Module 2: Modified

Adjusted Gross

Income (MAGI)

Office of Medicaid Eligibility Policy

Medicaid Eligibility and Community Support

2022

MAGI Introduction

MAGI Methodology

Modified adjusted gross income (MAGI) is how income is

calculated to determine eligibility for MAGI-based Washington

Apple Health (Medicaid) programs, and the Children’s Health

Insurance Program (CHIP or Apple Health for Kids with

Premiums).

Generally, the MAGI calculation is determined by calculating an

individual’s adjusted gross income (AGI) as determined by the

Internal Revenue Code (IRC), with a few modifications.

Adjusted

Gross Income

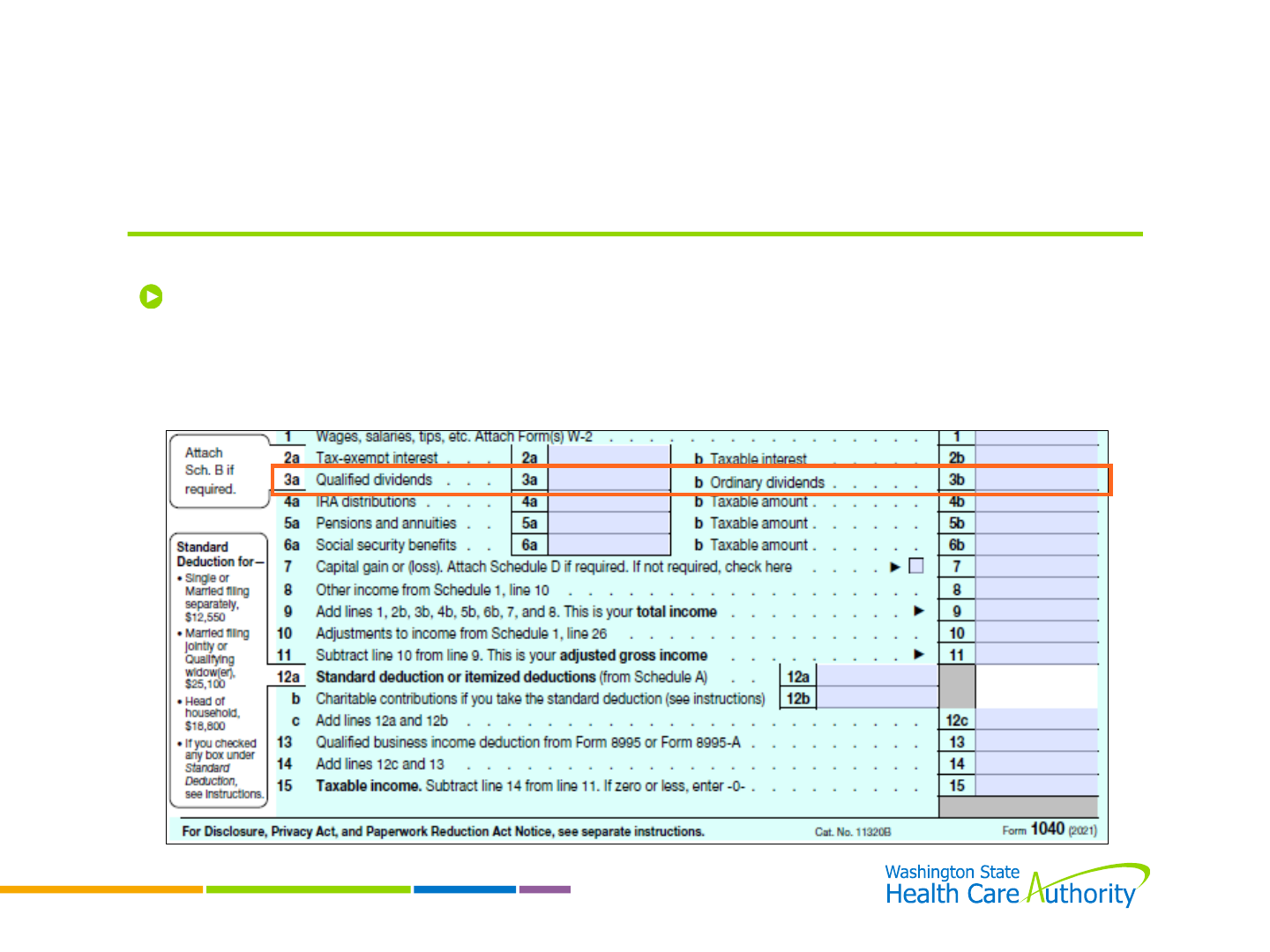

Adjusted gross income

(AGI) is the total gross

taxable income minus

any IRS allowable

adjustment(s).

The adjusted gross

income is reported on

line 11 of Form 1040.

What Turns AGI Into MAGI?

MAGI is the adjusted gross income (AGI) increased by:

Interest – Any amount of interest received or accrued by the

taxpayer during the taxable year which is exempt from tax.

Social Security and Railroad Retirement – Any amount of Title

II Social Security income or Tier 1 Railroad Retirement income,

which is excluded from gross income under Section 86 of the IRC.

Foreign Income – Any amount excluded from gross income

under Section 911 of the IRC.

What Turns AGI Into MAGI?

MAGI does not include:

Educational Income – Scholarships or fellowship grants used for

educational purposes, as described in WAC 182-509-0335.

American Indian / Alaska Native Income – Most sources of income

received by American Indian/Alaskan Native individuals, as described

in WAC 182-509-0340.

Lump Sums – Income received as a lump sum, as described in WAC

182-509-0375, is counted as income only in the month it is received.

Income of Tax Dependents or Children Age 18 or Younger –

Some income received by tax dependents, or children age eighteen

or younger, as described in WAC 182-509-0360, is excluded if it does

not meet the tax filing threshold.

Deductions

The AGI calculation

includes certain

allowable deductions

that reduce the total

gross income.

These deductions

follow IRS rules.

Some deductions may

have annual limits or

are variable.

5% FPL Income Disregard

Countable MAGI is reduced by an amount equal to five

percentage points of the federal poverty level (FPL) based

on the household size to determine net income.

Exception: Recipients of Parent/Caretakers) Medical (N01) do not

receive this income disregard unless they are receiving Medicare.

See WAC 182-509-0300

MAGI Calculation

Gross Countable Income

- Allowable IRS Deductions

- 5% FPL Income Disregard

Total MAGI

Point-In-Time Methodology

Point-In-Time Income

Definition: Income that is received or likely to be received

in the month a person applies, renews coverage, or has a

redetermination of Apple Health coverage.

A point-in-time calculation can be used to determine a

person’s countable income.

See WAC 182-509-0310

Point-In-Time Calculation

The following calculations are used to determine a

person’s countable income when they are paid more

than once per month:

Weekly: multiply weekly expected income by 4.3.

Every other week: multiply expected income by 2.15.

Twice per month: multiply expected income by 2.

For those paid less than once a month, individuals can

use an average to calculate monthly income.

Monthly average – total income for a period divided by the # of

months in the timeframe.

Point-In-Time Calculation

When reporting income for individuals whose income

varies seasonally, individuals can choose to use either the

point-in-time methodology or by calculating the

monthly average.

Example: Fishers who work seasonally during the summer.

Earned Income

Earned Income

Earned income is income received from working, which may

include:

Wages;

Salaries;

Tips;

Commissions;

Bonuses; and

Profits from self-employment activities.

The taxable gross amount of earnings are used to determine

eligibility.

See WAC 182-509-0330

Self-Employment Income

Self-Employment Income

Self-employment income is earned by an individual, from:

Running a business;

Performing a service;

Selling items that are made; or

Reselling items with the intent to make a profit.

This income can be earned if the person is:

Performing a trade;

In business as a sole proprietor or an independent contractor;

Member of partnership that carries on a business; or

Otherwise in business for themselves.

See WAC 182-509-0365

Determining Self-Employment

Self-employment income is determined using an

individual’s most recent federal tax return, unless:

The individual does not file taxes;

The individual has not been in business long enough to have filed

a tax return for their new business; or

The most recent tax return is not a good reflection of their current

income.

If any of these conditions apply, individuals can report

their income using their most recent three-month profit

and loss statement.

Calculating Self-Employment

Net self-employment is used to determine eligibility for

MAGI Apple Health programs.

Gross Self-Employment Income

- Allowable IRS Business Expenses

Net Self-Employment Income

Self-Employment Income

Types of self-employment for individuals can include:

Babysitting.

Drive for Uber or Lyft.

Rent out a room of their home.

Resell items on Ebay.

Own their own daycare.

Partner in a medical practice.

Shareholders in their own corporation.

Sole Proprietorship

Description

This common business structure is simple to form

and operate. The individual is in business alone and

personally liable for all debts incurred by the

business.

Can include royalties and some limited liability

companies (LLC).

Business

required to file taxes?

No

IRS Tax Form(s)

& Location

Schedules

C and Schedule 1, line 3

Common

Examples

Babysitters, bookkeepers, real estate agents,

shopkeepers, private contractors, translators, truck

drivers, insurance agents, etc.

Sole

Proprietorship

Tax Forms

Business profit or loss is

calculated and reported

using Schedule C.

The total business profit

or loss is reported on

Schedule 1 line 3, along

with other income and

adjustments to income.

Partnership

Description

Income received from a business when a relationship

exists between two or more persons who

join to

carry on a trade or business. The different types of

partnerships can include, general partnership, limited

partnership, limited liability partnership (LLP), and

limited liability limited partnership (LLLP).

Business

required to file taxes?

Yes

IRS Tax Form(s)

& Location

Form 1065, Schedules E, and Schedule 1, line 5

Common

Examples

Real estate businesses, dance studios, medical and

legal practices, marketing firms, small retail stores,

etc.

Partnership

Tax Forms

Partnership income is

calculated on Schedule E.

The total partnership

income is reported on

Schedule 1 line 5, along

with other income and

adjustments to income.

Corporation

Description

Has a more complex business structure. Shareholders or

owners of the corporation are employees of the

corporation that receive wages and can receive additional

income from the corporation. The types of corporations

can be C corporations, S corporations, non

-profit, and

some limited liability companies (LLCs).

Business

required to file taxes?

Yes

IRS Tax Form(s)

& Location

Form

1120/ 1120S,

Schedule E, Schedule 1, line 5. Wages

will show on line 1 of Form 1040.

Common

Examples

Gas stations, general stores, real estate businesses,

insurance agencies, chiropractors, dentists, etc.

Corporation

Tax Forms

Income from dividends or

the corporation’s gains or

losses is reported on various

tax forms, but notably listed

on line 5 of Schedule 1.

Employees of a corporation

receives wages, which

would be shown on line 1

of Form 1040.

Rental Income

Description

Income or services received from the use of real

estate or personal property. This can include

royalties (typically property royalties).

Business

required to file taxes?

No

IRS Tax Form

& Location

Schedule E and Schedule 1, line 5

Common

Examples

Renting

a room out of your house, leasing part

of

your property as storage, having numerous

rental homes, etc.

Rental Income

Tax Forms

Rental income is filed

on Schedule E and

reported on line 5 of

Schedule 1.

Royalty income from

property royalties are

similarly reported

using the same forms.

Farming

Description

Income received from farming activities.

Business

required to file taxes?

No

IRS Tax Form

& Location

Schedule F and Schedule 1, line 6

Common

Examples

Income received from dairy, poultry, fish

farming or operating a plantation, ranch, range,

orchard or grove.

Farming Tax

Forms

Farming income is filed

on Schedule F and

reported on line 6 of

Schedule 1.

Does not include income

received from tribal

activities since that is not

taxable.

Unearned Income

What is Unearned Income?

Unearned income is received from a source other than employment.

Common examples of unearned income include:

Title II Social Security benefits;

Unemployment compensation;

Interest income;

Pensions, annuities, and IRAs;

Dividends;

Military retirements;

Alimony; and

Rental income.

See WAC 182-509-0325

Title II Social Security Benefits

Social Security benefits are payments administered by the

Social Security Administration (SSA) based on age, survivor

status, or having a disability.

Although Title II Social Security benefits are typically exempt from

a person’s adjusted gross income for tax purposes, this income is

counted for MAGI-based Apple Health.

Countable Title II Social Security benefits include:

Retirement benefits;

Disability benefits (SSDI);

Dependent benefits; and

Survivor benefits.

SSDI vs. SSI

Sometimes, there is confusion between Title II Social Security Disability

Insurance Benefits (SSDI), and Supplemental Security Income (SSI).

Both are disability payments received from the Social Security

Administration, but only SSDI payments are countable income for

MAGI-based Apple Health.

SSI recipients automatically receive Apple Health Classic Medicaid and

are not eligible for MAGI-based Apple Health coverage.

SSDI (Countable)

SSI (Non

-countable)

This benefit is paid based on age or

disability, and the amount received is

based on the insured person’s lifetime

earnings and contributions to Social

Security taxes (FICA).

Recipients become Medicare eligible

after receiving SSDI for two years.

This benefit is paid to disabled adults or

children with limited income and

resources.

Benefit amounts are standardized

Eligible for Classic Medicaid (S01).

Title II SSDI

Benefits

Social Security benefits

are reported on line 6a of

Form 1040.

Only the taxable

amount is listed on line

6b, but all benefits are

countable.

SSDI recipients receive an

annual benefits letter that

can also be used to verify

income.

Dividend Income

Dividends are the distribution of property paid out to

shareholders of a corporation, or to individuals with an interest

in an estate, trust, S corporation, or other associations that are

taxable as a corporation.

Though most dividends are paid in cash, shareholders could

receive other property, services, stocks, etc., in lieu of cash.

Dividends are taxable income and countable for MAGI

eligibility.

Dividends

Qualified and ordinary dividends are listed separately on the

1040 tax form, but the total dividend amount is included on

line 3b.

Pensions, Annuities, and IRAs

Pensions, annuities, and individual retirement accounts (IRAs)

are fixed sums of money paid out to an individual for the rest

of their life.

Examples of this type of income include 401K distributions, pensions,

annual lottery payouts, etc.

Generally, these income types are taxable and countable for

MAGI eligibility

Though there are exceptions, the rules are complicated and

depend on the individual’s circumstances.

Pensions, Annuities, and IRAs

IRA distributions are listed on line 4a and 4b of Form 1040. Use the taxable

amount on line 4b.

Pensions and annuities are listed on line 5a and 5b of Form 1040. Use the

taxable amount on line 5b.

Capital Gain or Loss

The financial gain or loss from the sale or exchange of a capital

asset.

A capital asset includes physical property, such as your home or

car, as well as investment property such as stocks and bonds.

The frequency of this income type depends on the individual’s

circumstances. The income can be received at one time or

expected to be ongoing and continue over a length of time.

Capital Gain or Loss

Countable capital gains and losses:

Sale of assets for a business that is still operating.

Sale of a house by an individual who owns numerous homes.

Sale of stocks, shares, or other investment property.

The capital gain or loss is ongoing.

Non-countable capital gains and losses:

Sale of assets for a business that is no longer operating.

One-time sale of home or property.

The capital gain or loss is a one-time occurrence.

Capital Gains and Losses

Capital gain or loss are listed on line 7 of Form 1040.

Interest Income

This income is earned from investments that pay interest,

such as savings accounts, money market accounts, or

certificates of deposit.

For the purposes of MAGI eligibility, all interest income

received or accrued is countable, regardless of whether it

is taxable or not.

Interest Income

Tax-exempt interest is listed on line 2a of Form 1040, but for

MAGI-based Apple Health programs all interest income is

countable. Use the amounts listed in boxes 2a and 2b.

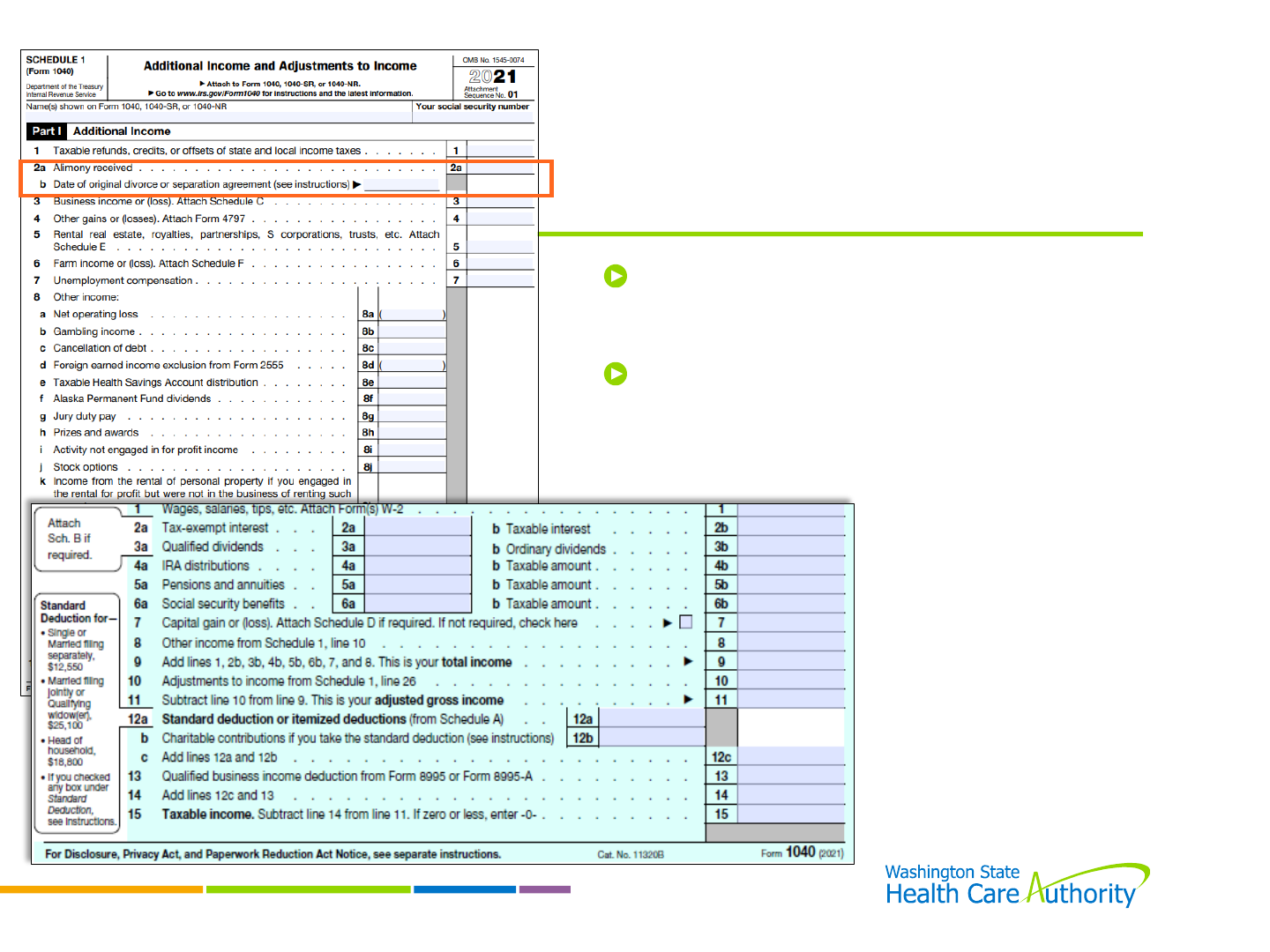

Alimony Income

This income is received from a current or former spouse,

as a result of a divorce decree or separation agreement.

Does not include voluntary payments or child support payments.

Alimony income is taxable and countable for purposes of

determining MAGI eligibility.

Alimony agreement must be unmodified and established by

December 31, 2018.

Alimony Income

Alimony income is listed on line 2a

on the Schedule 1.

This income is included in the total

adjustments included on line 8 of

Form 1040.

Unemployment Compensation

Unemployment compensation is temporary income received,

under the compensation laws, to replace lost wages for

workers who have become involuntarily unemployed.

Benefits are paid to the individual by the state or by the District

of Columbia (for DC residents).

All unemployment compensation benefits received are

countable for MAGI-based Apple Health.

Unemployment

Compensation

Unemployment is listed on line 7

of the Schedule 1.

This income is included in the total

adjustments included on line 8 of

Form 1040.

Other Countable Income or Loss

Other sources of less-common countable income may include:

Per capita income;

Net-operating loss;

Gambling, lottery, or raffle winnings;

Jury duty pay;

Rewards including Nobel, Pulitzer, or other prizes;

Strike or lockout benefits;

Whistleblower’s award;

Compensation for donations such as blood, plasma, egg,

embryo, or sperm; and

Unearned income-in-kind.

Other Income

The total other income is listed

on line 9 of the Schedule 1

Form.

Line 9 is the total of lines 8a-8z,

which lists the common types

of ‘Other Income.’

This income is included in the

total adjustments included on

line 8 of 1040 Form.

Foreign Income

Foreign Income

Foreign income that is typically excluded from a person’s AGI under

Section 911 of the IRC is countable income for MAGI-based Apple

Health.

This can include any earned or unearned income from a foreign

source, including:

Wages;

Salaries;

Pensions;

Annuities; and

Housing.

See WAC 182-509-0300

Non-Countable Income

Non-countable Income

For the purposes of MAGI eligibility for Apple Health, some types

of income are not counted.

Income that is not countable may include:

Bona fide loans;

Federal income tax returns;

Child support payments;

Title IV-E and state foster care maintenance payments;

Needs-based assistance from other agencies;

Veteran’s disability and educational benefits;

Non-taxable time loss benefits / L&I benefits; and

Death benefits from life insurance.

See WAC 182-509-0320

Educational Income

Educational Benefits

Income from educational assistance programs that is used for

educational purposes, and not living expenses, is not

countable.

These can include programs administered by:

Title IV of the Higher Education Amendments;

Department of Education;

Department of Veteran’s Affairs;

Bureau of Indian Affairs; and

Carl D. Perkins Vocational and Technology Education Act.

See WAC 182-509-0335

Educational Benefits

In addition, scholarships, awards, or fellowship grants used for

educational purposes, and not living expenses, are not

countable income for MAGI-based Apple Health programs.

Common examples include:

Pell grants;

State need grant;

GI bill payments; or

State and Federal work study.

American Indian/

Alaska Native Income

American Indian/Alaska Native

Income

For MAGI-based Apple Health, the following American Indian/

Alaska Native income is excluded.

Distributions from Alaska Native corporations or settlement trusts;

Distributions from property held in trust or within current or prior

boundaries of reservation;

Rents, leases, royalties, or natural resource extraction/harvest from

reservation or trust land, or from federally protected rights regarding

off-reservation hunting, fishing, gathering, or usage of natural

resources.

Payments related to culturally significant items, practices, or rights

that support traditional lifestyles;

Educational assistance from Bureau of Indian Affairs; and

Other exclusions as provided by federal law, regulation, or rule.

Income Types

Description

Counted

Per capita

- tribal

gaming

Payments made to tribal members from proceeds of tribal gaming.

Yes

Per capita

-

natural

resources

Payments made to tribal members from proceeds of the harvest or

sale of natural resources.

No

Needs based

payments

Payments paid to tribal members based on financial need. These can

include elder payments, child assistance payments, etc. Eligibility

requirements apply.

No

General welfare

payments

Payments paid to tribal members for the general welfare. These

payments can include elder payments, scholarships, etc.

No

Bureau of Indian

Affairs

Payments made

for educational assistance.

No

Earned

Income

Earned income that is related to the exercise of treaty rights,

extraction of natural resources on trust/reservation land, and sales of

culturally significant items.

This income can include working for a

tribal corporation as a fisherman, fish processor, accountant, and

even security guard.

No

Self

-employment

Income

Self

-employment income that is related to the exercise of treaty

rights, extraction

of natural resources on trust/reservation land, and

sales of culturally significant items

. This can include selling tribal

artwork, pottery, and, baskets.

No

Lump Sums

What is a Lump Sum?

A lump sum is a one-time payment received that is not

expected to continue or anticipated to be received again.

A lump sum is only countable if:

It is a countable source of income, and

It is received in the month of application

See WAC 182-509-0375

Lump Sum Scenario 1

Josephine applies for coverage in February. In March,

Josephine receives $12,000 from a fishing job in Alaska, where

she fishes twice a year. Is this income countable and a lump

sum?

Scenario 1 Answer

Yes, this is countable earned income. This is not a lump sum

since it is not received just one time but is ongoing or

anticipated to be received again. Additionally, since Josephine

is paid less than once per month, an average would be used to

calculate her monthly income at $1,000/mo.

Lump Sum Scenario 2

Maria applies for coverage in July. Maria sells her home in

that same month and receives a capital gain of $10,000.

This is Maria’s only home and she does not anticipate

any more home sales in the near future. Is this income

countable and a lump sum?

Scenario 2 Answer

Yes, since the capital gain is a lump sum payment this

income is countable in the month of application only.

This income is not countable in the ongoing months.

Income of Tax Dependents or

Children Age 18 or Younger

Income of Tax Dependents or

Children Age 18 or Younger

Income of tax dependents or children age 18 or younger is

only countable when it meets the tax filing threshold for a tax

filer (under 26 U.S.C. Sec 6012(a)(1)).

This rule applies regardless if the individual expects to file a

federal tax return or not.

Exception: Social Security income of tax dependents or children

age 18 or younger is not counted.

Income Threshold for Tax Dependents

or Children Age 18 or Younger

The 2021 tax filing threshold requirements:

Income

Type

Tax

Filing Threshold Limit

Unearned Income

$1,100

Earned Income

$12,550

Both

Earned/

Unearned

The larger of $1,100 or

earned (up to $12,200)

plus $350.

Deductions

Deductions

Deductions are IRS allowable adjustments to income that

that reduce an individual’s taxable income.

For MAGI-based Apple Health programs these

deductions are allowable and follow the same IRS rules

and limits.

Some deductions have yearly limits and others may vary.

Deductions are annualized through an individual’s certification

period.

See WAC 182-509-0300

Deductions

Tax Form

Deductions are listed on

Part II (page 2) of IRS

Form Schedule 1.

These deductions are

listed out on lines 11-25.

Educator Expenses

Definition

Deduction for unreimbursed educator expenses (e.g.,

books, supplies, and other equipment).

The individual must be a licensed educator (teaching

K

-12 and works 900+ hours per school year).

Deduction Limit

$300/year or

$25/month for

each educator

IRS Tax Form(s)

& Location:

Schedule 1, line

11

Other Document

Types

Receipts showing amounts paid out of pocket for

qualifying supplies.

Certain Business Expenses of U.S.

Reservists, Performing Artists, and

Fee-Based Government Officials

Definition

Deduction for U.S. reservists, performing artists, or fee

-

based government employees who have expenses

necessary for their job, including travel of more than 100

miles.

Max

Amount

Variable

IRS Tax Form(s) &

Location

Schedule 1, line 12

Other

Document

Types

IRS Form 2106 or 2106

-EZ; or

Receipts showing allowable expenses.

Health Savings Account

Definition

Deductions for pre

-

tax or tax deductible contributions made to

a health savings account while enrolled in a high

-deductible

health plan.

Max

Amount

Individual $3650/year or

$304.17/month

Family $7300/year or $608.33/month

Additional $1,000/year contribution is

allowed if the individual is age 55 or

older

IRS Tax

Form(s) &

Location

Schedule 1,

line 13

Other

Document

Types

Pre

-tax contributions show as

monthly amounts listed on wage

stubs.

Tax deductible

contributions show on IRS Tax Form 8889.

Moving Expenses for Armed

Forces

Definition

Deduction for moving expenses only for active

-duty

members of the Armed Forces that are ordered to move

because of a permanent change of station.

Max

Amount

Variable

IRS Tax Form(s)

& Location

Schedule 1, line 14

Other

Document

Types

IRS tax form 3903.

Self-Employment Tax

Definition

Deduction for tax paid to the federal government to fund

Medicare and Social Security for self

-employed individuals

who net more than $400 per year, or employees of

churches or church organizations with income of more than

$108.28 per year.

Max

Amount

Variable

IRS Tax Form(s)

& Location

Schedule 1, line 15

Other

Document

Types

Monthly or quarterly statement or receipt; or

IRS tax form Schedule SE.

Self-Employment Retirement Plan

Definition

Deduction for contributions made to a self

-

employment

retirement plan including SEP, Simple, or Qualified Plan

Max

Amount

Variable

IRS Tax Form(s)

& Location

Schedule 1,

line 16

Other

Document

Types

Statement or receipts showing contributions made to a

self

-employed retirement plan.

Self-Employment Health Insurance

Definition

Deduction for contributions made to self

-employment health

insurance plans.

Max

Amount

Variable; limited to net

profit of self

-

employment

business

IRS Tax Form(s)

& Location

Schedule 1,

line 17

Other

Document

Types

Statement or receipts showing premium payments made for

medical, dental, or qualifying long

-term care insurance

coverage.

Penalty on Early Withdrawal of

Savings

Definition

Deduction for penalty on withdrawal of funds from a

certificate of deposit or other deferred interest account

before maturity.

Max

Amount

Variable

IRS Tax Form(s)

& Location

Schedule 1, line 18

Other

Document

Types

IRS Form 1099

-INT box 2; or

Statement from financial institution.

Spousal Support / Alimony

Definition

Deduction for court ordered spousal support/alimony.

Does not include voluntary alimony payments or child

support payments.

This deduction is only allowable if the divorce decree was

established prior to January 1, 2019.

Max

Amount

Variable

IRS Tax Form(s)

& Location

Schedule 1, line 19a

Other

Document

Types

Court order with obligation amount.

Pre-Tax Retirement Account

Definition

Deduction for contributions made to a pre

-tax retirement

account.

Excludes Roth IRA or SIMPLE IRA contributions.

Max

Amount

Age 49

and

below $6,000/year

or

$500/month.

Age 50 or older $7,000/year or

$583.33/month.

IRS Tax

Form(s) &

Location

Schedule 1,

line 20

Other

Document

Types

IRS Form W

-2;

Wage stubs; or

IRS Tax Form 5498.

Student Loan Interest

Definition

Deduction for interest paid on student loans used for

qualifying educational expenses while attending an

educational institution. Principal payments are not deductible.

The loan payments must be for the individual, their spouse, or

their tax dependents (for tax filers) or their children in the

household (for non

-filers).

Max

Amount

$2500/year or

$208.33/month

IRS Tax Form(s)

& Location

Schedule 1, line 21

Other

Document

Types

IRS Form 1098

-E; or

Statement from the lender showing interest amount paid.

Resources

Resources

MAGI Income Part 1

http://hca.wa.gov/free-or-low-cost-health-care/i-help-

others-apply-and-access-apple-health/income-part-1

MAGI Income Part 2

https://www.hca.wa.gov/free-or-low-cost-health-care/i-help-

others-apply-and-access-apple-health/income-part-2

HCA Training & Education

http://hca.wa.gov/free-or-low-cost-health-care/i-need-

medical-dental-or-vision-care/stakeholder-training-and-

education

HCA Area Representatives

https://www.hca.wa.gov/assets/free-or-low-

cost/area_representatives.pdf

Contact Us

hcavolunt[email protected]

You’ve completed MODULE 2 of HCA

Community Based Training!

Please continue to MODULE 3 of the 7

module HCA Community Based

Training.

Congratulations!