Wickes Group plc Prospectus March 2021

Wickes Group plc Prospectus

March 2021

DOCUMENT AND ANY ACCOMPANYING DOCUMENTS ARE IMPORTANT AND REQUIRE YOUR IMMEDIATE ATTENTION. If you

are in any doubt as to the action you should take, you should consult your stockbroker, bank manager, solicitor, accountant or other

professional adviser authorised under the Financial Services and Markets Act 2000 (as amended) (“FSMA”) immediately, if you are in the

United Kingdom, or from another appropriately authorised independent professional adviser if you are taking advice in a territory outside

the United Kingdom.

This document comprises a prospectus (the “Prospectus”) relating to Wickes Group plc (the “Company” or “Wickes”) prepared in

accordance with the Prospectus Regulation Rules of the Financial Conduct Authority (the “FCA”) made under section 73A of FSMA. This

Prospectus has been filed with, and approved by, the FCA in accordance with section 87A of FSMA and has been made available to the

public in accordance with the Prospectus Regulation Rules by the same being made available, free of charge, at www.wickesplc.co.uk and

at the Company’s registered office at Vision House, 19 Colonial Way, Watford WD24 4JL, United Kingdom.

This Prospectus has been approved by the FCA, as competent authority under Regulation (EU) 2017/1129 (as it forms part of retained

European Union (“EU”) law as defined in the EU (Withdrawal) Act 2018) (the “Prospectus Regulation”). The FCA only approves this

Prospectus as meeting the standards of completeness, comprehensibility and consistency imposed by the Prospectus Regulation; such

approval should not be considered as an endorsement of the quality of the securities that are the subject of this Prospectus. Investors

should make their own assessment as to the suitability of investing in the securities. This Prospectus has been prepared in connection with

the proposed demerger of the Wickes Group from the Travis Perkins Group and on the assumptions that the Resolutions will be passed

at the General Meeting and that the Demerger will become effective as proposed.

Applications will be made to the FCA for all of the ordinary shares of the Company (the “Wickes Shares”) to be admitted to the premium

segment of the Official List of the FCA (the “Ofcial List”) and to trading on the main market of the London Stock Exchange plc (the

“London Stock Exchange”) for listed securities (together, “Admission”). It is expected that Admission will become effective, and that

dealings in the Wickes Shares will commence, at 8.00 a.m. (UK time) on 28 April 2021. No application is currently intended to be made for

the Wickes Shares to be admitted to listing or dealing on any other exchange.

The directors of the Company, whose names appear on page 33 of this Prospectus (the “Directors”), and the Company accept responsibility

for the information contained in this Prospectus. To the best of the knowledge of the Company and the Directors, the information contained

in this Prospectus is in accordance with the facts and contains no omission likely to affect the import of such information.

Wickes Group plc

(incorporated under the Companies Act 2006 and registered in England and Wales with registered number 12189061)

Prospectus

Admission to the premium listing segment of the Ofcial List and to trading on

the London Stock Exchange of the Wickes Shares

Joint Financial Advisors and Joint Sponsors

Citigroup Deutsche Bank

Issued and fully paid share capital immediately following Admission

Number

252,143,923

Nominal value

£0.10

This document does not constitute an offer or invitation to sell or issue, or a solicitation of an offer or invitation to purchase or

subscribe for, any securities offered by any person in the Company in any jurisdiction in which it is unlawful for such person

to make such an offer or solicitation. This document is intended solely for holders of Travis Perkins Shares. No Wickes Shares

have been marketed to, or are available for purchase by, the public in the United Kingdom or elsewhere in connection with the

introduction of the Wickes Shares to the premium listing segment of the Ofcial List or the Demerger. This document does not

constitute an offer or invitation for any person to subscribe for or purchase any securities in the Company or any other company.

Investors should read the entire Prospectus and, in particular, examine all the risks that might be relevant in connection with

an investment in the Wickes Shares. See Part I: “Risk Factors” for a discussion of certain risks and other factors that should be

considered prior to any investment in the Wickes Shares.

Citigroup Global Markets Limited (“Citi”) is authorised in the United Kingdom by the PRA and regulated in the United Kingdom by the PRA and

the FCA. Citi is acting exclusively as financial adviser and sponsor for the Company and Travis Perkins plc and for no one else in connection with

the Demerger and Admission or any other matters referred to in this document and will not be responsible to anyone other than the Company

and Travis Perkins plc for providing the protections afforded to clients of Citi nor for providing advice in connection with the Demerger, Admission,

or any other matters referred to in this document. Neither Citi nor any of its affiliates, directors or employees owes or accepts any duty, liability or

responsibility whatsoever (whether direct or indirect, consequential, whether in contract, in tort, in delict, under statute or otherwise) to any person

who is not a client of Citi in connection with the Demerger, Admission, this document, any statement contained herein, or otherwise.

Apart from the responsibilities and liabilities, if any, which may be imposed on Citi by FSMA or the regulatory regime established thereunder or

under the regulatory regime of any other applicable jurisdiction, where exclusion of liability under the relevant regulatory regime would be illegal,

void or unenforceable, neither Citi nor any of its affiliates, directors, officers, employees or advisers accepts any responsibility whatsoever for the

contents of this document, including its accuracy, completeness and verification or for any other statement made or purported to be made by it,

or on its behalf, in connection with the Company or its subsidiaries, Wickes Shares or the Demerger or Admission. Citi and its affiliates, directors,

officers, employees and advisers accordingly disclaim, to the fullest extent permitted by applicable law, all and any liability whether arising in tort,

contract or otherwise (save as referred to above) which they might otherwise be found to have in respect of this document or any such statement.

No representation or warranty, express or implied, is made by Citi or any of its affiliates, directors, officers, employees or advisers as to the

accuracy, completeness, verification or sufficiency of the information set out in this document, and nothing in this document will be relied upon as

a promise or representation in this respect, whether or not to the past or future.

Deutsche Bank AG is a joint stock corporation incorporated with limited liability in the Federal Republic of Germany, with its head office in

Frankfurt am Main where it is registered in the Commercial Register of the District Court under number HRB 30 000. Deutsche Bank AG is

authorised under German Banking Law banking law. The London branch of Deutsche Bank AG is registered in the register of companies

for England and Wales (registration number BR000005) with its registered address and principal place of business at Winchester House, 1

Great Winchester Street, London EC2N 2DB. Deutsche Bank AG is authorised and regulated by the European Central Bank and the German

Federal Financial Supervisory Authority (BaFin). With respect to activities undertaken in the UK, Deutsche Bank AG is authorised by the PRA

with deemed variation of permission. It is subject to regulation by the FCA and limited regulation by the PRA. Details about the Temporary

Permissions Regime, which allows EEA-based firms to operate in the UK for a limited period while seeking full authorisation, are available on

the FCA’s website. In connection with the Demerger and Admission, Deutsche Bank is acting through its London branch (“Deutsche Bank”

and together with Citi, the “Joint Sponsors”). Deutsche Bank is acting as financial adviser and sponsor exclusively for the Company and Travis

Perkins plc, and no one else in connection with the Demerger and Admission, and Deutsche Bank will not regard any other person (whether

or not a recipient of this document) as a client in relation to the Demerger or Admission and will not be responsible to anyone other than the

Company for providing the protections afforded to its clients or for providing advice in relation to the Demerger or Admission or any other

transaction, matter or arrangement referred to in this document.

Apart from the responsibilities and liabilities, if any, which may be imposed on Deutsche Bank by FSMA or the regulatory regime established

thereunder or under the regulatory regime of any other applicable jurisdiction, where exclusion of liability under the relevant regulatory

regime would be illegal, void or unenforceable, neither Deutsche Bank nor any of its affiliates, directors, officers, employees or advisers

accepts any responsibility whatsoever for the contents of this document, including its accuracy, completeness and verification or for any

other statement made or purported to be made by it, or on its behalf, in connection with the Company or its subsidiaries, Wickes Shares or

the Demerger or Admission. Citi and Deutsche Bank and their affiliates, directors, officers, employees and advisers accordingly disclaim,

to the fullest extent permitted by applicable law, all and any liability whether arising in tort, contract or otherwise (save as referred to above)

which they might otherwise be found to have in respect of this document or any such statement. No representation or warranty, express

or implied, is made by Deutsche Bank or any of its affiliates, directors, officers, employees or advisers as to the accuracy, completeness,

verification or sufficiency of the information set out in this document, and nothing in this document will be relied upon as a promise or

representation in this respect, whether or not to the past or future.

Investors acknowledge they have not relied on the Joint Sponsors or any person affiliated with the Joint Sponsors in connection with any

investigation of the accuracy of any information contained in this Prospectus or that investment decision. Each investor must rely on such

investor’s own examination, analysis and enquiry of the Company and Wickes Shares. Investors should be aware that an investment in

the Company involves a degree of risk and that, if certain risks described in the Prospectus occur, investors may find their investment

materially and adversely affected. The contents of this document should not be construed as legal, business, financial or tax advice. None

of the Company, Citi, Deutsche Bank or any of their respective representatives is making any representation to any prospective investor

regarding the legality of an investment in the Wickes Shares by such prospective investor under the laws applicable to such prospective

investor. Each prospective investor should consult such investor’s own legal, business, financial or tax advisers for advice.

This Prospectus does not constitute an offer to sell or an invitation to subscribe for, or the solicitation of an offer to buy or to subscribe for,

any securities to any person in any jurisdiction.

NOTICE TO US SHAREHOLDERS

The Wickes Shares have not been, and will not be, registered under the US Securities Act of 1933, as amended (the “US Securities

Act”) or with any securities regulatory authority of any state of the United States, and may not be offered or sold in the United States

absent registration under the US Securities Act an exemption from, or in transactions not subject to, the registration requirements of the

US Securities Act, and in compliance with any applicable State or local securities laws. The Wickes Shares are expected to be issued in

reliance on the position taken by the Division of Corporation Finance of the US Securities and Exchange Commission (“SEC”), set forth in

Staff Legal Bulletin No. 4, that shares distributed in a spin-off do not require registration under the US Securities Act if, as is the case with

respect to the Demerger, certain conditions are satisfied. None of the SEC, any other US federal or state securities commission or any US

regulatory authority has approved or disapproved of the Wickes Shares nor have such authorities reviewed, passed upon or endorsed the

accuracy or adequacy of this Prospectus. Any representation to the contrary is a criminal offence.

NOTICE TO OVERSEAS SHAREHOLDERS

Overseas Shareholders may be affected by the laws of other jurisdictions in relation to the Demerger. Overseas Shareholders should

inform themselves about and observe all applicable legal requirements.

It is the responsibility of any person into whose possession this document comes to satisfy themselves as to the full observance of the laws

of the relevant jurisdiction in connection with the allotment and issue of Wickes Shares following the Demerger, including the obtaining of

any governmental, exchange control or other consents which may be required and/or compliance with other necessary formalities which are

required to be observed and the payment of any issue, transfer or other taxes or levies due in such jurisdiction.

This document has been prepared for the purposes of complying with English law and the rules of the FCA, and the information disclosed

may not be the same as that which would have been disclosed if this document had been prepared in accordance with the laws of jurisdictions

outside the UK. No action has been taken or will be taken by the Company to permit a public offering of the Wickes Shares or to permit the

possession, issue or distribution of this Prospectus in any jurisdiction where action for that purpose may be required. Accordingly, neither

this Prospectus nor any advertisement nor any other offering material may be distributed or published in any jurisdiction, except under

circumstances that will result in compliance with any applicable laws and regulations. Persons into whose possession this Prospectus

comes should inform themselves about and observe any such restrictions. Any failure to comply with these restrictions may constitute a

violation of the securities laws of any such jurisdiction.

Overseas Shareholders should consult their own legal and tax advisers with respect to the legal and tax consequences of the Demerger

in their particular circumstances.

This document is dated 24 March 2021.

4

TABLE OF CONTENTS

SUMMARY INFORMATION ............................................................................................................ 5

EXPECTED TIMETABLE OF PRINCIPAL EVENTS ....................................................................... 12

PART I RISK FACTORS ................................................................................................................. 13

PART II PRESENTATION OF FINANCIAL AND OTHER INFORMATION ..................................... 29

PART III DIRECTORS, SECRETARY, REGISTERED AND HEAD OFFICE AND ADVISERS ...... 33

PART IV BUSINESS DESCRIPTION AND MARKET OVERVIEW ................................................. 34

PART V DIRECTORS, SENIOR MANAGEMENT AND CORPORATE GOVERNANCE ................ 63

PART VI SELECTED FINANCIAL INFORMATION ......................................................................... 69

PART VII OPERATING AND FINANCIAL REVIEW ........................................................................ 73

PART VIII CAPITALISATION AND INDEBTEDNESS..................................................................... 91

PART IX HISTORICAL FINANCIAL INFORMATION ...................................................................... 93

PART X UNAUDITED PRO FORMA STATEMENT OF NET ASSETS ........................................... 129

PART XI TAXATION ........................................................................................................................ 133

PART XII ADDITIONAL INFORMATION ......................................................................................... 138

PART XIII DEFINITIONS ................................................................................................................. 180

5

SUMMARY INFORMATION

A. INTRODUCTION AND WARNINGS

A.1.1 Name and international securities identier number (“ISIN”) of the securities

Ordinary shares in the capital of Wickes Group plc (the “Company” or “Wickes”) with a nominal

value of £0.10 (the “Wickes Shares”).

ISIN code GB00BL6C2002.

A.1.2 Identity and contact details of the issuer, including its legal entity identier (“LEI”)

The Company is a public limited company. Its registered office is at Vision House, 19 Colonial

Way, Watford WD24 4JL, United Kingdom. The Company’s telephone number is +44 (0)19 2365

6600 and its LEI is 213800IEX9ZXJRAOL133.

A.1.3 Identity and contact details of the competent authority approving this Prospectus

This Prospectus has been approved by the FCA, as competent authority, with its head office

at 12 Endeavour Square, London E20 1JN and telephone number: +44 (0)20 7066 1000, in

accordance with Regulation (EU) 2017/1129 (together with the delegated acts, implementing

acts and technical standards thereunder as such legislation forms part of retained EU law, the

“Prospectus Regulation”).

A.1.4 Date of approval of this Prospectus

This Prospectus was approved on 24 March 2021.

A.1.5 Warning

This summary has been prepared in accordance with Article 7 of the Prospectus Regulation

and should be read as an introduction to the Prospectus. Any decision to invest in the Wickes

Shares should be based on consideration of the Prospectus as a whole by the investor. Any

investor could lose all or part of their invested capital and, where any investor’s liability is not

limited to the amount of the investment, it could lose more than the invested capital. Civil liability

attaches only to those persons who have tabled the summary, including any translation thereof,

but only if the summary is misleading, inaccurate or inconsistent when read together with the

other parts of the Prospectus or if it does not provide, when read together with the other parts of

the Prospectus, key information in order to aid investors when considering whether to invest in

the Wickes Shares.

B. KEY INFORMATION ON THE ISSUER

B.1 Who is the issuer of the securities?

B.1.1 Domicile, legal form, jurisdiction of incorporation and country of operation

The Company is domiciled in England and Wales and was incorporated in England and Wales

under the Companies Act on 4 September 2019 as Wickes Group Limited with registered

number 12189061. Wickes Group Limited re-registered as a public limited company by shares

and changed its name to Wickes Group plc on 17 March 2021.

B.1.2 Principal activities

The principal activity of the Company is to act as the ultimate holding company of the Wickes

Group following the Demerger.

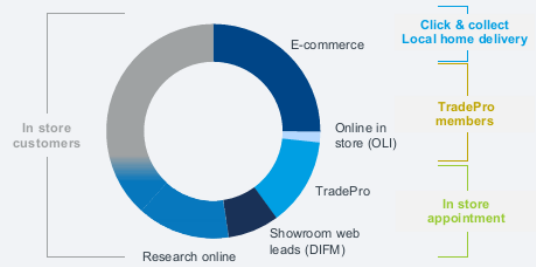

The Wickes Group is a digitally-led, service-enabled home improvement retailer, delivering

choice, convenience, value and best-in-class service to customers across the United Kingdom.

The Wickes Group’s mission is to be the home improver’s and the local tradesperson’s partner

of choice, with a vision for “a Wickes project in every home” and its purpose to “help the nation

feel houseproud”. The Wickes Group aims to support its customers however they decide to

undertake their home improvement projects through three tailored customer propositions aimed

at each customer segment: local trade; do-it-for-me; and do-it-yourself. The Wickes Group

drives sales through its estate of 233 retail stores, which support nationwide fulfilment from

convenient locations throughout the United Kingdom, and its website and TradePro mobile app

6

for trade members, which allow customers to research and order an extended range of the

Wickes Group’s products and services, arrange in-person or virtual design consultations, and

organise timely home delivery or “click-and-collect” from across the Wickes Group network.

B.1.3 Major shareholders

The Company was incorporated in anticipation of the Demerger and, as at 19 March 2021 (being

the latest practicable date prior to publication of this Prospectus) (the “Latest Practicable Date”),

is wholly owned by Travis Perkins. Immediately following the Demerger, the shareholders of the

Company, and the levels of their shareholdings, will be the same as the shareholders of Travis

Perkins as at the Record Time.

As at the Latest Practicable Date, insofar as it is known to the Company (by reference

to notifications to Travis Perkins made in accordance with the Disclosure Guidance and

Transparency Rules), the following persons are, directly or indirectly, interested in 3 per cent.

or more of Travis Perkins’ issued share capital and, assuming such persons do not acquire or

dispose of any Travis Perkins Shares and no changes are made to Travis Perkins’ issued share

capital (in each case, prior to the Record Time), the amount of such person’s holding of the total

voting rights in respect of Wickes Shares at Admission is expected to be as follows:

Shareholder

Percentage of total voting

rights at Admission

BlackRock Inc. ....................................................................... Less than 5 per cent.

Investec Asset Management ................................................. 5.05

Ninety One UK Limited .......................................................... 4.95

Harris Associates L.P. ........................................................... 4.92

OppenheimerFunds, Inc. ....................................................... 4.91

Sanderson Asset Management LLP ...................................... 4.89

B.1.4 Key managing directors

David Wood is Chief Executive Officer (“CEO”) of the Company.

Julie Wirth is Chief Financial Officer (“CFO”) of the Company.

B.1.5 Identity of the statutory auditors

The auditor of the Company since the date of its incorporation has been KPMG LLP, whose

registered office is at 15 Canada Square, Canary Wharf, London E14 5GL. KPMG LLP is a

member of the Institute of Chartered Accountants in England and Wales and has no material

interest in the Wickes Group.

B.2 What is the key nancial information regarding the issuer?

Selected historical key nancial information

The tables below set out selected key financial information for the Wickes Group as at and for

the 52-week periods ended 26 December 2020, 28 December 2019 and 29 December 2018.

7

Consolidated Prot or Loss and Other Comprehensive Income Data

For the Financial Year 2020, Financial Year 2019 and Financial Year 2018

Financial Year 2020 Financial Year 2019 Financial Year 2018

Adjusted

Adjusting

items

(1)

Total Adjusted

Adjusting

items

(1)

Total Adjusted

Adjusting

Items

(1)

Total

(£ millions)

Revenue .............................. 1,346.9 — 1,346.9 1,292.4 — 1,292.4 1,199.6 — 1,199.6

Cost of sales ........................ (837.8) — (837.8) (791.1) — (791.1) (729.9) — (729.9)

Gross prot ........................ 509.1 — 509.1 501.3 — 501.3 469.7 — 469.7

Selling costs ........................ (323.5) — (323.5) (303.1) — (303.1) (300.6) — (300.6)

Administrative expenses...... (104.0) (20.6) (124.6) (102.4) (39.6) (142.0) (93.2) (19.3) (112.5)

Operating prot ................. 81.6 (20.6) 61.0 95.8 (39.6) 56.2 75.9 (19.3) 56.6

Finance costs ...................... (32.1) — (32.1) (33.5) — (33.5) (34.5) — (34.5)

Prot before tax ................. 49.5 (20.6) 28.9 62.3 (39.6) 22.7 41.4 (19.3) 22.1

Tax....................................... (8.9) 6.3 (2.6) (11.8) 2.0 (9.8) (8.1) 0.9 (7.2)

Prot for the period and

total comprehensive

income ................................ 40.6 (14.3) 26.3 50.5 (37.6) 12.9 33.3 (18.4) 14.9

Note:

(1) In Financial Year 2020, adjusting items included £8.2 million arising from activities related to the Demerger, £10.2 million in impairment charges

relating to a small number of loss-making stores, £2.2 million in relation to restructuring the DIFM design consultant team, tax on adjusting

items of £(3.9) million and deferred tax rate change of £(2.4) million. In Financial Year 2019, adjusting items included Wickes Group separation

costs of £9.2 million, store impairment charge of £1.9 million, loss on legal entity restructuring of £26.6 million and IT impairment charges of

£0.7 million, restructuring costs of £1.2 million and tax on adjusting items of £(2.0) million. In Financial Year 2018, adjusting items included IT

impairment charges of £6.5 million, restructuring costs of £12.8 million, tax on adjusting items of £(3.5) million and deferred tax rate change of

£2.6 million.

Consolidated Balance Sheet Data

As at 26 December 2020, 28 December 2019 and 29 December 2018

26 December 2020 28 December 2019 29 December 2018

(£ millions)

Assets

Total non-current assets ................................ 802.0 886.3 950.1

Total current assets ....................................... 406.4 502.8 887.6

Total assets .................................................. 1,208.4 1,389.1 1,837.7

Equity and Liabilities ...................................

Total equity ................................................... 129.8 278.6 263.7

Total non-current liabilities............................. (713.1) (781.7) (820.9)

Total current liabilities .................................... (365.5) (328.8) (753.1)

Total liabilities .............................................. (1,078.6) (1,110.5) (1,574.0)

Total equity and liabilities ........................... 1,208.4 1,389.1 1,837.7

Consolidated Cash Flow Statement Data

For the Financial Year 2020, Financial Year 2019 and Financial Year 2018

Financial

Year 2020

Financial

Year 2019

Financial

Year 2018

(£ millions)

Net cash inflow from operating activities ....... 76.8 108.5 176.8

Net cash (outflow) from investing activities ... (19.9) (24.1) (41.3)

Net cash (outflow) from financing activities ... (75.8) (75.2) (125.9)

Net decrease/(increase) in cash and cash

equivalents ................................................... (18.9) 9.2 9.6

Cash and cash equivalents at the beginning

of the period................................................... 25.4 16.2 6.6

Cash and cash equivalents at the end of

the period ..................................................... 6.5 25.4 16.2

8

Selected pro forma key nancial information

This document presents certain pro forma financial information of the Wickes Group to illustrate the

impact of the Demerger on the net assets of the Wickes Group as if the Demerger had taken place on

26 December 2020.

The unaudited pro forma statement of net assets of the Wickes Group is based on the net assets of the

Wickes Group as at 26 December 2020 and has been prepared on the basis that the Demerger was

effective as of 26 December 2020 and in a manner consistent with the accounting policies adopted by the

Company in preparing its audited consolidated financial statements for the year ended 26 December 2020.

Because of its nature, the unaudited pro forma statement of net assets addresses a hypothetical situation

and, therefore, does not represent the Wickes Group’s actual financial position or results. It may not,

therefore, give a true picture of the Wickes Group’s financial position or results nor is it indicative of

the results that may, or may not, be expected to be achieved in the future. The pro forma statement

of net assets has been prepared for illustrative purposes only and in accordance with Annex 20 of the

PR Regulation.

9

Net assets of the

Wickes Group as

at 26 December

2020

Adjustment for

cash settlement

of intercompany

balances by the

Travis Perkins

Group

Adjustment

for the

repayment

of rate relief

Adjustment for

transaction

costs in

connection with

the Demerger

Adjustment

for settlement

of remaining

intercompany

balances with

the Travis

Perkins Group Pro Forma

Note 1

£’m

Note 2

£’m

Note 3

£’m

Note 4

£’m

Note 5

£’m £’m

Non-current assets

Goodwill ............................. 8.4 — — — — 8.4

Other intangible assets ...... 12.3 — — — — 12.3

Property, plant and

equipment .......................... 103.1 — — — — 103.1

Right-of-use assets............ 654.2 — — — — 654.2

Deferred tax asset ............. 24.0 — — — — 24.0

Total non-current assets . 802.0 — — — — 802.0

Current assets

Inventories ......................... 138.3 — — — — 138.3

Trade and other

receivables ........................ 261.6 (156.1) — — (30.0) 75.5

Cash and cash equivalents 6.5 156.1 (32.6) (5.0) — 125.0

Total current assets ......... 406.4 — (32.6) (5.0) (30.0) 338.8

Total assets ...................... 1,208.4 — (32.6) (5.0) (30.0) 1,140.8

Non-current liabilities

Lease liabilities .................. 712.8 — — — — 712.8

Long-term provisions ......... 0.3 — — — — 0.3

Total non-current

liabilities ........................... 713.1 — — — — 713.1

Current liabilities

Lease liabilities .................. 77.2 — — — — 77.2

Trade and other payables.. 277.9 — (32.6) — — 245.3

Short-term provisions ........ 10.4 — — — — 10.4

Total current liabilities 365.5 — (32.6) — — 332.9

Total liabilities .................. 1,078.6 — (32.6) — — 1,046.0

Net assets/(liabilities) 129.8 — — (5.0) (30.0) 94.8

Notes:

(1) The net assets of the Wickes Group as at 26 December 2020 have been extracted without material adjustment from the Group’s audited

consolidated financial statements as at and for the year ended 26 December 2020.

(2) The adjustment in Note 2 reflects the £156.1 million cash settlement of certain intercompany balances owed by the Travis Perkins Group to the

Wickes Group as part of the pre-Demerger Reorganisation in order to provide that the Wickes Group had a cash balance of £130.0 million as at

26 December 2020. On the settlement of these intercompany balances immediately prior to the Demerger the Wickes Group will derecognise

an equivalent amount of the intercompany receivables due from the Travis Perkins Group.

(3) The adjustment in Note 3 reflects the voluntary repayment of £32.6 million of business rates relief claimed by the Wickes Group in April to

December 2020.

(4) The adjustment in Note 4 reflects transaction costs that are directly attributable to the Demerger that are being borne by the Wickes Group and

which had not been incurred at 26 December 2020. These comprise estimated professional adviser fees and exclude one-off costs arising from

the separation of the Wickes Business from the Travis Perkins Group which are estimated to be £5.0 million.

(5) The adjustment in Note 5 reflects the settlement of the remaining intercompany balance by the Travis Perkins Group to the Wickes Group

achieved via the payment of dividends equal to a total amount of £30.0 million by the Wickes Group to the Travis Perkins Group, left outstanding

as an intercompany balance and offset against the remaining equivalent intercompany balances owed by the Travis Perkins Group.

(6) Each of the adjustments in Notes 2, 3, 4 and 5 are non-recurring items.

No adjustment has been made to reflect any other change in the Wickes Group financial position in this

period since 26 December 2020.

B.3 What are the key risks that are specic to the issuer?

Risks related to the Wickes Group’s business

The Wickes Group operates in the highly competitive UK home improvement market, and

competitive behaviour could negatively impact customer demand and sales.

The market for home improvement purchases, and as a result the Wickes Group’s business,

may be adversely affected by economic and political conditions and other factors influencing

disposable income in the United Kingdom.

10

The Wickes Group faces risks related to the impact of COVID-19 and other communicable

diseases or pandemics in the future.

The Wickes Group relies on its reputation as a trusted provider of high-quality home improvement

products and services at good value, and any deterioration in its reputation could adversely

affect its business.

The Wickes Group may experience interruptions involving its suppliers.

A failure to implement the Wickes Group’s integrated growth strategy may adversely affect

its business.

The Wickes Group may not be able to accurately predict and plan for changes in customer demand

and preferences, which could lead to reductions in sales or negatively impact operating margins.

A failure of a key information technology system or process, including due to a cyber-attack,

could adversely affect the Wickes Group’s operations or cause a loss of customer data.

The Wickes Group faces risks relating to any property damage or interruption of operations at

one of its delivery centres, which could significantly interrupt its operating activities.

Risks related to the Demerger

Wickes will incur new costs in its transition to a standalone public company and its management

team will be required to devote substantial time to new compliance matters.

Following the Demerger, Wickes will face new challenges as an independent company, which

could adversely affect its financial or operating performance.

The Wickes Group utilises Travis Perkins for the continued provision of certain transitional

services (specifically relating to IT and human resources), and a material interruption could

negatively impact the Wickes Group’s operating activities.

C. KEY INFORMATION ON THE SECURITIES

C.1 What are the main features of the securities?

C.1.1 Type, class and ISIN

The Wickes Shares are fully paid ordinary shares with a nominal value of £0.10 each. The

Company has, and on Admission will have, one class of ordinary shares, comprising the entire

issued share capital of the Company. On Admission, the Wickes Shares will be registered with

ISIN number GB00BL6C2002 and SEDOL number BL6C200.

C.1.2 Currency, denomination, par value, number of securities issued and duration

The currency of the Wickes Shares is pounds sterling.

On Admission, the number of Wickes Shares in issue will be equal to the number of Travis

Perkins Shares in issue at the Record Time, all of which will be fully paid or credited as fully paid.

At the Latest Practicable Date, Travis Perkins’ share capital consisted of 252,143,923 ordinary

shares and therefore the Company’s share capital also consisted of 252,143,923 ordinary

shares. Further Travis Perkins Shares may be issued by Travis Perkins to satisfy entitlements

under the Travis Perkins Share Plans, although it is not currently anticipated that any further

Travis Perkins Shares will be issued. Any additional Travis Perkins Shares will, if issued, be

issued prior to the Record Time and a corresponding number of Wickes Shares will also be

issued prior to the Record Time.

C.1.3 Rights attached to the Wickes Shares

The rights attaching to the Wickes Shares will be uniform in all respects and they will form a

single class for all purposes, including with respect to voting and for all dividends and other

distributions thereafter declared, made or paid on the Company’s share capital.

Subject to the provisions of the Companies Act, any equity securities issued by the Company

for cash must first be offered to the holders of Wickes Shares (“Wickes Shareholders”) in

proportion to their holdings of Wickes Shares. The Companies Act and Listing Rules allow for

11

the disapplication of pre-emption rights which may be waived by a special resolution of the

Wickes Shareholders, whether generally or specifically, for a maximum period not exceeding

five years.

On a show of hands, every Wickes Shareholder who is present in person shall have one vote

and, on a poll, every Wickes Shareholder present in person or by proxy shall have one vote per

Wickes Share.

Except as provided by the rights and restrictions attached to any class of shares, Wickes

Shareholders will under general law be entitled to participate in any surplus assets in a winding-

up in proportion to their shareholdings.

C.1.4 Rank of securities in the issuer’s capital structure in the event of insolvency

The Wickes Shares do not carry any rights with respect to capital to participate in a distribution

(including on a winding-up) other than those that exist as a matter of law. The Wickes Shares

will rank pari passu in all respects.

C.1.5 Restrictions on the free transferability of the securities

The Wickes Shares are freely transferable and there are no restrictions on transfer.

C.1.6 Dividend or payout policy

Wickes is a strongly cash generative business and the Board recognises the importance of

balancing investment in the business with dividends to shareholders. The Board intends to

adopt a progressive dividend policy and currently expects to start with a dividend of 30 per

cent. of adjusted profit after tax in respect of the full financial year ending 1 January 2022, split

approximately one-third and two-thirds between interim and final dividends, respectively. The

Company intends to put in place a dividend re-investment plan following Admission.

C.2 Where will the securities be traded?

Application will be made to the FCA for all of the Wickes Shares, issued and to be issued, to be

admitted to the premium listing segment of the Official List and to the London Stock Exchange

for such Wickes Shares to be admitted to trading on the London Stock Exchange’s main market

for listed securities.

C.3 What are the key risks that are specic to the securities?

There is no prior trading record for the Wickes Shares and an active trading market for the

Wickes Shares may not develop or be sustained.

Significant trading volumes of Wickes Shares in the public market in the period post-Demerger

and subsequently could impact the share price.

The Wickes Shares are priced in pounds sterling and will be quoted and traded in pounds

sterling. In addition, any dividends the Company may pay will be declared and paid in pounds

sterling. Accordingly, holders of the Wickes Shares resident outside the United Kingdom are

subject to risks arising from adverse movements in the value of their local currencies against the

pound sterling.

D. KEY INFORMATION ON THE ADMISSION TO TRADING ON A REGULATED MARKET

D.1 Under which conditions and timetable can I invest in this security?

It is expected that admission of the Wickes Shares to listing and trading on the London Stock

Exchange will become effective and that dealings will commence at 8.00 a.m. (UK time) on

28 April 2021.

D.2 Why is this Prospectus being produced?

This Prospectus does not constitute an offer or invitation to any person to subscribe for or

purchase any shares in the Company. It is intended solely for holders of Travis Perkins Shares

and has been prepared in connection with the application to list the Wickes Shares on the

premium listing segment of the Official List and to admit the Wickes Shares to trading on the

London Stock Exchange.

LR 2.2.4(1)

(11) 4.8

(1) 18.5.1

12

EXPECTED TIMETABLE OF PRINCIPAL EVENTS

Event Time and date

Publication of this Prospectus and the Travis Perkins

Circular

24 March 2021

Latest time and date for receipt of Proxy Forms and

CREST electronic proxy appointment instruction

10.4 a.m. on 23 April 2021

Travis Perkins’ Annual General Meeting 10.00 a.m. on 27 April 2021

General Meeting

(1)

10.45 a.m. on 27 April 2021

Announcement of result of General Meeting 27 April 2021 (after the General Meeting)

Latest time and date for transfers of Travis Perkins

Shares to be registered in order for the transferee to be

registered at the Record Time

6.00 p.m. on 27 April 2021

Record Time for determining entitlement to the

Demerger Dividend

6.00 p.m. on 27 April 2021

Demerger Dividend to Qualifying Travis Perkins

Shareholders

After 6.00 p.m. on 27 April 2021

Admission and commencement of dealings in Wickes

Shares on the London Stock Exchange

8.00 a.m. on 28 April 2021

CREST accounts credited in respect of Wickes Shares

in uncertificated form

As soon as practicable after 8.00 a.m. on

28 April 2021

Posting of share certificates for Wickes Shares Week commencing 10 May 2021

Notes:

(1) The start time for the General Meeting may be delayed if Travis Perkins’ annual general meeting runs over 10.45 a.m., in which case the General

Meeting shall commence immediately after Travis Perkins’ annual general meeting is concluded or adjourned.

All references to time in this document are to London time unless otherwise stated.

The dates given are based on the Company’s current expectations and may be subject to change. If any of the times or dates above change, Travis

Perkins will give notice of the change by issuing an announcement through a Regulatory Information Service.

13

PART I

RISK FACTORS

Any investment in the Wickes Shares is subject to a number of risks. Prior to investing in the Wickes

Shares, prospective investors should carefully consider the risk factors associated with any investment in

the Wickes Shares, the Wickes Group’s business and the industry in which it operates, together with all

other information contained in this Prospectus, including, in particular, the risk factors described below.

Prospective investors should note that the risks relating to the Wickes Group, its industry and the Wickes

Shares summarised in the section of this Prospectus headed “Summary Information” are the risks that

the Directors and the Company believe to be the most essential to an assessment by a prospective

investor of whether to consider an investment in the Wickes Shares. However, as the risks which the

Wickes Group faces relate to events and depend on circumstances that may or may not occur in the

future, prospective investors should consider not only the information on the key risks summarised in

the section of this Prospectus headed “Summary Information” but also, among other things, the risks

and uncertainties described below.

The risk factors described below are not an exhaustive list or explanation of all risks which investors may

face when making an investment in the Wickes Shares and should be used as guidance only. Additional

risks and uncertainties relating to the Wickes Group that are not currently known to the Wickes Group,

or that the Wickes Group currently deems immaterial, may individually or cumulatively also have a

material adverse effect on the Wickes Group’s business, results of operations and/or financial condition

and, if any such risk should occur, the price of the Wickes Shares may decline and investors could lose

all or part of their investment. An investment in the Wickes Shares involves complex financial risks and

is suitable only for investors who (either alone or in conjunction with an appropriate financial or other

adviser) are capable of evaluating the merits and risks of such an investment and who have sufficient

resources to be able to bear any losses that may result therefrom. Investors should consider carefully

whether an investment in the Wickes Shares is suitable for them in the light of the information in this

Prospectus and their personal circumstances.

The order in which the following risk factors are presented does not necessarily reect the

likelihood of their occurrence.

Risks related to the Wickes Group’s business

The Wickes Group operates in the highly competitive UK home improvement market, and

competitive behaviour could negatively impact customer demand and sales.

The UK market for home repair, maintenance and improvement products and services is highly

competitive, particularly with respect to customer experience, price, quality, availability, product and

delivery options, as well as digital capabilities. With respect to the Wickes Group’s stores, it also

competes based on store location and appearance as well as presentation of merchandise.

The Wickes Group’s competitors include other national home improvement retailers, as well as local

home improvement retailers and a variety of specialty design and home decorating stores in many

of the cities and towns where the Wickes Group’s stores are located, as well as online retailers. New

competitors could also emerge, including as a result of a non-UK home improvement or generalist

retailer expanding into the United Kingdom or merging with an existing UK home improvement retailer.

Consolidation in the industry could also alter the competitive landscape.

In the past, competitors have attempted to use aggressive pricing strategies in order to gain market

share, including for example Bunnings following its purchase of Homebase and brief entry into the UK

market from 2016 to 2018. This created market disruption which negatively affected the Wickes Group’s

market share, sales volumes and revenue. Competitors may also target certain of the Wickes Group’s

customer markets, for example, by offering a more attractive proposition for local trade customers, or

aiming to significantly improve customer service generally or competing kitchen and bathroom service

offerings, or any future do-it-for-me (“DIFM”) services offered by the Wickes Group. There can be no

assurance that existing or future competitors will not undertake similar strategies in the future, which

could negatively impact the Wickes Group’s market share and result in defensive pricing and other

strategies being undertaken by the Wickes Group in response. In particular, because DIFM services are

a strategic growth area for the Wickes Group, significantly increased competition – whether from new

entrants, or a return to this market by previous market participants – for these customers could have a

significant impact on the Wickes Group’s customer proposition and revenue from DIFM services.

14

The Wickes Group also competes with a variety of generalist retailers, including discounters and local

grocers, as well as online retailers such as Amazon, which sell various products offered by the Wickes

Group even if they do not specialise in home improvement products. As a result, the Wickes Group faces

competition for its target DIY and trade customers across a variety of the product lines that it offers.

Some of these competitors may have better market presence, name or brand recognition, financial

resources, supply chains, distribution platforms, economies of scale and/or lower cost bases than the

Wickes Group, in particular as compared to the Wickes Group’s historical operations as part of the

Travis Perkins Group, which could allow them to offer a wider range of products or products at lower

prices than the Wickes Group and to respond more swiftly to changes in market conditions. During

periods of deteriorating economic conditions, customers may become increasingly price-conscious and

competitors may respond accordingly in order to maintain volume. Certain competitors may also seek to

offer greater choice and convenience than the Wickes Group.

Actions taken by the Wickes Group’s competitors, as well as actions taken by it to maintain its

competitiveness and reputation, may place pressure on its pricing strategy, margins and profitability. The

Wickes Group’s competitors may also merge or form strategic partnerships, thus achieving economies

of scale in buying, distribution and logistics, which could cause additional competitive pressure for the

Wickes Group. There can be no assurance that the Wickes Group will be able to respond adequately

to these multiple sources and forms of competition, whether from existing competitors or new market

entrants. As a result of the above, or as a result of increasing competitive pressure due to factors

beyond the Wickes Group’s control, its business, results of operations, financial condition or prospects

could be materially adversely affected.

The market for home improvement purchases, and as a result the Wickes Group’s business,

may be adversely affected by economic and political conditions and other factors inuencing

disposable income in the United Kingdom.

The Wickes Group’s financial performance depends significantly on the strength of the UK home

improvement market, which is in turn influenced by the housing market in the United Kingdom. Trends

in home improvement, housing repair and maintenance expenditure have historically been linked to

leading housing market indicators, such as housing turnover and mortgage approvals. As a result, if

economic or political conditions lead to low growth levels, negatively impacting the UK housing market,

this may create uncertainty in the Wickes Group’s strategic business planning and negatively impact

demand for the Wickes Group’s products and services.

The UK housing market can be affected by a variety of economic factors, including inflation, real

disposable income, salaries, interest rates, the availability of consumer credit and consumer confidence,

as well as global economic conditions, health concerns (including related to COVID-19, see “—The

Wickes Group faces risks related to the impact of COVID-19 and other communicable diseases or

pandemics in the future”) and UK government policy. In particular, these factors could lead to a decline

in consumer confidence, increases in unemployment and repossession rates, and limited availability

of credit (including mortgages, home equity loans and consumer credit), which could result in lower

sales for the Wickes Group. For example, consumer confidence levels and housing transactions were

impacted by the result of the 2016 UK referendum to leave the European Union, and lockdown measures

early in the COVID-19 pandemic restricted home viewing activities and reduced transactions. Sentiment

can also be negatively impacted by consumer perception of economic and political conditions, as well as

changes to UK government regulation and policy, such as changes to stamp duty levels.

As a result, adverse conditions in, or uncertainty about, these markets, the economy or the political

climate could adversely impact the Wickes Group’s customers’ confidence or financial condition, causing

them to decide against purchasing home improvement products and services, causing them to delay

purchasing decisions or impacting their ability to pay for products and services. Any of these trends may

have a material adverse effect on the Wickes Group’s business, results of operations, financial condition

or prospects.

The Wickes Group faces risks related to the impact of COVID-19 and other communicable

diseases or pandemics in the future.

The spread of the COVID-19 strain of coronavirus and associated responses have caused significant

disruption to the global economy and financial markets, including supply chains, manufacturing

processes, and travel and shipment capabilities in various countries globally. On 11 March 2020, the

World Health Organisation officially declared the coronavirus outbreak a pandemic, and governments

15

around the world have at various times implemented emergency measures, including international and

domestic travel and other restrictions in an attempt to contain and slow down the further spread of the

virus. Emergency measures by central banks and governments around the world may not be sufficient

to offset the negative economic consequences caused by this outbreak, and there remains significant

uncertainty regarding the extent to which the pandemic will affect consumer behaviour (including in

relation to home purchase and home improvement activities, see “—The market for home improvement

purchases, and as a result the Wickes Group’s business, may be adversely affected by economic and

political conditions and other factors influencing disposable income in the United Kingdom”) in the future.

Preventative measures to contain the spread of COVID-19 have led, at times, to the temporary closure

of retail locations, factory and industrial facilities, schools and public spaces, as well as travel restrictions

impacting the movement of people and goods in the United Kingdom, a number of European countries

and other regions worldwide. Such closures and restrictions have caused disruptions to elements of

the Wickes Group’s supply chain (including through distributors and production of the Wickes Group’s

branded products), and significant delays or shortages could negatively impact its ability to serve

customers. In the longer term, the cost of production charged by such manufacturers may increase as

a result of supply or other issues arising as a result of the outbreak, which may negatively affect the

Wickes Group’s margins.

The Wickes Group faces risks arising from the impact of COVID-19 on its customers and the UK home

improvement market generally. Although the Wickes Group’s stores (as with other home improvement

retailers) have been classified as “essential businesses” and permitted to remain open throughout most

of the pandemic, the Wickes Group experienced a one-day closure of all stores on 24 March, followed

initially by an online-only light operating model, during which all locations (other than dedicated kitchen

and bathroom stores) continued to operate as fulfilment centres for click-and-collect and home delivery.

Subsequent public re-openings of these stores were staged, with an initial six stores on 30 April 2020 and

the remainder of these locations on 14 May and 19 May for all locations on 14 May and 19 May. Kitchen

and bathroom stores did not reopen until 1 July, and showroom space experienced intermittent closures

across the network, including during the November-December 2020 lockdown and since 5 January

2021. In the future, a significant deterioration of public health conditions could lead to implementation

of strict lockdown measures and forced closure of retail locations including Wickes stores or severely

limit the number of colleagues and customers allowed in a store at one time. Under severe lockdown

measures, the Wickes Group could also be prohibited from offering click-and-collect services or providing

home-delivery services from store locations, or from operating fulfilment and delivery activities from its

distribution centres, any of which would significantly limit the Wickes Group’s ability to continue serving

its customers. The pandemic could also affect the Wickes Group’s colleagues, see “The Wickes Group’s

success is dependent upon senior management and colleague teams, as well as skilled third-party

personnel”.

In addition, the pandemic has caused particular disruption to the DIFM and Local Trade markets, as

lockdowns, stay-at-home orders and social distancing measures have, at times, limited demand for

home improvement services that require third parties entering the home and, in particular in DIFM, limited

in-store showroom and in-person design activities due to social-distancing requirements. In addition,

the Wickes Group’s six kitchen and bath stores and its DIFM showrooms in a significant number of

stores have been closed at times during the course of the pandemic. Although the Wickes Group has

significantly expanded its virtual DIFM offering since the start of the pandemic, and it continues to engage

with customers through its expanded digitally-led offering and growth in delivery and click-and-collect

services, it has experienced periods of slow demand in Local Trade and significantly slower demand in

DIFM at times since the start of the pandemic and there remains uncertainty whether and when demand

in particular in DIFM, will reach levels observed prior to outbreak of the pandemic. In addition, while

the Wickes Group has experienced a significant increase in core DIY demand since the start of the

pandemic, this trend may not continue in the coming years.

Although the significance of COVID-19 and governmental actions to curtail its spread remain uncertain, it

is expected to continue to have a significant negative impact on the affected economies, negatively impact

global trade and markets and impact consumer demand. In the future, outbreaks of other communicable

diseases or pandemics could result in implementation of similar restrictions on travel and commercial

activity, or lead to supply disruptions in the United Kingdom or elsewhere, and negatively impact the

Wickes Group’s operations or demand for its products and services. If any of these events materialise,

it could have a material adverse effect on the Wickes Group’s business, results of operations, financial

condition or prospects.

16

The Wickes Group relies on its reputation as a trusted provider of high-quality home improvement

products and services at good value, and any deterioration in its reputation could adversely

affect its business.

The Wickes brand is an important asset, and maintaining the reputation of and value associated with

the Wickes brand is central to the success of the Wickes Group’s business. However, the Wickes Group

could be adversely affected if customers lose confidence in the perceived value, quality or safety of the

products or services offered by the Wickes Group, or in the Wickes Group’s reputation as a responsible

partner for home improvement projects.

In order to promote its products, the Wickes Group engages in promotional activity, such as limited time

price reductions and sales events, which may be subject to scrutiny. If consumers or the Advertising

Standards Authority (“ASA”) conclude that promotional activity by the Wickes Group does not provide an

accurate representation of the true or discounted value of a product, this could have a negative impact

on the perception of the Wickes Group as offering value for money to its customers, and therefore harm

its reputation and its operating and financial performance.

In addition, a significant portion of the home improvement products sold by the Wickes Group are

third-party branded products. As a result, the Wickes Group is, in part, dependent on manufacturers’

investment in their own marketing initiatives and efforts to promote their brands, in order for customers

to purchase these products. The Wickes Group also depends on its suppliers to comply with applicable

employment, environmental, safety and other laws and standards so as not to negatively impact their

branded products. However, there can be no assurance that suppliers are or will continue to effectively

promote their brands or remain in compliance with applicable law, and if they fail to do either of these,

it could lead to a deterioration in the reputation of the third-party brands stocked by the Wickes Group.

The Wickes Group also sells a number of products under the Wickes brand. However, the Wickes Group

sources these products from third parties and does not control the design or production of these items.

The Wickes Group could be adversely affected if customers lose confidence in the safety and quality of

the Wickes Group’s own-brand products. These products are important to the Wickes Group’s strategy

because they support the reputation of the Wickes brand and the Wickes Group typically earns a higher

margin on own-brand products than third-party branded items. Maintaining broad market acceptance

of its own-brand products depends on many factors, including pricing, costs, quality and customer

perception, and the Wickes Group may not achieve or maintain expected sales for its own-brand

products. A shift in the Wickes Group sales mix away from own-brand products, or a decline in overall

sales if any negative perception of these products adversely affects customers’ perception of the Wickes

Group more generally, could cause customers to switch to other home improvement retailers and have

a negative impact on the Wickes Group operating results.

The Wickes Group’s reputation may also depend on its perceived sustainability credentials. Across its

operations, and in light of increased public focus on environmental, social and governance matters,

the Wickes Group faces risks that customers and potential customers will not view it as a responsible

partner for their home improvement projects. As a result, any violation, or allegations of a violation, of

such laws, regulations or customer expectations by the Wickes Group or its suppliers could lead to

unfavourable publicity and reputational damage, which may cause a decline in public demand for the

Wickes Group’s products or services. In addition, if the Wickes Group does not meet applicable legal

requirements, it may be required to incur expenditure or make changes to its supply chain and other

business arrangements to ensure compliance.

If the Wickes Group is not perceived as providing value for money, or is not considered a trustworthy

and high-quality home improvement partner, and customers choose other products, retailers or service

providers over the Wickes Group, it could have a material adverse effect on the Wickes Group’s business,

results of operations, financial condition or prospects.

The Wickes Group relies on certain key suppliers, the loss of which could negatively impact

operating performance.

The Wickes Group product and service offerings rely on its relationships with a variety of domestic and

international suppliers. While the Wickes Group seeks to diversify its supplier network and maintains

relationships with approximately 370 different suppliers, certain key products that the Wickes Group

relies on, including kitchen cabinetry and timber, paint and plaster, are acquired from a limited number

of suppliers. As a result, if any one of the suppliers of key products fails to deliver on commitments or,

for any reason, cannot provide the Wickes Group with the products or supplies necessary for ongoing

17

operations, the Wickes Group could experience merchandise shortages or significant delays to its DIFM

services, which could lead to lost sales and reputational damage.

In addition, the Wickes Group may not be able to identify, develop and maintain relationships with

qualified suppliers who can satisfy its standards for price, quality, safety standards, quantity and other

requirements, including if an existing key supplier ceases trading or ends its relationship with the Wickes

Group and a new supplier needs to be located. The Wickes Group typically enters into contracts with

suppliers for an average of one to three years, which provides a measure of assurance of price and

supply (subject to the suppliers fulfilling their contractual obligations). However, when a contract expires,

the Wickes Group cannot be assured that it will be able to renew that contract or secure a contract with

a new supplier on equal or better terms and its sales and inventory levels could suffer if it is unable to

promptly replace a supplier.

Any substantial decrease in the availability of products from the Wickes Group’s key third-party suppliers

and own-brand manufacturers, including due to the loss of a key supplier, or significant changes to supply

terms at the time of renewal, could lead to lost sales or increased costs, which could have a material

adverse effect on the Wickes Group’s business, results of operations, financial condition or prospects.

The Wickes Group may experience interruptions involving its suppliers.

The products sold by the Wickes Group, whether they are sold under the Wickes brand or a third-party

label, are produced by third parties. In addition, third-party suppliers support a number of services

provided by the Wickes Group, including courier services as part of the Wickes Group’s fulfilment

capabilities and installation services as part of the Wickes Group’s DIFM offering. The Wickes Group

also relies on service providers for certain internal operating functions, such as information technology

integration.

A variety of issues might disrupt these supply chains and supplier relationships. For example, political

and economic instability in the countries in which foreign suppliers or manufacturers are located, the

financial instability of suppliers, suppliers’ failure to meet the Wickes Group’s standards, issues with

labour practices of its suppliers or labour problems they may experience (such as strikes), the availability

and cost of raw materials to suppliers, merchandise quality or safety issues, transport availability and

cost, inflation and other factors relating to the suppliers and the countries in which they are located or

from which they import could interrupt the Wickes Group’s sourcing activities. In addition, the COVID-19

pandemic, in particular if a significant deterioration in public health conditions leads to renewed lockdown

and other restrictions, could heighten the risks of certain of these supply risks. Any of these factors,

which are beyond the Wickes Group’s control, could have negative implications for the Wickes Group.

A significant proportion of the products sold by the Wickes Group, whether under the Wickes brand

or a third-party brand, are imported from outside the United Kingdom or purchased from domestic

distributors that import from outside the United Kingdom. As a result, the terms of the United Kingdom’s

departure from the European Union may impact the Wickes Group’s ability to procure these products

in a timely and cost-effective manner, whether from EU countries or from outside the European Union

pursuant to the United Kingdom’s existing trade arrangements. Further exchange rate volatility may

also negatively affect the Wickes Group’s cost of sales, as described in “—Cost inflation, including

wage inflation, could have an impact on the Wickes Group’s businesses, results of operations, nancial

condition or prospects”. Following its formal departure from the European Union on 31 January 2020,

the United Kingdom ceased trading as part of the European Union on 31 December 2020 following entry

by the United Kingdom and the European Union into the EU-UK Trade and Cooperation Agreement

(the “EU-UK TCA”). The impact of the changes in the trading relationship between the United Kingdom

following entry into and implementation of the EU-UK TCA is uncertain and may continue to change in

the coming years. However, if changes to the United Kingdom’s trading relationship with the European

Union result in the introduction of tariffs, in particular on products from third-party countries with whom

the United Kingdom needs to establish new trading relationships, or other costs arise from non-tariff

measures, there can be no assurance that these costs could be passed on to customers. Disruption to

the United Kingdom’s import capacity could also affect the availability of products sold by the Wickes

Group. As a result, the United Kingdom’s departure from the European Union may cause significant

disruption, which could negatively impact the Wickes Group’s ability to source products.

Disruptions due to labour stoppages, strikes or slowdowns that affect the Wickes Group’s suppliers, or

changes in global trade that negatively impact the Wickes Group’s ability to procure products on the

same terms it currently does, or other disruptions involving the Wickes Group’s suppliers or the shipping,

transportation and handling industries also may affect its ability to receive merchandise in a timely

18

manner and thus may negatively affect the Wickes Group’s sales and profitability. The Wickes Group

may in the future experience product shortages, due to any or all of the factors described above, which

could have a material adverse effect on the Wickes Group’s business, results of operations, financial

condition or prospects.

A failure to implement the Wickes Group’s integrated growth strategy may adversely affect

its business.

The Wickes Group’s growth strategy relies on its ability to provide customers with best-in-class service

and a fast and convenient shopping experience, whether they are shopping online or in-store. As a

result, the Wickes Group has undertaken efforts to improve its digital capabilities, further integrate its

operations across its service offering and to improve its in-store product selection and order fulfilment

services, so that the Wickes Group can provide its customers with the products they need when and

where they need them. In Financial Year 2020, the Wickes Group approached two-thirds of sales that

utilise its digitally-enabled capabilities, including online ordering, advanced “online, in-store” purchases

from in-store, the TradePro digital app, online research ahead of an in-store purchase, showroom web

leads and through the virtual DIFM journey. This strategy places the Wickes Group’s digital capabilities

at the heart of the customer journey and utilises its store estate to support efficient order fulfilment,

but it may prove unsuccessful or additional investment may be required to support further systems

improvements.

In addition, investment activities undertaken in the past may not deliver the targeted returns. For

example, the Wickes Group has undertaken significant work as part of its ongoing store transformation

initiative, including to improve the quality of the store estate and right-size certain store locations to

support more efficient operations and improve the customer experience. While the COVID-19 pandemic

has accelerated certain in-store reconfiguration activities, including to increase in-store storage space

in a number of high-volume, small-footprint locations to support click-and-collect activities, there can be

no assurance the extent to which they will support operating activities in the future or whether or where

further investment will be required. Future re-fit activities will require additional investment and may

not deliver a similar sales uplift and level of return as historical investment at other stores. The Wickes

Group anticipates undertaking re-fit activities at between 35 and 40 additional stores. In addition, a

decline in the Wickes Group’s operating performance could limit its ability to undertake future renovation

and re-fit works, which could negatively impact its revenue and reputation.

A number of factors, including the manifestation of the other risks described in this document, could

limit management’s ability to accurately project and strategically plan for shifts in customer demand and

preferences and, as a result, prevent the Wickes Group’s strategic initiatives from being successfully

or promptly completed. In addition, the Wickes Group’s strategy relies on customers finding the Wickes

Group’s website easy to use and helpful, welcoming and conveniently located stores, compelling

kitchen and bathroom service offerings, as well as any future DIFM offerings, and online and in-store

product range offerings that meet their needs. However, customers may not respond positively to

these initiatives and digitally-enabled sales may not continue growing. If the Wickes Group is unable to

continue developing and implementing its digitally-led, service-enabled strategy, it could have a material

adverse effect on the Wickes Group’s business, results of operations, financial condition or prospects.

The Wickes Group may not be able to accurately predict and plan for changes in customer demand

and preferences, which could lead to reductions in sales or negatively impact operating margins.

The Wickes Group derives revenue from the sale of products and provision of services that are subject to

changing customer demand. As a result, its success depends, in part, on its ability to effectively predict

and respond to changing market conditions and customer preferences in order to provide a compelling and

targeted service proposition to its local trade (“Local Trade”), DIFM and do-it-yourself (“DIY”) customers.

In recent years, the Wickes Group has invested significantly to transform its physical infrastructure, digital

capabilities and product and service proposition to better reflect changing behaviours in the UK home

improvement market, based on customer demand and projected market trends. These changes include

the expansion of its DIFM service offering and integration of operations to provide digitally-led solutions.

However, in the future, customer behaviour may shift in a way that the Wickes Group cannot predict or

plan for or the Wickes Group’s service proposition may not continue to meet customer home improvement

preferences or demands, either of which could lead to reductions in sales or require the Wickes Group

to incur additional costs to continue serving its customers. For example, the COVID-19 pandemic has

led to periodic lockdown restrictions, stay-at-home orders and otherwise impacted customer behaviour,

which has at times negatively impacted the broader DIFM and Local Trade markets (see “—The Wickes

19

Group faces risks related to the impact of COVID-19 and other communicable diseases or pandemics

in the future”) and resulted in increased demand for click-and-collect and home delivery services. The

Wickes Group responded to these changes by accelerating certain digital strategies, including its virtual

DIFM service, and expanding its distribution and fulfilment offering. However, significant changes, or

implementation moderate changes over the longer term, may require the Wickes Group to incur higher

costs than it has historically and negatively impact its operating margins.

As part of this transformation in recent years, the Wickes Group has undertaken significant work on its

product ranges. This strategy relies on providing curated ranges of products online and in-store, in an

effort to make the shopping experience easier for its trade and DIY customers. As a result, inventory

management is a key component of this strategy, and the Wickes Group must balance the need to

maintain sufficient inventory levels to meet its customers’ demands for timely delivery and in-store

collection options, with potential increased costs associated with excess inventory and the risk this

unduly impacts the Wickes Group’s financial condition. This strategy also relies on the Wickes Group’s

ability to ensure that the right products and brands are included in its curated in-store product ranges.

If the Wickes Group is unable to correctly predict the products and brands demanded by its customers,

or if it selects products and brands that are not in high demand, it may result in lower sales levels and

longer inventory turnover times.

In addition, the Wickes Group must ensure that it evaluates customer trends and procures the right

products with adequate lead time. A significant portion of the products offered in the Wickes Group’s

stores are manufactured outside of the United Kingdom. The Wickes Group regularly enters into

contracts for the purchase and manufacture of merchandise from suppliers outside the United Kingdom