Everyone can win...

ANNUAL REPORT 07

NSW LOTTERiES ANNUAL REPORT 2007

CONTENTS

LETTER TO ShAREhOLdER MiNiSTERS 1

OUR ViSiON, MiSSiON & VALUES 2

AbOUT ThiS REPORT 2

RESULTS 3

A MESSAgE fROM ThE ChAiRMAN

ANd ChiEf ExECUTiVE OffiCER 4

KEy fACTS 2006/2007 6

ThE yEAR iN bRiEf 7

WhO WE ARE ANd WhAT WE dO 10

Who We Are 10

What We Do – Our Charter 10

Our Games 10

Business Planning 10

Balanced Scorecard for Fiscal 2007 10

OUR PLAyERS 12

The Games 13

Player Services 19

Responsible Gaming 21

OUR RETAiLERS 23

The Retail Network 24

Agency Services 25

OUR bUSiNESS 27

The Gaming System 28

Staff and Agent Websites 29

Business Continuity 29

OUR ShAREhOLdERS 30

The Management Structure 32

Corporate Governance 32

The Board of Directors 36

The Executive Management Team 38

Risk Management 39

Insurance 39

Managing Resources 39

OUR STAff 41

Listening to Our Staff 42

Learning and Development 42

Rewarding Our Staff 44

Occupational Health and Safety 46

hiSTORy 47

fiNANCiAL OVERViEW 49

fiNANCiAL REPORT 50

STATUTORy REPORTiNg APPENdix 75

iNdEx 82

ACCESS TO SERViCES 84

NSW LOTTERIES ANNUAL REPORT 2007 1

The Hon. John Watkins, MP

Deputy Premier, Minister for Transport, and Minister for Finance

The Hon. Michael Costa, MLC

Treasurer, Minister for Infrastructure, and Minister for the Hunter

Dear Gentlemen

Report of Performance for the Year Ended 30 June 2007

We submit the NSW Lotteries Corporation’s Annual Report for the year ended 30 June 2007 for presentation to Parliament.

The Annual Report has been prepared in accordance with the relevant provisions of the State Owned Corporations Act 1989

and the Annual Reports (Statutory Bodies) Act 1984.

We are pleased to advise that the Auditor-General of NSW has certified the Corporation’s Financial Report that forms part of

the Annual Report, without qualification.

John Bagshaw Michael Howell

Chairman Chief Executive Officer

LETTER TO SHAREHOLDER MINISTERS

2 NSW LOTTERIES ANNUAL REPORT 2007

OUR VISION

We will continue to be a successful lottery operator.

OUR MISSION

We contribute to the community of NSW by maximising

the return to Government through providing quality lottery

products and services.

OUR VALUES

In all our activities we will:

• Operate with integrity

• Seek to provide excellent service to our customers

• Value the relationship with our retailers

• Acknowledge the contributions of our staff

• Be successful and continuously improve our business

• Be socially responsible

Throughout this report we will highlight how we practice

our values in our day to day business dealings.

OUR VISION, MISSION & VALUES ABOUT THIS REPORT

This report provides an account of the

operations of NSW Lotteries Corporation

for the financial year ended 30 June 2007.

The report analyses our achievements against

the performance measures and targets in the

NSW Lotteries Business Plan and the annual Statement

of Corporate Intent negotiated with the Corporation’s

Shareholder Ministers.

This annual report was produced in accordance with

the requirements of the Annual Reports (Statutory

Bodies) Act 1984 and complies with all relevant annual

reporting statutory requirements and disclosure guidelines.

We are committed to open and accountable reporting

and welcome your feedback.

An index is provided at the back of the report to assist

readers in searching for specific information.

Members of the public are encouraged to attend the Lucky Lottery draws held most weekdays. Who knows, you might even meet the

game’s mascot, Lucky the Cat.

NSW LOTTERIES ANNUAL REPORT 2007 3

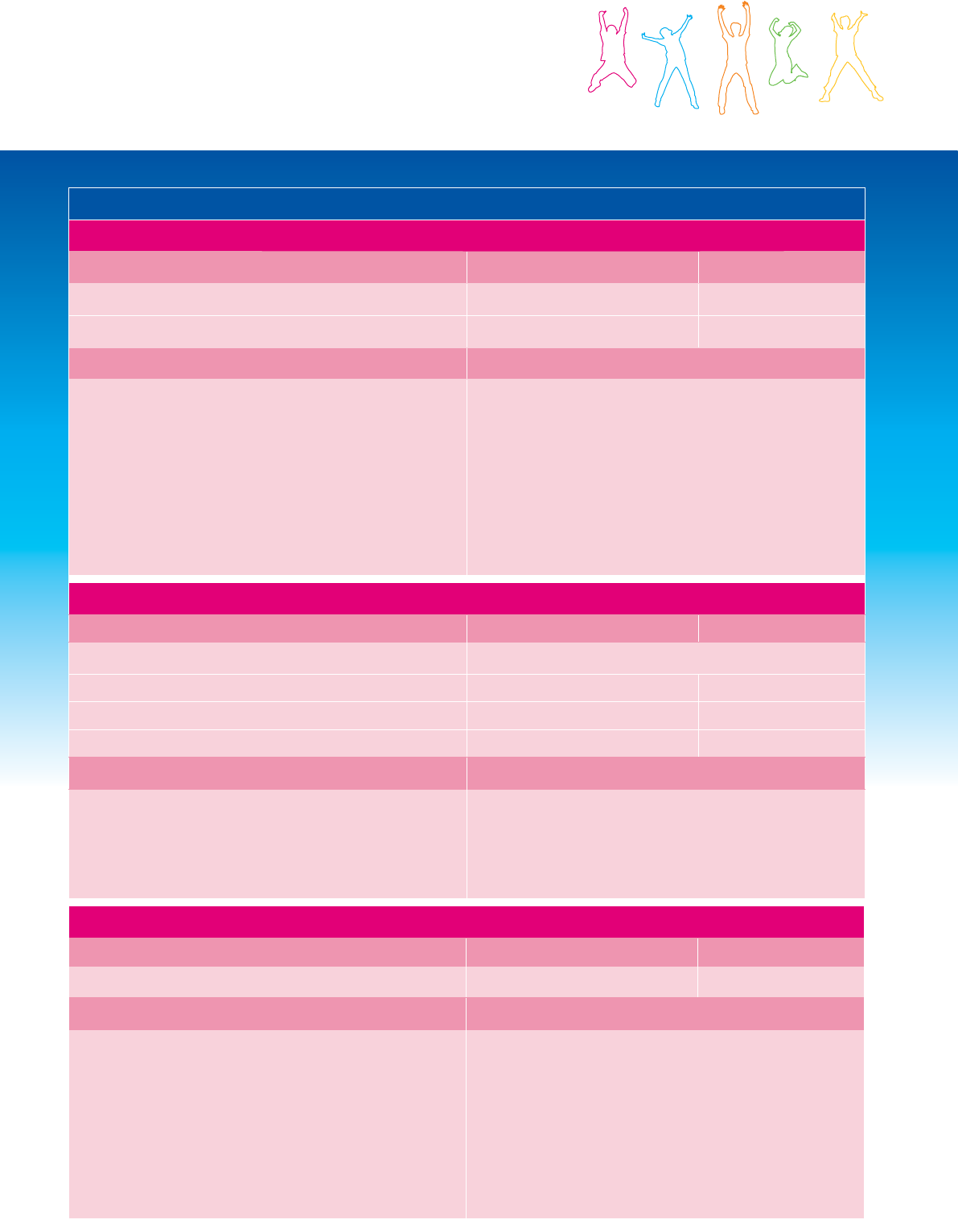

RESULTS

RESULTS FOR FISCAL 2007

PERFORMANCE MEASURE TARGET RESULT

Sales (including GST, excluding agent commission) $1,165.00 m $1,124.44 m

Profi t from Continuing Operations Before Signifi cant Item and

Income Tax Equivalent

$50.24 m $50.28 m

NSW Government Duty $295.69 m $284.08 m

Dividends and Income Tax Equivalent $50.24 m $50.28 m

Total $345.93 m $334.36 m

Return on Average Shareholder Equity (%) 107.54% 105.88%

Return on Corporate Assets (%) 48.07% 49.16%

SNAPSHOT OF KEY PERFORMANCE INDICATORS FOR THE LAST 7 YEARS

CATEGORY 2000/01 2001/02 2002/03 2003/04 2004/05 2005/06 2006/07

Sales ($M)** 1,010.7** 1,020.8** 1,092.9** 1,108.9** 1,116.0** 1,133.2** 1,124.4**

Total Government

Revenue ($M)

1

332.4** 343.6** 373.6** 371.8** 375.8** 381.6** 381.0**

Return on Average

Shareholder Equity (%)

55 64 90 95 105 104 106

Return on Corporate

Assets (%)

32 35 44 47 48 47 49

Selling System

Uptime (%)

99.96 99.99 99.99 99.99 100.00 99.99 99.99

Average Staff Number 205 201 195 183 176 172 170

Sales per

Employee ($M)

4.9 5.1 5.6 6.1 6.3 6.6 6.6

** Includes GST

1 Total Government Revenue includes Duty, GST, Dividends and Income Tax Equivalent payments, and excludes payments to the ACT Government

As a State Owned Corporation, NSW Lotteries is accountable to its Shareholder

Ministers for its commercial performance.

A Statement of Corporate Intent is negotiated annually between NSW Lotteries and the Shareholder Ministers and

sets out the agreed performance measures and financial targets to be achieved by the Corporation each financial year.

Key results for 2006/2007 were:

06/07

05/06

04/05

03/04

02/03

01/02

00/01

334.4*

334.7*

330.0*

326.8*

329.3*^

302.4*^

291.8*

TOTAL REVENUE TO NSW GOVERNMENT ($M)

* Excludes GST

^ Included a special dividend of $10 m

By agreement between the Commonwealth and State Governments, with

the introduction of the GST, the rate at which NSW Lotteries pays duty to the

NSW Government was reduced to compensate for the GST payable to the

Commonwealth Government

PRODUCT SALES ($M)

06/07

05/06

04/05

03/04

02/03

01/02

00/01

1,124.4*

1,133.2*

1,116.0*

1,108.9*

1,092.9*

1,020.8*

1,010.7*

* Includes GST

4 NSW LOTTERIES ANNUAL REPORT 2007

A YEAR OF CHALLENGE

This year’s results have been achieved in an extremely

challenging retail environment.

A number of major business issues flagged in previous

years – a mature portfolio of games, increasing competition

within and outside the portfolio, and player expectations

of ever-bigger jackpots – have been prominent throughout

the year.

Like all challenges, when properly addressed, these issues

presented new opportunities for NSW Lotteries to further

enhance its business.

STRONG CORPORATE VALUES

In actively responding to issues, we are able to rely on

a strong set of corporate values, and we measure our

success based on the positive benefits we provide to

our customers and the community.

This report outlines how NSW Lotteries has been

meeting its twin responsibilities as a successful business

and a good corporate citizen over the past fiscal year.

NSW Lotteries remains unashamedly at the soft end of

the gaming market.

Where a number of other local and international lottery

operators have diversified into more “continuous” gaming

products, NSW Lotteries has remained focused on its core

mission to be a successful lottery operator.

A HEALTHY PORTFOLIO

In recent years we have worked hard to enhance our

existing games with attributes which have the potential to

appeal to a new generation of players. At the same time,

we have fine-tuned the individual brands to maintain the

overall health of the portfolio.

In particular, we have sought to provide each of our lottery

games with an individual identity and player benefit, and

promote each game accordingly.

The success of this approach can be seen with our new

“Live a Lotto Life” campaign, which reminds players about

the fun and excitement of watching the winning Lotto

numbers come up each week.

Similarly, Instant Scratchies has undergone a major revamp

to reward players looking for more prizes between $50 and

$100 while waiting to win a life-changing major prize.

Other changes are planned for the big-jackpotting games

such as Powerball, OZ Lotto and Lucky Lotteries, which

aim to differentiate brand offerings, and reward each

game’s loyal followers.

FINANCIAL PERFORMANCE

While sales grew strongly towards the end of the fiscal

year as a result of careful portfolio management and some

welcome late jackpot runs for Powerball and OZ Lotto,

sales of $1,124.4 million were slightly below last year’s

sales record and 3.5% below our target for the year.

Adverse economic and retail conditions in NSW were

significant contributors to the lower than expected result.

These factors are cyclical and, by their very nature, will

inevitably change for the better. On the other hand,

systemic product and player behaviour issues such as the

increasing maturity of our portfolio of products and the

“desensitisation” of players to larger jackpot prize offers

will become bigger challenges as our products become

more mature.

Despite the decline in sales, the Corporation continued

to focus on identifying potential areas where business

efficiencies could be made to reduce costs without

impacting sales or customer service levels. As a result

of this strategy, the Corporation achieved a record profit

result of $50.28 million.

RECORD RETURNS TO OUR RETAILER PARTNERS

Our retail network once again enjoyed record revenues

from the sale of lottery products. Total income earned

by agents increased by 1.6% to over $86 million

demonstrating the Corporation’s commitment to

increasing returns to agents.

NEW DELIVERY MECHANISMS

NSW Lotteries needs to be able to rapidly respond to

player demand if it is to continue to grow.

We may all be would-be millionaires, but we are all

increasingly time-poor and finding it difficult to juggle

all the demands of our work/life balance.

Leisurely filling in a lottery entry form during normal retail

hours is simply no longer an option for many of our players

and NSW Lotteries is continually reviewing its retail

network to ensure that the needs of our players are met.

The huge number of current visitors to NSW Lotteries’

website for results and game information demonstrates

that new and emerging distribution channels, such as the

Internet, may provide the potential to deliver incremental

sales over time.

INDUSTRY LEADING SYSTEMS AND PROCESSES

NSW Lotteries can rightly claim to be among the world

leaders in our industry for systems and processes which

deliver a quality outcome for customers.

A MESSAGE FROM THE CHAIRMAN AND CHIEF EXECUTIVE OFFICER

NSW LOTTERIES ANNUAL REPORT 2007 5

Our gaming system ran at close to 100% availability

throughout the year, successfully processing more than

284 million customer transactions.

A range of system enhancements provided further

protection for players and retailers, including the important

new terminal “freeze” functionality, which automatically

alerts unregistered players when a major prize is won.

A Players 1

st

program has been developed and is part

of a series of measures aimed at encouraging players to

protect their prizes by registering entries and exercising

some simple steps to protect their entries.

A TEAM COMMITMENT

NSW Lotteries has an experienced team of executives

and staff. Of course, the structure of the Corporation

must periodically change to ensure our internal skills and

expertise match our current and projected business needs.

Accordingly, a comprehensive structural review was

undertaken across the organisation to ensure the necessary

resource alignment with our business requirements.

We would like to record our sincere thanks to all our

staff (past and present) for their efforts in helping the

Corporation to generate record profits and the other

significant business achievements, outlined in this year’s

report, in the difficult operating environment which

prevailed over the past fiscal year.

LOOKING AHEAD

There are no easy answers to the industry-wide challenges

associated with managing products in the mature stage

of their lifecycle. However, the Corporation has always

demonstrated a capacity to develop relevant business

objectives which deliver value to its stakeholders.

We have a clear strategy for the future, and a team with the

experience, skill and enthusiasm to make our plans a reality.

We will continue to seek feedback from our players and

other stakeholders to ensure we understand their wants

and expectations, and respond accordingly.

We will maintain the value of NSW Lotteries as a public

asset, based on a 76-year reputation for honesty, probity

and efficiency.

Whether you are a player of our games, one of our retailers,

or a member of the NSW community, you have a stake in

the success of our business, and we hope you will find this

report informative and useful.

John Bagshaw Michael Howell

Chairman Chief Executive Officer

We measure our

success based

on the positive

benefits we

provide to our

customers and

the community

John Bagshaw, Chairman and Michael Howell, Chief Executive Offi cer

6 NSW LOTTERIES ANNUAL REPORT 2007

SALES GAME MATRIX

NO. OF MILLIONAIRES

& 1

ST

PRIZE WINNERS

PRIZES WON

IN NSW

TOTAL NO.

WINNERS

LARGEST FIRST /

JACKPOT PRIZE

Lotto

$187.41 m 6 from 45 21 millionaires

72 Division One winners

$107.54 m 2,846,318 $2.6 m

Lotto

Strike

$10.85 m First 4 Lotto

numbers

1 millionaire

4 Strike 4 winners

$6.84 m 937,265 $1.2 m

Saturday

Lotto

$282.15 m 6 from 45 23 NSW millionaires

61 NSW Division One

winners

$164.55 m 2,704,942 $33 m

OZ Lotto

$153.93 m 7 from 45 4 NSW millionaires

4 NSW Division One winners

$99.63 m 2,742,427 $25 m

Powerball

$250.43 m 5 from 45

& 1 from 45

drawn by a 2

nd

machine

5 NSW millionaires

5 NSW Division One winners

$145.70 m 3,849,823 $35.3 m

Instant

Scratchies

$138.30 m Game

Pricepoints:

$1

$2

$2.50**

$3

$4**

$5

$10

**Pricepoint

discontinued

Nov. 2006

Number of Game

Top Prizes:

$1 18

$2 25

$2.50 Merchandise 2

$3 Made For Life 2

$3 18

$3 Merchandise 3

$4 Win For Life 1

$5 Win For Life 2

$5 6

$10 3

$90.16 m 13,807,621

$1 - $20k, $50k

$2 - $50k, $100k

$2.50 My RX8

$3 MFL - $600k

$3 - $75k, $150k

$3 Qantas Travel

Credit & $75k

Gold Bullion

$4 WFL - $1m

$5 WFL - $1.125m

$5 - $100k, $250k

$10 - $250k, $500k

Lucky

Lotteries

$95.60 m $2 Jackpot

Lottery –

200,000 tickets

$5 Jackpot

Lottery –

160,000 tickets

193 x 1

st

Prize winners

4 x $2 Jackpot Lottery

millionaires

23 x 1

st

Prize winners

There were no $5 Jackpot

Lottery millionaires

$61.12 m 10,147

Prizes in

every $2

Jackpot

Lottery draw

12,880

Prizes in

every $5

Jackpot

Lottery draw

$8.375 m Jackpot

won in August 2006

The 1

st

prize of

$200,000 was won

in each of the 23

draws

The jackpot was not

won in 2006/07

6 From

38 Pools

$5.77 m 6 from 38 5 Division One winners $2.11 m 72,811 $0.63 m

Total

$1,124.44 m $677.65 m

KEY FACTS 2006/2007

NSW LOTTERIES ANNUAL REPORT 2007 7

OUR PLAYERS

Objective: To increase sales and market share

Measure Target Result

Sales $1,165 million $1,124.44 million

Bloc Market Share – combined Saturday Lotto/OZ Lotto/Powerball 25% 24.1%

Key Activities and Issues Outlook and Future Challenges

• Sales totalled $1,124.4 million (GST inclusive)

– $8.8 million (or 0.8%) down on the previous year

• Prizes totalled $677.65 million

• Combined turnover for Lotto style games of $884.7 million –

$29.3 million (or 3.4%) up on previous year

• Lucky Lotteries sales of $95.6 million – $25.1 million (or 20.8%)

down on previous year

• Instant Scratchie sales of $138.3 million – $12.7 million

(or 8.4%) down on previous year

• 6 From 38 Pools sales of $6 million – $0.2 million (or 3.3%)

down on previous year

• Another year of record sales and record prizes,

with strong sales for Lotto-style games

• OZ Lotto jackpots anticipated to better refl ect probability

Objective: To ensure our products and services consistently attract players and meet their expectations

Measure Target Result

Customer Satisfaction Survey The survey was not scheduled to be undertaken in 2006/07

No. of complaints from players <200 152

Customer Hotline – average time taken to answer calls <15 secs 4 secs

Players Club Membership 930,000 873,537

Key Activities and Issues Outlook and Future Challenges

• More than 385,000 calls were received through the

Call Centre

• www.nswlotteries.com.au attracted 8.96 million user sessions

during the year – 22% up on the previous year

• Over 873,000 players benefi ted from the protection and

additional services provided by their Players Club membership

• Focusing on enhancing current games

• Seeking to continually improve service delivery

• Retaining existing customer base while attracting new players

• Improving access to on-line agencies for players

Objective: To be recognised as a responsible gaming operator

Measure Target Result

Compliance with the Corporation’s responsible gaming package 100% 100%

Key Activities and Issues Outlook and Future Challenges

• The Corporation continued to ensure that there were no

negative impacts from the sale and promotion of its range

of products

• NSW Lotteries’ comprehensive responsible gaming

policies were reviewed and amended and met all

legislative requirements

• Responsible gaming training sessions were conducted for

all new agents

• Territory Managers visited all agencies in NSW and the

ACT to ensure that retailers understood, and complied with,

various responsible gaming obligations

• We will continue to refi ne our responsible gaming program

to ensure it meets regulatory requirements and encourages

the responsible promotion and play of NSW Lotteries’ products

• Players 1

st

program will be introduced to alert players

to the importance of protecting their entries and providing

guidelines on the proper processes for checking tickets and

claiming prizes.

THE YEAR IN BRIEF

8 NSW LOTTERIES ANNUAL REPORT 2007

OUR RETAILERS

Objective: To ensure retailers meet our standards in selling our products and servicing our customers

Measure Target Result

Agent Satisfaction Survey 95% 95%

Agent Hotline – average time taken to answer calls <15 secs 6 secs

Key Activities and Issues Outlook and Future Challenges

• 1,524 on-line and 83 Instant Scratchies retail outlets

• Record commission on product sales paid to agents exceeded

$86 million – 1.6% up on previous year

• Over 10,000 visits to agencies by Territory Managers

• 61% of the total network in the agent reward and recognition

program ‘Top Shop’

• Over 1,100 agencies showcase the Corporation’s latest

retail image

• Over 1,000 promotions at key retail outlets

• Over 1,129 agents and staff trained in business management

and customer service skills

• Aiming to deliver another year of record commissions

• Building on our well-established retail network by identifying

new retail outlets in high traffi c areas

• An e-learning training program will be implemented via the

Internet to the entire retail agent network

OUR BUSINESS

Objective: Provide customers with easy and convenient access to our products

To ensure we continue to provide a sound and reliable gaming system

Measure Target Result

Number of on-line agencies 1,525 1,524

Gaming System uptime 99.99% 99.99%

Terminal availability – Mean Tickets Printed Between Failures 270,000 236,370

Key Activities and Issues Outlook and Future Challenges

• Processed over 284 million transactions through the

on-line gaming system – peak day was 1 March 2007

when nearly 1.8 million transactions were processed

• A number of signifi cant upgrades were made to the

Gaming System to further enhance lottery security

and customer care

• Successfully tested the Corporation’s Business Continuity Plan

• Continuing improvement in our core activities

• Agent website for retailers

THE YEAR IN BRIEF (CONTINUED)

NSW LOTTERIES ANNUAL REPORT 2007 9

OUR SHAREHOLDERS

Objective: To increase long-term Shareholder value by improved business performance

Measure Target Result

Duties paid to Governments $301.91 million $290.91 million

Profi t from ordinary activities before signifi cant item and

Income Tax Equivalent

$50.24 million $50.28 million

Return on Corporate Assets 48.07% 49.16%

Return on Average Shareholders’ Equity 107.54% 105.88%

Value Based Return 47.05% 47.17%

Operating expenses to sales 5.98% 5.79%

Profi t to sales 4.31% 4.47%

Key Activities and Issues Outlook and Future Challenges

• Total revenues exceeding $381 million were paid/payable to

the NSW Government in the form of duties, tax equivalent,

dividends and GST

• Despite lower sales, employee effi ciency, as measured by

total sales per employee was maintained at $6.6 million

• Aiming for another year of record return to Government

• In a diffi cult economic environment, the occurrence of jackpots

in the various games will be crucial to growth

• Changes to our games will enhance their competitive positions

and build on their unique strengths

• We will continue to focus on our profi tability and costs

OUR STAFF

Objective: To ensure the skills and knowledge necessary for our business are available when required

To ensure all our employees adopt a strong commercial orientation

Measure Target Result

Training expenditure per employee $1,535 $937

Training hours per employee 20 hours 17.73 hours

Sick leave ≤5 days 5.6 days

Staff turnover 5-10% 8.86%

Key Activities and Issues Outlook and Future Challenges

• A Staff Culture Survey was conducted to gauge employee

attitudes and opinions

• Commencement of a Management Development Program

• Organisational restructuring has occurred across

a majority of the organisation

• We will continue to develop the skills necessary to meet the

future needs of both the Corporation and its employees

THE YEAR IN BRIEF (CONTINUED)

10 NSW LOTTERIES ANNUAL REPORT 2007

WHO WE ARE

Following the passage of the State Lotteries Act, lottery

sales were legalised in NSW in 1931, when The State

Lotteries Office, as it was then known, was formed

and commenced operations. Since 1 January 1997, the

organisation has operated as a State Owned Corporation

established under the provisions of the NSW Lotteries

Corporatisation Act 1996.

NSW Lotteries Corporation is licensed by the Minister for

Gaming and Racing to sell lottery games in NSW pursuant

to the provisions of the Public Lotteries Act 1996. The

Corporation is also licensed to conduct lottery games in

the Australian Capital Territory (ACT).

WHAT WE DO – OUR CHARTER

In line with its statutory charter, NSW Lotteries has an

obligation to:

• Successfully develop, promote, conduct and otherwise

participate in any lawful forms of gambling and

gambling-related activities;

• Be a successful business and, to this end:

– to operate at least as efficiently as any comparable

businesses;

– to maximise the net worth of the State’s investment

in the Corporation;

– to be a successful participant (whether directly or

indirectly) in any other business or activity that the

Corporation determines is, or may be, of sound

commercial benefit to the Corporation;

• Exhibit a sense of social responsibility by having regard

to the interests of the community in which it operates

and by endeavouring to accommodate these interests

if it is possible to do so; and

• Exhibit a sense of responsibility towards regional

development and decentralisation in the way in

which the Corporation operates.

OUR GAMES

The Corporation is licensed to conduct these games in

NSW and the ACT:

• Lotto (drawn Monday, Wednesday and Saturday)

• Lotto Strike (drawn Monday, Wednesday and Saturday)

• Powerball (drawn Thursday)

• OZ Lotto (drawn Tuesday)

• Instant Scratchies

• Lucky Lotteries (drawn most weekdays)

• 6 From 38 Pools (conducted Saturdays)

Saturday Lotto, Powerball, OZ Lotto and 6 From 38 Pools

are national games operated in conjunction with other

Australian lottery operators. The Monday and Wednesday

Lotto game is operated in conjunction with the lottery

operators in South Australia and Western Australia.

BUSINESS PLANNING

The Corporation uses a formal Business Planning process

that continues to evolve and adapt to changes in the operating,

regulatory and competitive landscape. The process ensures

that NSW Lotteries remains focussed on achieving its key

business objectives. Each year, the major strategic issues

that are likely to impact the business are identified together

with appropriate strategies to address the challenges that

lie ahead. A comprehensive Business Plan is developed

which outlines the specific objectives, strategies and

actions to be undertaken to achieve our targets.

KEY AREAS FOR SUCCESS

There are five main aspects of our business that are

imperative to the achievement of our goals:

• Our Players • Our Retailers

• Our Business • Our Shareholders

• Our Staff

CORPORATE OBJECTIVES

Our Players

Objective: To increase sales and market share.

Objective: To ensure our products and services

consistently attract players and meet

their expectations.

Objective: To be recognised as a responsible

gaming operator.

Our Retailers

Objective: To ensure retailers meet our standards

in selling our products and servicing

our customers.

Our Business

Objective: Provide customers with easy and

convenient access to our products.

Objective: To ensure we continue to provide a

sound and reliable gaming system.

Our Shareholders

Objective: To increase long-term Shareholder value

by improved business performance.

Our Staff

Objective: To ensure the skills and knowledge

necessary for our business are available

when required.

Objective: To ensure all our employees adopt

a strong commercial orientation.

BALANCED SCORECARD FOR FISCAL 2007

The Business Plan incorporates an integrated set of

measures, with strategies, actions and targeted outcomes

that are continually reviewed and refined to ensure all

critical aspects of business performance are monitored.

Our performance against each of the corporate objectives is

detailed later in this report. The following table summarises

performance against the key target areas:

WHO WE ARE AND WHAT WE DO

NSW LOTTERIES ANNUAL REPORT 2007 11

OBJECTIVE MEASURE TARGET RESULT INDICATOR

OUR PLAYERS

To increase sales and

market share

Sales $1,165 m $1,124.44 m

✘

Note 1

To ensure our products and

services consistently attract

players and meet their

expectations

Bloc Market Share – combined

Saturday Lotto/OZ Lotto/Powerball

25.0% 24.1%

✘

Note 2

Customer Satisfaction Survey The survey was not

scheduled to be

undertaken in 2006/07

No. of complaints from players <200 152

✔

Customer Hotline – average time

taken to answer calls

<15

seconds

4 seconds

✔

Players Club membership 930,000 873,537

✘

Note 3

To be recognised as a

responsible gaming operator

Compliance with the Corporation’s

responsible gaming package

100% 100%

✔

OUR RETAILERS

To ensure retailers meet our

standards in selling our products

and servicing our customers

Agent Satisfaction Survey 95% 95%

✔

Agent Hotline – average time taken

to answer calls

<15

seconds

6 seconds

✔

OUR BUSINESS

Provide customers with easy and

convenient access to our products

Number of on-line agencies 1,525 1,524

✔

To ensure we continue to provide

a sound and reliable gaming system

Gaming System Uptime 99.99% 99.99%

✔

Terminal Availability:

Mean Tickets Printed

Between Failures

270,000 236,370

✘

Note 4

OUR SHAREHOLDERS

To increase long-term Shareholder

value by improved business

performance

Duties paid to Governments $301.91 m $290.91 m

✘

Note 5

Profi t from Continuing Operations

before Signifi cant Item and Income

Tax Equivalent

$50.24 m $50.28 m

✔

Return on Corporate Assets 48.07% 49.16%

✔

Return on Average

Shareholders’ Equity

107.54% 105.88%

✘

Note 6

Value Based Return 47.05% 47.17%

✔

Operating Expenses to Sales 5.98% 5.79%

✔

Profi t to Sales 4.31% 4.47%

✔

OUR STAFF

To ensure the skills and knowledge

necessary for our business are

available when required

Training expenditure per employee $1,535 $937

✘

Note 7

Training hours per employee 20 hours 17.73 hours

✘

Note 7

To ensure all our employees adopt

a strong commercial orientation

Sick leave ≤5 days 5.6 days

✘

Note 8

Staff turnover 5-10% 8.86%

✔

Note 1: Total sales were $40.56 million (or 3.5%) below target due to Powerball not performing to probability in the first half of the year.

Note 2: Bloc Market Share was adversely affected by low Powerball jackpots in the first half of the year.

Note 3: A greater reliance on jackpotting games increases the number of casual players – these players are less likely to become members of Players Club.

Note 4: Reflects the ageing of the selling terminals – now 7 years old.

Note 5: Duty paid was below target in proportion with the sales figure (see Note 1).

Note 6: Average shareholder equity increased through reduction in current liabilities compared to target.

Note 7: Training expenditure and hours did not meet target due to the rescheduling of training as a result of structural reviews across the organisation.

Note 8: The result exceeded target due to major health issues of a small number of staff.

12 NSW LOTTERIES ANNUAL REPORT 2007

OUR PLAYERS

WE OPERATE WITH INTEGRITY.

The overall portfolio is

healthy and well positioned

NSW LOTTERIES ANNUAL REPORT 2007 13

THE GAMES

GAMES OVERVIEW

During the year the NSW retail economy continued to

suffer the adverse effects of high interest rates and petrol

prices, felt especially in the areas of non-essential and

impulse retail purchases.

Lottery products were no exception. It was an extremely

challenging year for lottery games offering standard prize

offers, and even some larger jackpot offers failed to

motivate players as much as in previous years.

Major market research was conducted and a number of

game changes and marketing initiatives were introduced to

address the key aspects identified by our players.

In October 2006, a new Lotto branding campaign featuring

a new tagline and jingle ‘Live a Lotto Life’ was launched.

Other game enhancements were introduced to boost the

prize money available in Division One for regular Saturday

Lotto draws. Seven Superdraws offered massive prizes,

including a record $33 million offer in December 2006.

To boost Powerball’s position in the game portfolio,

game changes in August 2007 will introduce a new,

larger jackpot sequence.

OZ Lotto remains competitive as game changes

implemented in October 2005 deliver bigger jackpots,

including a record $25 million jackpot in July 2006.

Instant Scratchies underwent big changes in late 2006 to

provide a better winning experience for players, the most

important being an increase in overall prize payouts across

all Instant Scratchies games from 62.7% to 65.7%.

The jackpot in the $5 Jackpot Lottery, accelerated by the

game’s restructure in 2005, reached a record $6.18 million on

23 May 2007, passing the previous record of $6.05 million

set in July 2001. Its sibling, the $2 Jackpot Lottery, had

four jackpot runs this year, and both games benefited from

a makeover of brand icon “Lucky the Cat”, designed to

keep the game fresh and relevant to a new generation

of players.

The smallest game in the portfolio, 6 From 38 Pools,

continued to operate within a narrow category of player

appeal, boosted by promotions held during the Football

World Cup to capitalise on the game’s link to soccer.

The sales and performance of each game, along with

highlights for the year and other points of interest, are

summarised in Games at a Glance which follows:

OBJECTIVE: TO INCREASE SALES AND MARKET SHARE.

06/07

05/06

04/05

03/04

02/03

01/02

00/01

884.7

855.5

836.5

814.1

808.0

740.0

731.7

SALES OF THE LOTTO GAMES PORTFOLIO ($M)

Lotto (Mon, Wed, Sat & Strike) 480.4

Powerball 250.4

OZ Lotto 153.9

Instant Scratchies 138.3

Lucky Lotteries 95.6

Pools 5.8

Total 1,124.4

TURNOVER BY PRODUCT TYPE ($M)

14 NSW LOTTERIES ANNUAL REPORT 2007

2006/07

LOTTO (MON, WED, SAT & STRIKE)

SLOGAN

Live a Lotto Life

LAUNCHED

1979 (Monday), 1984 (Wednesday), 1995 (Lotto Strike),

2000 (Saturday)

HIGHLIGHTS

• There was a record $33 million offer for the December 2006

Saturday Superdraw.

• Seven Saturday Superdraws offered a total of $161 million

(compared to $156 million last year) – the highest amounts ever.

• Launch of new Lotto branding campaign in October 2006,

featuring a new tagline and jingle ‘Live a Lotto Life’ and

‘Brian the Seal’ media advertising and Point of Sale campaign.

• A new Superdraw creative campaign was introduced in

November 2006, offering greater fl exibility and signifi cant

cost reductions.

• Changes to the Saturday game were made to boost Division

1 prize money.

• 44 new Lotto millionaires created – bringing the total Lotto

millionaires to 788.

PERFORMANCE

• Superdraw performance affected by large Powerball and

OZ Lotto jackpot runs.

• Monday and Wednesday prize offers of $1 million and $750,000

struggle to compete with larger jackpot offers in the portfolio.

SALES

$480.41 million

VARIANCE ON PREVIOUS YEAR

Down 0.5%

SALES FOR SEVEN YEARS-GRAPH

SHARE OF NSWL TOTAL PORTFOLIO OF GAMES

42.7%

DIVISION ONE WINNERS

137 (45 millionaires including Lotto & Strike). As at 30 June 2007,

788 Lotto millionaires had been created since the launch of the

game in 1979.

LARGEST PRIZE OFFERED

$33 million (Saturday Lotto Superdraw)

PRIZEMONEY PAID

$278.93 million

OUTLOOK

• Increased competition from expected big OZ Lotto and

Powerball jackpots next year.

• Seven Superdraws will continue to be Lotto’s largest retail event.

• New campaign to retain existing customers and appeal to less

frequent players.

OUR PLAYERS

GAMES AT A GLANCE

SALES OF LOTTO – MON, WED, SAT & STRIKE ($M)

06/07

05/06

04/05

03/04

02/03

01/02

00/01

480.4

483.1

495.3

468.7

445.6

428.1

401.5

NSW LOTTERIES ANNUAL REPORT 2007 15

POWERBALL

OZ LOTTO

Spend the rest of your life A truckload of cash

1996 1994

• Powerball achieved a record $35.3 million jackpot in March 2007.

• Sales were a record $18.9 million for this draw as agent retail

activity increased signifi cantly.

• A total of $445 million worth of Division One prizes were on

offer in 2006/07, compared to $415 million for the previous year.

• Over 3.8 million prizes were paid during the year and 5

Powerball millionaires created.

• A single NSW winning entry received $11 million.

• The OZ Lotto game was revamped in October 2005.

2006/07 was the fi rst full year when the benefi ts of the

changes were realised.

• A record $396 million worth of Division One prizes was on

offer in 2006/07 compared to $250 million last year.

• The OZ Lotto offers included a record $25 million jackpot

in the fi rst week of July that attracted record sales and

entry numbers.

• The average fi rst division prize was $8.6 million compared to

$4.5 million in the previous year.

• Over 2.7 million prizes paid this year, over 900,000 more than

last year.

• Powerball started the year with lower jackpot offers and this

slowed sales growth. In the fi rst half of the year sales totalled

$98.5 million.

• Following a return to a larger jackpot sequence in the second

half of the year sales of $151.9 million were achieved.

• Powerball sales were impacted by the popularity of OZ Lotto

and its large jackpots.

• OZ Lotto’s popularity increased signifi cantly with jackpotting

closer to expectations and more prizes returned to players.

• 17.1 million entries were received this year (up 27.1% on the

previous year).

$250.43 million $153.93 million

Down 3.3% Up 35.7%

22.3% 13.7%

5 (5 NSW millionaires) 4 (4 NSW millionaires)

$35.3 million $25 million

$145.7 million $99.63 million

• Game changes are scheduled for August 2007 and will allow

the introduction of a larger jackpot sequence.

• The larger jackpots will increase player participation and boost

retail activity.

• Customer support for Powerball will increase in 2007/08.

• Further sales growth is forecast if jackpot activity falls within

statistical probability.

• Player participation rates will also show a further increase.

SALES OF POWERBALL ($M)

06/07

05/06

04/05

03/04

02/03

01/02

00/01

250.4

259.0

238.2

241.8

253.1

189.7

204.0

SALES OF OZ LOTTO ($M)

06/07

05/06

04/05

03/04

02/03

01/02

00/01

153.9

113.4

103.0

103.6

109.3

122.2

126.2

16 NSW LOTTERIES ANNUAL REPORT 2007

OUR PLAYERS

GAMES AT A GLANCE CONTINUED

2006/07

INSTANT SCRATCHIES

SLOGAN

Scratch Me Happy

LAUNCHED

1982

HIGHLIGHTS

• Increase in overall prize payout across all Instant Scratchies

games from 62.7% to 65.7%.

• All games were restructured to provide better prize wins

between $10 and $100.

• Special merchandise games, including Qantas Holiday Travel

Packs to the value of $44,500, and $75,000 worth of Gold Bullion.

• A major new branding campaign.

• Over 45 new Instant Scratchies games.

• Simplifi ed price points.

• The $5 Spider-Man Instant Scratchies game was a major

licensing opportunity for NSW Lotteries and brought all the

excitement of the record breaking Spider-Man 3 movie to an

Instant Scratchie game.

• $2 Happy Pig Lunar New Year Instant Scratchie.

• $2 Year of the Lifesaver Instant Scratchie to support our Surf

Lifesavers in their Centenary year.

• Biggest Agent Incentive Program ever, with one lucky Agent

winning a Toyota Yaris.

• Promotional offers, including Bonus ticket giveaways

at Christmas, Mother’s Day, Father’s Day & Easter plus

some exciting merchandise prizes in our Scratch “N” Win

promotions including 20 Harvey Norman Packages, 21 Hitachi

Entertainment Packs and 20 Toyota Yaris cars.

PERFORMANCE

Sales decline arrested and beginnings of growth.

SALES

$138.30 million

VARIANCE ON PREVIOUS YEAR

Down 8.4%

SALES FOR SEVEN YEARS-GRAPH

SHARE OF NSWL TOTAL PORTFOLIO OF GAMES

12.3%

DIVISION ONE WINNERS/FIRST PRIZE

AND JACKPOT WINNERS

2 x $5 Win For Life – equivalent to $1.125 million each

LARGEST PRIZE OFFERED

$5 Win For Life – equivalent to $1.125 million

PRIZEMONEY PAID

$90.16 million

OUTLOOK

• Increased sales as players experience better returns.

• New licensed games, new Win for Life prizes and fun Game

Play Scratchies including the popular Bingo games.

• Special holographic game to celebrate 25th Anniversary of

Instant Scratchies.

INSTANT SCRATCHIES SALES ($M)

06/07

05/06

04/05

03/04

02/03

01/02

00/01

138.3

151.0

167.4

166.2

172.3

176.1

164.7

NSW LOTTERIES ANNUAL REPORT 2007 17

LUCKY LOTTERIES

6 FROM 38 POOLS

You ought to buy yourself a lottery ticket Pools the smart choice

1931 Conducted by NSW Lotteries since 1989

• Overhaul of the Lucky Lotteries Brand Image and

Communication.

• New promotional website launched – www.feelinglucky.com.au.

• A full program of “Lucky Day” offers, including two Friday

13th promotions and highly successful cross-promotions with

Powerball and OZ Lotto.

• A new record jackpot of $6.18 million was set in the $5 Jackpot

Lottery on 23 May 2007 – this passed the previous record of

$6.05 million set in July 2001. As at 30 June 2007, the new

record jackpot stood at $6.69 million – this can be attributed to

the restructure of the $5 Jackpot Lottery in 2005.

• Checking of Lucky Lottery tickets, and payment of prizes, can

now be done immediately after the draw has been completed.

Previously there was a 24 hour delay for checking tickets in

both the $2 and $5 Jackpot Lotteries at agencies.

• Pools offered a total of $15 million worth of Division 1 prizes

during the year.

• Regular Pools promotions were held during the period of the

soccer World Cup tournament to reward loyal players and

boosted sales for these weeks by up to 40%.

• The $2 Jackpot Lottery has had slow sales, with four jackpot

runs this year, two of which were well short of probability.

• The $5 Jackpot Lottery has seen improved sales with a

growing jackpot.

Jackpots averaging $283 thousand were well below other game

offers and appealed to less players

$95.6 million $5.77 million

Down 20.8% Down 3.3%

8.5% 0.5%

• 193 x First prize winners – $2 Jackpot Lottery

• 4 x $2 Jackpot Lottery millionaires

• 23 x First prize winners – $5 Jackpot Lottery

5

$8.375 million in the $2 Jackpot Lottery in August 2006 $630,000

$61.12 million $2.11 million

• The $2 Jackpot Lottery sales are dependent on the size of its

jackpot prizes, but every effort will be made to maintain sales at

low jackpot levels and maximise sales at high jackpot levels.

• If the $5 Jackpot Lottery jackpot keeps growing, we can expect

signifi cant sales increases.

• Pools will continue to be supported by a player base attracted

to the game’s close link with soccer results. However, sales

will continue to decline as a result of larger offers from the

other games in the portfolio.

LUCKY LOTTERIES SALES ($M)

06/07

05/06

04/05

03/04

02/03

01/02

00/01

95.6

120.7

105.4

121.9

105.1

97.4

106.0

6 FROM 38 POOLS ($M)

06/07

05/06

04/05

03/04

02/03

01/02

00/01

5.8

6.0

6.7

6.7

7.5

7.3

8.3

18 NSW LOTTERIES ANNUAL REPORT 2007

LOOKING AHEAD

The overall portfolio is healthy and well positioned to

deliver the major prize offers our players demand.

To further increase player interest in our games and drive

sales growth during standard offers, the Corporation will

conduct branding campaigns and maximise promotional

opportunities.

NSW Lotteries will also focus on a number of new

distribution channels to generate incremental revenue,

while working hard to maintain the performance of our

business partners in the traditional agency network.

OUR PLAYERS

Mobile billboards to support OZ Lotto’s record $25 million jackpot

hit the streets of inner Sydney in July 2006.

NSW Government 287.4

ACT Government 6.9

Gross Income 102.6

GST on Gross Product Sales 48.3

Prizes 691.2

Total 1,136.4

PROJECTED SALES DISTRIBUTION 2007/2008 ($M)

NSW LOTTERIES ANNUAL REPORT 2007 19

WE PROVIDE EXCELLENT SERVICE

TO OUR CUSTOMERS.

PLAYER SERVICES

In an extremely competitive gaming and retail market and

with a mature range of products, there is a constant need

to build and enhance the existing relationship with our

players in order to maintain their loyalty. To ensure future

growth, the Corporation also needs to attract new players

to expand the overall base of players. To achieve these

goals, NSW Lotteries seeks to offer attractive products

whilst promoting the responsible play of lottery games.

We also need to ensure that the services we provide meet

and exceed the needs of our players. Our success in these

areas will ultimately be refl ected in our sales performance.

Our Corporate value refl ects the organisation’s commitment

to provide excellent service to our customers.

PLAYERS CLUB

This year saw a re-launch of the Players Club, aimed

at improving awareness of the service and increasing

membership beyond the current level of over 873,000

active players. For a small annual fee membership benefi ts

for players include:

• Immediate notifi cation of major prize wins;

• Smaller unclaimed prizes automatically mailed to

home address;

• The storing of ‘favourite’ entries thereby alleviating the

need to fi ll out entry forms;

• A convenient sized card easily carried in a purse

or wallet;

• Additional security if tickets are lost or stolen.

A main feature of the re-launch was the introduction

of a more modern style of Players Club card. Other

innovations included an updated information package,

e-mail notifi cation of jackpots and product promotions,

on-line Players Club registration, competitions conducted

on the Corporation’s website and advice of uncollected

prize wins when a Players Club card is next used at an

Agency (launching late 2007). In addition, players are able

to update their details via the NSW Lotteries website.

CALL CENTRE

As the fi rst contact point within NSW Lotteries, the

Call Centre is a critical link between players, retailers

and the Corporation.

Call Centre staff aim to help retailers resolve any issues

that have the potential to negatively impact their business

as quickly as possible, particularly restoring selling facilities

such as terminal hardware and telecommunications

equipment. They also provide advice on how to improve

customer service and ensure that the correct prize claim

process has been followed.

This year the Call Centre also began to initiate calls to

agents during major bonus offers and promotion periods

to increase awareness of player entitlements.

Other outbound call campaigns focused on helping agents

to maximise merchandising and point of sale presentation,

and offering new training opportunities for staff.

The service has been well received and has produced

positive results, with a number of agents signifi cantly

improving their business performance as a result of the

advice and support they have received from the Call Centre.

In addition to supporting the retail network, the Call Centre

handles hundreds of calls each day from players seeking

information on products, prize offers, games results,

agency locations, and how to claim prizes.

NSW Lotteries provides signifi cant resources to ensure that

agents and players are able to have their calls answered as

quickly and effectively as possible.

During the year, a major upgrade of telecommunications

technology and infrastructure was successfully

implemented including:

• The installation of a new PABX in March, including the

upgrade of handsets and the rationalisation of excess

lines; and

• The implementation of Computer Telephony Integration

(CTI) improving customer service levels through the use

of caller identifi cation, and automatically providing recent

Agent call history to Customer Service Representatives

answering calls.

OBJECTIVE: TO ENSURE OUR PRODUCTS AND SERVICES CONSISTENTLY

ATTRACT PLAYERS AND MEET THEIR EXPECTATIONS.

20 NSW LOTTERIES ANNUAL REPORT 2007

In addition, a new Interactive Voice Response (IVR)

system is scheduled for implementation in the fi rst half

of next fi nancial year to provide an enhanced presentation

of our traditional results and Players Club services, and to

add value to the Corporation’s marketing and promotional

activities. We will provide customers with an increased

range of historical results and dividends, multi-lingual

options, and the opportunity to leave a message for

follow-up and call back should the customer call outside

normal business hours.

During the year the Call Centre handled more than 116,000

calls from retailers and customers. Over 96% of these

calls were answered within 15 seconds, exceeding our

benchmark target of 90%. In addition, some 310,000

customers accessed our Results Services, with 27,000

callers requiring additional assistance from staff.

NETWORK SYNDICATES

Over the course of the year, more than 13,600 syndicates

were offered across the network in major Powerball and

OZ Lotto jackpot draws and Saturday Lotto Superdraws.

This service has proven to be extremely popular with

players and agents alike, especially when large prizes

are on offer, as it provides agents with additional selling

opportunities and players with the opportunity to try their

luck in a large system entry for a relatively small cost.

Some $13 million (or 1% of total sales) were generated

from syndicates and this clearly demonstrates the

increasing popularity of this entry type with players.

CONTINUALLY UPGRADING SECURITY

NSW Lotteries continually looks for ways to improve the

security of our players’ entries and prizes. This year all

existing prize payment and ticket cancellation processes

were reviewed to identify any area where controls could

be strengthened for the benefi t of our players.

A number of major enhancements were made to prize

claim processes during the year, including:

• ‘Freezing’ the terminal when large prizes are validated;

• Improving customer messaging through the selling

terminal customer Display Screen, increasing player

awareness of the results when their tickets are

checked; and

• Updating and reissuing our “Players Guide to Claiming

Prizes” instructions.

A new Players 1

st

program has been developed and will

be launched in the fi rst half of the next fi nancial year.

The aims of this initiative are to promote the benefi ts of

the Players Club service and to encourage players to take

a few simple steps to safeguard their ticket purchases.

CUSTOMER PRIVACY

NSW Lotteries values the privacy of its customers and

ensures that all player details are scrupulously protected.

There are strong protective mechanisms and associated

controls in place to safeguard both physical and electronic

access to confi dential information.

All personal and sensitive information held by the

Corporation is treated in accordance with the Privacy Act

1988 and the National Principles for the Fair Handling of

Personal Information.

Further information on our Privacy Policy can be obtained

by contacting NSW Lotteries or by visiting our website at

www.nswlotteries.com.au.

ELECTRONIC SERVICE DELIVERY

WEBSITE GROWTH

The NSW Lotteries website – www.nswlotteries.com.au –

is among the most visited websites in Australia. Continuing

our recent trend, this year our website recorded almost

nine million user sessions during the year, a 22% increase

on last year.

Website users are able to access all the information that

is available at retail outlets including copies of How to Play

material, prices and odds information.

During the year, a number of enhancements were

implemented to provide players using this channel of

communication with more information and easier access

to our services, including:

• Players Club membership drive – a number of exclusive

promotions for Players Club members were run on the

website and players were able to join on-line to protect

their prizes; and

• Enhanced Instant Scratchies Game Information – new

Instant Scratchies game information and major prizes

pages were launched in August to allow players to

identify when major prizes had been won. Previously this

information was only available in printed format.

OUR PLAYERS

06/07

05/06

04/05

03/04

02/03

01/02

00/01

8,966,086

7,364,200

4,882,140

3,247,025

2,473,168

1,977,000

1,500,000

USER SESSIONS

NSW LOTTERIES ANNUAL REPORT 2007 21

RESPONSIBLE GAMING

All the recent independent studies of gambling behaviour

quite clearly acknowledge that the “soft gaming” nature of

NSW Lotteries products is less likely to appeal to persons

susceptible to becoming over-involved in gambling than

the more “continuous” forms of gambling such as casino

games or electronic gaming machines.

However, with a customer base of more than two million

players, the Corporation plays a key role in fostering

responsible play and increasing awareness of this important

community issue in NSW and the ACT.

The Corporation, its advertising partners and its retail

network aim at 100% compliance with responsible

gaming regulations.

Our continuous achievement of this goal demonstrates

a high level of commitment and capability.

All our marketing and promotional activity is tempered by

the overriding principles of allowing our players to make

an informed choice about lottery play, and minimising any

possible negative impact.

We ensure that the privacy of our players is scrupulously

protected; all advertising is honest and responsible; and sale

to minors is clearly prohibited.

We also serve as one of the primary vehicles for promoting

the NSW Government’s G-line gambling referral service,

through the millions of tickets, entry forms and how to play

brochures printed each year, as well as signage in store

and on the Internet. As required by regulation, we make

available the Playsmart brochure – “know the odds of your

numbers coming up” – which provides the odds of winning

lottery games, and also publicises the G-line service.

The NSW Lotteries Responsible Gaming Program comprises

a statement of responsible gaming principles, codes of

self-regulation, player awareness activity, and a strategy to

ensure compliance with responsible gaming regulations in

NSW and the ACT.

Under this Program:

• Training sessions for new agents and their staff

cover responsible gambling and associated obligations.

Written information is also provided as part of an

induction package;

• All printed material dispatched to agents must be

formally approved to comply with responsible

gambling requirements;

• All agencies display a NSW Lotteries poster advising

that it is illegal to purchase lottery games by credit

and for under 18 year-olds to play. Copies of the poster

are regularly distributed and are also available to agents

on request;

• The G-line message is included on any printed matter

prepared by agents;

• The “Playsmart” brochure is displayed. Copies are

regularly distributed and are also available on request;

• Copies of all Game Rules are available on request; and

• Alcohol is not used in any lottery promotional activity.

In addition to training and regular written reminders,

agents’ compliance with responsible gambling requirements

is formally checked by NSW Lotteries Territory Managers

on each of the approximately 11,000 visits conducted

annually. Senior Managers review Territory Managers’

reports and address any defi ciencies not resolved at the

time of the visit.

Internal and external reviews during the fi scal year found

NSW Lotteries and its retail network continue to fully

comply with Responsible Gaming regulations and encourage

the responsible play of lottery games.

OBJECTIVE: TO BE RECOGNISED AS A RESPONSIBLE GAMING OPERATOR.

WE ARE SOCIALLY RESPONSIBLE.

The hopes and dreams of millions rest on the luck of the Lotto draw.

22 NSW LOTTERIES ANNUAL REPORT 2007

PLAYERS 1

ST

Just as harm minimisation is a crucial aspect of corporate

social responsibility for any lottery operator, appropriate

security controls and customer care measures are also vital

elements in total player protection.

NSW Lotteries has developed a major new awareness

campaign to ensure players know how to protect their

prizes and to encourage them to communicate directly to

NSW Lotteries if they have any concerns about how their

transactions have been handled.

Called Players 1

st

, the campaign will be implemented during

the fi rst quarter of the 2008 fi nancial year at point of sale

and on the NSW Lotteries website.

It includes:

• Posters and stickers with Players 1

st

information at all

1,600 agencies around NSW and the ACT;

• A dedicated customer hotline/e-mail address to report

any concerns and allow feedback on improving security

and customer care;

• Consolidation of other information about claiming prizes

and player registration under the Players 1

st

banner and

a dedicated brochure on the Players 1

st

program;

• Development of a consumer protection area on the NSW

Lotteries website, reproducing the retail information;

• Additional training for agents, focusing on a simple

easy-to-follow multi-step process for handling selling,

ticket checking and prize payment; and

• Communication of these initiatives, along with the

benefi t of player registration through Players Club,

to players.

Through Players 1

st

we aim to continue to earn the trust of

our players, and to encourage their ongoing support of the

individual agents who make up our retail network.

OUR PLAYERS

Lights, camera, action! “Brian” the seal gave up his day job at

Coffs Harbour’s Pet Porpoise Pool to fi lm the Live a Lotto Life

commercial. In this scene, he gets ready to check his winning

ticket at the Coffs Harbour Newsagency. (Courtesy of The Coffs

Coast Advocate)

NSW LOTTERIES ANNUAL REPORT 2007 23

OUR RETAILERS

WE VALUE THE RELATIONSHIP

WITH OUR RETAILERS.

The diversity of the network

continues to grow

24 NSW LOTTERIES ANNUAL REPORT 2007

THE RETAIL NETWORK

Our network of more than 1,600 lottery retailers spread

throughout NSW and the ACT provides the vital link in the

delivery of our lottery games to consumers. The diversity of

the network continues to grow with a wide range of small

businesses selling lottery products including newsagents,

petrol stations, convenience stores, bookstores,

supermarkets, bottleshops and clubs.

This increasing range of business types reflects the

Corporation’s strategy of providing our products in

locations that attract new customers and provide greater

convenience and ease of access.

Lottery outlets earned over $86 million in revenue from the

sale of lottery games during the year. This represented an

increase of 1.6% over the previous year.

This increase in lottery handling fees continues the trend of

recent years. Total revenue to lottery agents has increased

by more than 37% over the last five years.

This rate of growth is twice the rate of growth in the CPI

over the period and has resulted from a deliberate strategy

by the Corporation of continually increasing the value of the

lottery franchise in the network.

DEVELOPING THE NETWORK

The Corporation continued its strategy of establishing

agencies in new and redeveloped retail complexes and

areas of increasing population growth. There were 30 new

on-line agencies appointed during the year, including the

upgrade of 10 existing Instant Scratchie only agencies.

Around 150 agencies – less than 10% of the network –

changed hands throughout the year, compared to 180 last year.

As new agents join the network, we focus on providing

them with the necessary training in technical, business and

sales skills to ensure they provide the best possible service

to our players

Lottery agents are supported in the field by a team of

Territory Managers based in metropolitan and regional

locations around the State who made around 11,000 visits

during the year.

To further assist the retail network in meeting the needs

of our customers, agents also receive a weekly newsletter

with instructions, procedures, and selling tips, along with

regular memos and messages delivered through weekly

courier deliveries and via their terminal display screens.

TOP SHOP AWARDS

‘Top Shop’ is NSW Lotteries’ agent reward and recognition

program and has now been running for over 10 years. The

program has proven to be an effective means of motivating

and rewarding our agents for outstanding performance. The

ultimate beneficiaries of this outstanding performance are

our customers.

This year a record 1,000 agents registered for the program,

representing 61% of the network. The collective results

achieved by agents in the program have constantly shown

growth rates beyond the network average, meaning

Top Shop agents get even more from their business.

The annual Top Shop Awards Night was held at Sydney’s

Star City Casino again this year with the theme focusing

on the program’s 10th Anniversary. The Award winning

agencies for this year were:

TOP SHOP FOR 2006/2007

Theobalds Newsagency – Bathurst

TOP SHOP FINALISTS

Eastgardens Newsagency – Eastgardens

Talbragar Street Newsagency – Dubbo

Young Newsagency – Young

Bendalong Newsagency – Bendalong

NSW LOTTERIES CHAIRMAN’S AWARD

Rutherford Newsagency – Rutherford

MERCHANDISING AWARD

Nambucca Heads Newsagency – Nambucca Heads

TOP SHOP AGENCY CO-ORDINATOR AWARD

Kristin Moratidis – Greenhills Newsagency – East Maitland

TOP SELLING AGENCY IN THE NSW LOTTERIES RETAIL NETWORK

Eastgardens Newsagency – Eastgardens

OBJECTIVE: TO ENSURE OUR RETAILERS MEET OUR STANDARDS IN SELLING OUR

PRODUCTS AND SERVICING OUR CUSTOMERS.

06/07

05/06

04/05

03/04

02/03

01/02

00/01

86.0

84.7

79.2

74.1

71.1

62.5

59.8

COMMISSION PAID TO AGENTS ($M)

OUR RETAILERS

NSW LOTTERIES ANNUAL REPORT 2007 25

THE TOP SHOP IN EACH NSW LOTTERIES SALES TERRITORY

Territory 1 & 7 North Sydney Shoppingworld Newsagency

– North Sydney

Territory 2 Eastgardens Newsagency – Eastgardens

Territory 3 Cronulla Plaza Newsagency – Cronulla

Territory 4 Narellan Newsagency – Narellan

Territory 5 Winston Hills Newsagency – Winston Hills

Territory 6 Kenthurst Village News – Kenthurst

Territory 8 Greenhills Newsagency – East Maitland

Territory 9 Ocean Shores Newsagency & Post Office

– Ocean Shores

Territory 10 Theobalds Newsagency – Bathurst

Territory 11 Young Newsagency – Young

Territory 12 Bendalong Newsagency – Bendalong

RETAIL PROMOTIONAL ACTIVITY

Promotional activity at the point of sale is a valuable

reinforcement of mainstream media advertising. It

continues to be an effective way of generating store traffic,

creating excitement for players and increasing sales for the

agency network.

During the year, over 1,000 local in-store promotions were

conducted to support major events such as Mother’s Day,

Father’s Day, Christmas, Friday 13th, the seven Saturday

Lotto Superdraws, and big jackpots in Powerball, OZ Lotto

and Lucky Lotteries. These also included internal agency-

run promotions, such as second-chance draws.

AGENCY SERVICES

RETAIL TRAINING

The effective training of agents is critical to ensuring that

our customers receive the quality of service that they

expect from a lottery agent. Our comprehensive agent

training program is designed to assist agents to reach

the highest possible standards of retail operation and,

ultimately, provide excellent service to our customers.

It also ensures that retailers are equipped with the

knowledge to meet all legal and operational requirements.

This year, more than 1,100 retail managers and employees

were trained. The courses included in the training program are:

• The Lottery Management Course – a comprehensive

four day compulsory course for new and changeover

agencies;

• The Instant Lottery Management Course – a half-day

course for agents who sell Instant Scratchies only;

• The Terminal Operations Course – one day course

for agency staff;

• The Instant Scratchie Management and Reconciliation

Course; and

• Responsible Gambling training – including specialised

training for our ACT Agents and staff in the separate

regulations in force in that jurisdiction.

We also continued to offer our very successful ‘High

Performance Selling’ seminars across NSW, providing

agents and staff with a multitude of practical tips to help

build their sales. Results have demonstrated that agents

who use the skills from this seminar obtain significant real

sales increases.

With a widely distributed network, NSW Lotteries seeks

to provide training that is cost-effective, convenient and

tailored to the business requirements of small retailers.

As the Top Shop for 2007 is announced, the stage explodes

in a dazzling pyrotechnic display.

…and the winner is Theobalds Newsagency at Bathurst. Accepting

the award is the owner, Robert Theobald.

26 NSW LOTTERIES ANNUAL REPORT 2007

Advances in distance education technology means that it

is now possible to implement a major e-learning program,

which will be delivered via the Internet to the entire retail

agent network.

E-learning courses will cover vital lottery retail skills and

knowledge including operating the Altura selling terminal;

product information; lottery operational policies and

procedures; and customer service.

The new program means that all our agencies will have

ready access to high quality training, and customers can

rely on a skilled and competent agency network providing

high levels of service no matter where they are located

throughout NSW and the ACT.

RETAIL IMAGE

The most visible component of any NSW Lotteries agency

is the retail image, which provides the signal to players

that they can purchase their lottery entries at that outlet.

This year NSW Lotteries has continued to expand the

implementation of its current retail image into around

1,200 agencies, which is over 75% of the retail network.

AGENCY SATISFACTION SURVEY

Providing agents with the support they need to sell our

products remains a high priority of the Corporation. Our

success in providing that support is measured through

an annual survey of agent satisfaction with the services

offered by the Corporation. This year 95% of agents gave

NSW Lotteries an overall rating of either extremely satisfied

or very satisfied. Individual areas of the Corporation

received ratings of between 88% and 90% indicating a

very high level of knowledge, professional expertise and

customer service were provided.

The Corporation is committed to maintaining these levels

of satisfaction into the future and will be surveying our

agents again in 2008/09 to ensure that our high standards

of service continue to be delivered.

OUR RETAILERS

Chris Bristow, owner of the Bogangar Newsagency with just some of the $1.83 million in prize money scooped by one of his lucky

customers in the $22 million Saturday Lotto Superdraw in September 2006. (Courtesy of the Daily News)

NSW LOTTERIES ANNUAL REPORT 2007 27

OUR BUSINESS

WE CONTINUOUSLY IMPROVE

OUR BUSINESS.

All our business

processes must

be at the forefront

of industry best

practice

28 NSW LOTTERIES ANNUAL REPORT 2007

In order to maintain high levels of customer satisfaction, all

our business processes must be at the forefront of industry

best practice, particularly where the on-line gaming system

is concerned.

Each year an Information Technology Strategic Plan is

developed which identifi es the key issues and business

solutions needed to maintain the reliability and integrity

of the Corporation’s business systems. The underlying

objective is to provide our retailers and players with the

best and most reliable access to our products and services.

THE GAMING SYSTEM

PERFORMANCE

Annual system performance indicators clearly demonstrate

that the sound Information Technology business strategies

adopted by NSW Lotteries have been successful in

delivering continued high levels of service to our retail

network and our customers.

The on-line gaming system continued its industry leading

performance, achieving its benchmark target of 99.99%

availability during selling hours. The telecommunications

network that links the on-line agencies to the central

processing facility achieved 99.94% availability, which was

slightly below the target of 99.96%.

More than 284 million transactions were processed through

the on-line gaming system during the year, with a peak

of around 1.8 million transactions processed on a single

day during selling for the massive $35.3 million Powerball

jackpot drawn on 1 March 2007.

GAMING SYSTEM UPGRADES

A number of signifi cant upgrades were made to the

gaming system during the year (including replacement

of management terminals, software, system servers and

other hardware), as well as the operating system on which

the gaming system runs.

A range of gaming system changes were implemented

which enhanced the processes associated with the

payment of prizes.

An important new feature introduced this year was the

terminal “freeze” functionality, aimed at ensuring that

unregistered major prizewinners are immediately alerted to

the status of their ticket.

NSW Lotteries was one of the fi rst jurisdictions in the world

to introduce this new feature that is part of our business

objective of constantly updating key systems and controls

to meet the challenges of a dynamic and constantly

changing environment.

OBJECTIVE: PROVIDE CUSTOMERS WITH EASY AND CONVENIENT ACCESS TO

OUR PRODUCTS.

TO ENSURE WE CONTINUE TO PROVIDE A SOUND AND RELIABLE GAMING SYSTEM.

06/07

05/06

04/05

03/04

02/03

01/02

00/01

99.99

99.99

100.00

99.99

99.99

99.99

99.96

SELLING SYSTEM UPTIME (%)

OUR BUSINESS

The bold and attractive NSW Lotteries Retail Image ensures

that agencies stand out in the highly competitive retail

environment in NSW and the ACT.

NSW LOTTERIES ANNUAL REPORT 2007 29

TELECOMMUNICATIONS NETWORK

The current telecommunications network that connects

retail outlets to the gaming system is due to be phased out

over the next couple of years. Work has begun on replacing

the current network, which is based on Telstra’s Digital

Data Service. The new network is expected to be brought

into service within the next two years and will be based on

Internet Protocol and wireless technologies.

STAFF AND AGENT WEBSITES

INTRANET PORTAL

The Corporation’s Portal plays a crucial part in the way

NSW Lotteries staff share and use information within the

Corporation. During the year, a number of changes were

made to the functions of the portal, which consolidated

the site’s position as the fi rst port of call for staff to access

and retrieve business information. An additional portal

was implemented during the year, focusing on agency-

related information. This new site ensures that the latest

information, be it sales or service related, is immediately

available, thus improving the service that the Corporation

provides to its agencies.

AGENT WEBSITE

A new agent website was piloted during June 2007 and

will be rolled out to all agents in late 2007. The new site

will give our 1600 lottery agents and their staff access to

a broad range of information such as agency sales details,

policies and procedures, network conditions, upcoming

promotions and special offers, and general selling tips.

The site will also provide access to tailored computer-

based training for agents and staff. As outlined earlier in

this report under ‘Retail Training’ this e-learning training

and education system will generate signifi cant savings

and assist agents and their staff in remote locations who

currently fi nd it diffi cult to attend face-to-face training

offered in Sydney and other major population centres.

BUSINESS CONTINUITY

The NSW Lotteries Business Continuity Plan focuses on