Membership Information

for the

2024 Million Dollar Round Table

Requirements for the U.S. and

Select Markets

Based on 2023 production

Million Dollar Round Table

325 West Touhy Avenue, Park Ridge, Illinois USA Phone: +847.692.6378 | Fax: +1 847.518.8921 |

Email: [email protected]

Page 2

Non-Core – 11/3/2022

Apply for 2024 membership online at

https://www.mdrt.org/membership-application/

PLEASE NOTE

This document presents the membership requirements for the following Markets:

Australia, Belgium, Canada, Gibraltar, Ireland, Isle of Man, Israel, Italy, New Zealand,

South Africa, United Kingdom and United States. If you need requirements for other

Markets, please return to the MDRT web site and select the GLOBAL version.

Please discard any copies of this document that do not have the mark of

“Non-Core – 11/3/2022” at the foot of each page.

• The Market specific production requirements are listed on pages 3 and 11-16.

Table of Contents

Page

I. Production Requirements-------------------------------------------------------------------- 3

II. Eligibility ------------------------------------------------------------------------------------------ 4

III. Reporting ----------------------------------------------------------------------------------------- 5

IV. Additional Requirements -------------------------------------------------------------------- 6

V. Clarifications ------------------------------------------------------------------------------------- 7

VI. Illustrations -------------------------------------------------------------------------------------- 9

VII. Meetings ----------------------------------------------------------------------------------------- 10

VIII. Commission/Premium Production Requirements By Market ------------------- 11

IX. Income Production Requirements By Market ---------------------------------------- 14

Page 3

Non-Core – 11/3/2022

Elimination of the Risk-Protection/Core

Credit Requirement

MDRT has eliminated the requirement that a

minimum of 50 percent of an applicant’s

qualifying production come from Risk-Protection

Credit or “core products.” Applicants from the

Markets below will be able to qualify using any

MDRT eligible product in any combination or

proportion.

PLEASE NOTE

Applicants may not combine production credit from the methods above to attain the minimum

requirement. Applicants will be approved only under one method.

The 2024 production requirements for applicants outside the United States are expressed in local currency

in the tables at the end of this document. All commission, premium or income credit reported must be

converted to U.S. dollars using the MDRT conversion factor listed at the end of this document.

MEMBERSHIP INFORMATION FOR THE

2024 MILLION DOLLAR ROUND TABLE

I.

PRODUCTION REQUIREMENTS

1.

Production Methods

Membership in the 2024 Round Table will be based on the

following production methods: (See page 4 for products)

• Commission/Fee Method

A minimum of USD 74,000 of eligible commissions paid is

required.

• Premium Method

A minimum of USD 148,000 of eligible paid premium

is required.

• Income Qualification Method

A minimum of USD 128,200 in annual gross income

from the sale and service of insurance and financial

products is required. A minimum of USD 37,000 must

be income from new business generated during the

production year.

2.

Court of the Table

• Commission & Premium Method

A minimum of USD 222,000 of eligible commissions paid or

USD 444,000 of eligible paid premium is required.

• Income Method

A minimum of USD 384,600 of eligible annual gross income is

required. The applicant must meet the minimum of USD

37,000 in new business.

Top of the Table

• Commission & Premium Method

A minimum of USD 444,000 of eligible commissions paid

or USD 888,000 of eligible paid premium.

• Income Method

A minimum of USD 769,200 of eligible annual gross income

is required. The applicant must meet the minimum of USD

37,000 in new business.

• Top of the Table Waivers

Top of the Table members with a minimum of 10 years of

Top of the Table membership who do not meet the required

minimum production level may apply under the Top of the

Table waiver provision, but must submit required Top of the

Table dues.

Australia

Ireland

New Zealand

Belgium

Isle of Man

South Africa

Canada

Israel

United Kingdom

Gibraltar

Italy

United States

Page 4

Non-Core – 11/3/2022

3.

Eligible Products and Credit

RISK-PROTECTION PRODUCTS

Products from life insurance companies

Commission/Fee Credit

Premium Credit

Accidental death and dismemberment (individual)

100% of first year commission

100% of first year premium

Critical illness (individual)

100% of first year commission

100% of first year premium

Disability income contracts (individual)

100% of first year commission

100% of first year premium

Life (individual)

Up to annual premium/target premium

100% of first year commission

100% of first year premium

Deposits in excess of annual/target

premium/top up

100% of commission paid

6% of excess premium

Single premium (whole life and investment)

100% of first year commission

6% of first year premium

Short-term endowment rider (max 15 yrs.)

100% of first year commission

6% of first year premium

Long-term care (individual)

100% of first year commission

100% of first year premium

Accidental death and dismemberment (group)

100% of first year commission

10% of first year premium

Critical illness (group)

100% of first year commission

10% of first year premium

Disability income contracts (group)

100% of first year commission

10% of first year premium

Life (group)

100% of first year commission

10% of first year premium

Long-term care (group)

100% of first year commission

10% of first year premium

Annuities (individual and group)

100% of all commissions

6% of new money invested

Single premium and/or short-term endowment (max

15 yrs.)

100% of first year commission

6% of first year premium

OTHER PRODUCTS

Products

Commission/Fee Credit

Premium Credit

Health care (individual)

100% of first year commission

100% of first year premium

Health care (group)

100% of first year commission

10% of first year premium

Mutual funds

100% of all commissions/fee

6% of new money invested

Securities

100% of commission/fee on new

money invested

6% of new money invested

Wrap accounts/asset management accounts

100% of all commissions/fee

6% of new money invested

Financial Planning Fees/Fees for Advice

100% of the net fee

100% of the gross fee

II.

ELIGIBILITY

1.

Qualification Overview

• First-time applicants for MDRT must use either the

commission or premium methods to demonstrate

qualification for membership. (See chart on page 5.)

• Any individual with prior MDRT membership is eligible to

apply using the income qualification method.

2.

MDRT Status Designations

Each MDRT status designation is granted for one year only. All

members must apply every year to continue their affiliation with

MDRT.

• Qualifying Member

An individual who is a first-time applicant becomes a

Qualifying (Q) member when his/her application papers are

approved. Until the 10

th

year of membership is attained, the

member will be a Qualifying member.

• Qualifying And Life Member

An individual becomes a Qualifying and Life (QL) member

when approved for the 10

th

year of membership. Qualifying and

Life status is maintained in future years by submitting an

application each year, including certifying letter(s)

demonstrating qualifying production or by attesting to having

met current minimum production levels, and by paying the

required dues.

• Life Member

After Qualifying and Life membership has been attained,

Applicants for Life status will declare that they did not meet

the production requirement, but still wish to continue their

MDRT membership. Life members must annually submit an

application and pay dues.

Page 5

Non-Core – 11/3/2022

Member

Type

COMMISSION

Member

Type

PREMIUM

MDRT

COT

TOT

MDRT

COT

TOT

Total

Total

Total

Total

Total

Total

Production

$74,000

$222,000

$444,000

Production

$148,000

$444,000

$888,000

1st-Time

Member

1st-Time

Member

Certifying

letters

Required

Required

Required

Certifying

letters

Required

Required

Required

Signed by

Company

Company

Company

Signed by

Company

Company

Company

2 - 10 Year

Member

2 - 10 Year

Member

Certifying

letters

Required

Required

Required

Certifying

letters

Required

Required

Required

Signed by

Company

Company

Company

Signed by

Company

Company

Company

11+ Year

Member

11+ Year

Member

Certifying

letters

Not Required

Required if less

Required if less

Certifying

letters

Not Required

Required if less

Required if less

than 10 COT

than 10 TOT

than 10 COT

than 10 TOT

Signed by

Not Required

Company

Company

Signed by

Not Required

Company

Company

Member

Type

INCOME

MDRT

COT

TOT

New Business

Total

New Business

Total

New Business

Total

Production

$37,000

$128,200

$37,000

$384,600

$37,000

$769,200

1st-Time

Member

Not Eligible

Not Eligible

Not Eligible

Certifying

letters

Signed by

2 - 10 Year

Member

Certifying

letters

Required

Required

Required

Signed by

Self-signed

Self-signed

Self-signed

11+ Year

Member

Certifying

letters

Not Required

Required if less than 10 COT

Required if less than 10 TOT

Signed by

Not Required

Self-signed

Self-signed

III.

REPORTING

1.

Verifying Production

• Commission And Premium Verification

First-time applicants must apply using ONLY the

commission or premium methods and supply a certifying

letter(s) with third party verification. Those applying for

Qualifying membership (years two through 10) may submit

the customary certifying letters with third party verification

for commission or premium or submit a self-signed certifying

letter and attach supporting documents for the income

qualification method as outlined above. Certifying letters

may be completed by a representative of the company/broker

dealer/brokerage agency, a Certified Public Accountant (or

equivalent), or a representative of the applicant's personal

agency/corporation or office.

• Income Verification

Verification of eligible production under the income

qualification method will be accomplished via a certifying

letter signed by the applicant. All applications submitted

under the income method are subject to a random

production verification audit at a later date. If selected, the

individual will need to supply supporting documents, such

as commission statements, that verify the amounts claimed.

Other acceptable supporting documents would be a

statement of income signed by a representative of the

company/broker dealer/brokerage agency, a Certified Public

Accountant (or equivalent), or a representative of the

applicant’s personal agency/corporation/office. Tax

documents may also be used.

Page 6

Non-Core – 11/3/2022

• Simplified Reporting for Qualifying & Life and Life

Members

Once eligibility for Life status has been attained, members

who have achieved Qualifying and Life or Life status are

eligible to submit an application each year, including

certifying letter(s) demonstrating qualifying production or

by attesting to having met current minimum production

levels, and by paying the required dues. Proof of production

(i.e. certifying letters or commission/income documents)

will not be required beginning in the eleventh year.

Applicants for Life status will declare that they did not meet

the production requirement, but still wish to continue their

MDRT membership.

2.

Court of the Table

•

Applicants must continue to submit proof of production via

certifying letter(s) until achieving 10 years of membership

at the higher level. They may declare their eligibility

without certifying letters or income documents when

applying for the eleventh year of membership at Court of

the Table level.

3.

Top of the Table

• Applicants must continue to submit proof of production via

certifying letter(s) until achieving 10 years of membership

at the higher level. They may declare their eligibility

without certifying letters or income documents when

applying for the eleventh year of membership at Top of the

Table level.

4.

Application Forms

•

Applications for 2024 MDRT membership will be available on

November 1, 2023. Applicants may complete an online

application or download a paper application at www.mdrt.org.

A paper application may also be requested by phone, fax or

email at [email protected]rg.

5.

Certifying Letters

•

A certifying letter signed by an official from the company an

applicant is using for MDRT qualification is required when

applying under the commission or premium method.

Otherwise, the application will be considered incomplete and

membership may be denied. These companies may include

life insurance companies, agencies, brokerage companies,

broker/dealers, banks or mutual fund companies. Also

acceptable would be a certifying letter completed by a

representative of the company/broker dealer/brokerage

agency, a Certified Public Accountant (or equivalent), or a

representative of the applicant's personal

agency/corporation or office.

•

A Certified Public Accountant (CPA) or the equivalent may

sign certifying letters for financial planning fees/fees for

advice that are paid directly to the producer when applying

under the commission or premium method.

•

Brokerage companies are defined as third party wholesalers

of insurance and investment products that are provided to

agents on behalf of insurance and investment companies.

Should an applicant be an official of a brokerage company,

the product provider who pays the commissions must sign

the certifying letter unless applying under the income

qualification method.

•

Income certifying letters are self-reported, signed by the

applicant. If selected for a production verification audit, the

individual will need to supply supporting documents to

verify the amounts claimed, such as:

−

commission statements

−

a statement of income signed by a representative of the

company/broker dealer/ brokerage agency, a Certified

Public Accountant (or equivalent), or a representative

of the applicant’s personal agency/corporation/office

−

Tax documents

6.

Honor Roll

Individuals with at least 15 years of qualifying membership

(qualification by production) shall be designated as

members of the “Honor Roll.”

IV.

ADDITIONAL REQUIREMENTS

1.

Professional Association Membership Requirement

•

When applying for MDRT membership, applicants from the

Markets listed below must be members in good standing of

an association that meets all of the criteria below. (A list of

associations that meet the criteria may be found on our web

site at https://www.mdrt.org/join/member-requirements/).

•

The association must be an individual membership

organization, open to participation without regard to

company affiliation, one of the focuses of which is insurance

or financial services.

−

The association must have been in existence at least two

years and must have 100 or more members.

−

The association must be a nonprofit organization.

−

The association must have a code of ethics and an

effective means of dealing with breaches of its code.

•

Applicants using a disability waiver, as well as members with

50 or more years of membership, are exempt from the

professional association requirement.

•

Membership in an association is required of applicants from

the following Markets:

Australia

Ireland

Philippines

Bahamas

Israel

Singapore

Canada

Jamaica

Thailand

Greece

Japan

Trinidad & Tobago

Hong Kong,

Malaysia

United States

China

New Zealand

2.

Annual Membership Dues: USD 600

•

Required dues, completed application and other required

forms must be postmarked on or before March 1, 2024.

Applications postmarked after March 1 will be considered

only if accompanied by an additional fee of USD 200.

•

Members with 50 or more years of membership are exempt

from the MDRT-level dues. They must, however, pay Court

or Top of the Table dues.

3.

Court of the Table Dues: USD 50

•

In addition to remitting regular MDRT dues, a Court of the

Table applicant must remit the required Court of the Table

dues.

Page 7

Non-Core – 11/3/2022

4.

Top of the Table Dues: USD 550

•

In addition to remitting regular MDRT membership dues, a

Top of the Table applicant must remit the required Top of the

Table dues. Top of the Table membership dues includes Court

of the Table dues.

5.

Life, Reduced Dues: USD 200

•

Life members who meet all four of the criteria below are

eligible to pay a reduced dues amount. Those eligible for

reduced dues are not required to be members of a professional

association.

−

a Life or a Qualifying & Life member, and

−

applying as a Life member, and

−

65 years of age by December 31, 2023 and

−

have either 25 years of membership OR 20 years of

membership with production

Online payment options are available. For more information,

please refer to your 2024 Membership application.

6.

Disability Waiver

•

Life members who have been declared totally disabled for six

consecutive months during 2023 may petition for a waiver of

payment of dues for the 2024 Table. A disability petition

form and doctor’s statement must be submitted by March 1,

2024, with the membership application. Each petition will be

judged on its own merit. Those approved for the disability

waiver are not required to be members of a professional

association.

7.

Former Life Member Options

•

Former Life and Qualifying & Life members who wish to

rejoin MDRT have two options:

•

Option One: They may choose not to pay back dues for the

years missed and submit the current minimum production

and current membership dues with their application. Their

member status will revert to Qualifying and they must again

fulfill the requirements to attain Life or Qualifying & Life

status, which includes accumulating an additional 9 years of

Qualifying membership.

•

Option Two: They may retain Life or Qualifying & Life

member status by paying back dues for the number of years

missed, not to exceed a maximum of five years, and by

meeting the then current requirements for Life membership.

The maximum number of years for which back dues may be

required will be reduced to three years if the member submits

qualifying production for the current year. The amount of

back dues will be based upon the current dues at the time of

reinstatement. Please note: Payment of back dues does not

provide credit for member year(s) missed.

V.

CLARIFICATIONS

1.

Eligible Commissions, Fees

Production credit (for commissions) will be based on eligible

commissions received during 2023. Credit may include either

earned or advanced (annualized) commissions or both. Advanced

(annualized) or earned commissions must be paid to the applicant

in 2023 to be eligible for MDRT credit. Please note:

•

Commissions paid on a levelized basis may be reported using

the present value of up to the first five years’ commission

discounted at 10 percent per year, not to exceed 55 percent of

first-year premium.

•

Annualized commissions may be reported for credit if paid,

but any chargeback of annualized commissions in a

subsequent production year will result in a reduction of that

year’s production credit.

•

If commissions are paid as earned, a policy effective in 2022

may result in production credit for 2023. The policy must be

in force on December 31, 2022 but is not required to be in

force as of December 31, 2023.

•

Commission credit for pensions is based on the product used

to fund the pension (life insurance, annuities, mutual funds,

etc.) which determines whether it receives Risk-Protection or

Other Products credit.

•

Commissions that are part of a deferred compensation

program may be claimed up front for MDRT credit, provided

that they are not claimed again in later years.

•

Life insurance policies that exceed the annual premium or

target premium are eligible for credit. First year commission

credit may be given Risk-Protection category for the

commission paid on the amount up to the annual/target

premium. If the annual/target premium is exceeded,

(sometimes referred to as a “top up”) commission credit may

be given in the Risk-Protection category for the commission

paid on the amount that exceeded the annual/target premium.

•

Override commissions, training allowances, transition

packages, training or sign-on bonuses and other sales or

expense allowances do NOT qualify under the

commission/premium method.

•

Fees paid for the placement of a product are eligible for

credit toward the commission requirement, as are asset

management fees for mutual funds and wrap/asset

management accounts. The type of product placed

determines the type of credit the product receives (Risk-

Protection or Other).

•

Financial Planning Fees/Fees for Advice are eligible for

Other Products credit for the net fee paid to the agent/advisor.

Fees must be documented by certifying letter signed by a

company official, a broker dealer official, or a Certified

Public Accountant (or equivalent) for qualifying members.

•

Group health insurance commissions are eligible in the first

year of the policy only. Additions to the group policy in

subsequent years are not eligible for credit.

•

Single premium and/or short-term endowment commissions

are only eligible in the first year of the policy. Short-term

endowment riders (max 15 years) to life insurance policies

are eligible for 100 percent of first-year commissions in the

Risk-Protection category.

•

Long-term endowment commissions are only eligible in the

first year of the policy. Long-term endowment riders (16 or

more years) to life insurance policies are eligible for 100

percent of first-year commissions in the Risk-Protection

category.

For additional information, contact:

Million Dollar Round Table

Member Relations Department

325 West Touhy Avenue

Park Ridge, IL 60068 USA

Phone: +1 847.692.6378

Fax: +1 847.518.8921

Web site: https://www.mdrt.org

E-mail: memberrelations@mdrt.org

Page 8

Non-Core – 11/3/2022

2.

Eligible Premium

Production credit (for premium) will be based on eligible

premium paid or new money invested during 2023. Please note:

•

If commissions are paid as earned, premium credit should be

given only for the amount of premium actually received

during the production year.

•

If commissions are annualized, the premium credit should

also be annualized. Any chargeback of annualized

commissions should also result in a reduction of that year's

premium credit.

•

A policy that becomes effective in 2022 may result in

production credit for the amount of premium paid or new

money invested during 2023.

•

Life insurance policies that exceed the annual premium or

target premium are eligible for credit. First year premium

credit may be given in the Risk-Protection category up to

the amount of the annual/target premium. If the

annual/target premium is exceeded, (sometimes referred to

as a “top up”) premium credit may be given in the Risk-

Protection category for 6 percent of the amount that

exceeded the annual/target premium.

•

Financial Planning Fees/Fees for Advice are eligible for

Other Products credit for the gross fee paid to the company,

broker dealer or individual agent/advisor. Fees must be

documented by certifying letter signed by a company

official, a broker dealer official, or a Certified Public

Accountant (or equivalent) for qualifying members.

•

Group health insurance premium is eligible for credit in the

first year of the policy only. Additions to the group policy in

subsequent years are not eligible for credit.

•

Single premium and/or short-term endowment premium is

only eligible in the first year of the policy. Short-term

endowment riders (max 15 years) to life insurance policies

are eligible for 6 percent of first year premium credit.

•

Long-term endowment premium is only eligible in the first

year of the policy. Long-term endowment riders (16 or more

years) to life insurance policies are eligible for 100 percent

of first-year premium credit in the Risk-Protection category.

•

Premium credit for pensions is based on the product used to

fund the pension (life insurance, annuities, mutual funds,

etc.) which determines whether it receives Risk-Protection

or Other Products credit.

3.

Eligible Income

Production credit is based on annual gross income paid during

2023. Please note:

•

See chart on page 4 for eligible products.

•

Under this model, income is defined as first-year, trail and

renewal commissions, as well as fees for product

placement, asset management fees and fees for advice.

•

Other production-based compensation, such as salaries and

production-based bonuses, are also eligible for credit.

•

Income contributed as part of a deferred compensation plan

is eligible for credit. Credit should be taken during the

production year when the deferred income was earned.

•

Override commissions are eligible only for personal

production.

•

Income considered INELIGIBLE for MDRT credit

includes:

−

Training bonuses/allowances

−

Sales/expense allowances

−

Sign-on bonuses or transition packages

−

Overrides derived from the production of others

−

Non-cash compensation, such as incentive trips

−

Income from property and casualty insurance and

general insurance (fire, home, auto, etc.)

−

Income from the sale of mortgages

−

Life settlements

−

Money market accounts

4.

Credit for Coverage Written on the Applicant, Spouse

or Dependents

•

Any business written on the applicant, applicant’s spouse

or dependents may not exceed a maximum of 5 percent

of the current year's MDRT production requirement

(USD 3,700 eligible commissions or USD 7,400 of

eligible premium or USD 6,410 of eligible income) if any

of the premiums are paid, directly or indirectly, by the

applicant or spouse.

5.

Replacements

•

Credit for individual life insurance policies may be

claimed only for the amount of first-year commissions or

premium on the new policy that exceeds the first-year

commissions or premium for the policy being replaced. If

the amount is not known, then the amount of

commissions being replaced shall be calculated by

multiplying the current commission times the appropriate

premium for the policy being replaced. Premium credit

can be determined by subtracting the replaced premium

from the new premium.

•

Conversion of a permanent product to a permanent

product is to be treated as a replacement for MDRT

purposes. This applies only to replacement of individual

life insurance policies.

6.

Definitions And Interpretations

•

Business Paid for and Underwritten

Business to be credited shall be paid for during the MDRT

qualification period (January 1 through December 31).

Business shall be considered to have been paid for as of the

date when the coverage first became fully effective with

home office approval from the standpoint of payment of the

claim (regardless of company practice or the distance

between home and field office). However, no credit shall be

allowed until the home office has finally accepted the

premium and also until the first-year commissions have been

paid or credited to the agent's account without any right

reserved to the insurance company to recover same, except in

case of recall under the contestable provisions of the contract.

On joint, partnership, corporate and/or brokerage business,

MDRT credit shall be given for only that portion of the

business on which the applicant has been compensated, either

by first-year commission or the equivalent.

•

Health Insurance

Includes policies that relate to the health of the body. Dental,

vision, etc., are eligible for credit. See page 4 for specifics.

Page 9

Non-Core – 11/3/2022

Clarification of Income Qualification

•

A minimum of USD 128,200 in annual gross income from the sale

or service of insurance and financial products is required.

•

A minimum of USD 37,000 must be income from new business

generated during the production year.

ELIGIBLE for MDRT membership

Example 1

Applicant annual gross income 128,200

Applicant total new business 37,000

NOT Eligible for MDRT membership

Example 2

Applicant annual gross income 128,200

Applicant total new business 36,999

6. Definitions and Interpretations (Cont’d)

•

Policy and Case Definitions

A policy shall be defined as an individual contract covering

one or more lives as contrasted with a group policy, a

pension, profit sharing trust or a salary savings plan. Under a

qualified pension or profit-sharing trust or a salary savings

plan, each individual policy shall count as one (1) policy for

the purpose of computing total eligible policies. For purposes

of production, an employer-sponsored group life plan,

franchise life plan and group annuity plan and mutual fund

transaction with one (1) investor shall be considered one (1)

case regardless of the number of lives or funds involved.

•

In Force Requirement

Credited business shall include only business which has not

been terminated on or before the last day of the MDRT

qualification period (December 31) except for business

terminated by death or term conversion.

•

Securities

Includes stocks, bonds or other equities. See page 4 for

specifics.

VI.

ILLUSTRATION

Page 10

Non-Core – 11/3/2022

*Attendance at the MDRT Annual Meeting and

MDRT Global Conference is open to approved

2024 members and requires payment of

separate registration fees.

**Attendance at the Top of the Table Annual

Meeting is open to approved 2024 TOT

members and requires payment of separate

registration fees.

***MDRT EDGE Meeting is open to approved

2024 members from the U.S. and Canada and

requires payment of separate registration fees.

MDRT Annual Meeting*

9 – 12 June 2024

Vancouver, British Columbia, Canada

MDRT Global Conference*

2024

TBA

Top of the Table Annual Meeting**

25 –28 September 2024

Fairmont Orchid, Hawaii, USA

MDRT EDGE Meeting***

2024

TBA

Visit www.mdrt.org or contact MDRT at +1 847.692.6378 or email [email protected]g

for meeting information or for exhibitor and sponsorship opportunities.

Page 11

Non-Core – 11/3/2022

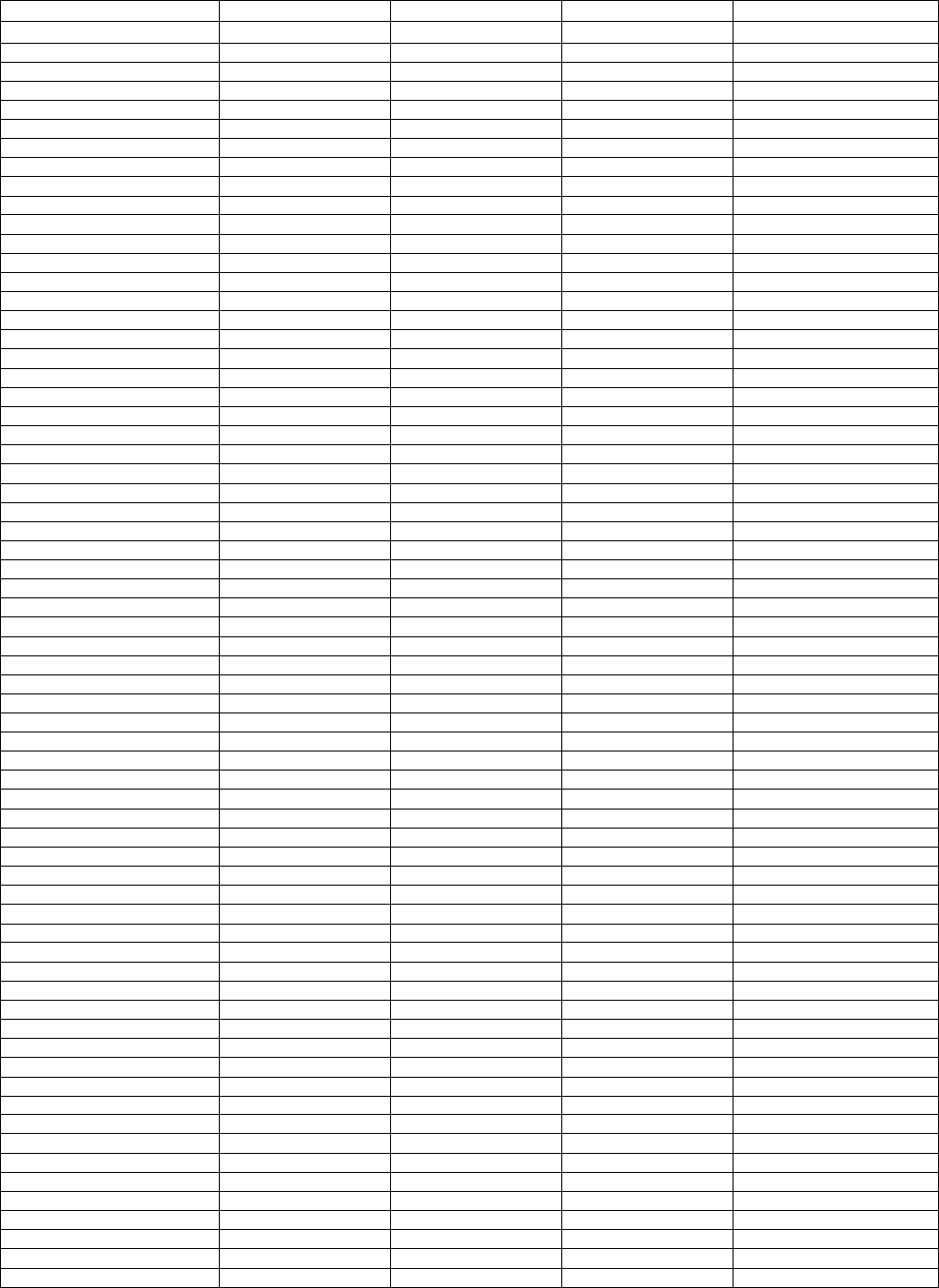

COMMISSION AND PREMIUM PRODUCTION REQUIREMENTS FOR MEMBERSHIP

IN THE 2024 MILLION DOLLAR ROUND TABLE

Based on 2023 Production, Expressed in Local Currency

Production credit must be reported in U.S. dollars on Certifying Letters

(Local currency divided by the conversion/standardization factor = MDRT requirement in U.S. dollars)

Production requirements are set independently for each Market. Conversion/standardization factors have no relationship to

currency exchange rates and are used only to standardize MDRT processing.

(For a complete list of Market requirements, see the MDRT web site at https://www.mdrt.org/join/member-requirements/.)

Market

MDRT

Commission

COT

Commission

TOT

Commission

Commission

Conv Factor

MDRT

Premium

COT Premium

TOT

Premium

Premium

Conv Factor

Angola

43,800

131,400

262,800

0.5918

87,600

262,800

525,600

0.5918

Anguilla

84,800

254,400

508,800

1.1459

169,600

508,800

1,017,600

1.1459

Antigua

132,900

398,700

797,400

1.7959

265,800

797,400

1,594,800

1.7959

Argentina

280,000

840,000

1,680,000

3.7837

560,000

1,680,000

3,360,000

3.7837

Armenia

11,540,900

34,622,700

69,245,400

155.9581

23,081,800

69,245,400

138,490,800

155.9581

Aruba

88,700

266,100

532,200

1.1986

177,400

532,200

1,064,400

1.1986

Australia

107,700

323,100

646,200

1.4554

215,400

646,200

1,292,400

1.4554

Azerbaijan

23,100

69,300

138,600

0.3121

46,200

138,600

277,200

0.3121

Bahamas

63,300

189,900

379,800

0.8554

126,600

379,800

759,600

0.8554

Bahrain

14,300

42,900

85,800

0.1932

28,600

85,800

171,600

0.1932

Bangladesh

1,943,000

5,829,000

11,658,000

26.2567

3,886,000

11,658,000

23,316,000

26.2567

Barbados

110,100

330,300

660,600

1.4878

220,200

660,600

1,321,200

1.4878

Belarus

87,534,300

262,602,900

525,205,800

1,182.8959

175,068,600

525,205,800

1,050,411,600

1,182.8959

Belgium

55,600

166,800

333,600

0.7513

111,200

333,600

667,200

0.7513

Belize

79,600

238,800

477,600

1.0756

159,200

477,600

955,200

1.0756

Bermuda

104,800

314,400

628,800

1.4162

209,600

628,800

1,257,600

1.4162

Bolivia

195,600

586,800

1,173,600

2.6432

391,200

1,173,600

2,347,200

2.6432

Bosnia-Herzegovina

50,000

150,000

300,000

0.6756

100,000

300,000

600,000

0.6756

Botswana

250,500

751,500

1,503,000

3.3851

501,000

1,503,000

3,006,000

3.3851

Brazil

166,400

499,200

998,400

2.2486

499,200

1,497,600

2,995,200

3.3729

British Virgin Islands

75,200

225,600

451,200

1.0162

150,400

451,200

902,400

1.0162

Brunei

46,200

138,600

277,200

0.6243

138,600

415,800

831,600

0.9364

Bulgaria

51,900

155,700

311,400

0.7013

103,800

311,400

622,800

0.7013

Cambodia

76,011,700

228,035,100

456,070,200

1,027.1851

304,046,800

912,140,400

1,824,280,800

2,054.3702

Cameroon

16,915,600

50,746,800

101,493,600

228.5891

33,831,200

101,493,600

202,987,200

228.5891

Canada

91,000

273,000

546,000

1.2297

182,000

546,000

1,092,000

1.2297

Cayman Islands

61,300

183,900

367,800

0.8283

122,600

367,800

735,600

0.8283

Channel Islands

51,500

154,500

309,000

0.6959

103,000

309,000

618,000

0.6959

Chile

29,259,100

87,777,300

175,554,600

395.3932

58,518,200

175,554,600

351,109,200

395.3932

China

218,400

655,200

1,310,400

2.9513

655,200

1,965,600

3,931,200

4.4270

Colombia

79,657,900

238,973,700

477,947,400

1,076.4581

159,315,800

477,947,400

955,894,800

1,076.4581

Costa Rica

24,273,100

72,819,300

145,638,600

328.0148

48,546,200

145,638,600

291,277,200

328.0148

Côte d'Ivoire

18,036,400

54,109,200

108,218,400

243.7351

36,072,800

108,218,400

216,436,800

243.7351

Croatia

242,800

728,400

1,456,800

3.2810

485,600

1,456,800

2,913,600

3.2810

Curacao

66,900

200,700

401,400

0.9040

133,800

401,400

802,800

0.9040

Cyprus

37,200

111,600

223,200

0.5027

74,400

223,200

446,400

0.5027

Czech Republic

938,000

2,814,000

5,628,000

12.6756

1,876,000

5,628,000

11,256,000

12.6756

Denmark

493,800

1,481,400

2,962,800

6.6729

987,600

2,962,800

5,925,600

6.6729

Dominica

118,300

354,900

709,800

1.5986

236,600

709,800

1,419,600

1.5986

Dominican Republic

1,227,300

3,681,900

7,363,800

16.5851

2,454,600

7,363,800

14,727,600

16.5851

Ecuador

38,300

114,900

229,800

0.5175

76,600

229,800

459,600

0.5175

Egypt

153,800

461,400

922,800

2.0783

461,400

1,384,200

2,768,400

3.1175

El Salvador

33,600

100,800

201,600

0.4540

67,200

201,600

403,200

0.4540

Estonia

40,300

120,900

241,800

0.5445

80,600

241,800

483,600

0.5445

Fiji

60,800

182,400

364,800

0.8216

121,600

364,800

729,600

0.8216

France

54,100

162,300

324,600

0.7310

108,200

324,600

649,200

0.7310

Georgia

62,700

188,100

376,200

0.8472

125,400

376,200

752,400

0.8472

Germany

55,000

165,000

330,000

0.7432

110,000

330,000

660,000

0.7432

Ghana

75,700

227,100

454,200

1.0229

151,400

454,200

908,400

1.0229

Gibraltar

48,500

145,500

291,000

0.6554

97,000

291,000

582,000

0.6554

Greece

41,000

123,000

246,000

0.5540

82,000

246,000

492,000

0.5540

Grenada

121,100

363,300

726,600

1.6364

242,200

726,600

1,453,200

1.6364

Guatemala

293,600

880,800

1,761,600

3.9675

587,200

1,761,600

3,523,200

3.9675

Guyana

6,618,100

19,854,300

39,708,600

89.4337

13,236,200

39,708,600

79,417,200

89.4337

Honduras

787,100

2,361,300

4,722,600

10.6364

1,574,200

4,722,600

9,445,200

10.6364

Hong Kong, China

444,400

1,333,200

2,666,400

6.0054

1,777,600

5,332,800

10,665,600

12.0108

Hungary

10,620,400

31,861,200

63,722,400

143.5189

21,240,800

63,722,400

127,444,800

143.5189

India

875,500

2,626,500

5,253,000

11.8310

3,502,000

10,506,000

21,012,000

23.6621

Indonesia

288,163,600

864,490,800

1,728,981,600

3,894.1027

576,327,200

1,728,981,600

3,457,963,200

3,894.1027

Page 12

Non-Core – 11/3/2022

Market

MDRT

Commission

COT

Commission

TOT

Commission

Commission

Conv Factor

MDRT

Premium

COT Premium

TOT

Premium

Premium

Conv Factor

Ireland

59,600

178,800

357,600

0.8054

119,200

357,600

715,200

0.8054

Isle of Man

50,700

152,100

304,200

0.6851

101,400

304,200

608,400

0.6851

Israel

278,400

835,200

1,670,400

3.7621

556,800

1,670,400

3,340,800

3.7621

Italy

49,200

147,600

295,200

0.6648

98,400

295,200

590,400

0.6648

Jamaica West Indies

3,857,500

11,572,500

23,145,000

52.1283

7,715,000

23,145,000

46,290,000

52.1283

Japan

7,547,000

22,641,000

45,282,000

101.9864

22,641,000

67,923,000

135,846,000

152.9797

Jordan

21,500

64,500

129,000

0.2905

43,000

129,000

258,000

0.2905

Kazakhstan

5,939,200

17,817,600

35,635,200

80.2594

11,878,400

35,635,200

71,270,400

80.2594

Kenya

3,097,300

9,291,900

18,583,800

41.8554

6,194,600

18,583,800

37,167,600

41.8554

Kuwait

14,700

44,100

88,200

0.1986

29,400

88,200

176,400

0.1986

Laos

206,132,800

618,398,400

1,236,796,800

2,785.5783

412,265,600

1,236,796,800

2,473,593,600

2,785.5783

Latvia

32,200

96,600

193,200

0.4351

64,400

193,200

386,400

0.4351

Lebanon

61,828,800

185,486,400

370,972,800

835.5243

123,657,600

370,972,800

741,945,600

835.5243

Lithuania

33,600

100,800

201,600

0.4540

67,200

201,600

403,200

0.4540

Luxembourg

63,600

190,800

381,600

0.8594

127,200

381,600

763,200

0.8594

Macau, China

330,200

990,600

1,981,200

4.4621

1,320,800

3,962,400

7,924,800

8.9243

Macedonia

1,409,300

4,227,900

8,455,800

19.0445

2,818,600

8,455,800

16,911,600

19.0445

Malaysia

117,300

351,900

703,800

1.5851

351,900

1,055,700

2,111,400

2.3777

Malta

22,100

66,300

132,600

0.2986

44,200

132,600

265,200

0.2986

Mauritius

1,222,300

3,666,900

7,333,800

16.5175

2,444,600

7,333,800

14,667,600

16.5175

Mexico

660,900

1,982,700

3,965,400

8.9310

1,321,800

3,965,400

7,930,800

8.9310

Montenegro

5,300

15,900

31,800

0.0716

10,600

31,800

63,600

0.0716

Montserrat

60,000

180,000

360,000

0.8108

120,000

360,000

720,000

0.8108

Mozambique

1,549,000

4,647,000

9,294,000

20.9324

3,098,000

9,294,000

18,588,000

20.9324

Myanmar

24,952,800

74,858,400

149,716,800

337.2000

49,905,600

149,716,800

299,433,600

337.2000

Namibia

404,800

1,214,400

2,428,800

5.4702

809,600

2,428,800

4,857,600

5.4702

Nepal

1,390,500

4,171,500

8,343,000

18.7905

4,171,500

12,514,500

25,029,000

28.1858

Netherlands

57,700

173,100

346,200

0.7797

115,400

346,200

692,400

0.7797

New Zealand

105,800

317,400

634,800

1.4297

211,600

634,800

1,269,600

1.4297

Nicaragua

833,600

2,500,800

5,001,600

11.2648

1,667,200

5,001,600

10,003,200

11.2648

Nigeria

5,759,100

17,277,300

34,554,600

77.8256

11,518,200

34,554,600

69,109,200

77.8256

Norway

729,100

2,187,300

4,374,600

9.8527

1,458,200

4,374,600

8,749,200

9.8527

Oman

13,300

39,900

79,800

0.1797

26,600

79,800

159,600

0.1797

Pakistan

1,776,100

5,328,300

10,656,600

24.0013

3,552,200

10,656,600

21,313,200

24.0013

Panama

34,700

104,100

208,200

0.4689

69,400

208,200

416,400

0.4689

Peru

120,100

360,300

720,600

1.6229

240,200

720,600

1,441,200

1.6229

Philippines

1,265,300

3,795,900

7,591,800

17.0986

2,530,600

7,591,800

15,183,600

17.0986

Poland

132,400

397,200

794,400

1.7891

264,800

794,400

1,588,800

1.7891

Portugal

TBD

TBD

TBD

TBD

TBD

TBD

TBD

T BD

Qatar

168,300

504,900

1,009,800

2.2743

336,600

1,009,800

2,019,600

2.2743

Republic of Korea

62,571,700

187,715,100

375,430,200

845.5635

156,429,250

469,287,750

938,575,500

1,056.9543

Romania

127,000

381,000

762,000

1.7162

254,000

762,000

1,524,000

1.7162

Saudi Arabia

147,300

441,900

883,800

1.9905

294,600

883,800

1,767,600

1.9905

Serbia

2,838,000

8,514,000

17,028,000

38.3513

5,676,000

17,028,000

34,056,000

38.3513

Singapore

72,400

217,200

434,400

0.9783

217,200

651,600

1,303,200

1.4675

Slovakia

39,600

118,800

237,600

0.5351

79,200

237,600

475,200

0.5351

Slovenia

41,900

125,700

251,400

0.5662

83,800

251,400

502,800

0.5662

South Africa

280,900

842,700

1,685,400

3.7959

561,800

1,685,400

3,370,800

3.7959

Spain

46,500

139,500

279,000

0.6283

93,000

279,000

558,000

0.6283

Sri Lanka

2,673,400

8,020,200

16,040,400

36.1270

5,346,800

16,040,400

32,080,800

36.1270

St. Kitts and Nevis

125,500

376,500

753,000

1.6959

251,000

753,000

1,506,000

1.6959

St. Lucia

140,200

420,600

841,200

1.8945

280,400

841,200

1,682,400

1.8945

St. Maarten

69,900

209,700

419,400

0.9445

139,800

419,400

838,800

0.9445

St. Vincent

116,100

348,300

696,600

1.5689

232,200

696,600

1,393,200

1.5689

Suriname

236,700

710,100

1,420,200

3.1986

473,400

1,420,200

2,840,400

3.1986

Sweden

652,500

1,957,500

3,915,000

8.8175

1,305,000

3,915,000

7,830,000

8.8175

Switzerland

84,400

253,200

506,400

1.1405

168,800

506,400

1,012,800

1.1405

Taiwan Area

1,357,500

4,072,500

8,145,000

18.3445

2,715,000

8,145,000

16,290,000

18.3445

Tanzania

54,884,300

164,652,900

329,305,800

741.6797

109,768,600

329,305,800

658,611,600

741.6797

Thailand

912,100

2,736,300

5,472,600

12.3256

1,824,200

5,472,600

10,945,200

12.3256

Togo

17,383,800

52,151,400

104,302,800

234.9162

34,767,600

104,302,800

208,605,600

234.9162

Tonga

120,100

360,300

720,600

1.6229

240,200

720,600

1,441,200

1.6229

Trinidad & Tobago

294,000

882,000

1,764,000

3.9729

588,000

1,764,000

3,528,000

3.9729

Turkey

TBD

TBD

TBD

TBD

TBD

TBD

TBD

T BD

Turks & Caicos

76,500

229,500

459,000

1.0337

153,000

459,000

918,000

1.0337

Uganda

97,251,200

291,753,600

583,507,200

1,314.2054

194,502,400

583,507,200

1,167,014,400

1,314.2054

Page 13

Non-Core – 11/3/2022

Market

MDRT

Commission

COT

Commission

TOT

Commission

Commission

Conv Factor

MDRT

Premium

COT Premium

TOT

Premium

Premium

Conv Factor

Ukraine

267,300

801,900

1,603,800

3.6121

534,600

1,603,800

3,207,600

3.6121

United Arab Emirates

175,000

525,000

1,050,000

2.3648

350,000

1,050,000

2,100,000

2.3648

United Kingdom

50,900

152,700

305,400

0.6878

101,800

305,400

610,800

0.6878

United States

74,000

222,000

444,000

1.0000

148,000

444,000

888,000

1.0000

Uruguay

1,193,000

3,579,000

7,158,000

16.1216

2,386,000

7,158,000

14,316,000

16.1216

Venezuela

549,000

1,647,000

3,294,000

7.4189

1,098,000

3,294,000

6,588,000

7.4189

Vietnam

360,813,300

1,082,439,900

2,164,879,800

4,875.8554

721,626,600

2,164,879,800

4,329,759,600

4,875.8554

Zambia

225,200

675,600

1,351,200

3.0432

450,400

1,351,200

2,702,400

3.0432

Zimbabwe

1,001,600

3,004,800

6,009,600

13.5351

2,003,200

6,009,600

12,019,200

13.5351

Page 14

Non-Core – 11/3/2022

INCOME PRODUCTION REQUIREMENTS FOR MEMBERSHIP

IN THE 2024 MILLION DOLLAR ROUND TABLE

Based on 2023 Production, Expressed in Local Currency

Production credit must be reported in U.S. dollars on certifying letters Production requirements are set independently for each Market. Conversion (Conv) factors have

no relationship to currency exchange rates and are used only to standardize MDRT processing. (Local currency divided by the income conversion = U.S. MDRT

requirement.) Qualification under this method is based on a requirement of USD 128,200 in annual gross income from insurance and financial products. A minimum of

USD 37,000 must be income from new business generated during the production year. (For a complete list of Market requirements, see the MDRT website at

https://www.mdrt.org/join/member-requirements/.)

Market

MDRT Income

COT Income

TOT Income

Income Conv Factor

Angola

75,900

227,700

455,400

0.5920

Anguilla

146,800

440,400

880,800

1.1450

Antigua

230,200

690,600

1,381,200

1.7956

Argentina

484,900

1,454,700

2,909,400

3.7823

Armenia

19,988,400

59,965,200

119,930,400

155.9157

Aruba

153,700

461,100

922,200

1.1989

Australia

186,500

559,500

1,119,000

1.4547

Azerbaijan

40,000

120,000

240,000

0.3120

Bahamas

109,600

328,800

657,600

0.8549

Bahrain

24,800

74,400

148,800

0.1934

Bangladesh

3,365,200

10,095,600

20,191,200

26.2496

Barbados

190,700

572,100

1,144,200

1.4875

Belarus

151,605,800

454,817,400

909,634,800

1,182.5725

Belgium

96,300

288,900

577,800

0.7511

Belize

137,800

413,400

826,800

1.0748

Bermuda

181,500

544,500

1,089,000

1.4157

Bolivia

338,700

1,016,100

2,032,200

2.6419

Bosnia-Herzegovina

86,700

260,100

520,200

0.6762

Botswana

433,800

1,301,400

2,602,800

3.3837

Brazil

288,200

864,600

1,729,200

2.2480

British Virgin Islands

130,300

390,900

781,800

1.0163

Brunei

80,100

240,300

480,600

0.6248

Bulgaria

89,900

269,700

539,400

0.7012

Cambodia

131,649,100

394,947,300

789,894,600

1,026.9040

Cameroon

29,295,300

87,885,900

175,771,800

228.5124

Canada

157,600

472,800

945,600

1.2293

Cayman Islands

106,200

318,600

637,200

0.8283

Channel Islands

89,200

267,600

535,200

0.6957

Chile

50,675,500

152,026,500

304,053,000

395.2847

China

378,300

1,134,900

2,269,800

2.9508

Colombia

137,964,200

413,892,600

827,785,200

1,076.1638

Costa Rica

42,040,000

126,120,000

252,240,000

327.9251

Côte d'Ivoire

31,238,300

93,714,900

187,429,800

243.6684

Croatia

420,500

1,261,500

2,523,000

3.2800

Curacao

115,800

347,400

694,800

0.9032

Cyprus

64,400

193,200

386,400

0.5023

Czech Republic

1,624,600

4,873,800

9,747,600

12.6723

Denmark

855,300

2,565,900

5,131,800

6.6716

Dominica

204,900

614,700

1,229,400

1.5982

Dominican Republic

2,125,700

6,377,100

12,754,200

16.5811

Ecuador

66,300

198,900

397,800

0.5171

Egypt

266,500

799,500

1,599,000

2.0787

El Salvador

58,200

174,600

349,200

0.4539

Estonia

69,800

209,400

418,800

0.5444

Fiji

105,300

315,900

631,800

0.8213

France

93,700

281,100

562,200

0.7308

Georgia

108,500

325,500

651,000

0.8463

Germany

95,300

285,900

571,800

0.7433

Ghana

131,100

393,300

786,600

1.0226

Gibraltar

83,600

250,800

501,600

0.6521

Greece

71,000

213,000

426,000

0.5538

Grenada

209,700

629,100

1,258,200

1.6357

Guatemala

508,500

1,525,500

3,051,000

3.9664

Guyana

11,462,300

34,386,900

68,773,800

89.4095

Honduras

1,363,200

4,089,600

8,179,200

10.6333

Hong Kong, China

769,700

2,309,100

4,618,200

6.0039

Hungary

18,394,100

55,182,300

110,364,600

143.4797

India

1,516,300

4,548,900

9,097,800

11.8276

Indonesia

499,087,500

1,497,262,500

2,994,525,000

3,893.0382

Page 15

Non-Core – 11/3/2022

Market

MDRT Income

COT Income

TOT Income

Income Conv Factor

Ireland

103,200

309,600

619,200

0.8049

Isle of Man

87,800

263,400

526,800

0.6848

Israel

482,200

1,446,600

2,893,200

3.7613

Italy

85,200

255,600

511,200

0.6645

Jamaica West Indies

6,681,100

20,043,300

40,086,600

52.1146

Japan

13,071,200

39,213,600

78,427,200

101.9594

Jordan

37,200

111,600

223,200

0.2901

Kazakhstan

10,286,500

30,859,500

61,719,000

80.2379

Kenya

5,364,500

16,093,500

32,187,000

41.8447

Kuwait

25,500

76,500

153,000

0.1989

Laos

356,609,700

1,069,829,100

2,139,658,200

2,781.6669

Latvia

55,700

167,100

334,200

0.4344

Lebanon

107,084,800

321,254,400

642,508,800

835.2948

Lithuania

58,300

174,900

349,800

0.4547

Luxembourg

110,200

330,600

661,200

0.8595

Macau, China

571,900

1,715,700

3,431,400

4.4609

Macedonia

2,440,800

7,322,400

14,644,800

19.0390

Malaysia

203,200

609,600

1,219,200

1.5850

Malta

38,300

114,900

229,800

0.2987

Mauritius

2,117,000

6,351,000

12,702,000

16.5132

Mexico

1,144,700

3,434,100

6,868,200

8.9290

Montenegro

9,200

27,600

55,200

0.0717

Montserrat

104,000

312,000

624,000

0.8112

Mozambique

2,682,800

8,048,400

16,096,800

20.9266

Myanmar

43,217,200

129,651,600

259,303,200

337.1076

Namibia

701,100

2,103,300

4,206,600

5.4687

Nepal

2,408,300

7,224,900

14,449,800

18.7854

Netherlands

99,900

299,700

599,400

0.7792

New Zealand

183,300

549,900

1,099,800

1.4297

Nicaragua

1,443,800

4,331,400

8,662,800

11.2620

Nigeria

9,974,500

29,923,500

59,847,000

77.8042

Norway

1,262,800

3,788,400

7,576,800

9.8502

Oman

23,100

69,300

138,600

0.1801

Pakistan

3,076,100

9,228,300

18,456,600

23.9945

Panama

60,100

180,300

360,600

0.4687

Peru

208,000

624,000

1,248,000

1.6224

Philippines

2,191,500

6,574,500

13,149,000

17.0943

Poland

229,300

687,900

1,375,800

1.7886

Portugal

TBD

TBD

TBD

TBD

Qatar

291,500

874,500

1,749,000

2.2737

Republic of Korea

108,371,600

325,114,800

650,229,600

845.3322

Romania

220,000

660,000

1,320,000

1.7160

Saudi Arabia

255,200

765,600

1,531,200

1.9906

Serbia

4,915,400

14,746,200

29,492,400

38.3416

Singapore

125,400

376,200

752,400

0.9781

Slovakia

68,600

205,800

411,600

0.5351

Slovenia

72,600

217,800

435,600

0.5663

South Africa

486,500

1,459,500

2,919,000

3.7948

Spain

80,500

241,500

483,000

0.6279

Sri Lanka

4,630,200

13,890,600

27,781,200

36.1170

St. Kitts and Nevis

217,300

651,900

1,303,800

1.6950

St. Lucia

242,800

728,400

1,456,800

1.8939

St. Maarten

121,000

363,000

726,000

0.9438

St. Vincent

201,000

603,000

1,206,000

1.5678

Suriname

410,000

1,230,000

2,460,000

3.1981

Sweden

1,130,000

3,390,000

6,780,000

8.8143

Switzerland

146,200

438,600

877,200

1.1404

Taiwan Area

2,351,200

7,053,600

14,107,200

18.3400

Tanzania

95,057,300

285,171,900

570,343,800

741.4765

Thailand

1,579,700

4,739,100

9,478,200

12.3221

Togo

30,108,200

90,324,600

180,649,200

234.8533

Tonga

208,100

624,300

1,248,600

1.6232

Trinidad & Tobago

509,200

1,527,600

3,055,200

3.9719

Turkey

TBD

TBD

TBD

TBD

Turks & Caicos

132,500

397,500

795,000

1.0335

Uganda

168,435,000

505,305,000

1,010,610,000

1,313.8455

Page 16

Non-Core – 11/3/2022

Market

MDRT Income

COT Income

TOT Income

Income Conv Factor

Ukraine

462,900

1,388,700

2,777,400

3.6107

United Arab Emirates

303,000

909,000

1,818,000

2.3634

United Kingdom

88,200

264,600

529,200

0.6879

United States

128,200

384,600

769,200

1.0000

Uruguay

2,066,300

6,198,900

12,397,800

16.1177

Venezuela

950,800

2,852,400

5,704,800

7.4165

Vietnam

624,913,700

1,874,741,100

3,749,482,200

4,874.5218

Zambia

390,000

1,170,000

2,340,000

3.0421

Zimbabwe

1,734,700

5,204,100

10,408,200

13.5312