01

2019

TRENDS REPORT

SECTION 01

INTRODUCTION

2019

Trend s

in the supply of accounting

graduates and the demand

for public accounting recruits

02

2019

TRENDS REPORT

SECTION 01

INTRODUCTION

By the Association of International Certifi ed Professional Accountants

ARC Research, an SVC Company

Copyright © 2019 Association of International Certifi ed Professional Accountants.

All rights reserved.

Requests for permission to make copies of any part of this work should be mailed to:

Permission Department, The Association, 220 Leigh Farm Road, Durham, NC 27707-8110

1234567890ACD920

01

2019

TRENDS REPORT

SECTION 01

INTRODUCTION

02

06

08

18

27

31

34

Introduction

A letter from the AICPA’s Academic-in-Residence

Interpreting the data

Key insights

Summary

Trends in the supply of accounting graduates

Supply | Enrollment

Supply | Graduates

Trends in the demand for public accounting recruits

Demand | New hires

Demand | Future expectations

U.S. fi rm demographics

Uniform CPA Examination

®

Appendix

CPA pipeline programs

Methods

Endnotes

Table

of Contents

02

2019

TRENDS REPORT

SECTION 01

INTRODUCTION

A message from

the AICPA’s

Academic-in-Residence

Thank you for your interest in the 2019 Trends in the Supply of

Accounting Graduates and the Demand for Public Accounting Recruits

report. This biennial report identifi es key trends in U.S. accounting

enrollments and graduations as well as hiring of new graduates in

the public accounting sector. Published since 1971, Trends provides

statistical projections and respondent expectations based upon

university responses for the 2017-2018 academic year and fi rm

responses for the 2018 calendar year.

The accounting profession is rapidly evolving. Technological innovations, especially in data science

and analytics, are becoming a more common part of the profession and are changing the way we do

business and whom we hire to do it. The fi ndings in this report refl ect those changes. The responses

received from participating U.S. universities and public accounting fi rms provide us with insights into

how these changes are impacting the profession from both a supply and a demand perspective.

This data, against the backdrop of the current macroeconomic environment – which impacts college

enrollment levels, choice of major, and hiring levels – provides us a snapshot of the profession in time

and allows us to forecast future trends.

Projected bachelor’s accounting enrollments are the second highest on record since the inception of our

Trends report. While there was a 4% decline from the 2016 number, they remain higher than 2014 levels.

Master’s and Ph.D. enrollments continue to decline (6% and 23%, respectively), with many opting to

enter or remain in the workforce in lieu of pursuing an advanced accounting degree or to pursue other

avenues for advanced education. As mentioned in the last Trends report, the previous infl ux of graduate

students we saw may have been infl uenced by the Great Recession of 2008. We could be seeing an

impact from both economic conditions and an expansion of the alternatives available to potential

graduate accounting students.

The more telling projections in this report about the profession come from the demand side in public

accounting. New hires assigned to audit-related services increased 4 percentage points. Across the

last two Trends reports, we have experienced an approximate 30% decline in hiring of new accounting

graduates. The marketplace continues to demand different competencies and, while accounting

graduates are still being hired, fi rms are seeking other skill sets to expand services. We are seeing that

the gap in skills required in the profession, especially as it relates to technology needs, is being met with

non-accounting graduates. There is also anecdotal evidence to suggest that some of this technology-

specifi c hiring is occurring at the experienced hire level.

After a signifi cant increase in the number of new CPA Exam candidates in 2016, largely attributed to the

new version of the exam launching in 2017, the number of candidates in 2018 dipped to its lowest level

in 10 years.

Yvonne Hinson, CPA, CGMA, Ph.D.

Academic in Residence, Academic &

Student Engagement

Association of International Certifi ed

Professional Accountants

03

2019

TRENDS REPORT

SECTION 01

INTRODUCTION

The increase in non-accounting graduate hiring and the decline in new exam registrants present areas of

opportunity. The AICPA has been working with key stakeholders on a number of profession-wide initiatives that

attract, inspire, and engage the next generation of CPAs.

These initiatives include the CPA Evolution project in partnership with the National Association of State Boards

of Accountancy. The goal of this project is to ensure that CPAs continue to have the competencies needed to

support an accounting profession that plays a critical role in protecting the public interest.

We believe that for CPAs to continue to serve the marketplace, they must incorporate new and different skill sets

and that it is incumbent upon the profession to take steps to cultivate these rapidly changing skills in accounting

graduates and newly licensed CPAs.

On a parallel effort, we have been working with universities to deepen the connection between practice and

academia to better incorporate the skills of the future into current curricula and bring more CPAs into the

classroom. The Accounting Accreditation Practitioner Engagement Program, which places CPA practitioners on

Association to Advance Collegiate Schools of Business (AACSB) accounting accreditation committees and peer

review teams, and the Accounting Doctoral Scholars Program, which provides funding for CPAs to obtain their

doctorates and ultimately teach, are helping to bridge the gap between practice and academia.

To ensure a diverse and robust pipeline of talent enters the profession, we have expanded our awareness efforts

at the high school level. The AICPA Accounting Program for Building the Profession trains high school educators

to teach a higher order college-level accounting class and increases students’ knowledge about the accounting

profession. We are working in collaboration with the National Academy of Finance, Junior Achievement, and

organizations such as the National Association of Black Accountants and the Association of Latino Professionals

for America to increase the likelihood that students from a multitude of backgrounds consider accounting a viable

option early in their career decision-making process. AICPA scholarships and programs such as the Accounting

Scholars Leadership Workshop help ensure accounting students have a meaningful and successful educational

journey.

This report also fi nds that, while enrollment by gender is nearly even at both the bachelor’s and master’s levels,

racial/ethnic diversity has increased with the highest percentage of non-white enrollees to date. There are many

other stakeholder and AICPA initiatives, like the ones mentioned above, around diversity in our profession, and we

are seeing positive movement here.

I encourage you to look at Appendix A in the back of this report for more information on how the AICPA, along

with other stakeholders, is working to attract, inspire, and engage the next generationof CPAs.

While this Trends report focuses on public accounting hiring of new graduates (it does not include trends in hiring

of experienced accountants or in sectors outside public accounting), those seeking accounting careers are hired

into a multitude of positions out of college and have even more opportunities as they gain experience in the

profession. According to the Bureau of Labor Statistics, employment in the broader accounting and auditing fi eld

is expected to grow faster than the average for all occupations through 2026 (Accountants and Auditors, 2019).

Once again, we are very appreciative of the universities and fi rms that took the time to participate in this long-

standing research initiative as it provides essential insights to our many stakeholders and interested parties within

the accounting profession.

Thank you,

Yvonne Hinson, CPA, CGMA, Ph.D.

Sources: Accountants and Auditors: Occupational Outlook

Handbook: https://www.bls.gov/ooh/business-and-financial/accountants-and-auditors.htm#tab-6

04

2019

TRENDS REPORT

SECTION 01

INTRODUCTION

The Trends report is broken down into three major reporting sections:

trends in supply, trends in demand, and fi rm demographics. There

is also a section that reports CPA Exam candidate data, as well as

an appendix that contains descriptions of AICPA programs that

are dedicated to growing the pipeline, survey methodologies, and

endnotes containing any changes or considerations for specifi c data.

The data presented for overall numbers of enrollments, graduates,

and hires are based on statistical projections. These projections are

calculated by creating a model that is meant to predict population

values based on data collected in the current survey cycle. This

data should be used to look at the overall trends in the reporting

areas, rather than taken as a statement of exact values.

Demographics and population breakdowns for enrollments, graduates,

new hires, and fi rm demographics are descriptive statistics. The data

received from respondents were weighted (based on variables such

as faculty size, number of employed CPAs, etc.) to represent the total

population. Demographic data by fi rm size are unavailable for this

period due to insuffi cient sample sizes in several fi rm size categories.

All trends data presented in the report includes only data that is

comparable. In some instances, data from previous reports was

recalculated for comparability purposes and is marked with endnotes.

Other changes or considerations are also endnoted within the report

and can be examined in the methods section of Appendix B.

The 2019 Trends in the Supply of Accounting Graduates

and the Demand for Public Accounting Recruits report

includes both statistical projections and descriptive statistics.

Please contact us at [email protected] with any questions or feedback as

we strive to make the information in these surveys relevant to your needs.

Interpreting

the data

04

2019

TRENDS REPORT

SECTION 01

INTRODUCTION

05

2019

TRENDS REPORT

SECTION 01

INTRODUCTION

Key

insights

Accounting Enrollments

Total projected accounting enrollments are down 4% from the highs of 2016, but are still

among the highest on record. Master’s enrollments are down 6% from 2016. Racial/ethnic

diversity has increased in the 2017-18 academic year. Universities have reported increases

in Hispanic or Latino enrollees of 3 and 8 percentage points at the bachelor’s and master’s

levels, respectively. Seventy-two percent of bachelor’s of accounting programs and 65% of

master’s of accounting programs expect to have the same or higher enrollment in 2019.

Accounting Graduates

Projected accounting graduates trended downward in the 2017-18 academic year, with decreases

of 4% at both the bachelor’s and master’s levels and overall. In 2018, female accounting graduates

outnumbered male graduates at the master’s level. Racial/ethnic diversity has increased in accounting

graduates, with a 7 percentage point increase in Hispanic or Latino accounting graduates.

Hiring

In 2018, new hires assigned to audit-related services increased by 4 percentage points, while

new graduates assigned to taxation declined by 4 percentage points. Hiring of new accounting

graduates slowed 11%. Across the last two Trends reports, we have experienced an approximate

30% decline in hiring of new accounting graduates. Non-accounting hires as a percentage of all

new graduate hires are up 11 percentage points to 31%. See footnote for more information.

Hiring Expectations

Of fi rms that hired one or more accounting graduates in 2018, 58% expect to hire the

same number or more in 2019. Ninety percent of all U.S. CPA fi rms expect to have the

same number or more CPAs on staff in 2019.

CPA Examination

The number of CPA Exam takers increased in 2015 and 2016 in preparation of the new CPA

Exam that launched in April 2017. CPA Examination candidates decreased 7% between

2017 and 2018. The number of CPA Exam candidates who passed their 4th section of the

exam decreased 6% between 2017 and 2018.

Footnote: New categories were collected for “non-accounting hires” in 2018, which may account for

some of the increase, but even without new categories there was still a significant increase.

06

2019

TRENDS REPORT

SECTION 02

SUMMARY

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

1971-72

1972-73

1973-74

1974-75

1975-76

1976-77

1977-78

1978-79

1979-80

1980-81

1981-82

1982-83

1983-84

1984-85

1985-86

1986-87

1987-88

1988-89

1989-90

1990-91

1991-92

1992-93

1993-94

1994-95

1995-96

1996-97

1997-98

1998-99

1999-00

2000-01

2001-02

2002

-0

3

2003-04

2004-05

2005-06

2006-07

2007-08

2008-09

2009-10

2010-1

1

2011-12

2012-13

2013-14

2014-15

2015-16

2016-1

7

2017-18

Summary

1.1 Accounting enrollment by program | 1993-2018

Total projected accounting enrollments are down 4% from the highs of 2016, but are still among the highest on record.

(See notes a, b, and c on page 39)

Projected accounting graduates trended downward in the 2017-18 academic year with decreases of 4% at both levels and overall.

(See note a on page 39)

1.2 Bachelor’s and master’s of accounting degrees awarded | 1971-2018

Total graduates

Bachelor’s

Master’s

1993-94

1994-95

1995-96

1998-99

1999-00

2000-01

2001-02

2002-03

2003-04

2006-07

2007-08

2009-10

2011-12

2014-15

2015-16

2017-18

207,806

216,482

207,071

201,570

187,534

181,075

173,299

142,735

141,175

133,435

134,775

127,960

134,050

174,010

192,870

189,863

27,482

29,428

39,641

29,648

29,464

24,065

21,253

18,795

17,540

12,565

10,375

9,455

8,620

9,430

10,010

10,114

2,645

3,177

2,068

2,840

2,822

2,305

3,239

3,595

3,550

3,555

2,395

3,130

2,600

4,760

6,510

5,942

3,208

3,014

3,107

5,132

5,100

4,166

4,482

4,030

5,270

4,065

4,000

2,445

3,770

3,360

3,510

3,398

732

946

1,195

1,189

1,188

1,224

1,095

955

1,085

890

800

680

770

770

870

1,002

253,047

253,082

240,379

226,108

212,835

203,368

170,110

168,620

154,510

152,345

143,670

149,810

192,330

213,770

210,319

Bachelor’s

Master’s in

Accounting

Master’s in

Taxation

MBA

Accounting

Ph.D. Total

241,873

76,542

54,947

21,595

07

2019

TRENDS REPORT

SECTION 02

SUMMARY

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

1971

1972

1973

1974

1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

Total graduates

Bachelor’s

Master’s

In 2018, hiring of new accounting graduates slowed 11% - a smaller shift than the decline between 2014 and 2016. (See note d on page 39)

1.3 New graduates hired into accounting/finance functions

of U.S. CPA firms | 1971-2018

1.4 Growing diversity in the CPA profession | 2018

This graph shows the 2017-18 race/ethnicity data at each major point in the CPA education and career path – from bachelor’s enrollees, to

bachelor’s and master’s graduates (the most likely to go into public accounting), all the way through partners. These numbers are derived

from both the survey of universities’ enrollments and graduates and the survey of fi rms’ hiring.

American Indian/

Alaskan Native

Asian/Pacifi c Islander

Black/African American

Hispanic/Latino

Multiethnic

Other

White

Total Non-White

Demand survey Supply survey

Enrollments

(BA)

Graduates

(BA+MA)

New Grad Hires

Professional

Staff

CPAs

Partners

9%

16%

29%

42%

44%

91%

84%

71%

58%

56%

0.4%

0.3%

0.4%

4%

6%

1%

1%

2%

2%

2%

2%

4%

6%

16%

15%

1%

2%

4%

6%

10%

4%

10%

17%

13%

11%

0.2%

0.2%

0.2%

0.3%

1%

0% 20% 40% 60% 80% 100%

30%

70%

0.2%

2%

10%

4%

14%

0.1%

30,903

19,498

11,405

8

2019

TRENDS REPORT

SECTION 03

SUPPLY | ENROLLMENT

Trends

in the supply

of accounting

graduates

Bachelor’s

Enrollment

Masters

Enrollment

Ph.D.

Enrollment

1993-94

1994-95

1995-96

1998-99

1999-00

2000-01

2001-02

2002-03

2003-04

2006-07

2007-08

2009-10

2011-12

2014-15

2015-16

2017-18

189,863

192,870

174,010

134,050

127,960

134,775

133,435

141,175

142,735

173,299

181,075

187,534

201,570

207,071

216,482

207,806

19,454

20,030

17,550

14,990

15,030

16,770

20,185

26,360

26,420

28,974

30,535

37,386

37,620

44,816

35,619

33,335

1,002

870

770

770

680

800

890

1,085

955

1,095

1,224

1,188

1,189

1,195

946

732

210,319

213,770

192,330

149,810

143,670

152,345

154,510

168,620

170,110

203,368

212,834

226,108

240,379

253,082

253,047

241,873

Total

Enrollment

9

2019

TRENDS REPORT

SECTION 03

SUPPLY | ENROLLMENT

(See notes a, b, and c on page 39)

2.1 Trends in total enrollment in accounting programs | 1993-2018

Master’s

Enrollment

10

2019

TRENDS REPORT

SECTION 03

SUPPLY | ENROLLMENT

American Indian/

Alaskan Native

Asian/Pacifi c Islander

Black/African American

Hispanic/Latino

Multiethnic

Other

White

51%49%

Male

Female

2.2 Demographics of bachelor’s and master’s of accounting enrollees | 2017-18

0.5%

11%

9%

15%

2%

6%

56%

by

gender

by

race/ethnicity

international students

enrolled in U.S.

accounting programs

(See note e on page 39)

10%

dual-degree

seeking

5%

11

2019

TRENDS REPORT

SECTION 03

SUPPLY | ENROLLMENT

American Indian/

Alaskan Native

Asian/Pacifi c Islander

Black/African American

Hispanic/Latino

Multiethnic

Other

White

51%49% 50%50%

2.3 Accounting enrollees by gender | 2017-18

Male

Female

2.4 Accounting enrollees by race/ethnicity | 2017-18

2.5 Accounting enrollees – international students

in U.S. accounting programs | 2017-18

1%

11%

10%

15%

2%

6%

56%

0.3%

16%

7%

15%

2%

7%

53%

8% 19%

bachelor’s master’s

bachelor’s master’s

bachelor’s master’s

12

2019

TRENDS REPORT

SECTION 03

SUPPLY | ENROLLMENT

2.6 Trends in bachelor’s and master’s of accounting enrollees

by gender | 2006-18

Male

Female

2.7 Trends in bachelor’s and master’s of accounting enrollees

by race/ethnicity | 2006-18

2.8 Accounting program enrollment expectations | 2018-19

(See note c on page 39)

(See notes c and f on page 39) (Due to rounding, data may not equal 100%)

30%

36%

42%

29%

21%

22%

7%

13%

0%

20%

40%

60%

80%

100%

BA MACC

Higher

Same

Lower

Not Sure

0%

10%

20%

30%

40%

50%

60%

70%

80%

2006-07 2007-08 2008-09 2009-10 2010-11 2011-12 2012-13 2013-14 2014-15 2015-16 2016-17 2017-18

2006-07 2007-08 2009-10 2011-12 2014-15 2015-16 2017-18

0.6%

0.6%

0.5%

0.4%

0.6%

0.4%

0.5%

8%

7%

7%

10

10 %

11

11 %

14

14 %

11

11 %

11%

11%

9%

7%

7%

9%

9%

6%

5%

6%

8%

7%

11%

15%

1%

1%

2%

1%

2%

13%

7%

7%

8%

17%

5%

6%

62%

69%

70%

66%

56%

59%

56%

0%

20%

40%

60%

80%

100%

American Indian/

Alaskan Native

Asian/Pacifi c Islander

Black/African American

Hispanic/Latino

Multiethnic

Other

White

51%

49%

13

2019

TRENDS REPORT

SECTION 03

SUPPLY | GRADUATES

(See note a on page 39)

2.9 Bachelor’s and master’s degrees in accounting awarded

by all universities | 1971-2018

1971-72

1972-73

1973-74

1974-75

1975-76

1976-77

1977-78

1978-79

1979-80

1980-81

1981-82

1982-83

1983-84

1984-85

1985-86

1986-87

1987-88

1988-89

1989-90

1990-91

1991-92

1992-93

1993-94

1994-95

1995-96

1998-99

1999-00

2000-01

2001-02

2002-03

2003-04

2006-07

2007-08

2009-10

2011-12

2013-14

2015-16

2017-18

Bachelor’s

Graduates

23,800

26,300

31,400

35,400

39,900

44,760

46,000

48,800

49,870

49,320

50,300

51,950

53,020

51,890

50,000

48,030

46,340

52,500

52,320

53,600

53,320

50,060

53,450

53,360

52,030

41,170

37,115

37,855

34,995

37,010

40,420

47,662

48,968

51,036

61,334

54,423

57,119

54,947

Master’s

Graduates

2,200

2,700

3,400

4,300

4,700

5,620

5,670

5,640

5,280

5,520

5,570

5,810

6,330

5,910

5,750

5,580

4,910

5,230

5,040

5,040

7,070

5,330

7,170

7,860

7,630

6,725

7,980

8,700

9,700

12,665

13,340

16,559

17,491

17,603

20,843

27,359

22,405

21,595

Bachelor’s + Master’s

Graduates

26,000

29,000

34,800

39,700

44,600

50,380

51,670

54,440

55,150

54,840

55,870

57,760

59,350

57,800

55,750

53,610

51,250

57,730

57,360

58,640

60,390

55,390

60,620

61,220

59,660

47,895

45,095

46,555

44,695

49,675

53,760

64,221

66,459

68,639

82,177

81,782

79,524

76,542

13

2019

TRENDS REPORT

SECTION 03

SUPPLY | GRADUATES

14

2019

TRENDS REPORT

SECTION 03

SUPPLY | GRADUATES

49%51%

0.3%

13%

6%

16%

2%

4%

58%

Male

Female

2.10 Demographics of new bachelor’s and master’s of accounting graduates | 2017-18

by

gender

international

students graduating from

U.S. accounting programs

12%

American Indian/

Alaskan Native

Asian/Pacifi c Islander

Black/African American

Hispanic/Latino

Multiethnic

Other

White

by

race/ethnicity

dual-degree

graduates

5%

15

2019

TRENDS REPORT

SECTION 03

SUPPLY | GRADUATES

47%53%

50%50%

0.3%

11%

6%

17%

2%

4%

59%

0.2%

19%

6%

14%

1%

5%

54%

2.11 New accounting graduates by gender | 2017-18

Male

Female

2.12 New accounting graduates by race/ethnicity | 2017-18

2.13 New accounting graduates – international students

from U.S. accounting programs | 2017-18

10%

bachelor’s master’s

bachelor’s master’s

bachelor’s

20%

master’s

American Indian/

Alaskan Native

Asian/Pacifi c Islander

Black/African American

Hispanic/Latino

Multiethnic

Other

White

16

2019

TRENDS REPORT

SECTION 03

SUPPLY | GRADUATES

0%

10%

20%

30%

40%

50%

60%

70%

80%

1%

0.3%

0.2%

0.3%

0.3%

0.2%

0.3%

8%

8%

7%

9%

11%

15%

13%

7%

7%

6%

6%

5%

7%

6%

5%

7%

5%

6%

6%

9%

16%

0%

0%

1%

1%

2%

1%

2%

11%

7%

6%

7%

14%

4%

4%

68%

70%

75%

70%

62%

63%

58%

0%

20%

40%

60%

80%

100%

2.14 Trends in new bachelor’s and master’s of accounting graduates

by gender | 2006-18

2.14 Trends in new bachelor’s and master’s of accounting graduates

by race/ethnicity | 2006-18

(See note f on page 39) (Due to rounding, data may not equal 100%)

Male

Female

American Indian/

Alaskan Native

Asian/Pacifi c Islander

Black/African American

Hispanic/Latino

Multiethnic

Other

White

2006-07 2007-08 2008-09 2009-10 2010-11 2011-12 2012-13 2013-14 2014-15 2015-16 2016-17 2017-18

2006-07 2007-08 2009-10 2011-12 2015-16 2017-18

51%

49%

2013-14

17

2019

TRENDS REPORT

SECTION 03

SUPPLY | GRADUATES

2.16 Trends in new accounting master’s graduates by program | 2006-18

Bachelor’s | Private

Bachelor’s | Public

Master’s | Private

Master’s | Public

2.17 Trends in new bachelor’s and master’s of accounting graduates

by sector | 2006-18

Master’s in Accounting

Master’s in Taxation

MBA in Accounting

2006-07 2007-08 2008-09 2009-10 2010-11 2011-12 2012-13 2013-14 2014-15 2015-16 2016-17 2017-18

2006-07 2007-08 2008-09 2009-10 2010-11 2011-12 2012-13 2013-14 2014-15 2015-16 2016-17 2017-18

0%

20%

40%

60%

80%

100%

7%

11%

83%

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

35,245

19,702

15,964

5,630

18

2019

TRENDS REPORT

SECTION 04

DEMAND | NEW HIRES

Trends

in the demand

for public

accounting

recruits

19

2019

TRENDS REPORT

SECTION 04

DEMAND | NEW HIRES

(See note d on page 39)

3.1 Trends in new accounting graduates hired into

accounting/finance functions of U.S. CPA firms | 1971-2018

Bachelor’s

Graduates

Master’s

Graduates

Bachelor’s + Master’s

Graduates

1971

1972

1973

1974

1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1999

2000

2001

2002

2003

2004

2007

2008

2010

2012

2014

2016

2018

6,800

8,900

10,000

9,500

9,200

10,010

11,660

12,770

13,500

14,100

14,200

11,970

14,490

15,640

16,510

16,110

16,720

16,740

25,240

21,340

18,840

19,870

19,320

18,500

18,560

17,820

16,960

17,265

13,335

12,630

13,270

14,985

28,025

19,110

19,870

23,793

24,931

21,167

19,498

2,000

2,400

2,600

2,600

2,800

3,350

3,310

2,890

2,900

2,460

2,210

2,210

2,180

2,180

2,250

2,030

2,050

2,220

2,600

2,500

1,760

2,650

2,670

2,970

3,375

2,650

3,250

3,686

3,035

3,295

3,555

4,720

8,087

6,378

13,451

16,557

18,321

13,722

11,405

8,800

11,300

12,600

12,100

12,000

13,360

14,970

15,660

16,400

16,560

16,410

14,180

16,670

17,820

18,760

18,140

18,770

18,960

27,840

23,840

20,600

22,520

21,990

21,470

21,935

20,470

20,210

20,951

16,370

15,925

16,825

19,705

36,112

25,488

33,321

40,350

43,252

34,889

30,903

20

2019

TRENDS REPORT

SECTION 04

DEMAND | NEW HIRES

0%

0.1%

14%

4%

10%

2%

0.2%

70%

49%51%

Male

Female

3.2 Demographics of new bachelor’s and master’s of accounting graduate hires hired into

accounting/finance functions of U.S. CPA firms | 2018

by

gender

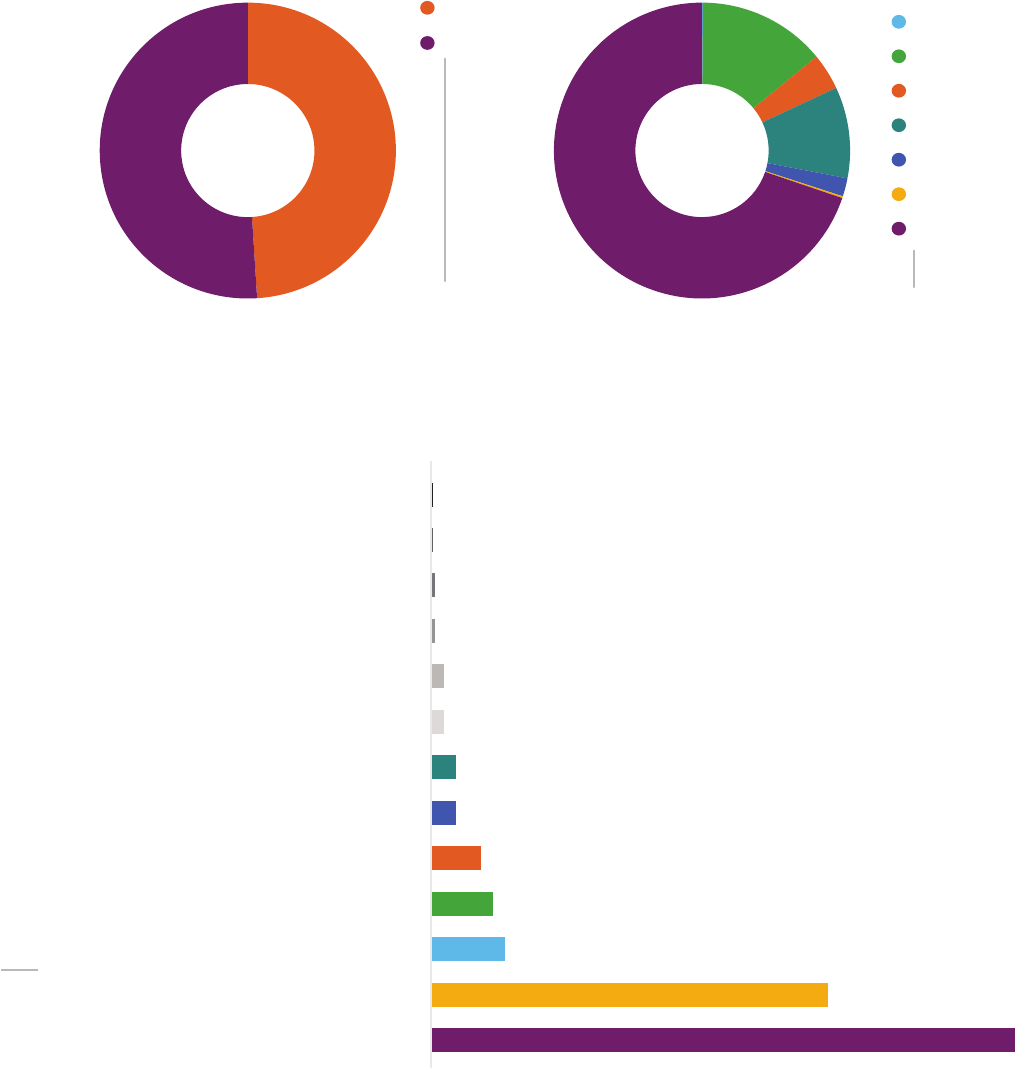

Personal Financial Planning

Management Accounting

Business Valuation

Financial Forensics

Consulting

Other Areas

Transaction Services

Information Management and Technology Assurance

Internal Audit

Financial Accounting

Assurance Services

Taxation

Auditing (not including Internal Audit)

by

area of assignment

(See note g on page 39)

50%

5%

47%

4%

6%

32%

2%

1%

0.3%

0.2%

0.01%

2%

1%

American Indian/

Alaskan Native

Asian/Pacifi c Islander

Black/African American

Hispanic/Latino

Multiethnic

Other

White

by

race/ethnicity

10% 20% 30% 40%

0.1%

21

2019

TRENDS REPORT

SECTION 04

DEMAND | NEW HIRES

3.3 Trends in new bachelor’s and master’s of accounting graduates hired

into accounting/finance functions of U.S. CPA firms by gender | 2007-18

3.4 Trends in new bachelor’s and master’s of accounting graduates hired

into accounting/finance functions of U.S. CPA firms

by race/ethnicity | 2007-18

(See note h on page 39) (Due to rounding, data may not equal 100%)

Male

Female

American Indian/

Alaskan Native

Asian/Pacifi c Islander

Black/African American

Hispanic/Latino

Multiethnic

Other

White

0%

10%

20%

30%

40%

50%

60%

70%

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

51%

49%

15%

1% 0%

0.1%

0.1% 0.2%

0%

20%

40%

60%

80%

100%

2007 2008 2010 2012 2014 2016

0.1%

72%

78%

73%

70%

70% 70% 70%

2%

2%

2%

1% 0.3% 0.2%

2%

0%

2%

2%

2%

4%

4%

7%

6%

8%

7%

10%

8%

4%

4%

4%

4%

4%

4%

13%

12%

12%

19%

16%

14%

3%

2%

2018

22

2019

TRENDS REPORT

SECTION 04

DEMAND | NEW HIRES

3.5 Trends in new bachelor’s and master’s of accounting graduates hired

into accounting/finance functions of U.S. CPA firms

as a percentage of total hires by degree | 2007-18

3.6 Trends in new master’s of accounting graduates hired

into accounting/finance functions of U.S. CPA firms

by type of degree | 2007-18

Bachelor’s

Master’s

Total Non-Accounting

Master’s in Accounting

Master’s in Taxation

MBA in Accounting

0%

10%

20%

30%

40%

50%

60%

70%

80%

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

0%

20%

40%

60%

80%

100%

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

43%

31%

25%

85%

10%

5%

Some of the increase in non-accounting hires is likely due to new categories added to the 2018 survey.

(See note i on page 39) (Due to rounding, data may not equal 100%)

23

2019

TRENDS REPORT

SECTION 04

DEMAND | NEW HIRES

3.7 Trends in new bachelor’s and master’s of accounting graduates hired

into accounting/finance functions of U.S. CPA firms

by area of assignment | 2007-18

Accounting/Auditing

Taxation

All other areas

See chart 3.2 for more specifi c 2018 assignments. (See note g on page 39)

0%

10%

20%

30%

40%

50%

60%

70%

80%

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

56%

32%

12%

24

2019

TRENDS REPORT

SECTION 04

DEMAND | FUTURE EXPECTATIONS

5%

32%

24%

39%

15%

43%

16%

27%

3.8 Expected hiring of new bachelor’s and master’s of accounting graduates

into accounting/finance functions of U.S. CPA firms who hired

new accounting graduates in 2018 | 2019

3.9 Expected hiring of new non-accounting business graduates

into accounting/finance functions of U.S. CPA firms who hired

new non-accounting graduates in 2018 | 2019

(See note j on page 39) (Due to rounding, data may not equal 100%)

Higher

Same

Lower

Not Sure

Higher

Same

Lower

Not Sure

firms who

hired accounting

graduates

firms who hired

non-accounting

graduates

There were too few respondents to generalize this data to the entire population.

(See notes j and k on page 39) (Due to rounding, data may not equal 100%)

25

2019

TRENDS REPORT

SECTION 04

DEMAND | FUTURE EXPECTATIONS

12%

77%

2%

9%

18%

72%

3%

7%

3.10 Expected number of CPAs on staff

in accounting/finance functions of U.S. CPA firms | 2019

3.11 Expected number of non-CPA professional staff

in accounting/finance functions of U.S. CPA firms | 2019

Higher

Same

Lower

Not Sure

Higher

Same

Lower

Not Sure

all firms

all firms

(Due to rounding, data may not equal 100%)

(Due to rounding, data may not equal 100%)

26

2019

TRENDS REPORT

SECTION 04

DEMAND | FUTURE EXPECTATIONS

3%

89%

3%

4%

3.12 Expected number of partners

in accounting/finance functions of U.S. CPA firms | 2019

Higher

Same

Lower

Not Sure

all firms

(Due to rounding, data may not equal 100%)

27

2019

TRENDS REPORT

SECTION 04

DEMAND | FUTURE EXPECTATIONS

U.S. fi rm

demographics

28

2019

TRENDS REPORT

SECTION 05

U.S. FIRM DEMOGRAPHICS

Male

Female

American Indian/

Alaskan Native

Asian/Pacifi c Islander

Black/African American

Hispanic/Latino

Multiethnic

Other

White

53%

47%

4.1 Demographics of all professional staff

in accounting/finance functions of U.S. CPA firms | 2018

by

gender

0.2%

17%

4%

6%

2%

0.4%

71%

by

ethnicity

(See note I on page 39)

29

2019

TRENDS REPORT

SECTION 05

U.S. FIRM DEMOGRAPHICS

0.2%

10%

2%

4%

1%

0.3%

84%

58%

42%

Male

Female

American Indian/

Alaskan Native

Asian/Pacifi c Islander

Black/African American

Hispanic/Latino

Multiethnic

Other

White

4.2 Demographics of CPAs

in accounting/finance functions of U.S. CPA firms | 2018

by

gender

by

ethnicity

(See note I on page 39)

30

2019

TRENDS REPORT

SECTION 05

U.S. FIRM DEMOGRAPHICS

0.2%

4%

1%

2%

1%

0.4%

91%

77%

23%

Male

Female

American Indian/

Alaskan Native

Asian/Pacifi c Islander

Black/African American

Hispanic/Latino

Multiethnic

Other

White

4.3 Demographics of partners

in accounting/finance functions of U.S. CPA firms | 2018

by

gender

(See note l on page 39)

by

ethnicity

31

2019

TRENDS REPORT

SECTION 06

UNIFORM CPA EXAMINATION

®

Uniform CPA

Examination

®

32

2019

TRENDS REPORT

SECTION 06

UNIFORM CPA EXAMINATION

®

The 16-hour exam comprises four 4-hour sections, which a

CPA candidate must pass within 18 months.

Auditing and Attestation (AUD)

Business Environment and Concepts (BEC)

Financial Accounting and Reporting (FAR)

Regulation (REG)

The AICPA’s Examinations team, with oversight by its Board of Examiners

(BOE), works with volunteers from the profession, academia, and boards

of accountancy to ensure the exam remains fair, legally defensible, and

aligned with the work of newly licensed CPAs. The team’s continuous

monitoring and updating of content based on changes to standards,

regulations, and laws keep the exam current and relevant to the profession.

In 2019, the Examinations team began a Practice Analysis focusing on

the impact technology has on the work of newly licensed CPAs which

could result in additions or changes to the exam. The research also is

analyzing content that may no longer be critical for newly licensed CPAs.

This research project involves meetings with public accounting fi rms

of varying sizes as well as focus group discussions with supervisors of

newly licensed CPAs. The supervisors work in public accounting fi rms and

business and industry, with some also serving on boards of accountancy.

Upon completion of the Practice Analysis, the Examinations team will

publish a research paper. The document will include an Exposure Draft

outlining recommendations for planned exam updates and content to be

added, changed, or deleted. It will also include an Invitation to Comment

portion that presents potential future exam changes based on feedback

received during the Practice Analysis. These are changes that may require

additional research and/or more extensive structural changes to the exam.

The Uniform CPA Examination

®

(exam) is the gateway to

the profession. The exam provides reasonable assurance to

boards of accountancy that individuals who pass possess the

technical knowledge and skills necessary for initial licensure.

33

2019

TRENDS REPORT

SECTION 06

UNIFORM CPA EXAMINATION

®

5.1 Trends in number of new CPA candidates by year | 2006-18

5.2 Trends in number of CPA candidates who passed their 4th section

of the CPA Exam

by year | 2006-18

(See note m on page 39)

20172006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2018

39,083

42,157

42,962

41,266

42,653

48,004

36,078

38,513

40,839

44,204

49,597

39,630

36,827

20172006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2018

25,558

14,101

18,444

23,190

26,163

29,539

23,418

26,020

26,911

26,077

27,889

25,514

23,941

34

2019

TRENDS REPORT

SECTION 07

CPA PIPELINE PROGRAMS

Appendix A

Accounting Accreditation Practitioner Engagement Program

The Accounting Accreditation Practitioner Engagement program, in partnership with the

Association to Advance Collegiate Schools of Business (AACSB) business and accounting

accrediting body, is focused on increasing CPA practitioner involvement throughout the

university accounting program’s accreditation/affi rmation process. By doing so, this

program provides value to universities, as practitioners can provide insights into the

accounting profession and share the skills and knowledge students need when entering

the profession. Since the fi rst training in November 2018, the program has trained over

20 CPA practitioners to be a part of AACSB peer review teams and committees.

Academic Champions

The AICPA launched the Academic Champions program in 2016 to help encourage

a pro-CPA culture on college campuses. The program provides support to academic

faculty at select universities and community colleges to help them increase awareness

of the CPA profession by using AICPA-provided resources and holding campus events

each semester. This program currently has 42 Academic Champions who are fostering

a stronger connection between their students and the accounting profession.

AICPA CPA Evolution Project

Launched in 2018 by the AICPA and the National Association of State Boards of Accountancy

(NASBA), the CPA Evolution initiative is an effort to explore modifying the requirements for

initial CPA licensure in response to the rapid pace of change in the environment in which

CPAs operate. Technological innovations are changing both the services CPAs provide and

how they provide them. The CPA profession must embrace these changes to maintain its

strength and support evolving business needs while continuing to serve the public interest.

In 2019, the AICPA and NASBA put forth guiding principles and are seeking

input from the profession, academia, and the regulatory community. During the

AICPA Fall Council and the NASBA Annual Meeting in October 2019, both groups

will present the collected feedback and will recommend next steps.

Accounting Doctoral Scholars Program (ADS)

In 2008, the AICPA launched the ADS program to address the shortage of qualifi ed CPA-

accredited faculty. The ADS program recruits CPAs to enroll in Ph.D. programs and ultimately

join the faculty at universities and colleges throughout the United States. To date, the AICPA

has recruited and funded 132 candidates with relevant practical experience into the program.

Combined, these candidates have produced 138 publications focused on areas such as fi rm

quality control initiatives, tax fraud, and fi nancial reporting and have taught 828 courses ranging

from introductory accounting to auditing for Ph.D.-level students, reaching over 31,000 students.

AICPA PROGRAMS DEDICATED TO

GROWING THE CPA PIPELINE

35

2019

TRENDS REPORT

SECTION 07

CPA PIPELINE PROGRAMS

Academic Executive Committee (AEC)

The AICPA has engaged the accounting academic community for over 100 years.

A leading example is the AICPA’s AEC. The AEC includes accounting faculty, high

school accounting teachers, accounting practitioners, and state CPA societies from

across the United States and serves to assist the AICPA in achieving its academic

initiatives, programs, and partnerships to grow and involve a community of diverse,

well-prepared, highly qualifi ed CPAs. Recent work of the committee includes:

The approved and implemented recommendation to include practitioners

on peer review teams for AACSB accreditation visits;

The development of the Accounting Advisory Council Toolkit, which

provides departments of accounting guidance on enhancing or starting an

advisory board that includes members of the business community;

Updating the Core Competency Framework for pre-licensure education; and

Pioneering advisory support that led to the launch of the Extra Credit newsletter,

which has helped to advance AICPA engagement with accounting faculty.

Accounting Program for Building the Profession (APBP)

The APBP program, which was created in 2006 by Dr. Dan Deines and purchased in 2017

by the AICPA, exists to help promote the accounting profession as a viable career option for

high school students. To achieve this, the college-level program equips high school teachers

with the tools needed to teach more advanced, engaging content in the classroom. Since its

inception, this program has trained over 1,500 educators across 48 states and has exposed

thousands of students to the many opportunities the accounting profession has to offer.

AICPA Fellowship for Minority Doctoral Students

The AICPA started the Fellowship for Minority Doctoral Students in 1969 to ensure

that CPAs of diverse backgrounds are visible in college and university classrooms.

The program has increased the number of minority CPAs who serve as role

models and mentors to young people in the academic environment and university

classrooms. For the 2018–19 academic year, the AICPA awarded scholarships

to 25 full-time accounting doctoral-level students, totaling $300,000.

AICPA Legacy Scholars Program

For over 50 years, the AICPA has helped grow the number of qualifi ed high school

and college students entering the accounting profession through scholarship funding.

Scholarships are awarded to students who demonstrate the potential to become

leaders in the CPA profession, who are taking nontraditional paths to becoming CPAs,

or who help promote the growth of diverse, talented professionals in the accounting

fi eld. During the 2018–19 academic year, the AICPA awarded 148 scholarships, totaling

over $650,000 to AICPA student members who plan to receive a CPA designation.

SECTION 07

CPA PIPELINE PROGRAMS

2019

TRENDS REPORT

36

AICPA Student Affi liate Membership

Launched in 2010, this membership is designed to help students interested in accounting

from the earliest stages of their college careers through graduation. By joining the AICPA for

free as a Student Affi liate, students get access to tools, resources, and exclusive discounts

and scholarship opportunities. According to a 2019 AICPA survey, 75% of accounting students

believe that the AICPA Student Affi liate membership is helpful for their professional goals.

Bank On It

This online accounting game is designed to challenge high school and college

students on accounting fundamentals while providing real-world scenarios and

reinforcing what they learn in the classroom. Since its launch in 2015, Bank On It has

completed over 100,000 games and hosted over 350 tournaments on its site.

Diversity & Inclusion Initiatives

The accounting profession serves communities and clients across the globe with varying cultures

and perspectives. As the profession continues to become more globalized, a greater need exists for

diversity and inclusion. The AICPA has created programs and initiatives to help increase the quantity

and quality of under-represented minorities in the profession. These include but are not limited to:

AICPA and NAF Recognition Program Partnership

The National Academy Foundation (NAF), Academy of Finance (AOF), and the AICPA

have partnered to expand high school student exposure to the accounting profession

by hosting an annual Bank On It tournament and other programs each year.

Accounting Scholars Leadership Workshop (ASLW)

ASLW is an annual, invitation-only student leadership conference hosted by the

AICPA. The workshop helps students develop leadership skills and expand their

knowledge of various pathways to success in the accounting profession.

Annual Accounting Profession Diversity Symposium

The Annual Accounting Profession Diversity Symposium provides a platform for

fi rms, academics, and state societies to explore best practices and identify ways to

overcome obstacles in fi lling the accounting pipeline with diverse professionals.

Real CPA Pipeline Campaign

To encourage students with diverse backgrounds to pursue an accounting career,

the AICPA has created a national awareness campaign called Real CPAs. This

campaign features real CPAs with diverse backgrounds. Each year features

new real CPAs that debunk the stereotype of accounting professionals.

HBCU Toolkit

To increase the recruiting and retention of African Americans in the accounting profession,

AICPA developed a toolkit for historically black colleges and universities. These toolkits are

provided to campus career service centers to ensure that their students are well equipped pro-

fessionally, being seen by recruiters, and receiving internship and job placement opportunities.

37

2019

TRENDS REPORT

SECTION 07

CPA PIPELINE PROGRAMS

Start Here, Go Places (SHGP)

Created in 2002, SHGP provides accounting profession information to students

and high school teachers that inspires students to join the accounting profession.

The website provides over 90 unique classroom activities and over 35 professional

development articles that teachers can download for free and use in their classroom.

Additionally, SHGP also provides teachers with printed classroom resources.

State Societies Dual Recruitment

Starting in 2016, the AICPA has partnered with accounting state societies to jointly

recruit student members. The partnership — which includes unifi ed messaging and

co-branded materials — helps students enhance their connection to the profession and

demonstrates the value of lifelong professional membership. Additionally, this program

provides an avenue for the AICPA and state societies to share ideas, create effi ciencies,

and overcome pipeline challenges together. Currently the AICPA is partnered with 14

state societies, and the effort has jointly recruited thousands of students since its launch.

This Way to CPA (TWTCPA)

TWTCPA was designed for college students interested in pursuing a CPA. Launched

in 2010, this initiative helps provide the clarity and direction needed to obtain a

CPA accreditation. Visitors learn about the education, work experience, and exam

and licensure process. The TWTCPA website features countless resources and

34 CPA profi les and 19 Exam profi les spanning 14 industries, including public

accounting, forensics, corporate, and more, to give students and graduates a

better understanding of the profession and what it takes to become a CPA.

Uniform CPA Examination

®

The AICPA’s Examinations team, with oversight by its Board of Examiners, works

with volunteers from the profession, academia, and boards of accountancy

to ensure the CPA Exam remains fair, legally defensible, and aligned with the

work of newly licensed CPAs. The team’s continuous monitoring and updating

of content based on changes to standards, regulations, and laws keep the

Exam current and relevant to the profession. This involves updating the CPA

Exam Blueprints one or two times each year to refl ect the changes.

Following a comprehensive Practice Analysis with input from the profession, in April

2017 the Uniform Examination team began assessing critical thinking and other

higher-order skills to a greater extent. The following year, the AICPA introduced new,

intuitive CPA Exam software designed to enhance the user testing experience, which

included access to Microsoft Excel

®

. In 2019, the AICPA began a new Practice Analysis

specifi cally targeting the impact technology has on the work of newly licensed CPAs.

38

2019

TRENDS REPORT

SECTION 07

METHODS

Appendix B

Supply

methodology

Demand

methodology

A census of colleges

and universities granting

accounting degrees was

invited to participate (n=907)

The survey opened on

October 18, 2018

The survey closed on

January 25, 2019

Response rate was 12%

(n=112)

Survey results presented

in this report are weighted

by faculty size and

geographic region

A census of public

accounting

fi rms was invited to

participate (n=30,529)

The survey opened on

October 18, 2018

The survey closed on

January 25, 2019

Response rate was

2.3% (n=706)

Survey results

presented in this report

are weighted by fi rm

size (number of CPAs)

METHODS

39

2019

TRENDS REPORT

SECTION 07

ENDNOTES

a. The statistical vendor changed from CXACT to ARC Research between the 2015 and 2017 reports. ARC did their due diligence in researching

methods from previous years and creating a model that is as comparable as possible to previous years’ data. The 2016 and 2018 models are based

on a linear regression on weighted data, using faculty size as a predictor. For 2016 and 2018, weights were applied across the whole survey sample.

For 2014, the previous vendor noted that separate weights were calculated for Bachelor’s, Master’s, and Ph.D. respondents.

b. For 2016 and 2018, the weighted proportions of MA program types were applied to the projected MA total to derive breakdowns by program type.

For 2014, it appears that the unweighted proportions of MA program types were used. For 2012 and years prior, it is unclear how proportions of MA

program types were derived.

c. Enrollment data collected for the 2015 Tr ends report represents the 2014-15 academic year instead of the 2013-14 academic year due to the wording

of the supply survey questionnaire for this period.

d. The statistical vendor changed from CXACT to ARC Research between the 2015 and 2017 reports. ARC did their due diligence in researching

methods from previous years and creating a model that is as comparable as possible to previous years’ data. The 2016 and 2018 models are based

on a linear regression on weighted data, using number of CPAs to predict total new graduate hires with accounting degrees. For 2016 and 2018, the

weighted proportions of BA vs. MA were applied to the projected total to derive breakdowns by degree level. For 2014, it appears that the unweighted

proportions of BA/MA were used. For 2012 and years prior, it is unclear how proportions of BA/MA hires were derived.

e. To avoid double counting of dual degree students, respondents were instructed to classify students as follows:

01. Enrollments - Respondents were instructed to classify students in years 1 through 4 as Bachelor’s and students in year 5 as Master’s.

02. Graduates - Respondents were instructed to exclude dual degree graduates from the Bachelor’s totals, and include them in the Master’s totals.

f. Data collection for the multiethnic race/ethnicity category began in 2010.

g. In 2014 and previous years, areas of assignment were limited to Accounting/Auditing, Taxation, MIS/Computers, and Other. In 2016, we broadened

the areas for the snapshot data (3.2), but kept the condensed categories for the trends data (3.7) as follows:

Additionally, this year we added an “Internal Audit” category for further segmentation.

AREAS OF ASSIGNMENT CONDENSED CATEGORY

Financial Accounting Acc./Aud.

Auditing, not Including Internal Audit Acc./Aud.

Internal Audit Acc./Aud.

Assurance Services Other

Taxation Taxation

Information Management and Technology Assurance Other

Consulting Other

Financial Forensics Other

Business Valuation Other

Personal Financial Planning Other

Management Accounting Other

Transaction Services Other

Other Areas Other

ENDNOTES

h. For this chart, 2014 race/ethnicity fi gures have been recalculated to exclude “Unknown” for comparability with other years.

i. In previous years, data on the hiring of non-accounting degree holders only included “non-accounting business majors” and “non-business

majors.” In 2018, we changed the categories to “non-accounting business majors – e.g., fi nance, marketing, etc.,” “STEM majors, not

including accounting or business,” and “all other majors.” Because of the addition of more specifi c categories, the total of non-accounting

new hires is likely artifi cially infl ated in 2018 and isn’t directly comparable to previous years. These new categories are indicative of trends

in the public accounting industry and are crucial in tracking industry trends accurately in the future.

j. In iterations of the report prior to 2016, the data in this chart included all fi rms that responded to the survey, rather than only fi rms that hired

in the survey year. Thus, some percentage of those in previous years that noted that they would hire “the same” next year as in the survey

year did not hire in that year and did not plan to hire in the future year (these tend to be smaller fi rms). This representation of the data was

improved upon and the charts in 2017 and 2019 only include prospective hiring of fi rms that hire.

k. Due to small sample size, this data cannot be generalized to the entire fi rm universe. This data, instead, is simply a report of the fi rms that

actually responded.

l. Firm demographics are not broken down by fi rm size due to the insuffi cient samples in the 50-200 and 200+ CPA categories. The number

of respondents in those categories is too small (i.e., there are fewer than 40 total respondents in each of those categories) to draw valid

conclusions from despite relatively higher response rates in those categories.

m. CPA Exam data often show increases in candidates prior to changes to the Exam followed by signifi cant decreases in the fi rst few years

after the CPA Examination changes. With the changes in 2017, decreases were expected in 2018.

040

2019

TRENDS REPORT

SECTION 01

INTRODUCTION

041

2019

TRENDS REPORT

SECTION 01

INTRODUCTION

042

2019

TRENDS REPORT

SECTION 01

INTRODUCTION