)

8,000

Total

$ 38,000

Overall estimated annual effective tax rate ($38,000/$100,000)

38%

Page 12 of 21 © RSM US LLP

ACCOUNTING FOR INCOME TAXES - INTERIM PERIOD TAX REPORTING DECEMBER 2023

Quarterly tax computations are as follows:

Ordinary Income

Tax

Reporting

Period

United

States

Country

A

Total

Year to

Date

Overall

Estimated

Annual

Effective

tax rate

Year to

Date:

Less

Previously

Reported

Reporting

Period

First

Quarter

$5,000

$15,000

$20,000

$20,000

38%

$7,600

$ -

$7,600

Second

Quarter

10,000

10,000

20,000

40,000

38%

15,200

7,600

7,600

Third

Quarter

10,000

10,000

20,000

60,000

38%

22,800

15,200

7,600

Fourth

Quarter

35,000

5,000

40,000

100,000

38%

38,000

22,800

15,200

Fiscal

year

$60,000

$40,000

$100,000

$38,000

Case B: Ordinary Loss in a Jurisdiction, Realization of the Tax Benefit Not More Likely than Not

In this Case, the entity operates through a separate corporate entity in Country B. Applicable tax rates in

Country B are 40 percent. Operations in Country B have resulted in losses in recent years and an

ordinary loss is anticipated for the current fiscal year in Country B. It is expected that the tax benefit of

those losses will not be recognizable as a deferred tax asset at the end of the current year; accordingly,

no tax benefit is recognized for losses in Country B, and interim period tax (or benefit) is separately

computed for the ordinary loss in Country B and for the overall ordinary income in the United States and

Country A. The tax applicable to the overall ordinary income in the United States and Country A is

computed as in Case A of this Example.

Page 13 of 21 © RSM US LLP

ACCOUNTING FOR INCOME TAXES - INTERIM PERIOD TAX REPORTING DECEMBER 2023

Quarterly tax provisions are as follows.

Ordinary Income (Loss)

Tax

Reporting

Period

United

States

Country

A

Combined

Excluding

Country B

Country

B

Total

Combined

Excluding

Country B

Country

B

Total

First

Quarter

$5,000

$15,000

$20,000

($5,000)

$15,000

$7,600

$ -

$7,600

Second

Quarter

10,000

10,000

20,000

(25,000)

(5,000)

7,600

-

7,600

Third

Quarter

10,000

10,000

20,000

(5,000)

15,000

7,600

-

7,600

Fourth

Quarter

35,000

5,000

40,000

(5,000)

35,000

15,200

-

15,200

Fiscal

Year

$60,000

$40,000

$100,000

($40,000)

$60,000

$38,000

$ -

$38,000

Case C: Ordinary Income or Tax Cannot Be Estimated in One Jurisdiction

In this Case, the entity operates through a separate corporate entity in Country C. Applicable tax rates in

Country C are 40 percent in foreign currency. Depreciation in that country is large and exchange rates

have changed in prior years. The entity is unable to make a reasonable estimate of its ordinary income for

the year in Country C and thus is unable to reasonably estimate its annual effective tax rate in Country C

in dollars. Accordingly, tax (or benefit) in Country C is separately computed as ordinary income (or loss)

occurs in Country C. The tax applicable to the overall ordinary income in the United States and Country A

is computed as in Case A of this Example.

Quarterly computations of tax applicable to Country C are as follows.

Foreign Currency Amounts

Translated Amounts in Dollars

Reporting

Period

Ordinary Income

In Reporting

Period

Tax (At 40%

Rate)

Ordinary Income

In Reporting

Period

Tax

First quarter

FC 10,000

FC 4,000

$ 12,500

$ 3,000

Second quarter

5,000

2,000

8,750

1,500

Third quarter

30,000

12,000

27,500

9,000

Fourth quarter

15,000

6,000

16,250

4,500

Fiscal year

FC 60,000

FC 24,000

$ 65,000

$ 18,000

Page 14 of 21 © RSM US LLP

ACCOUNTING FOR INCOME TAXES - INTERIM PERIOD TAX REPORTING DECEMBER 2023

2.5 Computation of the AETR

The estimated annual effective tax rate is an entity’s best estimate and would include federal, state and

foreign income taxes, as applicable. The AETR would also include any other items that would affect the

entity’s AETR, such as tax credits and changes in valuation allowances related to current year events. At

the end of each interim period, the interim tax expense or benefit would be calculated by applying the

AETR to the year-to-date results of operations. The entity would then add the tax effect, if any, of discrete

items to compute the total year-to-date interim tax provision. For quarters later than the first quarter, the

previously recognized interim period income tax is subtracted from the year-to-date interim tax provision

to calculate the current interim period tax provision. Due to this multi-step calculation, any specific interim

period may not have a predictable connection to the pre-tax income or AETR of the interim period.

The AETR and related annual ordinary income are an entity’s best estimates as of each interim period.

As with all estimates, they may be subject to change when more current and reliable information

becomes available. Further, ASC 740-270-30-18 states that if a reliable estimate cannot be made, the

entity should use the actual year to date effective tax rate.

ASC 740-270-20-3 provides an exception for an entity that may be unable to estimate a portion of its

ordinary income (loss) or related tax (benefit) but is able to estimate the remainder of its income and

related tax effect. In that case, an entity may report the actual tax or benefit applicable to the portion of

income that cannot be estimated, as a discrete item in the interim period, outside of the AETR.

3. Items treated outside of the AETR (discrete items)

ASC 740-270 includes guidance on common discrete items to exclude from the estimated annual

effective rate calculation. The explicit discrete items included in the guidance are:

• Change in tax law and rates-after adoption of ASU 2019-12 (see Section 3.1)

• Change in tax status (see Section 3.2)

• Change in accounting principle (see Section 3.3)

• Change in beginning of year valuation allowance (see Section 3.4)

Ordinary Income

Tax

Reporting

Period

United

States

Country

A

Combined

Excluding

Country C

Country

C

Total

Combined

Excluding

Country C

Country

C

Total

First

Quarter

$5,000

$15,000

$20,000

$12,500

$32,500

$7,600

$3,000

$10,600

Second

Quarter

10,000

10,000

20,000

8,750

28,750

7,600

1,500

9,100

Third

Quarter

10,000

10,000

20,000

27,500

47,500

7,600

9,000

16,600

Fourth

Quarter

35,000

5,000

40,000

16,250

56,250

15,200

4,500

19,700

Fiscal

year

$60,000

$40,000

$100,000

$65,000

$165,000

$38,000

$18,000

$56,000

Page 15 of 21 © RSM US LLP

ACCOUNTING FOR INCOME TAXES - INTERIM PERIOD TAX REPORTING DECEMBER 2023

• Investment tax credits (see Section 3.5)

• Interest and penalties (see Section 3.6)

• Change in the recognition of a deferred tax asset related to outside basis differences (see Section

3.7)

3.1 Change in tax laws and rates after adoption of ASU 2019-12

ASC 740-270-25-5

The effects of new tax legislation shall not be recognized prior to enactment. The tax effect of a

change in tax laws or rates on taxes currently payable or refundable for the current year shall be

reflected in the computation of the annual effective tax rate beginning in the first interim period that

includes the enactment date of the new legislation. The effect of a change in tax laws or rates on a

deferred tax liability or asset shall not be apportioned among interim periods through an

adjustment of the annual effective tax rate.

ASC 740-270-25-6

The tax effect of a change in tax laws or rates on taxes payable or refundable for a prior year

shall be recognized as of the enactment date of the change as tax expense (benefit) for the

current year.

See Section 2.3 for the effective date of ASU 2019-12. ASC 740-10-45-15 states that the effect of

adjustments to deferred tax balances resulting from changes in tax laws or rates would be included in

income from continuing operations in the period in which the new legislation is enacted. ASC 740-270-25-

5 to 25-6 describes how to measure the required adjustment The impact of the change in tax law or rates

on current year taxes payable (refundable) would be reflected in the calculation of the AETR beginning in

the first interim period which includes the enactment date. Conversely, the effect of such change in tax

laws or rates on deferred tax assets and liabilities would be considered a discrete item and recognized

within income from continuing operations in the interim period that includes the enactment date and would

not be allocated to subsequent interim periods by an adjustment of the estimated annual effective tax

rate. Retroactive changes in tax laws or rates are also considered discrete items, and the effect would

also be recognized separately in income from continuing operations in the interim period that includes the

enactment date. Similar to the treatment of the deferred tax assets, the impact of changes in tax laws and

rates on prior year taxes payable or refundable balances would be recognized as a discrete item (i.e., as

income tax expense (benefit) in the current year in the period that includes the enactment date).

3.2 Change in tax status

A change in an entity’s tax status occurs when a non-taxable entity (e.g. a partnership) becomes a

taxable entity (e.g. a corporation) or vice versa, ASC 740-10-25-32 to 25-34 state that a voluntary change

in an entity’s tax status would be recognized on the approval date granted by the taxing authority or on

the filing date if approval is not required. ASC 740-10-45-19 requires that the deferred tax effects of a

change in tax status be included in income from continuing operations. The effect of this change on

existing deferred tax assets and liabilities would be considered a discrete item and recognized in income

from continuing operations in the interim period that includes the approval or filing date, as appropriate.

3.3 Change in accounting principle

ASC 740-270-30-38 states that the tax expense or benefit related to the cumulative effect of a change in

accounting principle would be presented in the same manner as within the annual financial statements.

Income tax expense or benefit reduces or increases the related cumulative effect of a change in

accounting principle and is presented on a separate line below income from continuing operations within

the financial statements. ASC 740-270-30-12 and ASC 740-25-2 state that the income tax expense

Page 16 of 21 © RSM US LLP

ACCOUNTING FOR INCOME TAXES - INTERIM PERIOD TAX REPORTING DECEMBER 2023

(benefit) applicable to a cumulative effect of a change in accounting principle would be recognized as a

discrete item in the interim period of the change and excluded from the AETR calculation.

3.4 Change in beginning of year valuation allowance

Entities are required to reconsider whether a full or partial valuation allowance is required against existing

deferred tax assets as of the end of each interim reporting period. Under ASC 740-270-25-4 a change in

the valuation allowance may be reflected either in the AETR or recognized discretely when the change

occurs, depending on whether the change is caused by current year or future year income. Entities

would reflect a change in the beginning of the year valuation allowance within the AETR when the change

relates to either deductible temporary differences and carryforwards expected to originate during the

current year or when it relates to current year income. However, changes in judgement about the

realizability of the beginning of the year deferred tax asset based on expected income in future years

would be excluded from the AETR and instead recognized as a separate discrete item in the interim

period of the change.

3.5 Investment tax credits

ASC 740-270-30-14 to 30-15 discusses the treatment of changes in investment tax credits within interim

tax provisions. The treatment of these investment tax credits in the AETR depends on the accounting

method elected by the entity. If an entity elects the deferral method, the net benefit from the investment

tax credits would be excluded from the AETR.

3.6 Interest and penalties

ASC 740-10-25-56 requires accrual of interest commencing with the first period in which the interest

would begin accruing according to the provisions of the relevant tax law. ASC 740-10-25-57 requires that

statutory penalties be recorded either when the entity initially takes the position or expects to take the

position that is expected to result in such penalty. If a penalty was not initially recognized when the

position was taken, a penalty would subsequently be recognized in the period when the entity changed its

judgement about whether the position would result in a penalty. Interest and penalties would be excluded

from the AETR calculation and accounted for separately from continuing operations as it occurs, even if

the entity has elected to treat interest and penalties as a part of tax expense.

3.7 Change in the recognition of a deferred tax asset related to outside basis

differences

Outside tax basis differences are differences in the book basis and tax basis of an investment in a

subsidiary or a corporate joint venture. A deferred tax asset would be recognized for the excess of the tax

basis over the financial reporting basis for an investment that is essentially permanent in duration only if it

is apparent that the temporary difference will reverse in the foreseeable future. Changes in the

recognition of this type of deferred tax asset would be excluded from the AETR if the underlying

subsidiary is included in discontinued operations. In this case, the benefit recognized for the deductible

outside basis difference generally would be accounted for as a discrete event and generally is recognized

in discontinued operations. If the underlying subsidiary is recognized in continuing operations, the entity

would reflect the beginning of the year impact of the change as a discrete item while including the impact

on current year earnings within the AETR.

4. Balance sheet impact

ASC 740-270 outlines the guidance on calculating income taxes for interim periods. In other words, it

prescribes an income statement approach, and it does not address the measurement and presentation of

deferred tax assets and liabilities or other balance sheet tax accounts in interim periods. Absent of any

specific guidance, an entity should adjust its income tax balance sheet accounts during interim periods in

Page 17 of 21 © RSM US LLP

ACCOUNTING FOR INCOME TAXES - INTERIM PERIOD TAX REPORTING DECEMBER 2023

a methodical and rationale manner that aligns the income statement approach of ASC 740-270 or balance

sheet approach of ASC 740-10, considering significant changes in deferred tax balances by jurisdiction.

Page 18 of 21 © RSM US LLP

ACCOUNTING FOR INCOME TAXES - INTERIM PERIOD TAX REPORTING DECEMBER 2023

Appendix A: Acronyms

Acronym

Definition

AETR

Annual Effective Tax Rate

ASC

FASB Accounting Standards Codification

FASB

Financial Accounting Standards Board

MLTN

More Likely Than Not

Appendix B: Definitions

Several terms with specific meaning are used throughout this whitepaper. Those terms and the

corresponding definitions based on the FASB’s Master Glossary of the Codification are provided in the

table that follows.

Term

Definition

Carrybacks

Deductions or credits that cannot be utilized on the tax return during a year that

may be carried back to reduce taxable income or taxes payable in a prior year.

An operating loss carryback is an excess of tax deductions over gross income

in a year; a tax credit carryback is the amount by which tax credits available for

utilization exceed statutory limitations. Different tax jurisdictions have different

rules about whether excess deductions or credits may be carried back and the

length of the carryback period.

Carryforwards

Deductions or credits that cannot be utilized on the tax return during a year that

may be carried forward to reduce taxable income or taxes payable in a future

year. An operating loss carryforward is an excess of tax deductions over gross

income in a year; a tax credit carryforward is the amount by which tax credits

available for utilization exceed statutory limitations. Different tax jurisdictions

have different rules about whether excess deductions or credits may be carried

forward and the length of the carryforward period. The terms carryforward,

operating loss carryforward, and tax credit carryforward refer to the amounts of

those items, if any, reported in the tax return for the current year.

Current Tax

Expense (or Benefit)

The amount of income taxes paid or payable (or refundable) for a year as

determined by applying the provisions of the enacted tax law to the taxable

income or excess of deductions over revenues for that year.

Deductible

Temporary

Difference

Temporary differences that result in deductible amounts in future years when

the related asset or liability is recovered or settled, respectively. See Temporary

Difference.

Deferred Tax Asset

The deferred tax consequences attributable to deductible temporary differences

and carryforwards. A deferred tax asset is measured using the applicable

enacted tax rate and provisions of the enacted tax law. A deferred tax asset is

reduced by a valuation allowance if, based on the weight of evidence available,

Page 19 of 21 © RSM US LLP

ACCOUNTING FOR INCOME TAXES - INTERIM PERIOD TAX REPORTING DECEMBER 2023

Term

Definition

it is more likely than not that some portion or all of a deferred tax asset will not

be realized.

Deferred Tax

Consequences

The future effects on income taxes as measured by the applicable enacted tax

rate and provisions of the enacted tax law resulting from temporary differences

and carryforwards at the end of the current year.

Deferred Tax

Expense (or Benefit)

The change during the year in an entity's deferred tax liabilities and assets. For

deferred tax liabilities and assets acquired in a purchase business combination

during the year, it is the change since the combination date. Income tax

expense (or benefit) for the year is allocated among continuing operations,

discontinued operations, and items charged or credited directly to shareholders'

equity.

Deferred Tax

Liability

The deferred tax consequences attributable to taxable temporary differences. A

deferred tax liability is measured using the applicable enacted tax rate and

provisions of the enacted tax law.

Event

A happening of consequence to an entity. The term encompasses both

transactions and other events affecting an entity.

Income Tax

Expense (or Benefit)

The sum of current tax expense (or benefit) and deferred tax expense (or

benefit).

Income Taxes

Domestic and foreign federal (national), state, and local (including franchise)

taxes based on income.

Income Taxes

Currently Payable

(Refundable)

See Current Tax Expense (or Benefit).

Tax Consequences

The effects on income taxes—current or deferred—of an event.

Tax Position

A position in a previously filed tax return or a position expected to be taken in a

future tax return that is reflected in measuring current or deferred income tax

assets and liabilities for interim or annual periods. A tax position can result in a

permanent reduction of income taxes payable, a deferral of income taxes

otherwise currently payable to future years, or a change in the expected

realizability of deferred tax assets. The term tax position also encompasses, but

is not limited to:

a. A decision not to file a tax return

b. An allocation or a shift of income between jurisdictions

c. The characterization of income or a decision to exclude reporting

taxable income in a tax return

d. A decision to classify a transaction, entity, or other position in a tax

return as tax exempt

Page 20 of 21 © RSM US LLP

ACCOUNTING FOR INCOME TAXES - INTERIM PERIOD TAX REPORTING DECEMBER 2023

Term

Definition

e. An entity's status, including its status as a pass-through entity or a tax-

exempt not-for-profit entity.

Tax-Planning

Strategy

An action (including elections for tax purposes) that meets certain criteria (see

paragraph 740-10-30-19) and that would be implemented to realize a tax benefit

for an operating loss or tax credit carryforward before it expires. Tax-planning

strategies are considered when assessing the need for and amount of a

valuation allowance for deferred tax assets.

Taxable Income

The excess of taxable revenues over tax deductible expenses and exemptions

for the year as defined by the governmental taxing authority.

Taxable Temporary

Difference

Temporary differences that result in taxable amounts in future years when the

related asset is recovered or the related liability is settled. See Temporary

Difference.

Temporary

Difference

A difference between the tax basis of an asset or liability computed pursuant to

the requirements in Subtopic 740-10 for tax positions, and its reported amount

in the financial statements that will result in taxable or deductible amounts in

future years when the reported amount of the asset or liability is recovered or

settled, respectively. Paragraph 740-10-25-20 cites examples of temporary

differences. Some temporary differences cannot be identified with a particular

asset or liability for financial reporting (see paragraphs 740-10-05-10 and 740-

10-25-24 through 740-10-25-25), but those temporary differences do meet both

of the following conditions:

a. Result from events that have been recognized in the financial statements

b. Will result in taxable or deductible amounts in future years based on

provisions of the tax law.

Some events recognized in financial statements do not have tax consequences.

Certain revenues are exempt from taxation and certain expenses are not

deductible. Events that do not have tax consequences do not give rise to

temporary differences.

Valuation Allowance

The portion of a deferred tax asset for which it is more likely than not that a tax

benefit will not be realized.

Page 21 of 21 © RSM US LLP

ACCOUNTING FOR INCOME TAXES - INTERIM PERIOD TAX REPORTING DECEMBER 2023

The FASB material is copyrighted by the Financial Accounting Foundation, 801 Main Avenue, Norwalk, CT 06851, and is used with

permission.

+1 800 274 3978

rsmus.com

This document contains general information, may be based on authorities that are subject to

change, and is not a substitute for professional advice or services. This document does not

constitute audit, tax, consulting, business, financial, investment, legal or other professional advice,

and you should consult a qualified professional advisor before taking any action based on the

information herein. RSM US LLP, its affiliates and related entities are not responsible for any loss

resulting from or relating to reliance on this document by any person. Internal Revenue Service rules

require us to inform you that this communication may be deemed a solicitation to provide tax

services. This communication is being sent to individuals who have subscribed to receive it or who

we believe would have an interest in the topics discussed.

RSM US LLP is a limited liability partnership and the U.S. member firm of RSM International, a

global network of independent audit, tax and consulting firms. The member firms of RSM

International collaborate to provide services to global clients, but are separate and distinct legal

entities that cannot obligate each other. Each member firm is responsible only for its own acts and

omissions, and not those of any other party. Visit rsmus.com/aboutus for more information regarding

RSM US LLP and RSM International.

RSM, the RSM logo and the power of being understood are registered trademarks of RSM

International Association.

© 2023 RSM US LLP. All Rights Reserved.