Credit Risk, Credit Scoring, and

the Performance of Home Mortgages

Robert B. Avery, Raphael W. Bostic, Paul S. Calem,

and Glenn B. Canner, of the Board’s Division of

Research and Statistics, wrote this article. Jon

Matson provided research assistance.

Institutions involved in lending, including mortgage

lending, carefully assess credit risk, which is the

possibility that borrowers will fail to pay their loan

obligations as scheduled. The judgments of these

institutions affect the incidence of delinquency and

default, two important factors influencing profitabil-

ity. To assess credit risk, lenders gather information

on a range of factors, including the current and past

financial circumstances of the prospective borrower

and the nature and value of the property serving as

loan collateral. The precision with which credit risk

can be evaluated affects not only the profitability of

loans that are originated but also the extent to which

applications for mortgages that would have been

profitable are rejected. For these reasons, lenders con-

tinually search for better ways to assess credit risk.

This article examines the ways institutions

involved in mortgage lending assess credit risk and

how credit risk relates to loan performance.

1

The

discussion focuses mainly on the role of credit risk

assessment in the approval process rather than on its

effects on pricing. Although the market for home

purchase loans is characterized by some pricing of

credit risk (acceptance of below-standard risk quality

in exchange for a higher interest rate or higher fees),

mortgage applicants in general are either accepted or

rejected on the basis of whether they meet a lender’s

underwriting standards. The article draws on the

extensive literature that examines the performance of

home mortgages and the way that performance relates

to borrower, loan, and property characteristics.

An increasingly prominent tool used to facilitate

the assessment of credit risk in mortgage lending is

credit scoring based on credit history and other perti-

nent data, and the article presents new information

about the distribution of credit scores across popula-

tion groups and the way credit scores relate to the

performance of loans. In addition, the article takes a

special look at the performance of loans that were

made through nontraditional underwriting practices

and through ‘‘affordable’’ home lending programs.

DELINQUENCY AND DEFAULT

Delinquency occurs when a borrower fails to make a

scheduled payment on a loan. Since loan payments

are typically due monthly, the lending industry cus-

tomarily categorizes delinquent loans as either 30,

60, 90, or 120 or more days late depending on the

length of time the oldest unpaid loan payment has

been overdue.

Default occurs, technically, at the same time as

delinquency; that is, a loan is in default as soon as the

borrower misses a scheduled payment. In this article,

however, we reserve the term ‘‘default’’ for any of

the following four situations:

• A lender has been forced to foreclose on a mort-

gage to gain title to the property securing the loan.

• The borrower chooses to give the lender title to

the property ‘‘in lieu of foreclosure.’’

• The borrower sells the home and makes less than

full payment on the mortgage obligation.

• The lender agrees to renegotiate or modify the

terms of the loan and forgives some or all of the

delinquent principal and interest payments. Loan

modifications may take many forms including a

change in the interest rate on the loan, an extension of

the length of the loan, and an adjustment of the

principal balance due.

Because practices differ in the lending industry, not

all of the above situations are consistently recorded

as defaults by lenders. Moreover, the length of the

foreclosure process may vary considerably, affecting

1. Institutions that originate mortgages do not necessarily bear the

credit risk of the loans; the risk is often borne, at least in part, by a

mortgage insurer or by an institution that purchases mortgages. A

previous article in the Federal Reserve Bulletin assessed which insti-

tutions bear the risks of mortgage lending by examining the distribu-

tion of home loans originated in 1994 across the various institutions

participating in the mortgage market. See Glenn B. Canner and Wayne

Passmore, ‘‘Credit Risk and the Provision of Mortgages to Lower-

Income and Minority Homebuyers,’’ Federal Reserve Bulletin, vol. 81

(November 1995), pp. 989–1016.

the measured default rate. For these reasons, analyses

of default experiences can be difficult and are often

based on only a subset of actual defaults. Delinquen-

cies, on the other hand, are recorded contemporane-

ously and generally on a more consistent basis.

Therefore, delinquency data may provide a good

source of information for analysis, particularly for

evaluating the performance of newly originated loans.

and for identifying underperforming loans that

require greater attention.

The number of borrowers who become delinquent

on their loans is much greater than the number of

actual defaults. In some cases, delinquency results

from a temporary disruption in income or an unex-

pected expense, such as might arise from a medical

emergency. Many of these borrowers are able to

catch up on missed payments (and any associated late

payment fees) once their financial circumstances

improve. In other cases, lenders work with borrowers

to establish a repayment plan to bring payments back

on schedule.

Delinquencies, particularly serious ones, are often

resolved when the borrower sells the property and

uses the proceeds to pay off the loan. Even when the

proceeds of the sale are insufficient to fully repay the

mortgage obligation, the lender may accept a partial

payment to avoid foreclosure. Foreclosure is usually

a costly process. Lenders face a variety of expenses,

including interest accrued from the time of delin-

quency through foreclosure; legal expenses; costs to

maintain the property; expenses associated with the

sale of the property; and the loss that arises if the

foreclosed property sells for less than the outstanding

balance on the loan. Because foreclosure is so costly

to lenders, they may encourage delinquent borrowers

to sell their homes and avoid foreclosure even if the

proceeds of the sale would not cover the entire

amount owed on the loan.

2

This alternative is attrac-

tive to many borrowers because having a foreclosure

recorded on their credit histories is particularly

derogatory and will usually be a significant hindrance

in their future efforts to obtain credit.

Because default is costly, the interest rates lenders

charge incorporate a risk premium. To the extent that

the causes of default are not well understood, lenders

may charge a higher average price for mortgage

credit to reflect this uncertainty. Alternatively, lend-

ers may respond to this uncertainty by restricting

credit to only the most creditworthy borrowers. By

better distinguishing between applicants that are

likely to perform well on their loans from those that

are less likely to do so, lenders can ensure wider

availability of mortgages to borrowers at prices that

better reflect underlying risks.

Default also imposes great costs both on the bor-

rowers involved in the process and on society in

general. For borrowers, default ordinarily results in a

lower credit rating and reduced access to credit in the

future, a loss of assets, and the costs of finding and

moving to a new home. When geographically con-

centrated, defaults can also have a pronounced social

effect because they lower local property values,

reduce the incentives to invest in and maintain the

homes in the affected neighborhoods, increase the

risk of lending in those neighborhoods, and thus

reduce the availability of credit there.

THEORETICAL AND EMPIRICAL DETERMINANTS

OF

CREDIT RISK

Gaining a greater understanding of the factors that

determine mortgage loan delinquency and default has

been an objective of mortgage lenders, policy mak-

ers, and academics for decades. A better understand-

ing of these relationships holds the promise that

lenders can more accurately gauge the credit risk

posed by different applicants and increase the safety

and profitability of mortgage lending.

An extensive literature regarding the theoretical

and empirical determinants of mortgage credit risk

has developed over the past three decades.

3

This

literature emphasizes the important roles of equity in

the home and vulnerability to so-called triggering

events in determining the incidence of delinquency

and default. These studies have enhanced our under-

standing of the determinants of credit risk and have

established a better foundation for consistent and

effective mortgage lending.

Theoretical Determinants

of Mortgage Loan Performance

Most models of mortgage loan performance empha-

size the role of the borrower’s equity in the home in

the decision to default. So long as the market value of

2. For an assessment of the factors that influence the length of time

lenders are willing to allow mortgage loans to remain delinquent

before foreclosing, see Thomas M. Springer and Neil G. Waller, ‘‘A

New Look at Forbearance,’’ Mortgage Banking, December 1995,

pp. 81–84. For a discussion of the reduced losses to lenders associated

with alternatives to foreclosure, see John Bancroft, ‘‘Freddie Mac

Pushes Alternatives to Foreclosures,’’ Real Estate Finance Today,

November 6, 1995, pp. 12 and 18.

3. See Roberto G. Quercia and Michael A. Stegman, ‘‘Residential

Mortgage Default: A Review of the Literature,’’ Journal of Housing

Research, vol. 3, no. 1 (1993), pp. 341–79.

622 Federal Reserve Bulletin July 1996

the home (after accounting for sales expenses and

related costs) exceeds the market value of the mort-

gage, the borrower has a financial incentive to sell the

property to extract the equity rather than default.

4

‘‘Option-based’’ theories provide a framework for

understanding the relationship between equity and

loan performance; these theories view the amount of

equity accumulated in the property as the key deter-

minant of whether a borrower will default. Within

this framework, mortgage default is viewed as a put

option, in which the borrower has the right (option)

to transfer ownership of (put) the home to the lender

(through foreclosure or voluntarily) to retire the out-

standing balance on the loan. Borrowers will be

increasingly likely to exercise this option the further

the market value of the house falls below the value of

the mortgage. However, because of high transaction

and other costs (for example, moving expenses and

damage to the borrower’s credit rating resulting from

default), few borrowers would be expected to exer-

cise this option ‘‘ruthlessly’’ (that is, default as soon

as equity falls below zero).

5

Option-based theories of loan performance identify

a number of equity-related factors likely to influence

default rates. Included among these are the initial

loan-to-value ratio (the ratio of the loan amount to the

value of the property), which determines the amount

of equity at the time of loan origination; current and

expected future rates of home price appreciation,

which determine the direction, speed, and size of

changes in equity levels; the age of the loan, because

equity accumulates as payments on a mortgage

reduce the amount owed; and the term of the mort-

gage, because loans of shorter duration are amortized

more quickly. In addition, current mortgage interest

rates (relative to the rate on an outstanding loan)

influence the likelihood of default by affecting the

value of the mortgage to a borrower. For example, a

mortgage interest rate below current market levels is

a disincentive for the borrower to default because a

new mortgage would carry a higher rate.

While option-based theories emphasize the role of

equity in the home in determining loan performance,

other theories of loan performance additionally

emphasize the financial footing of borrowers and

their corresponding vulnerability to significant

adverse changes in their financial or personal circum-

stances, referred to as ‘‘triggering events.’’ In this

view, both negative equity and a triggering event

would be associated with most defaults. A triggering

event alone would not ordinarily cause a default

when a borrower has equity in a home; rather, the

borrower would sell the property and fully repay the

loan to keep the equity (net of transactions costs) and

avoid the adverse consequences of a default. On the

other hand, in the absence of a triggering event, a

borrower would not be expected to exercise the

default option ruthlessly because of the large (trans-

action and reputation) costs the borrower would bear.

A default, in this latter case, would occur only if, in

the owner’s view, the property’s value had declined

significantly and prospects for its near-term recovery

were poor.

Analysts who emphasize the role of triggering

events focus on adversities such as reductions in

income brought about by a period of unemployment.

Other events that may lead to repayment problems

include bouts of illness, which may result in both

large expenses and a disruption in income, and

changes in family circumstances, particularly divorce.

Measures of the borrower’s vulnerability to such

events include ratios of monthly debt payment to

income; the level of financial reserves available to the

borrower; measures of earnings stability, such as the

borrower’s employment history; and the borrower’s

credit history, which in part reflects the borrower’s

ability and willingness to manage debt payments in

the face of changing circumstances.

Option-based and triggering-event theories suggest

different relationships between delinquency and

default. In the options-based view, delinquency

occurs only as a precursor to default and would be

evident only among borrowers with substantial nega-

tive equity. Triggering-event theories view delinquen-

cies as related to an event and not necessarily to the

borrower’s level of equity. In this view, delinquen-

cies are not explicitly linked to default but can lead to

default if the triggering event is sufficiently severe

and the borrower has substantial negative equity in

the home.

Empirical Evidence on the Determinants

of Mortgage Loan Performance

Empirical investigations have found that both equity

and adverse changes in borrowers’ circumstances are

related to mortgage loan performance, as predicted

by theory. Studies consistently find that the level of

equity (whether proxied by the loan-to-value ratio at

4. The value of the mortgage is not determined solely by the

principal balance owed. It also depends on the relationship between

the rate of interest on the loan and the current market rate for

mortgages of similar duration.

5. In some states, lenders have the statutory right to seek deficiency

judgments against a borrower to try to recover losses incurred as a

consequence of default. Such statutory provisions tend to reduce the

ruthless exercise of the default option. In many instances, however,

borrowers do not have other assets available to cure deficiencies.

Credit Risk, Credit Scoring, and the Performance of Home Mortgages 623

the time of origination or by a contemporaneous

measure of the ratio) is closely related to both the

likelihood of default and the size of the loss in the

event of default.

A recent analysis of the performance of nearly

425,000 loans originated over the 1975–83 period

illustrates these relationships. The analysis found that

conventional mortgages with loan-to-value ratios at

origination in the range of 91 percent to 95 percent

default more than twice as frequently as loans with

loan-to-value ratios in the range of 81 percent to

90 percent and more than five times as often as loans

with loan-to-value ratios in the range of 71 percent to

80 percent (table 1). Loss severity (that is, loss to the

lender measured as a proportion of the original loan

balance) is about 40 percent higher for loans with

original loan-to-value ratios in the range of 91 per-

cent to 95 percent than it is with loans with loan-to-

value ratios in the range of 81 percent to 90 percent.

6

Additional evidence regarding the relationship

between loan-to-value ratios at time of origination

and mortgage default is provided in an analysis con-

ducted by Duff & Phelps Credit Rating Company.

They found that among thirty-year fixed rate mort-

gages, those with a 90 percent loan-to-value ratio are

230 percent more likely to default than loans with an

80 percent loan-to-value ratio and that loans with a

95 percent loan-to-value ratio are 350 percent more

likely to default than a loan with an 80 percent

loan-to-value ratio.

7

Research also finds that the likelihood of default is

positively related to loan-to-value ratios among

single-family loans insured by the Federal Housing

Administration (FHA). The default rate among FHA-

insured loans with down payments of 3 percent or

less is approximately twice as high as the rate among

those with down payments of 10 percent to 15 per-

cent, and five times as high as the rate among loans

with down payments of 25 percent or more.

8

While research suggests that negative equity is a

necessary condition for default, it also suggests that

negative equity is not a sufficient condition (most

loans with negative equity do not default).

9

In line

with the triggering-event explanations, measures of a

borrower’s ability to pay also explain default and

delinquency, although delinquency relationships are

less well documented. Default rates have been found

to decrease generally with increases in levels of

wealth and liquid assets. Further, default likelihoods

are closely linked to measures of income stability.

Default rates are generally higher for the self-

employed and for those with higher percentages of

nonsalary income and lower for those with longer

employment tenures. Perhaps surprisingly, after con-

trolling for other factors, the initial ratio of debt

payment to income has been found to be, at best, only

weakly related to the likelihood of default.

10

Although a borrower’s credit history may play an

important role in determining mortgage loan perform-

ance, few published studies have been able to incor-

porate such information in their analyses. Relevant

credit history data are often difficult to obtain and

hard to quantify. The available evidence, however,

indicates that loans made to borrowers with flawed

credit histories (those who have had difficulties meet-

ing scheduled payments on past loans) default or

6. See Robert Van Order and Peter Zorn, ‘‘Income, Location, and

Default: Some Implications for Community Lending,’’ paper pre-

sented at the Conference on Housing and Economics, Ohio State

University, Columbus, July 1995. Further, a number of studies have

found that neighborhood and property conditions, which ultimately

affect property values and thus equity, are significant factors for

mortgage performance. See, for example, James R. Barth, Joseph J.

Cordes, and Anthony M.J. Yezer, ‘‘Financial Institution Regulations,

Redlining, and Mortgage Markets,’’ in The Regulation of Financial

Institutions, Conference Series 21, Federal Reserve Bank of Boston

(April 1980), pp. 101–43.

7. ‘‘The State of the Private Mortgage Insurance Industry,’’ Special

Report, Duff & Phelps Credit Rating Company, December 1995.

8. See ‘‘An Actuarial Review of the Federal Housing Administra-

tion’s Mutual Mortgage Insurance Fund,’’ prepared by Price

Waterhouse for the U.S. Department of Housing and Urban Develop-

ment, June 6, 1990, p. 12.

9. See Robert Van Order and Ann B. Schnare, ‘‘Finding Common

Ground,’’ Secondary Mortgage Markets, vol. 11 (Winter 1994),

pp. 15–19.

10. See Quercia and Stegman, ‘‘Residential Mortgage Default’’;

and James A. Berkovec, Glenn B. Canner, Stuart A. Gabriel, and

Timothy H. Hannan, ‘‘Race, Redlining, and Residential Mortgage

Loan Performance,’’ Journal of Real Estate Finance and Economics,

vol. 9 (November 1993), pp. 263–94; and Van Order and Zorn,

‘‘Income, Location, and Default.’’

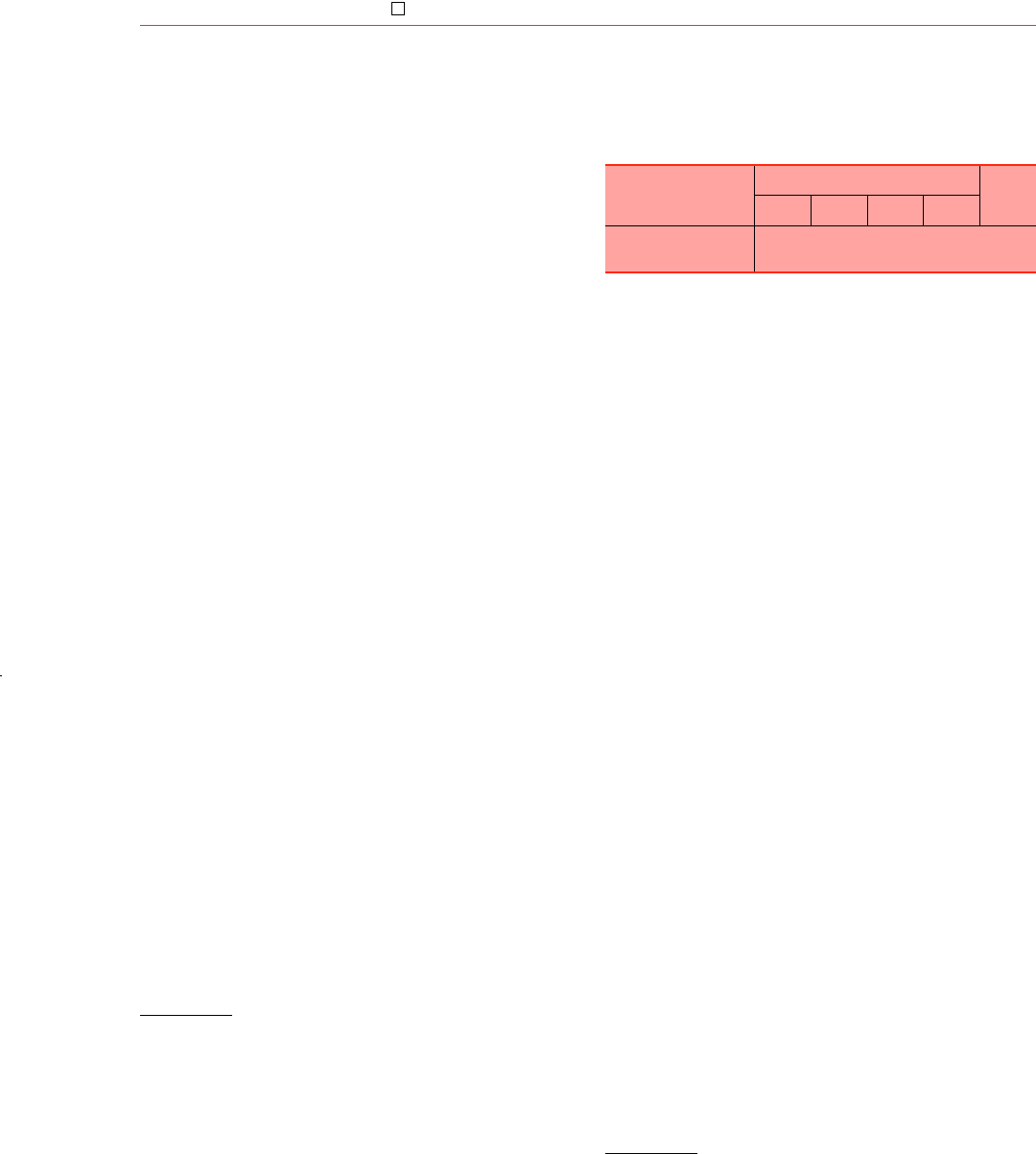

1. Proportion of selected mortgages that defaulted

by year-end 1992 and resulting severity of loss,

by selected loan-to-value ratio ranges

Percent

Performance measure

Loan-to-value ratio (percent)

All

10–70 71–80 81–90 91–95

Proportion defaulted .. . .24 1.11 2.74 6.20 2.16

Average loss severity . . 22.3 29.2 34.4 47.9 39.2

Note. Mortgages were originated during the 1975–83 period and purchased

by Freddie Mac. Defaulted loans are those on which Freddie Mac acquired the

property through foreclosure. Loan-to-value ratio is the original loan amount

divided by the value of the property at origination. Loss severity is the total loss

before mortgage insurance payouts (if any) resulting from foreclosure (including

interest and transaction costs) divided by the mortgage balance.

Source. Robert Van Order and Peter Zorn, ‘‘Income, Location and Default:

Some Implications for Community Lending,’’ paper presented at the Conference

on Housing and Economics, Ohio State University, Columbus, July 1995.

624 Federal Reserve Bulletin July 1996

become delinquent more often than loans made to

borrowers with good credit histories.

11

The relation-

ship between credit history and loan performance is

discussed further in the section on credit scoring.

On balance, defaults likely occur as a result of a

combination of factors. Almost uniformly, studies

indicate that the level of equity is a robust predictor

of default. Studies also demonstrate a significant rela-

tionship between mortgage performance and mea-

sures of vulnerability to triggering events.

MORTGAGE UNDERWRITING AND

RISK MITIGATION

Institutions that bear the credit risk of mortgage lend-

ing mitigate that risk by screening borrowers and

by sharing risk with others. Screening of prospective

borrowers is accomplished primarily through the

underwriting process, whereby information needed to

assess credit risk is collected, verified, and evaluated.

Risk-sharing may take a number of forms. First,

and most important, lenders share the risk of default

with the borrower by requiring a down payment and

establishing a schedule of payments that will fully

amortize the loan over a set period of time. Second,

lenders often share the credit risk of a loan with

either a private mortgage insurer or a government

agency such as the FHA or the Department of Veter-

ans Affairs (VA). Finally, lenders may sell a loan to

another party under arrangements that partly or fully

transfer the credit risk. The institutions that share or

assume the risk of lending do not solely rely on the

screening done by mortgage originators but also

make independent assessments.

The Underwriting Practices

of Mortgage Lenders

Lenders pursue different business strategies, and their

underwriting practices and standards reflect those

strategies. Some lenders choose to underwrite mort-

gages more strictly and thus limit their exposure to

losses. Others accept more credit risk but also price

for this risk, attempting to recoup higher expected

losses by charging higher fees or interest rates on

riskier mortgages. Still others may choose to spe-

cialize in financing certain types of properties or

borrowers.

In assessing credit risk, lenders consider the size of

the proposed down payment and the value of the

collateral as determined by a property appraisal,

which together determine the loan-to-value ratio.

Lenders also evaluate the capacity of the prospective

borrower to meet scheduled debt payments and to

provide the initial funds required to close the loan. In

so doing, lenders rely on many of the same factors

that researchers have found to be important predic-

tors of loan performance, including borrower sources

of income; employment history (such as measures of

employment stability and prospects for income

growth); ratios of debt payment to income; and asset

holdings, particularly the amount of liquid assets

available to meet down-payment, closing cost, and

cash reserve requirements.

12

In addition, lenders evaluate the credit history of

prospective borrowers as an indicator of their finan-

cial stability, ability to manage credit, and willing-

ness to make timely payments. Credit histories are

often complex and consist of many items, including

the number and age of credit accounts of different

types, the number of recent inquiries to the credit file,

account activity patterns, the incidence and severity

of payment problems, and the length of time since

any payment problems occurred.

Some applicants fall well within the underwriting

guidelines established by lenders, whereas others fall

far below the standards. The decision to either

approve or deny loan requests from such applicants is

generally straightforward. Frequently, however, the

decision is less clear-cut. For example, an applicant

may fail to meet one of many established underwrit-

ing guidelines, such as a satisfactory record of pay-

ments on past debts.

13

Lending policies generally allow for flexibility in

implementation so that applicants may offset weak-

ness in one factor with strength in others. For exam-

ple, even if an applicant’s ratio of debt payment to

income exceeds a lender’s established guidelines, the

11. See, for example, Wilson Thompson, ‘‘A Model of FHA’s

Origination Process and How it Relates to Default and Non-Default,’’

Working Paper, Department of Housing and Urban Development

(1980); and Gordon H. Steinbach, ‘‘Ready to Make the Grade,’’

Mortgage Banking (June 1995), pp. 36–42.

12. Most lenders require borrowers to have cash reserves sufficient

to cover two months of mortgage payments (including principal,

interest, and tax and insurance escrows) at the time of closing. This

reserve may provide a cushion should the borrower suffer a temporary

financial setback, and it is a signal to the lender that the borrower has

the discipline to accumulate savings.

13. For example, a study of mortgage lending in Boston found that

more than 80 percent of the applicants for home purchase loans

appeared either to have a weakness in their credit histories or to fail to

meet some other underwriting standard. See Alicia H. Munnell, Lynn

E. Browne, James McEneaney, and Geoffrey M.B. Tootell, ‘‘Mort-

gage Lending in Boston: Interpreting HMDA Data,’’ American Eco-

nomic Review, vol. 86 (March 1996), pp. 25–53.

Credit Risk, Credit Scoring, and the Performance of Home Mortgages 625

lender may approve the loan if the applicant exhibits

very stable income and an excellent credit history.

Similarly, a lender might consider a large down pay-

ment to be a compensating factor offsetting weakness

in some other area. Lenders will generally weigh all

the factors and in some cases seek additional informa-

tion in attempting to make a more precise evaluation

of credit risk.

Risk Sharing

Originators of mortgage loans typically share or

transfer risk by requiring borrowers to purchase mort-

gage insurance or by selling mortgages to secondary-

market institutions. For most mortgages, all or a

significant portion of the credit risk is borne by a

party other than the originator of the loan. For

instance, credit risk was either shared or transferred

on nearly three-fourths of all the home purchase

loans originated in 1994.

14

Mortgage lenders generally require a down pay-

ment of at least 20 percent of the appraised value of a

home, unless the mortgage is backed by a type of

insurance, paid for by the borrower, known as mort-

gage guarantee insurance. Mortgage insurance for

low-down-payment loans is available from the fed-

eral government, primarily through programs admin-

istered by the FHA and the VA and from private

mortgage insurance (PMI) companies.

When a loan is backed by mortgage insurance,

much of the credit risk is transferred to the insurer.

Should the borrower default, the insurer will reim-

burse the lender for the losses resulting from default,

up to certain limits. Mortgage insurers, like loan

originators, establish underwriting standards that

determine which loans they will insure and how

much credit risk they will bear. Lenders may encour-

age applicants seeking mortgages with low down

payments and those posing higher risks to apply for

government-backed loans rather than conventional

loans backed by PMI because the greater depth of

insurance coverage provided by the government on

such loans affords the lender greater protection in the

event of default.

Secondary-market institutions buy and sell billions

of dollars of mortgages and securities backed by

mortgages each year. Secondary-market institutions

promulgate the underwriting guidelines that loans

must meet to be eligible for purchase or securitiza-

tion. Three government-sponsored enterprises (GSEs)

dominate secondary-market activity—the Federal

National Mortgage Association (Fannie Mae), the

Federal Home Loan Mortgage Corporation (Freddie

Mac), and the Government National Mortgage Asso-

ciation (Ginnie Mae). Fannie Mae and Freddie Mac

mainly buy conventional mortgages, holding some in

portfolio and converting others into securities that are

sold to investors. Ginnie Mae does not purchase

loans but guarantees the timely payment of interest

and principal for privately issued securities backed

by mortgages insured by the FHA or VA. Various

non-GSE institutions, including commercial banks,

savings associations, insurance companies, and pen-

sion funds are also active purchasers of mortgages.

Mortgage insurers and secondary-market institu-

tions generally consider the same set of factors origi-

nators review when assessing credit risk. The under-

writing standards applied, however, will differ across

institutions in accordance with their various business

strategies and tolerance for risk. Private mortgage

insurers, for example, while backing loans with high

loan-to-value ratios, generally require borrowers to

make larger down payments and pay a larger share of

the closing costs than do the FHA and VA.

15

Sometimes mortgage originators do not share

credit risk with other institutions. Unlike mortgage

insurers and secondary-market institutions, which are

generally remote from borrowers, institutions that

both originate and bear the credit risk of mortgages

(known as portfolio lenders) are typically located in

the communities where they extend credit and have

numerous other financial relationships with their

communities. For these reasons, portfolio lenders

may have better information about local economic

conditions and the risks posed by individual borrow-

ers, which, in turn, may enable them to better mea-

sure and mitigate the risks associated with mortgage

lending. With better information to gauge credit risk,

portfolio lenders may be able to profitably originate

some loans that do not meet the underwriting stan-

dards established by secondary-market institutions

and PMI companies.

CREDIT SCORING AND THE

MORTGAGE LENDING PROCESS

Mortgage lending institutions establish guidelines for

underwriters to follow when evaluating applications

14. See Canner and Passmore, ‘‘Credit Risk and the Provision of

Mortgages,’’ p. 998.

15. See Glenn B. Canner, Wayne Passmore, and Monisha Mittal,

‘‘Private Mortgage Insurance,’’ Federal Reserve Bulletin, vol. 80

(October 1994), pp. 883–99.

626 Federal Reserve Bulletin July 1996

for credit, but they also rely heavily on the experi-

ence and judgment of underwriters when assessing

credit risk. Relying on subjective analysis has some

important limitations, however. Loan officers differ in

their experience and in their views regarding the

relationships between risk and specific credit charac-

teristics of applicants. Consequently, an institution

cannot be sure that its underwriters are approving all

applications that have risk profiles consistent with the

objectives of the institution. In addition, because of

the numerous and often complex factors mortgage

underwriters need to consider, subjective underwrit-

ing is time-consuming and costly.

To facilitate the mortgage underwriting process,

reduce costs, and promote consistency, ‘‘credit scor-

ing’’ models have been developed that numerically

weigh or ‘‘score’’ some or all of the factors consid-

ered in the underwriting process and provide an indi-

cation of the relative risk posed by each application.

In principle, a well-constructed credit scoring system

holds the promise of increasing the speed, accuracy,

and consistency of the credit evaluation process while

reducing costs. Thus, credit scoring can reduce risk

by helping lenders weed out applicants posing exces-

sive risk and can also increase the volume of loans by

better identifying creditworthy applicants.

Generically, scoring is a process that uses recorded

information about individuals and their loan requests

to predict, in a quantifiable and consistent manner,

their future performance regarding debt repayment.

Scores represent the estimated relationship between

information obtained from credit bureau reports or

loan applications and the likelihood of poor loan

performance, most often measured as delinquency or

default (see box ‘‘Developing a Credit History Scor-

ing System’’).

Scoring has been used to assess applications for

motor vehicle loans, credit cards, and other types

of consumer credit for decades.

16

Technological

advances in information processing and risk analysis

combined with competitive pressures to process

applications more quickly and efficiently are pushing

the lending industry to incorporate scoring in the

mortgage underwriting process.

Mortgage lenders ordinarily consider two kinds of

scores: those that are based primarily on the credit

histories of individuals and those that weigh credit

history as well as the other factors considered in the

underwriting process. The former will be referred to

here as ‘‘credit history’’ scores and the latter as

‘‘application’’ scores. Because they reflect the wide

range of factors considered in the evaluation of credit

risk, application scores are more comprehensive than

credit history scores. The credit history score is, then,

a single element to be weighed along with the other

factors in determining the total application score.

Credit History Scores

The difficulties in assessing the often complex infor-

mation about individuals’ past and current experience

with credit has helped motivate the adoption of scor-

ing methods for interpreting credit history. A credit

history score represents the estimated relationship

between information on the credit histories of indi-

viduals contained in credit bureau reports and the

likelihood of poor loan performance. In credit history

scoring systems, prospective applicants receive a

numerical score based on their individual credit his-

tory information; the score reflects the historic perfor-

mance of loans extended to individuals with similar

characteristics. Individuals with identical credit

scores may have received them for different reasons,

but within the context of the credit scoring index,

they are assessed to have equal likelihoods of the

predicted behavior, that is, they are considered to

pose the same credit risk.

Credit history scores can supplement or even

replace the traditional subjective assessment of credit

history with a quantitative measure summarizing the

pertinent information in an applicant’s credit report.

Adding a statistically derived measure of the credit

risk associated with a given credit history may allow

underwriters to better and more quickly assess the

strengths and weaknesses of applications.

Each of the three national credit bureaus, Equifax,

TRW, and Trans Union, make available credit history

scores—developed by Fair, Isaac and Company, Inc.

(FICO)—based on information contained in each of

the credit bureau’s files. These generic credit history

scores—the Equifax Beacon, the TRW-FICO, and

the Trans Union Empirica scores—are made avail-

able to help lenders assess risk on a wide variety of

loans. In addition, credit history scores tailored to the

mortgage market (mortgage credit history scores) are

now available; these scores are specifically designed

to assess the credit history risk of mortgage loans.

17

16. See Robert A. Eisenbeis, ‘‘Problems in Applying Discriminant

Analysis in Credit Scoring Models,’’ Board of Governors of the

Federal Reserve System, Staff Economic Studies (1977); and Edward

M. Lewis, An Introduction to Credit Scoring (San Rafael, Calif.:

Athena Press, 1990).

17. See ‘‘Equifax, Inc. Develops Mortgage Credit Scoring Sys-

tem,’’ National Mortgage News, June 13, 1994, p. 25. A number of

‘‘custom’’ credit history scoring models have been developed for

specific lenders to assess credit risk for specific loan products.

Credit Risk, Credit Scoring, and the Performance of Home Mortgages 627

Recent events have ensured that credit history

scores will be used much more often in the mort-

gage lending process than they have been in the

past. Most prominently, letters issued by Fannie

Mae and Freddie Mac in 1995 strongly encourage

the thousands of lenders from whom they purchase

loans to consider the Beacon, TRW-FICO, and

Empirica credit history scores in their loan

underwriting.

18

Application Scores

Based on all information relevant to a loan applica-

tion, application scores are most often used to deter-

18. See Fannie Mae Letter LL09-95 to all Fannie Mae lenders from

Robert J. Engelstad, ‘‘Measuring Credit Risk: Borrower Credit Scores

and Lender Profiles,’’ October 24, 1995; and Freddie Mac Industry

Letter from Michael K. Stamper, ‘‘The Predictive Power of Selected

Credit Scores,’’ July 11, 1995. As an alternative, Freddie Mac and

Fannie Mae recommend that, when underwriting loans, lenders con-

sider credit history scores that are calculated to predict bankruptcy.

The generic bankruptcy scores are the Equifax Delinquency Alert

System, Trans Union’s Delphi score, and the TRW-MDS score. Also

see Marshall Taylor, ‘‘Secondary Markets Explain Credit Scores,’’

Real Estate Finance Today, April 1, 1996, p. 16.

Developing a Credit History Scoring System

Developing a credit history scoring system requires infor-

mation about the experiences of individuals with credit.

1

Information is ordinarily drawn from credit account files

maintained by credit bureaus and sometimes from records

maintained by lending institutions. The credit account files

of individuals are segregated into groups based on measures

of loan performance. Ordinarily, the credit account files are

segregated into two distinct categories: those in which debts

have not been paid as scheduled as of a specified date or

during a specified time period (referred to here as ‘‘bad’’

accounts) and the rest (‘‘good’’ accounts). Bad credit

accounts can be defined in various ways depending on the

severity of observed credit difficulties. For example, bad

accounts might include any file with at least one thirty-day

delinquency within the past year, or they may be limited to

accounts that have had more serious delinquencies.

Having sorted the files according to performance as of a

specified date or during a specified period, the analyst then

focuses on information in the credit files from a preceding

time period that might have predicted the performance

outcome. Detailed information drawn from each credit file

is then recorded for statistical analysis. The selection of

specific items is often based on discussions with loan under-

writers plus a preliminary (bivariate) statistical analysis of

the relationship between individual credit factors and loan

performance. The information recorded pertains primarily

to the individual’s experience with credit.

The analyst then uses multivariate statistical analysis of

the recorded information to identify which set of character-

istics is most useful in identifying borrowers who are likely

to meet their scheduled payments and those who are not.

The statistical analysis provides weights (or scores) for each

factor, ranking its relative importance in predicting into

which group an individual will fall. Applying these weights

to the characteristics of individual accounts yields a total

score for each individual. Most credit scoring systems that

1. Federal law prohibits lenders from considering certain factors such as

gender, race, or ethnicity in making credit decisions. Consequently, these

factors are not used in constructing credit scoring models, and age and

marital status can be considered only under certain circumstances.

are widely used have adopted a scale with a range of scores

between 300 and 900, with higher scores corresponding to

lower credit risk.

Both the good accounts and the bad accounts will have

files with a wide range of scores. However, if the credit

scoring system is predictive of performance, good accounts

will have the highest percentage of high scores and bad

accounts likewise will have the highest percentage of low

scores. The predictive power or performance of a scoring

model is measurable, and the developer of the model looks

for the combination of attributes of the borrower’s credit

history that will maximize the score’s predictive power.

The distribution of total scores for individuals falling into

the good or bad categories can be described graphically (see

diagram). As shown, the good accounts tend to cluster

around a higher average score than do the bad accounts. To

operate a scoring system for credit underwriting, a lender

must select a cutoff score (such as 620) that can be used to

distinguish acceptable from unacceptable risks. Regardless

of the cutoff score selected, some customers with bad scores

will be offered credit because of offsetting factors, and

some customers with good scores will be denied credit, also

because of offsetting factors.

Distribution of credit scores of good and bad accounts

Percentage of accounts

Cutoff score

Bad accounts

620 Credit score

Good accounts

628 Federal Reserve Bulletin July 1996

mine which credit requests are clearly acceptable

under established underwriting guidelines and which

need further review. The use of application scores

differs among the participants in the mortgage mar-

ket: Loan originators generally use application scores

to identify applications eligible for streamlined

underwriting; secondary-market institutions use them

to facilitate loan purchases; and PMI companies

use them to help screen applications for mortgage

insurance.

As a screen for streamlined underwriting, a thresh-

old score corresponding to low credit risk is estab-

lished by the lender. Applicants with scores within

the low-risk range generally would be eligible for a

streamlined review that focuses primarily on verifica-

tion of reported information and evaluation of the

collateral. Streamlined underwriting allows those

making credit decisions to reduce costs by enabling

underwriters to spend less time on the low-risk appli-

cations and more time on those applications that

involve more complexity and potential risk.

19

Impor-

tantly, streamlined underwriting also benefits many

customers by shortening the amount of time between

the date of application and the credit decision.

Secondary-market institutions also use application

scores. Freddie Mac and Fannie Mae, for instance,

have developed application scoring systems that

indicate to the lender whether a prospective loan is

clearly eligible for sale to these institutions or

whether the lender will need to show that compensat-

ing factors exist that make the loan an acceptable

credit risk.

20

Private mortgage insurance companies use applica-

tion scoring systems to quickly identify those pro-

spective loans that clearly meet the underwriting

standards of the insurer. Loan applications that fail

the automated screen are reviewed by an underwriter

to determine whether compensating factors are

present that would make the loan insurable. Mort-

gage Guarantee Insurance Corporation (MGIC), for

example, reports that about 30 percent of the applica-

tions they receive for mortgage insurance are

approved through their automated application sys-

tem; the remaining applications are referred to under-

writers for closer review.

21

Most credit history and application scoring sys-

tems are proprietary, and the specific factors used and

the risk weights assigned to these factors in establish-

ing scores are not generally available to the public.

As a consequence, scoring systems have a ‘‘black

box’’ aspect to them. Nonetheless, most scoring sys-

tems share a number of elements. For example, most

credit history scoring systems consider records of

bankruptcy, current and historic ninety-day delin-

quencies, and the number of credit lines. Most

mortgage application scoring systems additionally

consider factors such as the loan-to-value ratio, the

ratio of debt payment to income, and measures of

employment stability. However, the risk weights

assigned to these factors vary from system to system.

Other Uses of Credit Scoring

Credit history scores and application scores have uses

other than in the loan underwriting process. To moni-

tor the quality of their portfolio and to determine the

appropriate level of reserves to set aside for losses,

lenders may periodically obtain credit scores for bor-

rowers with outstanding loans. Similarly, institutions

can use credit scores to evaluate the quality and value

of mortgages they are considering for sale. For exam-

ple, credit scores can help identify the credit risk of

seasoned loans and help determine the appropriate

grade (risk) pool into which individual loans should

be placed for sale to the secondary market.

Lenders may use credit scores to differentiate risk

categories of loans for pricing decisions. Rather than

reject higher-risk loans for origination or purchase,

the lender may decide to price the risk by requiring

an interest rate premium on those loans with higher

predicted probabilities of default. The use of credit

scores can also help with the collection and loss

mitigation process by, for example, allowing lenders

to concentrate staff resources on borrowers whose

credit scores indicate greater risk of delinquency.

Finally, lenders can use credit scores to facilitate

strategic planning decisions. For instance, lenders

concerned about possible attrition in their loan port-

folio due to competition for refinancings may offer a

new loan to those current borrowers whose credit

scores indicate that they would be most attractive to

potential competitors.

Limitations of Scoring

Although credit scoring can reduce costs and bring

more consistency to the underwriting process, its

reliability depends upon the accuracy, completeness,

and timeliness of the information used to generate the

19. See, for example, Janet Sonntag, ‘‘The Debate Over Credit

Scoring,’’ Mortgage Banking (November 1995), pp. 46–52.

20. The automated underwriting systems developed by Freddie

Mac and Fannie Mae are known respectively as ‘‘Loan Prospector’’

and ‘‘Desktop Underwriter.’’

21. See Jim Kunkel, ‘‘The Risks of Mortgage Automation,’’ Mort-

gage Banking (December 1995), pp. 45–57.

Credit Risk, Credit Scoring, and the Performance of Home Mortgages 629

scores. For example, credit scores based on erroneous

or seriously incomplete credit report information are

not likely to accurately measure the risk posed by an

individual applicant and may lead to unwarranted

actions on an application (see box ‘‘How To Obtain

Your Credit Report and What To Do To Correct

Errors in the Report’’).

Also, concerns have been expressed that credit

scores may not accurately gauge the creditworthiness

of individuals whose experiences differ substantially

from those on whom the index is based. If the base-

line population used to generate the scoring index is

not sufficiently diverse, then scores may lack predic-

tive power for the underrepresented segments of the

overall population. For example, rent, utility, and

other nonstandard payment histories, which are often

considered important for low-income populations, are

frequently left out of scoring models. Thus, scores for

these populations may not reliably assess individual

risk.

Another set of concerns surrounds the use of credit

scores more generally in the underwriting process.

Lenders relying too heavily on scores might not give

adequate consideration to special circumstances, such

as a recent illness, that might mitigate a low score.

Further, scores may lack predictive power if the

underlying model used to generate the scores does

not reflect current relationships between risk charac-

teristics and measures of loan performance. Builders

of credit scoring models report that model perfor-

mance deteriorates over time. Thus, periodic valida-

tion may be necessary to ensure that scoring models

retain their accuracy.

Credit scoring and its application to mortgage mar-

kets are evolving. Credit history scores, for example,

traditionally have been based on the payment perfor-

mance of a cross-section of consumers who have

used credit, not all of whom have incurred mortgage

debt. But consumer behavior with respect to mort-

gage debt may differ from behavior with respect to

consumer debt. Consumers facing financial difficul-

ties may, for instance, choose to pay their mortgage

obligations first and postpone payments on other

debts. For this reason, one might expect that a credit

scoring model developed specifically for the mort-

gage market would provide more accurate predic-

tions of future mortgage payment performance than a

generic credit history score, even before the borrower

has obtained a mortgage.

The development of models for credit history

scores and application scores based on the payment

performance of mortgage holders has historically

been hampered by incomplete information about

which consumers have mortgages and about other

characteristics of these consumers. Also, many indi-

vidual lenders have made too few mortgages to

develop a sound mortgage credit scoring model.

Recently, however, developers of scoring models

have integrated information from several sources to

develop both mortgage credit history scores and

mortgage application scores.

How To Obtain Your Credit Report and

What To Do To Correct Errors in the Report

In 1970 the Congress enacted the Fair Credit Reporting

Act (FCRA) to give consumers specific rights in dealing

with credit bureaus. The FCRA requires credit bureaus

to furnish a correct and complete consumer credit report

to businesses or persons to use in evaluating consumer

applications for credit, insurance, a job, or other legiti-

mate business need in connection with a transaction

involving the consumer.

Consumers can obtain a copy of their credit file from

a credit bureau. A reasonable fee may be charged for the

report. If a consumer has been denied credit, insurance,

or employment because of information that was supplied

by a credit bureau, the FCRA requires that the recipient

of the report give the consumer the name and address of

the credit bureau that supplied the information. The

consumer then has the right to obtain the report free of

charge if requested within thirty days of receiving a

notice of denial. Reports can be requested by phone at

the following numbers: Equifax—1-800-685-1111;

Trans Union—1-800-916-8800; and TRW—1-800-682-

7654.

Consumers have the right to dispute the information

in their credit files if they believe that their credit reports

contain errors or are incomplete. When a credit bureau

receives a complaint of this nature, it must investigate

and record the current status of the disputed items within

a reasonable period of time. If the credit bureau cannot

verify a disputed item, it must delete it from the file. The

credit bureau is required to correct any information

confirmed to be erroneous and to add any information

that has been omitted.

If the credit bureau’s investigation does not resolve a

dispute, the consumer may file a brief statement explain-

ing the nature of the dispute. The credit bureau must

include this statement in the report each time it is sent

out.

The Federal Trade Commission is the federal agency

that enforces the FCRA. Questions or complaints related

to a credit report may be directed to the Correspondence

Branch of the Federal Trade Commission, Washington,

DC 20580. Free copies of publications discussing credit

issues are available from Public Reference at the same

address.

630 Federal Reserve Bulletin July 1996

CREDIT HISTORY SCORES AND

MORTGAGE PERFORMANCE

Relatively little information about the relationship

between credit history scores and mortgage loan per-

formance is publicly available. However, recently

obtained proprietary information (courtesy of Equifax

Credit Information Services, Inc., one of the three

large national repositories of credit information)

relates credit scores to loan performance for a large

sample of mortgage loans. The sample contains virtu-

ally all of the mortgages that were outstanding and

whose payments were current as of September 1994

at three of the largest lenders in the country. The

sample is not, however, necessarily representative of

the pool of borrowers nationwide; these lenders do

not, for example, participate in all markets, nor do

they offer all types of mortgages. To ensure confiden-

tiality, no information was included in the data that

could be used to identify individuals or financial

institutions.

The data for each loan include a mortgage credit

history score, ‘‘The Mortgage Score’’ (TMS), devel-

oped by Equifax Mortgage Services and generated as

of September 1994.

22

TMS was developed by

Equifax on the basis of the credit records of mortgag-

ors and the payment performance on their mortgage

accounts. The data also include measures of the

performance of each loan over the subsequent twelve

months (to September 1995); the date the loan

was originated; the loan type (conventional or

government-insured and whether the interest rate

on the loan was fixed or variable); the ZIP code of

the property securing the loan; and characteristics of

the loan such as loan size and loan-to-value ratio at

the time of origination. All loans in the sample were

current in their mortgage payments as of Septem-

ber 1994, the date the TMS was determined. For our

analysis, loans with payments at least thirty days late

at any point during the performance period (Septem-

ber 1994 through September 1995) are defined as

delinquent.

For loans originated within the year preceding

September 1994, the TMS reasonably approximates

the credit history score that could have been used in

underwriting the loan. These loans, then, allow an

examination of the relationship between credit his-

tory scores at the time of origination and near-term

loan performance. For more seasoned (older) loans,

the TMS as of September 1994 does not necessarily

reflect the borrower’s credit record at the time the

loan was originated. Therefore, the sample relation-

ship between the TMS and loan performance does

not necessarily reflect the predictive value of credit

history scores at the time of loan origination. How-

ever, the older loans in the sample can be used to

demonstrate how lenders can use credit scores to help

monitor or evaluate the credit risk of seasoned loan

portfolios.

To analyze these relationships, we separated loans

into three types (conventional fixed rate, conven-

tional adjustable rate, and government-backed) and

two ‘‘seasoning’’ categories (newly originated and

seasoned) and then sorted them into three credit score

ranges—low, medium, and high—based on their

TMS scores (which, again, are mortgage credit his-

tory scores). Newly originated loans are those issued

after September 1993; seasoned loans are those that

were originated between January 1990 and Septem-

ber 1993. The three ranges of TMS scores correspond

to the specific ranges identified in the Fannie Mae

and Freddie Mac letters to mortgage lenders on the

use of the generic credit history scores (the Beacon,

TRW-FICO, and Empirica scores) in underwriting

loans.

23

TMS scores in the low range correspond to generic

credit history scores that Freddie Mac has identified

as showing ‘‘a strong indication that the borrower

does not show sufficient willingness to repay as

agreed’’ (generic credit history scores below 621).

TMS scores in the medium range correspond to

generic scores about which Freddie Mac has suffi-

cient concern to require a more detailed evaluation of

the credit history file (generic credit history scores in

the 621–660 range). TMS scores in the high range

correspond to generic scores in a range at which,

unless additional credit history risks are identified,

‘‘the borrower’s willingness to pay as agreed is con-

firmed’’ (generic credit history scores above 660).

The distributions of mortgage loans by credit score

range for the three types of loans sorted by seasoning

status, and the delinquency rate within each range,

are shown in table 2. The vast majority of both newly

originated and seasoned loans have credit scores in

the high range. For example, more than 90 percent of

conventional fixed rate mortgages have credit scores

22. The Mortgage Score and TMS are service marks of Equifax

Mortgage Services.

23. See note 18. The scales of the generic credit history scores and

of the TMS differ. Using the Equifax data on individuals scored with

both a generic credit history score and the TMS score, we set cutoffs

for the TMS score at a level designed to capture the same percentages

of borrowers in the low, medium, and high ranges as were implied by

the cutoffs of the generic credit history scores identified in the Freddie

Mac and Fannie Mae letters.

Credit Risk, Credit Scoring, and the Performance of Home Mortgages 631

in the high range. Relative to conventional fixed rate

mortgages, a larger proportion of conventional adjust-

able rate mortgages and an even larger proportion of

government-backed loans have low credit scores. For

each type of loan, the proportion of seasoned loans

with low scores is larger than that of newly originated

loans.

Delinquency rates are low for each loan type

regardless of seasoning status. The highest overall

rate of delinquency, that for government-backed

seasoned loans, is only 4.0 percent (table 2). These

delinquency rates should be viewed in the context of

several considerations that bias the results in opposite

directions. On one hand, the rate is for delinquencies

arising at any time over a twelve-month period and

thus overstates the likelihood of a loan being delin-

quent at any point in time. On the other hand, eco-

nomic conditions over this particular twelve-month

period were relatively favorable, and all loans had to

have been current in their payments at the beginning

of the performance period. These latter factors tend

to reduce measured delinquency rates.

The data indicate that TMS scores are a predictor

of loan performance. For each loan type, regardless

of seasoning status, borrowers with low scores have

substantially higher delinquency rates than those with

medium or high scores. For example, the delinquency

rate for newly originated government-backed loans

2. Mortgage loans, grouped by seasoning status, type, and payment status and distributed by credit score

Percent

Loan

Credit score range Memo: Number of sample loans

Low Medium High All Total Delinquent

Newly originated

Conventional fixed rate .......................... 1.5 4.9 93.6 100 109,433 417

Delinquencies in score range

As percentage of all delinquent loans of this

type and seasoning ..................... 17.3 21.8 60.9 100 . . . . . .

Memo: As percentage of all loans of this

type and seasoning in score range ....... 4.4 1.7 .2 .4 . . . . . .

Conventional adjustable rate ...................... 3.8 8.3 87.8 100 24,075 119

Delinquencies in score range

As percentage of all delinquent loans of this

type and seasoning ..................... 18.5 24.4 57.1 100 . . . . . .

Memo: As percentage of all loans of this

type and seasoning in score range ....... 2.4 1.4 .3 .5 . . . . . .

Government-backed fixed rate .................... 12.8 16.7 70.5 100 36,596 985

Delinquencies in score range

As percentage of all delinquent loans of this

type and seasoning ..................... 52.0 25.2 22.8 100 . . . . . .

Memo: As percentage of all loans of this

type and seasoning in score range ....... 10.9 4.0 .9 2.7 . . . . . .

Seasoned

Conventional fixed rate .......................... 2.1 4.9 93.0 100 257,741 1,909

Delinquencies in score range

As percentage of all delinquent loans of this

type and seasoning ..................... 32.4 19.6 48.0 100 . . . . . .

Memo: As percentage of all loans of this

type and seasoning in score range ....... 11.4 2.9 .4 .7 . . . . . .

Conventional adjustable rate ...................... 7.6 10.7 81.8 100 125,384 2,423

Delinquencies in score range

As percentage of all delinquent loans of this

type and seasoning ..................... 42.5 21.7 35.8 100 . . . . . .

Memo: As percentage of all loans of this

type and seasoning in score range ....... 10.9 3.9 .8 1.9 . . . . . .

Government-backed fixed rate .................... 13.7 15.5 70.9 100 67,913 2,786

Delinquencies in score range

As percentage of all delinquent loans of this

type and seasoning ..................... 59.9 19.4 20.7 100 . . . . . .

Memo: As percentage of all loans of this

type and seasoning in score range ....... 18.0 5.1 1.2 4.1 . . . . . .

Note. Newly originated loans were originated during the October 1993–

June 1994 period. Seasoned loans were originated during the January 1990–

September 1993 period.

The credit score is The Mortgage Score (TMS; service mark of Equifax

Mortgage Services), a mortgage credit history score derived from a model based

exclusively on the credit records of households with mortgages and their

payment performance on mortgage loans. The credit score for each loan was

calculated at the end of the third quarter of 1994.

Score ranges have been structured to roughly approximate the generic credit

bureau score ranges used by Freddie Mac for evaluating whether an application

for a mortgage meets its underwriting guidelines. The ranges for The Mortgage

Score correspond to generic credit bureau scores (Beacon, TRW-FICO,

Empirica) as follows: low = less than 621, medium = 621–660, and high = more

than 660.

Delinquent accounts are those on which a payment was at least thirty days

past due at any time during the period from September 30, 1994, through

September 30, 1995.

. . . Not applicable.

Source. Equifax Credit Information Services, Inc.

632 Federal Reserve Bulletin July 1996

with low TMS scores is 10.9 percent, compared with

4.0 percent for those with medium scores and 0.9 per-

cent for those with high scores.

The relationship between credit scores and delin-

quency rates is further evidenced by the distribution

of delinquent borrowers across credit score ranges for

each type of loan. These distributions show that

delinquent borrowers disproportionately have scores

in the low range. Borrowers with low credit scores

accounted for only 1.5 percent of all newly originated

conventional fixed rate loans but for 17 percent of

those that became delinquent (table 2, memo item).

This relationship holds for other product types and

seasoned loans as well. For example, borrowers

with low credit scores accounted for 2.1 percent of

all seasoned conventional fixed rate mortgages, but

they accounted for 32 percent of those that became

delinquent.

The data, however, also consistently show that

most borrowers with credit scores in the low range

are not delinquent. For example, in the case of newly

originated conventional fixed rate loans, only 4.4 per-

cent of borrowers with low credit scores became

delinquent over the performance period. Thus, while

delinquent borrowers disproportionately have low

scores, most borrowers with low scores are not

delinquent.

Distinct differences exist in delinquency rates

across loan types and seasoning status. Within each

credit score range and loan type, seasoned loans have

higher delinquency rates than newly originated loans

have.

24

For example, the delinquency rate for newly

originated conventional adjustable rate mortgages

with low credit scores is 2.4 percent, but the rate for

seasoned conventional adjustable rate loans with low

scores is 10.9 percent. Controlling for score and

seasoning, government-backed loans have the highest

rates of delinquency, a result consistent with data on

relative delinquency rates from other sources.

25

Detailed information on the distribution of TMS

scores by loan performance, type of loan, and

mortgage and location characteristics for newly origi-

nated loans is presented in tables 3, 4, and 5. In

general, loans with lower loan-to-value ratios and

loans on properties located in areas with higher rela-

tive incomes and higher relative home values have

higher mean and median TMS scores and a lower

percentage of borrowers with low and medium scores

than other loans. These relationships hold for delin-

quent loans as well as for loans that were paid on

schedule. For example, for newly originated conven-

tional fixed rate mortgage loans (table 3 and chart 1),

the mean TMS score for paid-as-scheduled loans

with loan-to-value ratios less than 81 percent is

50 points higher than the mean score for those with

loan-to-value ratios of more than 90 percent. Simi-

larly, 94.5 percent of the loans with loan-to-value

ratios of less than 81 percent are in the high credit

score range, compared with 84.6 percent for those

with loan-to-value ratios of more than 90 percent.

For each loan type, the mean and median TMS

scores for delinquent loans are 100 to 150 points

lower than the mean and median scores for those that

were paid on schedule, and these differences are

statistically significant. Similarly, the percentage of

borrowers in the low credit score range is at least four

to five times higher for delinquent loans than for

loans that were paid as scheduled. These relation-

ships hold across all subcategories of loans.

Additional information relating credit history

scores to mortgage loan performance was provided

by Freddie Mac (table 6). These data pertain to loans

for single-family owner-occupied properties pur-

chased by Freddie Mac in the first six months of

1994. Performance is measured by whether the loan

had entered into foreclosure by the end of 1995.

Foreclosure rates for different categories of loans are

expressed relative to the rate for borrowers with

loan-to-value ratios of 80 percent or less and high

credit history scores, which was set to 1.

26

Foreclosure rates are substantially higher for bor-

rowers with low credit scores as well as for those

with high loan-to-value ratios (table 6). Moreover,

borrowers with low credit scores perform worse

within each loan-to-value ratio category. The foreclo-

sure rate is particularly high for borrowers with both

low credit scores and high loan-to-value ratios—

almost 50 times higher than that for borrowers with

both high credit scores and low loan-to-value ratios.

This finding, that loan performance deteriorates sig-

nificantly when risks are high for multiple factors

(‘‘layering of risk’’), is discussed at length later in

this article.

The relationship between borrower income and

loan performance appears to be slight. Within each

credit score and loan-to-value ratio category, borrow-

ers with income below 80 percent of area median

24. This result is consistent with other research, which indicates

that delinquency rates increase as loans age, at least for the first few

years after origination. See, for example, chart 1 in The Market Pulse,

Mortgage Information Corporation (vol. 1, January 1996), p. 1.

25. See Mortgage Bankers Association National Delinquency

Survey.

26. The credit score ranges are comparable to those used in tables 2

through 5.

Credit Risk, Credit Scoring, and the Performance of Home Mortgages 633

income have somewhat higher foreclosure rates than

average, and those with incomes above 120 percent

of area median income have somewhat lower foreclo-

sure rates than average. Credit score and, to a lesser

extent, loan-to-value ratio appear to be much stronger

predictors of foreclosure rates than income.

3. Newly originated conventional fixed rate mortgage loans, grouped by payment performance and characteristic and distributed

by credit score

Percent except as noted

Performance of mortgage

and characteristic

Credit score

Total

Mean

4

Median

4

Low Medium High

Percent

of charac-

teristic

Memo:

Percent

of score

range

Percent

of charac-

teristic

Memo:

Percent

of score

range

Percent

of charac-

teristic

Memo:

Percent

of score

range

Percent

of charac-

teristic

Memo:

Percent

of all

loans

Paid as Scheduled

Mortgage characteristic

Loan-to-value ratio (percent)

Less than 81 ............... 845 865 1.2 72.9 4.3 77.6 94.5 87.1 100 86.5

81to90 .................. 818 840 2.6 19.8 7.1 16.2 90.3 10.5 100 10.9

More than 90 ............. 794 811 4.0 7.3 11.4 6.2 84.6 2.4 100 2.6

All

1

.................... 841 861 1.4 100 4.8 100 93.8 100 100 100

Loan size (dollars)

Less than 100,000 ......... 836 859 1.9 47.5 5.7 41.9 92.4 35.0 100 35.5

100,000–200,000 .......... 839 859 1.4 33.8 5.0 35.0 93.6 33.8 100 33.9

More than 200,000 ........ 847 866 .9 18.7 3.6 23.1 95.5 31.2 100 30.6

All ..................... 841 861 1.4 100 4.8 100 93.7 100 100 100

Location characteristic

ZIP code median income

(percentage of area median

income)

2

Less than 80 .............. 823 846 2.3 9.0 7.7 9.0 90.1 5.5 100 5.7

80to120 ................. 837 857 1.6 52.2 5.2 50.6 93.2 46.7 100 47.0

More than 120 ............ 847 867 1.2 38.8 4.1 40.4 94.7 47.8 100 47.3

All ..................... 841 861 1.4 100 4.8 100 93.7 100 100 100

Home values (percentage

of area median home value)

3

Less than 80 .............. 826 847 2.2 20.7 6.6 18.8 91.3 13.4 100 13.8

80to120 ................. 836 856 1.6 27.9 5.2 26.5 93.1 24.2 100 24.4

More than 120 ............ 846 866 1.2 51.4 4.3 54.7 94.5 62.3 100 61.8

All ..................... 841 861 1.4 100 4.8 100 93.7 100 100 100

Delinquent

Mortgage characteristic

Loan-to-value ratio (percent)

Less than 81 .............. 734 740 11.9 63.8 22.9 78.0 65.2 79.8 100 77.1

81to90 .................. 697 707 21.3 27.6 22.7 18.7 56.0 16.6 100 18.7

More than 90 ............. 699 744 29.4 8.6 17.6 3.3 52.9 3.6 100 4.2

All

1

.................... 720 730 14.4 100 22.6 100 62.9 100 100 100

Loan size (dollars)

Less than 100,000 ......... 692 686 25.1 59.7 24.6 46.2 50.3 33.9 100 41.0

100,000–200,000 .......... 720 730 14.7 29.2 23.8 37.4 61.5 34.6 100 34.3

More than 200,000 ........ 766 781 7.8 11.1 14.6 16.5 77.7 31.5 100 24.7

All ..................... 720 730 17.3 100 21.8 100 60.9 100 100 100

Location characteristic

ZIP code median income

(percentage of area median

income)

2

Less than 80 .............. 724 738 17.4 11.1 19.6 9.9 63.0 11.4 100 11.0

80to120 ................. 707 712 22.0 69.4 21.6 53.8 56.4 50.4 100 54.4