Financial M athem atics

fo r Act u a r ie s

Chapter 2

Ann uities

Learning Objectives

1. Annuit y-immediate and annuity-due

2. Present and future values of annuities

3. Perpetuities and deferred annuities

4. Other accumulation m ethods

5. Payment periods and com pounding periods

6. Varying annuities

2

2.1 A nn uit y-Im mediate

• Consider an annuit y with payments of 1 unit eac h, made at the end

of ev ery year for n years.

• T his kind of annuit y is called an annuit y-imm ediate (also called

an ordinary annuit y or an annuit y in arrears).

• The present value of an ann uit y is the sum of the present values

of eac h payment.

Example 2.1: Calculate the presen t value of an ann uity-imm ediate of

amount $100 paid ann ually for 5 years at the rate of in terest of 9%.

Solution: Table 2.1 summ arizes the presen t values of the payments as

well as their total.

3

Table 2.1: Presen t value of ann uity

Year Payment ($) Present value ($)

1100100 (1.09)

−1

=91.74

2100100 (1.09)

−2

=84.17

3100100 (1.09)

−3

=77.22

4100100 (1.09)

−4

=70.84

5100100 (1.09)

−5

=64.99

Total 388.97

2

• Weareinterestedinthevalueoftheannuityattime0,calledthe

present value, and the accumulated value of the ann uity at time n,

called the future value.

4

• Suppose the rate of in terest per period is i,andweassumethe

compound-in terest method applies.

• Let a

n

e

i

denote the present value of the ann uit y, whic h is sometim es

denoted as a

n

e

when the rate of in terest is understood.

• As the presen t value of the jth payment is v

j

,wherev =1/(1 + i) is

the discoun t factor, the present value of the annuity is (see Appendix

A.5 for the sum of a geometric progression)

a

n

e

= v + v

2

+ v

3

+ ···+ v

n

= v ×

∙

1 − v

n

1 − v

¸

=

1 − v

n

i

=

1 − (1 + i)

−n

i

. (2.1 )

5

• The accumulated value of the ann uit y at time n is denoted b y s

n

e

i

or s

n

e

.

• This is the future value of a

n

e

at time n.Thus,wehave

s

n

e

= a

n

e

× (1 + i)

n

=

(1 + i)

n

− 1

i

. (2.2 )

• If the ann uit y is of lev el payments of P, the present and future values

of the annuity are Pa

n

e

and Ps

n

e

, respectively.

Example 2.2: Calculate the presen t value of an ann uity-imm ediate of

am ount $100 paid annually for 5 y ears at the rate of in terest of 9% using

formula (2.1). Also calculate its future value at time 5.

6

Solution: From (2.1), the present value of the annuity is

100 a

5

e

=100×

"

1 − (1.09)

−5

0.09

#

=$388.97,

whic h agrees with the solution of Example 2.1. The future value of the

annuity is

(1.09)

5

× (100 a

5

e

)=(1.09)

5

× 388.97 = $598.47.

Alternativ ely, the future value can be calculated as

100 s

5

e

=100×

"

(1.09)

5

− 1

0.09

#

=$598.47.

2

Example 2.3: Calculate the presen t value of an ann uity-imm ediate of

amount $100 pa yable quarterly for 10 years at the annual rate of interest

7

of 8% convertible quarterly. A lso calculate its future value at the end of

10 years.

Solution: Note that the rate of in terest per pa ym ent period (quarter)

is (8/4)% = 2%,andthereare4 × 10 = 40 pa ym ents. Thus, from (2.1)

thepresentvalueoftheannuity-immediateis

100 a

40

e

0.02

=100×

"

1 − (1.02)

−40

0.02

#

=$2,735.55,

an d th e fut ure va lue of th e annuity-imme dia t e is

2735.55 × (1.02)

40

=$6,040.20.

2

• A common problem in financial m anagement is to determine the in-

stallm ents required to pay bac k a loan. We may use (2.1) to calculate

the amo unt of level installm ents required.

8

Example 2.4: A man borro w s a loan of $20,000 to purchase a car at

annual rate of interest of 6%. He will pay bac k the loan through m onthly

installments o ver 5 years, w ith the first insta llm ent to be m ad e one mo nth

after the release of the loan. What is the monthly installment he needs to

pa y?

Solution: The rate of interest per pa ym ent period is (6/12)% = 0.5%.

Let P be the monthly installm ent. As there are 5 × 12 = 60 pa ym ents,

from (2.1 ) we have

20,000 = Pa

60

e

0.005

= P ×

"

1 − (1.005)

−60

0.005

#

= P × 51.7256,

9

so that

P =

20,000

51.7256

=$386.66.

2

• The exam ple belo w illustrates the calculation of the required install-

ment for a targeted future value.

Example 2.5: A man wan ts to sav e $100,000 to pay for his son’s

education in 10 years’ time. An education fund requires the in vestors to

deposit equal installments ann ually at the end of eac h year. If in terest of

7.5% is paid, how much does the man need to save each y ear in order to

meet his target?

Solution: We first calculate s

10

e

, whic h is equal to

(1.075)

10

− 1

0.075

=14.1471.

10

Then the required amount of installm ent is

P =

100,000

s

10

e

=

100,000

14.1471

=$7,068.59.

2

11

2.2 Annuit y-Due

• An ann uit y-due is an annu ity for w hich the pay ments are ma de at

the beginning of the pa ym ent periods

• The first pa ym ent is made at time 0, and the last payment is made

at time n − 1.

• We denote the present value of the ann uity-due at time 0 b y ¨a

n

e

i

(or

¨a

n

e

), and the futu re value of the annuity at time n by ¨s

n

e

i

(or ¨s

n

e

).

• The formula for ¨a

n

e

can be derived as follo w s

¨a

n

e

=1+v + ···+ v

n−1

=

1 − v

n

1 − v

=

1 − v

n

d

. (2.3 )

12

• Also, w e ha v e

¨s

n

e

=¨a

n

e

× (1 + i)

n

=

(1 + i)

n

− 1

d

. (2.4 )

• As eac h pa ym ent in an annuit y-due is paid one period ahead of the

correspondin g payment of an annuity-imm ed iate, the present value

of each pa ym ent in an annuit y-due is (1+i) times of the presen t value

of the corresponding pa ym ent in an annuit y-immediate. Hence,

¨a

n

e

=(1+i) a

n

e

(2.5 )

and, similarly,

¨s

n

e

=(1+i) s

n

e

. (2.6 )

13

• As an annuit y-due of n paym ents consists of a paym ent at time 0

and an ann uity-imm ediate of n − 1 payments, the first payment of

whichistobemadeattime1,wehave

¨a

n

e

=1+a

n−1

e

. (2.7 )

• Similarly, if we consid er an annuity-im mediate with n +1 pa ym ents

at time 1, 2, ···, n +1as an annuity-due of n paym ents starting at

time 1 plus a final pa ymen t at time n +1, w e can conclude

s

n+1

e

=¨s

n

e

+1. (2.8 )

Example 2.6: A company wants to provide a retirement plan for an

employ ee who is aged 55 no w . The plan will pro vide her with an annuity-

imm ediate of $7,000 every y ear for 15 y ears upon her retirement at the

14

age of 65. The company is funding this plan with an annuity-due of 10

years.Iftherateofinterestis5%,whatistheamountofinstallmentthe

comp any should pay?

Solution: We first calculate the present value of the retirement annuit y.

Th is is equa l to

7,000 a

15

e

= 7,000 ×

"

1 − (1.05)

−15

0.05

#

=$72,657.61.

This amount should be equal to the future value of the com pany’s install-

men ts P ,whichisP ¨s

10

e

.Nowfrom(2.4),wehave

¨s

10

e

=

(1.05)

10

− 1

1 − (1.05)

−1

=13.2068,

so that

P =

72,657.61

13.2068

=$5,501.53.

15

2.3 Perpetuity, Deferred Annuity and Annuit y

Values at Other Times

• A perpetuity is an an nuity with no ter min at io n da te, i.e., n →∞.

• An example that resembles a perpetuity is the dividends of a pre-

ferred stock.

• To calculate the present value of a perpetuit y, we note that, as v<1,

v

n

→ 0 as n →∞. Thus, from (2.1 ), we have

a

∞

e

=

1

i

. (2.9 )

• For the case when the first pa ym ent is made immediately, w e ha ve,

from (2.3),

¨a

∞

e

=

1

d

. (2.10)

16

• A deferred ann uity is on e for w h ich the first paym ent starts some

time in the future.

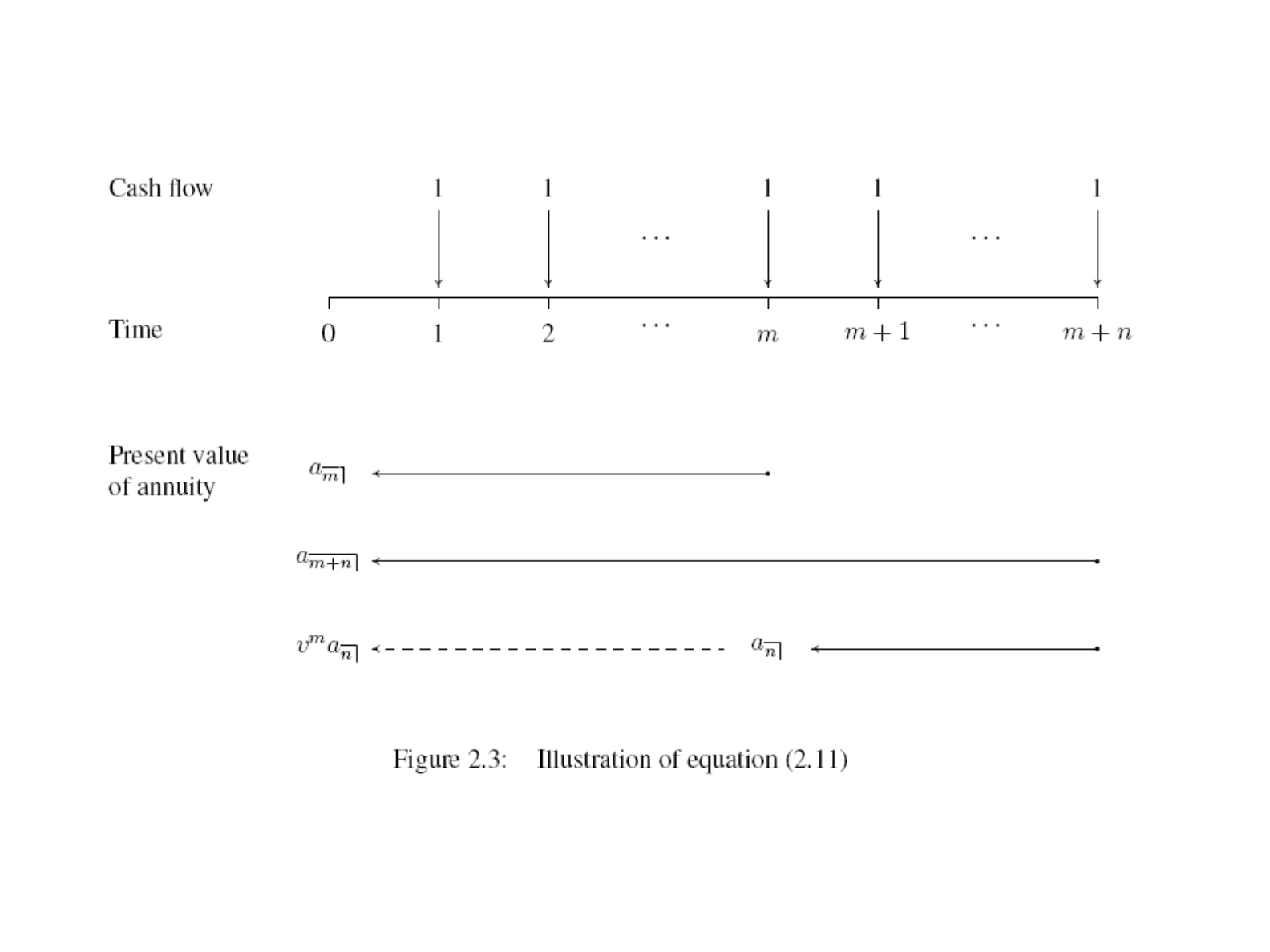

• Co n sid e r an annuity w ith n unit pa ym ents for whic h the first pay-

m e nt is du e at time m +1.

• This can be regarded as an n-period ann uity-imm ediate to start at

time m,anditspresentvalueisdenotedby

m|

a

n

e

i

(or

m|

a

n

e

for short).

Th us, w e ha ve

m|

a

n

e

= v

m

a

n

e

= v

m

×

∙

1 − v

n

i

¸

=

v

m

− v

m+n

i

=

(1 − v

m+n

) − (1 − v

m

)

i

17

= a

m+n

e

− a

m

e

. (2.11)

• To understand the abo ve equation, see Figure 2.3.

• From (2.11), we have

a

m+n

e

= a

m

e

+ v

m

a

n

e

= a

n

e

+ v

n

a

m

e

. (2.12)

• Multiplying the abo ve equations throughout by 1+i,wehave

¨a

m+n

e

=¨a

m

e

+ v

m

¨a

n

e

=¨a

n

e

+ v

n

¨a

m

e

. (2.13)

• We also denote v

m

¨a

n

e

as

m|

¨a

n

e

,whichisthepresentvalueofan-

payment annuit y of unit amounts due at time m, m+1, ···,m+n−1.

18

• If we multiply the equations in (2.12) throughout b y (1 + i)

m+n

,we

obtain

s

m+n

e

=(1+i)

n

s

m

e

+ s

n

e

=(1+i)

m

s

n

e

+ s

m

e

. (2.14)

• See Figure 2.4 for illustration.

• It is also straightfo rwa rd to see that

¨s

m+n

e

=(1+i)

n

¨s

m

e

+¨s

n

e

=(1+i)

m

¨s

n

e

+¨s

m

e

. (2.15)

• We now return to (2.2) and write it as

s

m+n

e

=(1+i)

m+n

a

m+n

e

,

19

so that

v

m

s

m+n

e

=(1+i)

n

a

m+n

e

, (2.16)

for arbitrary positiv e integers m and n.

• How do y ou interpret this equation?

20

2.4 A nnuities Under O ther Accumulation M ethods

• We ha ve so far discussed the calculations of the present and future

va lu e s of annuities assu min g compou n d inter est .

• We now extend our discussion to other interest-accumulation meth-

ods.

• We consider a general accumulation function a(·) and assume that

the function applies to any cash-flow transactions in the future.

• As stated in Section 1.7, an y payment at time t>0 starts to accu-

mulate interest according to a(·) as a pa yment made at time 0.

• Given the accumulation function a(·), the presen t value of a unit

payment due at time t is 1/a(t), so that the present value of a n-

21

period annuity-imm ediate of unit payments is

a

n

e

=

n

X

t=1

1

a(t)

. (2.17)

• The future value at time n of a unit paym ent at time t<nis

a(n − t), so that the future value of a n-period annuity-im m ed iate

of unit pa ym en ts is

s

n

e

=

n

X

t=1

a(n − t). (2.18)

• If (1.35) is satisfied so that a(n −t)=a(n)/a(t) for n>t>0,then

s

n

e

=

n

X

t=1

a(n)

a(t)

= a(n)

n

X

t=1

1

a(t)

= a(n) a

n

e

. (2.19)

• This result is satisfied for the compound-in terest method, but not

the simple-interest method or other accumulation sc hem es for which

equation (1.35) does not hold.

22

Example 2.7: Suppose δ(t)=0.02t for 0 ≤ t ≤ 5, find a

5

e

and s

5

e

.

Solution: We first calculate a(t), which, from (1.26), is

a(t)=exp

µ

Z

t

0

0.02sds

¶

=exp(0.01t

2

).

Hence, from (2.17),

a

5

e

=

1

e

0.01

+

1

e

0.04

+

1

e

0.09

+

1

e

0.16

+

1

e

0.25

=4.4957,

and, from (2.18),

s

5

e

=1+e

0.01

+ e

0.04

+ e

0.09

+ e

0.16

=5.3185.

Note that a(5) = e

0.25

=1.2840,sothat

a(5) a

5

e

=1.2840 × 4.4957 = 5.7724 6= s

5

e

.

23

2

• Note that in the abov e example, a(n − t)=exp[0.01(n − t)

2

] and

a(n)

a(t)

=exp[0.01(n

2

− t

2

)],

so that a(n − t) 6= a(n)/a(t) and (2.19) does not hold.

Example 2.8: Calculate a

3

e

and s

3

e

if the nominal rate of interest is

5% per ann um , assuming (a) compound interest, and (b) simple in terest.

Solution: (a) Assuming compound interest, we hav e

a

3

e

=

1 − (1.05)

−3

0.05

=2.723,

and

s

3

e

=(1.05)

3

× 2.72 = 3.153.

24

(b) For simple interest, the present value is

a

3

e

=

3

X

t=1

1

a(t)

=

3

X

t=1

1

1+rt

=

1

1.05

+

1

1.1

+

1

1.15

=2.731,

andthefuturevalueattime3is

s

3

e

=

3

X

t=1

a(3 − t)=

3

X

t=1

(1 + r(3 − t)) = 1.10 + 1.05 + 1.0=3.150.

At the same nominal rate of interest, the compound-interest m ethod gen-

erates higher in terest than the sim ple-interest m ethod. Therefore, the

future value under the compound-in terest method is higher, w hile its

present value is lower. Also, note that for the sim ple-interest method,

a(3) a

3

e

=1.15 × 2.731 = 3.141, w hich is different from s

3

e

=3.150. 2

25

2.5 Pa ym en t Periods, Compounding Periods and

Continuous Annuities

• We no w consider the case where the pa ym ent period differs from the

interest-conversion period.

Example 2.9: Find the present value of an ann uit y-due of $200 per

quarter for 2 years, if interest is compounded m onthly at the nominal rate

of 8%.

Solution: Thisisthesituationwherethepaymentsaremadeless

freq u e ntly th a n inter est is converte d . We first calculate the effective rate

of interest per quarter, whic h is

∙

1+

0.08

12

¸

3

− 1=2.01%.

26

As there are n =8payments, the required presen t value is

200 ¨a

8

e

0.0201

=200×

"

1 − (1.0201)

−8

1 − (1.0201)

−1

#

=$1,493.90.

2

Example 2.10: Find the present value of an ann uity-imm ediate of

$100 per quarter for 4 years, if interest is compounded semiannually at

the nominal rate of 6%.

Solution: This is the situation where paymen ts are made more fre-

quently than in terest is con verted. We first calculate the effective rate of

in terest per quarter, whic h is

∙

1+

0.06

2

¸

1

2

− 1=1.49%.

27

Thus, the required present value is

100 a

16

e

0.0149

=100×

"

1 − (1.0149)

−16

0.0149

#

=$1,414.27.

2

• It is possible to derive algebraic formulas to compute the presen t

and future values of annuities for whic h the period of installment is

different from the period of compounding.

• We first consider the case where payments are made less frequently

than interest con version, which occurs at time 1, 2, ···,etc.

• Let i denote the effective rate of interest per in terest-conversion pe-

riod. Suppose a m-payment ann uity-imm ediate consists of unit pay-

men ts at time k, 2k, ···, mk.Wedenoten = mk,whichisthe

number of interest-conversion periods for the annuity.

28

• Figure 2.6 illustrates the cash flows for the case of k =2.

• Thepresentvalueoftheaboveannuity-immediateis(weletw = v

k

)

v

k

+ v

2k

+ ···+ v

mk

= w + w

2

+ ···+ w

m

= w ×

∙

1 − w

m

1 − w

¸

= v

k

×

∙

1 − v

n

1 − v

k

¸

=

1 − v

n

(1 + i)

k

− 1

=

a

n

e

s

k

e

, (2.20)

and the future value of the annuity is

(1 + i)

n

a

n

e

s

k

e

=

s

n

e

s

k

e

. (2.21)

29

• We no w consider the case where the payments are made more fre-

quently than interest con version.

• Let there be mn pa ym ents for an ann uity-imm ediate occurring at

time 1/m, 2/m, ···, 1, 1+1/m, ···, 2, ···, n,andleti be the effective

rate of interest per in terest-conversion period. Thus, there are mn

payments ov er n interest-con version periods.

• Suppose eac h payment is of the amount 1/m, so that there is a

nominal am ount of unit pa ym ent in eac h interest-conv ersion period.

• Figure 2.7 illustrates the cash flows for the case of m =4.

• We denote the present value of this annuity at time 0 by a

(m)

n

e

i

,which

can be computed as follows (we let w = v

1

m

)

a

(m)

n

e

i

=

1

m

³

v

1

m

+ v

2

m

+ ···+ v + v

1+

1

m

+ ···+ v

n

´

30

=

1

m

(w + w

2

+ ···+ w

mn

)

=

1

m

∙

w ×

1 − w

mn

1 − w

¸

=

1

m

"

v

1

m

×

1 − v

n

1 − v

1

m

#

=

1

m

"

1 − v

n

(1 + i)

1

m

− 1

#

=

1 − v

n

r

(m)

, (2.22)

where

r

(m)

= m

h

(1 + i)

1

m

− 1

i

(2.23)

is the equivalent nom inal rate of in terest compounded m tim es per

interest-conversion period (see (1.19)).

31

• The future value of the annuit y-im mediate is

s

(m)

n

e

i

=(1+i)

n

a

(m)

n

e

i

=

(1 + i)

n

− 1

r

(m)

=

i

r

(m)

s

n

e

. (2.24)

• The abov e equation parallels (2.22), wh ich can also be written as

a

(m)

n

e

i

=

i

r

(m)

a

n

e

.

• If the mn-payment annuity is due at time 0, 1/m, 2/m, ···,n−1/m,

we den o t e its present valu e at tim e 0 by ¨a

(m)

n

e

,whichisgivenby

¨a

(m)

n

e

=(1+i)

1

m

a

(m)

n

e

=(1+i)

1

m

×

∙

1 − v

n

r

(m)

¸

. (2.25)

32

• Th us, from (1.22) w e conclude

¨a

(m)

n

e

=

1 − v

n

d

(m)

=

d

d

(m)

¨a

n

e

. (2.26)

• The future value of this ann uit y at time n is

¨s

(m)

n

e

=(1+i)

n

¨a

(m)

n

e

=

d

d

(m)

¨s

n

e

. (2.27)

• For deferred annuities, the follo w ing results apply

q|

a

(m)

n

e

= v

q

a

(m)

n

e

, (2.28)

and

q|

¨a

(m)

n

e

= v

q

¨a

(m)

n

e

. (2.29)

Exam ple 2.11: Solv e the problem in Example 2.9 using (2.20).

33

Solution: We first note that i =0.08/12 = 0.0067.Nowk =3and

n =24so that from (2.20), the present value of the annuity-im mediate is

200 ×

a

24

e

0.0067

s

3

e

0.0067

=200×

"

1 − (1.0067)

−24

(1.0067)

3

− 1

#

=$1,464.27.

Finally, the presen t value of the annuit y-due is

(1.0067)

3

× 1,464.27 =$1,493.90.

2

Example 2.12: Solv e the problem in Example 2.10 using (2.22) and

(2.23).

Solution: Note that m =2and n =8.Withi =0.03,wehave,from

34

(2.23)

r

(2)

=2× [

√

1.03 − 1] = 0.0298.

Therefore, from (2.22), we have

a

(2)

8

e

0.03

=

1 − (1.03)

−8

0.0298

=7.0720.

As the total pa ym ent in eac h in terest-conversion period is $200, the re-

quired present value is

200 × 7.0720 = $1,414.27.

2

• Now we consider (2.22) again. Suppose the ann uities are paid con-

tinuously attherateof1unitperinterest-conversionperiodover

n periods. Thus, m →∞and we denote the presen t value of this

continuous annuity by ¯a

n

e

.

35

• As lim

m→∞

r

(m)

= δ,wehave,from(2.22),

¯a

n

e

=

1 − v

n

δ

=

1 − v

n

ln(1 + i)

=

i

δ

a

n

e

. (2.30)

• Thepresentvalueofan-period continuous annuit y of unit payment

perperiodwithadeferredperiodofq is given by

q|

¯a

n

e

= v

q

¯a

n

e

=¯a

q+n

e

− ¯a

q

e

. (2.31)

• To compute the future value of a continuous annuit y of unit pa ym ent

per period over n per iods , we us e the following formula

¯s

n

e

=(1+i)

n

¯a

n

e

=

(1 + i)

n

− 1

ln(1 + i)

=

i

δ

s

n

e

. (2.32)

• Wenowgeneralizetheaboveresultstothecaseofageneralaccu-

mulation function a(·). The present value of a continuous ann uit y

36

of unit pa ym ent per period o ver n periods is

¯a

n

e

=

Z

n

0

v(t) dt =

Z

n

0

exp

µ

−

Z

t

0

δ(s) ds

¶

dt. (2.33)

• To compute the future value of the ann uit y at tim e n,weassume

that, as in Section 1.7, a unit payment at tim e t accumulates to

a(n − t) at time n,forn>t≥ 0.

• Th us, the future value of the ann uit y at time n is

¯s

n

e

=

Z

n

0

a(n − t) dt =

Z

n

0

exp

µ

Z

n−t

0

δ(s) ds

¶

dt. (2.34)

37

2.6 Varying A nnuities

• We consider ann uities the pa ym ents of which vary according to an

ar it h metic pr ogr e ss io n .

• Th us, w e consider an ann uit y-imm ediate and assume the initial pay-

men t is P , with subsequen t payments P + D, P +2D, ···,etc.,so

that the jth pa ym ent is P +(j − 1)D.

• We allow D to be negative so that the ann uity can be either stepping

up or stepping down.

• Ho w ev er, for a n-payment annuity, P +(n − 1)D must be positive

so that negative cash flow is ruled out.

• We can see that the ann uit y can be regarded as the sum of the

follo w ing annuities: (a) a n-period annuit y -imm ediate with constant

38

amount P ,and(b)n −1 deferred ann uities, where the jth deferred

annuit y is a (n − j)-period annuit y-imm ediate with lev el amoun t D

tostartattimej,forj =1, ···,n− 1.

• Th us, the presen t value of the varying annuity is

Pa

n

e

+ D

⎡

⎣

n−1

X

j=1

v

j

a

n−j

e

⎤

⎦

= Pa

n

e

+ D

⎡

⎣

n−1

X

j=1

v

j

(1 − v

n−j

)

i

⎤

⎦

= Pa

n

e

+ D

⎡

⎣

³

P

n−1

j=1

v

j

´

− (n − 1)v

n

i

⎤

⎦

= Pa

n

e

+ D

⎡

⎣

³

P

n

j=1

v

j

´

− nv

n

i

⎤

⎦

= Pa

n

e

+ D

"

a

n

e

− nv

n

i

#

. (2.35)

39

• For a n-period increasing ann uit y with P = D =1,wedenoteits

present and future values by (Ia)

n

e

and (Is)

n

e

, respectively.

• It can be sho w n that

(Ia)

n

e

=

¨a

n

e

− nv

n

i

(2.36)

and

(Is)

n

e

=

s

n+1

e

− (n +1)

i

=

¨s

n

e

− n

i

. (2.37)

• For an increasing n-pa ym en t annuity-due with pa ym en ts of 1, 2, ···,n

at time 0, 1, ···,n− 1, the present value of the annuit y is

(I¨a)

n

e

=(1+i)(Ia)

n

e

. (2.38)

• This is the sum of a n-period lev el annuity-due of unit paymen ts and

a (n − 1)-pay m ent increasin g annu ity-im mediate with startin g and

incremental paym ents of 1.

40

• Th us, we ha v e

(I¨a)

n

e

=¨a

n

e

+(Ia)

n−1

e

. (2.39)

• For the case of a n-period decreasing an nuity wit h P = n and D =

−1, we denote its presen t and future values b y (Da)

n

e

and (Ds)

n

e

,

respectively.

• Figure 2.9 presen ts the tim e diagram of this annuity.

• It can be sho w n that

(Da)

n

e

=

n − a

n

e

i

(2.40)

and

(Ds)

n

e

=

n(1 + i)

n

− s

n

e

i

. (2.41)

41

• We consider two types of increasing continuous annuities. First,

we consider the case of a contin uous n-period annuity with level

payment (i.e., at a constant rate) of τ units from tim e τ −1 through

time τ .

• We denote the present value of this ann uity b y (I¯a)

n

e

,whichisgiven

by

(I¯a)

n

e

=

n

X

τ =1

τ

Z

τ

τ −1

v

s

ds =

n

X

τ =1

τ

Z

τ

τ −1

e

−δs

ds. (2.42)

• The abo ve equation can be simplified to

(I¯a)

n

e

=

¨a

n

e

− nv

n

δ

. (2.43)

• Second, we may consider a con tinuous n-period annuit y for whic h

thepaymentintheintervalt to t + ∆t is t∆t, i.e., the instantan eou s

rateofpaymentattimet is t.

42

• We denote the present value of this ann uity b y (

¯

I¯a)

n

e

,whichisgiven

by

(

¯

I¯a)

n

e

=

Z

n

0

tv

t

dt =

Z

n

0

te

−δt

dt =

¯a

n

e

− nv

n

δ

. (2.44)

• We no w consider an ann uit y-immediate with pa yments following a

geometric progression.

• Let the first pa ym ent be 1, with subsequen t pa ym ents being 1+k

times the previous one. Thus, the present value of an ann uity with

n payments is (for k 6= i)

v + v

2

(1 + k)+···+ v

n

(1 + k)

n−1

= v

n−1

X

t=0

[v(1 + k)]

t

= v

n−1

X

t=0

"

1+k

1+i

#

t

43

= v

⎡

⎢

⎢

⎢

⎢

⎣

1 −

Ã

1+k

1+i

!

n

1 −

1+k

1+i

⎤

⎥

⎥

⎥

⎥

⎦

=

1 −

Ã

1+k

1+i

!

n

i − k

. (2.45)

Exam ple 2.13: An annuit y-im m ediate consists of a first payment of

$100, with subsequent payments increased by 10% o ver the previous one

until the 10th pa ym ent, after whic h subsequent pa ym ents decreases b y 5%

over the previous one. If the effective rate of intere st is 10% per payment

period, what is the presen t value of this ann uity with 20 pa y ments?

Solution: Thepresentvalueofthefirst10paymentsis(usethesecond

44

line of (2.4 5) )

100 × 10(1.1)

−1

= $909.09.

For the next 10 pa yments, k = −0.05 and their present value at time 10

is

100(1.10)

9

(0.95) ×

1 −

µ

0.95

1.1

¶

10

0.1+0.05

=1,148.64.

Hence, the presen t value of the 20 pa ym ents is

909.09 + 1,148.64(1.10)

−10

=$1,351.94.

2

Example 2.14: An investor wishes to accumulate $1,000 at the end of

year 5. He makes level deposits at the beginning of eac h year for 5 y ears.

The deposits earn a 6% ann ual effective rate of interest, wh ich is credited

45

at the end of each year. The interests on the deposits earn 5% effective

in terest rate annually. How much does he ha ve to deposit eac h y ear?

Solution: Let the lev el annual deposit be A. The interest receiv ed at

the end of y ear 1 is 0.06A, whic h increases by 0.06A ann u ally to 5 × 0.06A

at the end of year 5. T hus, the in terest is a 5-payment increasing annuit y

with P = D =0.06A, earning ann ual in terest of 5%. Hence, we have the

equation

1,000 = 5A +0.06A(Is)

5

e

0.05

.

From (2.37) we obtain (Is)

5

e

0.05

=16.0383,sothat

A =

1,000

5+0.06 × 16.0383

=$167.7206.

2

46

2.7 Term of Annuit y

• We now consider the case where the annuity period may not be an

integer. We consider a

n+k

e

,wheren is an integer and 0 <k<1.

We note that

a

n+k

e

=

1 − v

n+k

i

=

(1 − v

n

)+

³

v

n

− v

n+k

´

i

= a

n

e

+ v

n+k

"

(1 + i)

k

− 1

i

#

= a

n

e

+ v

n+k

s

k

e

. (2.46)

• Th us, a

n+k

e

is the sum of the present value of a n-period ann uit y -

immediate with unit amount and the present value of an amount s

k

e

47

paid at tim e n + k.

Exam ple 2.15: A principal of $5,000 generates incom e of $500 at the

end of every year at an effective rate of interest of 4.5% for as long as

possib le . Ca lc u la te the ter m of th e annu ity an d discu s s the possib ilitie s of

settling the last payment.

Solution: The equation of value

500 a

n

e

0.045

= 5,000

im p lie s a

n

e

0.045

=10. As a

13

e

0.045

=9.68 and a

14

e

0.045

=10.22, the principal

can generate 13 regular pa ym ents. The inv estm ent may be paid off with

an additional amount A at the end of year 13, in which case

500 s

13

e

0.045

+ A = 5,000 (1.045)

13

,

48

wh ich imp lies A = $281.02, so that the last pa ym ent is $781.02. Alter-

nativ ely, the last pa yment B ma y be made at the end of year 14, whic h

is

B =281.02 × 1.045 = $293.67.

If we adopt the approach in (2.46), we solve k from the equation

1 − (1.045)

−(13+k)

0.045

=10,

wh ich implies

(1.045)

13+k

=

1

0.55

,

from whic h we obtain

k =

ln

µ

1

0.55

¶

ln(1.045)

− 13 = 0.58.

49

Hence, the last payment C to be paid at time 13.58 years is

C =500×

"

(1.045)

0.58

− 1

0.045

#

=$288.32.

Note that A<C<B, which is as expected, as this follows the order

of the occurrence of the payments. In principle, all three approac hes are

justified. 2

• Generally, the effective rate of interest cannot be solv ed analytically

from the equation of value. Num erical methods must be used for

this purpose.

Exam ple 2.16: A principal of $5,000 generates incom e of $500 at the

end of ev ery year for 15 y ears. W hat is the effective rate of interest?

50

Solution: The equation of value is

a

15

e

i

=

5,000

500

=10,

so that

a

15

e

i

=

1 − (1 + i)

−15

i

=10.

A simple grid searc h pro vides the following results

i a

15

e

i

0.054 10.10

0.055

10.04

0.056

9.97

A finer search provides the answer 5.556%. 2

• The Excel Solver may be used to calculate the effectiverateofin-

ter e st in E x a mple 2.1 6 .

51

• The com putation is illustrated in Exhibit 2.1.

• We en ter a guessed value of 0.05 in Cell A1 in the Excel worksheet.

• The following expression is then en tered in Cell A2:

(1 −(1 + A1)ˆ(−15))/A1, whic h computes a

15

e

i

with i equal to the

value at A1.

• We can also use the Excel function RATE to calculate the rate of

in terest that equates the presen t value of an ann uit y-imm ediate to

a given value. Specifically, consider the equations

a

n

e

i

− A =0 and ¨a

n

e

i

− A =0.

Giv en n and A,wewishtosolvefori,whichistherateofinterest

per pa ym en t period of the ann uit y -imm ediate or ann uity-due. The

use of the Excel function RATE to com pute i is desc r ibed as follow s :

52

Exhibit2.1:UseofExcelSolverforExample 2.16

Excel function: RATE(np,1,pv,type,guess)

np = n,

pv = −A,

t ype = 0 (or omitted) for ann uit y-imm ediate, 1 for ann uity-due

gu ess = star tin g valu e , set to 0.1 if om itte d

Output = i, rate of interest per pa ym ent period of the annuit y

• To use RATE tosolveforExample2.16wekeyinthefollowing:

“=RATE(15,1,-10)” .

53