22

THE CALCULATION OF AGGREGATE LOSS DISTRIBUTIONS FROM

CLAIM SEVERITY AND CLAIM COUNT DISTRIBUTIONS

PHILIPE. HECKMAN

GLENNG.MEYERS

Abstract

This paper discusses aggregate loss distributions from the perspective of

collective risk theory. An accurate, efficient and practical algorithm is given for

calculating cumulative probabilities and excess pure premiums. The input re-

quired is the claim severity and claim count distributions.

One of the main drawbacks of the collective risk model is the uncertainty

of the parameters of the claim severity and claim count distributions. Modifi-

cations of the collective risk model are proposed to deal with these problems.

These modifications are incorporated into the algorithm.

Examples are given illustrating the use of this algorithm. They include (1)

calculating the pure premium for a policy with an aggregate limit; (2) calculating

the pure premium of an aggregate stop-loss policy for group life insurance; and

(3) calculating the insurance charge for a multi-line retrospective rating plan,

including a line which is itself subject to an aggregate limit.

1. INTRODUCTION

This paper discusses aggregate loss distributions from the perspective of

collective risk theory. Our objective is to provide an efficient algorithm for

calculating the cumulative probabilities and excess pure premium ratios for

aggregate loss distributions in terms of the claim severity and claim count

distributions. Examples illustrating the use of this algorithm will be given.

Aggregate loss distributions are playing an increasingly important role in

the pricing of insurance coverages. .The insurance buying public is becoming

more sophisticated and is recognizing that it is to their advantage to absorb as

much of their losses as they possibly can and to purchase excess insurance to

cover the catastrophic losses. With the degree of competition that exists in the

insurance marketplace, it is extremely important to obtain accurate estimates of

the losses that could arise from such an insurance contract.

AGGREGATE DlSTRlBUTlONS

23

Aggregate loss distributions have been widely discussed in the insurance

literature. Members of the Casualty Actuarial Society are familiar with the

papers of Dorweiler [I], Valerius [2], Simon [3] and Hewitt [4]. The aggregate

loss distributions in these papers are based on observed aggregate loss data of

individual insureds. A problem with this approach is that to get a sufficient

volume of data, one must combine the experience of insureds for which one

would expect different aggregate loss distributions.

The use of collective risk theory provides an alternative to the above ap-

proach. Aggregate loss distributions are calculated in terms of the underlying

claim severity and claim count distributions. Empirical data on claim severity

and claim count distributions are, in many cases, readily available. Many feel

that this approach is superior to observing actual aggregate losses because it

makes more efficient use of available data. Much relevant detail is buried when

one observes only aggregate loss data.

However, the collective risk model does have some drawbacks. There are

problems involved in fitting a distribution to the claim count. For a given insured

we get one measurement of the claim count per year. During the years that we

get the measurements, the exposure of the insured is most likely changing. In

addition, observations are clouded by the fact that we must estimate the number

of claims which have been incurred but not reported. Because of these problems

it is difficult to fit a distribution to the claim count. Often, we must assume a

distribution (usually Binomial, Poisson or Negative Binomial) with the param-

eters selected by judgment.

While empirical claim severity distributions are readily available, there are

still some formidable problems that must be solved. There is no consensus as

to how claim severity distributions should be adjusted for inflation. If we try to

minimize this problem by choosing a relatively recent claim severity distribution,

we will understate the variance of the ultimate claim severity distribution. To

see this, consider the following equation.

Var (Z) = &(Var (ZIR)) + VarR (E(ZIR))

Z = Ultimate Loss

R = Case Reserve

When case estimates are set at the expected value of the ultimate payment, the

variance of the immature distribution will be Var,@(ZIR)). The variance of the

ultimate claim severity distribution will be greater! Great care must be exercised

in selecting the ultimate loss distribution. Methods of solving this problem can

be found in the literature. [5][6].

24

AGGREGATE DISTRIBUTIONS

Another problem with the collective risk model is that the calculation of the

aggregate loss distribution has been very difficult. A great deal has been written

about the various methods of solving this problem. We shall attempt to sum-

marize these methods.

One general approach has been to calculate the moments of the aggregate

loss distribution in terms of the moments of the claim severity distribution and

the claim count distribution. One can then match the moments of the aggregate

loss distribution with an assumed distribution. Probably the best known example

of this approach is the Normal Power approximation 171. However, the condi-

tions required to insure the accuracy of this method can be very restrictive.

Gary Venter uses the transformed Gamma distribution and obtains better results

[S]. While it is easy to compute the results using these methods, one runs the

risk of inaccuracies because the assumed distribution is not the same as that

implied by the collective risk model.

A very popular method of calculating the aggregate loss distribution is by

Monte Carlo simulation. Glenn Meyers has written an article illustrating this

approach 191. This method is easy to understand and can be very accurate.

However, it currently requires a great deal of computer time.

A third method of calculating the aggregate loss distribution involves in-

verting its characteristic function. A recent article illustrating this approach was

written by Dr. Shaw Mong [IO]. This method requires that we have an explicit

‘representation of the characteristic function of the claim severity distribution.

Mong uses a shifted Gamma distribution to describe the claim severity distri-

bution. Mong gives formulas for approximating other claim severity distributions

with the shifted Gamma by matching the first three moments. The accuracy of

this method depends upon how well the shifted Gamma distribution approxi-

mates the desired claim severity distribution.

A fourth method is the so-called “recursive method.” This method assumes

a discrete claim severity distribution. By choosing a large enough number of

points for the claim severity distribution, one can obtain any desired degree of

accuracy. For this reason, it has been called an “exact” method. This method

requires far less computer time than Monte Carlo simulation. The recursive

method is derived in papers by Ethan Stroh [l l] and James Tilley [12] by

inverting the Laplace transform of the aggregate loss distribution. Much of the

mathematics involved is similar to that used in the characteristic function in-

version method. Harry Panjer gives a derivation of the recursive method which

does not involve inverting the Laplace transform [13].

AGGREGATE DISTRIBUTIONS

25

The method described in this paper inverts the characteristic function of the

aggregate loss distribution. Like the recursive method, it ‘is an exact method.

Its application goes beyond the recursive method in the following ways.

1. This method allows one to combine the aggregate loss distributions of

several different lines into a composite aggregate loss distribution. This

is necessary if one is to apply the results of the collective risk model to

multi-line retrospective rating plans.

2. This method allows for parameter uncertainty in, both the claim severity

distribution and the claim count distribution. Glenn Meyers and Nathaniel

Schenker have shown that allowing for parameter uncertainty signifi-

cantly improves the fit of the collective risk model to empirical data [ 141.

It should be noted that Gary Venter’s method of Reference [8] also

allows for parameter uncertainty.

3. Philip Heckman and Phillip Norton have used the results of this paper

to derive a method of selecting the specific and aggregate policy limits

that minimize the variance of the retained losses while holding the cost

of coverage constant [ 1.51.

In short, this method is applicable to a wide variety of insurance pricing

problems. We include several examples which illustrate this.

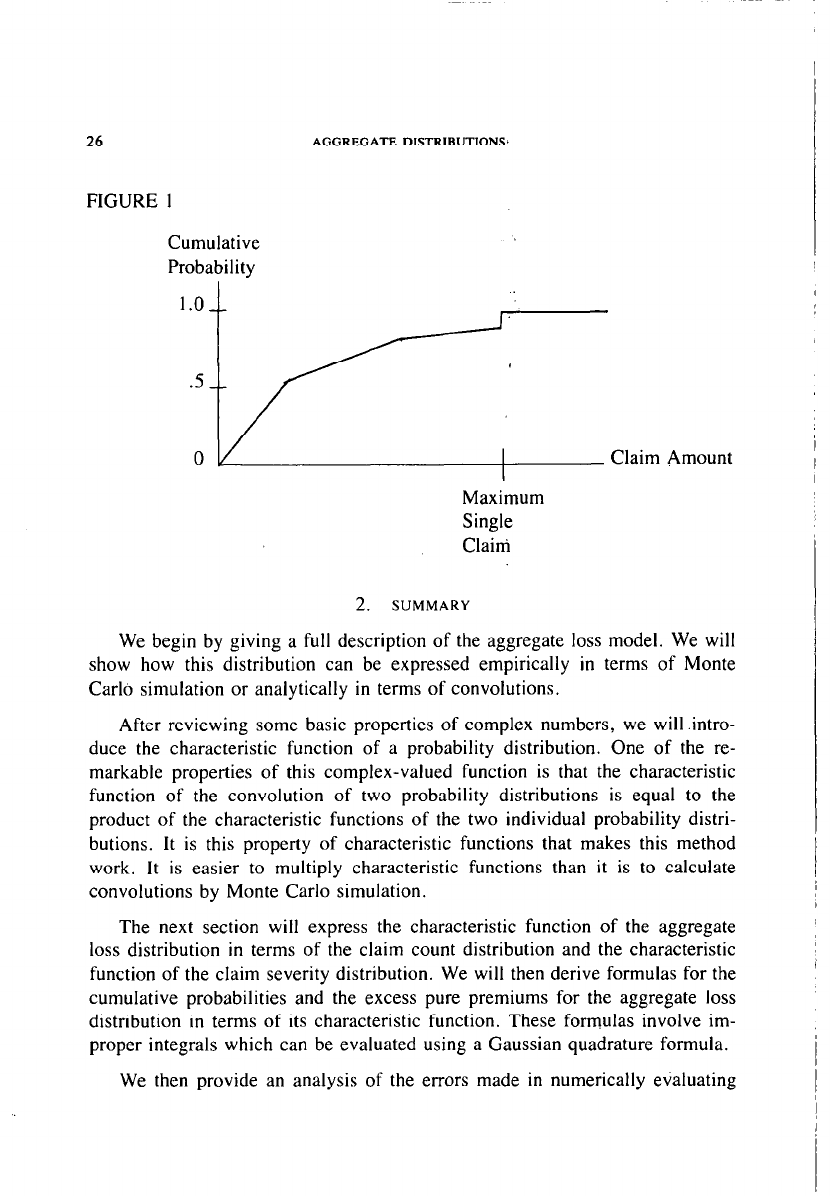

The input required for this algorithm will be the claim count distribution

and the claim severity distribution for each exposure class covered by the

insurance contract. The claim count distribution can be either Binomial, Poisson

or Negative Binomial. The cumulative claim severity distribution is assumed to

be piecewise linear. We also allow the highest possible claim amount to occur

with some non-zero probability. Figure 1 shows a cumulative distribution func-

tion that might typically be considered. Since most claim severity distributions

applicable to the insurance business can be approximated to any desired degree

of accuracy by a piecewise linear cumulative distribution, we feel we have a

completely general method of performing these calculations.

It should be noted that these calculations will require a computer. With the

nearly universal availability of computers, we do not consider this a drawback.

We will warn the reader that the calculations are very complex, but, at the risk

of being repetitious, we will stress the underlying concepts at every opportunity.

This method is far more efficient than the more easily understood process of

Monte Carlo simulation. Having fulfilled our duty to warn the reader, let us

now proceed.

26

AGGREGATE DISTRIBUTIONS

FIGURE 1

Cumulative

Probability

I Claim Amount

Maximum

Single

Claim

2.

SUMMARY

We begin by giving a full description of the aggregate loss model. We will

show how this distribution can be expressed empirically in terms of Monte

Carlo simulation or analytically in terms of convolutions.

After reviewing some basic properties of complex numbers, we will .intro-

duce the characteristic function of a probability distribution. One of the re-

markable properties of this complex-valued function is that the characteristic

function of the convolution of two probability distributions is equal to the

product of the characteristic functions of the two individual probability distri-

butions. It is this property of characteristic functions that makes this method

work. It is easier to multiply characteristic functions than it is to calculate

convolutions by Monte Carlo simulation.

The next section will express the characteristic function of the aggregate

loss distribution in terms of the claim count distribution and the characteristic

function of the claim severity distribution. We will then derive formulas for the

cumulative probabilities and the excess pure premiums for the aggregate loss

distribution in terms of its characteristic function. These formulas involve im-

proper integrals which can be evaluated using a Gaussian quadrature formula.

We then provide an analysis of the errors made in numerically evaluating

AGGREGATE DISTRIBUTIONS

27

the improper integrals. In some cases, the aggregate loss distribution is known.

We test this algorithm by comparing the calculated results with known results.

We also provide a comparison of the calculated results with results produced

by Monte Carlo simulation.

Four examples illustrating the use of this algorithm will be given: (1)

calculating the pure premium of a policy with aggregate limits; (2) calculating

the pure premium of an aggregate stop-loss policy for group life insurance; (3)

calculating the insurance charge for a retrospective rating plan involving two

policies, one of which is subject to an aggregate limit; and (4) an example

similar to (3) except that there is parameter uncertainty for the claim severity

distribution.

3.

THE COLLECTIVE RISK MODEL

Collective risk theory started by considering the generalized Poisson distri-

bution. However, it soon became apparent that the assumptions of this distri-

bution are violated for many applications. In this section we will discuss the

assumptions of the generalized Poisson distribution and indicate some common

violations of these assumptions. We will then state a version of the collective

risk model that can deal with certain violations of these assumptions.

We start by considering the Poisson distribution. The assumptions underlying

this distribution are as follows [16].

1. Claims occurring in two disjoint time intervals are independent.

2. The expected number of claims in a time interval (tl, tz) is dependent

only on the length of the interval and not on the initial value tl.

3. No more than one claim can occur at a given time.

There are situations when these assumptions are violated. We give three

examples.

I. Positive Contagion

A manufacturer can be held liable for defects in its products which, in

many cases, are mass produced. A successful claim against the manu-

facturer may result in several other claims against the manufacturer. The

notion that a higher than expected number of claims in an earlier period

can increase the expected number.of claims in a future period is what is

called positive contagion.

28

AGGREGATE DISTRIBUTIONS

2. Negative Contagion

Consider a group life insurance policy. A death in an earlier period will

reduce the expected number of deaths in a later period. One does not

die twice. The notion that a higher than expected number of claims in

an earlier period can decrease the expected number of claims in a future

period is called negative contagion.

3. Parameter Uncertainty

There are many cases when one feels that a Poisson distribution is

appropriate, but one does not know the expected number of claims. Two

options are available under these circumstances. The first option is to

estimate the expected number of claims using historical experience.

Parameter uncertainty can come from sample error. A second option is

to use the average number of claims for a group of insureds that are

similar to the insured under consideration. Parameter uncertainty arises

if each member of the group expects to have a different number of

claims.

The effect of parameter uncertainty is similar to that of positive

contagion. We give a heuristic argument for this which appeals to modem

credibility theory. Suppose one observes n claims during a certain time

period. Then one can estimate the number of claims, X, in a future period

of equal length using the following formula.

x=Z*n+(l -Z)*E

where E = Prior estimate

Z = Credibility factor.

Note that if the estimate of the expected number of claims is precise or

the group of insureds is homogeneous, the credibility factor will be 0.

If n is greater than expected, the number of claims expected in the

future will be greater than the prior estimate for non-zero values of

credibility.

It should be emphasized that we are not arguing that claims in an

earlier period will cause claims in a later period, as in the positive

contagion case. We are stating only that the claim count distributions

observed under the conditions of parameter uncertainty and positive

contagion should be similar.

We now turn to specifying the claim count distributions we shall use for

each of the above situations. We shall adopt the following notation.

AGGREGATE DISTRIBUTIONS

29

n - A random variable denoting the number of claims

A - The expected number of claims (A = E(n))

x - A random variable with E(X) = 1 and Var (x) = c

Parameter uncertainty can be modeled by the following algorithm.

Algorithm 3. I

1. Select x at random from the assumed distribution.

2. Select the number of claims, n, at random from a Poisson distribution

with parameter xh.

We have the following relationships.

E(n) = E(nlx) * E(X) = X

Var (n) = &War (nix)) + Var, MnlxN

= E,(xA) + Var, (xh)

= A + cA*.

(3.1)

(3.2)

If x has a Gamma distribution, the claim count distribution described by

Algorithm 3.1 is the Negative Binomial distribution [17]. We shall use the

Negative Binomial distribution to model both the positive contagion and the

parameter uncertainty cases.

We shall call the paramter c the contagion parameter for the claim count

distribution. We should note that c has also been called the contamination

parameter by some authors [ 181. It should be noted that if c = 0, Algorithm

3.1 yields the Poisson distribution.

We shall use the Binomial distribution to model the negative contagion case.

If m is the number of trials and p is the probability of success, we can formally

define the contagion parameter to be equal to -l/m. Substituting this into

Equation 3.2 yields the correct Binomial variance.

Var(n) = A - X*/m = mp - m2p2/m = mp( 1 - p)

While a negative contagion parameter makes no sense in terms of Algorithm

3.1, we shall see below that this is a very appropriate definition.

We now adopt the following notation.

z-A random variable denoting the amount of a claim

S(z)-The cumulative distribution function of z

x-A random variable denoting the aggregate loss for an insured

30

AGGREGATE DISTRIBUTIONS

Aggregate losses can be generated by the following algorithm.

Algorithm 3.2

1. Select the number of claims, n, at random from the assumed claim count

distribution.

2. Do the following n times.

2. I Select the claim amount, z, at random from the assumed claim

severity distribution.

3. The aggregate loss amount, X, is the sum of all claim amounts, z, selected

in step 2.1.

Let F(x) denote the cumulative distribution function for the aggregate losses

generated by Algorithm 3.2. We now give expressions for the mean and the

variance of this distribution.

E(x) = E(n) * E(z) = A * E(z)

(3.3)

Var (n) = E,,(Var (xln)) + Var,, (E(xln))

= E,,(n . Var (z)) + Var,, (n * E(z))

= A . Var (z) + (A + CA’) * E* (z)

= A . E(z*) + CA* . E* (z)

(3.4)

Implicit in the use of Algorithm 3.2 is the assumption that the claim severity

distribution, S(z), is known. In practice this distribution must be estimated from

historical observations, or it must be simply assumed. Parameter uncertainty of

the claim severity distribution can significantly affect the predictions of the

collective risk model, and it should not be ignored. Our response to this problem

is to make the simplifying (and we think reasonable) assumption that the shape

of the distribution is known but there is uncertainty in the scale of the distri-

bution.

More precisely, we specify parameter uncertainty of the claim severity

distribution in the following manner. Let p be a random variable satisfying the

conditions E(lIP) = 1 and Var (I/p) = b. We then model aggregate losses by

the following algorithm.

Algorithm 3.3

1. Select the number of claims, n, at random from the assumed claim count

distribution.

2. Select the scaling parameter, p, at random from the assumed distribution.

AGGREGATE DISTRlBUTIONS

31

3. Do the following n times.

3.1 Select the claim amount, z, at random from the assumed claim

severity distribution.

4. The aggregate loss amount, X, is the sum of all claim amounts, z, divided

by the scaling parameter, B.

Let 9(x) denote the cumulative distribution function for the aggregate losses

generated by Algorithm 3.3. Let U(B) be the cumulative distribution function

for the scaling parameter, B. Then the relationship between B(X) and F(x) is

given by the following equation.

x

S(x) =

I

~~P&wP)

(3.5)

0

We now give formulas for the mean and the variance for the aggregate

losses generated by Algorithm 3.3.

E(x) = E&WlPN

= Ep(A . E(z)@)

= A . E(z) . E(lIB)

= A . E(z)

(3.6)

Var (4 = .&War CUP>> + Varp (E(xlP))

= Ea[(A * E(z*) + CA* * E*(z))@*] + Varp (A . E(z)@)

= (A . E(z*) + CA* . E*(z)) * E(l/B2) + A* . E*(z) . Var (l/B)

= (A . E(z*) + CA* . E*(z)) . (I+b) + A2 . E*(z) . b

= A . E(z’) (l+b) + A* . E2(z) . (b+c+bc)

(3.7)

In this paper, we shall assume that B has a Gamma distribution. We shall

call b the mixing parameter. The mixing parameter is a measure of parameter

uncertainty for the claim severity distribution.

It should be noted that we have chosen mathematically convenient distri-

butions to model contagion and parameter uncertainty. We do not want to imply

that these distributions are in any way the “correct” ones. Since parameter

uncertainty is not directly observable, it is difficult to discover what the proper

distribution should be. It should be noted that it is possible to infer the variance

of the parameter uncertainty through the use of Equations 3.4 and 3.7 [ 141. But

until statistical methodology has advanced to the point where the proper distri-

bution can be determined, it should be acceptable to use ones which are math-

ematically convenient.

32

AGGREGATE DISTRIBUTIONS

4.

CONVOLUTIONS

The above discussion provides a complete description of the aggregate loss

model we use in this paper. Algorithms 3.2 and 3.3 provide the means to

calculate the cumulative distribution by Monte Carlo simulation. Unfortunately

this is a long and expensive process. We now begin to develop the mathematical

tools necessary to derive a more efficient process.

Initially we will be concerned with the cumulative distribution function F(x)

which is described by Algorithm 3.2. We will then make use of Equation 3.5

to derive the cumulative distribution function B(X) described by Algorithm 3.3.

Let x be a random variable which has a distribution function F(x). Similarly,

let y be a random variable which has distribution function G(y). Let z = x +

y. Then the convolution of F and G, denoted by F * G is the distribution

function for z. We can express this analytically by the equation

(F * G)(z) = 1’ F(z-y)dGCy).

0

Let S(z) be a claim severity distribution. Define

so’(z) = { ‘: ;: f ; ;

S”‘(z) = (P”’ * S)(z).

One can see that S”‘(z) is the distribution of the total amount of exactly n claims.

Algorithm 3.2 can be expressed in the following manner.

Algorithm 4. I

1. Select the claim count, n, at random.

2. Select the aggregate loss amount, X, from the distribution 5”‘.

We now give an analytical expression for this process. Let F(x) denote the

distribution function for the aggregate loss distribution. Let P(n) denote the

probability of exactly n claims. We then have

F(x) = n$o P(n) . S”‘(x).

(4.1)

AGGREGATE

DISTRIBUTIONS

33

5.

CHARACTERISTIC FUNCTIONS

It may be helpful at this point to review some properties of complex numbers.

A complex number, z, is one which can be written in the form

z = a + bi,

(5.1)

where a and b are real numbers and i = m. The number a is called the real

part of z and b is called the imaginary part of z. Alternatively, z can be written

in the form

z = t-e”,

(5.2)

where r is a nonnegative real number and 0 is any real number; r is called the

modulus of z, and 8 is called the argument of z.

The equivalence of Equations 5. I and 5.2 can be seen by using Euler’s

formula.

e

io = cos (0) + i * sin (0)

(5.3)

Using this formula it is not difficult to show that the following relationships

hold.

r=VTT?

(5.4)

1

arctan (b/a) if a > 0

7~ + arctan (b/a) if a < 0 and b 1 0

0=

arctan (b/a) - n if a < 0 and b 5 0

(5.5)

~12 if a = 0 and b > 0

- ~12 if a = 0 and b -C 0

a = r cos (0)

(5.6)

b = r sin (0)

(5.7)

Having given a brief discussion of complex numbers, we define the char-

acteristic function (or Fourier transform) of a cumulative distribution function

F.

&(t) = E(e’“) = Lm e”‘dF(x)

(5.8)

Let F and G be two cumulative distribution functions.

&p&t) = E(e’“) = 6 e’“d(F * G) ,

34

AGGREGATE DISTRIBUTIONS

Since z is the sum of x and y, and x and y are independent, we have

&-dt)

= Ede”‘) = .&de

i’(r+r)) = &(e’“) E,(e’“‘) = +F(t)$G(f).

Thus we have proved the following well known result.

+w*G)w

= +4t) 4kw

(5.9)

As a consequence of this equation we have the following.

4?dO = (~SWS’

(5.10)

Combining Equations 4. I and 5.10 we get the following expression for the

characteristic function of an aggregate loss distribution, F.

4+(t) = ,go m)(4&))”

(5.11)

As stated above, we assume that the claim severity distribution is piecewise

linear. We now specify the mathematical form of the claim severity distribution,

S(z).

1. Let n be a nonnegative integer.

2. Let 0 I 01 < . . . < a,, < a,,+!.

3. Let pk denote the probability that an individual loss is between ak and

ak+ I.

4. For up < z < u~+~, the probability density of z is given by

dk = pkl(an+, - ak).

5. The probability that a claim is equal to a,,+1 is given by

1 - i pk.

k=l

This allows us to describe the accumulation of claim values at the policy

limit (a,,+ I).

We now calculate the characteristic function of S(z).

+s(t) = [ e’“d.S(z)

dk . ei”dz + ( 1 - i, pk) eirr”‘-’

AGGREGATE DISTRIBUTIONS

Using Euler’s formula (Equation 5.3) we continue.

35

$s(t) = $ kg, dk(Sh (1

uk+,) - sin

(tak)) + 1 - i p, cos (tan+ I)

( k=, k)

+ i $ k$, dk (COS (tak) -

COS

(tak+,)) + i

(I - $, pk)

sin (r&+1)

Let h(t) and f(t) denote the real and imaginary parts of

+s(t)

respectively.

h(f) = ; $, dk

(Sin (tan+,) - Sin (t&c)) +

( ,, )

1 - z pk

COS (tan,,)

(5.12)

sin (ta,,+ ,) (5.13)

We now turn to the problem of calculating the characteristic function of the

aggregate loss distribution. Our main tool will be Equation 5.1 I.

Case I Binomial Distribution P(n) =

$F(Z) = 2 (“)

n=o n

p”( 1 -p>‘“-“(+s(t))”

W) = ,io (;) (phs(t))” - (1 -pyz

cbM = (P440+ 1 -p)

,”

&o) = ( 1 + p (W)- I))“’

If we make a change of notation and let A = mp and c = - I/m, we get

$F(r) = (1 - A(+&) -I))-“‘.

(5.14)

36

AGGREGATE DlSTRIBUTlONS

e- AX”

Case 2 Poisson Distribution F(n) = 7

.

(PM = ,zo $ (4sW

(Pp.(t) = go e-“(A ;*!4@)”

(b&) = e-A 5 (A * pw)”

n=o

,$&) = e-Ae”‘msc”

4~0)

= e

A.(+s(o- I )

Case 3 Negative Binomial Distribution

Qn)=(n’l~-f)(I +cA)-“‘.(A-

4F(0 = iii

,,=o(n+1~-1)il+cA)“‘(~~(4s(t))”

4FW = 5

n=o(n+ I;- I)(] +cA)-“C(+$!&)”

4FW = Ii

nzo(n+I;-l)(l +cA)-‘l’(e)”

4sw

where ’ = 1 - cA(+s(t) - 1)

&(t) = (I + CA)- I/c (I + cX)“c

&(t) = (I - cA(+s(t) - I))-“C

(5.15)

(5.16) :

Note that Equations 5.14 and 5. I6 are identical except for the different

I

interpretation of the contagion parameter c. It should also be noted that the

expression in Equations 5.14 and 5. I6 approaches the expression in Equation

5. I5 as c approaches 0.

AGGREGATE DISTRIBUTIONS

37

In the computer program described below, we set c = IO-’ whenever Ic( <

IO-‘. Thus the same computer code handles all three cases.

6.

THE AGGREGATE LOSS DISTRIBUTION

In the preceding section we derived the characteristic function for the ag-

gregate loss distribution for a single coverage or exposure class. In this section

we use the above results to derive formulas for the cumulative probabilities and

the excess pure premiums for multiple coverages or exposure classes.

For the sake of convenience, we make the following definitions.

F(x) = Cumulative distribution function of the aggregate losses for all cov-

erages combined

p = Mean of aggregate loss distribution

cr = Standard deviation of aggregate loss distribution

At) = modulus (4~(tla>)

g(t) = argument (+F(t/a))

For each coverage, j, we define the following.

hi(t) = hj(tlU) - I

(6.1)

kj(t)

= ij(t/U)

(6.2)

where hj and /?j are given in Equations 5.12 and 5.13.

Note the F(x) is the convolution of the aggregate loss distributions for each

individual coverage. Using Equations 5.4, 5.5, 5.9 and 5.12-5.16 we have the

following.

f(t) = n modulus (I - cjAj(+s,(tlo) - l))-“”

j

f(t) = n modulus (1 - cjAj(hj(t) + ikj(t)))-I”’

i

At) = I-J ((I - cjAjhj(t))* + (cjAjkj(t))2)-“2”’

j

g(t) = 2 argument (I - cjAj(+s,(t/o) - I))-“”

i

g(r) = z argument (I - cjAj(hj(t) + ik,{t)))-““j

i

(6.3)

(6.4)

38

AGGREGATE DISTRIBUTIONS

Once the modulus and the argument of the aggregate characteristic have

been determined, it is possible to calculate the cumulative probabilities by use

of the following formula.

(txlu - g(t)) dr

(6.5)

The excess pure premium can be obtained from the cumulative distribution

function by the following formula.

EP(x) =

i

r (u - xMF(u)

Applying this to Equation 6.5 we get the following formula.

7 (cos (g(t)) - cos (txlu - g(t)))dr

(6.6)

The excess pure premium ratio is defined by the following formula.

Ef?(x) = EP(x)Ipa

We now introduce parameter uncertainty of the severity distributions.

s(x) =; +; in”ly (] + (LJ)-““”

sin ((I + r) arctan ($)- g(t)) dr (6.7)

= At>

%9(x) = f-l - 5 + ; o 7 cos (g(r)) -

I [

(1 + ($)‘)-“‘cos (r . arctan ($) - g(r))] dr

In the above two formulas. r = 1 + l/b.

(6.8)

AGGREGATE DISTRIBUTIONS

39

Equations 6.5-6.8 are derived in Appendix A. It should be noted that

Equation 6.5 is the limit of Equation 6.7 as b approaches 0. Similarly Equation

6.6 is the limit of Equation 6.8 as b approaches 0. In our program we set b =

IO-’ whenever b < IO-’ and thus the same computer code handles both

situations.

Equations 6.7 and 6.8 are set up so that the parameter uncertainty of claim

severity affects all coverages in the same way. This may be realistic if one

believes that uncertainty in claim severity is due to inflation and that inflation

affects all coverages in the same way. If one wants parameter uncertainty of

claim severity for each coverage to be independent, several runs of the program

will be required. An example showing how to do this will be given below.

7.

NUMERICAL INTEGRATION

We now turn to the problem of evaluating the integrals given in Equations

6.7 and 6.8. It should also be noted that our program is written in FORTRAN

to run on a large (IBM 370) computer. In this environment, it gets nearly

instantaneous response at the computer terminal. The same algorithm has also

been coded in BASIC to run on a TRS80 Model III microcomputer where it

reproduces the mainframe results though with substantially greater running time.

The actual FORTRAN code is included as Exhibit IX.

We now outline our algorithm. Explanation for the steps will be given

below.

Step

1. Enter the parameters for the claim severity and the claim count distri-

butions.

2. Calculate the aggregate mean, )I, and standard deviation, cr.

3. Enter the loss amounts, x.

4. Calculate basic interval length, h.

12 = 2rru /(maximum loss amount)

5. In order to apply the Gaussian quadrature formulas, we must evaluate

the integrands at specified points. We evaluate the functions f(f) and

g(t) at the appropriate points in each of the following intervals.

40

AGGREGATE DISTRIBUTIONS

Interval Number

Interval

I

(0, h/16)

2 (h/16, h/8)

3 (h/8, h/4)

4 (h/4, h/2)

5 (h/2, h)

6 (h, 2h)

j+4

(0’ - l)h, jh)

j is determined so that At)t < .00002 for all values of t evaluated in the

interval ((j - I)h, jh).

6. For each loss amount, x, evaluate 9(x) and %9(x) by summing the results

of the Gaussian quadrature formulas over each of the intervals given in

Step 5.

We now give a more detailed explanation of the above steps

Step I

The parameters for each claim severity distribution are the claim severities

a,, ; . . ,

a,,+ I and the associated probabilities PI, . . .p,,.

The parameters for each claim count distribution are the expected number

of claims and the contagion parameter, c. Note that if ICI < IO-‘, we substitute

c = lo-‘.

We must also enter the mixing parameter, b. If b < IO-’ we substitute

b = IO-‘.

Step 2

For each coverage we calculate the aggregate mean and variance according

to Equations 3.6 and 3.7. The aggregate mean and variance are the sums of the

individual means and variances for each coverage.

Step 4

Evaluating a typical g(t) showed that g(t) changes slowly. See Figure 2.

Also, r * arctan (xtlru) is an increasing function of t which is bounded by xtl

u. Thus by choosing h = 2nu/(maximum loss amount) we assure that the

interval of integration will contain no more than one oscillation of the integrand.

AGGREGATE DISTRIBUTIONS

41

FIGURE 2

Step 5

The evaluation off(t) and g(t) is the most time consuming operation of this

entire algorithm. Thus f(t) and g(t) should only be evaluated once for any given

value of t, and the number of points, I, at which these functions are evaluated

should be as few as possible. Inspection of the integrands of Equations 6.7 and

6.8 revealed that they changed most rapidly in the interval (0, h). See Figures

3 and 4. Thus it was felt that the intervals used in the numerical integration

should be relatively short in the interval (0, h).

By a change of variables, each interval of integration was transformed from

the given interval to the interval (- 1, I). The Gaussian 5-point formula is then

applied. The points, tj, where fit) and g(r) must be evaluated are as follows.

11 = (-0.90617985 (b - u) + (b + a)) /2

t2 = (-0.53846931 (b - a) + (b + u)) /2

t3 = (b + a) /2

t.q = (0.53846931 (b - u) + (b + a)) 12

t5 = (0.90617985 (b - a) + (b + a)) /2

Here a is the left endpoint of the interval, and b is the right endpoint of the

interval under consideration. If f(<j) / Ij < .00002 for j = 1, . . . , 5 or the

number of intervals equals 256, no more intervals are used.

42

AGGREGATE DISTRIBUTIONS

FIGURE 3

FIGURE 4

AGGREGATE DISTRIBUTIONS

43

Step 6

Now that f(t) and g(t) are evaluated and stored in an array, it becomes an

easy task to evaluate B(X) and %9(.x). For each interval of integration we use

the following rule to evaluate the integral.

. (interval length/2)

where P(t) = fct,

t

(interval lengthl2)

1 + (zr)-““‘“sin ((1 + r) arctan (5) - g(r))

Q(t) = $? [ (

cos (g(t)) - (1 + ( $r)+2cos (r . arctan (z) - g(t))]

W, = Ws = 0.23692689

W2 =

W4 =

0.47862867

W3 = 0.56888889.

Then 3(x) = .5 + (Sum of all the f,,‘s) 1~ and

%9(x) = p, - x/2 + (Sum of all the IE’s) u/r.

8.

ERROR ANALYSIS

There are three sources of error in the above calculations.

Roundoff Error

We use double precision arithmetic at every stage of our calculation. Double

precision numbers are accurate to 16 significant digits on IBM equipment. Even

though the calculations leading to a particular output value could number in the

hundreds, it is doubtful that accumulated roundoff error could be an important

factor in our calculations.

Discretizution Error

The discretization error for the Gaussian 5-point formula is given by the

expression

44

AGGREGATE DISTRIBUTIONS

f’“‘(S)

73 52 38 = 8.08

x

11 2

lo-‘O

*

*f’“’ (EJ, 5 in (-l,l).

. . .

Since the integrands are reasonably smooth (see Figures 3 and 4) the bound on

f’“’ should be reasonable. Thus the discretization error should not be significant.

Truncation Error

The most significant source of error in these calculations is the truncation

error, or the error made by substituting an integral with finite limits of integration

for an integral with infinite limits of integration. We now turn to analyzing this

truncation error.

The truncation error, ET, for the excess pure premium is given by

(1 + (s)‘)-d2cos (r * arctan (2) - g(tJ)]df

where a is the limit of the finite integral.

Now IET/ I ; j-- ‘3 (1 + 1)dt

= % - max (f(t)) * i .

120

NowAt) = 1 6 e”“dF(x) / I [ 1 eirx 1 dF(x) = I.

(8.1)

(8.2)

AGGREGATE DISTRIBUTIONS

45

The bound on the truncation error given by Equation 8.2 is extremely

conservative because, as we show in Appendix B, maxrZ,Ar) will be signifi-

cantly less than one for most cases of interest. In fact, if each (piecewise linear)

claim severity distribution function is continuous, f(t) approaches the probability

of zero claims as t approaches infinity. For example, when the claim count

distribution is Poisson with a mean of 10 claims, f(t) will be close to e-” or

0.0000454 for large t.

The bound on the truncation error given by Equation 8.1 is also conservative

because the integrand repeatedly changes sign.

In our program, a is usually chosen so that max,,, (f(t)) * I/a < .00002.

Thus we would expect the truncation error for the excess pure premium ratio

to be bounded by .000013 * alp,.

The truncation error for the cumulative probabilities does not permit an

analysis similar to the above because the denominator of the integrand contains

t instead of t’. The examples in the next section will show that cumulative

probabilities calculated by this algorithm seem to be accurate. But they are

somewhat less accurate than the excess pure premium.

9.

NUMERICAL TESTS OF THE ALGORITHM

There are cases when the algorithm can be compared with known results.

We consider two such cases.

If the contagion parameter, c, is equal to - 1, then 4&r) = 4&r). The

choice of c = - I corresponds to the Binomial distribution with m = p = I.

For our first example, consider the following.

F(x) = S(x) = x for 0 I x 5 I

ER(x) = ;

I

I

(I - F(u))du = (I - x)~

I

Table 9. I compares computed to actual results.

\

46

X

.lO

.lOOO

.20

.2000

.30

.3000

.40

.4000

.50

.5000

.60

.6000

.70

.7000

.80

.8000

.90

.9000

1.00

1 .oooo

AGGREGATE DISTRIBUTIONS

TABLE 9.1

F(x)

F(x)

Actual Computed

Wx)

Actual

.lOOO

.8100 .8100

.2000

.6400

.6400

.3000

.4900 .4900

.4000

.3600 .3600

.5000

.2500 .2500

.6000

.1600 .1600

.7000

.0900 .0900

.8000

.0400 .0400

.9000

.OlOO .OlOO

.9995

. 0000 . 0000

ER tx)

Comuuted

For our next example, consider the following.

F(x) = S(x) = x12 for 0 % x < 1

F(1) = S(1) = I

ER(x) = L

1'

p .I

(1 - F(u))& = (3 - x)(1 - x)/3

For reasons described in Section 7 above, the program required 256 intervals

for the numerical integration. The value off(t)lt for the largest value of t was

equal to .OOl. Using Equation 8.2 we obtained an estimate of .00027 as a

bound on the truncation error for ER(x). Table 9.2 compares computed to actual

results.

These examples would seem to indicate that the calculation of ER(x) is more

accurate than that of F(x). If F(x) is continuous, the error appears to be small,

but, if F(x) is not continuous, the errors may not be so small near the points of

discontinuity.

We now turn to a more realistic example. Exhibit II shows an actual run of

our program. Details concerning the input will be given in the discussion of

aggregate increased limits factors which follows. Here we provide a comparison

between the results of our program and a Monte Carlo simulation. One should

not expect exact agreement between expected and observed results due to

AGGREGATE DISTRIBUTIONS

47

TABLE 9.2

x

F(x)

Actual

.lO

.0500 .0501 .8700 .8700

.20

.lOOO .lOOl

.7467

.7467

.30

.1500

.1502 .6300

.6300

.40 .2000 .2002 .5200 .5200

.50 .2500 .2502 .4167 .4167

.60

.3000 .3003 .3200 .3200

.70 .3500 .3504 .2300 .2300

.80 .4000 .4005 .1467 .1467

.90 .4500 .4511 .0700

.0700

.99 .4950

.4869

.0067 .0067

1.00

1.0000 .7499 .oooo .OOOl

1.01 1.0000 1.0081 . 0000

.oooo

1.05

1.0000 .9979 .oooo .oooo

F(x) Wx)

Computed Actual

J-(X)

Computed

simulation error. For this reason we performed a Chi-Square test on the results

to see if the difference could be explained by random fluctuations. The results

are in Table 9.3.

The expected number of claims in each cell was obtained from Exhibit II.

The observed number of claims in each cell was obtained by a Monte Carlo

simulation using exactly the same input parameters as those in Exhibit II. Ten

thousand trials were used.

If the differences between observed and expected values are due solely to

random fluctuations, one should expect a Chi-Square value of 25. In this case

we get a slightly higher value of Chi-Square. We have performed similar tests

on many occasions and have gotten similar results. The algorithm works.

10. AGGREGATE LIMITS

We now consider how this algorithm can be used to calculate the premium

for a policy that is subject to an aggregate limit.

Underwriters have long felt that lines of insurance such as Products Liability

and Medical Malpractice present a severe catastrophe potential. For example,

48

AGGREGATE DlSTRlBUTlONS

TABLE 9.3

CHI-SQUARE TEST FOR AGGREGATE

Loss

DISTRIBUTIONS

Upper Cell Boundary

Observed Expected

50,000

51

52

100,000

273

268

150,000

432

435

200,000 546

540

250,000 589

587

300,000

632

628

350,000

736

737

400,000

782

782

450,000

789 769

500,000

721

720

550,000

641

662

600,000 625

622

650,000 597

561

700,000

506 491

750,000

402

416

800,000 353

349

850,000 269

294

900,000

227

241

950,000

201

195

1 ,ooo,ooo 135

154

1,050,000 93

121

1,100,000

102 94

1,150,OOO

73 73

1,200,000

46

55

1,250,OOO 39

42

Over 1,250,OOO 140

112

Chi-Square = 26.0

Degrees of Freedom = 25

AGGREGATE DlSTRIBIJTIONS

49

the publicity given a Products Liability lawsuit may well provoke several ad-

ditional lawsuits by others who have purchased the same product. Thus under-

writers have justifiably sought to limit the total amount of losses that can be

paid out under a single policy.

The price for a policy with an aggregate limit (ignoring expense consider-

ations) will be the price of a similar policy with no aggregate limit less the

excess pure premium for the aggregate limit. Below, we will give several

examples of such calculations using Exhibits II to V. But, before we do this,

let us discuss the input parameters.

The claim severity distribution chosen is typical for Products Liability cov-

erages. We will not discuss selection of the claim severity distribution here.

Instead we will refer the interested reader to the literature [ 191 [20].

The claim severity distribution will be subject to a $250,000 occurrence

limit.

The mean of the claim count distribution was calculated by dividing total

expected losses by the severity mean ($18,198). In Exhibits II, IV and V a

contagion parameter of zero was chosen. This choice gives the Poisson distri-

bution. In Exhibit III we chose a contagion parameter of .25. In light of the

catastrophe potential for Products Liability that was discussed above, a more

highly skewed claim count distribution would indeed seem justified.

A mixing parameter of 0 is used in this example.

Tables 10.1 and 10.2 show the discounts expressed as a proportion of the

total expected loss.

While a more highly skewed claim count distribution may be justified for

Products Liability, it does not give a conservative price for a policy with an

aggregate limit. Thus we would recommend using a Poisson distribution for the

claim count unless one has definite evidence that a more skewed distribution is

appropriate.

Notice that the discounts depend upon the expected loss. Present tables of

increased limits factors do not reflect this dependence. We admit that there is a

practical problem involved in publishing increased limits factors that vary by

expected loss. However, the “practical” solution of not considering the expected

loss can produce embarrassing examples such as the following. This method is

identical to that given in I.S.O. rating manuals.

50

AGGREGATE DISTRIBUTIONS

TABLE 10.1

DISCOUNTS FOR AGGREGATE LIMITS

Expected Loss = $500,000

Contagion

Parameter

Aggregate Limit 0.00 0.25

$ 600,000 .I394 .2132

800,000 .0516 .1125

1 ,ooo,ooo .0165 .0570

1,200,000 .0046 .0279

1,400,000 .0012 .0133

TABLE 10.2

DISCOUNTS FOR AGGREGATE LIMITS

Contagion Parameter = 0.0

Expected Loss

Aggregate Limit

$250,000

$500,000

$1 ,ooo,oOO

$ 600,000 .0296 .1394 .4202

$ 800,000 .0060 .0516 .2665

$1 ,ooo,ooo

.OOlO

.Ol65

.1528

$1,200,000 .0002 .0046 .0791

$1,400,000 - .OOl2 .0371

Basic Limits - $25,000 per occurrence and $75,000 aggregate

Base Rate

- $1 .OO per unit of exposure

Exposure - I ,OOO,OOO units

If an insured bought a policy for the basic limits, he would pay $1 ,OOO,OOO and

the most he could recover in losses is $75,000! While it is unlikely that such a

policy has ever been sold, significant errors could be quite common.

AGGREGATE DISTRIBUTIONS

51

We propose the following as a remedy to this situation.

1. Publish increased limits tables for occurrence limits only.

2. Do not give discounts for aggregate limits. Instead, publish a table of

aggregate limits which are appropriate for a given expected loss. The

aggregate limits should be sufficiently high so that the indicated discount

is less than a nominal amount, say 0.5%.

Using Exhibits II, IV and V we can derive the appropriate aggregate limits.

Expected Loss

Aggregate Limit

$ 250,000

$ 825,000

500,000 1,200,000

1 ,ooo,ooo 1,900,000

11. GROUP LIFE AGGREGATE EXCESS INSURANCE

We now give the solution to a problem that was proposed to us by a life

actuary of our company.

A large employer wanted to self insure his group life insurance. To protect

against a catastrophe, he wanted to purchase aggregate excess insurance to cover

losses in excess of 1.25 times the expected loss. The following data were

provided to us.

Group

Age Range

Number of Lives Expected Loss

1

29 and Under 2,073 47,086

2 30-34

1,135 36,342

3 35-39

1,044 35,380

4

40-44

822 54,938

5 45-49

1,004 136,126

6 50-54

1,193 270,050

7

55-59

975 395,47 1

8 60-64

546

258,525

9

65 and Over 25 13,247

The expected loss was computed using a mortality table and the average

amount of insurance in each group.

It was felt that the claim count distribution should be binomial. Thus we

chose a contagion parameter of - l/(number of lives) for each group. We were

not given a distribution of insurance amounts for each group. Assuming that all

52

AGGREGATE DISTRIBUTIONS

insureds had the average amount of insurance in each group would understate

the excess pure premium. For this reason we requested rough estimates for

those distributions.

The mixing parameter selected was 0.0.

It should be noted that the assumptions of the collective risk model are

violated in this example. When a person dies, the amount of his insurance

policy is removed from the claim severity distribution. However the turnover

of group members should keep the claim severity distribution approximately the

same. Thus we feel that the collective risk model will be a good approximation

of the true situation.

Exhibit VI gives the computer run for the problem. The pure premium for

this coverage was calculated to be 1.53% of the expected loss.

12.

RETROSPECTIVE RATING; NESTED AGGREGATES

A retrospective rating plan is a rating plan in which the final premium is

determined after the policy period has expired [21]. While these plans have

many features, we will limit this discussion to plans where the insurer is liable

for all losses above an agreed upon amount.

Retrospective rating plans can cover several different policies under a single

plan. Here we provide a simple example showing how to calculate the pure

premium, or insurance charge, for such a rating plan. Our example will consist

of two coverages, Workers’ Compensation and Products Liability.

The Workers’ Compensation policy has an expected loss of $500,000. The

claim severity distribution is given in Exhibit I. The contagion parameter is .05.

The mixing parameter is 0.0.

The Products Liability policy has an expected loss of $500,000 before

application of the aggregate limit. The claim severity distribution is given in

Exhibit 1. The contagion parameter is .25. The policy that is written under the

retrospective rating plan is subject to a $1 ,OOO,OOO aggregate limit. The mixing

parameter is 0.0.

The presence of a policy subject to an aggregate limit in the retrospective

rating plan makes it necessary to run the program twice to determine the

insurance charges. Exhibit III will serve as the first run of the program. For the

second run we treat the Workers’ Compensation parameters in the usual manner.

For the Products Liability, we substitute the aggregate loss distribution in Exhibit

AGGREGATE

DISTRIBUTIONS

53

III for the claim severity distribution. We, of course, limit the aggregate losses

to $1 ,OOO,OOO. The contagion parameter is - 1. This corresponds to a binomial

claim count distribution with m = p = 1. The results of the second run are

shown in Exhibit VII. It can be seen, for example, that the insurance charge

for a plan which covers losses in excess of $1,500,000 is $21,894.

We now consider parameter uncertainty for the scale of the claim severity

distribution.

Misestimation of the claim severity distribution can occur because of limited

information on the individual coverage. In this case one would expect the scale

uncertainty for each coverage to be independent. Misestimation of future infla-

tion can also cause scale uncertainty. In this case one could expect the scale

uncertainty to affect each coverage in the same way. The following example

shows how to handle both of these cases. It will be necessary to run the program

once for each individual coverage. A final run is then required to combine the

individual coverages.

The Workers’ Compensation policy has the same parameters that were

specified in the above example with the exception that the mixing parameter is

set equal to .05. This reflects uncertainty in the scale of the claim severity

distribution for Workers’ Compensation. The aggregate loss distribution for this

coverage is given in Exhibit VIIIA.

The Products Liability policy has the same parameters that were specified

in the above example with the exception that the mixing parameter is set equal

to .05. This reflects uncertainty in the scale of the claim severity distribution

for Products Liability. The aggregate loss distribution is given in Exhibit VIIIB.

It should be noted that this aggregate loss model adjusts the policy limit with

the scaling parameter, while in the real world the policy limit remains fixed.

However this should not significantly affect the final results.

The aggregate loss distributions for Workers’ Compensation and Products

Liability are then combined to get the aggregate loss distribution for the total

losses of the two coverages. Here the aggregate loss distribution for each

coverage is treated as the claim severity distribution for the final run of the

program. The Products Liability loss is limited to $l,OOO,OOO. The contagion

parameter for each coverage is set equal to - 1. The mixing parameter is set

equal to .05. This reflects uncertainty in the scale of the aggregate loss distri-

bution. For a given year the scale parameter is identical for both coverages. It

should be noted that, as we do above, this aggregate loss model adjusts the

aggregate limit with the scaling factor.

54

AGGREGATE DISTRIBUTIONS

The results of the third run are shown in Exhibit VIIIC. It can be seen, for

example, that the insurance charge for a plan which covers losses in excess of

$1,500,000 is $46,424. Here one can see that that parameter uncertainty can

significantly affect the required insurance charge.

13.

CONCLUSION

We have described an efficient and accurate algorithm which calculates the

cumulative probabilities and excess pure premiums for the collective risk model.

The program and related programs have been used at our company in

applications described above and many others. These include the analysis of

profit sharing plans, large account pricing, aggregate deductibles and sliding

scale dividend plans. Also, we are currently exploring applications involving

the optimization of reinsurance retentions [IS] and designing a retrospective

rating plan which properly accounts for the “overlap” problem [22]. In short,

this is a very useful program.

Our exposure to these applications has led us to believe that further work

needs to be done with the collective risk model. In particular, we need to test

the predictions of the collective risk model against actual aggregate loss data.

We also need to test the sensitivity of the collective risk model to violations of

the assumptions underlying it.

14.

ACKNOWLEDGEMENTS

This paper had its origins in an anlysis of Shaw Mong’s paper [lo] which

was done by Glenn Meyers and Nathaniel Schenker. Comparisons of Mong’s

results with Monte Carlo simulations suggested that Mong’s technique worked

well when the claim severity distribution was a Gamma distribution, but oth-

erwise it worked poorly. It was also noted that Mong’s technique could be

modified to work for any claim severity distribution provided one could calculate

its characteristic function.

The classic book on risk theory by Beard, Pentikainen and Pesonen ]7] had

a very strong influence in our thinking, as can be noted by our several references

to it. We regard this paper, in part, as a synthesis of the ideas in Mong’s paper

and Chapter 8 of the book.

Another strong influence has been observing the various ways this algorithm,

and prior Monte Carlo simulations,

have been used. We received excellent

AGGREGATE

DISTRIBUTIONS

55

feedback from the following individuals: Burton Covitz, Michael Larsen, John

Meeks, Arthur Placek, and Philip Wolf: The following individuals made several

helpful comments while we were preparing this paper: Bradley Alpert, Yakov

Avichai, Sam Gutterman, Phillip Norton, Nathaniel Schenker, and Edward

Seligman. We offer our sincere thanks.

APPENDIX A

DERIVATION OF EQUATIONS

6.5-6.8

The purpose of this appendix is to derive Equations 6.5-6.8. We will first

derive expressions for the cumulative probability and the excess pure premium

in terms of c@(f) and U(p). Equations 6.5-6.8 will then be special cases of

these expressions.

The following formula is given by Kendall and Stuart [23].

F(Px) = f + & [ Pr’ * 44-O ; e-ip.r’ . 4%(0 dt

From Equation 3.5 we have the following.

=

++k

I [

Ox ; +F(-r) . +u(xt) - +FO) . Wij dt

(A. 1)

Thus we have the following.

Yw(x) =

I

,,; (v - x)dS(v) =

= 1; [ j-,= dWv)] du = 1; (1 - B(u)@

=

Jz (1 - B(v))dv - I’ (1 - S(v))dv

0

0

56

AGGREGATE DISTRIBUTIONS

$F( - t) * &/(vt) - c/%(t) * +U(-vf)

it

Mt) [ &A- VOdv] dt

Note: $(r) = f(t)e”“‘; At) =A-t) and g(-t) =

-g(t).

Case1 U(p)=Oforp<landU(P)= lforprl.

+u(t)

= err

+u(xt) = e’I’

+o(-xt) = e-“’

64.2)

(A.3)

(A.4)

I

ox +u(vt)dv = =

it

(A.5)

I

; +u( -vt)dv = ’ -,‘-lX’

(A.61

,

Equation 6.5 is obtained by substituting Equations A.3 and A.4 into Equation

A. 1. and replacing t with t/a. Equation 6.6 is obtained by substituting Equations

A.5 and A.6 into A.2 and replacing t with tla.

We first show that U(p) satisfies the conditions stated for Algorithm 3.3.

i

I

=-

rir) 0 (+)

‘- ‘em@@

=

1

AGGREGATE

DISTRIBUTIONS

r

I

x

r

=-

r - 1 r(r - 1) o

(rp)‘-2e-‘Pd@

r

=-

r- 1

If r = 1 + lib we have that Var (l/p) = (r/(r - 1)) - 1 = 6.

57

[( y-L II

I -

I

,,’ cjju(-vt)dv = ; [I - (I + :)-‘I

(A.91

(A. 10)

Equation 6.7 is obtained by substituting Equations A.7 and A.8 into Equation

A. 1 and replacing t with t/u. Equation 6.8 is obtained by substituting Equations

A.9 and A.10 into A.2 and replacing t with r/a.

58

AGGREGATE DISTRIBUTIONS

APPENDIX B

ASYMPTOTIC BEHAVIOR OFJI)

In the error analysis of Section 8 we indicated that max,z, f(r) could be

significantly less than one for large a. We now give a demonstration of this

fact. It will be sufficient to consider a single coverage or class of business.

We will adopt the following notation for use in this appendix.

D=l-iPa

k-l

A = a,,+,

As t + 30, we have the following.

h(t) + D cos (At)

k(t) --;, D sin (At)

+~(t) + D(cos (At) + i sin (At))

Case I Binomial Distribution

OF(f) = [1 + p f&(C) - 1)l”’

As t + ~0, we have the following.

At> + [(l - p + D p cos (At))’ + (D p sin (Af))2]““2

f(t) + [( 1 - p)’ + 2 D p cos (At) + (D p)2]‘n’2

If D = O,f(t) + (1 - p)“’ which is equal to the probability of having no claims.

If D > 0,flt) does not approach a limit, but the asymptotic upper bound off(r)

can be obtained by setting cos (At) = 1.

max,,, f(t) + [( 1 - p)’ + 2 D p + (D P)~]““~

As an example, consider the case when m = 100, p = .l and D = .I :

max j(t) + .0000905.

12”

AGGREGATE DISTRIBUTIONS

59

Case 2 Poisson Distribution

+&) = e

h(+sw - I)

As t + m,At) + emA * eW ‘OS (A’). If D = O,flt) + emA, which is equal to the

probability of having no claims. If D > 0, f(t) does not approach a limit, but

the asymptotic upper bound off(t) can be obtained by setting cos (At) = 1.

max f(t) + e-‘(‘+)

12=(1

As an example, consider the case when A = 10 and D = .I:

max fit) + ep9 = .0001234.

fZCl

Case 3 Negative Binomial Distribution

W) = [I - cA(+s(o - 111

--I/c

As t --+ w, we have the following.

fit) + [(I + CA + CA D cos (At))2 + (CA D sin (At))2]-“2c

At) ---, [(l + cA)~ + 2(1 + CA) 1 CA D cos (At) + (CA D)‘]-I”’

If D = 0, f(t) --j (1 + CA)-“‘,

which is the probability of having no claims. If

D > 0, f(t) does not approach a limit, but the asymptotic upper bound of f(t)

can be obtained by setting cos (At) = 1.

max fit) + [(I + cA)~ - 2( 1 + cA)(cAD) + (cAD)~]-“~“

,Z=O

As an, example, consider the case when A = 10, D = .I and c = .I :

maxflt) * .001631.

G=cI

60

AGGREGATE DlSTRIBUTTONS

NOTES AND REFERENCES

[l] Paul Dorweiler, “On Graduating Excess Pure Premium Ratios,” PCAS

XXVIII, 1941, p. 132.

[2] Nels M. Valerius, “Risk Distributions Underlying Insurance Charges in

the Retrospective Rating Plan,” PCAS XXIX, 1942, p. 96.

[3] LeRoy J. Simon, “The 1965 Table M,” PCAS LII, 1965, p. 1.

[4] Charles C. Hewitt, Jr., “Loss Ratio Distributions- A Model,” PCAS LIV,

1967, p. 70.

[5] Charles A. Hachemeister, “A Stochastic Model For Loss Reserving,”

Transactions of the 21st International Congress of Actuaries, Vol. 1980,

p. 185.

[6] Insurance Services Office, Report of the increased Limits Subcommittee:

A Review of Increased Limits Ratemaking, Insurance Services Office,

1980, p. 72.

[7] R. E. Beard, T. Pentiklinen, and E. Pesonen, Risk Theory, 2nd Edition,

Chapman and Hall, 1977, p. 43.

[8] Gary Venter, “Transformed Beta and Gamma Distributions and Aggregate

Losses,” Pricing, Underwriting, and Managing the Large Risk, Casualty

Actuarial Society 1982 Discussion Paper Program, p. 395. See also PCAS

LXX, (1983).

[9] Glenn Meyers, “An Analysis of Retrospective Rating,” PCAS LXVII,

1980, p. 110.

[lo] Shaw Mong, “Estimating Aggregate Loss Probability and Increased Limit

Factor,” Pricing Property and Casualty Insurance Products, Casualty Ac-

tuarial Society 1980 Discussion Paper Program, p. 358.

[ 1 I] Ethan Stroh, “Actuarial Note: The Distribution Functions of Collective

Risk Theory as Linear Compounds,” Actuarial Research Clearing House,

1978.1.

[12] James Tilley, Discussion of Harry Panjer, “The Aggregate Claim Distri-

bution and Stop-Loss Reinsurance,” TSA XxX11, 1980, p. 538.

[13] Harry Panjer, “Recursive Evaluation of a Family of Compound Distribu-

tions,” ASTIN Bulletin, Vol. 12, No. 1, 198 1, p. 22.

AGGREGATE DISTRIBUTIONS

61

[14] Glenn Meyers and Nathaniel Schenker,

“Parameter Uncertainty in the

Collective Risk Model,” Pricing, Underwriting, and Managing the Large

Risk, Casualty Actuarial Society 1982 Discussion Paper Program, p. 253.

See also PCAS LXX, (1983).

[15] Philip Heckman and Phillip Norton,

“Optimization of Excess Portfolios,”

Pricing, Underwriting, and Managing the Large Risk, Casualty Actuarial

Society 1982 Discussion Paper Program, p. 113.

[16] Beard et al., op. cit., p. 18

[17] Ibid., p. 110.

[I81 Ibid., p. 126.

[19] Insurance Services Office, op. cit., p. 46.

[20] Gary Patrik, “Estimating Casualty Insurance Loss Amount Distributions,”

PCAS LXVII, 1980, p. 57.

[21] National Council on Compensation Insurance, Retrospective Rating

Plan D.

[22] For a discussion of the overlap problem, see Meyers op. cit.

1231 Maurice Kendall and Alan Stuart, The Advanced Theory of Statistics, Vol.

I, 4th Edition, Macmillan, 1977, p. 98.

- . .

- -. _

- -- -.- - __.

NOTE

The exhibits associated with the paper “The Calculation of Aggre-

gate

LOSS

Distributions from Claim Severity and Claim Count Dis-

tributions” by Philip E. Heckman and Glenn G. Meyers (PCAS

LXX, 1983) appear in the subsequent volume of the Proceedings

(PCAS LXXI, 1984).