UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

☑ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2021

OR

☐TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from to

Commission file number: 0-50231

Federal National Mortgage Association

(Exact name of registrant as specified in its charter)

Fannie Mae

Federally chartered corporation 52-0883107 1100 15th Street, NW 800 232-6643

Washington, DC 20005

(State or other jurisdiction of

incorporation or organization)

(I.R.S. Employer

Identification No.)

(Address of principal executive

offices, including zip code)

(Registrant’s telephone number,

including area code)

Securities registered pursuant to Section 12(b) of the Act:

Title of each class Trading Symbol(s) Name of each exchange on which registered

None N/A N/A

Securities registered pursuant to Section 12(g) of the Act:

Common Stock, without par value

8.25% Non-Cumulative Preferred Stock, Series T, stated value $25 per share

Fixed-to-Floating Rate Non-Cumulative Preferred Stock, Series S, stated value $25 per share

7.625% Non-Cumulative Preferred Stock, Series R, stated value $25 per share

6.75% Non-Cumulative Preferred Stock, Series Q, stated value $25 per share

Variable Rate Non-Cumulative Preferred Stock, Series P, stated value $25 per share

Variable Rate Non-Cumulative Preferred Stock, Series O, stated value $50 per share

5.375% Non-Cumulative Convertible Series 2004-1 Preferred Stock, stated value $100,000 per share

5.50% Non-Cumulative Preferred Stock, Series N, stated value $50 per share

4.75% Non-Cumulative Preferred Stock, Series M, stated value $50 per share

5.125% Non-Cumulative Preferred Stock, Series L, stated value $50 per share

5.375% Non-Cumulative Preferred Stock, Series I, stated value $50 per share

5.81% Non-Cumulative Preferred Stock, Series H, stated value $50 per share

Variable Rate Non-Cumulative Preferred Stock, Series G, stated value $50 per share

Variable Rate Non-Cumulative Preferred Stock, Series F, stated value $50 per share

5.10% Non-Cumulative Preferred Stock, Series E, stated value $50 per share

5.25% Non-Cumulative Preferred Stock, Series D, stated value $50 per share

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No þ

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. Yes ¨ No þ

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the

preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the

past 90 days. Yes þ No ¨

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation

S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes þ No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging

growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of

the Exchange Act.

Large accelerated filer

☑

Accelerated filer

☐

Non-accelerated filer

☐

Smaller reporting company ☐

Emerging growth company

☐

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised

financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over

financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit

report.☑

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☑

The aggregate market value of the common stock held by non-affiliates computed by reference to the closing price of the common stock quoted on the OTCQB on

June 30, 2021 (the last business day of the registrant’s most recently completed second fiscal quarter) was approximately $1.8 billion.

As of February 1, 2022, there were 1,158,087,567 shares of common stock of the registrant outstanding.

Table of Contents

Page

PART I

Item 1.

Business . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

1

Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

1

Executive Summary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

2

Summary of Our Financial Performance . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

2

Liquidity Provided in 2021 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

4

Our Mission, Strategy and Charter . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

4

Mortgage Securitizations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

5

Managing Mortgage Credit Risk . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

8

Conservatorship, Treasury Agreements and Housing Finance Reform . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

11

Legislation and Regulation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

18

Human Capital . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

28

Where You Can Find Additional Information . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

30

Forward-Looking Statements . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

30

Item 1A.

Risk Factors . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

33

Risk Factors Summary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

33

GSE and Conservatorship Risk . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

35

Credit Risk . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

40

Operational Risk . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

44

Liquidity and Funding Risk . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

48

Market and Industry Risk . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

49

Legal and Regulatory Risk . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

52

General Risk . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

53

Item 1B.

Unresolved Staff Comments . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

54

Item 2.

Properties . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

54

Item 3.

Legal Proceedings . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

54

Item 4.

Mine Safety Disclosures . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

55

PART II

Item 5.

Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity

Securities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

56

Item 6.

[Reserved] . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

57

Item 7.

Management’s Discussion and Analysis of Financial Condition and Results of Operations . . . . . . . . . . . . . . .

58

Key Market Economic Indicators . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

58

Consolidated Results of Operations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

62

Consolidated Balance Sheet Analysis . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

76

Retained Mortgage Portfolio . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

78

Guaranty Book of Business . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

80

Business Segments . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

81

Single-Family Business . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

82

Single-Family Mortgage Market . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

85

Single-Family Market Activity . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

86

Single-Family Business Metrics . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

87

Single-Family Business Financial Results . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

89

Single-Family Mortgage Credit Risk Management . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

91

Multifamily Business . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

119

Fannie Mae 2021 Form 10-K i

Multifamily Mortgage Market . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

121

Multifamily Market Activity . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

122

Multifamily Business Metrics . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

122

Multifamily Business Financial Results . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

125

Multifamily Mortgage Credit Risk Management . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

126

Liquidity and Capital Management . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

133

Risk Management . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

143

Mortgage Credit Risk Management Overview . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

145

Climate Change and Natural Disaster Risk Management . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

145

Institutional Counterparty Credit Risk Management . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

147

Market Risk Management, including Interest-Rate Risk Management . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

155

Liquidity and Funding Risk Management . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

160

Operational Risk Management . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

160

Critical Accounting Estimates . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

161

Impact of Future Adoption of New Accounting Guidance . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

164

Glossary of Terms Used in This Report . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

164

Item 7A.

Quantitative and Qualitative Disclosures about Market Risk . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

168

Item 8.

Financial Statements and Supplementary Data . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

168

Item 9.

Changes in and Disagreements with Accountants on Accounting and Financial Disclosure . . . . . . . . . . . . . . .

168

Item 9A.

Controls and Procedures . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

168

Item 9B.

Other Information . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

173

Item 9C.

Disclosure Regarding Foreign Jurisdictions that Prevent Inspections . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

173

PART III

Item 10.

Directors, Executive Officers and Corporate Governance . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

173

Directors . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

173

Corporate Governance . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

179

ESG Matters . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

186

Report of the Audit Committee of the Board of Directors . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

190

Executive Officers . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

192

Item 11.

Executive Compensation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

195

Compensation Discussion and Analysis . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

195

Compensation Committee Report . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

217

Compensation Risk Assessment . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

217

Compensation Tables and Other Information . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

218

Item 12.

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters . . . . .

229

Item 13.

Certain Relationships and Related Transactions, and Director Independence . . . . . . . . . . . . . . . . . . . . . . . . . .

230

Policies and Procedures Relating to Transactions with Related Persons . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

230

Transactions with Related Persons . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

232

Director Independence . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

233

Item 14.

Principal Accounting Fees and Services . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

235

PART IV

Item 15.

Exhibits, Financial Statement Schedules . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

237

Item 16.

Form 10-K Summary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

239

INDEX TO CONSOLIDATED FINANCIAL STATEMENTS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F-1

Fannie Mae 2021 Form 10-K ii

PART I

We have been under conservatorship, with the Federal Housing Finance Agency (“FHFA”) acting as conservator,

since September 6, 2008. As conservator, FHFA succeeded to all rights, titles, powers and privileges of the

company, and of any shareholder, officer or director of the company with respect to the company and its assets.

The conservator has since provided for the exercise of certain functions and authorities by our Board of Directors.

Our directors do not have any fiduciary duties to any person or entity except to the conservator and, accordingly,

are not obligated to consider the interests of the company, the holders of our equity or debt securities, or the

holders of Fannie Mae MBS unless specifically directed to do so by the conservator.

We do not know when or how the conservatorship will terminate, what further changes to our business will be made

during or following conservatorship, what form we will have and what ownership interest, if any, our current common

and preferred stockholders will hold in us after the conservatorship is terminated or whether we will continue to exist

following conservatorship. Members of Congress and the Administration continue to express the importance of

housing finance system reform.

We are not currently permitted to pay dividends or other distributions to stockholders. Our agreements with the U.S.

Department of the Treasury (“Treasury”) include a commitment from Treasury to provide us with funds to maintain a

positive net worth under specified conditions; however, the U.S. government does not guarantee our securities or

other obligations. Our agreements with Treasury also include covenants that significantly restrict our business

activities. For additional information on the conservatorship, the uncertainty of our future, and our agreements with

Treasury, see “Business—Conservatorship, Treasury Agreements and Housing Finance Reform” and “Risk Factors

—GSE and Conservatorship Risk.”

Forward-looking statements in this report are based on management’s current expectations and are subject to

significant uncertainties and changes in circumstances, as we describe in “Business—Forward-Looking Statements.”

Future events and our future results may differ materially from those reflected in our forward-looking statements due to

a variety of factors, including those discussed in “Risk Factors” and elsewhere in this report.

You can find a “Glossary of Terms Used in This Report” in “Management’s Discussion and Analysis of Financial

Condition and Results of Operations (‘MD&A’).”

Item 1. Business

Introduction

Fannie Mae is a leading source of financing for mortgages in the United States, with $4.2 trillion in assets as of

December 31, 2021. Organized as a government-sponsored entity, Fannie Mae is a shareholder-owned corporation.

Our charter is an act of Congress, which establishes that our purposes are to provide liquidity and stability to the

residential mortgage market and to promote access to mortgage credit. We were initially established in 1938.

Our revenues are primarily driven by guaranty fees we receive for assuming the credit risk on loans underlying the

mortgage-backed securities we issue. We do not originate loans or lend money directly to borrowers. Rather, we work

primarily with lenders who originate loans to borrowers. We securitize those loans into Fannie Mae mortgage-backed

securities that we guarantee (which we refer to as Fannie Mae MBS or our MBS).

Effectively managing credit risk is key to our business. In exchange for assuming credit risk on the loans we acquire, we

receive guaranty fees. These fees take into account the credit risk characteristics of the loans we acquire. Guaranty

fees are set at the time we acquire loans and do not change over the life of the loan. How long a loan remains in our

guaranty book is heavily dependent on interest rates. When interest rates decrease, a larger portion of our book of

business turns over as more loans refinance. On the other hand, as interest rates increase, fewer loans refinance and

our book turns over more slowly. Since guaranty fees are set at the time a loan is originated, the impact of any change

in guaranty fees on future revenues depends on the rates at which loans in our book of business turn over and new

loans are added.

Business | Introduction

Fannie Mae 2021 Form 10-K 1

Executive Summary

Please read this summary together with our MD&A, our consolidated financial statements as of December 31, 2021 and

the accompanying notes.

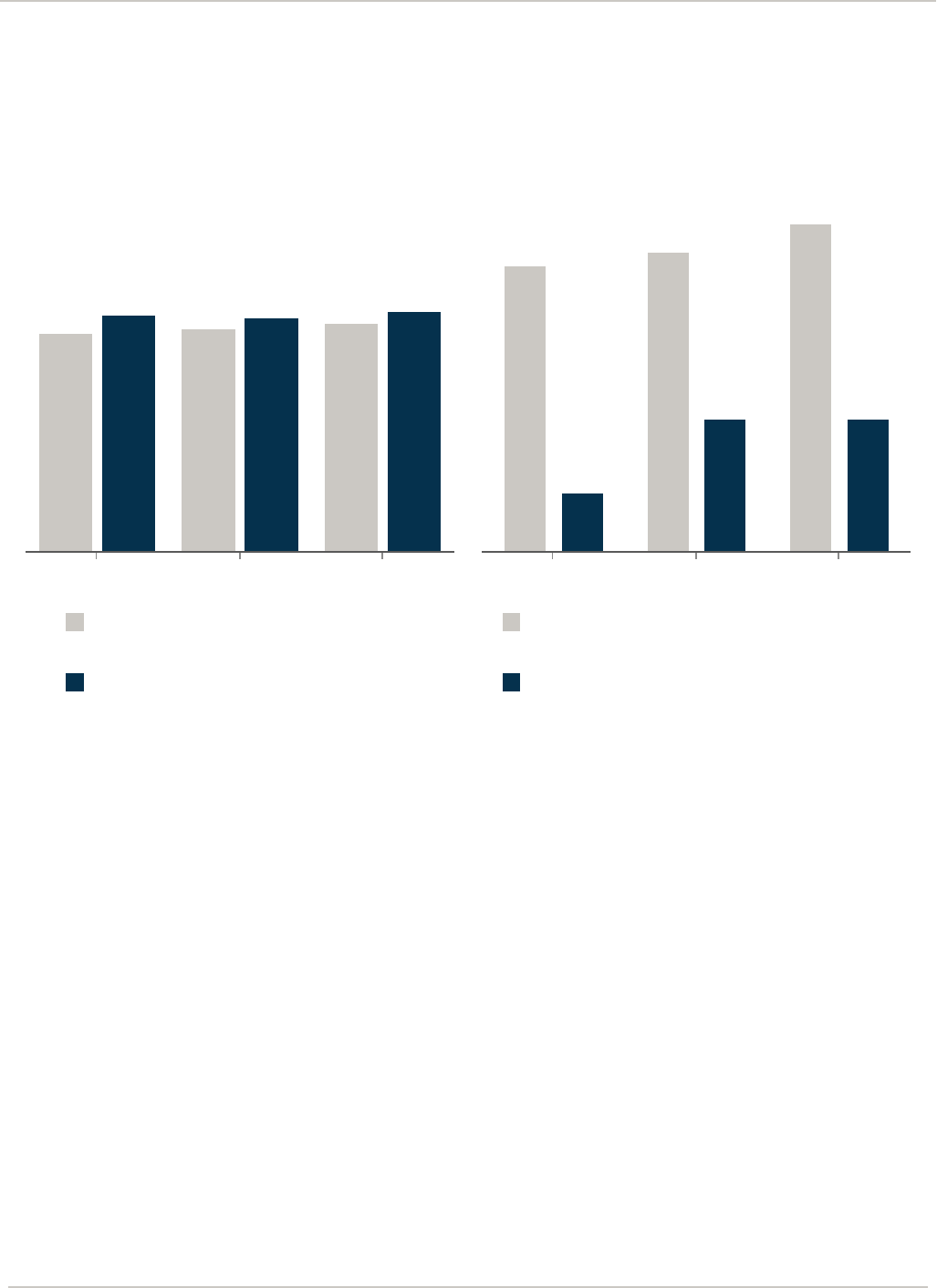

Summary of Our Financial Performance

Consolidated Results

(Dollars in billions)

$21.9

$25.3

$29.9

$14.2

$11.8

$22.2

$14.0

$11.8

$22.1

Net revenues Net income Comprehensive income

2019 2020 2021

2021 vs. 2020

• Net revenues increased $4.6 billion in 2021 compared with 2020, primarily due to higher base guaranty fee

income as the size of our guaranty book of business grew along with higher average guaranty fees related to

the loans in our book of business in 2021. This was coupled with an increase in net amortization income as a

result of high prepayment volumes from loan refinancings as a result of the continued low interest-rate

environment. The loans and associated debt of consolidated trusts that liquidated in 2021 had larger

unamortized deferred fees than those that liquidated in 2020. The increase in net revenues in 2021 was

partially offset by a decrease in net interest income from our portfolios compared with 2020 due to lower

average balances and lower yields on our mortgage loans and assets offset by lower borrowing costs on our

long-term funding debt.

• Net income increased $10.4 billion in 2021 compared with 2020, mainly due to higher net revenues as

discussed above plus a shift from credit-related expense in 2020 to credit-related income in 2021. Credit-

related income in 2021 was primarily driven by strong actual and forecasted home price growth, a benefit from

the redesignation of certain nonperforming and reperforming loans and a reduction in our estimate of losses we

expect to incur as a result of the COVID-19 pandemic, partially offset by a provision for higher actual and

projected interest rates. In addition, fair value gains in 2021 were primarily driven by declines in the fair value of

risk management derivatives and trading securities, offset by the impact of hedge accounting. Fair value losses

in 2020, before we implemented hedge accounting, were primarily driven by declines in the fair value of

commitments to sell mortgage-related securities as prices increased during the commitment period. See

“Consolidated Results of Operations—Hedge Accounting Impact” for further details on the impact of our fair

value hedge accounting.

• Net worth increased by $22.1 billion in 2021 to $47.4 billion as of December 31, 2021. The increase is

attributed to $22.1 billion of comprehensive income for the twelve months ended December 31, 2021.

Business | Executive Summary

Fannie Mae 2021 Form 10-K 2

2020 vs. 2019

• Net revenues increased $3.4 billion in 2020 compared with 2019, primarily driven by an increase in net

amortization income as a result of interest rates declining to historically low levels, leading to record levels of

refinancing activity in 2020.

• Net income decreased $2.4 billion in 2020 compared with 2019, primarily driven by a shift from credit-related

income to credit-related expense, driven by the economic dislocation caused by the COVID-19 pandemic and

lower loan redesignation activity, as well as a reduction in investment gains driven by a decrease in the volume

of reperforming loan sales. This was partially offset by the increase in net revenues from higher net

amortization income discussed above.

• Net worth increased by $10.7 billion to $25.3 billion in 2020. The increase is attributed to $11.8 billion of

comprehensive income for the twelve months ended December 31, 2020 offset by a charge of $1.1 billion to

retained earnings due to our implementation of Accounting Standards Update 2016-13, Financial Instruments—

Credit Losses, Measurement of Credit Losses on Financial Instruments and related amendments (the “CECL

standard”) on January 1, 2020. See “Note 1, Summary of Significant Accounting Policies—New Accounting

Guidance—Adoption of the CECL Standard” for further details on our implementation of the CECL standard.

Financial Performance Outlook

Our financial results benefited significantly in 2021 from high refinance volumes, which contributed to our net

amortization income, and the high pace of home price growth, which contributed to our credit-related income. We

expect the pace of home price growth to moderate in 2022, and we have already seen a decline in the volume of

refinancings beginning in the second half of 2021, as interest rates have risen. Specifically, we expect increases in

mortgage interest rates and fewer refinancings as the large number of borrowers who have refinanced recently will

result in fewer borrowers who can benefit from a refinancing in the future, leading to lower amortization income from

prepayment activity. In addition, we expect the positive benefit to credit-related income (expense) from home price

growth to decline in 2022 compared with 2021 as we expect home price growth to slow. See “MD&A—Key Market

Economic Indicators” for a discussion of how home prices, interest rates and other macroeconomic factors can affect

our financial results.

Our long-term financial performance will depend on many factors, including:

• the size of and our share of the U.S. mortgage market, which in turn will depend upon population growth,

household formation and housing supply;

• borrower performance, the guaranty fees we receive, and changes in home prices, interest rates and other

macroeconomic factors, including the impact of climate change on these factors; and

• the impact of actions by FHFA, the Administration and Congress relating to our business and housing finance

reform, including our capital requirements, our ongoing financial obligations to Treasury, restrictions on our

activities and our business footprint, our competitive environment and pricing, and actions we are required to

take to support borrowers or the mortgage market.

For information about how we may be impacted by general economic conditions, see “Risk Factors—Market and

Industry Risk.” For information about the potential impacts of climate change, see “Risk Factors—Credit Risk” and

“MD&A—Risk Management—Climate Change and Natural Disaster Risk Management.” For information about the

impact of actions by FHFA, the Administration and Congress, see “Risk Factors—GSE and Conservatorship Risk.”

Business | Executive Summary

Fannie Mae 2021 Form 10-K 3

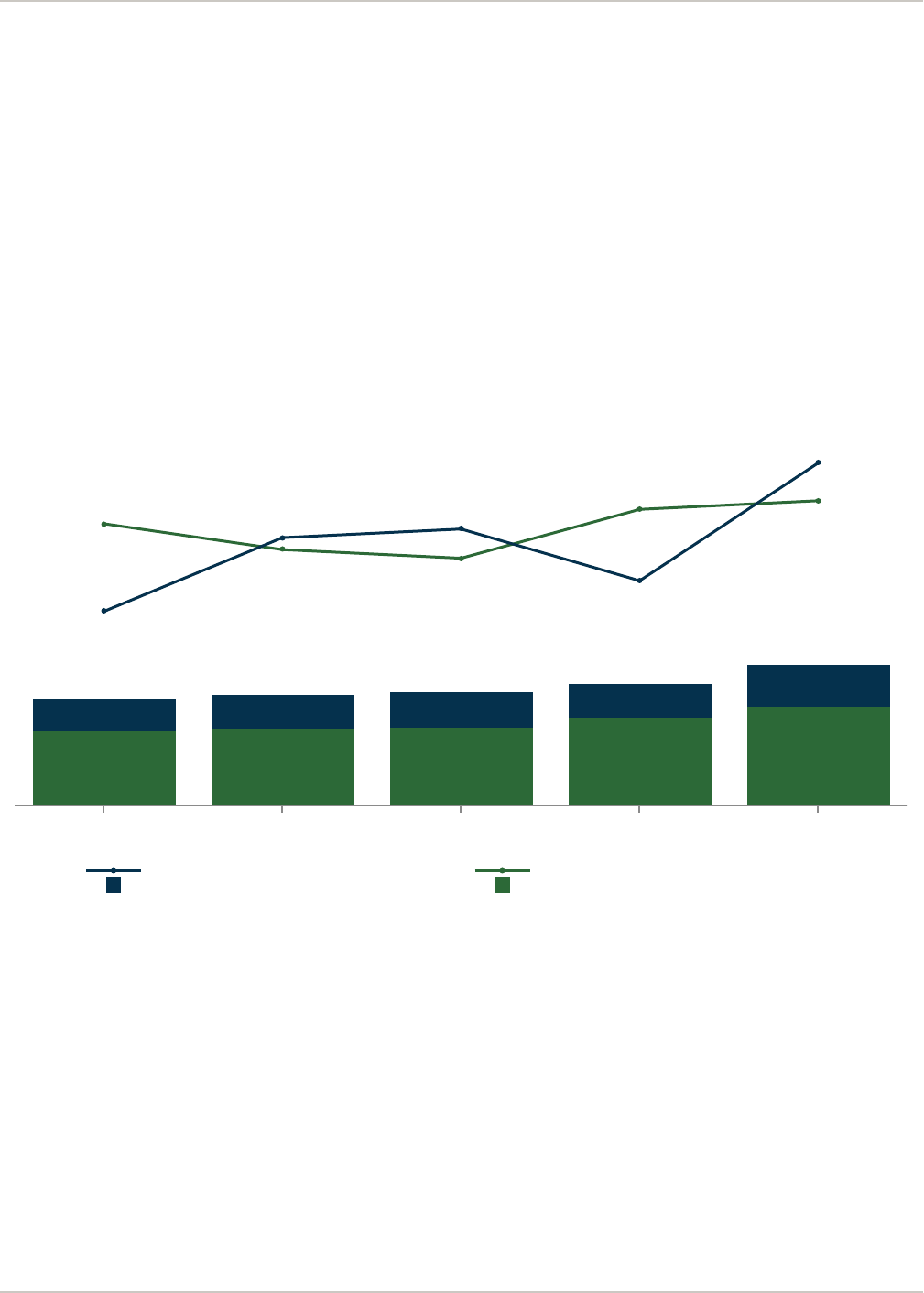

Liquidity Provided in 2021

Through our single-family and multifamily business segments, we provided $1.4 trillion in liquidity to the mortgage

market in 2021, which enabled the financing of approximately 5.5 million home purchases, refinancings and rental units.

Fannie Mae Provided $1.4 trillion in Liquidity in 2021

Unpaid Principal Balance

Units

$451B

1.5M

Single-Family Home Purchases

$904B

3.3M

Single-Family Refinancings

$69B

694K

Multifamily Rental Units

For information about the financing we have provided through our green bonds and our Sustainable Bond Framework,

see “Directors, Executive Officers and Corporate Governance—Corporate Governance—ESG Matters.”

Our Mission, Strategy and Charter

Our Mission and Strategy

Our mission is to facilitate equitable and sustainable access to homeownership and quality affordable rental housing

across America. We are pursuing this mission through our strategic objectives:

• Build on our mission-first culture to become a globally-recognized, top-performing environmental, social and

governance (ESG) financial services company by delivering positive mission and community outcomes to serve

homeowners and tenants.

• Ensure that Fannie Mae is a financially secure company that is able to attract private capital by managing risk

to the firm and the housing finance system to fulfill its mission.

• Increase operational agility and efficiency, accelerating the digital transformation of the firm to deliver more

value and reliable, modern platforms in support of the broader housing finance system.

Our Charter

The Federal National Mortgage Association Charter Act (the “Charter Act”) establishes the parameters under which we

operate and our purposes, which are to:

• provide stability in the secondary market for residential mortgages;

• respond appropriately to the private capital market;

• provide ongoing assistance to the secondary market for residential mortgages (including activities relating to

mortgages on housing for low- and moderate-income families involving a reasonable economic return that may

be less than the return earned on other activities) by increasing the liquidity of mortgage investments and

improving the distribution of investment capital available for residential mortgage financing; and

• promote access to mortgage credit throughout the nation (including central cities, rural areas and underserved

areas) by increasing the liquidity of mortgage investments and improving the distribution of investment capital

available for residential mortgage financing.

The Charter Act specifies that our operations are to be financed by private capital to the maximum extent feasible. We

are expected to earn reasonable economic returns on all our activities. However, we may accept lower returns on

certain activities relating to mortgages on housing for low- and moderate-income families in order to support those

segments of the market. We expect the lower returns to be offset by activities that yield higher returns.

Principal balance limitations. To meet our purposes, the Charter Act authorizes us to purchase and securitize mortgage

loans secured by single-family and multifamily properties. Our acquisitions of single-family conventional mortgage loans

are subject to maximum original principal balance limits, known as “conforming loan limits.” The conforming loan limits

are adjusted each year based on FHFA’s housing price index. For 2021, the conforming loan limit for mortgages

secured by one-family residences was set at $548,250, with higher limits for mortgages secured by two- to four-family

residences and in four statutorily-designated states and territories (Alaska, Hawaii, Guam and the U.S. Virgin Islands).

Business | Our Mission, Strategy and Charter

Fannie Mae 2021 Form 10-K 4

For 2022, FHFA increased the national conforming loan limit for one-family residences to $647,200. In addition, higher

loan limits of up to 150% of the otherwise applicable loan limit apply in certain high-cost areas. Certain loans above the

baseline conforming loan limit will be subject to a recently announced increase in upfront fees, which we discuss in

“MD&A—Single-Family Business—Single-Family Business Metrics.” The Charter Act does not impose maximum

original principal balance limits on loans we purchase or securitize that are insured by the Federal Housing

Administration (“FHA”) or guaranteed by the Department of Veterans Affairs (“VA”).

The Charter Act also includes the following provisions:

• Credit enhancement requirements. The Charter Act generally requires credit enhancement on any single-family

conventional mortgage loan that we purchase or securitize that has a loan-to-value (“LTV”) ratio over 80% at

the time of purchase. The credit enhancement may take the form of one or more of the following: (1) insurance

or a guaranty by a qualified insurer on the portion of the unpaid principal balance of a mortgage loan that

exceeds 80% of the property value; (2) a seller’s agreement to repurchase or replace the loan in the event of

default; or (3) retention by the seller of at least a 10% participation interest in the loan. Regardless of LTV ratio,

the Charter Act does not require us to obtain credit enhancement to purchase or securitize loans insured by

FHA or guaranteed by the VA.

• Issuances of our securities. We are authorized, upon the approval of the Secretary of the Treasury, to issue

debt obligations and mortgage-related securities. Neither the U.S. government nor any of its agencies

guarantees, directly or indirectly, our debt or mortgage-related securities.

• Authority of Treasury to purchase our debt obligations. At the discretion of the Secretary of the Treasury,

Treasury may purchase our debt obligations up to a maximum of $2.25 billion outstanding at any one time.

• Exemption for our securities offerings. Our securities offerings are exempt from registration requirements under

the federal securities laws. As a result, we do not file registration statements or prospectuses with the SEC with

respect to our securities offerings. However, our equity securities are not treated as exempt securities for

purposes of Sections 12, 13, 14 or 16 of the Securities Exchange Act of 1934 (the “Exchange Act”).

Consequently, we are required to file periodic and current reports with the SEC, including annual reports on

Form 10-K, quarterly reports on Form 10-Q, and current reports on Form 8-K. Our non-equity securities are

exempt securities under the Exchange Act.

• Exemption from specified taxes. Fannie Mae is exempt from taxation by states, territories, counties,

municipalities and local taxing authorities, except for taxation by those authorities on our real property. We are

not exempt from the payment of federal corporate income taxes.

• Limitations. We may not originate mortgage loans or advance funds to a mortgage seller on an interim basis,

using mortgage loans as collateral, pending the sale of the mortgages in the secondary market. We may

purchase or securitize mortgage loans only on properties located in the United States and its territories.

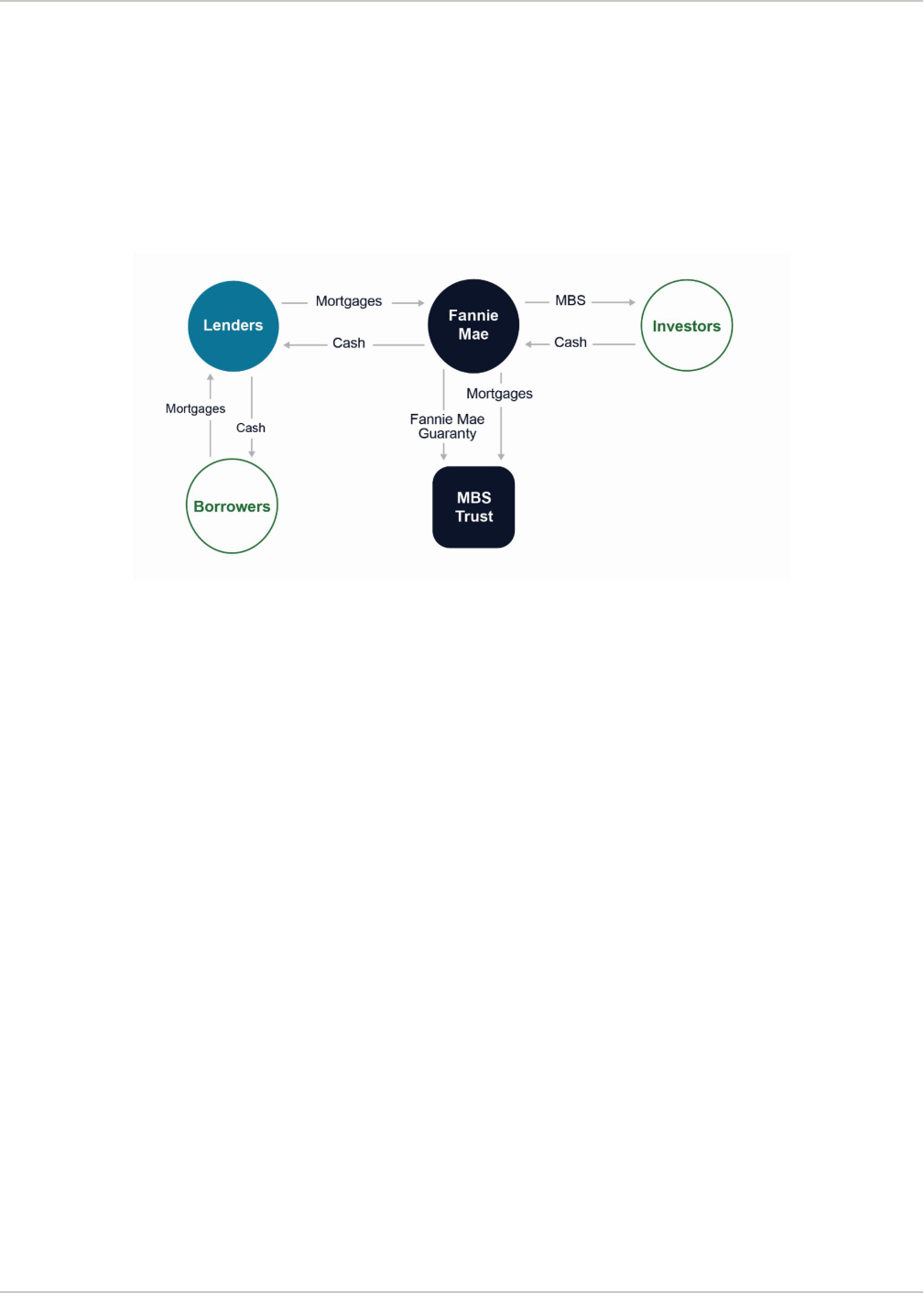

Mortgage Securitizations

We support market liquidity by issuing Fannie Mae MBS that are readily traded in the capital markets. We create Fannie

Mae MBS by placing mortgage loans in a trust and issuing securities that are backed by those mortgage loans. Monthly

payments received on the loans are the primary source of payments passed through to Fannie Mae MBS holders. We

guarantee to the MBS trust that we will supplement amounts received by the MBS trust as required to permit timely

payment of principal and interest on the trust certificates. In return for this guaranty, we receive guaranty fees.

Below we discuss the three broad categories of our securitization transactions and the uniform mortgage-backed

securities we issue.

Securitization Transactions

We currently securitize a substantial majority of the single-family and multifamily mortgage loans we acquire. Our

securitization transactions primarily fall within three broad categories: lender swap transactions, portfolio securitizations,

and structured securitizations.

Lender Swap Transactions

In a single-family “lender swap transaction,” a mortgage lender that operates in the primary mortgage market generally

delivers a pool of mortgage loans to us in exchange for Fannie Mae MBS backed by these mortgage loans. Lenders

may hold the Fannie Mae MBS they receive from us or sell them to investors. A pool of mortgage loans is a group of

mortgage loans with similar characteristics. After receiving the mortgage loans in a lender swap transaction, we place

them in a trust for which we serve as trustee. This trust is established for the sole purpose of holding the mortgage

Business | Our Mission, Strategy and Charter

Fannie Mae 2021 Form 10-K 5

loans separate and apart from our corporate assets. We guarantee to each MBS trust that we will supplement amounts

received by the MBS trust as required to permit timely payment of principal and interest on the related Fannie Mae

MBS. We are entitled to a portion of the interest payment as a fee for providing our guaranty. The mortgage servicer

also retains a portion of the interest payment as a fee for servicing the loan. Then, on behalf of the trust, we make

monthly distributions to the Fannie Mae MBS certificateholders from the principal and interest payments and other

collections on the underlying mortgage loans.

Lender Swap Transaction

Our Multifamily business generally creates multifamily Fannie Mae MBS in lender swap transactions in a manner similar

to our Single-Family business. Multifamily lenders typically deliver only one mortgage loan to back each multifamily

Fannie Mae MBS. The characteristics of each mortgage loan are used to establish guaranty fees on a risk-adjusted

basis. Securitizing a multifamily mortgage loan into a Fannie Mae MBS facilitates its sale into the secondary market.

Business | Mortgage Securitizations

Fannie Mae 2021 Form 10-K 6

Portfolio Securitization Transactions

We also purchase mortgage loans and mortgage-related securities for securitization and sale at a later date through our

“portfolio securitization transactions.” Most of our portfolio securitization transactions are driven by our single-family

whole loan conduit activities, pursuant to which we purchase single-family whole loans from a large group of typically

small to mid-sized lenders principally for the purpose of securitizing the loans into Fannie Mae MBS, which may then be

sold to dealers and investors.

Portfolio Securitization Transaction

Structured Securitization Transactions

In a “structured securitization transaction,” we create structured Fannie Mae MBS, typically for lenders or securities

dealers, in exchange for a transaction fee. In these transactions, the lender or dealer “swaps” a mortgage-related asset

that it owns (typically a mortgage security) in exchange for a structured Fannie Mae MBS we issue. The process for

issuing Fannie Mae MBS in a structured securitization is similar to the process involved in our lender swap

securitizations described above.

We also issue structured transactions backed by multifamily Fannie Mae MBS through the Fannie Mae Guaranteed

Multifamily Structures (“Fannie Mae GeMS

TM

”) program, which provides additional liquidity and stability to the

multifamily market, while expanding the investor base for multifamily Fannie Mae MBS.

Uniform Mortgage-Backed Securities, or UMBS

Overview

Since 2019, we and Freddie Mac have each been issuing UMBS

®

, a uniform mortgage-backed security intended to

maximize liquidity for both Fannie Mae and Freddie Mac mortgage-backed securities in the to-be-announced (“TBA”)

market.

Certain aspects of the securitization process for our single-family Fannie Mae MBS issuances are performed by

Common Securitization Solutions, LLC (“CSS”), which is a limited liability company we own jointly with Freddie Mac.

CSS operates a common securitization platform, which was designed to allow for the potential integration of additional

market participants in the future. In October 2021, FHFA announced its determination, after a nearly two-year review,

that CSS should focus on maintaining the resiliency of Fannie Mae’s and Freddie Mac’s mortgage-backed securities

platform instead of expanding its role to serve a broader market.

UMBS and Structured Securities

Each of Fannie Mae and Freddie Mac (the “GSEs”) issues and guarantees UMBS and structured securities backed by

UMBS and other securities, as described below.

• UMBS. Each of Fannie Mae and Freddie Mac issues and guarantees UMBS that are directly backed by the

mortgage loans it has acquired, referred to as “first-level securities.” UMBS issued by Fannie Mae are backed

only by mortgage loans that Fannie Mae has acquired, and similarly UMBS issued by Freddie Mac are backed

Business | Mortgage Securitizations

Fannie Mae 2021 Form 10-K 7

only by mortgage loans that Freddie Mac has acquired. There is no commingling of Fannie Mae- and Freddie

Mac-acquired loans within UMBS.

Mortgage loans backing UMBS are limited to fixed-rate mortgage loans eligible for financing through the TBA

market. We continue to issue some types of Fannie Mae MBS that are not TBA-eligible and therefore are not

issued as UMBS, such as single-family Fannie Mae MBS backed by adjustable-rate mortgages and all

multifamily Fannie Mae MBS.

• Structured Securities. Each of Fannie Mae and Freddie Mac also issues and guarantees structured mortgage-

backed securities, referred to as “second-level securities,” that are resecuritizations of UMBS or previously-

issued structured securities. In contrast to UMBS, second-level securities can be commingled—that is, they can

include both Fannie Mae securities and Freddie Mac securities as the underlying collateral for the security.

These structured securities include Supers®, which are single-class resecuritizations, and Real Estate

Mortgage Investment Conduits (“REMICs”), which are multi-class resecuritizations. While Supers are backed

only by TBA-eligible securities, REMICs can be backed by TBA-eligible or non-TBA-eligible securities.

The key features of UMBS are the same as those of legacy single-family Fannie Mae MBS. Accordingly, all single-family

Fannie Mae MBS that are directly backed by fixed-rate loans and generally eligible for trading in the TBA market are

considered UMBS, whether issued before or after the introduction of UMBS. In this report, we use the term “Fannie

Mae-issued UMBS” to refer to single-family Fannie Mae MBS that are directly backed by fixed-rate mortgage loans and

generally eligible for trading in the TBA market. We use the term “Fannie Mae MBS” or “our MBS” to refer to any type of

mortgage-backed security that we issue, including UMBS, Supers, REMICs and other types of single-family or

multifamily mortgage-backed securities. References to our single-family guaranty book of business in this report exclude

Freddie Mac-acquired mortgage loans underlying Freddie Mac mortgage-related securities that we have resecuritized.

Common Securitization Platform

We rely on the common securitization platform operated by CSS to securitize the single-family MBS we issue and for

ongoing administrative functions for our single-family MBS. We do not use the common securitization platform for

multifamily Fannie Mae MBS. See “Risk Factors—GSE and Conservatorship Risk” for a discussion of risks posed by

our reliance on CSS.

Managing Mortgage Credit Risk

Effectively pricing and managing credit risk is key to our business. Below we discuss key elements of how we are

compensated for and manage the risk of credit losses through the life cycle of our loans and how we measure our credit

risk.

Loan Acquisition Policies

Loans we acquire must be underwritten in accordance with our guidelines and standards.

• In Single-Family, the vast majority of loans we acquire are assessed by Desktop Underwriter

®

(DU

®

), our

proprietary single-family automated underwriting system. DU performs a comprehensive evaluation of the

primary risk factors of a mortgage. We regularly review DU’s underlying models to determine whether its risk

analysis and eligibility assessment appropriately reflect current market conditions and loan performance data to

ensure the loans we acquire are consistent with our risk appetite and FHFA guidance.

• In Multifamily, we acquire the vast majority of our loans through our Delegated Underwriting and Servicing

(DUS

®

) Program. DUS lenders, who must be pre-approved by us, are delegated the authority to underwrite and

service loans for delivery to us in accordance with our standards and requirements. Based on a given loan’s

unique characteristics and our established delegation criteria, lenders assess whether a loan must be reviewed

by us. If review is required, our internal credit team will assess the loan’s risk profile to determine if it meets our

risk tolerances. DUS lenders also share with us the risk of loss on our multifamily loans, thereby aligning our

interests throughout the life of the loan. FHFA has instructed us to limit the volume and nature of multifamily

loans we acquire, and our senior preferred stock purchase agreement with Treasury also includes covenants

with respect to our multifamily loan acquisition volume. We continue to closely monitor our multifamily loan

acquisitions and market conditions and, as appropriate, make changes to our standards and requirements to

Business | Mortgage Securitizations

Fannie Mae 2021 Form 10-K 8

ensure the multifamily loans we acquire are consistent with our risk appetite, the senior preferred stock

purchase agreement, and FHFA guidance.

For more information about our mortgage acquisition policies and underwriting standards, see “MD&A—Single-

Family Business—Single-Family Mortgage Credit Risk Management” and “MD&A—Multifamily Business—

Multifamily Mortgage Credit Risk Management.” For information on the restrictions on our single-family and

multifamily loan acquisitions, see “Conservatorship, Treasury Agreements and Housing Finance Reform—

Treasury Agreements—Covenants under Treasury Agreements” and “MD&A—Multifamily Business—

Multifamily Business Metrics.”

In exchange for managing credit risk on the loans we acquire, we receive guaranty fees that take into account, among

other factors, the credit risk characteristics of the loans we acquire. We provide information about our guaranty fees in

“MD&A—Single-Family Business—Single-Family Business Metrics” and in “MD&A—Multifamily Business—Multifamily

Business Metrics.”

Loan Performance Management

We closely monitor the performance of loans in our guaranty book of business and we work to reduce defaults and

mitigate the severity of credit losses through our servicing policies and practices.

Single-Family Loans

• For single-family loans, the most important loan performance criteria we monitor are (1) serious delinquency

rates, which are typically strong indicators of loans that are at a heightened risk of default, and (2) mark-to-

market LTV ratios, which affect both the likelihood of losses and the potential severity of any losses we may

ultimately realize. While mark-to-market LTV ratios are significantly impacted by changes in home prices, which

are outside our control, we have an array of loss mitigation tools to try to reduce defaults on delinquent loans

and to minimize the severity of the losses we do incur.

• We consider single-family loans to be seriously delinquent when they are 90 days or more past due or in the

foreclosure process. Once a single-family loan becomes 36 days past due, the servicer is required to make

weekly attempts, for the next six months, to contact the borrower to try to engage in steps to resolve the

delinquency. Our loss mitigation tools include payment forbearance, repayment plans, payment deferrals and

loan modifications. We describe these tools and discuss them further in “MD&A—Single-Family Business—

Single-Family Mortgage Credit Risk Management—Single-Family Problem Loan Management—Loan Workout

Metrics.” Successful loan reperformance is heavily influenced by the effective use of these tools and the

amount of equity the borrower has in their home.

• Some loans that become seriously delinquent subsequently become current or repay in full without a

modification or other loan workout. However, we modify a substantial portion of our seriously delinquent loans.

When a loan does not cure on its own and we are not able to provide a workout for it, the likelihood of default

increases. See “MD&A—Single-Family Business—Single-Family Mortgage Credit Risk Management” for more

information on the performance of our modified single-family loans.

• As a result of the COVID-19 pandemic, in 2020 our loss mitigation pivoted to payment forbearance, providing

up to 18 months in some cases to borrowers affected by the pandemic. Forbearance is typically used in

instances where the duration and impact of a borrower’s hardship are uncertain, such as disasters like

hurricanes and flooding, to give the borrower time to understand whether, and to what extent, a loss mitigation

solution will be needed to return to paying status. Because payments are not required during forbearance, our

serious delinquency rate increased as a result of the large number of loans in forbearance. Most of the loans

that entered forbearance as a result of the COVID-19 pandemic have since exited, resolving their delinquency

in many cases through a payment deferral or other form of loan workout. We provide information about our

single-family loans that received forbearance in “MD&A—Single-Family Business—Single-Family Mortgage

Credit Risk Management—Single-Family Problem Loan Management—Single-Family Loans in Forbearance.”

• For delinquent loans that are unable to reperform, we use alternatives to foreclosure where possible, such as

short sales, which reduce our credit losses while helping borrowers avoid foreclosure. We provide more

information on short sales and our other foreclosure alternatives in “MD&A—Single-Family Business—Single-

Family Mortgage Credit Risk Management—Single-Family Problem Loan Management—Loan Workout Metrics

—Foreclosure Alternatives.” We work to obtain the highest price possible for the properties sold in short sales.

When we acquire properties, including through foreclosure, our primary objectives are to facilitate equitable and

sustainable access to homeownership, quality affordable rental housing, and housing for owner occupant and

community-minded purchasers, while obtaining the highest price possible. The value of the underlying property

relative to the loan’s unpaid principal balance has a significant impact on the severity of loss we incur as a

Business | Managing Mortgage Credit Risk

Fannie Mae 2021 Form 10-K 9

result of loan default. We provide information on the mark-to-market LTV ratio of loans in our single-family

conventional book of business in “MD&A—Single-Family Business—Single-Family Mortgage Credit Risk

Management—Single-Family Portfolio Diversification and Monitoring.”

• Our credit loss mitigation strategy also involves selling nonperforming and reperforming loans thereby removing

them from our guaranty book of business. We discuss sales of nonperforming and reperforming single-family

loans in “MD&A—Single-Family Business—Single-Family Mortgage Credit Risk Management—Nonperforming

and Reperforming Loan Sales” and “MD&A—Single-Family Business—Single-Family Mortgage Credit Risk

Management—Other Single-Family Credit Information—Single-Family Credit Loss Metrics and Loan Sale

Performance.”

• We present additional information on the credit characteristics and performance of our single-family loans in

“MD&A—Single-Family Business—Single-Family Mortgage Credit Risk Management—Single-Family Portfolio

Diversification and Monitoring” and “Single-Family Problem Loan Management” and “Note 13, Concentrations

of Credit Risk—Risk Characteristics of our Guaranty Book of Business.”

Multifamily Loans

• For multifamily loans, key indicators of heightened risk of default are debt service coverage ratios (“DSCRs”),

particularly loans with an estimated current DSCR below 1.0, and serious delinquency rates. We consider a

multifamily loan seriously delinquent when it is 60 days or more past due.

• For loans with indicators of heightened default risk, our DUS lenders, through their delegated authority, work

with us to maintain the credit quality of the multifamily book of business and prevent foreclosures through loss

mitigation strategies such as payment forbearance or loan modification.

• For loans that ultimately default, we work to minimize the severity of loss in several ways, including pursuing

contractual remedies through our DUS loss-sharing arrangements and with providers of additional credit

enhancements where available.

• Similar to single-family, we also offer forbearance for borrowers experiencing temporary challenges, like natural

disasters and financial hardship, to help both borrowers and renters. During the COVID-19 pandemic, we

delegated to our multifamily lenders the ability to provide forbearance for up to six monthly payments for most

loan types. While FHFA extended the forbearance program indefinitely, the delegation to our lenders expired on

September 30, 2021, and we determine whether to offer forbearance relief based on the borrower’s

circumstances through our normal loss mitigation procedures. A majority of the loans that entered forbearance

as a result of the COVID-19 pandemic have since exited through completion of their repayment plan or

otherwise reinstating.

• We present information on the credit characteristics and performance of our multifamily loans in “MD&A—

Multifamily Business—Multifamily Mortgage Credit Risk Management—Multifamily Portfolio Diversification and

Monitoring” and “Note 13, Concentrations of Credit Risk—Risk Characteristics of our Guaranty Book of

Business.”

Sharing and Selling Credit Risk

In addition to managing credit risk through our selling and servicing practices, we also share and transfer credit risk to

third parties through a variety of credit enhancement products and programs.

• For single-family loans we acquire with an LTV ratio over 80% our charter requires credit enhancement, which

we typically meet through third-party primary mortgage insurance.

• Our Multifamily business uses a shared-risk business model that distributes credit risk to the private markets,

primarily through our DUS program. Under DUS, our multifamily lenders typically share with us approximately

one-third of the credit risk on these loans, aligning the interests of lenders and Fannie Mae. DUS lenders

receive credit-risk-related compensation in exchange for sharing risk. The lender risk-sharing we obtain through

our DUS program accompanies our multifamily loans at the time we acquire them.

• We use other types of credit enhancements, including pool mortgage insurance and credit risk transfer

transactions. In our credit risk transfer transactions, we use risk-sharing capabilities we have developed to

obtain credit enhancement by transferring portions of our single-family and multifamily mortgage credit risk on

reference pools of mortgage loans to the private market. In most of our credit risk transfer transactions,

investors receive payments, which effectively reduce the guaranty fee income we retain on the loans. Our credit

risk transfer transactions are designed to transfer to the investors, in exchange for these payments, a portion of

the losses we expect would be incurred in an economic downturn or a stressed credit environment.

Business | Managing Mortgage Credit Risk

Fannie Mae 2021 Form 10-K 10

For more information about our loans with credit enhancement, see “MD&A—Single-Family Business—Single-Family

Mortgage Credit Risk Management—Single-Family Credit Enhancement and Transfer of Mortgage Credit Risk” and

“MD&A—Multifamily Business—Multifamily Mortgage Credit Risk Management—Transfer of Multifamily Mortgage Credit

Risk.”

Measuring Credit Risk and the Impact of Changes on Our Results

Our best estimate of future credit losses is reflected in our single-family and multifamily loss reserves, which for periods

on or after January 1, 2020 are calculated using a lifetime credit loss methodology under the CECL standard. We

update our estimate of credit losses quarterly based on the credit profile of our loans as well as certain actual and

forecasted economic data. Changes in our estimate affect our benefit or provision for credit losses, which, combined

with foreclosed property expense, comprises our credit-related income or expense.

We provide information on our loss reserves in “MD&A—Single-Family Business—Single-Family Mortgage Credit Risk

Management—Single-Family Problem Loan Management—Other Single-Family Credit information” and “MD&A—

Multifamily Business—Multifamily Mortgage Credit Risk Management—Multifamily Problem Loan Management and

Foreclosure Prevention—Other Multifamily Credit information.” We provide information on our credit related income or

expense in “MD&A—Consolidated Results of Operations—Credit-Related Income (Expense).”

Conservatorship, Treasury Agreements and Housing Finance

Reform

Conservatorship

On September 6, 2008, the Director of FHFA appointed FHFA as our conservator, pursuant to authority provided by the

Federal Housing Enterprises Financial Safety and Soundness Act of 1992, as amended, including by the Housing and

Economic Recovery Act of 2008 (together, the “GSE Act”). The conservatorship is a statutory process designed to

preserve and conserve our assets and property and put the company in a sound and solvent condition.

The conservatorship has no specified termination date. For more information on the risks to our business relating to the

conservatorship and uncertainties regarding the future of our company and business, as well as the adverse effects of

the conservatorship on the rights of holders of our common and preferred stock, see “Risk Factors—GSE and

Conservatorship Risk.”

Our conservatorship could terminate through a receivership. For information on the circumstances under which FHFA is

required or permitted to place us into receivership and the potential consequences of receivership, see “Legislation and

Regulation—GSE-Focused Matters—Receivership” and “Risk Factors—GSE and Conservatorship Risk.”

Management of the Company during Conservatorship

Upon its appointment, the conservator immediately succeeded to (1) all rights, titles, powers and privileges of Fannie

Mae, and of any shareholder, officer or director of Fannie Mae with respect to Fannie Mae and its assets, and (2) title to

the books, records and assets of any other legal custodian of Fannie Mae. The conservator subsequently issued an

order that provided for our Board of Directors to exercise specified functions and authorities. The conservator also

provided instructions regarding matters for which conservator decision or notification is required. The conservator

retains the authority to amend or withdraw its order and instructions at any time. For more information on the functions

and authorities of our Board of Directors during conservatorship, see “Directors, Executive Officers and Corporate

Governance—Corporate Governance—Conservatorship and Board Authorities.”

Our directors serve on behalf of the conservator and exercise their authority as directed by and with the approval, where

required, of the conservator. Our directors have no fiduciary duties to any person or entity except to the conservator.

Accordingly, our directors are not obligated to consider the interests of the company, the holders of our equity or debt

securities, or the holders of Fannie Mae MBS unless specifically directed to do so by the conservator.

Because we are in conservatorship, our common stockholders currently do not have the ability to elect directors or to

vote on other matters. The conservator eliminated common and preferred stock dividends (other than dividends on the

senior preferred stock issued to Treasury) during the conservatorship.

Powers of the Conservator under the GSE Act

FHFA has broad powers when acting as our conservator. As conservator, FHFA can direct us to enter into contracts or

enter into contracts on our behalf. Further, FHFA may transfer or sell any of our assets or liabilities (subject to limitations

and post-transfer notice provisions for transfers of certain types of financial contracts), without any approval, assignment

of rights or consent of any party. However, mortgage loans and mortgage-related assets that have been transferred to a

Business | Managing Mortgage Credit Risk

Fannie Mae 2021 Form 10-K 11

Fannie Mae MBS trust must be held by the conservator for the beneficial owners of the Fannie Mae MBS and cannot be

used to satisfy the general creditors of the company. Neither the conservatorship nor the terms of our agreements with

Treasury change our obligation to make required payments on our debt securities or perform under our mortgage

guaranty obligations.

A Supreme Court decision in June 2021, in Collins et al. v. Yellen, Secretary of the Treasury, et al., held that the

President has the power to remove the Director of FHFA for any reason, not just for cause. The Supreme Court’s

opinion in Collins v. Yellen also included an expansive interpretation of FHFA’s authority as conservator under the

Housing and Economic Recovery Act of 2008, noting that “when the FHFA acts as a conservator, it may aim to

rehabilitate the regulated entity in a way that, while not in the best interests of the regulated entity, is beneficial to the

Agency and, by extension, the public it serves.” With FHFA’s broad powers as conservator, changes in leadership at

FHFA, including changes resulting from a change in Administration, could result in significant changes to the goals

FHFA establishes for us and could have a material impact on our business and financial results. See “Risk Factors—

GSE and Conservatorship Risk” for more information how conservatorship impacts us.

Treasury Agreements

On September 7, 2008, Fannie Mae, through FHFA in its capacity as conservator entered into a senior preferred stock

purchase agreement with Treasury, pursuant to which we issued to Treasury one million shares of Variable Liquidation

Preference Senior Preferred Stock, Series 2008-2, which we refer to as the “senior preferred stock,” and a warrant to

purchase shares of common stock equal to 79.9% of the total number of shares of our common stock outstanding on a

fully diluted basis at the time the warrant is exercised for a nominal price. The senior preferred stock purchase

agreement and the dividend and liquidation provisions of the senior preferred stock have been amended multiple times,

most recently in January 2021, pursuant to a letter agreement between us, through FHFA in its capacity as conservator,

and Treasury. Some provisions added to the agreement in January 2021 were subsequently temporarily suspended

pursuant to a September 2021 letter agreement. Below we discuss the terms of the senior preferred stock purchase

agreement and the senior preferred stock as they are currently in effect. See “Risk Factors—GSE and Conservatorship

Risk” for a description of the risks to our business relating to the senior preferred stock purchase agreement, as well as

the adverse effects of the senior preferred stock and the warrant on the rights of holders of our common stock and other

series of preferred stock.

Senior Preferred Stock Purchase Agreement

Funds Available for Draw

The senior preferred stock purchase agreement provides that, on a quarterly basis, we may draw funds up to the

amount, if any, by which our total liabilities exceed our total assets, as reflected in our consolidated balance sheet,

prepared in accordance with generally accepted accounting principles in the United States of America (“GAAP”), for the

applicable fiscal quarter (referred to as the “deficiency amount”), up to the maximum amount of remaining funding under

the agreement. As of the date of this filing, the maximum amount of remaining funding under the agreement is $113.9

billion. If we were to draw additional funds from Treasury under the agreement with respect to a future period, the

amount of remaining funding under the agreement would be reduced by the amount of our draw. The senior preferred

stock purchase agreement provides that the deficiency amount will be calculated differently if we become subject to

receivership or other liquidation process.

Commitment Fee and “Capital Reserve End Date”

The senior preferred stock purchase agreement provides for the payment of an unspecified quarterly commitment fee to

Treasury to compensate Treasury for its ongoing support under the senior preferred stock purchase agreement. The

amount of this fee, as well as a number of the agreement’s other terms and the terms of the senior preferred stock,

depend on whether we have reached the “capital reserve end date,” which is defined as the last day of the second

consecutive fiscal quarter during which we have maintained capital equal to, or in excess of, all of the capital

requirements and buffers under the enterprise regulatory capital framework discussed in “Legislation and Regulation—

GSE-Focused Matters—Capital.” Under the agreement, (1) through and continuing until the capital reserve end date,

the periodic commitment fee will not be set, accrue, or be payable, and (2) not later than the capital reserve end date,

we and Treasury, in consultation with the Chair of the Federal Reserve, will agree to set the periodic commitment fee.

Treasury’s funding commitment under the senior preferred stock purchase agreement has no expiration date. The

agreement provides that Treasury’s funding commitment will terminate under any of the following circumstances: (1) the

completion of our liquidation and fulfillment of Treasury’s obligations under its funding commitment at that time; (2) the

payment in full of, or reasonable provision for, all of our liabilities (whether or not contingent, including mortgage

guaranty obligations); or (3) the funding by Treasury of the maximum amount that may be funded under the agreement.

In addition, Treasury may terminate its funding commitment and declare the agreement null and void if a court vacates,

Business | Conservatorship, Treasury Agreements and Housing Finance Reform

Fannie Mae 2021 Form 10-K 12

modifies, amends, conditions, enjoins, stays or otherwise affects the appointment of the conservator or otherwise

curtails the conservator’s powers.

Debt and MBS Holders

In the event of our default on payments with respect to our debt securities or guaranteed Fannie Mae MBS, if Treasury

fails to perform its obligations under its funding commitment and if we and/or the conservator are not diligently pursuing

remedies with respect to that failure, the agreement provides that any holder of such defaulted debt securities or Fannie

Mae MBS may file a claim in the United States Court of Federal Claims for relief requiring Treasury to fund us up to

(1) the amount necessary to cure the payment defaults on our debt and Fannie Mae MBS, (2) the deficiency amount, or

(3) the amount of remaining funding under the senior preferred stock purchase agreement, whichever is the least. Any

payment that Treasury makes under those circumstances will be treated for all purposes as a draw under the

agreement that will increase the liquidation preference of the senior preferred stock.

Most provisions of the senior preferred stock purchase agreement may be waived or amended by mutual agreement of

the parties; however, no waiver or amendment of the agreement is permitted that would decrease Treasury’s aggregate

funding commitment or add conditions to Treasury’s funding commitment if the waiver or amendment would adversely

affect in any material respect the holders of our debt securities or guaranteed Fannie Mae MBS.

Senior Preferred Stock

Dividend Provisions

Treasury, as the holder of the senior preferred stock, is entitled to receive, when, as and if declared, out of legally

available funds, cumulative quarterly cash dividends. The dividends we have paid to Treasury on the senior preferred

stock during conservatorship have been declared by, and paid at the direction of, our conservator, acting as successor

to the rights, titles, powers and privileges of the Board of Directors. Dividend payments we make to Treasury do not

restore or increase the amount of funding available to us under the senior preferred stock purchase agreement.

The dividend provisions of the senior preferred stock were amended pursuant to the January 2021 letter agreement to

permit us to retain increases in our net worth until our net worth exceeds the amount of adjusted total capital necessary

for us to meet the capital requirements and buffers under the enterprise regulatory capital framework. As described

more fully below, after the capital reserve end date, the amount of quarterly dividends to Treasury will be equal to the

lesser of any quarterly increase in our net worth and a 10% annual rate on the then-current liquidation preference of the

senior preferred stock. As a result of these provisions, our ability to retain earnings in excess of the capital requirements

and buffers set forth in the enterprise regulatory capital framework will be limited.

Dividend Amount Prior to Capital Reserve End Date

The terms of the senior preferred stock provide for dividends each quarter in the amount, if any, by which our net worth

as of the end of the immediately preceding fiscal quarter exceeds an applicable capital reserve amount. The January

2021 letter agreement increased the applicable capital reserve amount, starting with the quarterly dividend period

ending on December 31, 2020, from $25 billion to the amount of adjusted total capital necessary for us to meet the

capital requirements and buffers set forth in enterprise regulatory capital framework. If our net worth does not exceed

this amount as of the end of the immediately preceding fiscal quarter, then dividends will neither accumulate nor be

payable for such period. Our net worth is defined as the amount, if any, by which our total assets (excluding Treasury’s

funding commitment and any unfunded amounts related to the commitment) exceed our total liabilities (excluding any

obligation with respect to capital stock), in each case as reflected on our balance sheet prepared in accordance with

GAAP.

Dividend Amount Following Capital Reserve End Date

Beginning on the first dividend period following the capital reserve end date, the applicable quarterly dividend amount

on the senior preferred stock will be the lesser of:

(1) a 10% annual rate on the then-current liquidation preference of the senior preferred stock; and

(2) an amount equal to the incremental increase in our net worth during the immediately prior fiscal quarter.

However, the applicable quarterly dividend amount will immediately increase to a 12% annual rate on the then-current

liquidation preference of the senior preferred stock if we fail to timely pay dividends in cash to Treasury. This increased

dividend amount will continue until the dividend period following the date we have paid, in cash, full cumulative

dividends to Treasury (including any unpaid dividends), at which point the applicable quarterly dividend amount will

revert to the prior calculation method.

Business | Conservatorship, Treasury Agreements and Housing Finance Reform

Fannie Mae 2021 Form 10-K 13

Liquidation Preference

Shares of the senior preferred stock have no par value and have a stated value and initial liquidation preference equal

to $1,000 per share, for an aggregate initial liquidation preference of $1 billion.

Under the terms that currently govern the senior preferred stock, the aggregate liquidation preference will be increased

by the following:

• any amounts Treasury pays to us pursuant to its funding commitment under the senior preferred stock

purchase agreement (a total of $119.8 billion as of the date of this filing);

• any quarterly commitment fees that are payable but not paid in cash (no such fees have become payable, nor

will they under the current terms of the senior preferred stock purchase agreement and the senior preferred

stock);

• any dividends that are payable but not paid in cash to Treasury, regardless of whether or not they are declared;

and

• at the end of each fiscal quarter through and including the capital reserve end date, an amount equal to the

increase in our net worth, if any, during the immediately prior fiscal quarter.

The aggregate liquidation preference of the senior preferred stock was $163.7 billion as of December 31, 2021. It will

increase to $168.9 billion as of March 31, 2022 due to the increase in our net worth during the fourth quarter of 2021.

The senior preferred stock ranks ahead of our common stock and all other outstanding series of our preferred stock, as

well as any capital stock we issue in the future, as to both dividends and rights upon liquidation. As a result, if we are