EN EN

EUROPEAN

COMMISSION

Brussels, 5.5.2021

SWD(2021) 352 final

COMMISSION STAFF WORKING DOCUMENT

Strategic dependencies and capacities

Accompanying the

Communication from the Commission to the European Parliament, the Council, the

European Economic and Social Committee and the Committee of the Regions

Updating the 2020 New Industrial Strategy: Building a stronger Single Market for

Europe's recovery

{COM(2021) 350 final} - {SWD(2021) 351 final} - {SWD(2021) 353 final}

1

COMMISSION STAFF WORKING DOCUMENT

Strategic dependencies and capacities

Accompanying the

Communication from the Commission to the European Parliament, the Council, the

European Economic and Social Committee and the Committee of the Regions

Updating the 2020 New Industrial Strategy: Building a stronger Single Market for

Europe's recovery

Executive Summary

The COVID-19 pandemic has tested the resilience of economies worldwide. Despite severe

disruptions in production, transport and people’s mobility, most value and supply chains have

shown remarkable resilience. Still, the crisis has also highlighted that while the EU gains

resilience from world markets being open and integrated in global value chains, disruptions in

these global value chains can affect specific essential products and inputs that are particularly

critical for society and the EU economy. One of the key lessons of the crisis is that there is a

need to get a better grip and understanding of where Europe’s current and possible future

strategic dependencies lie. This can provide the basis for the development of facts-based and

proportionate policy measures informed by anticipation to address such strategic dependencies

while safeguarding the open and trade-based EU economy. In this context, the European Council

invited the Commission to “identify strategic dependencies, particularly in the most sensitive

industrial ecosystems such as for health, and to propose measures to reduce these dependencies,

including by diversifying production and supply chains, ensuring strategic stockpiling, as well as

fostering production and investment in Europe”.

Strategic dependencies affect the EU’s core interests. They notably relate to areas as regards

security and safety, the health of Europeans as well as the ability to access goods, services and

technologies that are key for the green and digital transitions at the core of the EU’s priorities.

Such strategic dependencies are more likely to be found in the most sensitive ecosystems, which

are the focus of this staff working document. This staff working document provides a further step

towards a more structural, systematic and cross-sector monitoring of the EU’s possible strategic

dependencies and an additional basis to consider when taking measures to address them.

Bottom-up mapping of strategic dependencies in the area of products (chapter 2)

A bottom-up (quantitative) mapping using external trade flows for more than 5,000 products as

its starting point identifies 137 products in the most sensitive ecosystems where the EU can be

considered highly dependent on imports from third countries (representing about 6% of the

extra-EU import value of goods). The three main foreign sources of EU import value for these

dependent products are China (representing about half of import value), Vietnam and Brazil. The

identified dependent products are situated mainly in the energy intensive industries ecosystem

2

(with 99 dependent products identified, including raw/processed materials and chemicals), as

well as in the health ecosystem (including active pharmaceutical ingredients and other health-

related products) and other inputs and products that are relevant to support the green and digital

transformation. Out of the 137 products identified as dependencies in the most sensitive

ecosystems, 34 (representing 0.6% of extra-EU import value of goods) could be considered as

potentially more vulnerable given their possibly low potential for further diversification as well

as substitution with EU production. At the same time, the EU can also be a source of dependency

vis-à-vis important trading partners. The analysis provides examples of products where the US is

highly dependent on the EU (“reverse dependencies”) and vice-versa. Furthermore, “common

dependencies” that the EU and the US share vis-à-vis China and the world can also be identified.

Reliance on international trade is not a vulnerability but rather helps to sustain diversified supply

and demand. Still, some of the identified dependencies could be considered of potential strategic

importance. Discussing the results of this bottom-up mapping with Member States and industry

(e.g. in the context of the Industrial Forum) will allow assessing the exact nature of identified

dependencies in more detail, including the risks they entail to the resilience and functioning of

the EU’s industrial ecosystems as well as possible prospects for reducing these dependencies in

the future including through the development of alternatives.

Also internal dependencies may exist within the Single Market whereby the EU relies on a

limited number of sources within the Single Market, linked to a concentration of supply or

activities at the level of individual firms. This underlines the importance of a well-functioning

Single Market – especially during times of crisis – that also remains open to the global economy.

Strategic dependencies in the area of key technologies (chapter 3)

The Industry Strategy of March 2020 highlighted that the EU should build competitiveness for

technologies that are strategically important for Europe’s industrial future. Complementary to the

analysis of trade flows done in chapter 2, an assessment of the EU’s performance as regards the

generation and uptake of certain key technologies shows both strengths and weaknesses. The EU

faces particular challenges in comparison with its global competitors for technologies in the

digital ecosystem such as cloud and micro-electronics. This provides important indications of

risks concerning future dependencies with regard to these technologies, while not precluding

possible technological dependencies in other ecosystems. If left unaddressed, dependencies in

the area of these technologies could further materialise and possibly new ones might emerge.

Finally, when it comes to the renewables ecosystem, the EU has a strong competitive position in

several technologies that are of key importance to achieve Europe’s climate ambitions (e.g. in the

area of hydrogen). Still, there are indications of risks concerning possible (future) dependencies

in this area as well and continued efforts are needed to facilitate scaling up and deployment of

these technologies.

Possible policy measures to address strategic dependencies (chapter 4)

For several of the dependencies identified in the bottom-up analysis of this staff working

document, work has already been initiated since the March 2020 Industry Strategy to address

these dependencies or assess them in more detail together with relevant stakeholders. Such

3

actions notably include the Action Plan on Critical Raw Materials and the European Raw

Materials Alliance, the structured dialogue taking place in the context of the Pharmaceuticals

Strategy, strengthened foresight in the context of the Chemicals Strategy as well as other specific

actions with regard to essential products or inputs necessary for the green and digital transition

(e.g. batteries, semi-conductors).

Any possible additional measures to address strategic dependencies need to be tailored to the

specific nature of the dependency and ecosystem concerned. They would need to build on in-

depth discussion and dialogue with Member States and industry, be proportionate and consider

all available options and tools. Policy measures can, on the one hand, reinforce the EU’s position

in global value chains by strengthening and diversifying external trade. Actions under the EU’s

Trade Policy Review will promote a level playing field and enable international trade and

investments to ensure more diversified sources of supply and demand to cushion future shocks

and enhance competitiveness. On the other hand, the EU can strengthen its own capacity in

strategic areas where necessary with targeted tools and investments in key strategic areas,

building on the strengths of a fully functioning Single Market and competition policy facilitating

open and dynamic markets that promote innovation.

When it comes to possible internal dependencies on a limited number of firms within the Single

Market, the COVID-19 pandemic has shown that the Single Market and its unhindered Treaty

freedoms should be at the core the Union’s readiness for potential crises. Competition policy, as

an enabler of strong business dynamics within the Single Market, as well as the EU’s integration

into diversified global value chains and undistorted access to export markets are also important

in mitigating possible risks related to such internal dependencies.

As regard possible strategic dependencies identified in the area of key technologies, the

Recovery and Resilience Facility provides an important step-up in investments in digital

technologies, together with other programmes such as Digital Europe. Relevant actions to

identify and address strategic dependencies are being taken also in the context of the

Communication on the Digital Decade and the Action Plan on synergies between civil, defence

and space industries (through an observatory on critical technologies and technology roadmaps).

Tools such as Important Projects of Common European Interest where proved well targeted,

justified and efficient as well as industrial alliances can continue to play an important role in

specific sectors. Targeted research and innovation efforts (such as through Horizon Europe and

the European Defence Fund) are also key in addressing the EU’s R&I gap in comparison with its

global competitors and thereby reducing strategic dependencies. Existing capacities (including

those under the EU space programmes) contribute strongly to the EU’s open strategic autonomy

and act as a positive lever for multilateral cooperation.

In-depth reviews of strategic dependencies (chapter 5)

The in-depth reviews presented in this staff working document provide a selected number of

analyses across a number of key areas that can be considered strategic, notably raw materials,

batteries, active pharmaceutical ingredients, hydrogen, semiconductors and cloud and edge

technologies. These assessments provide further insights on the origin of strategic dependencies

and their impact as well as relevant (ongoing) policy measures. They provide a first set of

4

analyses for a limited number of specific areas. As a follow-up to this staff working document,

further such detailed reviews of possible dependencies can be carried out covering other

strategically important areas, including products, services or technologies key to the twin

transition, such as renewables or energy storage.

5

Contents

1. Context and approach ........................................................................................................................ 6

1.1 Terminology and the concepts of “dependencies” and “strategic” ............................................ 7

1.2 Approach of the staff working document .................................................................................. 13

2. Mapping of EU dependencies in the most sensitive ecosystems .................................................... 16

2.1 Context ........................................................................................................................................ 16

2.2 Methodology to identify foreign dependencies .......................................................................... 19

2.2.1 Core Dependency Indicators .............................................................................................. 19

2.2.2 Identifying foreign dependencies....................................................................................... 21

2.3 Results......................................................................................................................................... 22

2.4 Assessing the further vulnerability of dependent products: potential for diversification and

substitution ............................................................................................................................................. 27

2.5 Single Market dependencies linked to concentration of economy activity .............................. 28

3. EU performance in key technologies and research & innovation ................................................ 30

3.1 Key technologies for (future) competitiveness .......................................................................... 30

3.2 Europe’s research and innovation performance ...................................................................... 36

3.3 Conclusions ................................................................................................................................ 41

4 Policy measures with a potential to address strategic dependencies ............................................ 42

4.1 Relevant measures to address external and internal strategic trade dependencies ................. 42

4.2 Relevant measures in the area of key technologies .................................................................. 48

5 Reviews of a selected number of strategic areas ............................................................................ 51

5.1 Raw materials ............................................................................................................................. 52

5.2 Active pharmaceutical ingredients ............................................................................................ 60

5.3 Li-ion batteries ........................................................................................................................... 68

5.4 Hydrogen .................................................................................................................................... 77

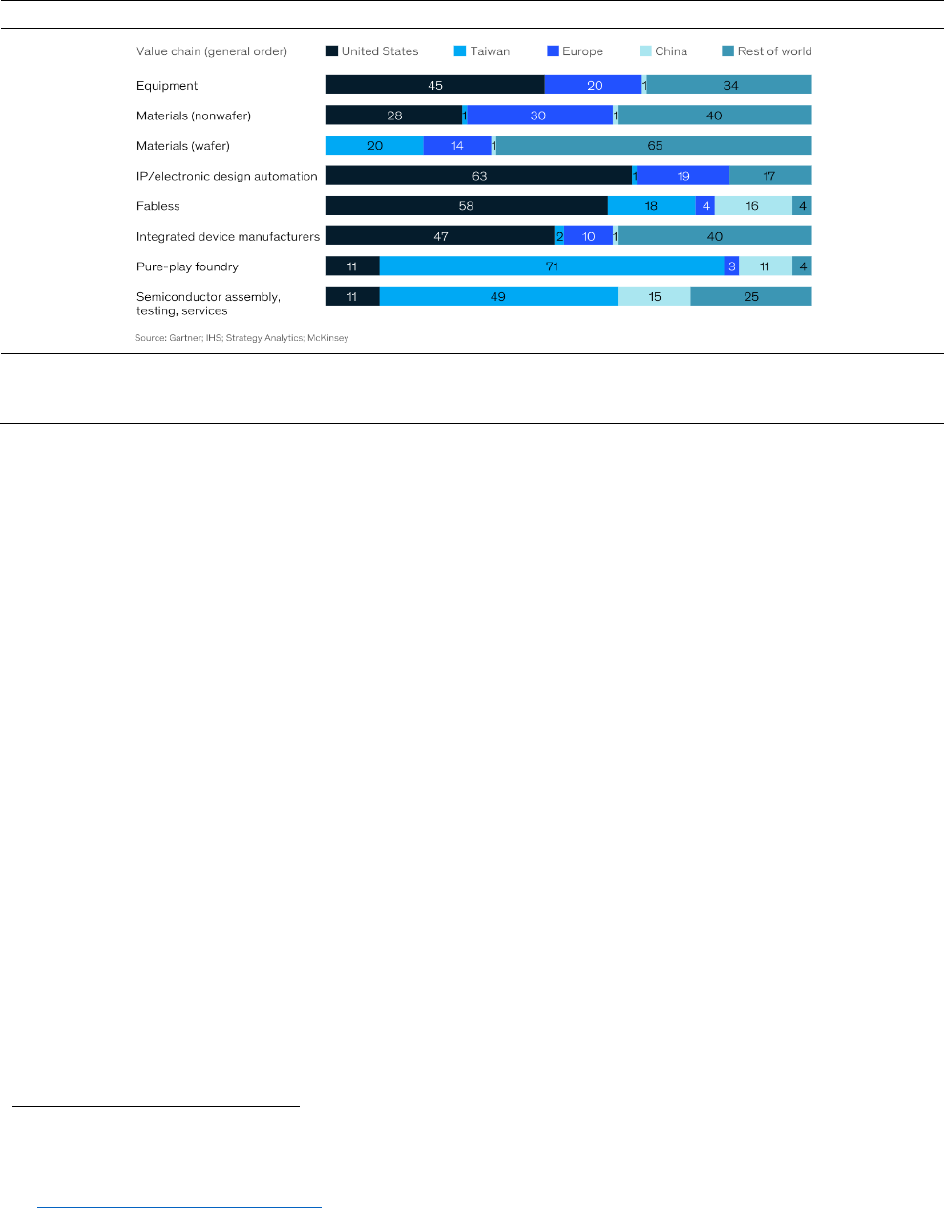

5.5 Semiconductors .......................................................................................................................... 82

5.6 Cloud and Edge Computing....................................................................................................... 91

6 Conclusions ...................................................................................................................................... 103

6

1. Context and approach

The EU economy is both a major importer and exporter on the international stage. Ensuring an

open and fair trading system is of key importance for the prosperity and future growth of EU

industry and to the benefit of European consumers and citizens. The EU plays a central role in

developing a more resilient and open global economy with undistorted trade, investments and

mutually beneficial bilateral relations. The COVID-19 crisis demonstrates how the Single

Market’s integration into global value chains not only maximises economic efficiency but is also

essential in times of crisis to absorb shocks, offer options to adjust and speed up recovery.

1

At the same time, the Industrial Strategy of March 2020

2

already underlined the importance for

the EU of “reducing dependence on others for things we need the most: critical materials and

technologies, food, infrastructure, security and other strategic areas”. The COVID-19 crisis

further emphasised the relevance of this issue in turbulent and challenging times, as it exposed

further some strategic dependencies and specific disruptions caught Europe by surprise.

One of the key lessons of the crisis is that there is a need to get a better grip and understanding of

where Europe’s current and possible future strategic dependencies lie. The European Council,

highlighting that “Achieving strategic autonomy while preserving an open economy is a key

objective of the Union”, invited the Commission to “identify strategic dependencies, particularly

in the most sensitive industrial ecosystems such as for health, and to propose measures to reduce

these dependencies, including by diversifying production and supply chains, ensuring strategic

stockpiling, as well as fostering production and investment in Europe”.

3

The Commission’s 2020 Strategic Foresight Report

4

provided a broad assessment of the EU’s

and Member States’ resilience. It also introduced resilience dashboards as a possible tool

allowing to monitor for the social and economic, geopolitical, green, and digital dimensions of

resilience. The Commission’s Communication on the Trade Policy Review

5

makes the case for

an open, sustainable and assertive trade policy that contributes to more resilient and sustainable

value chains by providing a stable rules-based trading framework, opening up new markets to

diversify sources of supply, and developing cooperative frameworks for fair and equitable access

to critical supplies. Identifying and addressing the EU’s strategic dependencies is an essential

step to increasing resilience. In addition, it is equally important to ensure competitiveness and

stimulate investments in technologies that are of key importance for the EU’s future. The

Communication on the Digital Decade

6

presents a vision, targets and avenues for a successful

digital transformation of Europe by 2030. Finally, this staff working document should also be

seen in relation with the upcoming 2021 Strategic Foresight Report on Europe’s open strategic

autonomy.

1

See also OECD: Shocks, risks and global value chains: insights from the OECD METRO model, 2020 and Trade

Policy Review (COM(2021)66)

2

COM(2020)102

3

EUCO 13/20

4

COM(2020)493

5

COM(2021)66

6

COM(2021)118

7

The assessment of strategic dependencies involves not only the identification of dependencies,

but also an assessment of whether they are of a strategic nature that leads to a vulnerability for

the EU, taking into account the risks such dependencies may represent to the EU’s core strategic

interests.

7

This assessment can contribute to the development of facts-based and proportionate

measures while at the same time safeguarding the open and trade-based EU economy.

The staff working document takes both a bottom-up and a top-down perspective. A bottom-up

(quantitative) analysis taking trade statistics in products as its starting point, while characterised

by data limitations and caveats, can provide first and indicative insights into areas where the

EU’s dependence on a limited number of suppliers is most prominent in particular for a number

of more sensitive ecosystems

8

. A top-down assessment needs to complement this bottom-up

approach, taking into account (at a more detailed level) other risks and possible dependencies of

strategic nature (e.g. related to services, infrastructures, technologies, skills, etc.) that cannot be

captured by relying on quantitative trade statistics and data. A first qualitative assessment for

selected areas is presented.

The analysis presented provides a contribution and a first step to a more systematic monitoring

of strategic dependencies in the EU’s most sensitive ecosystems. It complements actions that

have already been initiated on the analysis and identification of the EU’s strategic dependencies

in specific policy fields.

9

It is also worthwhile highlighting that other countries (including

notably the US

10

) are in the process of carrying out similar types of analyses to identify possible

risks and vulnerabilities in global supply chains as well as ways to address them.

1.1 Terminology and the concepts of “dependencies” and “strategic”

Key concepts used for the purposes of this staff working document are set out in box 1.

Box 1 – Terminology and definitions

The following concepts and definitions are used for the purposes of this staff working document:

- Resilience: the ability not only to withstand and cope with challenges but also to undergo

transitions in a sustainable, fair, and democratic manner.

11

Resilience is necessary in all

policy areas, also to undergo the green and digital transitions, while maintaining the EU’s

core purpose and integrity in a dynamic and at times turbulent environment;

- Open strategic autonomy: the ability to shape the new system of global economic

governance and develop mutually beneficial bilateral relations, while protecting the EU

from unfair and abusive practices, including to diversify and solidify global supply chains

7

The concept of “strategic dependency” is further explained in chapter 1.1

8

The concept of “sensitive ecosystems” is further explained in chapter 1.1

9

For example in the context of the critical raw materials action plan (COM(2020)474) and the Pharmaceutical

Strategy for Europe (COM(2020)761)

10

See Executive Order on America’s Supply Chains (https://www.whitehouse.gov/briefing-room/presidential-

actions/2021/02/24/executive-order-on-americas-supply-chains/)

11

COM(2020)493

8

to enhance resilience to future crises;

- Strategic capacity: a certain level of capabilities held within the EU allowing to produce,

provide or rely on strategic goods, services, data, infrastructures, skills, industrial know-

how and technologies

12

;

- Dependencies: reliance on a limited number of actors for the supply of goods, services,

data, infrastructures, skills and technologies combined with a limited capacity for internal

production to substitute imports

13

;

- Strategic dependencies: dependencies that are considered of critical importance to the

EU and its Member States’ strategic interests such as security, safety, health and the

green and digital transformation.

External and internal dependencies

Both external and internal dependencies co-exist. External dependencies concern the EU’s

reliance on external partners (third countries or firms). Internal dependencies are dependencies

within the EU Single Market, notably related to the possible concentration of activity at firm

level. The risks related to external dependencies are different from the risks related to internal

dependencies. This is the case, for example, in relation to political tensions and geo-political

uncertainty, which can be important risks for the EU at an international level. At the same time,

dependence on a very limited set of companies for supplies in a specific sector can result in

vulnerabilities even if these companies are based in the EU.

14

Such internal dependencies linked

to a concentration of supplies can have a potentially important impact on the functioning of EU

value chains within the Single Market (e.g. in the case of natural disasters or closing down of

production).

There are different types of shocks that play a role when assessing the impact of

dependencies. Such shocks can be supply-related (e.g. a given supplier within a value chain no

longer producing or delivering certain goods and services, or in reduced quantities; or the

country where the supplier is based imposing certain export restrictions) as well as demand-

related (e.g. a sudden important drop in EU or global demand for goods and services, or a sudden

global rise in market demand for certain goods or services) and they can have multiple origins

(man-made, natural, etc.). Scarcity of resources (e.g. related to critical raw materials) is also an

important element to be taken into account when considering the impact of dependencies and

shocks. Companies, through their own corporate decisions and corporate policies, play a key role

in mitigating and adapting to possible shocks, as they have the ability to diversify supply and

demand sources to become more resilient. At the same time, they cannot always accommodate

all types and magnitudes of unanticipated demand or supply shocks.

12

This may include the availability of scalable manufacturing capacities that can be relied on during a crisis

situation and increase of demand

13

Dependencies can also be extended to exports and the possibility to rely on internal consumption to substitute

exports

14

Furthermore, the ownership of companies by EU entities or foreign investors may also be relevant

9

Box 2 – Demand and supply shocks during COVID-19

The EU experienced the impact of different types of shocks to global value chains during

the COVID-19 crisis. These shocks were both demand and supply related.

On the one hand, the pandemic has caused significant effects on the demand side. The most

important impact from the crisis across many ecosystems has been the sudden and very

significant reduction of demand within the EU and on export markets. At the same time, other

ecosystems saw large peaks in demand. Most notably, the crisis led to a global surge in the

demand for medical supplies and devices. This led to shortages in this sector, including for

example with regard to personal protective equipment and ventilators. Another example of a

positive demand shock has been the global surge in demand for semi-conductors that resulted in

shortages during the first months of 2021

15

, entailing risks of a slowed down recovery in sectors

that are dependent on the supply of these semi-conductors (e.g. the automotive industry).

The crisis has also seen important supply related shocks, notably in the health sector. For

example, for some key medical supplies, several foreign countries introduced measures

restricting or banning exports. This worsened the situation of acute under-capacity due to an

exploding global demand in these products in addition to the aggravating factor of reduced

production capacity due to the fact that many businesses active across global value chains were

forced to reduce or halt production due to the spread of the virus and health precautions such as

lockdowns, quarantines and social distancing. Restrictions concerning the movement of people

and their impact on international transport networks represented another important supply shock.

Disruptions were also experienced within the EU Single Market. Several Member States

introduced exports bans in particular during the early stages of the pandemic. In addition, border

restrictions, quarantine requirements and other measures limiting free movement of persons,

goods, services also hampered the functioning of supply chains within Single Market.

Strategic nature of dependencies

Determining the specific areas and dependencies that are “strategic” for the EU requires a

careful assessment of the current and future interests at stake and potential risks, building

on a collective understanding of what matters most and what is critical for Europe.

Dependencies that are strategic can be identified by taking into account the extent to which they

affect these core interests. This can only be done on a case-by-case basis, taking into account not

only quantitative data but also qualitative, ecosystem-specific elements and expert knowledge.

Firstly, dependencies are likely strategic when they impact the security and safety of

Europeans or limit the possibility for the EU to exercise a foreign and security policy in line

with its values and strategic interests.

16

The EU framework for screening of foreign direct

15

Pandemic-related spikes in demand contributed to a shortage of chips, while also being linked to structural

problems such as distortive government subsidies and export restrictions. Further details are provided in chapter 5.5

16

It should be noted that the European Council has also requested the Commission in the context of security and

defence to prepare “a technology roadmap by October 2021 for boosting research, technology development and

innovation and reducing our strategic dependencies in critical technologies and value chains” (SN 2/21)

10

investment provides a reference in this regard, outlining specific infrastructure, technologies and

inputs that are considered to be critical. Dependencies with an impact on security and safety are

of particular relevance for the aerospace and defence ecosystem and may also exist in various

other ecosystems (such as for example digital and electronics). Examples of actions which

already address strategic dependencies in this area include the Space Strategy for Europe

17

aimed

at reinforcing Europe's autonomy in accessing space in a safe and secure environment, the

European Defence Action Plan

18

towards a strong, competitive and innovative defence industrial

base, the European Defence Fund

19

as well as strengthening the competitiveness of EU security

industry through investment in civil security research and innovation in the Horizon Europe

Programme

20

and most recently the Action Plan on synergies between civil, defence and space

industries

21

.

Secondly, the impact on the health of EU citizens is another important driver to define

dependencies as strategic. For example, the COVID-19 crisis exposed a number of strategic

dependencies in the area of health (e.g. access to medical supplies such as personnel protective

equipment). The European Council has also asked the Commission to “identify strategic

dependencies, particularly in the most sensitive industrial ecosystems such as for health”. The

Commission has already initiated work in the context of the Pharmaceuticals Strategy for

Europe

22

with concrete actions to ensure accessibility, availability and affordability of medicines,

including an assessment of security of supply chains.

Thirdly, in certain cases dependencies can also be considered strategic when they

significantly impact the EU’s access to inputs, technologies and services that are key for the

green and digital transitions at the core of the EU’s priorities.

23

The Commission has

recently reconfirmed the importance of these green and digital ambitions in the context of the

Recovery and Resilience Facility, requiring that each national recovery and resilience plan

includes a minimum of 37% of expenditure related to climate and 20% related to digital.

Dependencies that have a significant negative impact on the ability of the EU to remain at the

edge of innovation and transformation towards an increasingly green and digital economy and

society will ultimately be detrimental to the functioning of the EU economy and the welfare of

its citizens. The Commission has already recognised the strategic nature of third country

dependencies in relation to its green and digital ambitions in several recent initiatives. Such

dependencies are mainly related to critical inputs needed to support the digital and green

transition

24

as well as the ability of the EU to access key enabling technologies.

25

17

COM(2016)705

18

COM(2016)950

19

https://ec.europa.eu/growth/sectors/defence/european-defence-fund_en

20

Horizon Europe Cluster 3 – Civil security for society

21

COM(2021)70

22

COM(2020)761

23

Political Guidelines for the Next European Commission 2019-2024

24

See for example the Action plan on critical raw materials (COM(2020)474), the Hydrogen strategy for a climate-

neutral Europe (COM(2020)301), the Commission proposal for a new regulatory framework on batteries

(COM(2020)798/3)

11

Within these areas, the individual nature of the dependency and the degree of risks

involved need to be assessed. It is important to underline that a certain reliance on international

trade and commercial relations and partnerships with companies in third countries do not

necessarily give rise to an external dependency that would result in a vulnerability for the EU

economy. To the contrary, such relations and partnerships help to strengthen the EU’s resilience

to supply and demand shocks, in addition to the substantial efficiency gains that help to sustain

the competitiveness of the EU economy over time. Only those dependencies that significantly

affect the EU’s core interests and limit the EU’s freedom to analyse, make decisions and act

according to its own priorities can be considered strategic.

Box 3 – FDI screening Regulation, critical raw materials list and Action Plan on synergies

between civil, defence and space industries

The strategic nature of certain areas and dependencies has already been established in the

EU framework for screening of foreign direct investment, the EU’s critical raw materials

list as well as the recent Action Plan on synergies between civil, defence and space

industries.

Regulation (EU) 2019/452 establishing a framework for the screening of foreign direct

investments into the Union created a cooperation mechanism for Member States and the

Commission to screen foreign investment. The mechanism (operational as of 11 October 2020)

establishes cooperation and the exchange of information between EU Member States and the

Commission and provides the possibility to raise concerns related to specific foreign

investments, where warranted. The Commission may issue opinions when an investment poses a

threat to the security or public order of more than one Member State or when an investment

could pose a risk to a project or programme of Union interest. The screening framework also

establishes core requirements for Member States who maintain or adopt a national screening

mechanism. In Article 4, the Regulation outlines certain factors that may be taken into

consideration by Member States or the Commission in determining whether a foreign direct

investment is likely to affect security or public order. These include potential effects on critical

infrastructure, critical technologies and dual use items and supply of critical inputs. Several of

the criticalities defined in this Regulation are of particular relevance for the analysis in this staff

working document including critical technologies (e.g. artificial intelligence, robotics,

semiconductors, cybersecurity, aerospace, defence, energy storage, quantum and nuclear

technologies as well as nanotechnologies and biotechnologies) as well as critical inputs (e.g. raw

materials).

The EU’s critical raw materials list provides an overview of the raw materials that are

considered to be most important economically and having a high supply risk. The list

26

is

25

See for example, the White Paper on Artificial Intelligence (COM(2020)65), the joint declaration by Member

States on processors and semiconductor welcomed by the Commission (https://ec.europa.eu/digital-single-

market/en/news/joint-declaration-processors-and-semiconductor-technologies)

26

Available in COM(2020)474

12

reviewed every three years by the Commission, based on a comprehensive screening and

assessment methodology

27

. The Commission takes it into consideration when developing and

implementing policies relating to raw materials, including when negotiating trade agreements

and seeking to eliminate trade distortions. It also helps to identify investment needs and guide

research and innovation.

The Commission’s Action plan on synergies between civil, defence and space industries

identifies a list of examples of critical technologies relevant across the civil (including

security), defence and space industry domains. Using this list as a basis, a new EU

Observatory of Critical Technologies will start, in 2021, regular monitoring and analysis of

critical technologies, their potential applications, value chains, needed research and testing

infrastructure, desired level of EU control over them, and existing gaps and dependencies. Every

second year, the Observatory, in consultation with key stakeholders, will produce a classified

report on critical technologies, dependencies, value chains and testing infrastructure for the

defence, space and related civil industries. On the basis of these reports, the Commission will

develop technology roadmaps to boost innovation on these critical technologies. These

technology roadmaps may lead to the launch of new flagship projects taking into account their

likely impact on the technological sovereignty and leadership of the EU, their sources of

financing and their governance.

In general, the existence or risks of strategic dependencies are more probable in a few

“sensitive ecosystems”. Ecosystems such as tourism, textiles and proximity and social economy

might be unlikely to hold important risks for strategic dependencies as a whole. On the other

hand, dependencies within the aerospace and defence as well as the health ecosystem are more

likely to be of a strategic nature. In addition, certain dependencies within ecosystems such as

digital, electronics, renewable energy and energy intensive industries can also be strategic when

they impact health or security interests or significantly affect the EU’s ability to achieve the

green and digital transformation. Furthermore, some ecosystems are also more closely related to

critical areas already listed in the FDI screening Regulation (e.g. aerospace and defence

ecosystem), the EU’s critical raw materials list (e.g. energy intensive industries ecosystems) as

well as the critical technologies outlined in the Action Plan on synergies between civil, defence

and space industries (e.g. digital and electronics ecosystem). Therefore, the bottom-up mapping

of dependencies developed in chapter 2 will focus on a number of these more sensitive

ecosystems (see Graph 1) when considering the question of identifying possible strategic

dependencies. This also follows the Council conclusions of 16 November 2020, which

specifically highlighted health, defence, space, digital, energy and critical raw materials as

examples of sensitive industrial ecosystems and areas.

28

Nevertheless, this does not exclude the

27

European Commission: Study on the EU's list of Critical Raw Materials, 2020

28

13004/20 (paragraph 3)

13

existence of possible risks or dependencies in other ecosystems not covered by the analysis in

this staff working document.

29

Graph 1: More sensitive ecosystems for the purposes of this staff working document

Source: European Commission

Note: Circles represent a selection of more sensitive ecosystems for the purpose of this staff working document

1.2 Approach of the staff working document

The staff working document combines a number of elements to address the objective of

identifying and addressing strategic dependencies.

Firstly, Chapter 2 develops a bottom-up (quantitative) analysis of trade dependencies in

goods, taking as its starting point a detailed assessment of the EU’s trade flows, following a step-

by-step approach:

- In a first step, the analysis identifies goods where the EU is dependent on a limited

number of sources, based on the concentration of suppliers, the relative importance of

extra EU imports as well as their possible substitution with internal EU production;

- In a second step, the dependencies identified in step 1 are narrowed down to more

sensitive ecosystems with a higher risk of dependencies being of a possible strategic

nature (as outlined in chapter 1.1);

29

For example in the agri-food ecosystem, the international dimension is important in the common agricultural

policy (CAP), as maintaining a healthy balance of imports and exports is key to safeguarding internal market

stability. There are already tools in place to monitor this ecosystem. Notably, in order to ensure the delivery of the

CAP objectives, the Commission collects statistics and produces analyses of agricultural trade and international agri-

food policy developments. The most up to date information is published monthly in “Monitoring EU agri-food

trade”, while a more in-depth examination of how the EU agri-food trade flows have changed in the past year is

provided in the annual “Monitoring agri-trade policy” report.

14

- In a third step, consisting of a qualitative assessment, specific dependencies are identified

that might be strategic for the EU (in line with the different elements set out in chapter

1.1 concerning the concept of “strategic”) or that require further in-depth analysis to

assess their impact and strategic nature.

For each of the identified product dependencies spotted in the more sensitive ecosystems the

analysis also gives an indication of the potential to further diversify the EU’s import sources for

these products as well as the potential for substitution with EU production (see chapter 2.4).

This bottom-up analysis faces a number of data limitations and caveats as to the

conclusions that can be drawn. The first relates to the level of aggregation. While the analysis

covers more than 5,000 traded products or product groups, in some cases the level of detail is not

sufficient to capture dependencies on specific or specialised products or inputs.

30

Second,

sufficiently detailed trade statistics are not available for services and trade statistics cannot

(clearly) identify dependencies in the area of complex technologies including those that are of a

more emerging nature. Third, the analysis only looks at trade dependencies at one point in time

and cannot capture changing or emerging trends. In addition, the assessment whether

dependencies are strategic (step 3) is a qualitative exercise and this staff working document can

only provide a first indication, which needs to be complemented through further dialogue with

industry on the exact nature and impact of identified dependencies.

As a consequence, the bottom-up mapping cannot be considered to be an exhaustive

screening of all possible product dependencies. In addition, it needs to be complemented by

discussions with industry and Member States on the strategic nature of the identified

dependencies taking into account the specific ecosystems concerned. Despite these limitations,

the analysis offers a methodical screening giving preliminary insights into individual products

and inputs where the EU has a higher level of dependence on third countries including some with

a possible strategic character. This analysis is dynamic by nature and requires regular updating

and refinement, given the changing nature of dependencies. Further details on the approach and

methodology of the bottom-up mapping are set out in chapter 2.

Secondly, the Industry Strategy of March 2020 highlighted the importance of developing key

enabling technologies that are strategically important for Europe’s industrial future. In addition,

the recent Communication on the Digital Decade underlined that digital technologies are

currently mostly developed outside of Europe and highlighted the importance of reinforcing

internal strengths and capacities for the EU to achieve digital leadership. The EU’s performance

in comparison with its global competitors in the area of these key technologies cannot be clearly

captured by an analysis of trade statistics as performed in chapter 2. In this context, chapter 3

aims to complement the assessment done in chapter 2 by considering the EU’s position in

comparison with its global competitors in the area of key technologies that will drive future

competitiveness. It does this on the basis of a range of indicators (considering e.g. research,

30

In addition, the bottom-up product mapping faces a number of specific limitations when it comes to identifying

dependencies within the defence and aerospace ecosystem, linked to the sensitivity of data associated to defence

goods, as well as the classification level of most defence contracts. Further work is needed to assess this specific

area in detail.

15

investments, innovation and business dynamics), looking into the EU’s relative performance in

comparison with its global competitors. These provide important indications, albeit not complete,

as to possible risks of potential (future) dependencies in the area of such technologies. For

example, comparatively low levels of innovation and investments may result in Europe

becoming more dependent on other countries for access to state-of-the-art technologies. Chapter

3 relies on information obtained from different sources, including the Advanced Technologies for

Industry project as well as other data and analyses on the EU’s performance in research and

innovation.

Thirdly, chapter 4 provides indications of relevant possible measures that might be able to

mitigate strategic dependencies and related risks. Such measures would need to build on in-

depth discussion and dialogue with and between Member States and industry. They should build

on the opportunities of international trade to diversify and strengthen sources of supply as well

as, where needed, the strengths of the Single Market to build up adequate EU capacity. Measures

would need to be carefully examined with a view to maintain the competitiveness of the EU,

choosing to address dependencies and increase resilience in the most cost-efficient manner.

Finally, for those specifically identified dependencies of strategic importance, possible policy

intervention would need to build on a thorough understanding and detailed analysis of the

functioning of relevant value chains as well as the underlying drivers of Europe’s current and

possible future strategic dependencies. Chapter 5 presents a selected number of in-depth

reviews of possible dependencies identified in chapters 2 and 3 that can be considered

strategic across a number of key areas (including health, digital, green). These reviews

provide an overview of the origin of strategic dependencies, their impact on the EU economy as

well as possible relevant (ongoing) measures. They provide a first stage of assessments in

strategic areas and should not be considered to be an exhaustive analysis of all the EU’s strategic

dependencies. Further key areas, including products, services or technologies key to the twin

transition such as renewables or energy storage, might be considered in the future.

16

2. Mapping of EU dependencies in the most sensitive ecosystems

The COVID-19 crisis showed the importance of obtaining a more comprehensive

understanding of the EU’s strategic dependencies as a first step to strengthening resilience.

This chapter provides a bottom-up mapping of the EU’s ecosystems and their reliance on

international trade. It covers trade flows for some 5,000 products classifying goods as dependent

based on various meaningful and objective economic criteria. While this assessment faces a

number of data limitations and caveats, it provides a first indication of goods (final products and

inputs) where the EU might have a higher level of dependence on a limited number of suppliers,

including those with a possible strategic character in more sensitive ecosystems.

2.1 Context

Over the last decades, production processes and supply chains have become increasingly

interlinked across countries and continents. The drivers explaining the continuous integration

of Global Value Chains (GVCs) include, among others, cost reduction, greater market openness

(lower tariff and non-tariff barriers), changes in the political environment, as well as multiple

technological innovations. GVCs enable firms to improve their market position through

delocalisation strategies and generate benefits from a more efficient production process

(including in some cases lower prices for final consumers) and help firms to reduce risks. In

addition, when firms become geographically closer to their final customers, they may also gain

from a better consumer knowledge.

While global value chains are highly efficient from a cost, growth, and a diversification

perspective,

31

they could also entail vulnerabilities to external demand and supply shocks.

Reliance of EU firms on international trade is a strength for the resilience of the EU economy

and it is fundamental to safeguard the wealth and competitiveness of the EU through efficiency

and productivity gains, as well as to sustain demand for EU output. In that regard, private firms

have the ability, the incentive and the information to diversify supply and demand sources

sufficiently to absorb normal discontinuities in trade flows. However, not all of them might be

able to accommodate unanticipated demand and/or supply shocks exceeding by far what normal

business operations would dictate. In such instances, the collective cost of a potential demand

and supply shock to the general EU public may exceed the lost profits to the market operator

importing specific goods or services. Given the result, akin to a market failure, policy action

addressing strategic dependencies may be justified.

While the majority of value chains have shown resilience during the pandemic, the crisis

has shown that disruptions in GVCs might affect specific products, some of which are

particularly critical for society. For instance, the greatest disruptions have been felt in medical

(e.g. personal protective equipment) and medical-pharmaceutical supplies. These products have

been under severe strain due to the enormous surge in demand compared to supply.

32

Export

31

OECD: Shocks, risks and global value chains: insights from the OECD METRO model, 2020

32

See OECD: Global Value Chains: Efficiency and Risks in the Context of COVID-19, 2020; S. Evenett: Chinese

whispers: COVID-19, global supply chains in essential goods, and public policy, 2020 (Journal of International

17

restrictions imposed by some countries on these specific products or their components have

worsened the situation. At the same time, other measures adopted by governments cut import

duties, facilitated customs-clearance and streamlined approval requirements for medical

supplies

33

.

While observing significant differences across sectors, overall, the EU is an important

supplier and customer for extra EU countries. Using GVC data, national and international

links between sectors along value chains can be tracked, by looking for each sector at both

upstream links (which shape supply chains) and downstream links (which contribute to final

demand). Graph 2 shows the exposure of EU industry to extra EU markets both in terms of

demand and supply, which are then used in the production process of each sector. It shows that

the sectors with the highest upstream and downstream foreign links are Computer & electronics,

Chemicals and Pharmaceuticals, Basic Metals and Electrical equipment. Sectors above the 45

degree line rely more on extra EU demand than on the supply from extra EU countries.

With few exceptions, extra EU demand is relatively more important for the EU aggregate

than extra EU supply. However, foreign supply from certain sectors still plays a significant role

for EU production. Graph 3 ranks sectors according to the extent to which EU production

depends on foreign supply. The EU relies on extra EU countries particularly in raw materials and

electronics, but also textiles, financial activities, as well as chemicals and active pharmaceutical

ingredients. Consequently, this highlights the need for the EU to continue being integrated in the

global economy.

EU trade diversification is high and stable over time. At a macro level, extra-EU trade is

diversified. Both extra-EU exports and extra-EU imports concentration have not varied much in

the last decade (see Graph 4). Compared to other countries, while extra-EU import concentration

has remained broadly constant over the last two decades, concentration decreased significantly in

China and increased in the US. For example, US imports at an aggregate level are currently

around twice as concentrated as EU imports.

Macro and sectoral trade give an overview of dependencies, but a more granular detail is

required to identify specific products where the EU has strong external dependencies.

34

Ideally, the identification of dependent products would use product information at a 8-10 digit

level on the Harmonised Standardisation (HS) system or firm level data. However, comparable

data sources across all countries in the world are not available. This would jeopardise the

calculation of the dependency indicators proposed in this chapter and their comparison across

countries. Thus, a 6-digit level of disaggregation is used, which already provides informative

results of the level of dependency across products.

Business Policy); OECD: COVID-19 and global value chains: Policy options to build more resilient production

networks, 2020

33

In this respect see, for example, European Commission Decision 2020/491 and European Commission Notice

2020/C 96/I/01.

34

To be noted is that trade in services is not captured in the database used for this analysis.

18

The following section outlines a methodology to identify existing dependencies of the EU,

including dependencies of a possible strategic nature in more sensitive ecosystems. This exercise

has certain limits dictated by the information sources available as already outlined in Chapter

1.2.

Graph 2: Downstream and upstream exposure to extra EU markets

Source: Commission elaborations based on OECD 2016-AMNE data. Note: on the horizontal axis, the indicator measures for

each EU sector the share of value added that depends on intermediate inputs generated by extra EU supply chains; on the vertical

axis the indicator measures for each EU sector the share of final demand absorbed by exports to extra EU countries. These figures

are based on the most recent available data (2016). As the share of value added has stayed rather stable over time, more recent

figures are not expected to substantially depart from this illustration.

Graph 3: Foreign (extra EU) dependency for EU production

Source: Commission elaborations based on OECD-AMNE 2016 data. This graph shows the share of value added embedded in

the production process that comes from non-EU countries for 20 sectors in decreasing order. Note that this level of aggregation is

not suited to identify dependencies in some sectors/ecosystems such as defence and aerospace.

19

Graph 4: Foreign (extra EU) trade is very diversified and has remained stable over time

Source: Felbermayr presentation to Informal Meeting of Trade Ministers Berlin, Sept. 21, 2020 “Fostering the Resilience of EU

Trade Links”.

Data source: BACI (CEPII). The Herfindahl index takes a value of 100 if trade is fully concentrated on 1 foreign country,

2.2 Methodology to identify foreign dependencies

The bottom-up mapping of foreign dependencies relies on an agnostic, data-driven

perspective with the objective of identifying products with extra EU dependency. The

bottom-up mapping follows a step-by step approach. In a first step, the analysis identifies traded

products where the EU is more dependent on third countries based on three economic indicators.

Then, the identified dependencies are narrowed down to the most sensitive ecosystems. On this

basis, a further qualitative assessment consists in spotting dependencies in the most sensitive

ecosystems, with a possible strategic nature (in line with definition of “strategic” outlined in

Chapter 1.1).

Graph 5: Approach bottom-up analysis

Source: European Commission

2.2.1 Core Dependency Indicators

The bottom-up approach classifies products as highly foreign dependent if the levels of

import diversification and potential substitutability with EU supply are low. This mapping

of dependencies builds on the approach used by Bonneau and Nakaa (2020), but it extends their

20

analysis by considering potential substitutability with EU production.

35

Data covering the

universe of country trade in goods is used, including more than 5,000 products defined at the six-

digit level using the international nomenclature of the Harmonized System (HS6),

36

across all

industrial ecosystems.

37

Given that the level of dependency cannot be characterised by a single

metric, the bottom-up approach combines three complementary economic indicators that are

referred to as the core dependency indicators (CDIs) as presented in Graph 6.

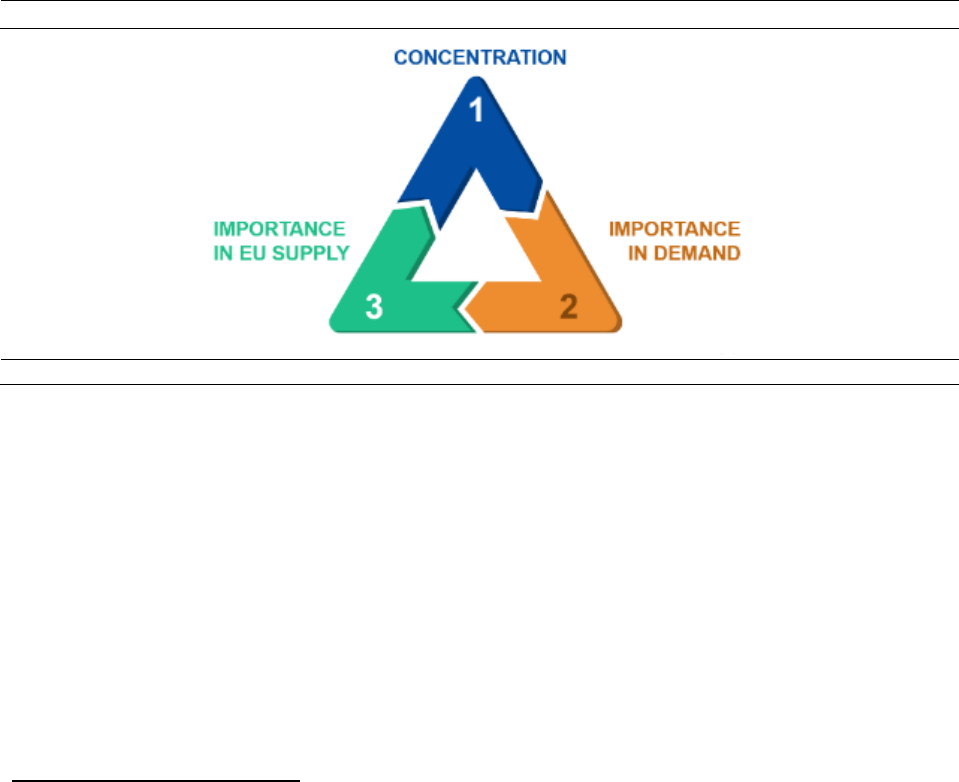

Graph 6: Core Dependency Indicators

Source: European Commission

1. Concentration of EU imports from extra EU sources: The first indicator aims at

quantifying the concentration of EU imports with respect to the rest of the world, in order

to capture the risk of disruptions faced by the EU due to low diversification of extra EU

sources. In particular, this indicator identifies products for which EU imports (in values)

are highly concentrated in a few extra EU countries. To this end, the Herfindahl-

Hirschman Index (HHI) index is used, computed as detailed below:

where

is the market share of the extra EU supplying country i in EU’s imports, and n is

the total number of extra EU supplying countries.

35

See Bonneau and Nakaa: Vulnérabilité des approvisionnements français et européens, 2020 and other recent

studies that have analysed the foreign dependencies by looking at the diversification of EU imports from non-EU

sources (e.g. G. Felbermayr: Fostering the Resilience of EU Trade Links, 2020 and Cernat and Guinea: On ants,

dinosaurs, and how to survive a trade apocalypse, 2020)

36

The first two digits (HS-2) identify the chapter the goods are classified in, the next two digits (HS-4) identify

groupings within that chapter. The next two digits (HS-6) are even more specific. Up to the HS-6 digit level, all

countries classify products in the same way. While HS-6 classification is already highly disaggregated and suitable

for analysing dependencies across ecosystems, for some specific products, an analysis at a higher level of

disaggregation would be necessary to complement this assessment.

37

The notion of ecosystems captures the complex set of interlinkages and interdependencies among sectors and

firms spreading across countries in the Single Market. This concept takes into account specificities of business

models, presence of vulnerable players (SMEs and micro) and interdependencies.

21

2. Importance of extra EU imports in total demand: The second indicator measures the

importance of extra EU imports in total EU imports (i.e. extra and intra EU imports), so

as to identify the products for which the EU mainly relies on foreign sources. It is

computed as the share of extra EU imports in total EU imports (in values):

3. Substitutability of extra EU imports with EU production: The third indicator aims at

capturing whether the EU production can cover the extra EU import needs in the event of

trade disruptions. For this purpose, EU total exports, including intra and extra EU

exports, are used as a proxy for the EU internal production capacity.

38

For each product,

the ratio between the extra EU import value and the total EU export value (i.e. extra and

intra EU exports) is computed as detailed below:

2.2.2 Identifying foreign dependencies

The narrowing down of foreign dependencies is based on the application of thresholds on

the three indicators. As depicted in Graph 5, the whole sample of around 5000 products is

considered, with the objective of narrowing the number of products down to most dependent

goods, satisfying the following thresholds for each indicator:

i.

The indicator suggests that the higher the concentration, the lower the diversification of

EU imports from extra EU sources. Consequently, this threshold implies that the EU

import value originates mainly from 2.5 foreign countries.

39

It is important to

acknowledge that the diversification of imports could be complemented with additional

information on the trading partner in question, so as to assess the overall level of risk.

ii.

38

Ideally, production data should be used for the purpose of this indicator but European production data do not

allow to analyse dependencies at 6-digit level. Databases like PRODCOM contains many missing values at this level

of product disaggregation.

39

This threshold is more conservative than 0.25, which is considered by the economic literature as an indication of a

high concentration.

22

The indicator suggests that the higher the share, the higher the importance of extra EU

imports in total EU imports. Hence, this threshold implies that the value of extra EU

imports accounts for the majority (> 50%) of the value of total EU imports.

iii.

The indicator suggests that the higher the ratio, the less able the EU is to substitute extra

EU imports with EU production in case of a trade disruption. Therefore, this threshold

implies that the value of extra EU imports is higher than the value of total EU exports.

A sensitivity analysis is conducted, based on the whole distribution of the three indicators. More

precisely, all 5000 products are ranked based on each indicator. The ranks of these three

indicators are combined in a composite indicator measuring the overall foreign dependency of

each product. Broadly, the results of the approach based on thresholds corresponds to the most

dependent products based on a composite indicator.

Graph 7: Identification of dependencies on extra EU supplies

Source: European Commission

2.3 Results

As highlighted in chapter 2.2, the bottom-up mapping consists in the application of three

economic indicators and their respective thresholds to the whole sample of about 5,000

products to identify foreign dependencies (Graph 7). The mapping exercise first identifies

around 390 dependent products across all ecosystems. In a second step, the list of products

identified as dependent is narrowed down to the most sensitive ecosystems. Finally, in the third

step, only the most dependent products in the most sensitive ecosystems are considered.

23

The bottom-up mapping identifies 137 products in the most sensitive ecosystems where the

EU can be considered highly dependent on imports from third countries. These pre-

identified products represent about 6% of the EU’s total import value of goods.

The three main foreign sources of EU import value for the 137 products identified as highly

dependent are China, Vietnam and Brazil (Graph 8). China represents around 52% of the

total value of imports of the most foreign dependent products and it is among the top three

suppliers for around 54% of these goods. In terms of stages of processing, around 16% of the

most foreign dependent products are raw materials, around 57% are intermediate goods and

around 27% final goods. At the same time, the EU can also be a source of dependency for other

countries (see Box 4 for an example of reverse dependencies of the EU and US and their

common dependencies vis-à-vis important trading partners).

Graph 8: Share of EU imports value of dependent products

Source: European Commission based on BACI database

The strategic nature of these identified dependencies needs to be assessed on a case-by-case

basis, relying on in-depth discussions with Member States and relevant industries. Further

discussions with Member States and relevant industries would be needed to assess the possible

strategic character of these dependencies, as well as their impact and the risks that they entail on

the functioning of the more sensitive ecosystems (including e.g. taking into account risks linked

to the specific trading partners in question). In what follows, a preliminary description of the

dependencies identified in the more sensitive ecosystems as well as a number of considerations

on the possible strategic nature of the identified dependencies is provided.

A large group of identified dependencies are raw and processed materials and chemicals

that can be classified in the energy intensive ecosystem but that have also wider importance

and implications across several other ecosystems. The bottom-up mapping exercise highlights

foreign dependencies for 99 products related to raw/processed materials and chemicals (e.g.

beryllium, cobalt, antimony, lithium, aluminium, tungstates, chromium, nickel, molybdenum,

24

manganese, ferro-alloys, steel,

40

various chemical products). Several of these identified raw

materials have already been assessed as critical in the context of the EU’s regular monitoring of

critical raw materials.

41

The mapping also highlights dependencies regarding imported energy

products (e.g. petroleum products and fossil fuels), which are important to consider in the

context of the decarbonisation of EU industry. Chapter 5 of this staff working document provides

more in-depth reviews of the EU’s dependencies and possible vulnerabilities in the areas of raw

materials as well as hydrogen as a key contributor to the EU’s future decarbonised economy.

42

A second important group of dependencies belongs to the health ecosystem, including active

pharmaceutical ingredients (APIs), other medicines and COVID-19 related goods in the

health ecosystem. Access to medical products and pharmaceuticals is crucial for the health of

Europeans and the EU’s open strategic autonomy, as evidenced by the COVID-19 crisis. The

bottom-up mapping identifies 14 products as foreign dependent, some of which have been of

high relevance during the COVID-19 crisis (e.g. part of protective garments). Others include

chemical substances known as APIs (i.e. antibiotics, vitamins, hormones, heterocyclic

compounds), which are particularly important in the manufacturing of medicines. The mapping

indicates for a range of APIs that they are concentrated in a few sourcing countries, with little

potential for substitution with domestic production as the EU produces different products

compared to the ones imported. In this regard, given that APIs are potentially essential inputs for

producing a wide range of medicines, Chapter 5 of this staff working document provides a more

in-depth review of the EU’s potential strategic dependencies in the area of APIs.

An important number of dependent products are also identified in the renewables, digital

and electronics ecosystems as they are directly related to the green and digital transition.

The bottom-up analysis notably reveals that that the EU has a high level of foreign dependency

with respect to 17 products related to renewable energy production, green mobility and

digital/electronics (e.g. permanent magnets, electric accumulators, electric motors, radio

broadcast receivers, laptops, mobile phones).

The production of many green and digital products relies on various (critical) raw

materials. As highlighted above, several of these raw materials are identified by the bottom-up

mapping as dependent (e.g. lithium, cobalt, nickel, copper, chromium, molybdenum). For

example, the production of permanent magnets, which are used in different types of wind

turbines, is reliant on various raw materials. The bottom-up mapping indicates that not only the

relevant raw materials but also the permanent magnets themselves are foreign dependent goods.

As for green mobility, the dependent electric accumulators might use raw materials on which the

EU is foreign dependent as well. More broadly, in the renewable ecosystem, several

40

Steel is a vital component in most of the EU’s industrial ecosystems. For this reason, the Staff Working Document

“Towards competitive and clean European steel” shows different policies that the EU already has at its disposal to

help the steel industry in its transformation – from research funding, through regulatory measures to trade

instruments.

41

See European Commission: Critical Raw Materials for Strategic Technologies and Sectors in the EU - A Foresight

Study, 2020

42

This is in line with the objectives of the European energy union, which aims at creating a reliable, affordable and

sustainable energy system.

25

dependencies may have an impact on the decarbonisation and continued proper functioning of

the EU electricity system.

43

For example, several hydrogen related technologies depend on

imports of raw materials for key components such as electrolysers and fuel cells. In the area of

digital, for example, some of the identified dependent raw materials are used in the production of

semi-conductors, the basic building blocks of all digital products and services. Chapter 5 of this

staff working document provides more in-depth reviews concerning Li-ion batteries and

hydrogen technologies.

The bottom-up product mapping faces a number of limitations when it comes to identifying

dependencies within the defence and aerospace ecosystem and can only provide tentative

insights. Identifying foreign dependent products within this ecosystem through a bottom-up

mapping faces a number of challenges given the lack of complete data (notably for

confidentiality reasons) and the required level of detail. For these reasons, in this ecosystem in

particular, the bottom-up methodology relying on trade data should be complemented with other

more qualitative, ecosystem-specific assessments (at a more granular level). This specific

assessment will be tackled through the EU Observatory on Critical Technologies for civil,

defence and space industries.

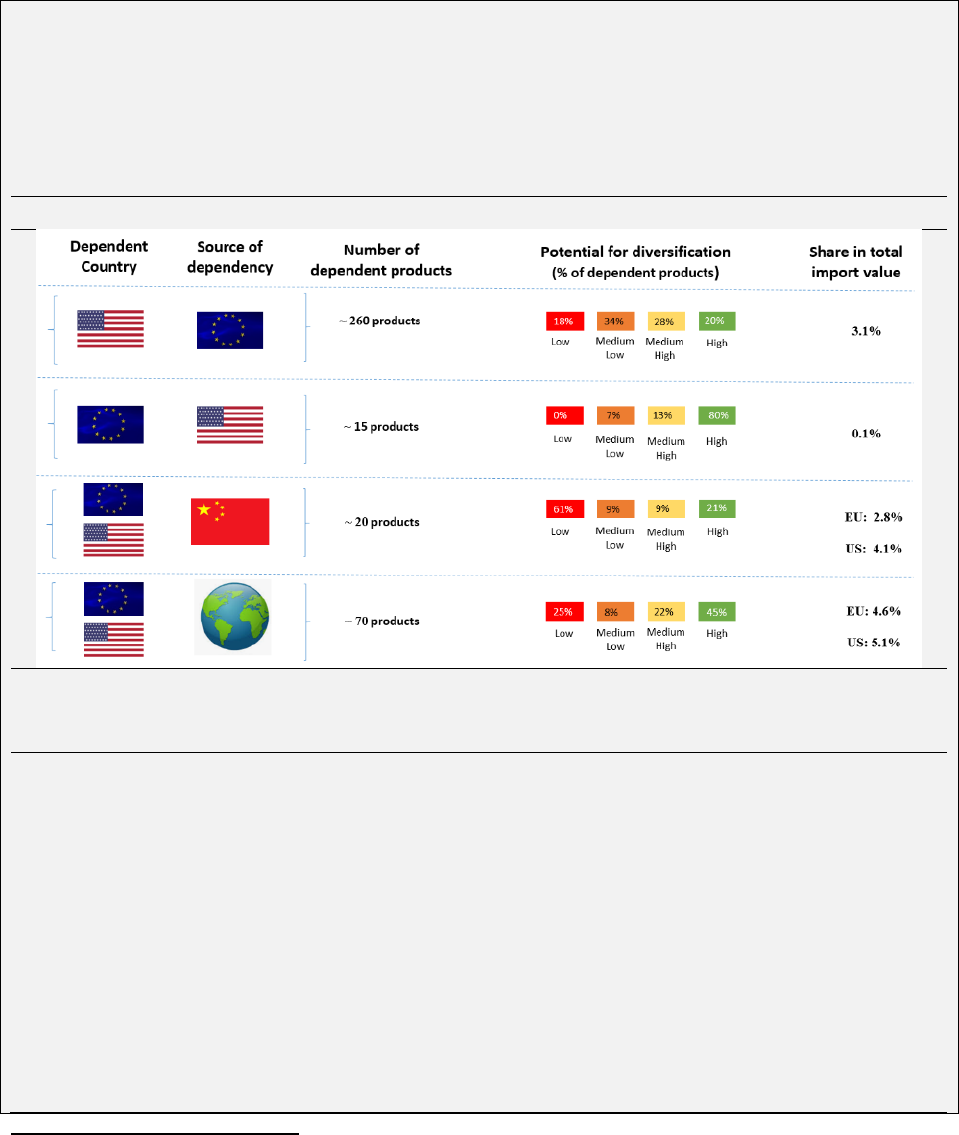

Box 4 – Reverse and common dependencies in products

The main trading partners of the EU (notably the US and China) are also conducting

comprehensive reviews of the resilience of their own strategic supply chains. The US issued

an Executive Order on America’s Supply Chains

44

with the goal of strengthening supply chain

resilience and security, building capacity and diversifying sources. Concerning China, a review

of strategic supply chains is part of the Chinese 5-year plan (5YP) which, among other

objectives, aims at minimising external dependencies.

Given the current global environment, this box intends to shed light on the foreign

dependencies in goods that the EU and the US have with each other, as well as their

common dependencies vis-à-vis the rest of the world and China specifically (being the main

source of dependencies for both the EU and the US). As a starting point, the analysis

identifies the general foreign dependencies in goods of the EU and the US based on two out of

the three the economic indicators detailed in Section 2.2.1. More precisely, in this context, a high

level of foreign dependency is associated with a low diversification of import sources (i.e. high

concentration) and a limited domestic capacity (i.e. low substitutability of imports with domestic

43

A dedicated study for the Commission (forthcoming, May 2021) assesses the resilience of the critical supply

chains for energy security and clean energy transition during and after the COVID-19 crisis. It assesses

dependencies and criticalities related to different key areas such as the cables, conductors and equipment needed to

transport and distribute electricity, the production of renewable energy sources (especially wind and solar energy),

the storage of electricity and smart grid technologies required for operating the electricity system.

44

President Biden signed on 24 February an Executive Order on America’s Supply Chains launching a

comprehensive review of US supply chains for semiconductors, high-capacity batteries, pharmaceuticals and

medical supplies and strategic and critical minerals that will identify ways to secure supply chains against risks and

vulnerabilities. This review should be completed in 100 days (i.e. by early June). There will also be an in-depth

one-year review of six industrial bases covering defence, public health and biological preparedness, ICT,

transportation, energy, and agricultural commodities and food production.

26

production) as defined above.

45

Then, relying on the identified general foreign dependencies, the

analysis identifies those products where the US is highly dependent on the EU (“reverse

dependencies”) and vice-versa. Furthermore, “common dependencies” that the EU and the US

share vis-à-vis China and the world can also be identified. These identified reverse and common

dependencies are then further assessed by evaluating their potential for diversification using the

existing global trade networks as a proxy.

46

Overview of EU & US dependencies in sensitive ecosystems

Note: This table focuses on potentially sensitive ecosystems; The chart shows products where the US can be considered

dependent on the EU (first row); the EU dependent on the US (second row); common dependencies for the EU and the US on

China (third row); and common dependencies for the EU and the US on the world (fourth row)

Source: Commission analysis based on BACI database

The EU is less dependent on the US than vice-versa and both countries have important

dependencies vis-à-vis China. The US appears more dependent on imported products from

the EU than vice-versa. This is in line with the aggregate finding that the US has more

concentrated sources of imports compared to the EU (see Graph 4). In addition, the EU and the

US have an important amount of common dependencies vis-à-vis China. Furthermore, for

many of these common EU/US dependencies vis-à-vis China, the potential for trade

diversification to other countries (beyond China) appears limited given the current structure of

world trade where China takes up a very central position for these dependent products.

These common dependencies of the EU and the US on China include various goods in

sensitive ecosystems. Notable examples include products in the Health ecosystem (e.g.

various Covid-related goods and APIs including vitamins, antibiotics, hormones) and goods

45

The indicator corresponding to the importance of extra EU imports in total demand is not used in this analysis, as

it is specific to the EU context and cannot be mirrored within the US.

46

To measure the potential of diversification of different products, an indicator measuring the risk of centrality is

used (IMF Working Paper No. 17/30), which identifies situations where an exporter is central to a large number of

countries in a trade network. The classification of the potential for diversification across four categories is done

based on the quartiles of the distribution of the indicator taking into account more than 5000 products.

27

belonging to the ecosystems relevant for the EU’s twin transition (e.g. permanent magnets,

electric accumulators, cell phones, radio broadcast receivers). Similarly as for the bottom-up

mapping carried out in chapter 2 of this staff working document, these analytical findings

would need to be further corroborated with qualitative analysis and discussion with Member

States and industry.

Common and reverse dependencies (EU & US) in sensitive ecosystems: examples at