CONS UMER FINANCIAL PROTECTION BUREAU | MAY 2021

Manufactured Housing

Finance: New Insights from

the Home Mortgage

Disclosure Act Data

Consumer Financial Protection Bureau’s Offices of Research

and Mortgage Markets

1 CONSUMER FINANCIAL PROTECTION BUREAU

This is another in an occasional series of publications from the Consumer Financial Protection

Bureau’s (CFPB) Office of Research, in collaboration with the Office of Mortgage Markets. These

publications are intended to further the CFPB’s objective of providing an evidence-based

perspective on consumer financial markets, consumer behavior, and regulations to inform the

public discourse. See 12 U.S.C. §5493(d).

1

1

This Data Point was prepared by Jessica Russell, Nora O’Reilly, Karl Schneider, Nicolas Melton, Nick Schwartz, and

Sam Leitner.

2 CONSUMER FINANCIAL PROTECTION BUREAU

Table of contents

Table of contents ..............................................................................................................2

2. Introduction & Key Findings ....................................................................................3

3. Background and Data ...............................................................................................7

3.1 Manufactured housing............................................................................... 7

3.2 Data ........................................................................................................... 11

4. Sales and Financing ................................................................................................15

4.1 Applications and originations ..................................................................15

4.2 Geography of manufactured housing lending ........................................ 18

4.3 Loan characteristics of manufactured housing loans..............................21

4.4 HOEPA ..................................................................................................... 25

5. Borrowers and Lenders ..........................................................................................30

5.1 Borrower demographics .......................................................................... 30

5.2 Borrower creditworthiness: chattel and mortgage................................. 33

5.3 Owned vs. Leased Land ........................................................................... 33

5.4 Manufactured housing lenders ............................................................... 43

6. Conclusion and Future Research .........................................................................48

Appendix: Comparison of HMDA to Other MH Data Sources .................................50

3 CONSUMER FINANCIAL PROTECTION BUREAU

2. Introduction & Key Findings

Manufactured housing (MH) accounts for about six percent of occupied housing stock in the

U.S. and is the largest source of unsubsidized affordable housing in the country. Unlike

traditional site-built homes, manufactured homes are built in a factory according to national

standards and then transported to the site of use. They can be placed on land that is owned or

leased by the homeowner. Whether the homeowner owns the underlying land plays a key role in

whether the manufactured home is titled as personal (chattel) property or real property, a

distinction which in turn affects many aspects of the home financing and can have major

implications for the homeowner in terms of cost and security of tenure.

The CFPB is interested in manufactured housing because of its status as an important source of

low-income housing, because its consumers are often financially vulnerable, and because of the

unique consumer protection concerns its financing market raises. The CFPB’s 2014 report on

manufactured housing found that manufactured-home owners tend to live in rural areas, to be

older, and to have lower incomes and net worth than site-built homeowners. In terms of race

and ethnicity, the analysis found that Black and African American and Asian borrowers are

under-represented in manufactured housing relative to site-built, whereas Hispanic whites,

non-Hispanic whites, and American Indian and Alaska Native borrowers are overrepresented.

While manufactured homes typically cost less than site-built homes, manufactured-home

owners typically pay higher interest rates than site-built homeowners and have fewer consumer

protections.

2

This Data Point article provides insights into manufactured housing finance using Home

Mortgage Disclosure Act (HMDA) data, which have loan-level information on a variety of

pricing, underwriting, and applicant characteristics as reported by financial institutions.

3

Many

of the analyses in this report are made possible by the new and revised fields that are available

in HMDA data beginning in 2018, including two fields that are specific to manufactured housing

and provide insight about landownership and chattel lending.

This report uses the new HMDA data to explore the differences between mortgage loans for site-

built homes, mortgage loans for manufactured homes (hereafter referred to as “MH

2

“Manufactured-housing consumer finance in the Uni ted States.” CFPB. September 2014 (2014 CFPB Report).

https://files.consumerfinance.gov/f/201409_cfpb_report_manufactured-housing.pdf

3

For more information on HMDA data see http://www.consumerfinance.gov/data-research/hmda/. To see if a

specific loan or an institution has to report under HMDA, see

https://www.consumerfinance.gov/documents/7052/HMDA_Data_Disclosure_Policy_Guidance.Executive_Sum

mary.FINAL.12212018.pdf.

4 CONSUMER FINANCIAL PROTECTION BUREAU

mortgages”), and chattel loans for manufactured homes. Chattel loans are loans for

manufactured housing that are secured solely by the manufactured home and not land, while

MH mortgage loans are secured by the manufactured home and land.

4

Most of the analyses

focus on home purchases rather than refinances, given the paucity of MH refinancing lending.

Findings include:

• The majority of applications for manufactured housing loans do not result

in an origination. Only 27 percent of manufactured home loan applications resulted in

the loan being financed, compared to 74 percent of applications for site-built homes.

These differences remain even after controlling for credit score. Applications for

manufactured homes were more likely to be denied and also more likely to be incomplete

than applications for site-built homes, and rates of denial and incompletion were higher

still for chattel loan applications.

• Although mortgage interest rates fell in 2019, less than four percent of

chattel originations were for refinances, whereas about 31 percent of MH

mortgage and 44 percent of site-built mortgages were for standard or cash-out

refinancing. While smaller loans are less likely to benefit from refinancing because the

savings from a lower interest rate may not offset the costs of origination, more research

is needed to understand whether more MH consumers could benefit from refinancing.

• Manufactured housing lenders appear to have adjusted their pricing in

response to changes to the implementation of the Home Ownership and

Equity Protection Act (HOEPA) rule in 2014. After the new rule went into effect in

2014, a significant number of manufactured housing loans were priced just below the

HOEPA thresholds, suggesting that the market was sensitive to the new threshold and

priced loans accordingly. These changes in pricing have continued and can be seen in the

2019 data. Meanwhile, loan volume and origination rates increased in the years

following the rule change.

• Around 42 percent of manufactured housing loans are chattel loans, which

are loans secured by the home but not the land. While this estimate is lower than

estimates from other data sources, underlying differences between datasets help explain

the disparities.

4

See Paragraph 4(a)(29) within https://www.consumerfinance.gov/policy-

compliance/rulemaking/regulations/1003/4/#a-28.

5 CONSUMER FINANCIAL PROTECTION BUREAU

• Over 60 percent of manufactured housing borrowers directly own the land

where their home is located, meaning they may be eligible for a MH

mortgage. However, 17 percent of these borrowers take out a chattel loan.

The 2014 CFPB report had estimated that 65 percent of landowners get chattel financing

based on a proxy for financing type in the American Housing Survey (AHS). The CFPB

has concluded that this proxy was imperfect and therefore the statistic from the 2014

report is not valid.

• Hispanic, Black and African American, American Indian and Alaska Native,

and elderly borrowers are more likely than other consumers to take out

chattel loans, even after controlling for land ownership. Determining the reasons for

these differences is a vital area of future research. Black and African American borrowers

are the only racial group that are underrepresented in manufactured housing lending

overall compared to site-built, but overrepresented in chattel lending compared to site-

built.

• Landowners face tradeoffs between chattel loans and MH mortgages, and

this report analyzes to what extent some of these tradeoffs can be measured using the

HMDA data. Chattel loans are often considered to have lower upfront costs and shorter

closing times, but this analysis concludes that closing times are in fact similar, though it

cannot draw conclusions about upfront costs. Additionally, landowners who opt for

chattel loans have somewhat stronger credit characteristics—similar median credits

scores and incomes and better loan-to-value and debt-to-income ratios—than

landowners who get mortgages, which suggests that chattel borrowers’ credit profiles

would not have prevented them from getting a mortgage. However, borrowers may

encounter difficulty getting mortgages with small loan amounts. Other reasons for

getting chattel loans include not wanting to encumber the land, lowering their property

taxes, being influenced by the fact that manufactured housing is personal property by

default in many states, being unaware of the downsides of chattel loans or potentially

being steered to a chattel loan by a lender, dealer or retailer.

• The market for MH lending—and chattel in particular—is more

concentrated than the market for mortgages on site-built homes. The top five

lenders made more than 40 percent of home purchase manufactured housing loans,

including nearly 75 percent of chattel loans and 18 percent of MH mortgages. The four

largest MH originators are specialty lenders that cater to MH consumers and offer

primarily chattel loans. Many of the remaining top 15 lenders are banks and nonbanks

that only offer mortgages and for whom MH loans are a small share of their business. In

the past decade, nonbank lenders have played an increasing role in the manufactured

6 CONSUMER FINANCIAL PROTECTION BUREAU

housing lending market, while banks have decreased their activity or exited the market

altogether.

• Texas is often in the focal point of manufactured housing research because

of the comparatively rich data available on MH, it has a significantly higher

proportion of chattel lending than the U.S. as a whole. Manufactured housing

density varies between states, with rural and southern areas often having higher

concentrations of manufactured housing. Texas has a high volume of manufactured

housing and a high percentage of manufactured housing loans that are chattel. Texas has

been studied using detailed public data available in Texas Manufactured Home

Ownership records, but the Texas manufactured housing environment is likely not

representative of national trends, particularly in financing. Additionally, the Texas

homeownership records are often missing lien information for homes titled as real

property, which leads to undercounting MH mortgages.

7 CONSUMER FINANCIAL PROTECTION BUREAU

3. Background and Data

3.1 Manufactured housing

Manufactured homes are factory-built housing constructed after June 15, 1976 in accordance

with the U.S. Department of Housing and Urban Development’s Manufactured Home

Construction and Safety Standards code (HUD Code). Manufactured homes are at least 320

square feet and are built on a permanent chassis before being transported to a site for

placement. Homes that fit these criteria are marked with a HUD label that signals compliance

with HUD codes.

Manufactured homes are distinct from RVs and park-model homes, which are generally treated

as motor vehicles, not housing. They are also different from modular homes. Modular home

sections are built in a factory, like manufactured homes, but they must comply with the same

regional, state, or local codes as traditional site-built homes, while manufactured homes must

comply with the national HUD Code. Lastly, manufactured homes are not the same as mobile

homes or trailers, even though the terms are sometimes used interchangeably. Mobile homes

and trailers refer to factory-built housing constructed before June 15, 1976 and do not meet the

HUD standards for manufactured housing.

5

Throughout the paper, we refer to manufactured

housing and manufactured homes synonymously.

There are approximately 6.7 million occupied manufactured homes in the U.S., accounting for

approximately six percent of U.S. housing stock.

6

This rate varies by region and housing density,

with manufactured housing making up 13 percent of all occupied homes in rural and small town

communities.

7

Over half of manufactured homes are located in the South.

8

Over 70 percent of

5

For more information about what constitutes manufactured housing, see

https://www.hud.gov/program_offices/housing/rmra/mhs/faqs.

6

American Community Survey, 2019 5- Year Estimates.

https://data.census.gov/cedsci/table?q=ACSDT1Y2019.B25024&tid=ACSDT5Y2019.B25024&hidePreview=tr ue

7

The Housing Assistance Council defines rural areas as Census tracts with fewer than 16 housing units per square

mile and small towns as Census tracts with 16 -64 housing units per square mile and a low degree of commuting to a

metropolitan core area. See additional methodology here:

http://www.ruralhome.org/storage/documents/policy_comments/dts/TECHNICAL_DOCUMENTATION_HAC_

Rural__Small_Town_Definition.pdf. For a map of manufactured housing by county, see the Housing Assistance

Council’s July 2020 Rural Research Brief

http://www.ruralhome.org/storage/documents/rrbriefs/Manufactured_Housing_RRB.pdf.

8

American Community Survey, 2019 5-Year Estimates.

https://data.census.gov/cedsci/table?q=ACSDT1Y2019.B25032&t=Housing&g=0100000US_0200000US3&tid=A

CSDT1Y2019.B25032&moe=false&hidePreview=true

8 CONSUMER FINANCIAL PROTECTION BUREAU

occupied manufactured homes are owner-occupied, and this report focuses on manufactured

homeowners rather than home-renters.

9

However, this report includes both homeowners who

own the land their home is located on and homeowners who rent the underlying land. An

estimated 17.5 million Americans live in manufactured homes.

10

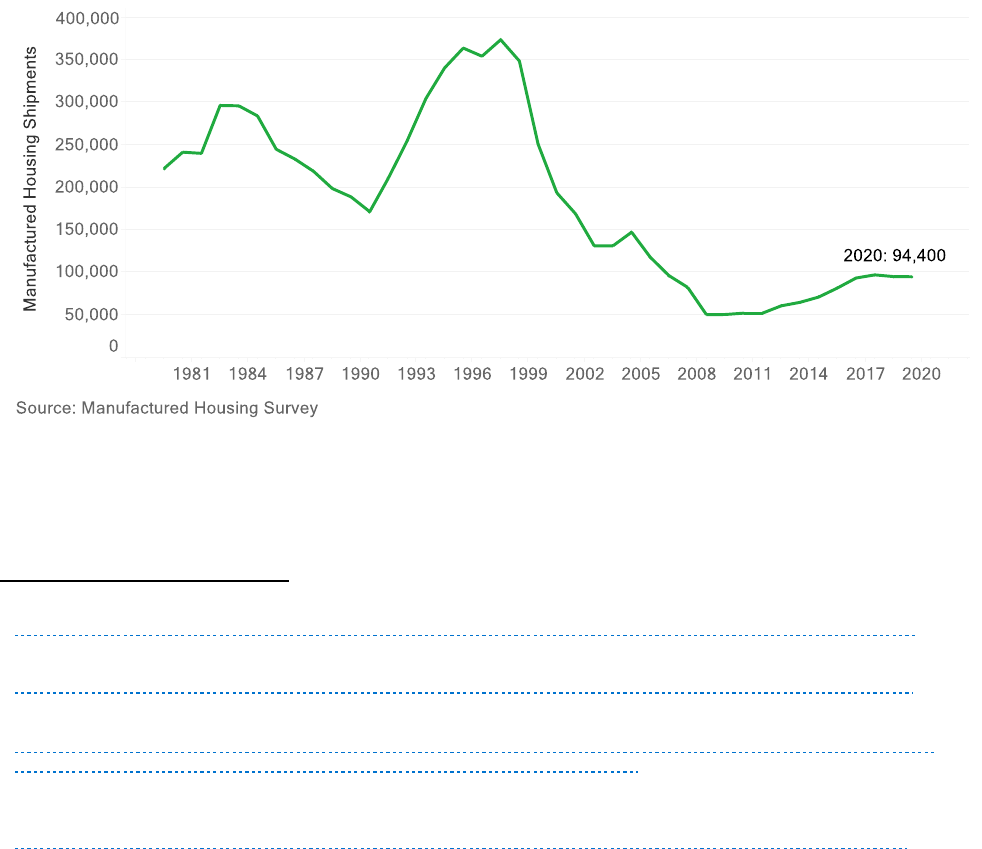

In 2020, approximately 94,000

new manufactured homes were shipped nationally which represents an increase from a low of

50,000 in 2009.

11

Shown below in Figure 1, the manufactured housing market experienced rapid

growth during the 1990s, peaking at over 370,000 units shipped in 1998, but crashed in the

early 2000s followed by further depression during the Great Recession and a modest recovery.

Manufactured housing borrowers have had a harder time making housing payments during the

coronavirus pandemic in 2020 than their site-built counterparts.

12

FIGURE 1: MANUFACTURED HOUSING SHIPMENTS 1980-2020

Although manufactured homes account for a small share of all housing, the manufactured

housing is an important source of low-income housing. Manufactured housing is the largest

9

American Community Survey, 2019 5-Year Estimates.

https://data.census.gov/cedsci/table?q=ACSDT1Y2019.B25032&tid=ACSDT5Y2019.B25032&hidePreview=true

10

American Community Survey, 2019 5-Year Estimates.

https://data.census.gov/cedsci/table?q=ACSDT1Y2019.B25033&tid=ACSDT5Y2019.B25033&hidePreview=true

11

Manufactured Housing Survey, 2019.

https://www.census.gov/econ/currentdata/dbsearch?program=MHS2&startYear=2014&endYear=2020&categorie

s=T&dataType=SH&geoLevel=US&adjusted=0¬Adjusted=1&errorData=0

12

For more information about the housing impacts of the COVID-19 pandemic, see the CFPB’s Housing Insecurity

and the COVID-19 pandemic report:

https://files.consumerfinance.gov/f/documents/cfpb_Housing_insecurity_and_the_COVID-19_pandemic.pdf.

9 CONSUMER FINANCIAL PROTECTION BUREAU

source of unsubsidized affordable housing in the country.

13

A report from HUD found

manufactured housing to be a low-cost housing alternative and “good value” for low income

households.

14

More recently, a study from the Urban Institute showed that manufactured

housing is less expensive per square foot than either existing site-built homes or new site-built

homes.

15

Despite being 35 to 47 percent less expensive per square foot than new or existing site-

built homes, the number of new manufactured homes shipped each year is down significantly

from the late 1990s, as mentioned in the previous paragraph. Authors of the same study argued

that restrictive zoning, restrictive or unavailable financing, and lower appreciation than that for

site-built housing are the main reasons why manufactured housing production has remained

low.

Manufactured homes are placed on either land owned by the manufactured-home owner, on

land owned by someone else without rent, or on rented land, including on leased lots within

manufactured home communities. Once placed, manufactured homes are typically not moved

from their original site. Typically, the land in a manufactured housing community is owned by a

landlord, but in a small number of communities, the land is owned by a cooperative of

homeowners as a resident-owned community (ROC).

16

The financing of manufactured housing raises unique consumer protection concerns. Whether

borrowers own the land on which their manufactured housing is located plays a key role in

whether the manufactured home is titled as personal (chattel) property or real property, a

distinction which in turn affects the type and pricing of the loan that the homeowner is able to

receive.

17

The difference in title type is important for the homebuyer since financing costs are

higher and consumer protections are weaker for manufactured homes titled as personal

property than for homes titled as real property.

18

Specifically, chattel loans are not covered by

either the Real Estate Settlement Procedures Act (RESPA) or the Coronavirus Aid, Relief, and

13

“Factory-Built Housing for Affordability, Efficiency, and Resilience .” HUD. Winter/Spring 2020.

https://www.huduser.gov/portal/periodicals/em/WinterSpring20/highlight1.html

14

Boehm and Schlottmann. “Is Manufactured Housing a Good Alternative for Low-Income Families?” U.S.

Department of Housing and Urban Development. December 2004.

https://www.huduser.gov/publications/pdf/ismanufacturedhousingagoodalternativeforlow-

incomefamiliesevidencefromtheamericanhousingsurvey.pdf

15

Goodman, Golding, McCargo, and Ganesh. “Manufactured homes could e ase the affordable housing crisis. So why

are so few being made?” Ubran.org. Urban Institute. 29 January 2018. https://www.urban.org/urban-

wire/manufactured-homes-could-ease-affordable-housing-crisis-so-why-are-so-few-being-made

16

For more information about ROCs, see https://rocusa.org/whats-a-roc/what-is-a-roc-how-is-it-different/.

17

Goodman and Ganesh, “Four ways financing differs for manufactured homes,” 27 July 2018.

https://www.urban.org/urban-wire/four-ways-financing-differs-manufactured-homes

18

Goodman and Ganesh, “Challenges to Obtaining Manufactured Home Financing ,” 27 June 2018.

https://www.urban.org/research/publication/challenges-obtaining-manufactured-home-financing

10 CONSUMER FINANCIAL PROTECTION BUREAU

Economic Security (CARES) Act. In the case of default, manufactured housing mortgages are

eligible for the same foreclosure protections as traditional site-built homes, whereas chattel

properties are not protected and instead go through repossession, a process with less consumer

protections and less opportunity for the borrower to remain in the home, depending on the state

and local protections.

19

Many chattel homeowners pay rent for the land their home is located on,

and therefore are vulnerable to both repossession by the lender and rent-hikes or eviction by the

owner of the land.

20

This report reviews differences in borrower characteristics and pricing for

chattel and MH mortgage loans and outlines some of the advantages and disadvantages of each

type of financing.

Whether the homeowner owns the land also affects the home’s appreciation. Previous studies

provide some evidence that manufactured homes can appreciate just as much as site-built

homes if the consumer owns the land, though there is more volatility in appreciation for

manufactured homes.

21

However, manufactured housing where the consumer does not own the

land generally does not promote wealth-building via homeownership.

22

The 2014 CFPB Report on manufactured housing finance offered many insights into the history

and state of the manufactured housing market and regulatory environment in 2014, and into

manufactured housing consumers. The report explored the reasons for the manufactured

housing market collapse in the early 2000s and the subsequent depressed inventory and

contraction of the secondary market. The CFPB found that, though manufactured homes

typically cost less than site-built homes, manufactured-home owners typically pay higher

interest rates than site-built homeowners. The CFPB also found that manufactured-home

owners tend to live in rural areas, to be older, and to have lower incomes and net worth than

site-built homeowners. In terms of race and ethnicity, the analysis found that Black and African

19

For example, for more information on the legal landscape of manufactured housing personal property

repossessions, see section 1.4.12 “Special Issues in Manufactured Home Repossessions” of the National Consumer

Law Center’s (NCLC) treatise Repossessions: https://library.nclc.org/repo/010412-0.

20

For example, see discussion in Sheelah Kolhatkar’s “What happens when investment firms acquire trailer parks?”

from March 2021. https://www.newyorker.com/magazine/2021/03/15/what-happens-when-investment-firms-

acquire-trailer-parks

21

Boehm and Schlottmann, “Is Manufactured Housing a Good Alternative for Low-Income Families?” U.S.

Department of Housing and Urban Development. December 2004.

https://www.huduser.gov/publications/pdf/ismanufacturedhousingagoodalternativeforlow-

incomefamiliesevidencefromtheamericanhousingsurvey.pdf ; Goodman, Golding, Bai, and Strochak, “New evidence

shows manufactured homes appreciate as well as site-built homes,” 13 September 2018.

https://www.urban.org/urban-wire/new-evidence-shows-manufactured-homes-appreciate-well-site-built-homes

22

Boehm and Schlottmann conclude that generally, “manufactured housing where the lot is not owned with the unit

is not an investment in any sense.” Boehm and Schlottmann, “Is Manufactured Housing a Good Alternative for

Low-Income Families?” December 2004.

https://www.huduser.gov/publications/pdf/ismanufacturedhousingagoodalternativeforlow-

incomefamiliesevidencefromtheamericanhousingsurvey.pdf

11 CONSUMER FINANCIAL PROTECTION BUREAU

American and Asian residents are under-represented in manufactured housing relative to site-

built, whereas Hispanic whites, non-Hispanic whites, and American Indian and Alaska Native

residents are overrepresented. The 2014 report emphasized the potential importance of

manufactured housing as a source of affordable housing and highlighted the difference in legal

treatment of manufactured housing and site-built housing.

3.2 Data

This Data Point makes use of the new data points in HMDA to expand understanding of

manufactured housing along dimensions for which there previously has been no systematic

data, such as the share of borrowers who own their land and take out a chattel loan. The Data

Point employs existing research using the AHS and the Manufactured Housing Survey (MHS)

but does not conduct any original analysis using these two datasets. We compare HMDA to

commonly cited Texas Manufactured Housing Ownership Records (THOR)

23

, but don’t use the

THOR data in our main analyses because the Texas Manufactured Housing Division confirmed

that the records cannot be used to reliably estimate the proportion of manufactured home loans

that are secured by real versus personal property. A detailed discussion of the THOR data and

analyses based on address matches with HMDA are in the Appendix. Additionally, as described

in Section 3.2, MH financing varies by geography and many patterns in Texas are not

representative of the United States as a whole.

Home Mortgage Disclosure Act (HMDA)

24

The Home Mortgage Disclosure Act requires many financial institutions to maintain, report, and

publicly disclose loan-level information about their lending activity for loans secured by a

consumer dwelling. As part of the Dodd-Frank Wall Street Reform and Consumer Protection Act

of 2010 (Dodd-Frank Act), Congress amended HMDA to, among other things, expand the

number of data points required to be collected and reported and give the CFPB authority to

require additional data points to be collected and reported. The CFPB issued a final rule

23

“THOR” is the acronym used throughout the paper for convenience. The Manufactured Housing Division did not

have a specific acronym that it used for the manufactured home ownership records.

24

This report relies primarily on 2019 HMDA data, and the analysis in this report generally relies on medians and

buck eting to mitigate the impact of these outliers on the underlying analyses. The public 2019 HMDA data can be

found here: https://www.consumerfinance.gov/about-us/newsroom/ffiec-announces-availability-2019-data-

mortgage-lending/.

12 CONSUMER FINANCIAL PROTECTION BUREAU

implementing these and other changes in October 2015. Most of the rule’s provisions took effect

on January 1, 2018 and affected data to be collected starting in 2018.

25

Two of the new data points are specific to manufactured housing and provide information about

chattel lending and whether the consumer owns or leases the land.

Some lenders are exempt

from reporting certain HMDA data points, including the manufactured housing data points,

following the amendment to HMDA by the Economic Growth, Regulatory Relief, and Consumer

Protection Act in 2018.

• Manufactured Home Secured Property Type identifies whether a manufactured home

loan is a personal property loan, meaning secured by the manufactured home and not

land (chattel) or secured by the manufactured home and the land (mortgage).

• Manufactured Home Land Property Interest indicates if the land on which a

manufactured housing unit is located is directly owned, indirectly owned, or if the

borrower has an unpaid or paid lease.

o Direct ownership means the borrower owns the land on which the manufactured

housing unit is located.

o Indirect ownership can occur when the borrower is a member of a ROC acting as

a housing cooperative where the members of the community collectively own the

land where the manufactured housing is located.

o Paid leasehold typically indicates the borrower is paying rent for the property.

o Unpaid leasehold indicates the borrower is not making rent payments and

includes loans where the manufactured home is located on land owned by a

family member without a written lease and no agreement to rent payments.

While HMDA provides robust data on manufactured housing loan originations, it has some

limitations. It does not include data on cash sales and thus the conclusions drawn from the data

cannot be applied to the overall manufactured housing market. Additionally, unlike some

datasets related to manufactured housing, HMDA does not distinguish between new and

existing homes, which can be of particular significance for MH borrowers because of the

transportation and setup costs required for new (and some used) home purchases. Lastly,

HMDA data are limited to applications and originations; they do not provide any information

about loan performance or default risk.

25

See Home Mortgage Disclosure (Regulation C), 80 FR 66128 (Oct. 28, 2015).

13 CONSUMER FINANCIAL PROTECTION BUREAU

Reconciling HMDA with Other Sources of MH Data

Table 1 compares the new HMDA data points with results from commonly used manufactured

housing datasets, filtered to make them as comparable as possible to the two new HMDA MH

data points. Each of the datasets is described in more detail in the Appendix.

At first glance, HMDA estimates of chattel properties appear significantly lower than those from

other datasets. However, underlying differences between these datasets can help explain the

disparities. MHS data, for example, are based on shipments of new manufactured homes and

include cash sales, while HMDA data contain both new and used housing and do not capture

cash transactions. While we can’t compare the datasets directly, it seems likely that both provide

reasonable estimates for the populations that they are measuring, especially in light of evidence

that new homes appear far more likely than used homes to be financed with chattel loans.

26

HMDA results appear more similar to results from THOR, even without accounting for the fact

that THOR data undercounts loans secured by real property.

27

For landownership, HMDA

estimates are comparable to those from other datasets.

26

See Figure 22 in the Appendix.

27

About 89 percent of HMDA chattel loans in Texas had a lien recorded in THOR, compared to only 47 percent of

MH mortgages.

14 CONSUMER FINANCIAL PROTECTION BUREAU

TABLE 1: COMPARISON OF MANUFACTURED HOUSING DATA SOURCES

Data Source

Population

% Chattel

National

% Chattel

Texas

% Land

Ownership

HMDA, 2019

• 2019 originations

• New and used homes

• Home purchase financed

42%

66%

64%

AHS, 2019

• Homes owned in 2019 but financed

at any point in time

• New and used homes

• Home purchase financed

--

--

73%

MHS, 2019

• Units shipped and placed in 2019

• New homes

• Financed and cash sales

76%

--

--

THOR, 2019

• 2019 changes in ownership

• New and used homes

• Home purchase financed

--

78%

28

--

UNC/Freddie Mac’s

MH Survey and

Report on Loan

Shopping Experiences

• Data is based on survey responses,

sample for survey is based on THOR

• 2015-2018 purchases

• New and used homes

• Home purchase financed

--

73%

61%

(TX only)

28

In THOR, some manufactured homes that were financed do not have a lien, a limitation of the dataset explained in

further detail in the Appendix. Because of this, the “financed” population based of the presence of a lien does not

accurately represent those who finance manufactured housing in Texas.

15 CONSUMER FINANCIAL PROTECTION BUREAU

4. Sales and Financing

This section focuses on trends in sales and characteristics of financing for manufactured housing

loans. Analyses address patterns in loan applications and originations and then delve into the

characteristics, pricing, and affordability of manufactured housing loans. This section also

includes an analysis of the impact of HOEPA on the sales and financing of manufactured

housing.

With the exception of some analyses of refinancing rates in Section 3.1, the rest of this analysis

in this report focuses on manufactured housing home purchase loans. It only includes 1-4

family, owner-occupied, first-lien properties and it excludes open-end lines of credit, loan

purchases between financial institutions, and loans designated primarily for a business or

commercial purpose.

29

The report is accompanied by a set of Excel tables with the data for all

the charts and tables found in this report, to facilitate accessibility and further research.

4.1 Applications and originations

Financial institutions reported approximately 420,000 applications for home purchase loans for

manufactured homes, which is about eight percent of all home purchase applications in the 2019

HMDA data.

30

Figure 2 shows that a minority (27 percent) of consumers who applied for a loan to buy a

manufactured home succeeded in obtaining financing. Of those who did not obtain financing,

the majority were denied and a smaller share either did not complete their application or turned

down financing. An estimated 42 percent of all manufactured housing home purchase

applications were denied, including 50 percent of chattel applications and 33 percent of

mortgage applications. In comparison, only 7 percent of site-built applications were denied.

29

To designate this population in the HMDA data, the following codes were used: “Total Units” equal to 1,2,3 or 4,

“Occupancy Type” equal to 1, “Lien Status” equal to 1, “Open-End Line of Credit” not equal to 1, “Action Taken” not

equal to 6, and “Business or Commercial Purpose” not equal to 1.

30

Adding the chattel and MH mortgage applications does not equal total manufactured housing applications—there

are also applications that are either exempt or NA for the manufactured home secured property type field.

Throughout the report, these records are dropped from the dataset when the analysis breaks out chattel and MH

mortgage designations, but are included in the analyses pertaining to total manufactured housing.

16 CONSUMER FINANCIAL PROTECTION BUREAU

FIGURE 2: ACTION TYPE BY SECURED PROPERTY TYPE

31

The same pattern holds after controlling for credit score (Figure 3). While approval rates were

higher for consumers with better credit scores, even in the super-prime bucket with credit scores

above 720, chattel (63 percent) and MH mortgage (80 percent) approval rates lag behind site-

built mortgages (95 percent). Sub-prime consumers who applied for financing on a site-built

home were more likely to be approved for a loan than super-prime consumers with chattel

applications or prime consumers with MH mortgage applications. Lenders have reported that

borrowers may not know which lenders offer chattel loans and, therefore, apply for chattel loans

from lenders that do not offer them, which leads to higher denial rates.

31

This analysis excludes preapprovals, which make up less than one percent of manufactured housing applications.

Percentages may not sum to 100 percent due to rounding. Manufactured housing chattel applications that were

withdrawn by the applicant, site-built applications that were approved but not accepted, and site-built application

files that were closed for incompleteness each made up less than three percent of their respective categories.

17 CONSUMER FINANCIAL PROTECTION BUREAU

FIGURE 3: APPROVAL RATE BY SECURED PROPERTY TYPE AND CREDIT SCORE

32

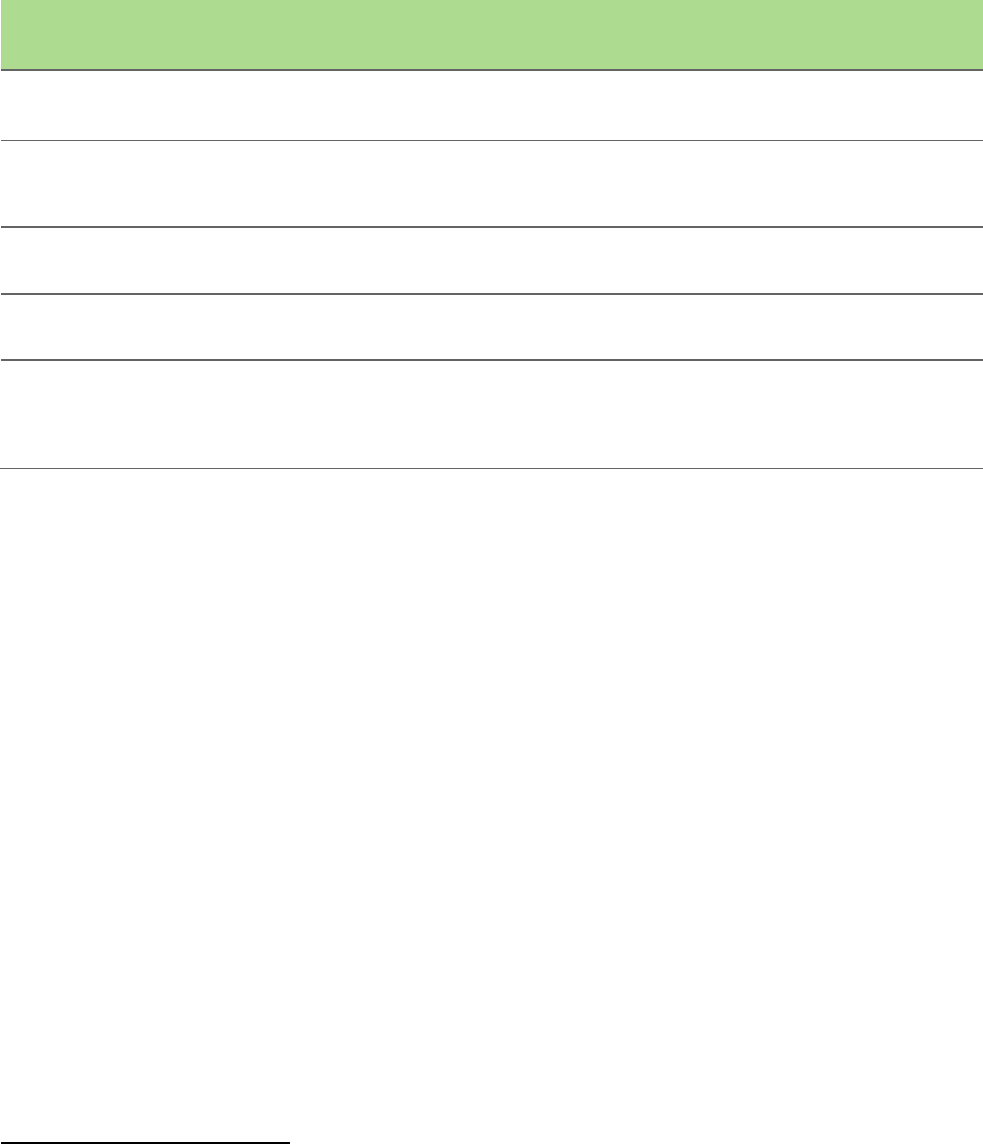

Figure 4 shows the origination volume for site-built and manufactured housing from 2004-

2019. In both markets, home purchase originations declined in the wake of the Great Recession,

hit a low in 2011, and have been increasing in the years since. Over this time period, between 2.3

percent and 3.7 percent of home purchase loans were for manufactured housing.

32

Approval rate is calculated by calculating the total number of loans originated and applications that were approved

and not accepted and dividing it by total loans originated, applications approved and not accepted, and applica tions

that were denied.

18 CONSUMER FINANCIAL PROTECTION BUREAU

FIGURE 4: SITE-BUILT AND MANUFACTURED HOUSING HOME PURCHASE ORIGINATIONS, 2004—2019

33

4.2 Geography of manufactured housing

lending

Manufactured housing accounts for approximately three percent of home purchase loan

originations nationwide in the 2019 HMDA data, or 115,000 loans, though this rate varies by

state, with the highest concentrations of manufactured housing in Mississippi, Louisiana, and

West Virginia.

Figure 5 shows the proportion of total home purchase, owner-occupied, first-lien originations

that are manufactured housing by state.

34

Table 16 in the accompanying data tables includes

33

The data behind this visualization is from Table 1 of the 2019 HMDA Data Point, found here:

https://www.consumerfinance.gov/data-research/research-reports/data-point-2019-mortgage-market-activity-

and-trends/.

34

This is calculated by dividing the number of manufacturing housing home purchase loans by the total number of

home purchase loans in 2019.

19 CONSUMER FINANCIAL PROTECTION BUREAU

data for the proportion of originations that are manufactured housing as well a breakdown of

the number of loans by manufactured housing secured property type.

FIGURE 5: MANUFACTURED HOUSING AS A PROPORTION OF HOME PURCHASE ORIGINATIONS IN 2019

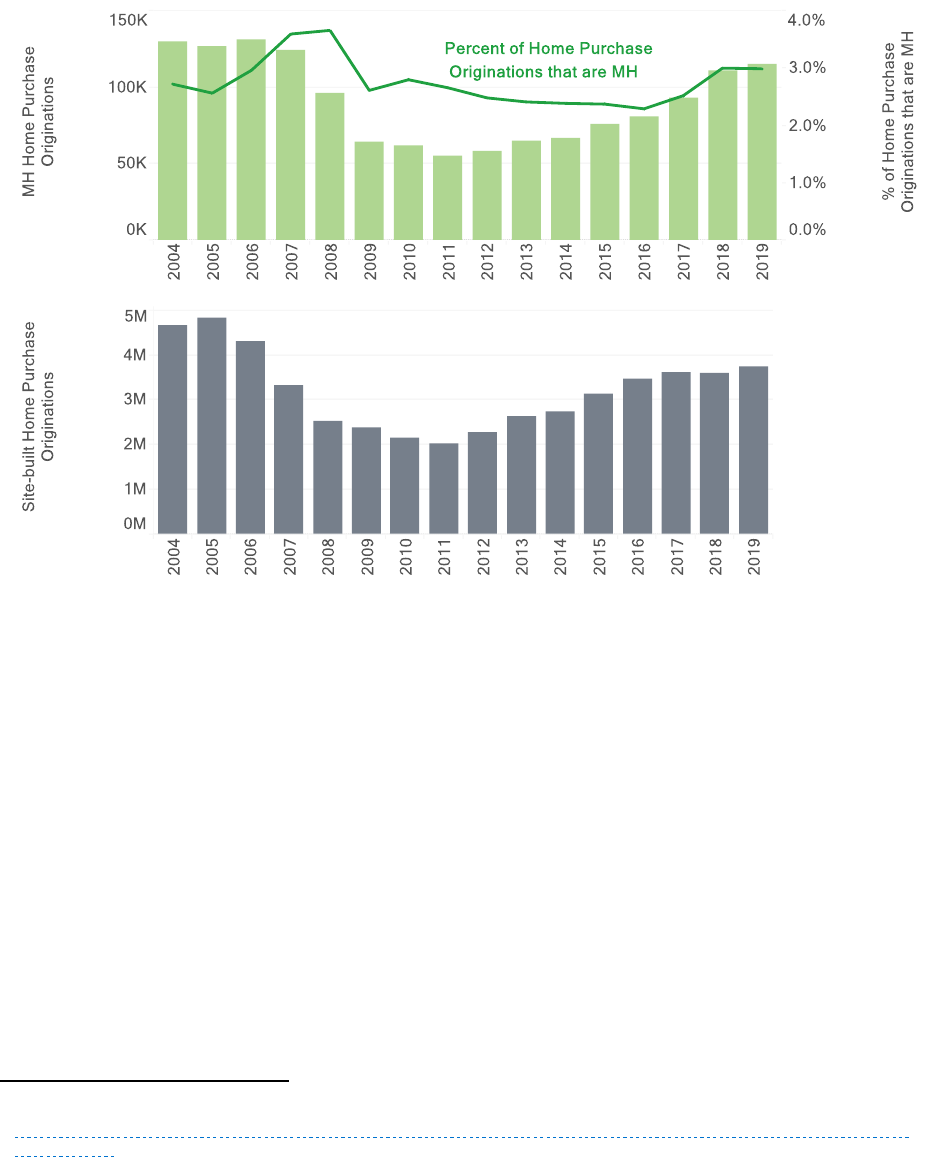

Figure 6 illustrates the proportion of manufactured housing home purchase loans that are

chattel across the country in 2019, demonstrating that chattel lending varies significantly by

region. For example, in Texas 65.7 percent of manufactured housing home purchase loans are

chattel, compared to only 10.6 percent in Washington, and both states have a sizable number of

manufactured homes. Chattel lending can even vary significantly within region—the rate is 46.1

percent in New Mexico but only 16.6 percent in neighboring Arizona. See Figure 6 for an

example of how to interpret the map. Section 4.3 further examines some of the state-level trends

in chattel lending.

20 CONSUMER FINANCIAL PROTECTION BUREAU

FIGURE 6: HOME PURCHASE LENDING BY STATE: CHATTEL AND MH MORTGAGES 2019

21 CONSUMER FINANCIAL PROTECTION BUREAU

4.3 Loan characteristics of manufactured

housing loans

Compared to mortgages for site-built homes, MH mortgages tend to have smaller loan amounts,

higher interest rates, fewer refinances, and less of a secondary market, patterns that are even

more acute for chattel loans. Additionally, chattel loans have shorter loan terms than mortgages

for either MH or site-built homes.

Site-built and manufactured housing mortgage loans vary significantly in their loan purpose,

while chattel loans are overwhelmingly home-purchase loans. In response to falling interest

rates during 2019, many consumers refinanced their loans. However, manufactured

homeowners were less likely to take advantage of the lower rates through refinancing. Chattel

loans had a much higher percentage of originations (95.9 percent) devoted to home purchases

than either mortgage or site-built originations, and significantly fewer refinance originations

then these other types of loans at 2.5 percent, as shown in Table 2. Smaller loans are less likely

to benefit from refinancing because the savings from a lower interest rate may not offset the

costs of origination, which may partially explain why chattel loans are rarely refinanced.

However, more research is needed to understand whether consumers with small loan amounts

could benefit from refinancing and whether that matches consumers’ expectations at

origination. MH mortgage loan purposes more closely resemble the loan purpose of site-built

loan purposes.

35

TABLE 2: LOAN PURPOSE OF SITE-BUILT AND MANUFACTURED HOUSING ORIGINATIONS BY

SECURED PROPERTY TYPE

LOAN PURPOSE

MANUFACTURED

HOUSING: CHATTEL

LOANS (%)

MANUFACTURED

HOUSING: MORTGAGE

LOANS (%)

SITE-BUILT (%)

HOME PURCHASE

95.9

66.4

53.9

HOME IMPROVEMENT

0.3

1.2

0.9

REFINANCING

2.5

18.0

25.9

CASH-OUT REFINANCING

0.9

12.8

18.3

OTHER PURPOSE

0.5

1.6

1.0

Table 3 shows that chattel loans are nearly all conventional, despite being potentially eligible for

Federal Housing Administration (FHA) or Department of Veterans Affairs (VA) loans.

36

Higher

35

Statistics for Loan Purpose and Loan Type exclude those coded as “not applicable”.

36

There was little demand in 2012 for the Ginnie Mae MH program. See 2014 CFPB Report, p . 38.

22 CONSUMER FINANCIAL PROTECTION BUREAU

percentages of mortgage manufactured housing originations were FHA-insured and VA

guaranteed, and a lower percentage were conventional loans. Table 3 also shows the current

distribution of purchasers among originated home purchase loans within the 2019 HMDA

Dataset. Mortgage manufactured housing loans feature a much higher percentage of Ginnie Mae

purchased originations (included in FHA, USDA, and VA) opposed to their site-built

counterparts, offsetting a slightly lower share of Freddie Mac purchased loans. Both chattel and

mortgage manufactured housing loans were less likely to be sold at all than site-built

originations.

This table shows that the secondary market for chattel loans is small, as currently conventional

chattel loans are not generally eligible for purchasing by Fannie Mae and Freddie Mac.

37

Fannie

Mae and Freddie Mac’s proposed pilot program for purchasing chattel loans could potentially

change this—however, as of May 2021 the pilot program is on pause.

38

37

For more information regarding the purchasing market rules for manufactured housing specific to GSEs, see the

table on page 6 of Fannie Mae’s Duty to Serve Report:

https://www.fhfa.gov/PolicyProgramsResearch/Programs/Documents/FannieMaeDTSPlan_2018-2021.pdf.

38

For more information regarding this pilot program, reference Fannie Mae’s Duty to Serve Manufactured Housing

Report: https://www.fhfa.gov/PolicyProgramsResearch/Programs/Documents/FannieMaeDTSPlan_2018 -

2021.pdf.

23 CONSUMER FINANCIAL PROTECTION BUREAU

TABLE 3: LOAN TYPE AND PURCHASER OF SITE-BUILT AND MANUFACTURED HOUSING ORIGINATIONS

BY SECURED PROPERTY TYPE

39

LOAN TYPE & PURCHASER

MANUFACTURED

HOUSING: CHATTEL

LOANS (%)

MANUFACTURED

HOUSING: MORTGAGE

LOANS (%)

SITE-BUILT (%)

CONVENTIONAL: FANNIE MAE

0.2

12.2

15.5

CONVENTIONAL: FREDDIE MAC

0.0

4.9

13.6

CONVENTIONAL: PRIVATE

PURCHASER

40

OR OTHER

41

18.0

6.3

21.6

CONVENTIONAL: NOT SOLD

80.9

24.6

15.9

FHA

0.7

39.4

20.1

VA

0.2

11.6

10.6

RHS OR FSA

0.0

1.0

2.6

Loan amounts for home purchases are generally lower for manufactured housing compared to

site-built homes, as shown in Table 4, reflecting the lower prices of the homes that secure the

loans. Loan amounts are higher for manufactured housing mortgage loans than chattel loans in

part because they may also include the cost of the land the unit is sited on.

TABLE 4: LOAN AMOUNTS OF HOME PURCHASE SITE-BUILT AND MANUFACTURED HOUSNG

ORIGINATIONS BY SECURED PROPERTY TYPE

CHARACTERISTIC

MANUFACTURED

HOUSING: CHATTEL

LOAN ($)

MANUFACTURED

HOUSING: MORTGAGE

LOAN ($)

SITE-BUILT LOAN

($)

25

TH

PERCENTILE

40,500

90,330

162,011

MEDIAN

58,672

127,056

236,624

75

TH

PERCENTILE

80,785

172,812

342,678

39

Rural Housing Service (RHS) and Farm Service Agency (FSA) loans are insured by the United States Department of

Agriculture (USDA).

40

Private Purchaser within this table combines four of the Type of Purchaser categories from HMDA: 1 ) Private

securitizer, 2) Commercial bank, savings bank, or savings association, Life in surance company, 3) Credit union,

mortgage company, or finance company 4) Affiliate institution.

41

The incidence of loan sales tends to decline for loans originated toward the end of the year, as lenders report a loan

as sold only if the sale occurs within the same year as origination. As a result, full-year HMDA data may

overestimate the percent of loans not sold. In this table, "Other" also includes the "Other" HMDA Type of Purchaser

category as well as a small number of loans (less than 200) that were re ported as conventional and purchased by

Ginnie Mae or Farmer Mac.

24 CONSUMER FINANCIAL PROTECTION BUREAU

Though loan amounts for manufactured housing mortgages are lower than site built loan

amounts, both typically have loan terms of 30 years, as can be seen in Table 5. Chattel loan

terms however are often shorter, typically for lengths between 20 and 23 years.

TABLE 5: LOAN TERMS OF HOME PURCHASE SITE-BUILT AND MANUFACTURED HOUSNG

ORIGINATIONS BY SECURED PROPERTY TYPE

PERCENTILE

MANUFACTURED

HOUSING: CHATTEL

LOAN (YEARS)

MANUFACTURED

HOUSING: MORTGAGE

LOAN (YEARS)

SITE-BUILT LOAN

(YEARS)

25

TH

PERCENTILE

20

30

30

MEDIAN

23

30

30

75

TH

PERCENTILE

23

30

30

While manufactured homes are generally less expensive than site-built homes, the same is not

true for the associated financing. Table 6 looks at select pricing characteristics among site-built

and manufactured housing originations by secured property type. Table 6 includes rate spread

which refers to the difference between the Annual Percentage Rate (APR) and the Average

Prime Offer Rate (APOR).

42

Because APR reflects the interest rate, points, fees, and other

associated charges, these additional costs are also accounted for in the rate spread. The rate

spread for chattel loans is substantially higher than for either MH mortgages or site-built

mortgages. Manufactured housing loans – both chattel and mortgage – are more likely than

site-built mortgages to be classified as a Higher-Priced Mortgage Loan (HPML) or a high-cost

mortgage as defined under HOEPA.

43

Nearly all of the chattel loans are HPML loans and a

higher percentage also are classified as HOEPA loans.

42

APOR refers to the hypothetical APR that a financial institution may offer to a prime mortgage borrower in a given

week. For a deeper discussion on how APOR is calculated see https://ffiec.cfpb.gov/tools/rate-

spread/methodology.

43

For purposes of this analysis, HPMLs are calculated using the same criteria as previously used for reporting HPML

rate spread under in Regulation C, 12 C.F.R. § 1003.4(a)(12) (2017): if a first lien loan has a rate spread of 1.5

percent or greater or if a junior lien loan has a rate spread of 3.5 percent or greater. (These criteria differ from the

determination of HPMLs under Regulation Z.) HOEPA loans refer to any loans with a first lien transaction, with a

rate spread of 6.5 percent or greater, with the exception of first lien transactions that are less than $50,000 and

secured by personal property including manufactured housing (in that case th e rate spread must be 8.5 percent or

greater). HOEPA loans include junior lien loans with a rate spread of 8.5 percent or greater.

25 CONSUMER FINANCIAL PROTECTION BUREAU

TABLE 6: PRICING CHARACTERISTICS OF SITE-BUILT AND MANUFACTURED HOUSING ORIGINATIONS

BY SECURED PROPERTY TYPE

CHARACTERISTIC

MANUFACTURED

HOUSING: CHATTEL

LOANS

MANUFACTURED

HOUSING: NON-

CHATTEL LOANS

SITE-BUILT

MEDIAN INTEREST RATE

8.6%

4.9%

4.1%

MEDIAN RATE SPREAD

5.2

1.6

0.4

% HPML

93.8%

52.4%

11.1%

% HOEPA

0.7%

0.2%

0.1%

To further analyze mortgage pricing, section 3.4 explores the impacts of HOEPA on the

manufactured housing market.

4.4 HOEPA

Under the Home Ownership and Equity Protection Act, certain mortgage loans that have APRs

or fees above specified levels (i.e., HOEPA loans or high-cost mortgages) are subject to

additional consumer protections, such as special disclosures and restrictions on loan features. In

2010, the Dodd-Frank Act expanded the scope of HOEPA coverage to include purchase-money

mortgages, among other changes. In 2013, the CFPB issued its final rule implementing the

HOEPA changes , and the new requirements went into effect January 10, 2014 (HOEPA Rule).

A key provision of the HOEPA Rule included additional disclosure requirements for mortgage

originators that report under HMDA.

44

The HOEPA Rule applies to first-lien loans with a rate

spread

45

of 6.5 percent or greater, with the exception of first-lien transactions that are less than

$50,000 and secured by personal property including manufactured housing. For those first-lien

loans that are less than $50,ooo and secured by personal property, or for junior-lien loans, the

rate spread must be 8.5 percent or greater to trigger the additional reporting requirements.

A key question on the impact of HOEPA on manufactured housing loans is what would happen

to borrowers above the HOEPA thresholds who would have received loans prior to the HOEPA

44

The HOEPA Rule applied to applications for which a creditor or lender received an application on January 10, 2014

or later meaning that this first impacted borrowers that took out loans in 2014 HMDA da ta. For more information

on the HOEPA Rule see: https://files.consumerfinance.gov/f/documents/bcfp_hoepa_small-entity_compliance-

guide.pdf

45

As noted in the previous section, rate spread refers to the difference between the Annual Percentage Rate (APR)

and the Average Prime Offer Rate (APOR). APOR refers to the hypothetical APR that a financial institution may

offer to a prime mortgage borrower in a gi ven week. For a deeper discussion on how APOR is calculated see

https://ffiec.cfpb.gov/tools/rate-spread/methodology. Because APR reflects the interest rate, points, fees, and other

associated charges, these additional costs are also accounted for in the rate spread.

26 CONSUMER FINANCIAL PROTECTION BUREAU

Rule taking effect. There are two potential impacts—one being a loss in access to credit among

those HOEPA borrowers who would have received MH loans prior to the HOEPA Rule and now

did not as a result of the additional costs associated with the HOEPA Rule. Another potential

impact is that borrowers are still approved for their loan and get a lower interest rate as a result

of the HOEPA rule.

Figure 7 attempts to tease out the impact the HOEPA Rule has had on rate spread in the

manufactured housing marketplace by showing manufactured housing rate spreads for 2013

and 2014 with reference lines at 6.5 percent and 8.5 percent rate spreads. In 2013, 13 percent of

loans had a rate spread of 8.5 percent or higher, while in 2014, 2.0 percent of loans had a rate

spread of 8.5 percent or higher. There was significant bunching in the rate spread bucket

immediately below both the 6.5 and 8.5 percent threshold.

46

The bunching suggests that lenders

responded to the HOEPA changes by adjusting their pricing to fall right below the thresholds.

46

Prior to 2018, HMDA data only featured rate spreads for loans with spreads above 1.5 percent. Among

manufactured housing loans in the 2013 HMDA data, approximately 65 percent of manufactured housing loans had

a reported rate spread, and thus these median rate spread statistics do not fully take into account loans with rate

spreads less than 1.5 percent.

27 CONSUMER FINANCIAL PROTECTION BUREAU

FIGURE 7: MANUFACTURED HOUSING HOME PURCHASE RATE SPREADS: 2013 & 2014

While Figure 7 shows that pricing adjusted to fall below HOEPA thresholds, it does not show

how access to credit changed following implementation. Two metrics that get at the overall level

of credit offered to borrowers is the number of originations and origination rate. Per Figure 4,

the number of manufactured housing originations grew from 65,000 in 2013 to 67,000 in 2014

and the home purchase origination rate remained steady. These metrics do not suggest an

overall loss of credit for borrowers from the HOEPA changes.

However, this simple comparison is not enough to draw a conclusion on the impact of the rule

on similarly situated borrowers. Additionally, it is possible that lenders adjusted the pricing of

factors other than interest rate in response, so the overall effect on profitability cannot be

hypothesized. This descriptive evidence is not enough to make any definitive determinations on

the impact of HOEPA but suggests that the market responded to the HOEPA Rule by lowering

the rate spreads on manufactured home loans and may have done so without decreasing the

availability of credit for such loans.

As of 2019, a substantial portion of MH loans continue to have rate spreads just below the

HOEPA thresholds, as illustrated below. Figure 8 shows the distributions of rate spread for four

28 CONSUMER FINANCIAL PROTECTION BUREAU

different types of originated loans from the 2019 HMDA data: site-built homes, chattel loans for

manufactured homes for over and under $50,000, and mortgage loans for manufactured

homes. There are vertical lines drawn at HPML and HOEPA thresholds.

47

The HOEPA threshold

at 8.5 percent applies to first lien chattel loans of under $50,000, while the threshold at 6.5

percent applies to the other three groups of loans. Mortgages for site-built homes have rate

spreads well below the HOEPA thresholds, while loans for manufactured homes are often priced

so that the rate spread falls just below the HOEPA threshold. Nearly 5 percent of MH mortgages,

26 percent of chattel loans over $50,000, and 16 percent of chattel loans under $50,000 have

rate spreads that were below the HOEPA threshold but within 25 basis points.

47

The percentages for HOEPA and HPML refer to the percentage of ori ginations that fall within these pricing

categories.

29 CONSUMER FINANCIAL PROTECTION BUREAU

FIGURE 8: 2019 RATE SPREAD FOR HOME PURCHASE ORIGINATED SITE-BUILT, MORTGAGE

MANUFACTURED HOUSING, AND CHATTEL MANUFACTURED HOUSING LOANS UNDER AND OVER

$50,000

30 CONSUMER FINANCIAL PROTECTION BUREAU

5. Borrowers and Lenders

This section focuses on the characteristics of the borrowers, lenders, and loans that make up the

manufactured housing market.

Analysis of borrowers focuses on their demographics, creditworthiness, and selection of a

chattel or mortgage loan. Of particular significance in the manufactured housing market is how

borrowers finance their home depending on whether they own or lease the land it is sited on.

This section analyzes how land ownership and financing decisions affect overall loan costs. It

focuses in particular on borrowers who own their land and take out a chattel loan despite being

eligible for a mortgage.

This section also analyzes manufactured housing originators and purchasers to understand who

finances manufactured housing loans and how this has changed over time, particularly since the

Great Recession.

5.1 Borrower demographics

The composition of race and ethnicity of borrowers differs significantly between site-built and

manufactured housing and between chattel and mortgage loans for manufactured housing.

Figure 9 shows the classification of ethnicity and race among the borrowers taking out

manufactured housing loans in comparison to loans for site-built homes.

48

In terms of

manufactured housing financing overall, non-Hispanic whites, Hispanic whites, and American

Indian and Alaska Natives make up a larger share of manufactured housing borrowing than site-

built housing, while Black and African Americans and Asians make up a smaller share of

manufactured housing borrowing relative to site-built.

In comparison to site-built and chattel loans, non-Hispanic whites make up a larger share of

MH mortgage borrowers. Asians, Native Hawaiians, and Pacific Islanders make up a smaller

share of both chattel and mortgage borrowers than site-built borrowers. However, much of the

differences in the racial composition of borrowers corresponds with a higher percentage of

48

In the HMDA data, race and ethnicity are reported for the applicant and co-applicant. Ethnicity is reported as

either “Hispanic or Latino” or “Not Hispanic or Latino”. Race is reported as “American Indian or Alaska Native”,

“Asian”, “Black or African American”, “Native Hawaiian or Other Pacific Islander”, or white and borrowers can

select multiple races. Entities can also report "Not provide”" or “Not applicable” for each field. In this analysis, the

fields are combined to create a single field for race and ethnicity; the methodology is explained later on.

31 CONSUMER FINANCIAL PROTECTION BUREAU

manufactured housing originations occurring in rural areas—where there is a higher percentage

of non-Hispanic whites and a lower percentage of Asians.

49

Distinguishing between chattel and MH mortgage borrowing, Hispanic white, Black and African

American, and American Indian and Alaska Native borrowers make up larger shares of chattel

loan borrowers than among MH mortgage loan borrowers or among site-built loan borrowers.

Therefore, Black and African American borrowers are the only racial group that are

underrepresented (though only slightly) in manufactured housing lending overall compared to

site-built, but overrepresented in chattel lending compared to site-built. These varying

concentrations indicate that experiences with financing manufactured housing can differ by race

and ethnicity.

FIGURE 9: ETHNICITY AND RACE OF BORROWERS OF SITE-BUILT AND MANUFACTURED HOUSING

ORIGINATIONS (PERCENT)

50

49

Pew Research Center, May 2018, “What Unites and Divides Urban, Suburban and Rural Communities”.

https://www.pewresearch.org/social-trends/2018/05/22/what-unites-and-divides-urban-suburban-and-rural-

communities/

50

If an applicant reports two races and one is white, that applicant is categorized under the minority race. Otherwise,

the applicant is categorized under the first race reported.

The applicant is categorized as “Hispanic white” if the applicant reports Hispanic and white or if the applicant reports

Hispanic and race is not provided. The application is designated as “Non -Hispanic white” if the applicant reports

Non-Hispanic and white or if the applicant reports white and ethnicity is not provided.

32 CONSUMER FINANCIAL PROTECTION BUREAU

Figure 10 shows that borrowers 24 years old or younger and borrowers 55 and over are

overrepresented in manufactured housing when compared to site-built borrowers.

FIGURE 10:AGE OF BORROWERS OF SITE-BUILT AND MANUFACTURED HOUSING ORIGINATIONS

The applicant is categorized as “joint” if one applicant was reported as white and the other was reported as one or

more minority races or if the application is designated as white with one Hispanic applicant and one non -Hispanic

applicant. If the applicant reports two or more minority races or there are two applicants and each reports a

different minority race, the application is designated as two or more minority races.

"Missing" refers to applicants in which the race of the applicant(s) has not been reported or is not applicable, unless

the ethnicity is reported as Hispanic, in which case the application is categorized under “Hispanic white”.

American Indian and Alaskan Native, Native Hawaiian and Pacific Islander, and multi-minority applicants are

grouped together in this visualization due to their relatively small populations. However, it is important to note that

American Indian and Alaskan Native applicants make up nearly 60 percent this group. Within the American Indian

or Alaska Native population, there are 819 chattel borrowers, 564 MH mortgage borrowers, and 17,242 site-built

borrowers, representing 1.7 percent, .9 percent, and .5 percent respectively of each loan category. Within the Native

Hawaiian and Pacific Islander population, there are 92 chattel borrowers, 72 MH mortgage borrowers, and 7,363

site-built borrowers, representing .2 percent, .1 percent, and .2 percent respectively of each loan category. Within

the multi-minority population, there are 74 chattel borrowers, 48 MH mortgage borrowers, and 5,578 site-built

borrowers, representing .2 percent, .1 percent, and .1 percent respectively of each loan category. This disaggregated

data can also be found in the accompanying tables.

33 CONSUMER FINANCIAL PROTECTION BUREAU

5.2 Borrower creditworthiness: chattel and

mortgage

Borrowers of site-built mortgages have higher median income and credit score than

manufactured housing borrowers, as shown in Table 7 below. Among manufactured-home

borrowers, chattel and mortgage borrowers have similar median incomes, though mortgage

borrowers have a slightly higher median credit score and higher debt-to-income ratio (DTI).

Median Combined Loan-To-Value Ratios (CLTVs) are highest on mortgage manufactured home

loans and lowest for chattel loans.

51

TABLE 7: BORROWER CHARACTERISTICS OF SITE-BUILT AND MANUFACTURED HOUSING HOME

PURCHASE ORIGINATIONS BY SECURED PROPERTY TYPE

CHARACTERISTIC

(MEDIAN)

MANUFACTURED

HOUSING: CHATTEL

LOANS

MANUFACTURED

HOUSING: MORTGAGE

LOANS

SITE-BUILT

CREDIT SCORE

676

691

739

INCOME

$52,000

$53,000

$83,000

CLTV

87.0

96.5

95

DTI

35.7

38.9

38.7

5.3 Owned vs. Leased Land

As discussed in Section 2.1, manufactured homes can be owned separately from the land on

which they are located, which affects both the way in which a manufactured home is titled and

how it is financed.

Borrowers who own their land can either finance their home purchase with a chattel loan or a

mortgage, whereas those who do not own their land are typically only able to finance with a

chattel loan.

52

In general, chattel loans have higher interest rates and fewer consumer

51

CLTV refers to the ratio of the total amount of debt that is secured by the property to the value of the property, see

variable number 34 in the HMDA Guide. DTI refers to the ratio of the applicant’s total monthly debt to the total

monthly income., see variable description of number 33 in the HMDA guide, se e

https://www.ffiec.gov/hmda/pdf/2018guide.pdf.

52

Arizona, Colorado, Iowa, New Hampshire, North Dakota, Oregon, Texas, Vermont, Washington and Wisconsin

allow manufactured homes on leased land to be titled as real property if a variety of conditions are met, including

provisions about lease term and foundation type , see

https://www.nclc.org/images/pdf/manufactured_housing/Titling_Reform-

How_States_Can_Encourage_GSE_Invest_Manuf_Homes.pdf.

34 CONSUMER FINANCIAL PROTECTION BUREAU

protections than mortgages. However, consumers who get chattel loans avoid putting the

underlying land at risk in the event that they default on the loan, and some landowners express

a desire to avoid encumbering their land.

53

This section examines some of the other plausible

reasons that consumers who own their land may get chattel loans instead of MH mortgages,

such as borrowers’ credit characteristics, closing times, and closing costs. Knowing the

proportion of direct owners that have chattel loans and understanding why they took out chattel

loans as opposed to MH mortgages is important to the CFPB, particularly if consumers are not

educated about the downsides of chattel loans or if they are potentially being steered into a

chattel loan even in cases where a mortgage would be better suited to the consumer’s situation.

As mentioned in Section 2.2, the new information on Manufactured Home Land Property

Interest in HMDA data point shine light on this issue.

As expected, consumers’ land ownership affects their financing outcomes as seen in Figure 11.

Nearly all consumers who purchased a manufactured home with mortgage financing were direct

owners of the underlying land, and a small fraction were members of ROCs communities or

similar indirect owners. Among those with chattel loans, almost half (49 percent) rented the

land, while another 24 percent leased the land for free. Discussions with industry indicate that

many consumers who do not pay rent are leasing from family members in either formal or

informal agreements. HMDA data indicate that these arrangements may play an important role

for manufactured housing consumers. Lastly, 27 percent of consumers who received chattel

loans owned their land, even though they may have been eligible for mortgage financing.

54

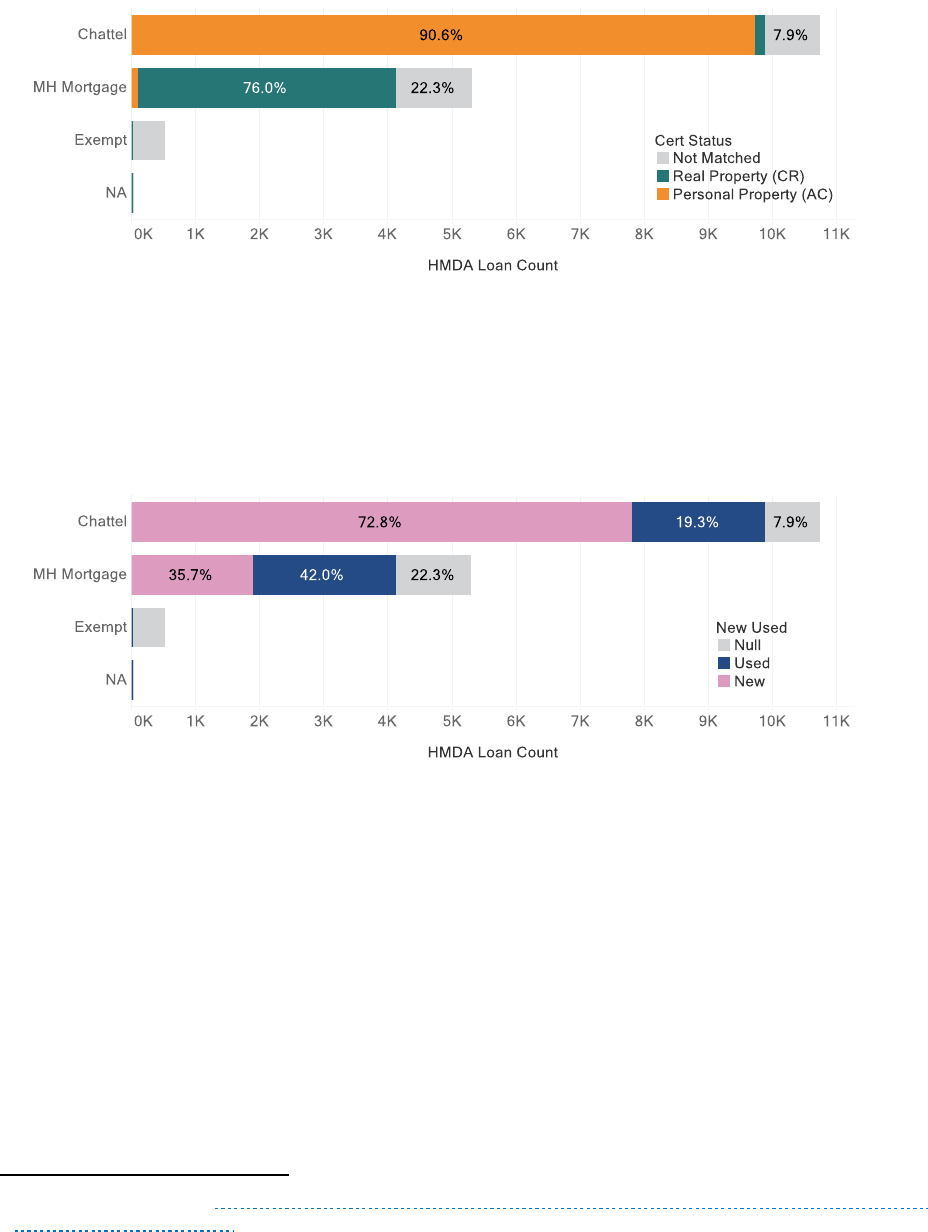

Figure 11 also shows that around 6,000 loans, or five percent of manufactured housing loans,

are exempt from reporting both the manufactured home secured property type and the

manufactured home land property interest.

55

Based on pricing, purpose, amounts, term length,

and other characteristics, these loans appear to be a mix of chattel loans and manufactured

housing mortgages.

53

“The Loan Shopping Experiences of Manufactured Homeowners: Survey Report,” Freddie Mac and the Center for

Community Capital at the University of North Carolina.

https://sf.freddiemac.com/content/_assets/resources/pdf/report/manufactured-homeowners-survey-and-report-

on-loan-shopping-experiences.pdf

54

Though the analysis in this paper only includes owner-occupied (primary) residences, it is worth noting that over

half of investment properties (occupancy type = 3) with direct owners have chattel loans, compared to only about 17

percent of primary residences (occupancy type =1) and 15 percent of secondary residences (occupancy type = 2).

55

Under the Economic Growth, Regulatory Relief, and Consumer Protection Act (EGRRCPA), certain depository

institutions and insured credit unions are exempted from reporting some HMDA data, including the two

manufactured housing data points, for certain transactions.

35 CONSUMER FINANCIAL PROTECTION BUREAU

FIGURE 11: SECURED PROPERTY TYPE BY LAND PROPERTY INTEREST

Chattel lending varies by state, as discussed in Section 3.2, and the ownership and leasing

arrangements for chattel loans also have a geographic component. Figure 12 shows the Land

Property Interest for chattel loans only — the pie charts in Figure 12 represent just the orange

slices of the pie charts from Figure 6. See Figure 12 for an example of how to interpret this map.

Throughout the West, Midwest, and Northeast, the vast majority of chattel borrowers pay to

rent their land (“paid leasehold”) and, therefore, do not have the option to get a mortgage. In the

South, chattel borrowers are more likely to either own their land or rent it for free (“unpaid

leasehold”). Notably, upwards of 90 percent of unpaid leaseholds are in Southern states.

56

The

data in Figure 12 can also be found in the accompanying data tables.

56

Texas, Alabama, Mississippi, Louisiana, South Carolina, Ark ansas, Georgia, North Carolina, Oklahoma, Florida,

Kentucky, and Tennessee accounted for approximately 90 percent of home purchases with unpaid leaseholds.

36 CONSUMER FINANCIAL PROTECTION BUREAU

FIGURE 12: LAND PROPERTY INTEREST FOR CHATTEL BORROWERS

The remainder of this section looks in depth at the borrowers who own their land and, therefore,

may have a choice between financing with a mortgage or a chattel loan. In the context of this

report, the term “landowner” refers to those who reported “Direct Ownership” for the field

“Manufactured Home Land Property Interest” in HMDA—it does not include those who report

“Indirect Ownership.” The analyses examine the prevalence of chattel loans for all borrowers

who own their land, break out the data by race and age, and provide metrics on borrowers’

credit characteristics and on the loans’ interest rates, upfront costs, and closing times.

37 CONSUMER FINANCIAL PROTECTION BUREAU

In addition to these loan characteristics, landowners’ decisions about financing options may be

influenced by other financial and behavioral factors as well. In some states, tax rates are lower

on personal property than real property, which anecdotal evidence suggests is a factor for some

borrowers. Lenders have stated that some consumers own their land or family land and prefer

not to encumber it with a mortgage, and findings from UNC/Freddie Mac survey of MH

borrowers also indicate that many Texas borrowers that choose chattel have a strong desire not

to encumber the land.

57

Additionally, consumers may not be aware of their options or the

tradeoffs between the two types of loans, such as the differences in consumer protections during

foreclosure or repossession. Others may be influenced by the fact that manufactured homes are

titled as personal property by default in many states.

58

The 2019 HMDA data indicate that 17 percent of all landowning manufactured housing

borrowers take out chattel loans. This result is lower than estimates from previous research,

including the 2014 CFPB Report where the CFPB used AHS data to estimate that 65 percent of

all borrowers who own their land and who took out a loan to buy a manufactured home between

2001 and 2010 financed the purchase with a chattel loan. As noted in Section 2.2, AHS does not

have specific fields tracking chattel versus mortgage financing. Therefore, the CFPB used a

proxy to estimate the percent of chattel borrowers. Specifically, the CFPB used mobile home

foundation type and annual real estate tax as a proxy for financing type to estimate the chattel

population. Generally, the CFPB labeled records that reported a “permanent foundation” as

“mortgage” and labeled records with all other foundation types as “chattel”.

59

However, later

analysis of MHS found that real and personal property in MHS have a variety of foundation

types. Based on this, the CFPB concludes that the foundation type variable in AHS is an

imperfect proxy for secured property type, and ultimately the estimates about the proportion of

lending that is chattel from the 2014 report are not valid.

After adding the data points about manufactured housing in 2018, HMDA became the only

national level dataset that directly tracks financing type. These new HMDA data allow

researchers to study financing behavior in manufactured housing without having to make the

assumptions required in past studies.

57

Full report here: https://sf.freddiemac.com/resources/manufactured-homeowners-survey-and-report-on-loan-

shopping-experiences

58

For further discussion on some of the tradeoffs, see the National Consumer Law Cent er’s report “Titling Home as

Real Property.” https://www.nclc.org/images/pdf/manufactured_housing/cfed -titling-homes.pdf.

59

This proxy is used because in most cases, manufactured homes must be permanently affixed to the land in order to

be eligible for traditional mortgage financing, though the definition of “permanently affixed to the land” is defined

differently by each state. For further insight into how titling requirements for real property differ by state, see the

National Consumer Law Center’s report “Titling Homes as Real Property.”

https://www.nclc.org/images/pdf/manufactured_housing/cfed-titling-homes.pdf

38 CONSUMER FINANCIAL PROTECTION BUREAU

5.3.1 Landowners

As shown previously in Figure 11, around 13,000 of the approximately 73,000 total direct

owners took out a chattel loan, indicating that most direct owners take out a MH mortgage.

Table 8 considers manufactured-home borrowers who owned their land and compare those who

got chattel loans to those who got mortgages. One possible explanation for borrowers who own

land and take out chattel loans is a lack of creditworthiness to qualify for mortgage loans, but

these tables seem to offer contradictory evidence, as many landowners who get chattel loans

have similar if not slightly better credit profiles than landowners who get MH mortgages.

However, borrowers may encounter difficulty getting mortgages with small loan amounts.

Chattel borrowers have a median loan term of 23 years, which is much shorter than loan terms

for mortgage borrowers. A plurality of MH mortgage borrowers have loan terms of 30 years—

typical of mortgages. Shorter loan terms, all else equal, result in higher monthly payments. Loan

amounts are lower for chattel loans, which likely reflects the fact that chattel loans do not

include the value of the underlying land.

TABLE 8: BORROWER CHARACTERISTICS: DIRECT OWNERS

CHARACTERISTIC (MEDIAN)

MANUFACTURED HOUSING:

CHATTEL LOANS

MANUFACTURED HOUSING:

MORTGAGE LOANS

APPLICANT CREDIT SCORE

688

691

COMBINED LTV

90.8

96.5

DEBT-TO-INCOME RATIO

35.5

39.0

APPLICANT INCOME

$55,000

$53,000

LOAN TERM (YEARS)

23

30

LOAN AMOUNT

$70,731

$127,200

Figures 13, 14, and 15 report the volume and percentage of direct landowners that took out a

chattel loan across groups of credit scores, ages, and race and ethnicity. The proportions are

created by dividing the number of chattel loans by the total number of manufactured housing

home purchase originations for which the borrower directly owned the land. Among direct

owners, those in the deep subprime and subprime buckets are more likely to take out chattel

loans than the near prime and prime borrowers.

39 CONSUMER FINANCIAL PROTECTION BUREAU

FIGURE 13:SECURED PROPERTY TYPE FOR DIRECT OWNERS BY CREDIT SCORE

60

Figure 14 shows that older direct owner borrowers are more likely to take out chattel loans than

younger borrowers.

60

An example of how to interpret this graph: 34 percent of direct owners with a credit score of 579 or lower took out a

chattel loan. Loans where secured property type is exempt or not applicable have been excluded f rom the percent of

total calculation.

40 CONSUMER FINANCIAL PROTECTION BUREAU

FIGURE 14:SECURED PROPERTY TYPE FOR DIRECT OWNERS BY AGE

61

Figure 15 below displays the number and percentages of chattel loans across race and ethnicity

among direct owner home purchase borrowers. Blacks and African Americans; Hispanic whites;

and American Indians and Alaskan Natives had a substantially higher percentage of chattel