ISSN: 1962-5361

Disclaimer: This Philadelphia Fed working paper represents preliminary research that is being circulated for discussion purposes. The views

expressed in these papers are solely those of the authors and do not necessarily reflect the views of the Federal Reserve Bank of

Philadelphia or the Federal Reserve System. Any errors or omissions are the responsibility of the authors. Philadelphia Fed working papers

are free to download at: https://philadelphiafed.org/research-and-data/publications/working-papers.

Working Papers

Using High-Frequency Evaluations

to Estimate Discrimination: Evidence

from Mortgage Loan Officers

Marco Giacoletti

University of Southern California

Rawley Z. Heimer

Boston College

Edison G. Yu

Federal Reserve Bank of Philadelphia Research Department

WP 21-04

Revised April 2021

February 2021

https://doi.org/10.21799/frbp.wp.2021.04

Using High-Frequency Evaluations to Estimate Discrimination:

Evidence from Mortgage Loan Officers

∗

Marco Giacoletti

†

USC

Rawley Z. Heimer

‡

Boston College

Edison G. Yu

§

FRB-Philadelphia

Current Draft: March 1, 2021

First Draft: August 24, 2020

Abstract

We develop empirical tests for discrimination that use high-frequency evaluations to address

the problem of unobserved heterogeneity in a conventional benchmarking test. Our approach

to identifying discrimination requires two conditions: (1) the subject pool is time-invariant in

a short time horizon and (2) there is high-frequency variation in the extent to which evaluators

can rely on their subjective assessments. We bring our approach to the residential mortgage

market, using data on the near-universe of U.S. mortgage applications from 1994 to 2018.

Monthly volume quotas reduce how much subjectivity loan officers apply to loans they process

at the end of the month. As a result, the volume of new originations increases by 150% at the

end of the month, while application volume and applicants’ quality are constant within the

month. Owing to within-month variation in loan officers’ subjectivity, we estimate that Black

mortgage applicants have 3.5% to 5% lower approval rates, which explains at least half of the

observed approval gap for Blacks. When we use this approach to evaluate policies, we find

that market concentration and FinTech lending have had no effect on lending discrimination,

but that shadow banking has reduced discrimination presumably by having a larger presence

in under-served communities.

Keywords: Performance Incentives, Loan Officers, Mortgages, FinTech Lending, Lend-

ing Discrimination

∗

Previously titled “To the Back of the (Lending) Bus: How Loan Officers’ Performance Incentives Reveal Lend-

ing Discrimination.” We thank Michael Fitzpatrick for excellent research assistance. We thank Pat Akey, Mitchell

Berlin, Greg Buchak, Yulyia Demyanak, Ran Duchin, Andreas Fuster, Antonio Gargano, Hajime Hadeishi, Chris

Parsons, Micah Spector, Phil Strahan, and seminar participants at Baruch, ASU Finance Winter Conference, Boston

College, Federal Reserve Bank of Philadelphia, the Joint Finance Seminar, University of Oregon, and University

of Southern California for helpful feedback. This paper does not reflect the views of the Federal Reserve Bank of

Philadelphia or of the Federal Reserve System. Any remaining errors or omissions are the authors’ responsibility.

†

University of Southern California, Marshall School of Business. Phone: +1 (650) 475-6410, Email: mgia-

‡

§

1 Introduction

Racial and gender disparities have been documented in a range of fields, such as labor markets,

the legal system, and credit markets. Yet whether these disparities are the result of discrimination

by economic decision-makers—defined as an evaluator treating otherwise identical subjects from

minority groups worse than subjects from the majority group—remains in dispute. There has been

a growing trend toward using experiments and correspondence studies to test for discrimination

(Bertrand and Duflo, 2017). Nonetheless, tests for discrimination that use observational data have

several advantageous features. Such tests are accessible to a wide range of researchers, they are

easy to replicate and scale, they can be used to estimate aggregate costs of discrimination in a given

market, and policymakers can easily implement them.

However, tests for discrimination based on observational data face a number of economet-

ric challenges that limit their appeal. The most straightforward test for discrimination is an audit

or “benchmarking” test. Benchmarking tests claim to find discrimination when minority groups

receive unfavorable evaluations relative to the majority group. But, benchmarking tests are vul-

nerable to criticisms of omitted variable bias—differences in group characteristics, which the re-

searcher does not observe, can cause differences in evaluations across groups.

Alternatively, Becker (1957) proposed an “outcome test.” Instead of comparing differences

in how groups are evaluated, outcome tests compare the ex-post success of these evaluations.

The marginal minority will have better ex-post outcomes than the marginal majority subject be-

cause minority groups face higher thresholds for inclusion when they are subject to discrimination.

Though intuitively appealing, outcome tests are notoriously difficult to implement, most notably

because of the “infra-marginality” problem—the average difference in ex-post outcomes can be

a poor approximation of the difference in marginal outcomes (Ayres, 2002). Recent research has

made significant progress to improve econometric methods (e.g., Arnold et al., 2018), but address-

ing the infra-marginality problem requires additional modelling and distributional assumptions

(Simoiu et al., 2017). Furthermore, ex-post outcomes can be the result of self-fulfilling prophecies

1

(e.g., female students underperform in math because gender stereotypes reduce investment in fe-

males’ math education; Bordalo et al., 2016) and ex-post outcomes are often not easily measured

(e.g., worker productivity can be difficult to measure and proxies for productivity, such as wages,

can also be affected by discrimination).

We propose an alternative way to test for discrimination. The approach is motivated by the

observation that evaluators’ subjectivity can often vary substantially within short time intervals.

For example, employers that have immediate staffing needs can ill afford to turn away job appli-

cants. TSA agents might reduce their screening of travelers when they are at the end of their shifts

or there are long queues. Police officers that have monthly quotas would issue tickets to all drivers

that exceed the speed limit on the last day of the month. Our approach starts with a benchmarking

test, but addresses the problem of omitted variables by exploiting such high-frequency evaluations.

The approach requires two simple assumptions: time-varying discrimination and time-invariant

unobserved characteristics both in a short time interval (e.g., a month). The identification ratio-

nale is straightforward. If the evaluations of a group vary within a short time interval, then these

differences cannot be driven by unobserved subject characteristics, because the unobserved char-

acteristics are time-invariant.

We apply our approach to high-frequency data on mortgage applications, to test for discrim-

ination in the U.S. residential mortgage market.

1

We obtain the time-stamped version of the Home

Mortgage Disclosure Act (HMDA) data, covering the near-universe of mortgage applications from

1994 to 2018 with 500 million loan applications across more than 28,000 lenders. Crucial to our

empirical approach, we observe the exact application and decision date of each application.

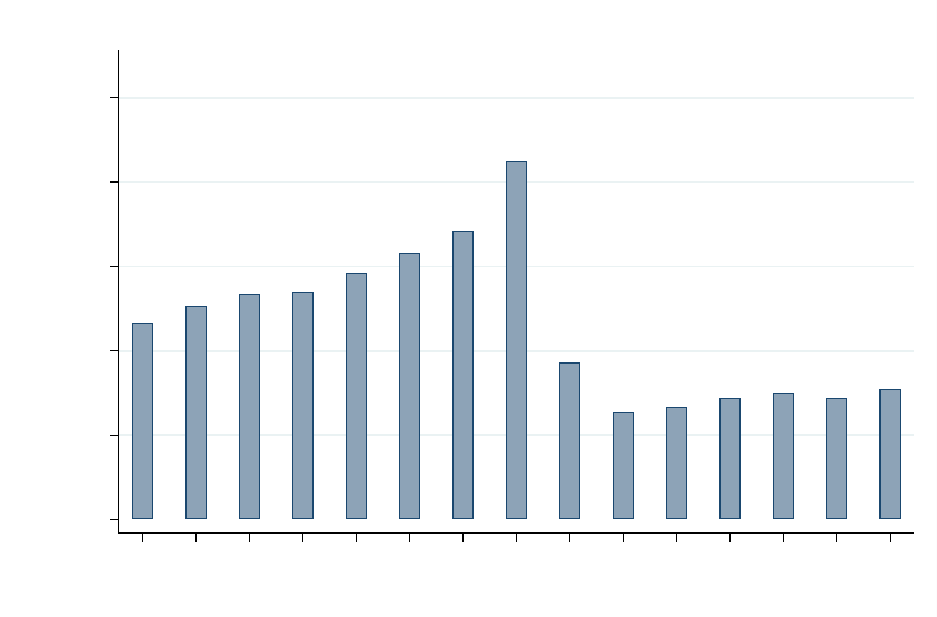

Figure 1 demonstrates our key source of high-frequency variation in the mortgage market

and the foundation of our empirical approach. The figure shows the volume of new originations

and new applications relative to the first day of a given month. The total volume of new mortgage

originations increases by more than 150% on the last day relative to the first day of a given month.

1

The literature can be traced back at least as far as the public release of HMDA data and the work of Munnell

et al. (1996). Ladd (1998) summarizes much of the older literature and frames longstanding debates. Other founda-

tional papers include Berkovec et al. (1994); Tootell (1996); Berkovec et al. (1998). Recent work has begun to study

differences in mortgage rates and fees (e.g., Bhutta and Hizmo, 2020).

2

0

50

100

150

200

percent

-7 -6 -5 -4 -3 -2 -1 0 1 2 3 4 5 6 7

days around last day of month

origination application

Number of loans originated vs applied (relative to first day of month)

Figure 1: The figure shows average percentage abnormal daily loan origination volume, and loan application vol-

ume (measured as number of originations and applications) in the U.S., for the last eight days of the month, and the

first seven days of the following month. The figure reports the average across all months over the sample period from

January 1994 to December 2018 from the HMDA data. Abnormal volume is computed with respect to loan origina-

tions and applications on the first day of the following month.

At the same time, the number of submitted mortgage applications stays constant over the course of

the month. These patterns reveal a crucial feature of the mortgage application process: loans are

processed by individual loan officers who have monthly performance targets that determine their

compensation.

2

Moreover, this within-month pattern in loan approvals unveils the component of

loan officers’ decision-making that is orthogonal to observable and unobservable factors affecting

loan originations (e.g., credit market conditions, applicant characteristics, and firm-level charac-

teristics). Drawing from Becker (1957), a profit-maximizing agent can give disparate treatment

to minority populations until market competition makes discrimination economically untenable.

2

Though we do not directly measure the compensation of any individual loan officer, for the most part, com-

missions are set based on the number of loans and the loan amount originated. And the compensation scheme

is common across employers. For example, see the following link for an article on the website of the Mort-

gage Bankers Association that discusses the industry standards for loan officers’ compensation in the U.S.

(https://www.mba.org/publications/insights/archive/mba-insights-archive/2019/is-it-time-to-rethink-compensation-

x253848). Tzioumis and Gee (2013) also note that loan officers face disciplinary actions if they fail to meet their

quotas several months in a row. Given this non-linear incentive scheme, Tzioumis and Gee (2013) and Cao et al.

(2020) document end-of-month bunching in a large U.S. commercial bank and in two Chinese banks, respectively.

3

Loan officers have an economic incentive to meet end-of-month performance incentives. As such,

loan officers’ subjective favoritism toward applicants has to attenuate at the end of the month

relative to the beginning of the month. Therefore, the within-month pattern, combined with a con-

ventional benchmark test, allows us to estimate the extent to which loan approval decisions can be

attributed to loan officers’ subjectivity towards applicants.

-.25

-.2

-.15

-.1

-7 -6 -5 -4 -3 -2 -1 0 1 2 3 4 5 6 7

days around last day of month

Average approval rate gap (Black minus white applications)

Figure 2: The figure reports the difference between the fraction of approved loans, out of all approved and denied

loans in the U.S., for Blacks minus the one for whites, on each of the last eight days of the month and the first seven

days of the following month.

Exploiting this within-month variation, our tests for discrimination estimate the difference in

approval rates between Black and white applicants at the start of the month relative to the end of

the month. Our key finding is summarized in Figure 2, which shows the difference in application

approval rates between Black and white applicants over the course of any given month. In the first

seven days of the month, Black applicants have 20 percentage point lower approval rates than white

applicants. The approval gap gets smaller over the course of the month. The approval gap between

Blacks and whites is just 10 percentage points on the last day of the month. The regression tests that

correspond to the graphical evidence in Figure 2 are saturated with a rich set of fixed effects that

control for time-varying economic conditions at precise geographic levels, namely county-month.

4

The regressions also include lender-month fixed effects that control for factors, such as regulations,

that would affect lending at the institution level. Confirming the graphical evidence, the difference

in the Black-white approval gap between the start and the end of the month is 3 to 5 percentage

points. This constitutes a lower bound on the share of the Black-white approval gap that is due

to loan officers’ subjectivity, relative to the approval gap that can be attributed to unobservable

group-differences. We estimate, in our most stringent regressions, that loan officers’ subjective

decision-making explains at least half of the overall difference in approval rates between Black

and white applicants even after controlling for observable characteristics. In terms of aggregate

magnitudes, if the approval rate gap for every day of the month was as small as the last day of the

month, about 1.4 million more Black applications would have been approved rather than denied

between 1994 and 2018, which corresponds to a total loan size of about $213 billion in 2018

dollars.

Our approach to estimating discrimination hinges on a set of simple assumptions that we de-

rive and that are easily supportable, either in the data or via narrative, or both. The first assumption

is that the loan officer has time-varying costs of being subjective. In our setting, loan officers have

nonlinear contract incentives.

3

Loan officers that fail to meet their volume quotas will have re-

duced compensation and risk getting fired. The second assumption is that the characteristics of the

subject pool are time invariant. Indeed, we find that application volume, the relative share of Black

applications, and loan application quality (for both Black and white applications) are all constant

over the course of the month. The remaining threat to identification is that there are differential

trends by race in the quality of applications that get processed over the course of the month. As

evidence against this explanation, we find that high-quality and low-quality Black mortgages have

similar amounts of bunching toward the end of the month.

3

Importantly, with volume quotas, the optimal strategy would be to approve all loan applications. However, in

practice, there are several constraints on this strategy. Lenders set origination standards that an application has to

exceed and loan officers may have a fixed quantity of mortgage credit that they can distribute within a month. Loan

officers can use their discretion and work to sidestep the origination standards by either using risk-based pricing or

appealing to other “soft” criteria, such as noting that the applicant is a customer of the bank.

5

In contrast to other methodologies, our approach does not require ex-post outcomes to test

for discrimination. Nevertheless, we show that a conventional outcome test is potentially mislead-

ing about the levels of discrimination in mortgage lending. We find that Black mortgages have

significantly higher rates of default, which could be interpreted as evidence of reverse discrimina-

tion that favors minorities. Instead, this result is almost certainly caused by the infra-marginality

problem – the fact that Black and white mortgage applicants have different risk distributions. We

compare the subsequent default rates of applications approved at the start of the month to those

approved at the end of the month. The within-month differential significantly shrinks the raw dif-

ference between Black and white default rates. As such, these findings suggest that our approach

potentially counteracts the shortcomings of a conventional outcome test.

Furthermore, our approach offers guidance, relative to both benchmarking and outcome tests,

as to whether observed discrimination is caused by taste-based versus statistical discrimination. We

develop an additional set of assumptions to distinguish between the two theories. Put simply, the

case for statistical discrimination requires asymmetric information between evaluators and sub-

jects. Because of the high-frequency nature of our data, statistical discrimination would require

the loan officers’ information set about applicants to change from the start to the end of the month.

This explanation is unlikely because we show that the applicant pool is time invariant. Related,

we consider the role of inaccurate beliefs (i.e., stereotypes Bordalo et al., 2016) and a similar logic

precludes this explanation.

Finally, our approach is advantageous because it can easily be applied to evaluate the effect

of market policies and market innovations on the quantity of discrimination. We consider three im-

portant features of modern mortgage lending: market concentration in banking, FinTech lending,

and shadow banking. We find that the amount of discrimination due to loan officers’ subjectivity

is unaffected by both market concentration and FinTech lending. This result is largely consistent

with the fact that our regressions include lender-by-month fixed effects and that the component

of loan officer subjectivity our approach uncovers occurs within-lender. Moreover, despite these

changes to the banking sector, loan officer compensation incentives have largely remained con-

6

stant throughout our sample, and even mortgage lending at FinTech lenders involves significant

discretion from human loan officers. On the other hand, we find that shadow banks have lower

levels of subjective discrimination against Black applicants. This is likely the result of shadow

banks—owing to their lower regulatory requirements—having a larger presence in under-served

communities.

Related Literature

Our paper is related to advances in the literature on identifying discrimination by economic decision-

makers. Our approach bears closest resemblance to empirical papers that use changes to evaluation

settings to identify discrimination against minority groups. For example, Goldin and Rouse (2000)

shows that blind auditions reduce employment discrimination against female orchestra musicians.

Police officers are less likely at night than during the day to pull over Black motorists because

the driver’s race is difficult to identify (Pierson et al., 2020). These empirical papers identify

discrimination by comparing situations in which evaluators know the subject’s gender and race to

situations in which they do not. Our approach is different because there is no change in the loan of-

ficer’s knowledge of applicants’ race. We show that discrimination can be identified under a set of

simple assumptions about the applicant pool and loan officers’ reliance on subjective assessments.

More specifically, our paper joins a large and important literature on discriminatory lending

practices in consumer credit markets. Our empirical approach is grounded in evidence that loan

officers have significant discretion in loan processing decisions (see e.g., Engelberg et al., 2012;

Chen et al., 2016; Demiroglu et al., 2019). Most similar to our analysis, Cort

´

es et al. (2016) also use

confidential HMDA data to disentangle application dates from processing dates to show that loan

officers are more likely to approve mortgages on sunny days. Guided by this finding, we bring the

confidential HMDA data to the question of lending discrimination. Several papers find compelling

evidence that individual loan officers discriminate against other races and women.

4

We advance

4

In no particular order, Fisman et al. (2017, 2020) use data from Indian banks to show that loan officers are more

favorable to culturally proximate applicants. Beck et al. (2018) use evidence from an Albanian bank and Montoya

et al. (2019) use a field experiment at a Chilean bank to uncover evidence of gender discrimination in consumer lend-

ing. Ambrose et al. (2020) find that minorities pay higher fees when they have a white mortgage broker.

7

this literature in a few ways. With a few exceptions (e.g., Bohren et al., 2019; Dobbie et al., 2020),

most papers are unable to distinguish between taste-based and statistical discrimination. Our ap-

proach can offer guidance about which type of discrimination is most likely. Also, these papers use

evidence from confidential internal data from one or two lending institutions. In contrast, our paper

uses the universe of U.S. mortgage applications over a 25-year period to connect racial disparities

in lending to the incentives of individual loan officers. This allows us to address crucial questions

about external validity, investigate the effects of the market structure, and quantify the scope of

racial bias in mortgage markets.

Second, our paper contributes to a growing literature on how market structure and technology

affect consumer lending. First, recent papers find support for classic theories arguing that compe-

tition reduces discrimination in consumer lending (Buchak and Jørring, 2017; Butler et al., 2019).

Such papers suggest that racial discrimination declines because of changes to the composition of

lending institutions. We find that discrimination by individual decision-makers can persist within

organizations even when there are differences in institution-level competition across markets. Sec-

ond, there is significant debate over how the growth of FinTech lending affects the allocation of

credit, with a particular interest in the effects on disadvantaged borrowers. In theory, FinTech can

reduce intermediation costs which can pass through to consumers (e.g., Tang, 2019) or improve

screening (Berg et al., 2020a). However, the literature finds that FinTech algorithms have either no

effect or negative effects on the supply of credit to disadvantaged consumers (see e.g., Fuster et al.,

2017; Bartlett et al., 2019). Our contribution is to show that biases in human decision-making can

survive advances in loan processing technology (similar to findings on the introduction of machine

learning to judicial outcomes, as shown by Kleinberg et al., 2018).

Finally, we make a unique contribution to the literature on performance-based compensation,

with a particular focus on financial intermediation. The effects of performance-based compensa-

tion have been studied in a range of settings, such as manufacturing (Oyer, 1998), software sales

(Larkin, 2014), government contracts (Liebman and Mahoney, 2017), healthcare (Li et al., 2014;

Gravelle et al., 2010), firm managers (Bandiera et al., 2007) and accounting (Murphy, 2000). The

8

literature has also studied how performance incentives within banks affect loan officers’ effort

and performance (Agarwal and Ben-David, 2012; Cole et al., 2015), and information production

(Hertzberg et al., 2010; Qian et al., 2015; Berg et al., 2020b). To the best of our knowledge, our

paper is the first to study variation in performance incentives combined with racial biases in human

decision-making.

2 Identifying Discrimination

This section presents a formal discussion of our empirical setup. We compare our approach to

existing frameworks for identifying discrimination. Differences in unobserved characteristics of

different subject groups pose a challenge for conventional tests for discrimination. Our approach

is to filter out these unobserved differences across subject groups by using high frequency data.

Our approach extends conventional tests for discrimination, called either audit or bench-

marking. These tests compare the conditional likelihood that a minority subject group receives

disparate treatment relative to the majority group, after controlling for other observable character-

istics from the point of view of the researcher. Consider the case of a Black mortgage applicant.

The researcher claims to have uncovered discrimination when she rejects the null of no difference

in the conditional likelihood of approval between Blacks and whites, and instead finds that the

likelihood is significantly smaller for Blacks. Specifically, the researcher claims discrimination

when she finds that:

P (a|W, X) > P (a|B, X) (1)

where P (a|R, X) is the probability of loan application approval, conditional on race R ∈ {W, B}

(white or Black) and a vector of observable characteristics X to the researcher. However, this

approach is exposed to the criticism that the difference in approval rates between white and Black

applicants might be driven by unobserved characteristics that are relevant for the assessment of

applicants’ credit risk used by the loan officers, but are not included in the vector of controls X

9

used by the researcher. To see that, assume for simplicity that there is a binary unobserved variable

Z ∈ {Z

L

, Z

H

}, such that the following assumptions are satisfied:

Assumptions Set (A)

No discrimination: P (a|W, X, Z

k

) = P (a|B, X, Z

k

)

for k ∈ {H, L}

Higher quality predicts higher approval probability: P (a|R, X, Z

H

) > P (a|R, X, Z

L

)

On average white applicants have better unobservables: P (Z

H

|W, X) > P (Z

L

|B, X)

The inequality in approval rates formalized by equation (1) holds under the set assumptions above

when omitting the variable Z, even though decision-makers do not discriminate when all of the

characteristics are accounted for (see Appendix A.I). The differences in approval rates for dif-

ferent races simply capture the differences in the unobserved characteristics. In the mortgage-

lending setting, Black and white applicants have substantially different observable characteristics

(see Table 1). Such differences raise concern that there might be also substantial differences in

unobservables.

In this paper, we show that we can refine existing approaches to address the identification

problems due to the systematic differences in unobservables across subject groups. Rather than

only testing for the differences in the likelihood of approval between white and Black applicants,

we use high-frequency data to test whether those differences vary over a short period of time.

Because discrimination is determined by the subjective judgment of the evaluators, under the null

of no discrimination, and if applicant characteristics remain constant over time, there shall be no

change in the approval rates over time. On the other hand, discrimination would predict a change

in the relative approval rates over time.

To formalize this idea, let there be two time periods, T ∈ {Start, End}. Assume that

evaluators have more scope to be subjective in period Start relative to period End. Then, in the

10

presence of time-varying discrimination we expect to find:

P (a|W, X, End) − P (a|B, X, End) < P (a|W, X, Start) − P (a|B, X, Start) (2)

where P (a|., X, .) is the probability of approval, conditional on race (white or Black), a vector of

observable characteristics X, and in a specific period (Start or End). Note that the presence of

unobservable quality characteristics systematically correlated with race cannot alone explain the

effects in equation (2). Consider the following set of assumptions that characterize a situation in

which there is no discrimination:

Assumptions Set (B)

No discrimination: P (a|W, X, Z

k

, T ) = P (a|B, X, Z

k

, T )

for k ∈ {H, L}

Higher quality predicts higher approval probability: P (a|X, Z

H

, T ) > P (a|X, Z

L

, T )

On average white applicants have better unobservables: P (Z

H

|W, T ) > P (Z

H

|B, T )

No time pattern in applications quality: P (Z

H

|R, X, Start) = P (Z

H

|R, X, End)

The first three assumptions are the same as in Assumptions Set (A), while the last assumption

states that the unobserved characteristics of the applicants, for both whites and Blacks, are on

average constant over time. Jointly, these assumptions imply (see Appendix A.I):

P (a|W, X, End) − P (a|B, X, End) = P (a|W, X, Start) − P (a|B, X, Start).

Thus, the condition in equation (2) indeed amounts to a rejection of the null of no discrimination.

2.1 Distinguishing Taste-Based from Statistical Discrimination

This section explores the extent to which our approach can distinguish between the two broad

categories of discrimination. Under “taste-based” discrimination, minorities are subject to dis-

parate treatment because evaluators have animus toward them. Under “statistical” discrimination,

11

evaluators are uncertain about the abilities of any given subject. Evaluators form their beliefs after

observing the subject’s race. Minorities are subject to disparate treatment when evaluators have de-

veloped beliefs that minority subjects have worse abilities. Evaluators do not need to have accurate

beliefs about minorities to apply disparate treatment (see e.g., Bohren et al., 2020).

We consider evaluators j who, over a short time-period, for example a month or a week,

evaluate subjects i. Each evaluator j has perceived net benefits from making decisions that favor

subject i equal to U

j

(X

i

, Z

i

, R

i

, t), where X

i

and Z

i

are vectors of observable and unobservable

(from the perspective of the researcher) characteristics, R

i

is the subjects’ race (e.g., R

i

= W

for a white applicant and R

i

= B for a Black applicant), and t is the point in time in which the

evaluation is conducted.

The evaluator’s net benefits can be decomposed into two components:

U

j

(X

i

, Z

i

, R

i

, t) = b

j

(X

i

, Z

i

, R

i

, t) + E

j

[u

i

|X

i

, Z

i

, R

i

, t], (3)

where b

j

(X

i

, Z

i

, r

i

, t) is the subjective net benefits of evaluator j conditional on all characteristics,

and E

j

[u

i

|V

i

, Z

i

, R

i

, t] is the statistical component. The statistical component can be written as

E

j

[u

i

|X

i

, Z

i

, R

i

, t] = E[u

i

|X

i

, Z

i

, R

i

, t] + τ

j

(R

i

, t), (4)

where τ

j

(.) is the bias of decision maker j when forming expectations conditional only on the

information about the race of an applicant.

We can then use our stylized framework to characterize different types of discrimination, for

example against Black subjects with respect to white subjects:

- Taste-based discrimination: b

j

(X

i

, Z

i

, W, t) > b

j

(X

i

, Z

i

, B, t)

- Statistical discrimination: τ

j

(W, t) > τ

j

(B, t)

12

The decision maker will take a decision favorable to subject i as long as the net benefit is

positive:

b

j

(X

i

, Z

i

, R

i

, t) + E

j

[u

i

|X

i

, Z

i

, R

i

, t] + v

i,j,t

> 0,

where v

i,j,t

is a random preference shock, i.i.d. across subjects and evaluators, and independent of

information on subject characteristics and evaluators’ beliefs. We can then introduce the variable

y

i,j,t

, which is equal to one if subject i receives a favorable decision from evaluator j at time t, and

has likelihood function:

L(y

i,j,t

) = P r(y

i,j,t

= 1)

I(y

i,j,t

=1)

[1 − P r(y

i,j,t

= 1)]

1−I(y

i,j,t

=1)

P r(y

i,j,t

= 1) = E[y

i,j,t

|X

i

, Z

i

, R

i

, j, t] = F (X

i

, Z

i

, R

i

, j, t).

If we assume the function F (X

i

, Z

i

, R

i

, j, t) can be approximated with a liner specification,

then we can write:

y

i,j,t

= β

1

r

i

+ β

2

(r

i

× t) + ηX

i

+ φZ

i

+ a

t

+

i,j,t

(5)

where r

i

= 1 if R

i

= B. Equation (5) can be estimated in the data. Within this specific framework,

we can state the predictions of our general discussion in the previous section along the following

lines:

1. The two types of discrimination listed above (driven by taste or statistical) would cause

estimates of β

1

< 0. However, as the previous section outlines, β

1

will be a biased estimate

unless the researcher fully controls for observable (X

i

) and unobservable (Z

i

) characteristics,

or r

i

is uncorrelated with any omitted characteristics.

2. Estimates of β

2

will be different from zero if the magnitude of discrimination changes over

time, regardless of the type of discrimination. If subject pool characteristics (X

i

and Z

i

)

are not correlated with the evaluation time t, estimates of β

2

will be unbiased even if the

researcher does not perfectly control for time-invariant characteristics.

13

How can this approach distinguish between different theories of discrimination? In principle,

any type of discrimination can be subject to high-frequency fluctuations, and thus produce non-

zero estimates of β

2

. However, if the unobserved variation across subject pools and the evaluator’s

statistical inference problem are time-invariant, our approach allows the researcher to attribute

discrimination to the source of time-variation in the evaluator’s decision-making.

Consider the case of statistical discrimination. Statistical discrimination is caused by the

evaluators’ statistical inference problem. Therefore, the researcher can reasonably assume the

findings are caused by statistical discrimination if she can provide evidence of time-variation in the

evaluators’ information set. Now consider taste-based discrimination. The evaluator’s subjective

preferences against minorities causes disparate treatment. The researcher can assume taste-based

discrimination if she has evidence that evaluators’ subjectivity is time-varying.

In the following empirical analysis, we focus on residential mortgage lending in the U.S.

Our source of time-variation in evaluations is the fact that loan officers have monthly volume quo-

tas. These monthly volume quotas generate within-month variation in loan officers’ subjectivity.

The volume quotas pressure loan officers to increase their approval rates at the end of the month,

whereas at the start of the month, loan officers have scope to apply their subjective preferences. At

the same time, loan officers observe the same information about applications that they process at

the start of the month relative to the end of the month. As such, any finding of discrimination due to

within-month differences in evaluations can be attributed to loan officers’ subjective preferences.

3 Data

The empirical results in this paper are based on the confidential version of the HMDA data available

to researchers in the Federal Reserve System. The dataset contains the largest sample of mortgage

applications available in the U.S. The public version of the data includes information on applicant

characteristics – race, gender, reported income, and location of the property – and identifiers for

the lenders that received the applications. The data cover the entire geography of the U.S. over

the period from January 1994 through December 2018. Moreover, the data provide information on

14

mortgage contract characteristics, such as whether the application is for a new home purchase or

refinancing, the loan amount, the lien, and whether the property is owner-occupied. The primary

distinguishing feature of the confidential version of the HMDA data is that it contains the exact

date on which each application was submitted by a potential borrower and the date on which each

application was processed by the lender (either approved or denied) or withdrawn by the applicant.

This information has been employed in several prior papers (see e.g., Cort

´

es et al., 2016).

Table 1, panel (a) shows summary statistics of the mortgage applications in our dataset, for

each year from 1994 to 2018. Annual mortgage applications are between 10.1 and 37.3 million,

and originations between 7.2 and 23.7 million. The number of active lenders by year is between

5,700 and 9,800, and the average number of originations per lender is between 750 and 2,900.

Panel (b) shows statistics over the entire period from 1994 to 2018, and across different applicant

groups based on race. Approximately 67% of applicants are white and 7% are Black. Other races

are not separately identified and are grouped, along with applications that do not specify race, into

a single category called “Other race” that includes 26% of all observations. Black applicants apply

for smaller loans on average, have the highest fraction of low income applicants (59.8%, compared

to 46% for whites and 47.8% for other races), and have the lowest approval rate (63.25%, compared

to 80.72% for whites and 69% for other races). When considering approved loans, 73.7% are to

whites, 5.7% to Blacks and 20.6% to applicants of other races.

To obtain more detailed information on characteristics and performance of originated mort-

gage loans, we merge HMDA with the Black Knight McDash (McDash) dataset. We construct the

merged sample with an algorithm similar to the one used by Rosen (2011). Individual observations

in HMDA and McDash are merged using loan origination date, loan amount, zip code, lien type,

loan type, loan purpose, and occupancy type (owner occupied, absentee or investment property).

The match rate of the merge is about 60%.

5

McDash provides further information on individual

loan contracts, such as the mortgage interest rate, rate type (fixed or adjustable rate), the mortgage

5

Lender and consumer identities were anonymized for the merged dataset used in this analysis.

15

term, whether the loan is conforming, borrowers’ FICO scores, and the quality of the supporting

documentation submitted by the borrower.

4 Identifying Assumptions

Our identification strategy relies on high-frequency variation in evaluators’ subjective decision

making. This section provides support for the identification assumptions: (1) the pool of mort-

gage applicants is time-invariant and (2) there is time-variation in loan officers’ reliance on their

subjective assessments.

4.1 The Applicant Pool is Time-Invariant

The first identifying assumption in our tests for discrimination is that the composition of the appli-

cant pool is time-invariant. Figure 3 shows how the composition of new applicants evolves over the

course of the month. Panel (a) plots the average share of Black applicants submitted on each day

of the month. Black applicants’ share of new applications is roughly constant at approximately 7%

on each day of the month. This confirms our identifying assumption that the racial composition of

applicants is time-invariant.

We also verify that other characteristics of the applicant pool—characteristics that could

correlate with race—are constant over the course of the month. The HMDA data has limited infor-

mation on the creditworthiness of applicants. However, the data contain applicants’ income, which

is an important input into lender’s decision-making and is likely correlated with other variables that

determine whether an application is approved (e.g., credit scores). Figure 3, Panel (b) reports the

fraction of applicants that have levels of personal income that are below the median of applicants

within a county during a given year. Panel (c) shows the share of such applicants with the added

restriction that the application becomes a new origination. In both panels, we divide the sample

into applications submitted by Black and white applicants. As such, these figures explore whether

the quality of applications within and across races changes within the month. These figures show

that application quality is constant.

16

Lastly, Panel (d) studies the composition of the applicant pool with outstanding applications

(i.e., applications that have been submitted but have yet to receive an approval decision) in the

lenders’ inventory over the course of the month. We explore this measure of application inventory

because it captures what applications the loan officer has the opportunity to work on at any point

during the month. Panel (d) also sorts the outstanding applications by income and by race. Again,

we find that the applicant pool is constant over the course of the month, both in terms of the racial

composition of the applicant pool and the quality of the applications outstanding.

4.2 Time-Variation in Subjective Assessments of Applicants

4.2.1 Loan Officers Have Monthly Volume Quotas

Mortgage loan officers tend to receive commissions calculated as a percentage of the total amount

they originate over the month. They can also receive bonuses for meeting monthly origination

targets, as well as face disciplinary actions or be fired for failing to meet volume targets.

6

The use

of volume-based incentives is acknowledged by U.S. regulations and directives from the Consumer

Financial Protection Bureau (CFPB). U.S. law permits the use of volume-based incentives, but it

restricts the use of commissions based on the terms and performance of individual loans (see, most

recently, the dispositions of Regulation Z, implementing the Truth in Lending Act).

7

Seeing as loan officers have monthly volume targets, how would these non-linear contract

incentives affect loan officer behavior? We consider several theories, even though such theories

are not distinguishable in our data, nor do we intend to establish a single theory. However, many

such theories share a common feature: loan officers’ decision criteria vary in a way that lessens

6

See Tzioumis and Gee (2013), and evidence from practitioners’ research and discussions, such as

what is reported in the following articles on industry standards for loan officers’ compensation in the U.S.,

published by the Mortgage Bankers Association (https://www.mba.org/publications/insights/archive/mba-

insights-archive/2019/is-it-time-to-rethink-compensation-x253848), and by consumer websites

(https://www.investopedia.com/ask/answers/120214/whats-average-salary-loan-officer.asp and

https://www.thetruthaboutmortgage.com/loan-officer-jobs/#salary).

7

Volume-based incentives are the first form of compensation mentioned in the section on

Permissible Methods of Compensation in the most recent revision of Regulation Z, available at

https://www.federalregister.gov/documents/2013/02/15/2013-01503/loan-originator-compensation-requirements-

under-the-truth-in-lending-act-regulation-z.

17

their scope for subjective decision making as the end of month nears. Instead, in order to meet

their volume quotas, loan officers have to approve more loans at the end of month regardless of

their preferences toward any given applicant. Nevertheless, the following outlines these theories to

guide our understanding of the setting.

First, the end-of-month increase in new originations can be caused by rational loan officers

that get dis-utility from exerting effort. Assume that loan officers prefer to work fewer than a

certain number of hours per day. Whether or not the loan officer meets his volume target is a

function of the effort he exerts, as well as how much effort it takes to finalize a loan approval.

The amount of effort each loan takes is determined by random factors that the loan officer does

not control, such as macroeconomic shocks and loan-specific idiosyncratic shocks. Assuming that

new loan applications arrive randomly over the course of the month, loan officers’ optimal strategy

would be to start with a lower effort at the beginning of the month and gradually increase their

effort over the course of the month. And when the end of month nears, they would increase their

effort in order to exceed the volume threshold. This strategy by loan officers will cause large

increases in loan originations at month-end. The strategy also implies that loan officers can be

more subjective about loans processed at the start of the month, but need to be less discerning and

seek approvals for all loans that they process at the end of the month.

Behavioral biases, such as procrastination (Akerlof, 1991), can also cause loan officers to

delay the approval of loans until the end of the month. Alternatively, decision-makers can be

overconfident—they overestimate their own abilities. Loan officers that have an overconfidence

bias would overestimate their abilities to process loans over the course of the month and would

have to work overtime at the end of the month in order to meet their quotas.

4.2.2 Monthly Volume Quotas Cause End-of-Month Bunching in Mortgage Originations

We find that monthly volume quotas cause large increases in new mortgage originations at the

end of the month. Figure 1, described in the introduction, presents the average volume of new

originations per day relative to the first day of any given month. The volume of new mortgage

18

originations grows over the course of the month. The origination volume is more than 150% larger

on the last day relative to the first day of a given month. The figure documents clear evidence of

“bunching” at the end of any given month.

The end-of-month bunching in mortgage originations is robust across time and to seasonal

factors. The end-of-month increase in originations occurs in every year of our sample, which

suggests that the finding is not caused by business cycles and is therefore unlikely to be caused

by fluctuations in the demand for mortgages (see Appendix Figure A.1). Also, the end-of-month

bunching occurs in every month of the calendar year (see Appendix Figure A.2, which plots the

average number of new originations on the first and last seven days of each month within a given

year). This suggests that the finding is not caused by seasonality in mortgage demand.

8

Building on our graphical evidence, we use regression analysis to show that the within-month

pattern in originations is not caused by confounding factors. We estimate the following regression:

log(N

t

) = β

lw

I

lw

+ β

fw

I

fw

+ a

ym

+ a

dow

+ a

holiday

+ e

t

(6)

where the dependent variable log(N

t

) is the log of the number of originated mortgages by lender i

on day t. The regression includes year-month, day-of-week, and bank-holiday fixed effects, which

are a

ym

, a

dow

, and a

holiday

, respectively. I

lw

and I

fw

are dummies equal to one for days in the last

week of the month and the first week of the following month. The coefficient of interest, β

lw

(β

fw

),

measures the difference between the average origination volume in the last (first) seven days of the

month, relative to the middle days of the month.

The regression estimates confirm that loan origination volume increases significantly in the

last days of the month relative to the middle days. In Table 2, when origination volume is measured

as the log number of loans, the point estimate of β

lw

is 31%, and the estimate of β

fw

is -15%. When

origination volume is measured as the total dollar amount originated per day, the point estimates

are 36% and -14%. This gives us estimates of the increase in origination volume between the

8

As a testament to the quality of our micro-level data, recurring-day bank-holidays are clearly visible in Figure

A.2. Origination volume is abnormally low on the first day of January, on Christmas and on July 4th.

19

first and last week of the month of 46% and 50%, which are qualitatively consistent with the

evidence shown using the raw data in Figure 1. Our findings are unlikely to be explained by

lending seasonality because the estimates are robust to including a rich set of calendar time fixed

effects (see e.g., Murfin and Petersen, 2016).

9

We also show that the end-of-month bunching in new originations is consistent with loan

officers managing the inventory of applications over the course of the month. Figure A.3 in the

Appendix shows the inventory of applications that await a decision (approval, denial, or withdrawal

by the applicant) for each day within the month. There is a sharp drop in inventory over the last

week of the month, driven by the spike in originations, and then a steady increase taking place over

the first two weeks of the following month.

4.2.3 Linking Origination Volume to Loan Officers’ Performance

Next, we connect loan officers’ performance incentives to the end-of-month bunching in new orig-

inations. To do so, we consider how loan officers’ monthly volume targets affect their economic

incentive to approve and deny applications. Specifically, we expect that loan officers have to in-

crease the pace of new originations when they are not on track to meet their quotas. Though our

data does not contain the origination targets set by each lender, we infer that loan officers’ vol-

ume targets are a function of mortgage lending seasonality and the lender’s internal projections.

As such, we expect that each lender will have their own month-by-month benchmarks that are a

function of their origination volume in prior years (e.g., origination volume in March 2012 is a

reasonable estimate of the volume target in March 2013).

Based on these observations, we construct a measure of whether or not loan officers at a

given lender are likely to be on track to meet their performance targets. The measure relates the

9

The month-end increase in originations is also robust across applicant characteristics. Table A.1 in the Ap-

pendix estimates equation (6) separately for different sub-samples: white applicants, Black applicants, and other

applicants, as well as white and Black samples sorted into income quartiles. New origination volume increases sub-

stantially at the end of the month for all applicant sub-groups.

20

current month’s origination volume relative to prior year’s:

RelP erf

i,ym

=

AvgV ol

i,ym

AvgV ol

i,ym

0

(7)

where AvgV ol

i,ym

is the average daily volume of mortgage loans that have been issued by lending

institution i and in year and month ym, excluding the last 7 days of the month. The denominator

is the average daily volume of mortgage loans issued by the same lending institution in month

ym

0

, exactly one year before ym. We conjecture that the denominator of equation (7) proxies

for the volume target for institution i, which is based on the performance in the same month of

the previous year. We expect loan officers to be behind their volume targets when the value of

RelP erf

i,ym

is small. Loan officers that are behind their volume targets would be motivated to

increase their lending at the end of the month.

Indeed, origination volume at the end of the month increases by a larger amount when loan

officers are more likely to miss their quotas. Figure 4(a) shows origination volume around the end

of the month. The figure splits the sample into lenders that have values of RelP erf

i,ym

in the top

quartile of lenders in a given month and lenders with values of RelP erf

i,ym

in the bottom quartile.

The month-end increase in originations is substantially larger when RelP erf

i,ym

is in the bottom

quartile. This provides evidence that loan officers increase the pace of new originations at the

end of the month in order to meet their performance targets, and suggests that the end-of-month

increase in origination volume is caused by loan officers’ monthly volume quotas.

10

4.2.4 Alternative Explanation for the End-of-Month Bunching

Though we attribute the increase in new originations at the end of the month to loan officers’

monthly volume quotas, we consider alternative explanations. The leading alternative explana-

tion is that consumer lending regulations incentivize lenders to increase origination volume at the

end of the month. Lenders have incentive to “window-dress” prior to regulatory examinations by

increasing originations of certain types of loans.

10

Figure 4(b) replicates these findings using approval rates rather than origination volume.

21

We test the “window-dressing” explanation by exploring how origination volume changes

when lenders are subject to examinations conducted under the Community Reinvestment Act

(CRA). CRA exams are conducted every two years for large banks and every five years for small

and medium size lenders. Lenders know in advance the exam dates. CRA exams consist of a re-

view of the lender’s fair lending practices, designed to ensure that lenders meet the credit needs of

disadvantaged communities in markets that they serve. The primary alternative explanation for the

month-end effect would be that lenders increase originations to disadvantaged neighborhoods in an

effort to meet the requirements of upcoming CRA examinations. Indeed, prior research shows that

the CRA encourages high-risk lending (see e.g., Bhutta, 2011; Agarwal et al., 2012; Akey et al.,

2020).

We test whether the increase in new originations at the end of the month is caused by upcom-

ing CRA examinations. We sort lenders by whether or not they have a CRA exam scheduled in the

following month. Then, separately for the two samples, we estimate the specification in equation

(6) where the dependent variable is the logarithm of daily origination volume. Table 2 reports the

regression estimates in columns (5) and (6). We find that the month-end effect occurs regardless of

whether the lenders are subject to CRA examinations. Surprisingly, the end-of-month increase in

lending is smaller for institutions that are subject to CRA exams. Lenders that have (do not have)

CRA exams increase their origination volume by 29% (54%) at the end of the month.

11

4.2.5 Performance Incentives Affect Loan Officers’ Decision-Making

The previous section shows that monthly volume quotas motivate loan officers to increase the

volume of originations at the end of the month. Next, we show that such volume quotas affect

loan officers’ decision-making on individual loan applications. Specifically, we study mortgage

approval and rejection decisions and how they vary over the course of the month. Holding constant

the characteristics of the application, a loan approval (denial) implies that the loan officer was more

11

We also use approval rates to confirm that CRA examinations do not cause the increase in originations at the

end of the month. We expand regression equation (8) to include controls for past and upcoming CRA exams. Our

estimates are reported in Table A.2 in the Appendix. We find that controlling for CRA exams does not significantly

affect the coefficient estimates on the indicator variables for start-of-month and end-of-month loans.

22

(less) favorable toward the applicant. The within-month variation in loan approval decisions gives

us an estimate of loan officers’ subjectivity towards individual loan applications.

Figure 5 shows the average approval rate in the U.S. for mortgage applications processed in

each of the last eight days of the month, and each of the first seven days of the following month.

There is roughly a 15% difference in the approval rates between the start and end of the month.

The approval rate gradually increases from 76% seven days before month-end to more than 86%

on the last day of the month. Then, it drops abruptly at the start of the following month, reaching

a bottom value of 71% on the second day of the month.

We use regression analysis to show that the within-month increase in approval rates is robust

to a rich set of fixed effects for time, seasonality, and supply-side factors. We estimate:

Appr

i,t

= γ

lw

I

last−week

+ γ

fw

I

first−week

+ a

ym

+ a

i

+ a

dow

+ a

holiday

+ u

i,t

(8)

where Appr

i,t

is the approval rate for lender i on day t. a

ym

is a year-month fixed effect, a

i

is a

lender fixed effect, and a

dow

and a

holiday

are day-of-the-week and holiday fixed effects. The coef-

ficients of interest, γ

lw

and γ

fw

, capture abnormal approval rates in the first and last week of the

month, for the same lender in the same month. The specification in equation (8) is strict. If month-

end effects are explained by persistent differences across lenders, or by transitory differences in

each specific month, then estimates of γ

lw

and γ

fw

would be indistinguishable from zero. More-

over, because the dependent variable is the approval rate, if month-end increases in originations

are caused by lagged demand, but not by higher propensity to originate loans, γ

lw

and γ

fw

will not

be different from zero.

Table 3 reports estimates of the coefficients in equation (8). Column (1) reports results

based on approval rates for all processed applications. We find that estimates of γ

lw

and γ

fw

are statistically significant, and show higher approval rates than average in the last week of the

month, and lower approval rates than average in the first week of the month. The difference

γ

lw

− γ

fw

measures the increase in approval rates around month-end, and is equal to 4.5% and

23

highly statistically significant. The other columns sort the data by various applicant characteristics,

namely racial groups, by income quartiles, and by various loan characteristics. We find that the

increase in approval rates is present across all groups, but is particularly pronounced for Black

applicants, for which it is equal to 7.6%. Because the average approval rate for Black applicants

is 63%, our estimates imply a 12% relative decline in approval rates for this group of applicants

when comparing the last and first week of the month.

5 Testing for Lending Discrimination Using High-Frequency Evaluations

This section uses the framework developed in Section 2 to test for discrimination in the mort-

gage lending data. Our approach exploits a change in the propensity for evaluators (in this case,

mortgage loan officers) to rely on their subjective judgment in decision making. In our setting of

mortgage lending, monthly volume quotas compel loan officers to generate more originations near

the end of the month. While loan officers can reject applications at the start of the month based on

their subjective assessments and personal biases, they will be less willing to do so at the end of the

month when they face pressure to meet their volume quotas.

We can then exploit within-month variation—comparing the first to the last week of the

month—in the difference in approval rates between whites and Blacks to conduct the formal dis-

crimination test presented in equation (2). Under the assumption that there is no discrimination,

and that application quality is constant within the month, we should find that the difference in

approval rates between Black and white applicants is constant over the course of the month. How-

ever, we find that Black applicants are relatively more likely to be approved at the end of the month.

These findings point toward taste-based discrimination against Black applicants in mortgage loan

approval decisions.

5.1 Empirical Evidence

We start our analysis by examining the aggregate (U.S.-level) differences in mortgage origination

volume for different groups of applicants around month-end. Figure 6 shows daily origination

24

volume in percentages relative to the first day of the month for whites, Blacks and others. All three

groups experience increased origination volume at the end of the month. However, the magnitude

is substantially larger for Blacks—the number of originations is on average more than 240% larger

on the last day of the month than on the first day of the following month. Even after controlling

for seasonality, the results in Table A.1 show that the average increase in daily originations from

the first week of the month to the last week of the month is 11% larger for Blacks than for whites.

5.2 Testing for lending discrimination

We test for discrimination in mortgage lending by examining within-month differences in approval

rates across races. Our tests use the following regression specification:

Appr

j

= δ

lw,Black

(I

lw

× I

Black

) + δ

fw,Black

(I

fw

× I

Black

) + δ

lw

I

lw

+ δ

fw

I

fw

+ (9)

+ δ

Black

I

Black

+ BX

j

+ a

ym,c

+ a

ym,i

+ a

dow

+ a

holiday

+ u

j,t

where the unit of observation is the individual loan application. The dependent variable Appr

j

equals one if the loan is approved. Independent variables I

fw

and I

lw

equal one when the appli-

cation decision is made in the first or the last week of the month, respectively. I

Black

is equal to

one for Black applicants. X

j

is a vector that contains characteristics for mortgage application j

and the corresponding applicant: loan amount, conforming loan status, loan type (conventional, or

government guaranteed or insured, such as FHA, VA, and USDA loans), occupancy type (owner

occupied or absentee), loan purpose (new purchase or refinancing), and applicant income. Year-

month-county, year-month-lender, day of the week, and holiday fixed effects are a

ym,c

, a

ym,i

, a

dow

,

and a

holiday

, respectively. The coefficients of interest, δ

lw,Black

and δ

fw,Black

, capture the abnormal

approval rate for Black applicants in the last and first week of the month.

We begin the regression analysis by reporting split-sample tests of Black and white applicants

that compare approval rates at the start of the month to those at the end of the month (Table 4).

We find that approval rates for Black applicants are 12 percentage points larger in the last week of

25

the month relative to the first week (column 1). Approval rates for white (and other) applicants are

8 percentage points larger in the last week (column 2). Comparing these results, Black applicants

gain an additional 4 percentage point increase in approval rates over the course of the month relative

to white applicants.

Next, we use the entire sample of HMDA data to test the regression model in equation (9)

that contains the complete set of interaction terms between Black applicants and applicants of

other races (Table 4, columns 3 through 6). Because we find that the estimates are robust across

specifications, we describe the most restrictive specification: column (6). The point estimate of

δ

lw,Black

, the abnormal approval rate for Black applicants in the last week of the month, is equal

to 2.7 ppt. The estimate of δ

fw,Black

, the abnormal approval rate in the first week of the month,

is equal to -0.7 ppt. This implies that the relative likelihood of approval for Black applications

increases by 3.4 ppt if the application is processed in the last seven days of the month.

The estimates of the within-month difference in approval rates for Black applicants are large.

For context, we estimate a baseline 6.8 ppt difference in approval rates between Black applicants

and applicants of other races (the coefficient estimate on I

Black

). This estimate is equivalent to what

a conventional benchmarking test would estimate as the amount of discrimination against Black

applicants. However, a conventional benchmarking test is unable to determine whether the 6.8

ppt difference is caused by racial biases or whether it reflects the unobserved heterogeneity across

races. On the other hand, because our empirical design suppresses the cross-sectional variation

across applicants’ races, we can confidently attribute the within-month approval gap of 3.4 ppt to

loan officers’ subjectivity. As such, the ratio of the within-month difference to the unconditional

difference—3.4 divided by 6.8, or 50%—approximates the share of the observed racial gap in

approval rates that can be attributed to subjective decision-making. In other words, we attribute at

least half of the racial gap in approval rates to racial bias.

Our finding that the approval gap for Black applicants is reduced at the end of the month is

highly robust (see Appendix Table A.3 for the following robustness tests). The estimates are not

much changed across different types of mortgage applications – new home purchases, conforming

26

mortgages, and refinances. Controlling for the applicant’s gender and including Black-year fixed

effects also do not affect the estimates. Lastly, the results are robust to replacing calendar month

fixed effects with fixed effects that span the end and start of successive calendar months (e.g.,

January 15 to February 14).

These regression tests confirm the graphical evidence that the approval gap between Black

and other applicants converges over the course of the month (presented in Figure 2 and described in

the Introduction). We augment this aggregate evidence by plotting how the approval gap changes

over the course of the month estimated from the saturated regression model in Table 4, column (6).

Figure 7(b) plots the average day-by-day residual difference in approval rates after controlling for

application characteristics. The approval gap in the first seven days of the month is approximately

equal to 7 ppt. The approval gap during the last seven days of the month shrinks to approximately

1 ppt on the last day of the month. Therefore, after controlling for loan characteristics, there is

almost no difference in application approval rates across races on the last day of any given month.

The regressions in Table 4 also convey insight into how differences across lending institu-

tions affect mortgage credit for Black applicants. Notably, the literature has argued that much of

the difference in approval rates between Black and white applicants can be attributed to different

lending institutions catering to different types of borrowers and that different applicants choose to

apply for mortgages at certain types of institutions. We gain insight into the role of selection across

institutions by examining how including lender fixed effects affects the regression estimates. In-

cluding lender fixed effects reduces the magnitude of the un-interacted coefficient on I

Black

from

-0.10 in column (2) to -0.07 in column (3). This result implies that lender fixed effects are a cru-

cial source of unobservable variation driving the Black-white approval gap. On the other hand,

lender fixed effects have a negligible effect on the within-month approval gap. The difference in

approval gaps between the start and end of the month is 0.040 without and 0.035 with lender fixed

effects. These results suggest that we capture a component of loan officer decision-making that

exists within lenders and is consistent across institutions. These results are reassuring for our em-

27

pirical design and the interpretation of the findings, because loan officer compensation schemes do

not vary much across lending institutions.

We also provide evidence that the within-month reduction in approval gap for Black appli-

cants can be linked to the inventory of loan applications that lenders have in their queue. Figure

8(a) plots the share of all approved applications on a given day submitted by Black applicants. On

the first day of the month, Black applicants account for approximately 4.4% of approved loans. In

the last week of the month, the share increases steadily, reaching just over 6% on the last day of

the month.

Furthermore, we study whether the within-month convergence in approval gap is sensitive

to the share of Black applicants that a lender processes. Figure 8(b) shows that the within-month

change in approvals occurs across the full range of lenders. The figure reports the median share

of approved loans from Black applicants, along with the 25th and 75th percentile, across lenders

that issued at least 10 loans per day on average over the year. The median share is close to 5.5%

in the first two weeks of the month. However, it steadily increases in the last week of the month.

The shift involves the entire distribution. On the last day of the month, the median share is above

6%, the 25th percentile is approximately 4% and the 75th percentile is close to 10%. On the first

day of the month, the median is below 5.5%, the 75th percentile shrinks close to 9% and the 25th

percentile falls below 3.5%.

5.3 Alternative Explanations

The evidence that the approval gap for Black applicants declines at the end of the month is consis-

tent with loan officers having less scope for subjective decision-making when they have monthly

volume quotas, as shown by the framework outlined in Section 2. Yet, we consider plausible al-

ternative explanations, other than taste-based discrimination, for the change in approval rates over

the course of the month.

Before considering specific alternative explanations, we describe how the empirical design

limits the scope for alternative theories. First, it is unlikely that the within-month variation in ap-

28

proval rates can be explained by variation across lenders, because the estimates are hardly changed

by the inclusion of lender fixed effects.

Second, our empirical strategy rules out the possibility of unobserved differences across

applicant groups. Therefore, any candidate alternative explanation has to have within-month vari-

ation and also has to have differential effects on Black applicants relative to other applicants. Not

only does this confine alternative explanations to factors that vary within the month, it gives us

an avenue to test alternative theories. In particular, suppose that the indicator variable for Black

applicants reflects other unobserved characteristics, such as the riskiness of the loan, and that loan

officers delay processing high-risk applications. If application risk explains the convergence in

approval rates across races over the course of the month, then the observed riskiness of the loan

application would explain within-month changes in approval rates. Put simply, we would expect

to find that originations of observably high-risk applications submitted by Black applicants would

bunch at the end of the month, whereas low-risk applications would be relatively more evenly

distributed throughout the month.

Guided by these bounds on alternative theories, we take a holistic approach to confronting

alternative explanations by examining the within-month quantity of loan originations sorted by

credit scores (and applicant incomes). We study credit scores because they are possibly the most

important ingredient in loan approval decisions and mortgage pricing. They would also corre-

late with the most plausible alternative explanations: they directly measure the ex-ante risk of the

application, and low credit score applicants would be more likely to file low-documentation ap-

plications. As section 3 describes, the data only contains credit scores for applications that are

approved. As such, we study the quantity of new originations over the course of the month instead

of approval rates. However, such tests would be nearly equivalent to testing approval rates because

we have shown that mortgage demand does not vary within the month.

We find that alternative explanations related to application quality are unlikely to explain the

within-month approval gap. Figures 9(a) and 10(a) plot the quantity of new originations sorted by

credit scores and incomes for applications submitted by Blacks and whites, respectively. Strikingly,

29

the volume of originations for prime-credit-score (FICO ≥ 660) and subprime (FICO < 660) Black

applicants are nearly identical over the course of the month (Figure 9(a)). We would have expected

to find relatively more end-of-month bunching for subprime Black applicants if the results simply

reflected characteristics—such as risk—that correlate with applicants’ credit scores. Also, the end-

of-month bunching of originations is larger for Blacks than whites for both prime and subprime

applicants (comparing the levels in Figure 9(a) to those in Figure 10(a)). The difference between

Black and white originations would have been attenuated for prime applicants if characteristics

related to credit scores explained the within-month approval gap.

We find similar evidence when we sort the volume of new originations into quartiles by appli-

cant incomes (Figure 9(b) and Figure 10(b)). Testing for end-of-month bunching across applicant

incomes not only fortifies evidence from sorting by credit scores but also allows us to present ev-

idence from the full HMDA sample. We find that there is substantial end-of-month bunching for

all four income quartiles. Moreover, in each corresponding quartile, the end-of-month bunching

for Black applicants is significantly larger than for white applicants. These findings cast doubt on

alternative explanations related to within-month variation in application quality.

We provide additional evidence that racial differences in approval rates over the course of