CONSUMER FINANCIAL PROTECTION BUREAU | JUNE 2023

Consumer Finances in

Rural Areas of the

Southern Region

Data Point

Office of Research

This data point is part of an occasional series of publications from the Consumer

Financial Protection Bureau’s Office of Research. These publications are intended

to further the CFPB’s objective of providing an evidence-based perspective on

consumer financial markets, consumer behavior, and regulations to inform the

public discourse. See 12 U.S.C. §5493(d).

DATA POINT: CONSUMER FINANCES IN THE RURAL SOUTHERN REGION 1

Table of contents

Table of contents ......................................................................................................... 2

Executive Summary ....................................................................................................3

1. Demographic and Economic Profile of the Rural Southern Region .................6

2. Consumer Finance Profiles ...............................................................................10

2.1 Credit Cards.................................................................................................. 12

2.2 Auto Loans ....................................................................................................15

2.3 Home Loans ................................................................................................. 18

2.4 Student Loans .............................................................................................. 21

3. Consumer Distress and Delinquencies ............................................................23

3.1 Medical Collections ...................................................................................... 23

3.2 Consumer Delinquencies ............................................................................. 25

4. Conclusion ..........................................................................................................28

Appendix A: Auto Originations in Majority-Minority Census Tracts ................29

Appendix B: State-Level Analysis .......................................................................30

Alabama .................................................................................................................. 30

Arkansas ................................................................................................................. 34

Georgia ...................................................................................................................38

Louisiana ................................................................................................................42

Mississippi .............................................................................................................. 46

North Carolina ........................................................................................................50

South Carolina ........................................................................................................ 54

Tennessee ...............................................................................................................58

DATA POINT: CONSUMER FINANCES IN THE RURAL SOUTHERN REGION 2

Executive Summary

This report is the second in a series profiling the finances of consumers in rural communities.

1

It

takes a broad look at consumer financial profiles in the southern region of the U.S. compared to

other geographies, including credit scores, financial distress, medical debt, and other debt

categories. Nearly 48 million people live in the southern region examined in this report, which

includes Alabama, Arkansas, Georgia, Louisiana, Mississippi, North Carolina, South Carolina,

and Tennessee.

2

Twenty-three percent of consumers in the southern region live in rural counties

and 15 percent live in Persistent Poverty Counties (PPCs), about double the national rural and

PPC shares of 14 percent and 7 percent respectively. This report is intended to provide a starting

point in better understanding the financial situations, needs and challenges of consumers in

rural areas in the southern region. For an in-depth look at issues related to banking and credit

access in both rural and non-rural areas in the southern region, see the CFPB’s report on

Banking and Credit Access in the Southern Region of the U.S.

3

Many consumers in the region’s rural areas may face challenges in the consumer financial

marketplace. Like rural consumers in other areas, rural southerners are older and earn less than

non-rural consumers on average.

4

Consumers in the southern region’s rural areas also face

distinct challenges. They are more likely to have a subprime credit score and tend to have less

digital and physical access to financial service providers than other rural consumers. This can

make it more difficult and expensive to get credit. These challenges may reflect in part persistent

correlations between race and economic outcomes.

5

Twenty-four percent of rural southerners in

this region are Black, for example, compared to 3 percent of Americans in other rural areas.

1

The first report in the series is on rural Appalachia. See Liu, Luce, Orevba, Sebastian, and Shupe, “Consumer

Finances in Rural Appalachia,” (September 2022), available at

https://files.consumerfinance.gov/f/documents/cfpb_consumer-finances-in-rural-appalachia_report_2022-09.pdf

2

These are a subset of the states in, for example, the Census Bureau’s South Region.

3

CFPB, “Banking and Credit Access in the Southern Region of the U.S.,” (June 2023).

4

For brevity, we refer to consumers in the eight-state southern region examined in this report as “southerners” and

those in rural areas in the region as “rural southerners”

5

See, for example, Bynum “Testimony of William J. Bynum, Hope Enterprise Corporation / Hope Credit Union /

Hope Policy Institute before the United States Senate Committee on Banking, Housing and Urban Affairs,” (April

2021) available at https://www.banking.senate.gov/imo/media/doc/Bynum%20Testimony%204-20-21.pdf. For a

recent academic paper on these issues, see Feigenbaum, Lee, and Mezzanotti. "Capital Destruction and Economic

Growth: The Effects of Sherman's March, 1850–1920." (October 2022) available at

https://doi.org/10.1257/app.20200397

DATA POINT: CONSUMER FINANCES IN THE RURAL SOUTHERN REGION 3

Key Findings

Section 2 summarizes how rural southerners and rural southerners living in Persistent Poverty

Counties fare across consumer financial products. Key findings include:

Sixty-seven percent of rural southerners have a credit card, compared to 75 percent in

rural areas outside the southern region and 80 percent nationwide. Rural southerners

who do have credit cards have higher utilization rates than consumers elsewhere. The

average consumer in the rural southern region has a balance of 38 percent of their credit

limit, compared to a national average of 31 percent.

Rural southerners and rural southerners living in Persistent Poverty Counties are as

likely to have an auto loan as the national average (42 percent), slightly less than the

average for rural counties outside the southern region (45 percent). However, two-year

delinquency rates in the rural southern region (16 percent) and rural southern Persistent

Poverty Counties (20 percent) are higher than the national average (11 percent) and in

rural areas outside the southern region (10 percent).

6

Twenty-three percent of rural southerners have an outstanding mortgage, lower than the

average for rural areas outside the southern region (28 percent). Seven percent of

mortgages in the rural southern region are home-only secured manufactured home

loans, compared to 3 percent in other rural areas and 1 percent nationally.

The median remaining balance for rural southerners with student loans ($17,499) is

similar to the median for rural consumers outside the southern region ($17,231) and

lower than the national median ($20,286). However, median scheduled monthly

payments are lower in the rural southern region. The median rural southerner has a

scheduled monthly payment of $157, compared to $169 in other rural areas and a

national average of $192.

Rural southerners who apply for credit are less likely to obtain it and take it out than the

national average, even when comparing across groups with similar credit scores. For

example, the share of credit card applications that are eventually originated in the rural

south is 4 percentage points lower than the national average for consumers with both

subprime and super-prime credit scores.

6

Delinquency rates are the share of consumers with at least one 60+ day delinquency, charge-off, or collection in a

given category during the 24 months between March 2020 and April 2022.

DATA POINT: CONSUMER FINANCES IN THE RURAL SOUTHERN REGION 4

Across credit products, rural southerners tend to pay higher interest rates on average. In

rural parts of the southern region, the average interest rate on a mortgage was 3.51

percent in 2021, compared to 3.13 percent nationally. For credit cards, the median

interest rate in the region’s rural areas is 18.99 percent, compared to 17.74 percent in

other rural areas and 17.90 percent nationwide.

In Section 3, this report further examines consumer distress in medical collections and other

markets in the rural southern region, compared to other geographic areas, with distress

measured as the two-year delinquency rate. Key findings include:

Rural southerners are more likely to have medical collections on their credit report (28

percent) than consumers elsewhere (17 percent). The prevalence of reported medical

collections varies widely among states in the southern region; 34 percent of rural South

Carolinians have a medical debt collection tradeline, over 41 percent more than the share

of rural consumers with a medical collection in Mississippi (24 percent).

Nationwide consumer reporting agencies have recently changed their reporting practices

to remove medical collections that are paid or under $500. Rural southerners are more

likely to have at least one medical collection eligible for removal (20 percent) than rural

non-southerners (15 percent) or the national average (12 percent).

Medical collections are the most common type of delinquency in the rural southern

region, followed by student loans (21 percent) and credit cards (18 percent). Rural

southerners with medical collections are much more likely to have a delinquency on

other types of debt. For example, 16 percent of rural southerners with an auto loan were

at least 60 days delinquent at some point over a two-year period. For those with medical

collections, the auto loan delinquency rate more than doubles, to 33 percent.

DATA POINT: CONSUMER FINANCES IN THE RURAL SOUTHERN REGION 5

1. Demographic and Economic

Profile of the Rural Southern

Region

This report examines the following southern states: Alabama, Arkansas, Georgia, Louisiana,

Mississippi, North Carolina, South Carolina, and Tennessee.

7

These states are home to 48

million people and share a number of demographic characteristics. The region is

disproportionately rural, with 23 percent living in a rural county compared to 14 percent of the

population nationwide.

This region is also rich in its diversity, with a mix of race, age, and incomes, across both rural

and non-rural communities. This region has a large rural Black population. Nearly a quarter of

rural southerners are Black, and 70 percent of the national rural Black population resides in the

eight states covered by this report. Although the share of the population born outside the United

States living in the South (7 percent) is lower than the national average (14 percent), over 3

million immigrants live in the region. While the region’s rural areas have a substantial

population of older residents, 21 percent rural southerners are between 18 and 34 years old.

Understanding these variations within the region, and how they compare to elsewhere,

contributes to understanding different experiences people may have in accessing financial

services.

Nearly half (48 percent) of the nation’s Persistent Poverty Counties, in which poverty rates have

been 20 percent or more for at least 30 years, are in the southern region (shown in Figure 1.)

More than seven million people live in southern Persistent Poverty Counties. Following the

national pattern, most southern Persistent Poverty Counties are also rural (187 out of 240), and

these rural Persistent Poverty Counties include roughly four million people.

7

For brevity, we refer to consumers in the eight-state southern region examined in this report as “southerners” and

those in rural areas in the region as “rural southerners.”

DATA POINT: CONSUMER FINANCES IN THE RURAL SOUTHERN REGION 6

FIGURE 1: MAP OF SOUTHERN COUNTIES

Note: The southern region includes Alabama, Arkansas, Georgia, Louisiana, Mississippi, North Carolina, South

Carolina, and Tennessee. PPC stands for persistent poverty county. Source: Rural and urban status definitions are

from the U.S. Department of Agriculture (USDA) Rural-Urban Commuting Area Codes. PPC definitions stem from

the Economic Development Administration (EDA).

Table 1 below details selected characteristics for rural Persistent Poverty Counties and rural

areas as a whole in the southern region and compares these to other rural areas outside of the

region and to the national average. There are only 4.0 bank or credit union branches per 10,000

residents in the rural south, well below the 6.3 branches per 10,000 people in non-southern

rural areas.

8

Furthermore, just 69 percent of households in rural parts of the southern region

have access to broadband, compared to 83 percent of households nationally. The CFPB’s report

on banking and credit access in the South discusses how these factors may impact banking

access and credit access in the region.

9

8

Branches per 10,000 people is a common metric for measuring access to financial services, but may not capture

other important aspects of accessibility, such as the distance consumers must travel to visit a branch. Consumers in

sparsely populated rural counties with relatively high branches per capita may lack ready access to banking services

due to long or inconvenient travel times.

9

CFPB, “Banking and Credit Access in the Southern Region of the U.S.,” (June 2023).

DATA POINT: CONSUMER FINANCES IN THE RURAL SOUTHERN REGION 7

TABLE 1: REGIONAL CHARACTERISTICS

DATA POINT: CONSUMER FINANCES IN THE RURAL SOUTHERN REGION 8

Rural

PPCs in

southern

region

Rural

southern

region

Rural

non-

southern

region

Non-

rural

southern

region

Southern

region

Nationwide

Median

household

income

$36,827

$42,021

$52,028

$58,200

$54,527

$65,770

Percent age

18-34

22

21 21

24

23 23

Percent age

60+

24

25

26

21

22

22

High school

graduation rate

(percent)

82

83 88

89

88 90

Percent with at

least some

college

44

47

52

61

58

62

Percent with a

post-secondary

degree

22

24 29

37

34 39

Percent Black 41 24 3 26 3 12

Percent

Hispanic

4 5 10 8 10 18

Percent White 52 67 81 61 81 61

Percent Asian 1 1 1 3 1 5

Percent

American

Indian or

Alaska Native

2 1 2 0 2 1

Percent

foreign-born

2 3 4 8 7 14

Percent

speaking a

language other

than English at

home

5 5

10

11 9

22

Percent of

households

with broadband

access

64

69 76

81

78 83

Bank/CU

branches per

10,000

residents

4.3 4.0 6.3 3.0 3.6 5.0

Rural Rural Non-

Rural

PPCs in non- rural Southern

southern Nationwide

southern southern southern region

region

region region region

Percent of

owner-occupied 67 70 73 67 67 66

housing

Number of

counties

187 399 1,576 289 688 3,142

Note: The southern region includes Alabama, Arkansas, Georgia, Louisiana, Mississippi, North Carolina, South

Carolina, and Tennessee. PPC stands for persistent poverty county. Source: 2019 5-year American Community Survey

(ACS) county-level data. Sample size refers to the number of counties. Bank branch data is derived from CFPB

analysis of Federal Financial Institutions Examination Council, National Information Center (December 2021),

National Credit Union Administration, Credit Union and Corporate Call Report Data, Quarterly Data (December

2021), and Census Bureau’s Annual Population Estimates (December 2020).

DATA POINT: CONSUMER FINANCES IN THE RURAL SOUTHERN REGION 9

2. Consumer Finance Profiles

This section compares credit and debt portfolios of rural southerners with 1) the national

average and 2) other rural consumers in other parts of the U.S. For example, we contrast the

prevalence of and typical balances on credit cards, auto loans, mortgages, and student loans

across groups of consumers to illuminate how the financial situations of rural southerners

compare to and differ from those for consumers elsewhere. Moreover, we show these measures

for Persistent Poverty Counties (PPCs) within the rural southern region to highlight consumer

finance profiles of individuals in counties with persistently lower incomes.

10

We draw on the

CFPB’s Consumer Credit Panel (CCP), a comprehensive, national, 1-in-48 sample of de-

identified credit records maintained by one of the three nationwide consumer reporting agencies

(NCRAs). In doing so, we consider all open credit tradelines of consumers who appear in the

CCP sample at least once between the first quarter of 2020 and the first quarter of 2022.

11

For

Table 2 and subsequent tables, the sample size of unique consumer-level observations is as

follows: 64,776 in rural Persistent Poverty Counties in the southern region, 181,899 in the rural

southern region, 584,789 in non-southern region rural areas, and 5,734,997 for the national

average.

Table 2 shows the share of consumers in each region with an average credit score (over the

2020–2022 period) in each credit score category.

12

Compared with all consumers nationally, a

larger share of rural southerners have a deep subprime or subprime credit score (37 percent

compared to 26 percent), and a smaller share has a prime or super-prime score (49 percent

compared to 63 percent). These differences are more pronounced in rural Persistent Poverty

Counties in the southern region, where 42 percent of consumers have a deep subprime or

subprime credit score and only 43 percent have prime or super-prime credit scores. Likewise, as

shown in Table 3, among majority-minority census tracts in the region, there are differences

10

A Persistent Poverty County (PPC) is defined as any county or county equivalent that has had 20 percent or more of

its population living in poverty over the last 30 years, as measured by the decennial census.

11

For the purposes of this analysis, consumers in the panel without a census tract and consumers who reside in U.S.

territories (American Samoa, Puerto Rico, U.S. Virgin Islands, and Guam) were excluded from the sample. The time

period is chosen for comparability with the previous report on Consumer Finances in Rural Appalachia and includes

the effects of the COVID-19 pandemic and related emergency financial support efforts.

12

Credit scores are designed to help lenders assess potential borrowers’ credit risk. However, they may not always

accurately reflect an individual consumer’s likelihood to repay. For example, studies have found that a substantial

minority of consumers have errors on their credit reports with the three nationwide consumer reporting agencies

(CRAs), including errors substantial enough to meaningfully affect consumers’ credit scores. From October 2021 to

September 2022, the CFPB received nearly one million credit or consumer reporting complaints. The CFPB sent more

than 565,000 credit or consumer reporting complaints to companies for response. See CFPB, “Annual Report of

Credit and Consumer Reporting Complaints” (January 2023) available at https://www.consumerfinance.gov/data-

research/research-reports/annual-report-consumer-credit-reporting-complaints-analysis-of-complaint-responses-

equifax-experian-transunion-2022/

DATA POINT: CONSUMER FINANCES IN THE RURAL SOUTHERN REGION 10

between rural and non-rural areas. Low credit scores may hinder access to low-interest credit

products and increase the likelihood that a consumer uses higher-interest alternative financial

services such as payday, pawn, or auto title loans.

13

TABLE 2: PERCENT OF CONSUMERS IN EACH CREDIT SCORE GROUP IN THE RURAL SOUTHERN

REGION AND NATIONWIDE

Credit Score Group

Rural

PPCs in

southern

region

Rural

southern

region

Rural

non-

southern

region

Southern

Region

Nationwide

Deep Subprime 5 4 2 3 2

Subprime 37 32 22 28 22

Near Prime 15 14 12 13 12

Prime 28 31 35 34 37

Super-Prime 15 19 28 22 26

Note: Credit score categories are defined as: deep subprime (credit scores below 499), subprime (credit scores of 500-

599), near prime (credit scores of 600-659), prime (credit scores of 660-779) and super-prime (credit scores of 780 or

above). The southern region includes Alabama, Arkansas, Georgia, Louisiana, Mississippi, North Carolina, South

Carolina, and Tennessee. PPC stands for persistent poverty county. Source: CFPB CCP 2020–2022.

TABLE 3: PERCENT OF CONSUMERS IN EACH CREDIT SCORE GROUP IN MAJORITY-MINORITY

CENSUS TRACTS FOR SOUTHERN REGION AND NATIONWIDE

Rural Non-rural Non-

Credit Score Group

southern

majority-

southern

majority-

rural

southern

Southern

region

Nationwide

minority minority region

Deep Subprime 5 4 3 3 2

Subprime 40 32 27 28 22

Near Prime 16 14 13 13 12

Prime 26 33 34 34 37

Super-Prime 14 18 22 22 26

Note: Credit score categories are defined as: deep subprime (credit scores below 499), subprime (credit scores of 500-

599), near prime (credit scores of 600-659), prime (credit scores of 660-779) and super-prime (credit scores of 780 or

above). The southern region includes Alabama, Arkansas, Georgia, Louisiana, Mississippi, North Carolina, South

Carolina, and Tennessee. Source: CFPB CCP 2020–2022.

13

See for example Fulford and Shupe, “Consumer use of payday, auto title, and pawn loans: Insights from the Making

Ends Meet Survey” (May 2021) available at: https://www.consumerfinance.gov/data-

research/researchreports/consumer-use-of-payday-auto-title-and-pawn-loans-insights-making-ends-meet-survey/.

Data regarding use of payday, auto title and pawn loan usage stem from the Making Ends Meet survey. The CCP does

not contain this information.

DATA POINT: CONSUMER FINANCES IN THE RURAL SOUTHERN REGION 11

2.1 Credit Cards

Rural southerners are less likely than consumers nationally to have a general-purpose credit

card.

14

As shown in Table 4, only 67 percent of rural southerners, and 62 percent of rural

southerners living in Persistent Poverty Counties, have an open credit card, compared to 80

percent of consumers nationally. Rural southerners who do have credit cards typically have

lower balances. The median credit card balance among consumers in the rural south is 17

percent lower than the median for consumers nationwide, or $1,000 compared to $1,207.

The lower credit card balances observed in the rural south do not necessarily indicate lower debt

burdens. Average credit card utilization rates, defined as the total balance amount on a

consumer’s credit cards divided by their total credit limit, are notably higher in the region, at 38

percent in the rural south and 42 percent in rural southern Persistent Poverty Counties

compared to 31 percent nationwide. High utilization rates are one measure of potential financial

distress, and utilization rates above 30 percent may adversely impact credit scores.

15

Higher

utilization rates mean consumers have less credit available in case of an emergency or

unexpected expense.

TABLE 4: CREDIT CARD USAGE, IN THE RURAL SOUTHERN REGION AND NATIONWIDE

Rural Rural

Rural

PPCs in non-

southern Nationwide

southern southern

region

region region

Percent with credit card 62 67 75 80

Median balance on credit cards $890 $1,000 $1,121 $1,207

Mean utilization rate on credit cards 42 38 32 31

Percent with at least one credit card

delinquency over two-year period

21 18 13 14

Note: Median balance exclude accounts with $0 balances. The southern region includes Alabama, Arkansas, Georgia,

Louisiana, Mississippi, North Carolina, South Carolina, and Tennessee. PPC stands for persistent poverty county.

Source: CFPB CCP 2020–2022.

A more direct sign of financial distress is inability to make required payments on debt, or

delinquency. Eighteen percent of rural southerners were severely delinquent on one or more

credit cards between March 2020 and April 2022, four percentage points higher than the

national average. In rural southern Persistent Poverty Counties, the credit card delinquency rate

is 21 percent. Despite lower median balances, high utilization rates and high delinquency rates

14

In this report, we count authorized users as having a general purpose credit card.

15

See, e.g. Experian, “What is a Credit Utilization Rate?”, available at https://www.experian.com/blogs/ask-

experian/credit-education/score-basics/credit-utilization-rate/. Accessed March 1, 2023

DATA POINT: CONSUMER FINANCES IN THE RURAL SOUTHERN REGION 12

suggest that, on average, the burden of credit card debt is higher among rural southerners than

nationally.

Both perceived creditworthiness and general credit market conditions affect consumers’ ability

to access a credit card when they wish to borrow. The CCP allows us to measure the likelihood

that a consumer receives a credit card or a higher limit when they apply.

16

Figure 2 displays the

percent of credit card applications originated for consumers living in the rural south compared

to the national average. Because the likelihood of successful origination is highly dependent on

credit score, we show origination rates for the five standard credit score categories and for

unscored consumers. This controls, in part, for average differences in credit scores between

regions.

Analysis of data on credit card accounts (not shown) reveals that rural southerners who get

credit cards pay higher interest rates on average. Median interest rates on credit card accounts

in rural southern Persistent Poverty Counties (19.99 percent) are higher than in the rural

southern region as a whole (18.99 percent) or the national average (17.90 percent.) Consumers

generally pay interest on their credit card balances only if they do not pay the balance in full

each month. Credit card accounts that carry a balance from month to month are called revolving

accounts. Credit card accounts are also much more likely to be revolving in the rural south (64.5

percent) and thus subject to these interest rates, compared to the national average (56.2

percent.)

17

Nationally, 51 percent of credit card applications result in new credit in our data, compared to

40 percent in the rural southern region and 36 percent in rural southern Persistent Poverty

Counties.

18

This is partially explained by lower average credit scores among consumers in the

16

For most forms of credit, when a consumer submits an application, the lender will seek information about the

consumer from a nationwide credit reporting company. This is referred to as a “hard inquiry.” Hard inquiries are

visible on consumers’ credit reports and are one input into most credit scoring models. Most, but not all, hard

inquiries result from applications for a new account. For example, applications for a credit limit increase on an

existing account may also generate a hard inquiry. We define success as an inquiry that results in the opening of a

new, corresponding account or a limit increase of at least 5 percent within 14 days of the inquiry date. A consumer

may have several inquiries within this time period, with some successful. We take the average success rate for each

consumer between March 2020 and April 2022 and then average over all consumers in each region. If lenders deny a

credit application before initiating a hard inquiry, the inquiry will not appear in the CFPB’s Consumer Credit Panel

(CCP) and will not be counted as a failed origination in the success rates presented here. Furthermore, lenders do not

always send inquiries to all three NCRAs. Because the CCP includes data from only one of the three NCRAs, there are

likely to be additional applications not captured by our data.

17

We calculated the share of general purpose credit card accounts in the Federal Reserve Board’s Y-14 dataset that are

revolving divided by the total number of revolving and transacting accounts in November 2021. The Y-14 dataset

contains monthly bank holding companies with total consolidated assets exceeding $50 billion.

18

The overall origination rate, aggregated across credit score bins, can be obtained from the distribution of

consumers’ credit scores in a region, shown in Table 2, multiplied by the origination rates in Figure 2.

DATA POINT: CONSUMER FINANCES IN THE RURAL SOUTHERN REGION 13

rural southern region, as shown in Table 2.

19

However, Figure 2 shows that credit card

applications in the rural southern region are generally 3–5 percentage points less likely to be

approved than applications by consumers with similar credit scores the nationally across every

credit score tier. This difference means that rural southerners with subprime credit scores are

20 percent less likely to successfully obtain a credit card than consumers with subprime credit

scores nationwide. There are many potential explanations for this gap in success rates. Further

analysis to differentiate between these factors is beyond the scope of this report.

FIGURE 2: PERCENT OF CREDIT CARD APPLICATIONS ORIGINATED

Note: Credit score categories are defined as: deep subprime (credit scores below 499), subprime (credit scores of 500-

599), near prime (credit scores of 600-659), prime (credit scores of 660-779) and super-prime (credit scores of 780 or

above). People without a credit score were categorized as unscored. The southern region includes Alabama, Arkansas,

Georgia, Louisiana, Mississippi, North Carolina, South Carolina, and Tennessee. PPC stands for persistent poverty

county. Success rates are defined as the share of inquiries that result in the opening of a new, corresponding account

or a limit increase of at least 5 percent within 14 days of the inquiry date. Source: CFPB CCP March 2020-March

2022.

19

For example, if success rates in rural southern PPCs were equal to the national averages, the overall success rate

would be 41.4 percent, rather than 36 percent.

DATA POINT: CONSUMER FINANCES IN THE RURAL SOUTHERN REGION 14

2.2 Auto Loans

Forty-two percent of rural southerners and of the subset of those consumers living in Persistent

Poverty Counties have auto loans. This percentage is similar to that for consumers nationwide

but three percentage points lower than the percentage of consumers in other rural areas of the

U.S with an auto loan. As shown in Table 5, the median balance outstanding on auto loans for

rural southerners is a bit higher compared to consumers in other parts of the country.

20

However, because median incomes in the rural south are much lower than the national average,

the burden of auto loans may be comparatively higher for consumers in rural areas in the

southern region. The median auto loan balance as a percent of tract-level median income in the

rural south, for example, is 40 percent compared to 26 percent nationwide. In rural southern

Persistent Poverty Counties, the median ratio rises to 46 percent. This means that in southern

rural Persistent Poverty Counties, the median auto loan balance is nearly half of median

household income.

Relatively high delinquency rates may also indicate that that auto loans are more likely to pose a

financial burden for rural consumers in the region. Consumers with auto loans in rural southern

Persistent Poverty Counties are almost twice as likely to be more than 60 days delinquent on at

least one auto loan than consumers nationwide (20 percent compared to 11 percent.) In the rural

southern region as a whole, 16 percent of consumers with auto loans had a severe delinquency

between March 2020 and April 2022.

TABLE 5: AUTO LOANS, IN THE RURAL SOUTHERN REGION AND NATIONWIDE

Rural Rural

Rural

PPCs in non-

southern Nationwide

southern southern

region

region region

Percent with auto loan 42 42 45 42

Median balance on auto loan

Median tract-level household income

among consumers with an auto loan

Ratio of median auto loan balance to

tract median household income in

$14,792

$38,443

46

$14,496

$43,917

40

$13,450

$53,800

31

$13,249

$71,687

26

percent

20

Most auto lenders furnish to the nationwide credit reporting agencies. However, many small finance companies

and Buy-Here-Pay-Here dealerships do not. Therefore, the estimated share of consumers with an auto loan is likely

underestimated using only the information in the CCP. Small finance companies and Buy-Here-Pay-Here dealerships

are more likely to serve subprime consumers, we are especially likely to underestimate subprime and deep subprime

auto loans. For more information, see Clarkberg, Gardner, and Low, “Data Point: Subprime Auto Loan Outcomes by

Lender Type” (September 2021) available at https://files.consumerfinance.gov/f/documents/cfpb_subprime-

auto_data-point_2021-09.pdf

DATA POINT: CONSUMER FINANCES IN THE RURAL SOUTHERN REGION 15

Rural Rural

Rural

PPCs in non-

southern Nationwide

southern southern

region

region region

Percent with a delinquency on auto

20 16 10 11

loan over a two-year period

Note: The southern region includes Alabama, Arkansas, Georgia, Louisiana, Mississippi, North Carolina, South

Carolina, and Tennessee. PPC stands for persistent poverty county. Source: CFPB CCP 2020–2022.

DATA POINT: CONSUMER FINANCES IN THE RURAL SOUTHERN REGION 16

Figure 3 displays the percent of auto loan applications from people living in the region that were

successfully originated compared to the national average.

21

Among consumers with the highest

credit scores, origination rates in the rural south are similar to rates nationwide. However,

consumers with subprime or deep subprime credit scores are 19 to 24 percent less likely to

successfully originate an auto loan in the rural south compared to the national average. For

additional analysis by majority-minority Census tract, see Appendix A. Due to longer commutes

and a lack of alternative transit infrastructure compared to urban dwellers, many rural

southerners remain highly dependent on personal vehicles for transportation, and may

therefore be particularly impacted by difficulty obtaining an auto loan.

FIGURE 3: PERCENT OF AUTO LOAN APPLICATIONS ORIGINATED

Note: Credit score categories are defined as: deep subprime (credit scores below 499), subprime (credit scores of 500-

599), near prime (credit scores of 600-659), prime (credit scores of 660-779) and super-prime (credit scores of 780 or

above). People without a credit score were categorized as unscored. The southern region includes Alabama, Arkansas,

Georgia, Louisiana, Mississippi, North Carolina, South Carolina, and Tennessee. PPC stands for persistent poverty

county. Source: CFPB CCP March 2020-2022.

21

If lenders deny a credit application before initiating a hard inquiry, the inquiry will not appear in the CFPB’s

Consumer Credit Panel (CCP) and will not be counted as a failed origination in the success rates presented here.

Furthermore, lenders do not always send inquiries to all three NCRAs. Because the CCP includes data from only one

of the three NCRAs, there are likely to be additional applications not captured by our data.

DATA POINT: CONSUMER FINANCES IN THE RURAL SOUTHERN REGION 17

2.3 Home Loans

Most consumers, particularly low- and middle-income consumers, cannot purchase a home with

cash up front and therefore need to finance their home purchase through mortgages. Rural

southerners are less likely to have a first-lien mortgage than consumers nationally.

22

Nineteen

percent of consumers in rural southern Persistent Poverty Counties and 23 percent of rural

southerners have a first-lien mortgage, compared to 29 percent of consumers nationally and 28

percent in other rural areas. This may be partially explained by a higher share of rural

southerners who have paid off their mortgages. Slightly fewer rural southerners (70 percent) live

in owner-occupied housing than consumers in rural areas outside the southern region (73

percent.) Among consumers with a first-lien mortgage, the median mortgage balance in the

rural southern region is slightly lower than the median balance in other rural areas ($95,790

compared to $103,489.) Unlike with auto loans, mortgage debt balances relative to income do

not appear to be much higher in the rural southern region. The median first-lien mortgage

balance as a percent of tract-level median income in the region (257 percent) is less than the

national average (268 percent), but greater than in other rural areas (233 percent). However,

other measures of mortgage debt burden, such as delinquency rates, are higher in the rural

south. For example, consumers in rural southern Persistent Poverty Counties are twice as likely

to be delinquent on their mortgage as rural consumers outside the southern region.

23

TABLE 6: FIRST-LIEN MORTGAGES, IN THE RURAL SOUTHERN REGION AND NATIONWIDE

Rural Rural

Rural

PPCs in non-

southern Nationwide

southern southern

region

region region

Percent with mortgage 19 23 28 29

Median balance on mortgage $76,627 $95,790 $103,489 $165,975

Median tract-level household

income among consumers with a $40,117 $46,189 $56,169 $79,862

mortgage

Ratio of median mortgage balance to

median income (percent)

251 257 233 268

22

A first-lien mortgage loan is paid first in the event of default, and a second-lien or “subordinated” loan is paid out

only if there is money left over after paying off the first-lien mortgage. Typically, home purchase loans are first-lien

mortgages and other mortgage products such as home equity loans are not. It is possible to use a second-lien

mortgage to finance a down payment for home purchase and mortgage products like home equity loans or HELOCs

may be first-lien if the first mortgage has been paid off.

23

This data covers the period from 2020-2022 and therefore reflects the challenges of the pandemic as well as the

flow of pandemic relief to historically underserved and rural areas. Many of the Housing Assistance Fund programs

administered by the states for homeowners behind on mortgage payments due to the pandemic did not begin

receiving applications until early 2022 and therefore may not be fully reflected in this report.

DATA POINT: CONSUMER FINANCES IN THE RURAL SOUTHERN REGION 18

Rural Rural

Rural

PPCs in non-

southern Nationwide

southern southern

region

region region

Percent with a mortgage delinquency

6 4 3 2

over a two-year period

Note: The southern region includes Alabama, Arkansas, Georgia, Louisiana, Mississippi, North Carolina, South

Carolina, and Tennessee. PPC stands for persistent poverty county. Source: CFPB CCP 2020–2022.

We examine differences in mortgage interest rates and the share of manufactured home loans

more fully using data from the Home Mortgage Disclosure Act (HMDA) for the most recent year

available, 2021.

24

For further analysis and discussion of mortgage lending in the southern

region, see the CFPB’s report on banking and credit access in the South.

25

Rural southerners

who take out mortgages tend to pay higher rates than consumers elsewhere. In 2021, the mean

interest rate for a home purchase loan in rural southern Persistent Poverty Counties was 3.942

percent, compared to 3.127 percent nationally. The difference in median interest rates is much

smaller (25 basis points), which indicates that the distribution of interest rates has a long right

tail, with some consumers paying much higher interest rates than the median mortgage holder.

TABLE 7: HOME PURCHASE MORTGAGE APPLICATIONS IN 2021, IN THE RURAL SOUTHERN REGION

AND NATIONWIDE

Rural Rural

Rural

PPCs in non-

southern Nationwide

southern southern

region

region region

Total mortgage applications for home

purchase

65,011 206,133 555,446 6,334,679

Total mortgage applications for home

purchase per 1,000 residents

16 19 16 19

Median interest rate 3.250 3.125 3.125 3.000

Mean interest rate 3.942 3.512 3.262 3.127

Percent originated 44 55 67 71

Percent denied 39 27 15 11

Percent of originations that are

manufactured homes (home and land 5 9 10 3

secured)

24

For more information on this dataset, see Liu, Jo, Skhirtladze, and Barriere, “An Updated Review of the New and

Revised Data Points in HMDA,” (August 2020), available at

https://files.consumerfinance.gov/f/documents/cfpb_data-points_updated-review-hmda_report.pdf.

25

See CFPB, “Banking and Credit Access in the Southern Region of the U.S.,” (June 2023).

DATA POINT: CONSUMER FINANCES IN THE RURAL SOUTHERN REGION 19

Rural Rural

Rural

PPCs in non-

southern Nationwide

southern southern

region

region region

Percent of originations that are

manufactured homes (only home 6 7 3 1

secured)

Note: All rows refer to loans for home purchases and exclude refinance applications. The southern region includes

Alabama, Arkansas, Georgia, Louisiana, Mississippi, North Carolina, South Carolina, and Tennessee. PPC stands for

persistent poverty county. Source: HMDA 2021.

As is the case for other credit markets, perceived creditworthiness and general credit market

conditions influence the share of home loan applications that are originated or denied as well as

the interest rate paid when originated. In the mortgage market, these measures are also affected

by characteristics of the product itself, such as the loan-to-value ratio of the property, the

duration of the loan, the type of property. It is important to note that the numbers displayed in

Table 7 are unconditional and do not account for important differences in these factors.

26

Additionally, HMDA data do not capture certain types of alternative home financing such as

seller-financing, land contracts, or lease-to-own arrangements, which are disproportionately

used by low-income consumers.

27

Mortgage borrowers in the rural southern region are four times more likely to get mortgages for

manufactured homes than mortgage borrowers nationwide (16 percent compared to 4 percent.)

The share of home-only (chattel) loans, for which the land underneath the home is not used as

collateral, is seven times higher in the rural southern region (7 percent compared to 1 percent.)

These loans tend to be much more expensive than other mortgages.

28

Furthermore, many of

these homeowners rent the land where their home is located, making them vulnerable to both

repossession by the lender and rent hikes or eviction by the owner of the land. Consumers can

26

While the HMDA data contain information about many of these variables, further analysis controlling for these

factors is beyond the scope of this report.

27

Among consumers who have ever borrowed to buy a home, an estimated six percent had used a lease-purchase

(rent-to-own) agreement, six percent had used a seller-financed mortgage, five percent had used a land contract, and

11 percent had used a home-only loan. See The Pew Charitable Trusts, “Millions of Americans Have Used Risky

Financing Arrangements to Buy Homes,” (April 2022), available www.pewtrusts.org/-

/media/assets/2022/05/millionsofamericanshaveusedriskyfinancing_brief.pdf

28

Manufactured homes are factory-built housing constructed after June 15, 1976 in accordance with the U.S.

Department of Housing and Urban Development’s Manufactured Home Construction and Safety Standards codes.

Manufactured homes are distinct from RVs, park model homes, and modular home sections. See Russell, O’Reilly,

Schneider, Melton, Schwartz and Leitner, “Manufactured Housing Finance: New Insights from the Home Mortgage

Disclosure Act Data,” (May 2021), available at https://www.consumerfinance.gov/data-

research/researchreports/manufactured-housing-finance-new-insights-hmda/ and “Manufactured-housing

consumer finance in the United States,” available at

https://files.consumerfinance.gov/f/201409_cfpb_report_manufactured-housing.pdf.

DATA POINT: CONSUMER FINANCES IN THE RURAL SOUTHERN REGION 20

lose their home if they fall behind on their lot rent and lack the means to move their home to a

new location.

2.4 Student Loans

Eighteen percent of consumers nationwide have an open student loan compared to 15 percent

within the rural south. The ratio of consumers with a student loan to residents with at least

some college education is slightly higher in the rural southern region (32 percent) than for the

nation as a whole (29 percent). For those that do have student loan debt, the following analysis

shows it may be more of a burden for those in the rural southern region than nationally,

particularly when looking at balance-to-income ratios, delinquency rates, and lower levels of

accessing relief options such as income driven relief (IDR) plans.

Table 8 displays the characteristics of student loan borrowers in the rural south and nationally.

Due to payment suspensions during the pandemic, this analysis focuses on all student loan

borrowers as of February 2020, prior to the enactment of the CARES Act.

29

Table 8 provides a

baseline for several measures that are correlated with the ability of borrowers to repay their

loans after the measures end.

30

TABLE 8: STUDENT LOAN BORROWERS AS OF MARCH 2020, IN THE RURAL SOUTHERN REGION AND

NATIONWIDE

Rural Rural

Rural

PPCs in non-

southern Nationwide

southern southern

region

region region

Median scheduled monthly student

loan payment

$151 $157 $169 $192

Median remaining student loan

balance

$18,233 $17,499 $17,231 $20,286

Median tract-level household annual

income

$37,230 $42,780 $53,718 $71,017

Student loan balance as a percent of

tract-level income (median)

59 52 44 43

29

While federal student loans comprise the majority of student loans, the credit bureau data do not allow us to

distinguish between federally held and privately held student loans. The latter did not necessarily benefit from the

payment suspensions afforded to federal student loans. However, we do not expect the inclusion of some privately

held student loans to substantially impact this analysis.

30

For more information on student loan borrowers and the construction of these measures, see Conkling, Gibbs and

Jimenez-Read, “Student Loan Borrowers Potentially At-Risk when Payment Suspension Ends,” (April 2022) available

at: https://files.consumerfinance.gov/f/documents/cfpb_cares-vulnerable-student-loan-borrowers_report_2022-

04.pdf (hereinafter Conkling, Gibbs and Jimenez-Read 2022).

DATA POINT: CONSUMER FINANCES IN THE RURAL SOUTHERN REGION 21

Rural Rural

Rural

PPCs in non-

southern Nationwide

southern southern

region

region region

Percent of borrowers delinquent 11 9 7 7

Median balance if delinquent $19,566 $19,766 $22,202 $25,089

Percent of borrowers in default 16 14 10 9

Percent receiving assistance

through IDR

20 19 21 21

Note: For this table, the sample is restricted to borrowers with outstanding student loans in February 2020. Median

scheduled monthly payments exclude borrowers who have defaulted or have deferred payments. Delinquencies are

defined as at least 90 days past due but not yet in default. Delinquency and default are measured for a single month,

not cumulatively. Median balances exclude accounts with $0 balances. Receiving assistance excludes accounts with a

remaining $0 balance. The CCP does not contain consumer-level income information. The southern region includes

Alabama, Arkansas, Georgia, Louisiana, Mississippi, North Carolina, South Carolina, and Tennessee. PPC stands for

persistent poverty county. Sample size refers to the number of unique consumer observations.

Student loan borrowers in the rural south have lower monthly payments and delinquent balance

amounts than the respective national averages. Student loan borrowers in rural parts of the

southern region, especially those in Persistent Poverty Counties, however, tend to live in tracts

with lower median incomes. Consequently, these borrowers face a much higher student loan

debt burden. The median ratio of student loan balances to tract-level household annual income

is 52 percent in the rural south compared to 43 percent for consumers nationally. Comparatively

high rates of delinquency and default on student loans among rural southerners also potentially

point to greater student-loan debt burdens in the region. Meanwhile, rural southern student

loan borrowers are slightly less likely to be on income-driven repayment (IDR) plans before the

pandemic and subsequent relief measures.

31

The combination of these factors indicates that, relative to both student loan borrowers

nationally and to borrowers in non-southern rural counties, consumers in the rural south may

have a harder time meeting their payment obligations when pandemic relief policies end.

31

Payment assistance refers to borrowers who are likely enrolled in an income-driven repayment (IDR) plan (See

Conkling, Gibbs and Jimenez-Read 2022).

DATA POINT: CONSUMER FINANCES IN THE RURAL SOUTHERN REGION 22

3. Consumer Distress and

Delinquencies

3.1 Medical Collections

Medical debts are the most common type of third-party collection furnished on consumers’

credit reports.

32

Such collections can adversely affect a consumer’s ability to access financial

products, housing, or employment. In March 2022, in response to concerns of erroneous

reporting of medical debt and the consequences for consumers, Equifax, Experian, and

TransUnion announced their decision to stop reporting certain types of medical debt on credit

reports, to be implemented over time and completed in April 2023. This entailed not reporting

medical bills until they are one year past due (compared to 180 days previously), removing paid

medical collections entirely, and no longer reporting medical debt tradelines under $500.

33

A 2022 CFPB publication explored the impact these changes may have on consumers nationally

and found that about half of consumers with medical collection tradelines will have all of them

removed. Moreover, the removals will be concentrated geographically. South Carolina had the

second-highest per-capita share of medical collections to be removed, following West Virginia.

34

Moreover, the southern region has the highest percentage of individuals with medical debt in

collections.

35

Rural southerners are also more likely to have paid off medical debt or collections

less than $500 than consumers nationwide. A 2023 CFPB publication finds that removing

medical collections from a consumer’s credit report increases their credit score by 25 points on

average, leading to expanded access to credit at a lower cost.

36

32

See Sandler and Nathe “Consumer Credit Trends: Paid and Low-Balance Medical Collections on Consumer Credit

Reports,” (July 2022), available at https://www.consumerfinance.gov/data-research/research-reports/paid-and-

low-balance-medical-collections-on-consumer-credit-reports/ (hereinafter Sandler and Nathe 2022).

33

See “Equifax, Experian, and TransUnion Support U.S. Consumers with Changes to Medical Collection Debt

Reporting”, March 18. 2022., Press Release. Available at https://newsroom.transunion.com/equifax-experian-

andtransunion-support-us-consumers-with-changes-to-medical-collection-debt-reporting/.

34

See Sandler and Nathe 2022

35

See Figure 3 in “Medical Debt Burden in the United States,” (March 2023), available at

https://files.consumerfinance.gov/f/documents/cfpb_medical-debt-burden-in-the-united-states_report_2022-

03.pdf.

36

See Brown and Wilson, “Data Point: Consumer Credit and the Removal of Medical Collections from Credit

Reports,” (April 2023), available at https://files.consumerfinance.gov/f/documents/cfpb_consumer-credit-removal-

medical-collections-from-credit-reports_2023-04.pdf

DATA POINT: CONSUMER FINANCES IN THE RURAL SOUTHERN REGION 23

TABLE 9: MEDICAL COLLECTIONS, IN THE RURAL SOUTHERN REGION AND NATIONWIDE

Rural

PPCs in

southern

region

Rural

southern

region

Rural non-

southern Na

region

tionwide

Percent with medical debt

collection over a two-year 29 28 19 17

period

Percent with any medical

debt collection paid or less

than $500 over a two-year

20 20 15 12

period

Note: The southern region includes Alabama, Arkansas, Georgia, Louisiana, Mississippi, North Carolina, South

Carolina, and Tennessee. PPC stands for persistent poverty county. NCRAs are expected to remove paid medical debt

as well as that with an initial balance below at least $500 from credit reports in 2023. Source: CCP 2020–2022.

An above-average share of consumers in the rural south (28 percent), and, in particular, in rural

southern Persistent Poverty Counties (29 percent), has at least one medical collection on their

credit record over a two-year period. This share is only 17 percent on average for consumers

nationally and 19 percent among rural consumers outside of the southern region. The share of

rural consumers with a medical collection tradeline varies widely among states in the southern

region, 34 percent of rural South Carolinians have a medical debt collection tradeline, over 41

percent more than the share of rural consumers with a medical collection in Mississippi (24

percent.) This means that all eight states in the rural southern region have a higher share of

consumers with medical collections than the national average or rural areas outside the

southern region.

Table 9 shows that, compared to consumers nationally, a greater share of consumers in the rural

south may have at least one medical collection removed from their credit records. Twenty

percent of consumers in both the rural southern region and in rural Persistent Poverty Counties

in the southern region will likely see at least one medical collection removed from their credit

report as part of the nationwide credit reporting agencies’ plan to exclude paid medical

collections and reported medical collections less than $500 as it is implemented. This share is

five percentage points higher than in other rural areas across the country and 8 percentage

points higher than the national average (12 percent). This appears to be driven primarily by the

higher prevalence of medical collections in the rural southern region, not a higher share of

consumers with medical collections benefiting from the changes. Seventy-one percent (20

percent out of 28 percent) of rural southerners with medical collections will have at least one

medical collection record removed. This is comparable to the national average, and much lower

than the share of rural consumers with medical collections outside the southern region who will

benefit (79 percent.)

DATA POINT: CONSUMER FINANCES IN THE RURAL SOUTHERN REGION 24

We display the relative importance of medical collection removals for consumers in the southern

region at the county level in Figure 4. The figure shows the share of consumers who are likely to

have at least one collection removed from their credit reports in each county, either because the

medical collection had been paid or it was less than $500, relative to the national average of 12

percent.

37

The share of consumers with at least one reported medical collection that would be

removed is more than 150 percent of the national average in southern counties and almost all

counties in South Carolina. One reason for the large share of removals in South Carolina is that

South Carolina has the second highest share (behind West Virginia) of consumers with at least

one medical collection on their credit report.

FIGURE 4: RELATIVE SHARE OF CONSUMERS WITH LIKELY MEDICAL COLLECTIONS REMOVALS FROM

CREDIT REPORTS

Note: The southern region includes Alabama, Arkansas, Georgia, Louisiana, Mississippi, North Carolina, South

Carolina, and Tennessee. CCP 2020–2022.

3.2 Consumer Delinquencies

Consumers who have trouble paying for a bill or expense often have multiple financial

difficulties. We investigate the likelihood that consumers in the southern region who have one

type of delinquency also have a delinquency on a consumer debt of another kind. Figure 5 shows

these likelihoods for consumers in the rural southern region, which look similar to those of

37

Specifically, we calculate the share of consumers in each county who will have at least one collection removed

divided by the national share. Removals include previous collections that are paid in full as of March 2022 and

collections with an initial balance less than $500. However, removals are primarily driven by collections with an

initial balance of less than $500, as most medical collections nationally and in the southern region remain unpaid.

The policies of medical providers may drive differences in the share of collections furnished to credit reporting

companies.

DATA POINT: CONSUMER FINANCES IN THE RURAL SOUTHERN REGION 25

consumers nationally (not shown). Among rural southerners who have each type of tradeline

(medical collection, mortgage, student loan, auto loan, and credit card), the y-axis labels show

the percent who also had at least one severe delinquency in the corresponding loan type between

March 2020 and April 2022.

38

FIGURE 5: SHARE OF RURAL SOUTHERN CONSUMERS WITH MEDICAL DEBT OR DELINQUENCY ON

VARIOUS TYPES OF CREDIT

Note: Delinquencies are defined as loans at least 60 days past due, charged-off, or in collection at least once over the

period of March 2020-April 2022. All percentages are conditional on the consumer having that type of loan except

medical collections, due to a lack of data on who has medical debt. For consistency with the other loan types, the

definition of student loan delinquency differs here from what we present in Table 8. Notably, our definition of student

loan delinquency here includes loans that are in default. The southern region includes Alabama, Arkansas, Georgia,

Louisiana, Mississippi, North Carolina, South Carolina, and Tennessee. Source: CFPB CCP.

Overall, rural southern consumers are most likely to have a reported medical collection (at 28

percent) compared to other types of delinquencies. Among borrowers with the corresponding

type of debt, the next most prevalent delinquency categories are student loans (21 percent) and

credit cards (18 percent). Each row corresponds to the sample of borrowers with a delinquency

38

We report only delinquencies of more than 60 days, collections, and charge-offs in order to highlight severe

delinquencies that are more substantial than an occasional missed payment of a few days. These delinquencies may

include those on active accounts as well as closed accounts and those that have been charged off and remain on the

consumer’s credit record.

DATA POINT: CONSUMER FINANCES IN THE RURAL SOUTHERN REGION 26

of the loan type indicated on the y-axis, and each cell contains the percentage of this sample with

an additional delinquency, corresponding to the type indicated on the x-axis.

Rural southerners are considerably more likely to have a medical collection on their credit

report (28 percent) compared to consumers nationally (17 percent, Table 9). Those with a

medical collection have a dramatically higher prevalence of other types of delinquencies on their

credit accounts. For example, Figure 5 shows that 18 percent of credit card holders in the rural

southern region have a delinquency on at least one credit card account. However, among credit

card holders with a reported medical collection, the delinquency rate is 38 percent.

39

We cannot

distinguish whether having a reported medical collection leads to higher rates of credit card

delinquency or whether consumers with medical collections are also consumers who would

otherwise have relatively high credit card delinquency rates.

Similarly, the mortgage delinquency rate among mortgage holders in the rural south is only four

percent; however, among those with a medical collection tradeline, the rate is over twice as high,

at 10 percent. This pattern is even starker for those with a reported medical collection and an

auto loan or student loan. While 16 percent of rural southerners with auto loans had at least one

severe delinquency on an auto loan between March 2020 and April 2022, those with a medical

collection tradeline have a 33 percent rate of auto loan delinquency, and while 21 percent of

consumers with student loans are delinquent in the same region, those with a medical collection

tradeline had a 36 percent rate of student loan delinquency.

Delinquency rates on other kinds of loan products are even higher among consumers with an

auto loan delinquency. For example, 20 percent of consumers with an auto loan delinquency

also had a mortgage delinquency, nearly five times higher than the overall mortgage

delinquency rate (4 percent). Among those with an auto delinquency and a credit card, the share

with a credit card delinquency is 58 percent, over three times the credit card delinquency rate

for all consumers in the sample (18 percent). Likewise, the share of student loan borrowers with

a delinquency is 21 percent, but among borrowers with a delinquent auto loan, the student loan

delinquency rate is 38 percent.

39

We use delinquency rate here to refer to the percent of consumers with at least one delinquency, rather than the

share of accounts or balances that are delinquent.

DATA POINT: CONSUMER FINANCES IN THE RURAL SOUTHERN REGION 27

4. Conclusion

The findings above present an initial overview of the consumer finances of rural southerners and

is intended to start a conversation with stakeholders in the region about priorities for further

research and policy development. Key findings include:

Compared to the nation as a whole, rural southerners are 10.6 percent less likely to have

a credit card and 17.9 percent less likely to have an outstanding mortgage. These gaps

may partially reflect relatively lower likelihoods of successfully taking out credit, even

within credit score tiers. Without adequate access to these products, consumers may

experience increased difficulty responding to unexpected expenses or building wealth

through home equity.

Across credit products, rural southerners who obtain credit tend to pay higher interest

rates on average. In rural parts of the southern region, the average interest rate on a

mortgage was 3.51 percent, compared to 3.13 percent nationally. For credit cards, the

median interest rate in the region’s rural areas is 18.99 percent, compared to 17.74

percent in other rural areas and 17.90 percent nationwide.

Rural southerners are more likely to have medical collections (28 percent) than

consumers elsewhere (17 percent). The prevalence of medical collections varies widely

among states in the southern region, 34 percent of rural South Carolinians have a

medical debt collection tradeline, over 41 percent more than the share of rural

consumers with a medical collection in Mississippi (24 percent).

Medical collections are the most common type of delinquency in the rural southern

region, followed by student loans (21 percent) and credit cards (18 percent). Rural

southerners with medical collections are much more likely to be delinquent on other

types of debt. For example, 16 percent of rural southerners with an auto loan were at

least 60 days delinquent at some point over a two-year period. For those with medical

collections, the auto loan two-year delinquency rate more than doubles, to 33 percent.

This report is intended to provide a starting point in better understanding the financial

situations, needs, and challenges of consumers in rural areas in the southern region. The CFPB

continues to monitor credit conditions in rural southern region and other areas within the

United States of America.

DATA POINT: CONSUMER FINANCES IN THE RURAL SOUTHERN REGION 28

APPENDIX A: AUTO ORIGINATIONS IN MAJORITY-

MINORITY CENSUS TRACTS

FIGURE 6: PERCENT OF AUTO LOAN APPLICATIONS ORIGINATED

Note: Credit score categories are defined as: deep subprime (credit scores below 499), subprime (credit scores of 500-

599), near prime (credit scores of 600-659), prime (credit scores of 660-779) and super-prime (credit scores of 780 or

above). People without a credit score were categorized as unscored. The southern region includes Alabama, Arkansas,

Georgia, Louisiana, Mississippi, North Carolina, South Carolina, and Tennessee. PPC stands for persistent poverty

county. Source: CFPB CCP March 2020-2022.

DATA POINT: CONSUMER FINANCES IN THE RURAL SOUTHERN REGION 29

Consumer Financial

Protection Bureau

Learn more at consumernance.gov

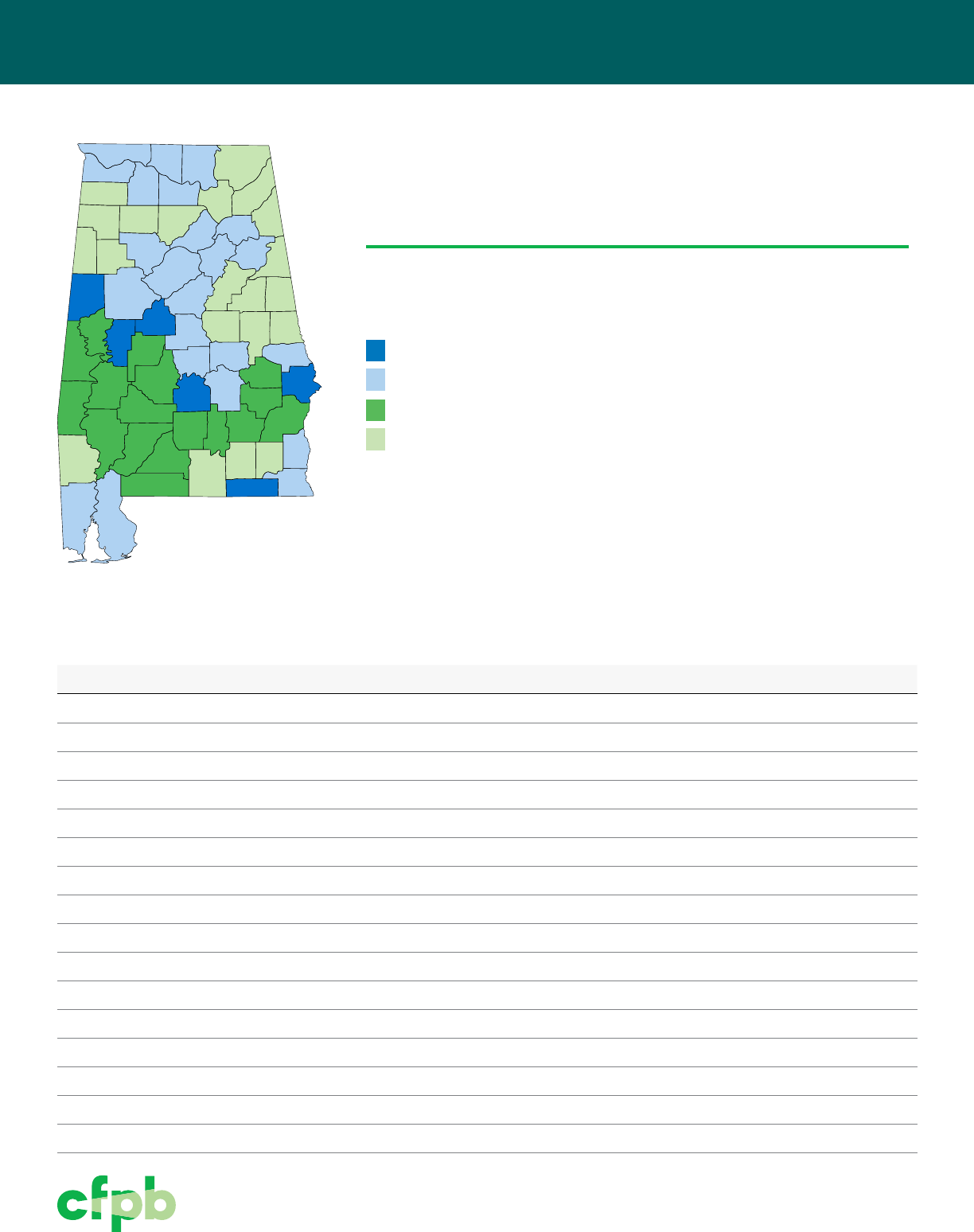

ALABAMA

CONSUMER FINANCES IN RURAL AREAS OF THE SOUTHERN REGION

Alabama

Map of counties in Alabama.

Metro PPC

*

Metro, non-PPC

Rural PPC

Rural, non-PPC

*

persistent poverty county

Consumer credit proles in the southern region in comparison: Alabama.

Credit characteristic National average Alabama Rural Alabama

Percent with mortgage 29 27 22

Median balance on mortgage $165,975 $124,220 $88,831

Percent with credit card (cc) 80 71 66

Median balance on cc $1,207 $1,117 $980

Utilization rate (cc) 31 37 41

Percent with auto loan 42 43 43

Median balance on auto loan $13,249 $14,415 $14,533

Percent with student loan 18 18 14

Percent w/ medical debt collection 17 22 25

Median household income $63,929 $50,833 $41,603

Deep subprime 4 6 6

Subprime 22 29 32

Near prime 12 13 15

Prime 37 32 30

Super-prime 26 20 17

Observations 5,734,997 88,659 19,773

CONSUMER FINANCES IN RURAL AREAS OF THE SOUTHERN REGION

Consumer Financial

Protection Bureau

Learn more at consumernance.gov

ALABAMA

CONSUMER FINANCES IN RURAL AREAS OF THE SOUTHERN REGION

Share of rural southern consumers in Alabama with delinquencies on multiple types

of credit.

Percent

100

90

80

70

60

50

40

30

20

10

0

38 37 40 13

57 47 12 31

51 37 6 42

61 36 24 41

39 32 14 32

Mortgage

Mortgage

(4%)

Medical

collection

Medical

collection

(25%)

(19%)

Student loan

Student

loan

(17%)

Auto loan

Auto loan

(19%)

Credit card

Credit card

Also had this kind of delinquency

Consumers who had

this kind of delinquency

Relative share of consumers with likely

medical debt collections removals from

credit report.

Below national average

1-50% above national average

More than 50% above

national average

CONSUMER FINANCES IN RURAL AREAS OF THE SOUTHERN REGION

Consumer Financial

Protection Bureau

Learn more at consumernance.gov

Rural Alabama

National average

ALABAMA

CONSUMER FINANCES IN RURAL AREAS OF THE SOUTHERN REGION

Student loan borrowers in Alabama.

Credit characteristic National average Alabama Rural Alabama

Median scheduled monthly student loan

payment

$192 $175 $156

Median annual household income $71,017 $56,550 $41,604

Median student loan debt balance to

income

43 56 64

Share delinquent 7 8 8

Median balance if delinquent $25,089 $27, 336 $26,434

Share in default 9 12 13

Share receiving assistance through IDR

*

21 21 18

Observations 917, 310 13,906 2,408

*

Income-driven repayment

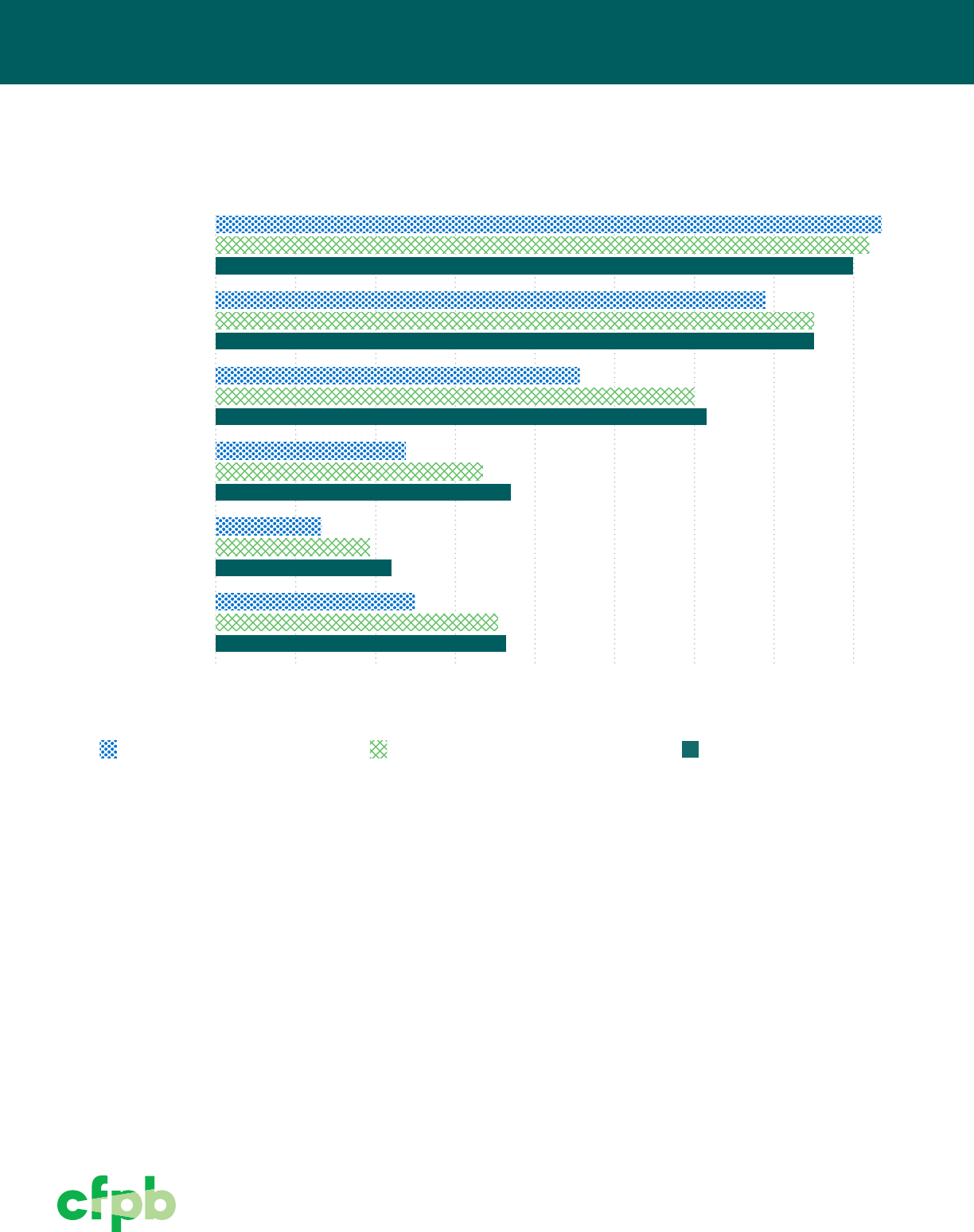

Percent of applications originated for credit cards and auto loans,

rural Alabama vs. national average.

Credit card

Success rate %

Credit score

prole

0 20 40 60 80

Super-prime

Prime

Near prime

Subprime

Deep subprime

Unscored

69

72

56

61

36

40

16

20

3

6

14

26

Auto loans

Success rate %

Credit score

prole

0 20 40 60 80

Super-prime

Prime

Near prime

Subprime

Deep subprime

Unscored

82

74

51

27

15

27

80

75

61

37

21

39

CONSUMER FINANCES IN RURAL AREAS OF THE SOUTHERN REGION

Consumer Financial

Protection Bureau

Learn more at consumernance.gov

Credit score prole

ALABAMA

CONSUMER FINANCES IN RURAL AREAS OF THE SOUTHERN REGION

Auto loan application acceptance rates in Alabama, by credit score.

Auto loans

Success rate %

0 20 40 60 80

Super-prime

Prime

Near prime

Subprime

Deep subprime

Unscored

AL majority-minority

census tracts

AL non-majority-minority

census tracts

National average

75

67

49

27

17

23

33

38

17

21

32

37

58

61

74

75

81

80

CONSUMER FINANCES IN RURAL AREAS OF THE SOUTHERN REGION

Consumer Financial

Protection Bureau

Learn more at consumernance.gov

ARKANSAS

Arkansas

Metro PPC

*

Metro, non-PPC

Rural PPC

Rural, non-PPC

*

persistent poverty county

Map of counties in Arkansas.

Consumer credit proles in the southern region in comparison: Arkansas.

Credit characteristic National average Arkansas Rural Arkansas

Percent with mortgage 29 27 23

Median balance on mortgage $165,975 $112,171 $81,769

Percent with credit card (cc) 80 72 68

Median balance on cc $1,207 $1,082 $981

Utilization rate (cc) 31 38 39

Percent with auto loan 42 47 46

Median balance on auto loan $13,249 $14,786 $14,633

Percent with student loan 18 18 15

Percent w/ medical debt collection 17 23 27

Median household income $63,929 $48,724 $41,574

Deep subprime 4 5 5

Subprime 22 29 31

Near prime 12 13 14

Prime 37 32 30

Super-prime 26 20 20

Observations 5,734,997 52,716 19,043

CONSUMER FINANCES IN RURAL AREAS OF THE SOUTHERN REGION

Consumer Financial

Protection Bureau

Learn more at consumernance.gov

ARKANSAS

Share of rural southern consumers in Arkansas with delinquencies on multiple types

of credit.

Percent

100

90

80

70

60

50

40

30

20

10

0

39 36 35 8

65 38 41 36

47 42 13 48

60 38 16 46

37 29 13 35

Mortgage

Mortgage

(4%)

Medical

collection

Medical

collection

(27%)

(22%)

Student loan

Student

loan

(17%)

Auto loan

Auto loan

(19%)

Credit card

Credit card

Also had this kind of delinquency

Consumers who had

this kind of delinquency

Relative share of consumers

with likely medical debt

collections removals from

credit report.

Below national average

1-50% above national average

More than 50% above

national average

CONSUMER FINANCES IN RURAL AREAS OF THE SOUTHERN REGION

Consumer Financial

Protection Bureau

Learn more at consumernance.gov

ARKANSAS

Student loan borrowers in Arkansas.

Credit characteristic National average Arkansas Rural Arkansas

Median scheduled monthly student loan

payment

$192 $166 $140

Median annual household income $71,017 $52,301 $41,794

Median student loan debt balance to

income

43 47 37

Share delinquent 7 9 9

Median balance if delinquent $25,089 $21,027 $15,117

Share in default 9 12 15

Share receiving assistance through IDR

*

21 20 18

Observations 917, 310 8,560 2,487

*

Income-driven repayment

Percent of applications originated for credit cards and auto loans,

rural Arkansas vs. national average.

Credit card

Success rate %

Credit score

prole

C

0 20 40 60 80

Super-prime

Prime

Near prime

Subprime

Deep subprime

Unscored

S

Dee

Rural Arkansas

National averag

66

72

57

61

38

40

17

20

3

6

16

26

r

u

N

p

e

edi

pe

ea

Su

su

Un

Auto loans

Success rate %

t score

prole

0 20 40 60 80

r-prime

Prime

r prime

bprime

bprime

scored

82

75

59

33

21

37

80

75

61

37

21

39

CONSUMER FINANCES IN RURAL AREAS OF THE SOUTHERN REGION

Consumer Financial

Protection Bureau

Learn more at consumernance.gov

ARKANSAS

Auto loan application acceptance rates in Arkansas, by credit score.

Auto loans

Success rate %

Credit score prole

0 20 40 60 80

Super-prime

Prime

Near prime

Subprime

Deep subprime

Unscored