RESEARCH AND INFORMATION DIVISION

No. 64/ RN/Ref/December /2021 Reference Note December 2021

PARLIAMENT LIBRARY AND REFERENCE, RESEARCH,

DOCUMENTATION AND INFORMATION SERVICE

(LARRDIS)

REFERENCE DIVISION

BANKING OMBUDSMAN IN INDIA

Feedback : [email protected]

Prepared by RD Desk, Reference Division; Officers associated with the preparation – Smt Priyanka

Mahanta, Junior Library Assistant and Smt. Pooja Singh, Joint Director; supervised by Shri

Naushad Alam, Director and Shri Prasenjit Singh, Additional Secretary (23034134).

The Reference Note is for personal use of the Members in the discharge of their Parliamentary duties,

and is not for publication.

The Reserve Bank - Integrated Ombudsman Scheme, 2021 was launched

on 12 November 2021 in virtual mode by Hon‟ble Prime Minister Shri Narendra

Modi. The Scheme integrates the existing three Ombudsman Schemes of RBI,

the Banking Ombudsman Scheme, 2006; the Ombudsman Scheme for Non-

Banking Financial Companies, 2018, and the Ombudsman Scheme for Digital

Transactions, 2019, realizing „One Nation One Ombudsman‟.

The Banking Ombudsman Scheme (BOS) in India has been implemented

by the Reserve Bank of India (RBI) to redress the complaints of customers on

certain types of banking services provided by banks and to facilitate the

settlement of those complaints. This Scheme is an expeditious and inexpensive

forum for bank customers for resolution of complaints.

2

Introduction

The Banking Ombudsman Scheme was first notified by the RBI in 1995

under Section 35A of the Banking Regulation Act, 1949. Until the launch of the

Integrated Ombudsman Scheme, 2021 the Banking Ombudsman Scheme 2006 (as

amended in 2017) along with other services were in operation.

Who is a Banking Ombudsman?

Banking Ombudsman is a senior official appointed by the RBI as an appellate

body where customers can escalate complaints if the financial institution fails to

address the complaint within 30 days. Even when customers are not satisfied with

the resolution offered or explanation given by the financial institution they can

approach the ombudsman. The Reserve Bank may appoint one or more of its

officers as Ombudsman and Deputy Ombudsman, to carry out the functions

entrusted to them for a period not exceeding three years at a time.

The Reserve Bank - Integrated Ombudsman Scheme, 2021

The Reserve Bank - Integrated Ombudsman Scheme, 2021

1

seeks to resolve

customer grievances in relation to services provided by entities regulated by

Reserve Bank of India in an expeditious and cost-effective manner under Section

35A of the Banking Regulation Act, 1949, Section 45L of the Reserve Bank of

India Act, 1934, and Section 18 of the Payment and Settlement Systems Act, 2007

which will provide cost-free redress of customer complaints involving deficiency

1

https://www.rbi.org.in/Scripts/BS_PressReleaseDisplay.aspx?prid=52549

Hon`ble Prime Minister launches the Integrated Ombudsman Scheme 2021

“One Nation, One Ombudsman System has taken shape in the banking sector with the

Integrated Ombudsman Scheme today. It will help in resolution of every complaint and problem

of the bank customers on time and without any hassle. My opinion is that the biggest strength of

democracy is how strong, sensitive and proactive the grievance redressal system is. This is the

biggest test of democracy.”

3

in services rendered by entities regulated by RBI, if not resolved to the satisfaction

of the customers or not replied within a period of 30 days by the regulated entity.

In addition to integrating the three existing Ombudsman Schemes as mentioned (at

para 1), the Scheme also includes under its ambit Non-Scheduled Primary Co-

operative Banks with a deposit size of Rs 50 crore and above.

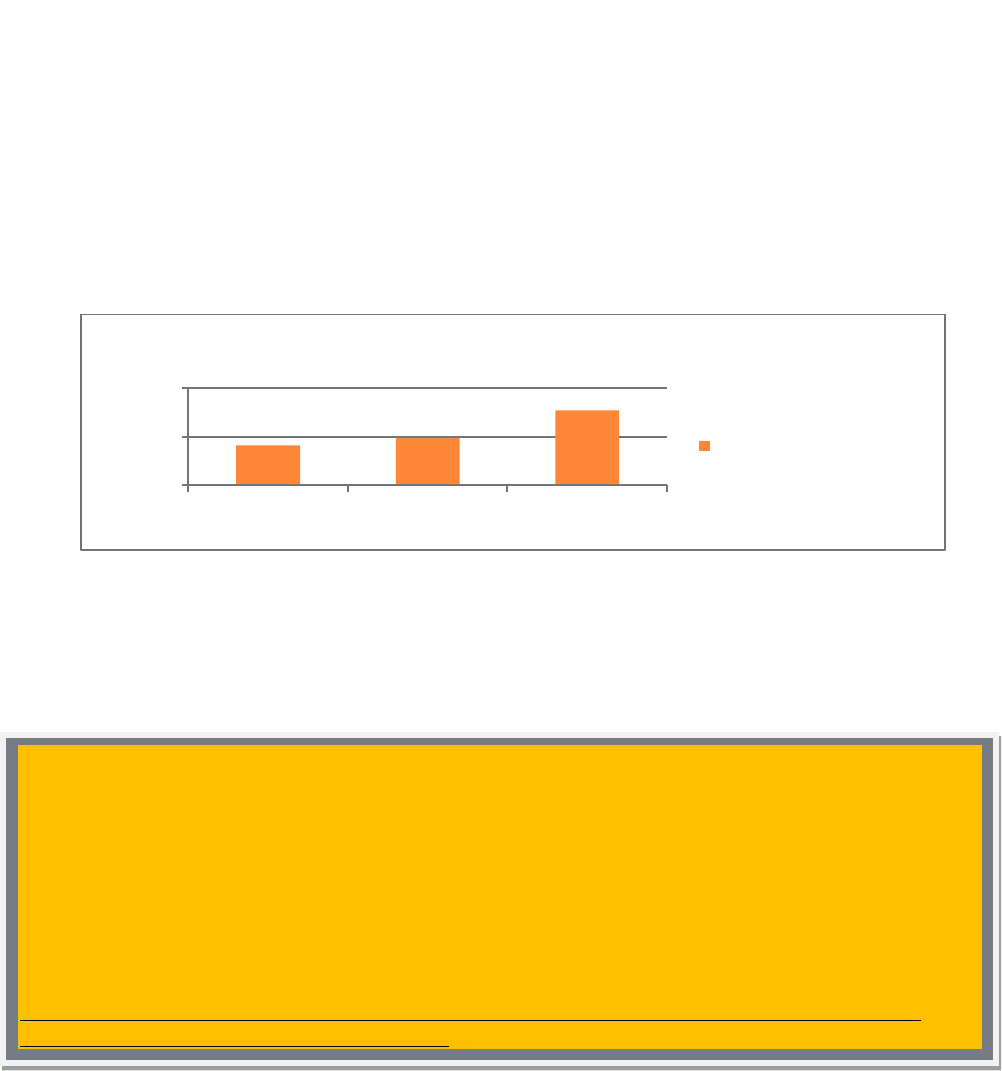

Receipt of Complaints Received at Offices of Banking Ombudsmen (OBOs)

The year wise details of complains received at the Banking Ombudsman

Offices in the last three years are as under:

Source: https://rbidocs.rbi.org.in/rdocs/Publications/PDFs/OMBUDSMANSCHEMES902211DE3C3948649EFC99C9AA53B22B.PDF

During 2019-20, there was an increase of 57.54 percent over the previous

year in receipts of complaints under the Banking Ombudsman Scheme.

163590

195901

308630

0

200000

400000

2017-18

2018-19

2019-20

Number of Complaints Received by OBOs

Number of Complaints

Received by OBOs

‘One Nation One Ombudsman'

“To make the alternate dispute redress mechanism simpler and more responsive to the customers of

regulated entities, it has been decided to implement, inter alia, integration of the three Ombudsman

schemes and adoption of the „One Nation One Ombudsman‟ approach for grievance redressal. The

move is intended to make the process of redress of grievances easier by enabling the customers of

the banks, NBFCs and non-bank issuers of prepaid payment instruments to register their

complaints under the integrated scheme, with one centralised reference point.” By RBI Governor

Shri. Shaktikanta Das.

https://www.thehindu.com/business/Economy/one-nation-one-ombudsman-rbi-to-integrate-consumer-

grievance-redressal-scheme/article33758518.ece

4

Salient Features of the Integrated Ombudsman Scheme, 2021

The Integrated Ombudsman Scheme, 2021 have been designed and defined

to be responsive to customers grievances. Some of its salient features include:

The Scheme will have one portal, one email and one address for the

customers to lodge their complaints;

It has done away with the jurisdiction of each ombudsman office;

The Scheme defines „deficiency in service‟ as the ground for filing

a complaint, with a specified list of exclusions. Therefore, the

complaints would no longer be rejected simply on account of “not

covered under the grounds listed in the scheme”;

It will no longer be necessary for a complainant to identify under

which scheme he/she should file complaint with the Ombudsman;

The Scheme has done away with the jurisdiction of each

ombudsman office;

A Centralised Receipt and Processing Centre has been set up at

RBI, Chandigarh for receipt and initial processing of physical and

email complaints in any language;

The responsibility of representing the Regulated Entity and

furnishing information in respect of complaints filed by customers

against the Regulated Entity would be that of the Principal Nodal

Officer in the rank of a General Manager in a Public Sector Bank or

equivalent; and

The Regulated Entity will not have the right to appeal in cases

where an Award is issued by the ombudsman against it for not

furnishing satisfactory and timely information/documents.

The Executive Director-in charge of Consumer Education and

Protection Department of RBI would be the Appellate Authority

under the Scheme.

Registering a Complaint with the Banking Ombudsman

Complaints under the new system can be filed with the Banking Ombudsman

through the online portal at https://cms.rbi.org.in. Complaints can also be filed

through the dedicated e-mail on [email protected]n or sent in physical mode to the

„Centralised Receipt and Processing Centre‟ set up at Reserve Bank of India in

Chandigarh. Additionally, operationalisation of a Contact Centre supported with a

5

toll-free number has also been announced. This Contact Centre will provide

information in eight regional languages to begin with besides Hindi and English.

The Contact Centre is mandated to provide information/clarifications regarding the

alternate grievance redress mechanism of RBI and to guide complainants in filing

of a complaint.

When to Approach the Ombudsman

One can file a complaint with the Banking Ombudsman if the reply to the

registered complaint from the regulated bank is not received within a period of one

month after the concerned bank receives the request, or the bank rejects the

complaint, or if the complainant is not satisfied with the reply given by the bank.

The Banking Ombudsman can receive and consider any complaint relating to the

deficiency in banking services [Details at Annexure I]. If a complaint is not settled

by an agreement within a period of one month, the Banking Ombudsman proceeds

further to pass an Award

2

. Before passing an award, the Banking Ombudsman

provides reasonable opportunity to the complainant and the bank, to present their

case. It is up to the complainant to accept the award in full and final settlement of

or to reject it.

Benefits of Integrated Banking Ombudsman

The Integrated Banking Ombudsman is bound to make the client service

more efficient and responsive. Being a citizen centric initiative it will provide

further impetus to the country‟s journey towards a more inclusive and responsive

financial system. It focuses on strengthening the grievance redress mechanism for

consumers of various services provided by the RBI regulated entities like Banks,

NBFCs and payment system operators. It offers the benefit of a single platform to

2 RBI has allowed banking ombudsmen to award compensation to the complainant for loss of time, expenses

incurred, harassment and mental anguish.

6

customers for getting speedy resolution of their grievances. This integrated scheme

will reinforce confidence and trust in the financial system with a single point of

reference to file complaints, submit documents, track the status of complaints and

receive feedback.

An aggrieved customer can, therefore, approach the Ombudsman following

failure in getting any remedy for his complaint against any bank where he operates

a bank account and does his transaction. Complaints like non-payment and delay in

payment, collection of drafts and cheques, bills, non-acceptance of small

denomination notes, delay in payment of inward remittances, failure issuing drafts,

pay orders, non-adherence to prescribed working hours besides any deficiency of

services provided by the Banks will now be decided by the banking ombudsman

within thirty days in accordance with the Integrated Banking Ombudsman Scheme

of RBI exemplifying „One Nation One Ombudsman‟.

References:

1. Reserve Bank of India Integrated Ombudsman Scheme 2021

https://rbidocs.rbi.org.in/rdocs/content/pdfs/RBIOS2021_121121.pdf

2. RBI Launched New Ombudsman Scheme :Step by Step Guide to File Complaint

Online https://www.news18.com/news/business/rbi-launches-new-ombudsman-scheme-

step-by-step-guide-to-file-complaint-online-4453247.html

3. RBI Expands Scope of banking Ombudsman Scheme; Includes Fair Banking

Practices https://rbi.org.in/Scripts/BS_PressReleaseDisplay.aspx?prid=14063

4. Annual Report of Ombudsman Scheme , 2019-20

https://rbi.org.in/Scripts/PublicationsView.aspx?id=20327

5. Launch of RBI-Retail Direct Scheme and Reserve Bank- Integrated Ombudsman

Scheme by Hon’ble Prime Minister on November 12, 2021

https://rbidocs.rbi.org.in/rdocs/PressRelease/PDFs/PR1185C760BB08CF994D55ABE7B

82B0F244E43.PDF

6. The Reserve Bank - Integrated Ombudsman Scheme, 2021

https://www.rbi.org.in/Scripts/BS_PressReleaseDisplay.aspx?prid=52549

8

Annexure 1

Conditions Amounting to Deficiency in Banking Services

non-payment or inordinate delay in the payment or collection of cheques, drafts, bills

etc.;

non-acceptance, without sufficient cause, of small denomination notes tendered for any

purpose, and for charging of commission in respect thereof;

non-acceptance, without sufficient cause, of coins tendered and for charging of

commission in respect thereof;

non-payment or delay in payment of inward remittances ;

failure to issue or delay in issue of drafts, pay orders or bankers‟ cheques;

non-adherence to prescribed working hours ;

failure to provide or delay in providing a banking facility (other than loans and advances)

promised in writing by a bank or its direct selling agents;

delays, non-credit of proceeds to parties' accounts, non-payment of deposit or non-

observance of the Reserve Bank directives, if any, applicable to rate of interest on

deposits in any savings, current or other account maintained with a bank ;

complaints from Non-Resident Indians having accounts in India in relation to their

remittances from abroad, deposits and other bank related matters;

refusal to open deposit accounts without any valid reason for refusal;

levying of charges without adequate prior notice to the customer;

Non-adherence to the instructions of Reserve Bank on ATM / Debit Card and Prepaid

Card operations in India by the bank or its subsidiaries

Non-adherence by the bank or its subsidiaries to the instructions of Reserve Bank on

credit card operations

Non-adherence to the instructions of Reserve Bank with regard to Mobile Banking /

Electronic Banking service in India by the bank

Non-disbursement or delay in disbursement of pension (to the extent the grievance can be

attributed to the action on the part of the bank concerned, but not with regard to its

employees);

Refusal to accept or delay in accepting payment towards taxes, as required by Reserve

Bank/Government;

Refusal to issue or delay in issuing, or failure to service or delay in servicing or

redemption of Government securities;

Forced closure of deposit accounts without due notice or without sufficient reason;

Refusal to close or delay in closing the accounts;

Non-adherence to the fair practices code as adopted by the bank;

Non-adherence to the provisions of the Code of Bank's Commitments to Customers

issued by Banking Codes and Standards Board of India and as adopted by the bank ;

Non-observance of Reserve Bank guidelines on engagement of recovery agents by banks;

Non-adherence to Reserve Bank guidelines on para-banking activities like sale of

insurance / mutual fund /other third party investment products by banks;

Any other matter relating to the violation of the directives issued by the Reserve Bank in

relation to banking or other services;

non-observance of Reserve Bank Directives on interest rates;

9

delays in sanction, disbursement or non-observance of prescribed time schedule for

disposal of loan applications;

non-acceptance of application for loans without furnishing valid reasons to the applicant;

non-adherence to the provisions of the fair practices code for lenders as adopted by the

bank or Code of Bank‟s Commitment to Customers, as the case may be;

non-observance of any other direction or instruction of the Reserve Bank as may be

specified by the Reserve Bank for this purpose from time to time; and

the Banking Ombudsman may also deal with such other matter as may be specified by

the Reserve Bank from time to time.