1 | Page 2/10/2023

SAMHSA Detailed Budget and Narrative Template User Guide

SAMHSA Detailed Budget and Narrative

Template User Guide

For Budget Narrative Template Version 4.0 (Released January 2023)

2 | Page 2/10/2023

SAMHSA Detailed Budget and Narrative Template User Guide

Table of Contents

Using This Guide............................................................................................................................................ 7

Introduction .............................................................................................................................................. 7

Budget Types ............................................................................................................................................. 7

Acronyms Used in This Guide ................................................................................................................... 7

Icons Used in This Guide ........................................................................................................................... 8

Key Features .................................................................................................................................................. 8

Function, navigation, and shortcut keys ................................................................................................... 8

Guidance provided in tool tips, text boxes, and buttons.......................................................................... 9

Fillable data fields are highlighted ............................................................................................................ 9

Connections between budget categories to auto-populate data and totals: ......................................... 10

Validation errors ..................................................................................................................................... 10

Validation warnings ................................................................................................................................ 10

Quick Start Guide ........................................................................................................................................ 11

Introduction ............................................................................................................................................ 11

Save the PDF Budget Template ............................................................................................................... 11

Opening the PDF Budget Template ........................................................................................................ 11

Index/Bookmarks .................................................................................................................................... 11

Tool Tips and Buttons ............................................................................................................................. 11

Add and Delete Row Buttons .................................................................................................................. 11

Budget Year ............................................................................................................................................. 12

Cost Sharing and Matching ................................................................................................................ 12

For Multi-Year Funded Awards ......................................................................................................... 12

The Template has built-in validations in the form of Errors and Warnings ............................................ 12

Personnel ................................................................................................................................................ 12

Fringe Benefits ........................................................................................................................................ 12

Travel ...................................................................................................................................................... 13

Equipment ............................................................................................................................................... 13

Supplies & Other ..................................................................................................................................... 13

Contractual.............................................................................................................................................. 13

Indirect

Charges ...................................................................................................................................... 13

3 | Page 2/10/2023

SAMHSA Detailed Budget and Narrative Template User Guide

Review of Cost Sharing and Matching ............................................................................................... 13

Budget Summary ..................................................................................................................................... 14

Funding Limitations/Restrictions ............................................................................................................ 14

SF-424A ................................................................................................................................................... 14

Print to PDF ............................................................................................................................................. 14

Printing To PDF ............................................................................................................................................ 15

Why Print to PDF ..................................................................................................................................... 15

How To .................................................................................................................................................... 15

Always Double Check Before Submitting ........................................................................................ 15

Tooltips and Guidance ................................................................................................................................ 17

Starting Out ............................................................................................................................................. 17

Date Modified Box .................................................................................................................................. 20

Applicant / Recipient Identification Information .................................................................................... 21

For Multi-Year Funded (MYF) awards only ....................................................................................... 22

COST SHARING AND MATCHING ....................................................................................................... 25

A. Personnel ............................................................................................................................................ 28

Personnel Cost Table ............................................................................................................. 30

Personnel Narrative ............................................................................................................... 32

In-K

ind Personnel .................................................................................................................................... 34

In-Kind Personnel Table ......................................................................................................... 34

In-Kind Personnel Narrative .................................................................................................. 36

B

. Fringe Benefits .................................................................................................................................... 37

Fringe Components Table ...................................................................................................... 38

Fringe Benefits Cost Table ..................................................................................................... 39

Fringe Benefits Narrative ....................................................................................................... 40

C

. Travel .................................................................................................................................................. 41

Travel Cost Table ................................................................................................................... 41

Travel Narrative ..................................................................................................................... 43

D

. Equipment .......................................................................................................................................... 45

Equipment Cost Table ............................................................................................................ 45

4 | Page 2/10/2023

SAMHSA Detailed Budget and Narrative Template User Guide

Equipment Narrative ............................................................................................................. 47

E

. Supplies ............................................................................................................................................... 49

Supplies Cost Table ................................................................................................................ 49

Supplies Narrative.................................................................................................................. 50

F

. Contractual .......................................................................................................................................... 52

Summary of Contractual Costs Table ................................................................................ 55

CONTRACTUAL DETAILS ......................................................................................................... 56

G.

Construction: Not Applicable ............................................................................................................. 85

H. Other ................................................................................................................................................... 86

Other Cost Table .................................................................................................................... 87

Other Narrative ...................................................................................................................... 89

I

. Total Direct Charges ............................................................................................................................. 91

Total Direct Charges Table ..................................................................................................... 91

J

. Indirect Charges ................................................................................................................................... 92

Type of IDC Rate / Cost Allocation Plan ................................................................................. 92

J.1 We will not Charge IDC to the Award ......................................................................... 94

J.2 De Minimis Rate ......................................................................................................... 95

J.3 Approved Federally Negotiated IDC Rate Agreement ............................................... 99

J.4 Training Grant Rate of 8%......................................................................................... 102

J.5 Cost Allocation Plan .................................................................................................. 104

R

EVIEW OF COST SHARING AND MATCHING .................................................................................. 106

Cost Sharing and Matching Narrative.................................................................................. 107

B

UDGET SUMMARY .............................................................................................................................. 108

A. Personnel ......................................................................................................................... 109

B. Fringe Benefits ................................................................................................................. 109

C. Travel ............................................................................................................................... 109

D. Equipment ....................................................................................................................... 109

E. Supplies ............................................................................................................................ 109

F. Contractual ...................................................................................................................... 110

H. Other ............................................................................................................................... 110

5 | Page 2/10/2023

SAMHSA Detailed Budget and Narrative Template User Guide

I. Total Direct Charges ......................................................................................................... 110

J. Indirect Charges ................................................................................................................ 110

K. Total Project Costs ........................................................................................................... 111

B

UDGET SUMMARY FOR REQUESTED FUTURE YEARS ......................................................................... 112

Budget Summary Narrative ................................................................................................. 112

F

UNDING LIMITATIONS/RESTRICTIONS ................................................................................................ 113

Funding Limitation/Restriction Narrative ............................................................................ 114

I

MPORTANT: Print to PDF Before Submission ...................................................................................... 115

IMPORTANT SF-424A GUIDANCE .......................................................................................................... 115

Frequently Asked Questions ..................................................................................................................... 116

Why do we need to Print to PDF before submitting to SAMHSA? ....................................................... 116

Where can I find information on Funding Limitations? Key Personnel requirements? Matching

requirements? ....................................................................................................................................... 116

What is the difference between the Quantity and Duration fields in the Supplies and Other budget

categories? ............................................................................................................................................ 116

I am having technical issues with the budget template. Who should I contact? ................................. 116

Are we required to use this budget template? ..................................................................................... 116

How do I have in-kind costs when my grant doesn’t require matching? ............................................. 116

After adding all costs and calculating Indirect Costs, I am over budget. How can I fix this? ................ 116

Why is there both a Fringe Rate and a Lump Sum field in the Fringe Benefits table? ......................... 117

I tried to open the budget template, but I get a warning message saying “Please wait... If this message

is not eventually replaced by the proper contents of the document, your PDF viewer may not be able

to display this type of document”. What does this mean? How do I fix it? ......................................... 117

References And Resources ........................................................................................................................ 118

Official Regulations and Guidance ........................................................................................................ 118

Notice of Funding Opportunities .......................................................................................................... 118

Blank SAMHSA Detailed Budget and Narrative Template .................................................................... 118

Blank Microsoft Word Budget Templates ............................................................................................. 118

Sample Budgets..................................................................................................................................... 118

Pop-Out Guidance ..................................................................................................................................... 119

Summary of Unallowable Costs ............................................................................................................ 119

Matching ............................................................................................................................................... 120

Printing To PDF ...................................................................................................................................... 121

6 | Page 2/10/2023

SAMHSA Detailed Budget and Narrative Template User Guide

VEHICLE LEASE/RENTAL OR PURCHASE ................................................................................................ 122

Minor Alteration and Renovation (A&R) .............................................................................................. 123

Guidance on Calculating Sallaries and Paid Time Off (PTO) ................................................................. 124

When to Complete the Fringe Component Table ................................................................................. 125

7 | Page 2/10/2023

SAMHSA Detailed Budget and Narrative Template User Guide

Using This Guide

Introduction

This guide is designed to help you get started using the SAMHSA Budget Narrative Template right away

as well as provide a general reference to all aspects of the SAMHSA Budget Narrative Template.

This guide is divided into seven sections:

1. Key Features – This describes the main features of the Budget Narrative Template

2. Quick Start Guide – This is a short tutorial on how to complete the Budget Narrative Template

3. Tooltips and Guidance – This section lists all tooltips and guidance provided within the Budget

Narrative Template

4. Frequently Asked Questions – These are some commonly asked questions we have received

from grantees and the associated answers we provide

5. Resources and References – This section contains links to various external resources and

documentation that you may need when preparing your SAMHSA budget

6. Pop-Out Guidance – These are copies of the embedded guidance found in the Budget Template.

Budget Types

There are three types of budgets referenced throughout this guide:

1. No Match Required – These are the simplest budgets to complete. Applicants/recipients do not

have to provide any matching funds, they are for a single year, and they do not have to split

funding between multiple SAMHSA centers

2. Match Required – These budgets require the grantees to provide a specified portion of the total

project costs from non-federal sources. Refer to the NOFO for more information

3. Multi-Year Funded (MYF) Awards – Budgets for MYF awards do not apply to new applications

for funding, These budgets span more than 12 months and must be broken down by each

incremental period.

Acronyms Used in This Guide

• CMHS – Center for Mental Health Services

• CSAP – Center for Substance Abuse Prevention

• CSAT – Center for Substance Abuse Treatment

• FG – Flex Grants

• FY – Fiscal Year

• GMS – Grants Management Specialist

• IDC – Indirect Costs

• LOE – Level of Effort

o Percentage of time worked based on a full-time work schedule of 2,080 hours per year

• MTDC – Modified Total Direct Cost

• NoA – Notice of Award

• NOFO – Notice of Funding Opportunity

8 | Page 2/10/2023

SAMHSA Detailed Budget and Narrative Template User Guide

• PD – Project Director

Icons Used in This Guide

This represents a button that will allow you to add a line item to the budget.

This represents a button that will allow you to remove a line item in the budget.

This represents a button, which will either provide guidance or will perform an action

(like saving or printing). Buttons will NOT be visible on the document printed to PDF or to a printer.

This indicates a new or updated feature from the previous version.

This indicates a feature specific to Multi-Year budgets

This indicates a feature specific to budgets that requires matching.

This indicates that a field is automatically populated.

This indicates a message that will pop up when clicking on one of the informational buttons. These

messages will provide general guidance that will help you develop a good budget.

This indicates a tool tip that appears when you hover over a part of the template.

This indicates a warning message. The template will not overwrite anything you have entered,

but you should try to address the issue raised.

This indicates an error message. The system will remove the last item entered and will not

allow you to proceed until you have addressed the issue raised.

Key Features

Function, navigation, and shortcut keys

The dynamic PDF template works best with Adobe Acrobat or Reader.

Before entering data, save the template, then open it directly in Acrobat or Reader.

BUTTON

9 | Page 2/10/2023

SAMHSA Detailed Budget and Narrative Template User Guide

Click the green + button to add a new row or table with a corresponding narrative section.

Click the red x button to delete only the row or table with the X button and its corresponding

narrative section. You cannot delete a row if it is the last remaining row.

Use the bookmarks or Adobe thumbnails feature for faster navigation between pages.

The “hot” keys in the table below may be used when entering text in data fields.

Function

Windows OS

Mac OS

Select All

CRTL + A

CTRL + A or Command (or Cmd) + A

Bold

CTRL + B

CTRL + B or Command (or Cmd) + B

Italics

CTRL + I

CTRL + I or Command (or Cmd) + I

Underline

CTRL + U

CTRL + U or Command (or Cmd) + U

Copy

CTRL + C

CTRL + C or Command (or Cmd) + C

Cut

CTRL + X

CTRL + X or Command (or Cmd) + X

Paste

CTRL + V

CTRL + V or Command (or Cmd) + V

Undo

CTRL + Z

CTRL + V or Command (or Cmd) + Z

Reduce font size

CTRL +=

CTRL += or Command (or Cmd) +=

Guidance provided in tool tips, text boxes, and buttons

To view tool tips (yellow pop-up boxes) with instructions and guidance, hover your

mouse over the table headers, text boxes, and data fields.

Text in gray font and buttons with instructions/guidance are visible only on the

screen – they will not appear in the document printed to PDF.

Fillable data fields are highlighted

Data may be entered only in highlighted fields (if you have enabled “fields

highlight color” in Acrobat or Reader). Auto-calculated or read- only fields will

not appear highlighted.

Text fields in tables are limited to between 60 and 300 characters (including

spaces) or up to several lines of text. However, text fields in narrative sections

are unlimited.

Drop-down lists and calendar windows

Items may be selected from drop-down lists. In the Travel table, items selected from

the drop-down list will auto-populate the Basis.

10 | Page 2/10/2023

SAMHSA Detailed Budget and Narrative Template User Guide

In the IDC budget category, the type of IDC Rate or Cost Allocation Plan selected from the

drop-down list will show the relevant IDC table.

Dates must be selected from the calendar window in the date fields.

Connections between budget categories to auto-populate data and totals:

• The Budget Year selection on page 1 auto-populates the Year(s) in the Budget Summary, Budget

Summary for Requested Future Years, and Funding Limitations/Restrictions tables.

• Relevant data from the Personnel table auto-populates the Fringe Benefits Cost table.

• The name of the organization or consultant used to identify each agreement only has to be

entered once to auto-populate the budget detail section for that agreement.

• The Budget Summary table is completely auto-populated

Validation errors

Values/amounts exceeding certain thresholds will be flagged as errors, which must be addressed before

the line-item cost can be calculated. Examples include:

• Annual Salaries and Hourly Rates in the Personnel and Contractual budget categories (unless

Consultant is selected) cannot exceed the Executive Level II salary of the Federal Executive Pay

Scale.

• Levels of Effort (LOE) cannot exceed 100%.

• Total Fringe Rate cannot exceed the total of the fringe component rates

• Percentage of Equipment Cost Charged to the Project cannot exceed 100%.

• Unit Cost for Supplies cannot exceed $5,000

• Bases to determine Indirect Charges cannot exceed the Total Direct Costs

Validation warnings

These warnings will prompt you to review the values/amounts entered if they exceed certain

thresholds.

11 | Page 2/10/2023

SAMHSA Detailed Budget and Narrative Template User Guide

Quick Start Guide

Introduction

This SAMHSA PDF budget template facilitates completion of the Detailed Budget and Narrative

Justification explaining the federal and the non-federal expenditures broken out by the object class

categories in the SF-424A – Section B. It enables Applicants and Recipients to provide detailed

calculations showing how each line-item expense was determined.

The PDF budget template provides applicants and recipients with guidance via tool tips, text boxes and

buttons; Auto-calculated data fields and totals; Data validations and much more.

Save the PDF Budget Template

Please save this PDF budget template to your computer before opening it directly in Adobe Acrobat or

Acrobat Reader. To save this template, click the save button, choose where you would like to save the

template, and click Save.

Opening the PDF Budget Template

To open the template, first open Adobe Acrobat or Acrobat Reader. Then click on File, select open, and

Select the Budget Template PDF document. The dynamic PDF may not open up properly in your internet

browser, and the template may not function as designed if you use a third-party PDF software other

than Adobe to open the budget template.

Index/Bookmarks

At the top of each page, you will notice an Index or Bookmarks button. Click this button to reveal the

various sections of the budget template. Clicking the section name will take you directly to that section.

Tool Tips and Buttons

The budget template has several buttons with instruction and guidance. Remember to click these

buttons to view guidance or to be redirected to SAMHSA’s website with additional information. The

guidance and buttons will disappear when printing to PDF for submission to SAMHSA.

This template has useful tooltips on nearly every text field and header. To reveal the tool tips, hover

your cursor over the text field you wish to reveal. Please review the tooltips before completing each

section.

Add and Delete Row Buttons

The tables have buttons that allow you to add and remove rows. When you add a row to a table, an

additional blank narrative row will appear below the table. When you remove a row, the corresponding

narrative row will be removed. If a table has only one row, you will not be able to delete it.

12 | Page 2/10/2023

SAMHSA Detailed Budget and Narrative Template User Guide

Budget Year

The budget year you select for your budget submission will appear in the header of the BUDGET

SUMMARY section. The budget year will also determine how many columns will appear in the BUDGET

SUMMARY FOR REQUESTED FUTURE YEARS and THE FUNDING LIMITATIONS AND RESTRICTIONS tables

at the end of the template.

Cost Sharing and Matching

The default Cost Sharing and Matching option is No. Selecting Yes will reveal hidden data fields for you

to complete. If your grant does not require matching, simply leave the selection as No.

For grants with cost sharing requirements, select Yes and complete the two new fields (Match Ratio

stated in the NOFO). Refer to the NOFO for the match rate specific to your grant.

Next to each line item in the budget, you will now see a column labeled “Non-Federal Match”. Once you

fill out each line item, simply insert the amount of matching funds apply to each item. Please note that

this cannot be more than the amount calculated cost for that item. The Federal Request column will

automatically update.

For Multi-Year Funded Awards

If your award is Multi-Year Funded, select the box that says “Check the box to select the incremental

period. You can then select the Incremental Period from the dropdown list.

The Template has built-in validations in the form of Errors and Warnings

One example of an error can be seen in the Personnel table. If the Annual Salary or Hourly Rate exceeds

the Executive Level II salary limitation you will receive an error message and your entry will be deleted.

Personnel

Note that in the Personnel table, you may use either Hourly Rate and Hours or Annual Salary and Level

of Effort or LOE to calculate personnel costs. The default option is Annual Salary and LOE. Check the box

to enable Hourly Rate and Hours. Additionally, if there are multiple staff with the same information, you

can group them together. Simply fill out the information for the first staff member and enter the # of

staff in the “# of Staff” field.

Fringe Benefits

The Position, Name and Personnel Cost from the Personnel table will be automatically populated in the

Fringe Benefits table. If you add a row to the Personnel table, a row will automatically be added to the

Fringe Benefits table.

If you enter a percentage in the Total Fringe Rate in the Fringe Benefits table greater than the Total

Fringe Rate in the Fringe Components table, you will receive an error and your entry will be deleted.

13 | Page 2/10/2023

SAMHSA Detailed Budget and Narrative Template User Guide

Travel

Remember not to show registration fees in the Travel table. Instead, show registration fees in the

Section H. Other table or, if the registration fee is for a consultant or contractor, show it in the

Contractual Other table.

Equipment

Note that if the equipment will also be used by projects other than those supported by the SAMHSA

award, adjust the percentage charged to the project accordingly to reflect SAMHSA’s fair share. If

requesting to rent or purchase vehicles, be sure to follow the guidance in the PDF popup on vehicle

lease/rental or purchase. This same functionality exists in the Contractual Equipment section.

Supplies & Other

In the Supplies table as well as in the Other table in Section H, you may enter values in either Quantity

or Duration or BOTH. For example, to enter project supplies at $100 per month, you would enter “$100”

in Unit Cost, enter “per month” in Basis, and “12” under Duration. This same functionality exists in the

Contractual Supplies section and in the Contractual Other section.

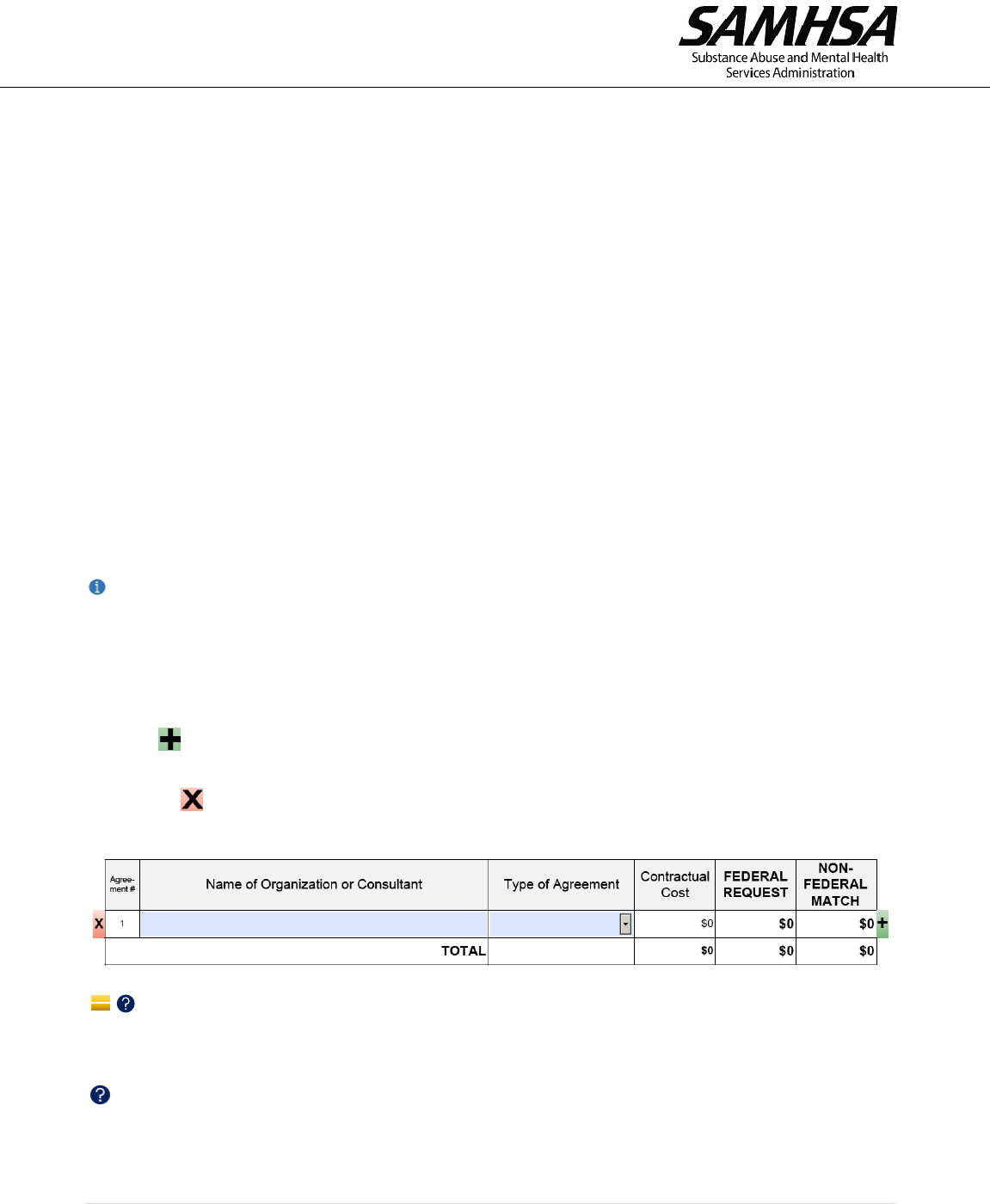

Contractual

The Contractual Cost and FEDERAL REQUEST and if matching is required, the NON-FEDERAL MATCH

columns, are automatically populated from the tables in the Contractual Details section below. You will

notice that for the first “contract” shown, there are seven check boxes to reveal budget category tables

for that “contract.” Please use these tables to show line-item costs for each “contract.”

After listing the name of each contractor or organization in the Summary of Contractual Costs table,

select the type of agreement from the dropdown.

Each “contract” you add to the Summary of Contractual Costs table will generate its own Contractual

Details section with seven check boxes for that “contract.”

When you delete a “contract” from the Summary of Contractual Costs table, all of the budget category

tables for that “contract” will be deleted.

Indirect Charges

In Section J, Indirect Charges, select one of the five options that reflects your situation. Follow the

instructions provided in the template and in tooltips to ensure you accurately complete this section.

Note the amount of the base you enter cannot exceed your total direct charges shown under Total

Federal Request in Section I. Total Direct Charges.

Review of Cost Sharing and Matching

If you had selected matching is required on page 1, you may see a message in the Review of Cost Sharing

and Matching section stating that you have not met the minimum required match based on the match

ratio entered on page 1. If you see this message, review the amount of NON-FEDERAL MATCH entered in

the various tables.

14 | Page 2/10/2023

SAMHSA Detailed Budget and Narrative Template User Guide

Budget Summary

The Budget Summary table is auto-populated from data entered in the previous Sections A – Personnel

through J – Indirect Charges.

Funding Limitations/Restrictions

In the narrative for each Funding Limitation or Restriction, remember to identify which line-item

expense in your budget relate to the amounts shown in the Funding Limitation or Restriction table.

SF-424A

The SF-424A – Budget Information is included with this budget template to facilitate your completion of

the SF-424A submission required by grant.gov and eRA.

The amounts shown in Section A columns (e) and (f) and Section B columns (1) and (2) are auto-

populated from the budget template. Ensure the amounts in Sections A and B of the SF-424A in this

budget template are entered exactly as shown into the SF-424A submission required by grant.gov and

eRA online forms.

Note that for programs that require matching contributions, the Non-Federal Match (matching

contributions) is shown separately from the Federal Request in Section B. The Federal Request for each

budget category is shown in column (1) and the Non-Federal Match (matching contributions) is shown in

column (2).

Print to PDF

Printing to PDF ensures that SAMHSA will be able to see all of your budget data. Therefore, before

submitting your budget to SAMHSA, remember to print the budget to PDF.

To print to PDF, click the Print button on the first page of the template, in the printer dropdown menu,

select “Print to PDF,” and click the Print button. Choose your location to save the PDF and use this PDF

version for your eRA Commons submission.

15 | Page 2/10/2023

SAMHSA Detailed Budget and Narrative Template User Guide

Printing To PDF

Why Print to PDF

Before you submit your budget narrative to eRA, please print to PDF.

There is an issue with submitting the dynamic PDF (the editable budget narrative template) to eRA,

whereby the submitted PDF becomes corrupted. When you PRINT TO PDF, this issue does not occur.

How To

To PRINT TO PDF, click on the Print button on the upper right of the template.

This will open the Print dialogue box with the printer set to something like Microsoft Print to PDF, which

when you click the Print button it will ask you to save the PDF. This saved PDF is what we need you to

submit.

The Print dialogue box will look like this when printing from Adobe Acrobat:

Always Double Check Before Submitting

You should always double check the budget narrative before you submit it. If you see the following

buttons at the top of the first page, you are NOT submitting the correct version:

16 | Page 2/10/2023

SAMHSA Detailed Budget and Narrative Template User Guide

I

f you see the following without buttons at the top, you are submitting the correct version:

17 | Page 2/10/2023

SAMHSA Detailed Budget and Narrative Template User Guide

Tooltips and Guidance

Starting Out

Introduction

Click for Introduction / Overview of the budget template.

BUDGET TEMPLATE

This budget template facilitates completion of the Detailed Budget and Narrative Justification explaining

the federal and the non-federal expenditures broken out by the object class categories in the SF-424A −

Section B (Budget Categories). It enables applicants/recipients to provide detailed calculations showing

how each line-item expense was determined.

The Detailed Budget and Narrative Justification must match the costs shown in the SF-424A and the

estimated funding in the SF-424 (Section 18) and must be consistent with and support the project

narrative. The activities, resources, staff, and other items described in the project narrative must be

referenced in the Detailed Budget and Narrative Justification.

Before preparing the Detailed Budget and Narrative Justification, be sure to review the Notice of

Funding Opportunity (NOFO) including the Funding Limitations/Restrictions in Section IV-3 and the

Standard Funding Restrictions in the appendix.

Applicants/recipients must demonstrate that costs are allowable (45 CFR §75.403). In other words, costs

must be necessary and reasonable for the performance of the Federal award and must be allocable

under the cost principles in the 45 CFR §75 Subpart E.

A cost is “necessary” if it meets a program objective.

A cost is “reasonable” if it meets the “prudent person” standard (45 CFR §75.404).

A cost is “allocable” to a particular Federal award if the goods or services involved are assignable to that

Federal award in accordance with relative benefits received. In other words, if you charge 100 percent

of an expenditure to a federal program, you must ensure that the federal program receives the entire

benefit of the expenditure.

Costs must meet the following additional in order to be allowable (45 CFR §75.403):

1. Be necessary and reasonable for the performance of the Federal award and be allocable under

these principles

2. Conform to any limitations or exclusions set forth in the cost principles or in the Federal award.

3. Be consistent with the policies, regulations, and procedures that apply uniformly to both Federal

awards and other activities of the applicant/recipient.

Introduction

18 | Page 2/10/2023

SAMHSA Detailed Budget and Narrative Template User Guide

4. Be accorded consistent treatment. A cost may not be assigned to a Federal award as a direct

cost if any other cost incurred for the same purpose in like circumstances has already been

allocated to the Federal award as an indirect cost.

5. Be determined in accordance with generally accepted accounting principles (GAAP), except for

state and local governments and Indian tribes only as otherwise provided in this part of the

regulation (45 CFR 75).

6. Not be included as a cost or used to meet a cost-sharing or matching requirement for any other

federally-financed project in either the current or a prior period

7. Be adequately documented.

Instructions

Click for instructions to review before completing the budget template.

INSTRUCTIONS

1. SAVE PDF BUDGET TEMPLATE

Before completing this budget template, save the PDF document to a location on your computer.

2. OPEN PDF BUDGET TEMPLATE

The dynamic PDF budget template works best with Adobe Acrobat or Reader. Open the budget template

directly in Acrobat or Reader to enter data.

3. PRINT TO PDF BEFORE SUBMISSION TO SAMHSA

Before submission to SAMHSA, you must print the budget to PDF. To print to PDF, click the “Print”

button or go to File > Print > Printer > Adobe PDF.

4. INCLUDE A COPY OF YOUR INDIRECT COST (IDC) RATE AGREEMENT

If you are charging IDC to the award based on an approved federally negotiated IDC rate agreement, you

must include with your budget submission a copy of the IDC rate agreement in effect at the beginning of

the budget period. This is required even if you have previously submitted your IDC rate agreement.

NOTE:

1. Guidance (see gray text and buttons) provided in the budget template will be visible only on the

screen and will not appear in the document sent to your printer or printed to PDF.

2. Text data fields in most tables are limited to between 60 and 300 characters (including spaces) or

about 2 to 3 lines of text, whereas text data fields in all narrative sections are unlimited.

Adobe Tips

INSTRUCTIONS

ADOBE TIPS

19 | Page 2/10/2023

SAMHSA Detailed Budget and Narrative Template User Guide

Click for tips to troubleshoot any issues with the budget template.

ADOBE TIPS

1. IF JAVASCRIPT IS NOT ENABLED

If you are unable to click the buttons and access other features of this PDF template, JavaScript may not

be enabled. If JavaScript is not enabled (“Enabled” is the typical default setting), open Adobe Reader or

Acrobat and go to Edit > Preferences > JavaScript and select “Enable Acrobat JavaScript.”

2. IF FILLABLE FIELDS ARE NOT HIGHLIGHTED

If you are unable to see the color highlight that indicates which fields require data, you may turn on the

fields highlight color as follows: Go to Edit > Form Options > and click “Highlight Existing Fields.”

Alternatively, you may go to Edit > Preferences > Forms > Highlight Color and select “Show border hover

color for fields.”

3. IF THE ACTIVE FIELD IS FILLED WITH BLACK

If the active (blinking cursor) data field is filled with black and you cannot see what you are typing, go to

Edit > Preferences > Accessibility and uncheck the box for “Replace Document Colors.”

4. IF SOME TOOL TIP TEXT APPEARS TO BE CUT OFF

If you are unable to see all of the text in the tool Tip that appears when your mouse hovers over the

cell/field, you should reduce the Windows/Mac OS scale setting to 100%.

For Windows OS, go to Settings > System > Display and reduce the “Change the size of text, apps, and

other items” setting to 100%. Consider reducing the text size setting to 100% as well.

For Mac OS, go to System Preferences > Displays > and click the Display tab, then select the “Scaled”

option under Resolution to adjust the scaling.

5. IF THE PAGE ORIENTATION OF THE SF-424A IS NOT LANDSCAPE (WIDER THAN IT IS TALL)

If the page orientation of the SF-424A is in portrait instead of landscape, go to File > Print and in the

Print dialog box, check the option for Choose paper source by PDF page size” and ensure “Auto” is

selected under Orientation.

Save

Click to save document. Once saved, open the document directly in Adobe Acrobat or Reader.

Print

SAVE

PRINT

20 | Page 2/10/2023

SAMHSA Detailed Budget and Narrative Template User Guide

Click to print document to PDF or printer.

You must PRINT TO PDF before submission to SAMHSA.

Date Modified Box

At the top of each page, there is a box with the date the budget narrative template was most recently

updated. This will be used by SAMHSA staff to determine the latest version of a given budget if no other

information is provided.

It is highly recommended that the file is named with a version number added to the end to ensure

SAMSHA can properly determine which budget is the most recent. Example: “Revised Budget 02-02-

2022 version 2.pdf”

21 | Page 2/10/2023

SAMHSA Detailed Budget and Narrative Template User Guide

Applicant / Recipient Identification Information

Applicant/Recipient:

Enter the name of your organization.

Application/Award Number:

Enter the application or award number. If your project has been awarded, refer to your Notice of Award

(NoA) for the award number.

An example of the application or award number is SM012345 where SM is the Institute Code or Center

from which the grant originates, for example, SM, SP, TI, and FG; and 012345 is the six-digit core grant

number unique to that specified project.

• SM refers to the Center for Mental Health Services (CMHS).

• SP refers to the Center for Substance Abuse Prevention (CSAP).

• TI refers to the Center for Substance Abuse Treatment (CSAT).

• FG refers to the Center for Flex Grants.

Project Title:

Enter the title of the project.

Budget Period:

Enter the actual budget period start and end dates from your Notice of Award (NoA) if your project has

been awarded. Otherwise, enter the proposed/ projected budget period dates based on the anticipated

project start date in the NOFO.

Most SAMHSA grants have budget periods beginning 09/30 of one year and ending on 09/29 of the next.

Start Date:

Select the budget period start date from the calendar window.

End Date:

Select the budget period end date from the calendar window.

22 | Page 2/10/2023

SAMHSA Detailed Budget and Narrative Template User Guide

Budget Year:

Select the budget year (1, 2, 3, 4, or 5) from the drop-down list. If your project has been awarded, refer

to your Notice of Award (NoA) for the budget year.

The budget year you select will auto-populate “Year” in the following tables:

• BUDGET SUMMARY

• BUDGET SUMMARY FOR REQUESTED FUTURE YEARS

• FUNDING LIMITATIONS AND RESTRICTIONS

Note: If after entering amounts in the FUNDING LIMITATIONS AND RESTRICTIONS table(s), you change

the budget year to remove future years from the table(s), remember to delete any amounts entered in

those future years to ensure they are not included in the Total for Budget Category.

For Multi-Year Funded (MYF) awards only

Multi-Year Funded (MYF) awards only:

Check the box to select the Incremental Period.

Not applicable to new applications for funding

Note that MYF awards have budget periods longer than one year. An award may be MYF for all, a

portion, or none of the project period. A no-cost extension (NCE) of an existing award does not

constitute MYF. An NCE can extend the final budget period and the project period end date beyond the

original award end date.

Select incremental period

Select the incremental period (1, 2, 3, 4, or 5) from the drop-down list.

Guidance

Guidance.

LINK: [https://www.samhsa.gov/grants/grants-dashboard]

Click the button in the template for the list of Notices of Funding Opportunity (NOFOs) by Fiscal Year on

SAMHSA’s website.

List of NOFOs by Fiscal Year

23 | Page 2/10/2023

SAMHSA Detailed Budget and Narrative Template User Guide

Before preparing your Detailed Budget and Narrative Justification, ensure you review the NOFO

including the Funding Limitations/Restrictions in Section IV-3 and the Standard Funding Restrictions in

the appendix.

LINK: [[https://www.ecfr.gov/cgi-bin/text-idx?node=pt45.1.75]

Click the button in the template for the electronic 45 CFR §75.

Summary of Unallowable Costs:

Click the button in the template for a summary of unallowable costs

Summary of Unallowable Costs

The costs listed below are usually unallowable under the 45 CFR §75 Subpart E, the HHS Grant Policy

Statement (GPS), and SAMHSA's Notice of Funding Opportunity (NOFOs). Note that this list does not

include all unallowable costs.

The allowability of costs under individual awards may also be governed by requirements specified in the

program legislation, regulations, or the specific terms and conditions of the award, which will take

precedence over the general discussion provided here (HHS GPS, pg. II-28).

1. Advertising And Public Relations (§75.421 and HHS GPS, pg. II-30): Advertising and public

relations costs are generally not allowable except under the instances allowed by federal

regulations such as program outreach and other specific purposes necessary to meet the

requirements of the federal award.

2. Automobile Costs for Personal Use (§75.431 f): That portion of automobile costs furnished by

the entity that relates to personal use by employees (including transportation to and from work)

is unallowable as ither fringe benefit or indirect (F&A) costs.

3. Contingency Funds (§75.433 and HHS GPS, pg. II-33): Contingency funds or funds set aside for

events whose occurrence cannot be foretold with certainty as to time, intensity, or assurance of

their happening are unallowable under non-construction grants.

4. Entertainment (§75.438 and HHS GPS, pg. II-33): Costs of entertainment, including amusement,

diversion, and social activities and any associated costs are unallowable, except where specific

costs that might otherwise be considered entertainment have a programmatic purpose and are

authorized either in the approved budget for the Federal award or with SAMHSA’s prior written

approval.

5. Goods and Services for Personal Use by the non-Federal entity’s employees (§75.445). Costs

for these items are unallowable

Electronic 45 CFR §75

Summary of Unallowable Costs

24 | Page 2/10/2023

SAMHSA Detailed Budget and Narrative Template User Guide

6. Honoraria (HHS GPS, pg. II-34): Unallowable when the primary intent is to confer distinction on,

or to symbolize respect, esteem, or admiration for, the recipient of the honorarium. A payment

for services rendered, such as a speaker's fee under a conference grant, is allowable.

7. Incentive Compensation (§75.430(f) and HHS GPS, p. II-40): Generally unallowable; however,

allowable for employees only if based on cost reduction, or efficient performance, suggestion

awards, safety awards, etc., to the extent that the overall compensation is reasonable and paid

or accrued based on an agreement between the organization and the employees before the

services were rendered, or based on an established plan followed by the organization so

consistently as to imply an agreement to make such payment.

8. Lobbying/Political Activities (§75.450 and HHS GPS, pg. II-35): The costs of certain influencing

activities (i.e., attempts to influence the enactment or modification of any pending legislation

through communication with any member or employee of the state legislature, or with any

government official or employee concerning a decision to sign or veto enrolled legislation)

associated with obtaining grants, contracts, cooperative agreements, or loans is unallowable.

9. Major Alteration and Renovation (A&R) (NOFO): Payment for the purchase or construction of

any building or structure to house any part of the program is unallowable under non-

construction grants. However, SAMHSA applicants/recipients may request up to 25 percent of

the total approved budget (direct and indirect costs) for a budget period, or $150,000,

whichever is less, for minor A&R of existing facilities, if necessary and appropriate for the

project. Minor A&R may not include a structural change (e.g., to the foundation, roof, floor, or

exterior or loadbearing walls of a facility, or extension of an existing facility) to achieve the

following: Increase the floor area; and/or, change the function and purpose of the facility. All

minor A&R must be approved by SAMHSA

10. Meals (HHS GPS, pg. II-36 and NOFO): Meals are generally unallowable unless they are an

integral part of a conference grant (provided that such charges are not duplicated in

participant's per diem or subsistence allowances) or they are specifically stated as an allowable

expense in the NOFO. Also, refer to https://www.hhs.gov/grants/contracts/contract-policies-

regulations/spending-on-food/index.html

11. Miscellaneous expenses (NOFO): “Miscellaneous” expenses are unallowable. Budget line items

should reflect specific expenses only. Also refer to item 4 – Contingency Funds.

12. Promotional Materials (§75.421(e)(3) and NOFO): Appropriated funds shall not be used to pay

for promotional items and memorabilia including, but not limited to, gifts, souvenirs, clothing

and commemorative items such as pens, mugs/cups, folders/folios, lanyards, and conference

bags. Also, refer to https://www.hhs.gov/grants/contracts/contract-policies-

regulations/spending-on-promotional-items/index.html

13. Stipends (HHS GPS, pg. II-41): Stipends or payments made to individuals are generally

unallowable unless they are permitted by a program’s statute authorizing or implementing

regulations or they are payments made to individuals under a Traineeship, Fellowship, and

Similar Award Made to Organizations on Behalf of Individuals.

25 | Page 2/10/2023

SAMHSA Detailed Budget and Narrative Template User Guide

COST SHARING AND MATCHING

Cost Sharing and Matching

Review the NOFO Section III-2 – Cost Sharing and Matching Requirements to determine whether the

project requires non-federal matching funds or contributions.

To determine whether the project requires non-federal matching funds or contributions, review the

NOFO Section III-2 – Cost Sharing and Matching Requirements.

Information on Matching

Click the button in the template for more information on matching

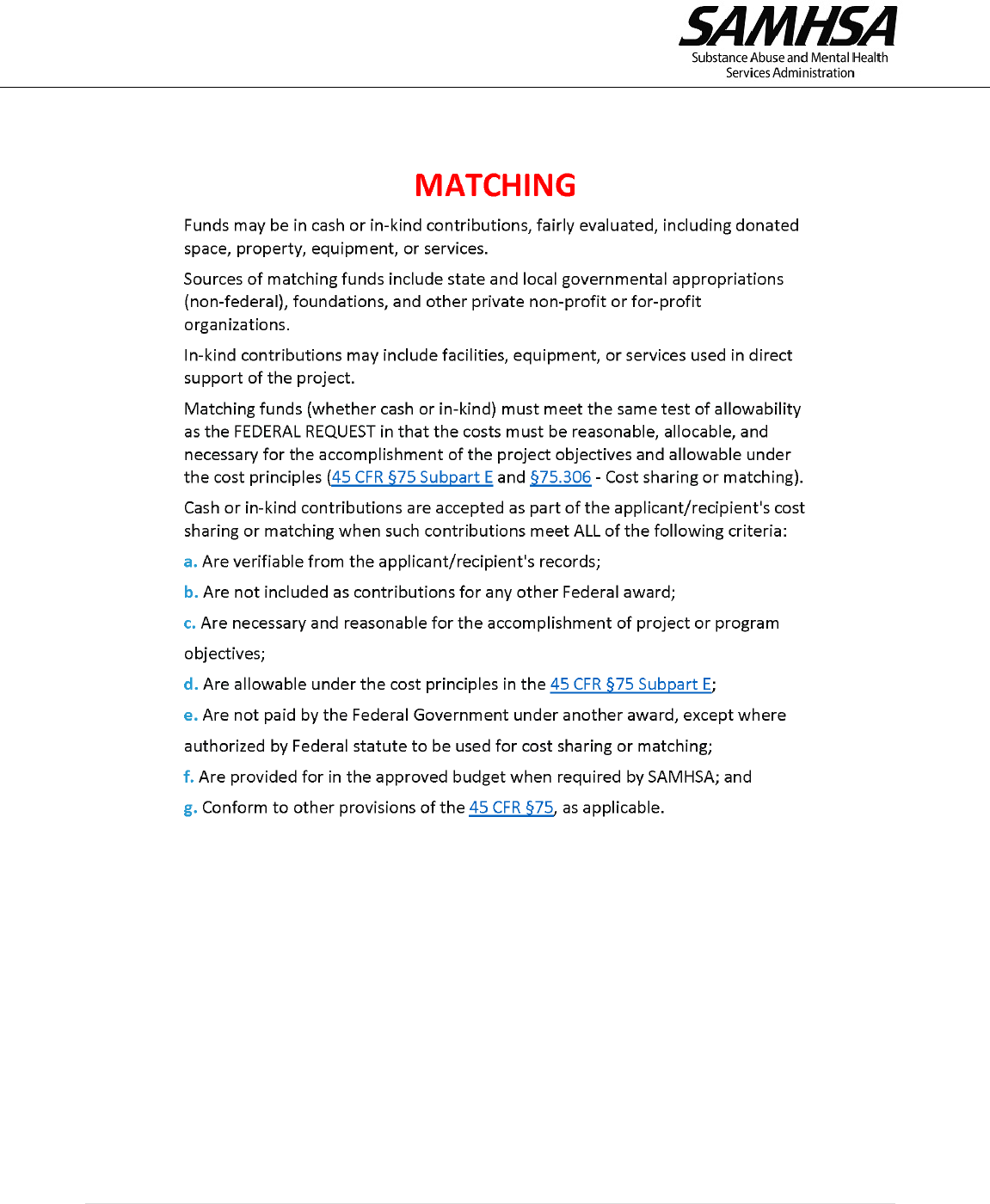

MATCHING

Funds may be in cash or in-kind contributions, fairly evaluated, including donated space, property,

equipment, or services.

Sources of matching funds include state and local governmental appropriations (non-federal),

foundations, and other private non-profit or for-profit organizations.

In-kind contributions may include facilities, equipment, or services used in direct support of the project.

Matching funds (whether cash or in-kind) must meet the same test of allowability as the FEDERAL

REQUEST in that the costs must be reasonable, allocable, and necessary for the accomplishment of the

project objectives and allowable under the cost principles (45 CFR §75 Subpart E and §75.306 - Cost

sharing or matching).

Cash or in-kind contributions are accepted as part of the applicant/recipient's cost sharing or matching

when such contributions meet ALL of the following criteria:

1. Are verifiable from the applicant/recipient's records;

2. Are not included as contributions for any other Federal award;

3. Are necessary and reasonable for the accomplishment of project or program objectives;

4. Are allowable under the cost principles in the 45 CFR §75 Subpart E;

5. Are not paid by the Federal Government under another award, except where authorized by

Federal statute to be used for cost sharing or matching;

Information on Matching

26 | Page 2/10/2023

SAMHSA Detailed Budget and Narrative Template User Guide

6. Are provided for in the approved budget when required by SAMHSA; and

7. Conform to other provisions of the 45 CFR §75, as applicable.

Select the applicable match option below. The default option is “NO.”

Match Required: NO

“NO” is the default option. The NON-FEDERAL MATCH data fields in the budget tables will NOT be

available to enter matching funds.

Match Required: YES

Selecting “YES” will make the NON-FEDERAL MATCH data fields available to enter matching funds.

The Match Ratio section will be hidden if NO is selected for Match Required.

Match Ratio stated in the NOFO:

The match ratio for the Budget Year as stated in the NOFO, Section III-2 – Cost Sharing and Matching

Requirements.

First $x

Enter the first number in the match ratio statement for the budget year as stated in the NOFO, Section

III-2 – Cost Sharing and Matching Requirements.

Second $x

Enter the second number in the match ratio statement for the budget year as stated in the NOFO,

Section III-2 – Cost Sharing and Matching Requirements.

If the NOFO requires cost sharing or matching, you should enter the amount of matching funds in NON-

FEDERAL MATCH and describe in the narrative justification the funding/resources, whether cash or in-

kind contributions, that your organization will provide and any contributions you expect to receive from

the State or other sources.

Matching funds (whether cash or in-kind) must meet the same test of allowability as the FEDERAL

REQUEST in that the costs must be reasonable, allocable, and necessary for the accomplishment of the

28 | Page 2/10/2023

SAMHSA Detailed Budget and Narrative Template User Guide

A. Personnel

A. Personnel

All positions shown must be relevant and allowable under the project. You must include in this section

the key positions identified in Section I-2 of the NOFO; however, if the key positions will be held by

consultants or subrecipients, show them in F. Contractual.

The Project Director (PD) shown must be the same PD identified in the SF-424 section 8f.

SALARIES OF INDIRECT OR FACILITIES AND ADMINISTRATION (F&A) PERSONNEL

Salaries of administrative and clerical staff should normally be covered by indirect (F&A) costs (45 CFR

§75.413c).

Examples of Indirect/Facilities and Administrative Personnel include, but are not limited to,

Administrative Assistants, HR Specialists, Accountants, and Clerical Assistants

EXECUTIVE LEVEL II SALARY LIMITATION

Recipients are restricted from using funds awarded under a SAMHSA grant, cooperative agreement, or

applicable contract to pay the direct salary of an individual at a rate in excess of the Executive Level II of

the Federal Executive Pay Scale. For the purposes of the salary limitation, the direct salary is exclusive of

fringe benefits and indirect (F&A) costs. The Office of Personnel Management will release new salary

levels for the Federal Executive Pay Scale annually. Please refer to the SAMHSA Standard Terms and

Conditions for the current Executive Level II salary level.

The salary limitation applies to organization staff and to all contracts and subawards, but does not apply

to consultants; however, consultant payments must meet the test of reasonableness and be consistent

with institutional policy for rates paid to consultants, regardless of funding source.

An individual's institutional base salary is not constrained by the legislative provision for a limitation of

salary. The rate limitation simply limits the amount that may be awarded and charged to SAMHSA

grants, cooperative agreements, and contracts. For individuals whose salary rates are in excess of

Executive Level II, the applicant/recipient, contractor or subrecipient may pay the excess from non-

Federal funds.

Guidance on Calculating Salaries and Paid Time Off (PTO)

Guidance on the Executive Level II Salary Limitation

Guidance on Calculating Salaries and Paid Time Off (PTO)

Guidance on the Salaries of Indirect or F&A Administrative and Clerical Staff

29 | Page 2/10/2023

SAMHSA Detailed Budget and Narrative Template User Guide

After answering important questions, such as: (1) who from your organization will work on the grant;

(2), their authorized pay; and (3) level of effort needed, you will also need to identify whether you are

budgeting using hourly rates or percentages of annual salary and how your organization recovers paid

absences (vacation, holiday, sick, and other paid leave). You will be prompted below to tell us if you will

be using hourly rates vs. annual salaries. Regarding recovery of paid absences, there are two (2)

possibilities: (1) you recover paid absences as part of a rate; or (2) you recover paid absences as part of

salaries and wages.

You recover paid absences as part of a rate.

This means you recover paid absences: (a) through a federally-approved fringe benefit or indirect cost rate,

including the de minimis rate; or (b) through an internally-calculated fringe benefit rate. If paid absences

are recovered through a rate, the number of hours and hourly rate, or percentages and annual salary, and

the resulting budget request using either option, is calculated as shown in the examples below under

Hourly Rate and Annual Salary.

Example 1 - Budget Calculations Using an Hourly Rate:

If an employee receives 240 hours of paid absences each year as a fringe benefit (vacation-120; holiday-

80; sick-40), the maximum number of hours budgeted for the grant cannot exceed 1,840 hours (2,080 –

240 = 1,840). NOTE: the maximum number of hours budgeted on the grant will necessarily be less than

the industry-standard 2,080 hours which denotes total, possible annual hours. Instead, up to 1,840

hours can be recovered as a direct cost from the grant with the remaining 240 paid absence hours

recovered through the rate. Therefore, if an employee’s Annual Salary is $75,000, the Hourly Rate

should be $36.06 ($75,000 / 2080 = $36.06). If the employee is budgeted to work full-time on the grant,

the salary requested will be $66,350 (1,840 hours x $36.06 = $66,350). The remaining $8,650 of salary

($75,000 - $66,350) relates to paid absences and will be recovered through the rate (240 hours x $36.06

= $8,650).

Example 2 - Budget Calculations Using Percentages of Annual Salary:

If an employee receives 240 hours of paid absences each year as a fringe benefit (vacation-120; holiday-

80; sick-40), the maximum percentage of annual salary budgeted for the grant cannot exceed 88.5

percent (2,080 -240 = 1,840/ 2,080 = 88.5 percent, rounded). Up to 88.5 percent of annual salary can be

recovered as a direct cost from the grant with the remaining 11.5 percent related to paid absences and

recovered through the rate. Therefore, if an employee’s Annual Salary is $75,000 and budgeted to work

full-time on the grant, the salary requested will be $66,350 ($75,000 x 88.5% = $66,350). The remaining

$8,650 of salary ($75,000 - $66,350) relates to paid absences and will be recovered through the rate.

You recover paid absences as part of salaries and wages.

This likely means: (a) you have a federally approved indirect cost rate that is directing you to recover

paid absences as part of salaries and wages; or (b) you elected the de minimis rate to recover indirect

costs, but chose to recover paid absences, not as part of the de minimis rate, but rather as part of

salaries and wages. If paid absences are recovered as part of salaries and wages, you may not use

percentages of effort and annual salaries to budget salaries. Rather, you must use hourly rates to

calculate budgeted salaries. You must also use hourly rates in your accounting system when recovering

30 | Page 2/10/2023

SAMHSA Detailed Budget and Narrative Template User Guide

incurred salary costs related to employees’ efforts on federal grants. The use of hourly rates is

necessary because paid absences must be “loaded” into salaries and wages as demonstrated in the

following example:

Example:

An employee receives 240 hours of paid absences each year as a fringe benefit (vacation-120; holiday-

80; sick-40). Paid absences must be “loaded” into the employee’s labor rate to achieve a fair and

equitable allocation of paid absence costs distributed across all cost centers on which the employee

works (2,080 – 240 = 1,840). NOTE: 2,080 hours represents maximum possible annual hours. Therefore,

if an employee’s Annual Salary is $75,000, the Hourly Rate should be $40.76 ($75,000 / 1,840 hours). If

the employee is budgeted to work 700 hours on the grant, the salary requested will be $28,532 (700

hours x $40.76).

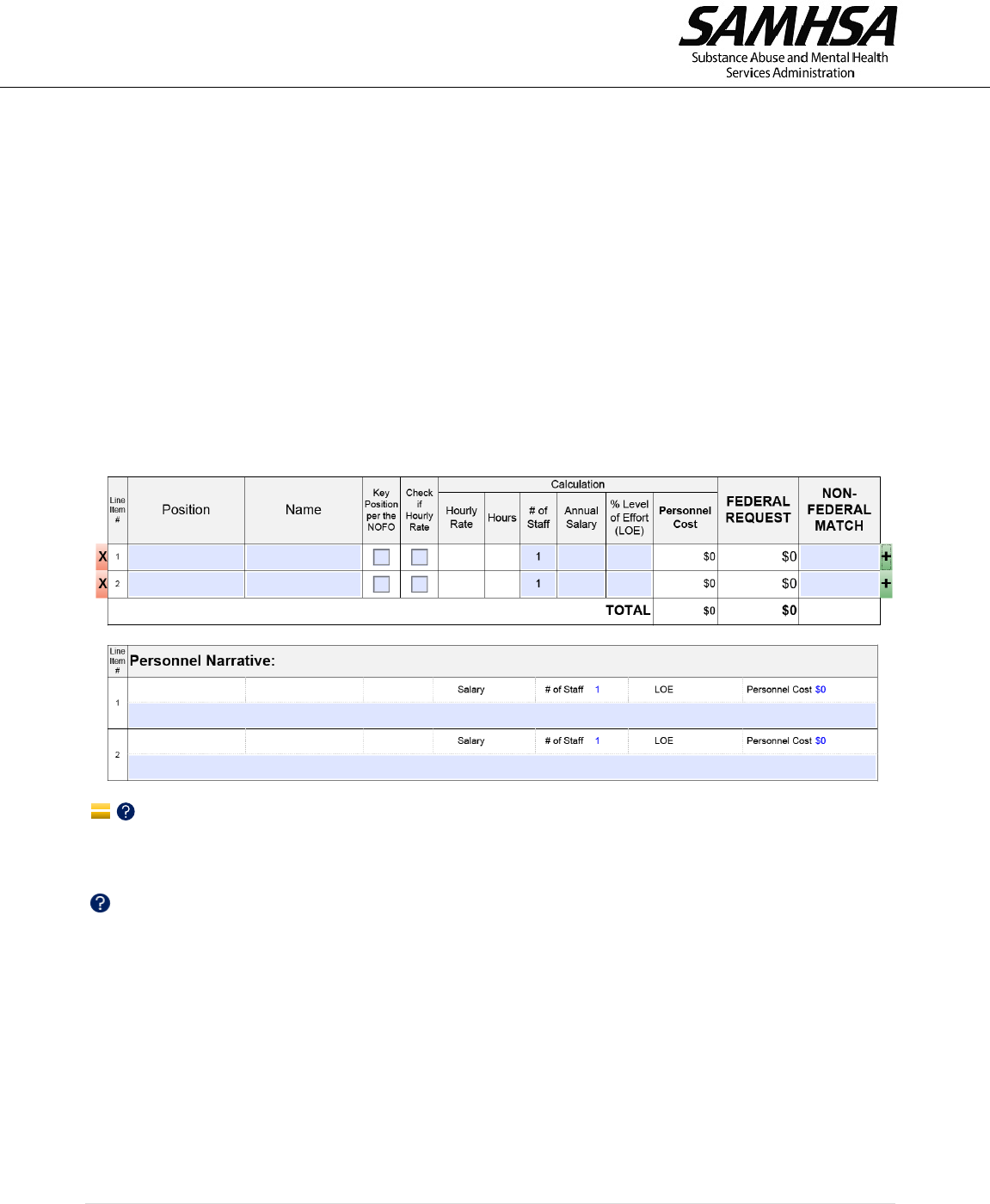

Personnel Cost Table

Line Item #

An auto-generated number.

Position:

Enter the title of the position. Ensure the position titles for key personnel are identical to those stated in

the NOFO.

The position must be relevant and allowable under the project.

Show only positions held by full-time, part-time, or temporary employees of your organization in A.

Personnel.

Show consultants, contractors, subrecipients and other persons who are NOT employees of your

organization in F. Contractual.

31 | Page 2/10/2023

SAMHSA Detailed Budget and Narrative Template User Guide

Note that the salaries of indirect or facilities & administration (F&A) administrative and clerical staff are

usually covered by your indirect costs requested in J. Indirect Charges.

Name:

Enter the name of your organization’s employee in the position. If the position is vacant, state “vacant”

or “TBD” and indicate the anticipated hire date or time frame for hire (e.g., 3 months, 4 months etc.).

If the position is held by someone who is not a full-time, part-time, or temporary employee of your

organization, show the position in F. Contractual.

Key Position per the NOFO:

Check the box if the position is identified as key personnel in the NOFO.

Personnel in key positions require prior approval by SAMHSA after review of qualifications and position

descriptions.

Check if Hourly Rate:

Check the box if you would prefer to use Hourly Rate instead of Annual Salary.

Checking this box will remove values entered in Annual Salary and LOE.

Un-checking this box will remove values entered in Hourly Rate and Hours.

Hourly Rate:

Enter the actual or projected Hourly Rate.

The Hourly Rate must not exceed the Executive Level II salary. The Office of Personnel Management will

release new salary levels for the Federal Executive Pay Scale annually. Please refer to the SAMHSA

Standard Terms and Conditions for the current Executive Level II salary.

The Hourly Rate must be reasonable for the services provided and conform to the established policy of

the organization, consistently applied to both federal and non-federal activities.

Hours:

Enter the number of hours.

Hours must not exceed 2,080, which is typically full-time status or 100% level of effort for an individual.

# of Staff:

Enter the number of organizational staff. The default number of staff is 1.

Annual Salary:

32 | Page 2/10/2023

SAMHSA Detailed Budget and Narrative Template User Guide

Enter the actual or projected Annual Salary.

The Annual Salary must not exceed the Executive Level II salary. The Office of Personnel Management

will release new salary levels for the Federal Executive Pay Scale annually. Please refer to the SAMHSA

Standard Terms and Conditions for the current Executive Level II salary.

Annual salaries must be reasonable for the services provided and conform to the established policy of the

organization, consistently applied to both federal and non-federal activities.

% Level of Effort (LOE):

Enter the percentage of time the employee will work on the project during the budget period.

An employee’s total LOE across all active projects (including other Federal awards) must NOT exceed

100%.

Personnel Cost:

This is an auto-calculated field showing the personnel cost.

If Annual Salary and Percent LOE are entered: Personnel Cost = Annual Salary x Percent LOE x # of Staff

If Hourly Rate and Hours are entered: Personnel Cost = Hourly Rate x Hours x # of Staff

If the position will not be charged to the project and cost-sharing or matching is not required, identify

the position as an “in-kind” cost in the In-Kind Personnel table.

FEDERAL REQUEST:

The FEDERAL REQUEST equals the amount in Personnel Cost.

(Enter TOTAL in SF-424A Section B, line 6a, column 1)

NON-FEDERAL MATCH:

If matching is required by the NOFO, enter the amount of matching funds in NON-FEDERAL MATCH.

Note that the FEDERAL REQUEST will automatically decrease by the amount entered in NON-FEDERAL

MATCH.

In the Personnel Narrative section, indicate whether the matching funds are cash or in-kind

contributions and identify the source(s) of the matching funds, that is, specify the name of the state

and/or local governmental appropriations (non-federal), foundations, and other private non-profit or

for-profit organizations providing the matching funds.

(Enter TOTAL in SF-424A Section B, line 6a, column 2)

Personnel Narrative

Personnel Narrative

33 | Page 2/10/2023

SAMHSA Detailed Budget and Narrative Template User Guide

Describe the roles and responsibilities of each position and explain how they relate to achieving the

goals and objectives of the project.

For employees whose Annual Salaries or Hourly Rates exceed the Executive Level II Salary Limitation,

provide their actual institutional base salaries or hourly rates.

Individuals cannot exceed 100% level of effort across all active projects including other federal awards.

If salaries of indirect or facilities & administrative and clerical staff are requested, then for each

individual proposed explain whether:

1. Administrative or clerical services are directly integral to the project or activity;

2. Individuals involved can be specifically identified with the project or activity; and

3. The costs are not also recovered as indirect costs in J. Indirect Charges.

34 | Page 2/10/2023

SAMHSA Detailed Budget and Narrative Template User Guide

In-Kind Personnel

The In-kind Personnel Table will be hidden if YES is selected for Match Required.

In-Kind Personnel Check Box

If an employee will be working on the project, but the position will not be charged to the project, enter

the position in the In-Kind Personnel Table as an “in-kind” cost.

In-Kind Personnel

If an employee will be working on the project, but the position will not be charged to the project, enter

the position as an “in-kind” cost in the table below.

In-Kind Personnel Table

Line Item #

An auto-generated number.

Position:

Enter the title of the position. Ensure the position titles for key personnel are identical to those stated in

the NOFO.

The position must be relevant and allowable under the project.

Show only positions held by full-time, part-time, or temporary employees of your organization in this

table.

Show consultants, contractors, subrecipients and other persons who are NOT employees of your

organization in F. Contractual.

Note that the salaries of indirect or facilities & administration (F&A) administrative and clerical staff are

usually covered by your indirect costs requested in J. Indirect Charges.

Name:

35 | Page 2/10/2023

SAMHSA Detailed Budget and Narrative Template User Guide

Enter the name of your organization’s employee in the position. If the position is vacant, state “vacant”

or “TBD” and indicate the anticipated hire date or time frame for hire (e.g., 3 months, 4 months etc.).

If the position is held by someone other than a full-time, part-time, or temporary employee of your

organization, show the position in F. Contractual.

Key Position per the NOFO:

Check the box if the position is identified as key personnel in the NOFO.

Personnel in key positions require prior approval by SAMHSA after review of qualifications and job

descriptions.

Check if Annual Salary:

Check the box if you would prefer to use Hourly Rate instead of Annual Salary.

Checking this box will remove values entered in Annual Salary and LOE.

Un-checking this box will remove values entered in Hourly Rate and Hours.

Hourly Rate:

Enter the actual or projected Hourly Rate.

The Hourly Rate must not exceed the Executive Level II salary. The Office of Personnel Management

will release new salary levels for the Federal Executive Pay Scale annually. Please refer to the SAMHSA

Standard Terms and Conditions for the current Executive Level II salary.

The Hourly Rate must be reasonable for the services provided and conform to the established policy of

the organization, consistently applied to both federal and non-federal activities.

Hours:

Enter the number of hours.

Hours must not exceed 2,080, which is typically full-time status or 100% level of effort for an individual.

# of Staff:

Enter the number of organizational staff. The default number of staff is 1.

Annual Salary:

Enter the actual or projected Annual Salary.

36 | Page 2/10/2023

SAMHSA Detailed Budget and Narrative Template User Guide

The Annual Salary must not exceed the Executive Level II salary. The Office of Personnel Management

will release new salary levels for the Federal Executive Pay Scale annually. Please refer to the SAMHSA

Standard Terms and Conditions for the current Executive Level II salary.

The annual salary must be reasonable for the services provided and conform to the established policy of

the organization, consistently applied to both federal and non-federal activities.

% Level of Effort (LOE):

Enter the percentage of time the employee will work on the project during the budget period.

An employee’s total LOE across all active projects (including other Federal awards) must NOT exceed

100%.

In-Kind Personnel Narrative

In-Kind Personnel Narrative

Describe the roles and responsibilities of each position and explain how they relate to achieving the

goals and objectives of the project.

For employees whose Annual Salaries or Hourly Rates exceed the Executive Level II Salary Limitation,

provide their actual institutional base salaries or hourly rates.

Individuals cannot exceed 100% level of effort across all active projects including other federal awards.

37 | Page 2/10/2023

SAMHSA Detailed Budget and Narrative Template User Guide

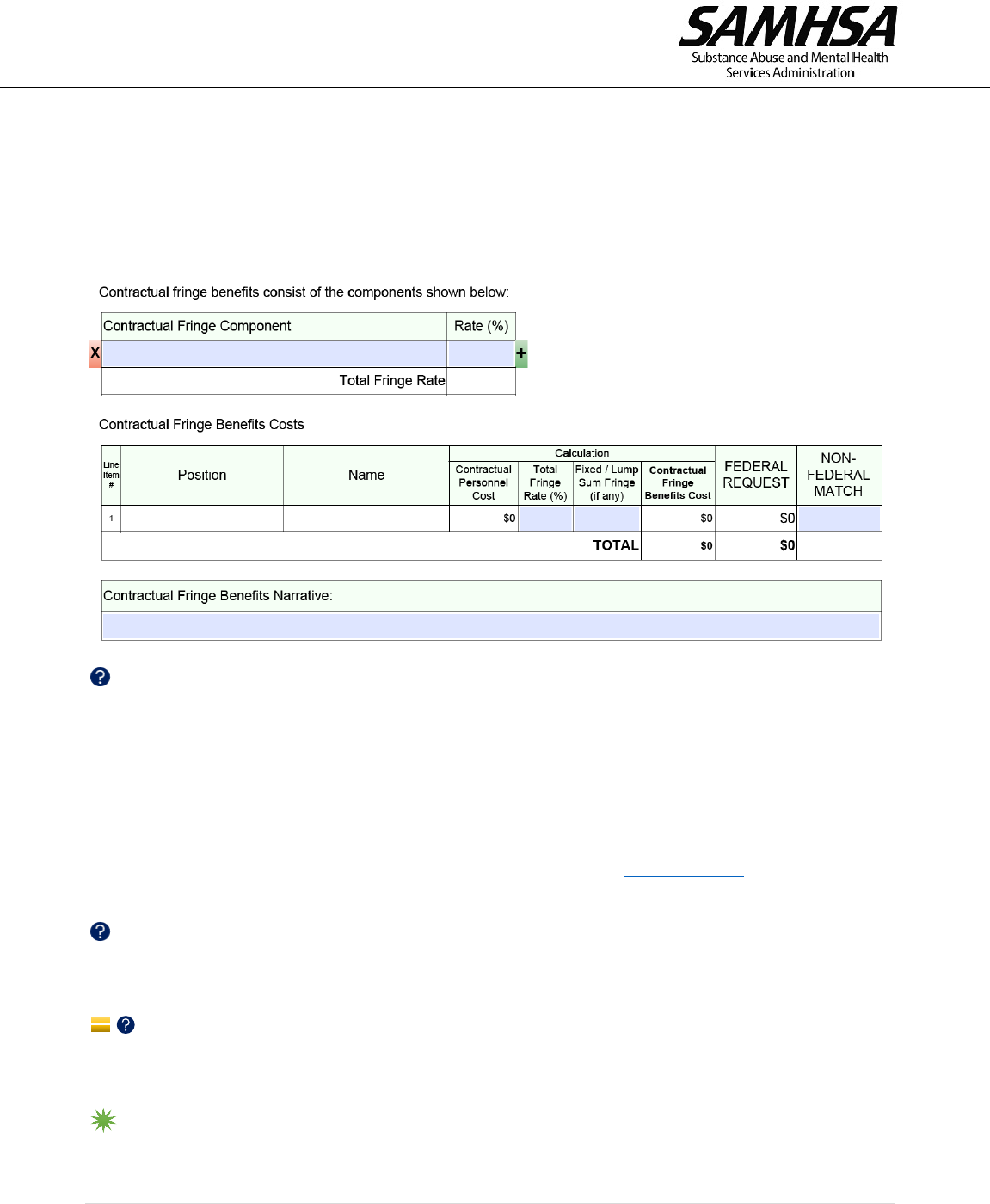

B. Fringe Benefits

B. Fringe Benefits

Fringe benefits are allowances and services provided to employees as compensation in addition to

regular salaries and wages.

Applicants/recipients with an approved indirect cost (IDC) rate agreement must ensure that the

treatment of fringe benefits including the fringe benefits rate base, fringe benefit components, and the

applicable fringe benefits rate are consistent with the rate agreement.

Fringe benefits charged to an award must comply with HHS regulations at 45 CFR §75.431

(Compensation – fringe benefits). The cost of fringe benefits in the form of employer contributions or

expenses for social security; employee life, health, unemployment, and worker's compensation

insurance (except as indicated in §75.447 – Insurance and indemnification); pension plan costs; paid

absences; and other similar benefits are allowable, provided such benefits are reasonable and are

required by law, organization-employee agreement, or an established written policy of the

applicant/recipient organization.

Guidance on Calculating Salaries and Paid Time Off (PTO)

It is unnecessary to populate the Fringe Benefits Components Table in the following situations:

1. Your organization has a federally approved fringe benefit rate. Populate the Fringe Component

column with the following description, “Fringe benefits are recovered through a federally

approved fringe rate.” Then, in the Rate (%) column, provide the federally approved rate

percentage. It is unnecessary to populate the Fringe Benefits Narrative box.

2. Your organization has a federally approved indirect cost rate (including a de minimis rate) and all

fringe benefits listed above (see above definition) are recovered through the indirect cost or de

minimis rate. Leave the Fringe Component and Rate (%) columns blank. In the Fringe Benefits

Narrative box, include the following description, “Fringe benefits are not separately requested,

but rather are recovered through a federally approved indirect cost rate or de minimis rate.”

Only populate the Fringe Benefits Components Table in the following situations: